51

1 Owner-Manager Tax Planning 5 th Annual Tax Planning for the Wealthy Family James A. Hutchinson Miller Thomson LLP 416.597.4381 [email protected] Wednesday, September 9, 2009

1

Owner-Manager Tax Planning5th Annual Tax Planning for the Wealthy Family

James A. HutchinsonMiller Thomson LLP

[email protected], September 9, 2009

2

Overview

1. Personal and Corporate Income Tax Rates for 2009

2. Background on Owner-Manager Remuneration

3. Planning Considerations4. Cases on Owner-Manager Remuneration5. Technical Interpretations on Owner-Manager

Remuneration

3

1. Personal and Corporate Income Tax Rates 20092009 Rates for Individuals – Highlights:Income & Capital Gains• Decrease in highest marginal income tax rate in New

Brunswick by 0.95% (and consequent decrease in capital gains rate by approx 0.48%)

• Decrease in Newfoundland & Labrador of 0.5% (and consequent decrease on capital gains rate by 0.25%)

Eligible Dividends• Decreases in Alberta (1.45%), New Brunswick

(1.38%), Newfoundland & Labrador (5.22%), and Ontario (0.9%)

• Increase in British Columbia (1.45%)

4

1. Personal and Corporate Income Tax Rates 2009 (cont’d)

2009 Rates for Individuals – Highlights cont’d:Non-Eligible Dividends• Decreases in New Brunswick (1.19%), and

Newfoundland & Labrador (0.62%)– Further decrease by 2.7% in New Brunswick for 2010, to bring

highest marginal income tax rate down to 43.3% (assuming no change in top federal rate)

• Increases in Alberta (1.25%), British Columbia (1.13%), Manitoba (0.81%), and Prince Edward Island (1.52%)

5

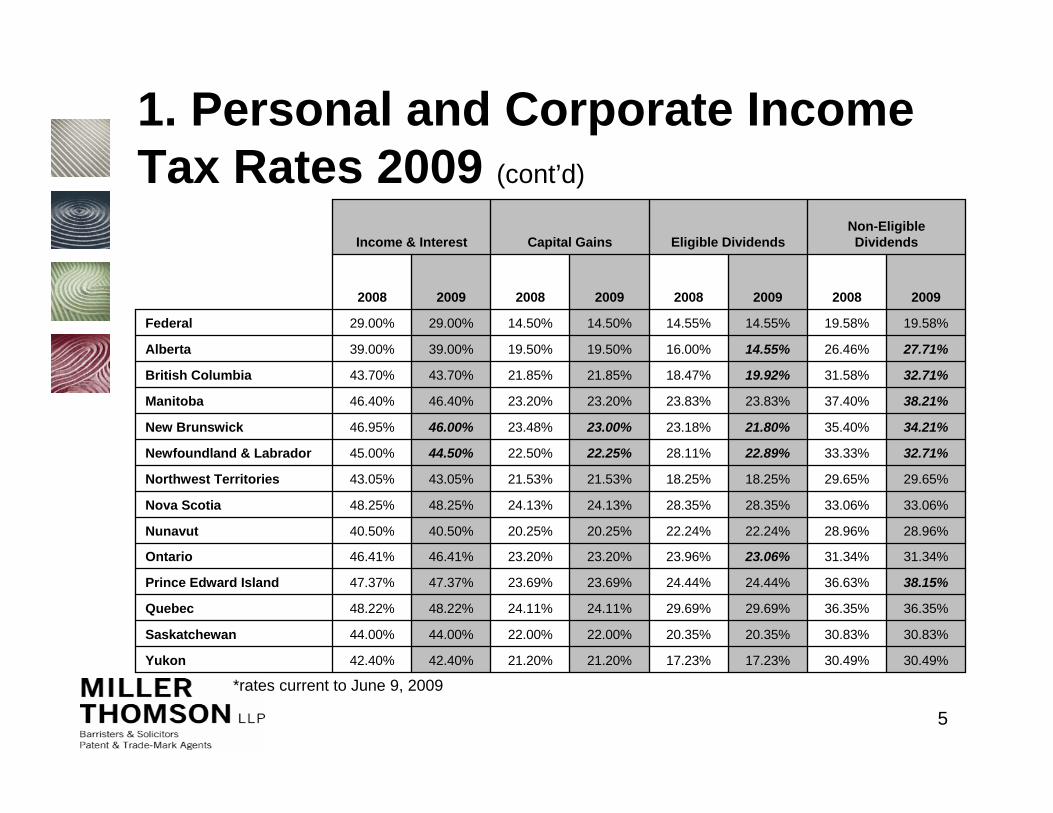

1. Personal and Corporate Income Tax Rates 2009 (cont’d)

30.49%30.49%17.23%17.23%21.20%21.20%42.40%42.40%Yukon

30.83%30.83%20.35%20.35%22.00%22.00%44.00%44.00%Saskatchewan

36.35%36.35%29.69%29.69%24.11%24.11%48.22%48.22%Quebec

38.15%36.63%24.44%24.44%23.69%23.69%47.37%47.37%Prince Edward Island

31.34%31.34%23.06%23.96%23.20%23.20%46.41%46.41%Ontario

28.96%28.96%22.24%22.24%20.25%20.25%40.50%40.50%Nunavut

33.06%33.06%28.35%28.35%24.13%24.13%48.25%48.25%Nova Scotia

29.65%29.65%18.25%18.25%21.53%21.53%43.05%43.05%Northwest Territories

32.71%33.33%22.89%28.11%22.25%22.50%44.50%45.00%Newfoundland & Labrador

34.21%35.40%21.80%23.18%23.00%23.48%46.00%46.95%New Brunswick

38.21%37.40%23.83%23.83%23.20%23.20%46.40%46.40%Manitoba

32.71%31.58%19.92%18.47%21.85%21.85%43.70%43.70%British Columbia

27.71%26.46%14.55%16.00%19.50%19.50%39.00%39.00%Alberta

19.58%19.58%14.55%14.55%14.50%14.50%29.00%29.00%Federal

20092008200920082009200820092008

Non-Eligible DividendsEligible DividendsCapital GainsIncome & Interest

*rates current to June 9, 2009

6

1. Personal and Corporate Income Tax Rates 2009 (cont’d)

2009 Rates for CCPCs – Highlights:Small Business Limit• 2009 Federal budget increased small business limit from

$400,000 to $500,000• Applies to qualifying active business income earned by CCPCs

eligible for federal income tax rate of 11%• Pro-rated for CCPCs whose taxation year does not coincide with

calendar year• In Manitoba, Nova Scotia and Yukon, small business limit

remains $400,000• Enhanced investment tax credit of 35% for CCPCs on up to $3

million of eligible SR&ED expenditures available for up to $500,000 of taxable income (formerly $400,000)– Completely phased out after $800,000 of taxable income

(formerly $700,000)

7

1. Personal and Corporate Income Tax Rates 2009 (cont’d)

2009 Rates for CCPCs – Highlights cont’d:Active Business Income > $500,000• Reduction in federal corporate tax rate on active business income

exceeding $500,000 by 0.5%• Caused decrease in combined federal and provincial rates in

every province and territory• Exception: Quebec, which raised its corporate tax rate by 0.5%• Ontario to further reduce rate on active business income up to

$500,000 by 1.0%Investment Income• Decrease in rate on investment income by 1% in Manitoba and

New Brunswick• Increase in rate by 0.5% in Quebec

8

1. Personal and Corporate Income Tax Rates 2009 (cont’d)

49.70%49.70%34.00%34.50%26.00%n/a15.00%15.00%Yukon

46.70%47.7/46.7%31.00%32.5/31/5%15.50%n/a15.50%15.50%Saskatchewan

46.60%46.10%30.90%30.90%22.9/19.0%n/a19.00%19.00%Quebec

50.70%50.70%35.00%35.50%14.2/13.1%n/a14.2/13.1%15.3/14.2%Prince Edward Island

48.70%48.70%33.00%33.50%16.50%n/a16.50%16.50%Ontario

46.70%46.70%31.00%31.50%15.00%n/a15.00%15.00%Nunavut

50.70%50.70%35.00%35.50%27.00%n/a16.00%16.00%Nova Scotia

46.20%46.20%30.50%31.00%15.00%n/a15.00%15.00%Northwest Territories

48.70%48.70%33.00%33.50%16.00%n/a16.00%16.00%Newfoundland & Labrador

47.7/46.7%47.70%32.0/31.0%32.50%16.00%n/a16.00%16.00%New Brunswick

47.7/46.7%48.7/47.7%32.0/31.0%33.5/32.5%24.0/23.0%n/a12.00%13.00%Manitoba

45.70%46.7/45.7%30.00%31.5/30.5%22.00%n/a13.50%15.5/14.5/13.5%British Columbia

44.70%44.70%29.00%29.50%21.0/14.0%n/a14.00%14.00%Alberta

34.70%34.70%19.00%19.50%11.00%n/a11.00%11.00%Federal

20092008200920082009200820092008

Investment IncomeGeneral Active Business$400,000-$500,000up to $400,000

*rates current to June 9, 2009

9

1. Personal and Corporate Income Tax Rates 2009 (cont’d)

2009 Rates for General Corporations – Highlights:• Decrease in federal corporate tax rate on general

active business income and investment income by 0.5%

• Quebec rate increase by 0.5%• Ontario proposes further reductions in rates on

general active business income and M&P to 10% by 2013

10

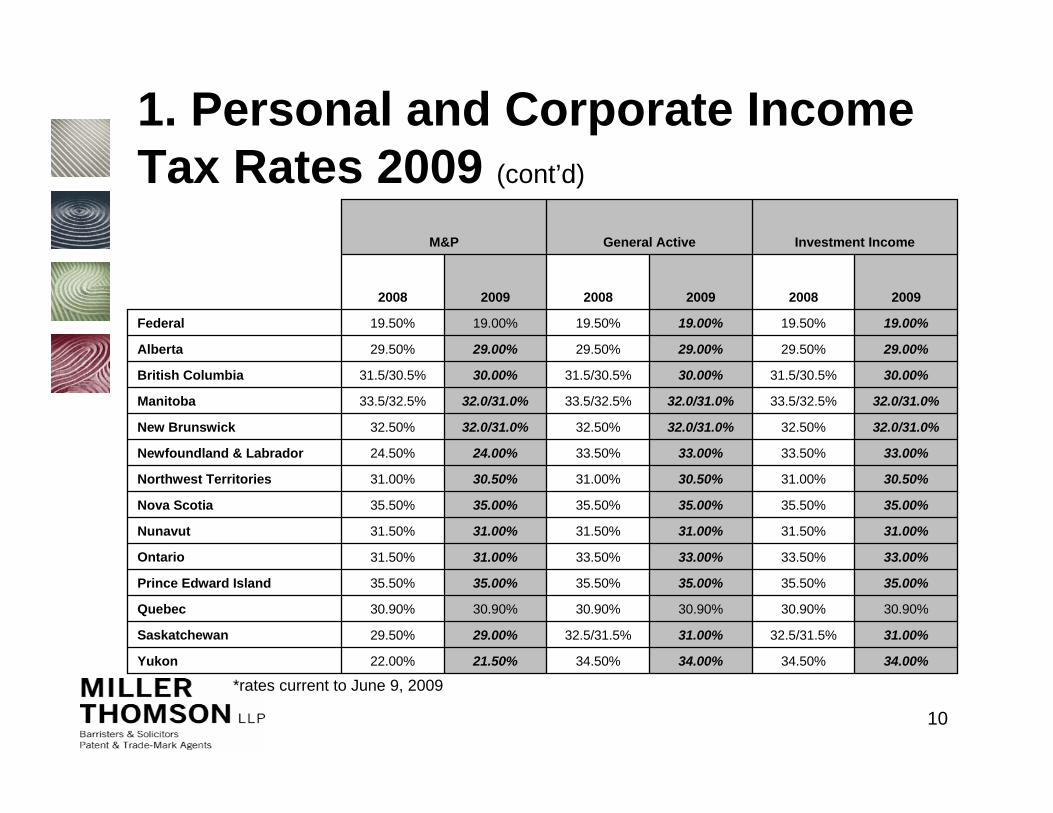

1. Personal and Corporate Income Tax Rates 2009 (cont’d)

34.00%34.50%34.00%34.50%21.50%22.00%Yukon

31.00%32.5/31.5%31.00%32.5/31.5%29.00%29.50%Saskatchewan

30.90%30.90%30.90%30.90%30.90%30.90%Quebec

35.00%35.50%35.00%35.50%35.00%35.50%Prince Edward Island

33.00%33.50%33.00%33.50%31.00%31.50%Ontario

31.00%31.50%31.00%31.50%31.00%31.50%Nunavut

35.00%35.50%35.00%35.50%35.00%35.50%Nova Scotia

30.50%31.00%30.50%31.00%30.50%31.00%Northwest Territories

33.00%33.50%33.00%33.50%24.00%24.50%Newfoundland & Labrador

32.0/31.0%32.50%32.0/31.0%32.50%32.0/31.0%32.50%New Brunswick

32.0/31.0%33.5/32.5%32.0/31.0%33.5/32.5%32.0/31.0%33.5/32.5%Manitoba

30.00%31.5/30.5%30.00%31.5/30.5%30.00%31.5/30.5%British Columbia

29.00%29.50%29.00%29.50%29.00%29.50%Alberta

19.00%19.50%19.00%19.50%19.00%19.50%Federal

200920082009200820092008

Investment IncomeGeneral ActiveM&P

*rates current to June 9, 2009

11

2. Background on Owner-Manager RemunerationOverview:• Para. 18(1)(a) of the ITA governs the

deductibility of salaries, wages, remuneration• In accordance with s. 67, salary or bonus paid

must be “reasonable in the circumstances”• Bonus/salary must be paid within 179 days of

end of taxation year of corporation to be deductible

• May be reasonable if paid to spouse or children providing services to corporation, depending on circumstances

12

2. Background on Owner-Manager Remuneration (cont’d)

CRA Administrative Policy:• Long-standing CRA policy[1] dating back to 1981 that it will not

challenge the reasonableness of salaries and bonuses paid to principal shareholder-managers of a corporation where:

1. The corporation’s general practice is to distribute profits to shareholder-managers in the form of bonuses or additional salaries; or

2. The corporation has adopted a policy of declaring bonuses to shareholders to remunerate them for profits earned by corporation attributable to know-how or entrepreneurial skills of shareholders

[1] See “Revenue Canada Round Table” in the Report of the Proceedings of the Thirty-Third Tax Conference (Toronto: Canadian Tax Foundation, 1982), Q. 42

13

2. Background on Owner-Manager Remuneration (cont’d)

CRA Administrative Policy cont’d:• Acceptable to pay bonuses in such circumstances, even if

purpose of paying is to reduce active business income of the corporation to the small business limit

• On the other hand, bonuses to shareholders who are not principal shareholder-managers, and who do not provide services to corporation will not be considered reasonable (unless to remunerate for special expertise), and will be subject to reasonableness test

• In Information Circular IC 88-2 at para. 18, CRA stated that it would not apply GAAR in circumstances where CCPC has paid salary to shareholder-manager to reduce ABI to small business limit, so long as salary reasonable

14

2. Background on Owner-Manager Remuneration (cont’d)

CRA Administrative Policy cont’d:• CRA has been asked to elaborate on its position with respect to

regular shareholders on numerous occasions[1]• CRA has outlined criteria on reasonableness in Income Tax

Technical News No. 22, dated January 11, 2002:1. Salaries/bonuses paid to managers who are shareholders

(either directly or indirectly) of a CCPC;2. Shareholder-managers are Canadian residents; and3. Shareholder-managers are actively involved in the day-to-day

operations of the business and contribute to the income-producing activities from which remuneration is paid

[1] See e.g. “Revenue Canada Round Table” in the Report of the Proceedings of the Thirty-Sixth Tax Conference (Toronto: Canadian Tax Foundation, 1985), Q. 82; “Revenue Canada Round Table” in the Report of the Proceedings of the Thirty-Seventh Tax Conference(Toronto: Canadian Tax Foundation, 1986), Q. 16; ; “Revenue Canada Round Table” in the Report of the Proceedings of the Forty-Second Tax Conference (Toronto: Canadian Tax Foundation, 1991), Q. 56; “Revenue Canada Round Table” in the Report of the Proceedings of the Forty-Fifth Tax Conference (Toronto: Canadian Tax Foundation, 1994), Q. 21.

15

2. Background on Owner-Manager Remuneration (cont’d)

CRA Administrative Policy cont’d:• Policy of not questioning reasonableness does not apply to:

– Inactive shareholders (Tech. Int. 2004-0406951I7);– Non-residents (e.g. Tech. Int. 2001-0092515);– Inter-corporate management fees (Tech. Int. 2001-0114993);– Income of CCPC derived from management fees or dividends that

have flowed through a “complex corporate structure” (Tech. Int. 2008-0170981I7)

• According to Income Tax Technical News No. 30, dated May 21, 2004, CRA’s stated intent with respect to its policy is to:

“provide flexibility to a CCPC and its active shareholder/managers to take advantage of marginal tax rates by reducing the corporation’s taxable income to or below the small business deduction limit through the payment of salaries and bonuses from income that is derived fromnormal business operations, and to provide certainty as to the taxable status of the transactions.”

16

3. Planning ConsiderationsRemuneration Strategies:• Since introduction of eligible dividend regime, the

optimal remuneration strategy has been a topic of interest for business professionals and their advisors

• No longer an automatic decision to “bonus down” to the small business limit

• Requires understanding of the concept of integration and consideration of what is most tax effective, given lower corporate tax rates and rates on eligible dividends

• Also requires consideration of a number of other factors that are not necessarily tax related

17

3. Planning Considerations (cont’d)

$3,741.10Tax savings by paying corporate tax and tax on non-eligible dividend vs. earning income directly

($26,168.90)Personal tax paid on non-eligible dividend[4]

$83,500Net cash if earned by CCPC and available to be paid as non-eligible dividend

$53,590Net cash if earned directly as individual

$29,910Tax deferral by leaving money in CCPC[3]

($16,500)Corporate tax on active business income up to $500,000[2]

($46,410)Personal tax paid if income earned directly[1]

$100,000Active business income of a CCPC

2009

[1] Based on the highest marginal income tax rate in Ontario of 46.41%[2] Based on combined federal and provincial corporate tax rate on business income up to $500,000 in Ontario of 16.5%[3] Based on the difference between the highest marginal income tax rate (46.41%) and corporate income tax rate (16.5%)[4] Based on non-eligible dividend tax rate of 31.34% in Ontario

Example 1: Effect of Earning Active Business Income up to Small Business Limit and Paying Non-Eligible Dividend in Ontario

18

3. Planning Considerations (cont’d)

$10,654.90Tax savings by paying corporate tax and tax on eligible dividend vs. earning income directly

($19,255.10)Personal tax paid on eligible dividend[4]

$83,500Net cash if earned by CCPC available to be paid as eligible dividend

$53,590Net cash if earned directly as individual

$29,910Tax deferral by leaving money in CCPC[3]

($16,500)Corporate tax on business income up to $500,000 small business limit[2]

($46,410)Personal tax paid if income earned directly[1]

$100,000Active business income of a CCPC

2009

[1] Based on the highest marginal income tax rate in Ontario of 46.41%[2] Based on combined federal and provincial corporate tax rate on business income up to $500,000 in Ontario of 16.5%[3] Based on the difference between the highest marginal income tax rate (46.41%) and corporate income tax rate (16.5%)[4] Based on eligible dividend tax rate of 23.06%

Example 2: Effect of Earning Active Business Income up to Small Business Limit and Paying Eligible Dividend in Ontario

19

3. Planning Considerations (cont’d)

($2,040.20)Tax cost of paying corporate tax and tax on eligible dividend vs. earning income directly

($15,450.20)Personal tax paid on eligible dividend[4]

$67,000Net cash if earned by CCPC and available to be paid as eligible dividend

$53,590Net cash if earned directly as individual

$13,410Tax deferral by leaving money in CCPC[3]

($33,000)Corporate tax on active business income above the small business limit[2]

($46,410)Personal tax paid if income earned directly[1]

$100,000Active business income of a CCPC

2009

[1] Based on the highest marginal income tax rate in Ontario of 46.41%[2] Based on combined federal and provincial corporate tax rate on active business income above the small business limit of 33% in Ontario[3] Based on the difference between the highest marginal income tax rate (46.41%) and corporate income tax rate (33%)[4] Based on eligible dividend tax rate of 23.06% in Ontario

Example 3: Effect of Earning Active Business Income in Excess of Small Business Limit and Paying Eligible Dividend in Ontario

20

3. Planning Considerations (cont’d)

Factors to Consider in Declaring Eligible Dividends:• 45% gross-up, as opposed to 25%, for purposes of calculating

the dividend tax credit (“DTC”)• Enhanced DTC of 18.966%, as compared to 13.33%

– DTC currently calculated as 11/18ths of 45% gross-up– Reductions to gross-up and DTC rate from 2008 Federal Budget

• 10/17ths of gross-up for 2010;• 13/23rds of gross-up for 2011; and• 6/11ths for 2012 and later years

• Can only be paid to extent there is a positive General Rate Income Pool (GRIP) balance at the end of a taxation year

• Need to determine current and future cash needs of individual• Asset protection and creditor-proofing• Ability to later claim the capital gains exemption (CGE) (now

$750,000) and maintain CCPC status

21

3. Planning Considerations (cont’d)

Factors to Consider in Declaring Eligible Dividends cont’d:

• In Ontario, rate on eligible dividends to go up to 26.57% in 2010, 28.19% in 2011 and 29.54% after 2011 (assuming top marginal income tax rate remains 46.41%)

• Makes 2009 an attractive year for declaring eligible dividends• Rules for declaring an eligible dividend (i.e. dividend designation

and written notice to all shareholders)• GRIP calculated at the end of the taxation year; potential for

making an “excessive eligible dividend designation” (defined in subsection 89(1), ITA) and incurring penalty tax under subsection 185.1(1) of the ITA– But see subsection 185.1(2) of the ITA for making election in

respect of excessive eligible dividend designation

22

3. Planning Considerations (cont’d)

Some Advantages of Paying Eligible Dividends:• RDTOH recovery• No source deductions for taxes, CPP, EI• Employer Health Tax (“EHT”) may be avoided• No reasonableness of remuneration test• Reduces cumulative net investment losses (CNILs),

and increases capital gains exemption (“CGE”) claim• Creates safe income on hand• Income-splitting opportunities

23

3. Planning Considerations (cont’d)

Some Disadvantages of Paying Eligible Dividends:• Effect on child tax benefits• Effect on amount of medical expenses that can be

claimed• Old Age Security (OAS) clawback if income too high• Possible effect on spousal credit• Do not create RRSP contribution room because not

employment income• No CPP or EI benefits for individual• Payment of salaries (not bonuses) can form part of

qualified expenditures for SR&ED

24

3. Planning Considerations (cont’d)

Income-Splitting:

Parentco

ParentBeforeCommon

Parentco

Family TrustClass A special

Class B specialClass C special

Parent

After

Child A Child BChild C

Fixed-value Pref. shares & New Common Shares

25

3. Planning Considerations (cont’d)

Income-Splitting cont’d:• Issue of whether “dividend sprinkling shares” acceptable

– i.e. whether separate classes of certain types of shares with same attributes on which dividends declared and paid separately acceptable

• Done in order to retain flexibility with respect to payment of dividends to different shareholders

• Potential solution to create separate classes of shares that aresimilar in most regards, but have nominal differences– e.g. alterations in voting rights– e.g. different rights upon liquidation

26

3. Planning Considerations (cont’d)

Income-Splitting cont’d:• CRA administrative policy dating back to 1995 that separate classes of

shares may exist when shares are identical in all respects (e.g. Class A special, Class B special and Class C special with same attributes, save for name), depending on the applicable corporate legislation

– See 1995 APFF Round Table, Question 33 (CRA Document No. 9522490)• Case law interpreting whether subsection 56(2) of the ITA (indirect

payment provision) would apply to such dividends:– Champ v. The Queen, 83 DTC 5029 (FCTD): terms and conditions of shares

did not permit directors to declare and pay dividends “selectively”– McClurg v. MNR, 91 DTC 5001 (SCC): terms and conditions of shares

expressly provided that certain classes could receive dividends to the exclusion of others, and other bases for distinguishing classes of shares; sufficient to rebut presumption of equality

– Neuman v. Canada, [1998] 3 C.T.C. 177 (SCC): 56(2) does not apply to dividends in family income-splitting situation; a shareholder need not contribute services to the corporation to be entitled to a dividend; profits belong to corporation as retained earnings.

27

3. Planning Considerations (cont’d)

Income-Splitting cont’d:• Subsection 22(7) added to the OBCA providing for two or more classes

of shares, or two or more series within a class of shares, having identical rights, privileges, restrictions and conditions

– To eliminate need to create such artificial distinctions• CRA response was that amendment to OBCA appears to sanction the

creation of separate classes that each have the same rights, privileges, restrictions and conditions, including right to have dividends declared on one particular class to exclusion of others

• However, CRA stated that it depends on facts and circumstances of each case and dividend entitlements of shares as set out in articles of incorporation

• OBCA amendment should not alter the decision in Champ, where dividends declared on one class of shares even though other classes entitled to dividends

– See e.g. CRA Round Table, 2007 STEP National Conference, Q. 15

28

3. Planning Considerations (cont’d)

Trust Residence:• Generally, trust considered to be resident of province in which the majority of

trustees who exercise management and control reside– Thibodeau Family Trust v. The Queen, 78 DTC 6376 (FCTD) the leading

case on trust residence• Other factors to determine trust residence, such as location where legal rights with

respect to trust assets are enforceable• CRA administrative position that trust residence a question of fact; trustee will

generally be found to exercise management and control where trustee has number of powers, such as: responsibility for management of business of trust, investment portfolio, banking and financing, control over trust assets etc.

– See e.g. CRA Interpretation Bulletin IT-447, “Residence of a Trust”• Overall income tax rate payable by Canadian trust varies from province to

province, depending on residence of trust• Incentive to establish trust resident in Alberta because it has the lowest income

tax rate on regular income and interest – i.e. 39%• However, recent indications that CRA has created an audit team to look at the

issue of trust residence

29

3. Planning Considerations (cont’d)

Incorporating a Professional:• Option for lawyers, doctors, engineers, architects and

accountants carrying on business of professional practice• Must not be precluded by provincial legislation governing relevant

professional body• CCPC carrying on professional practice may qualify for small

business deduction, assuming certain conditions met• See CRA Interpretation Bulletin IT-189R2, “Corporations Used by

Practising Members of Professions” for CRA’s administrative policy on use of a professional corporation

30

3. Planning Considerations (cont’d)

The Use of a Management Corporation:• May be used in tandem with professional practice, in lieu of a

professional corporation, or otherwise• To provide management and administration services (day-to-day

operations of corporation)– i.e. planning, direction, control, co-ordination, systems and

other functions at managerial level• Can charge reasonable management fees in respect of services• CRA accepts charge of a reasonable mark-up (15%) on

management fees– Although there is case law that suggests that reasonable

management fees may be more than 15% (e.g. Bertomeu, 2006 TCC 85)

• To be deductible, there must be a legal obligation to pay the management fees

31

3. Planning Considerations (cont’d)

Advantages of Using a Professional Corporation or a Management Corporation:

• Access to small business deduction• Income-splitting opportunities through paying

dividends to family members in lower tax brackets• Tax deferral equal to the difference between top

marginal income tax rate and low corporate income tax rate on active business income on every dollar of taxable income

32

3. Planning Considerations (cont’d)

Disadvantage – Personal Services Business:• Concern when exploring possibility of professional

corporation or management corporation• Defined in subsection 125(7) of the ITA to mean a

business of providing services where an individual (or a related person) performing services on behalf of a corporation is a “specified shareholder”, and could reasonably be regarded as an officer or employee of the corporation or partnership to whom such services are provided but for the existence of the corporation

33

3. Planning Considerations (cont’d)

Personal Services Business cont’d:In other words, where:• an individual or a related person (called an “incorporated

employee”) is a specified shareholder of Corporation A, and• the incorporated employee provides services on behalf of

Corporation A to Corporation B, and• but for the existence of Corporation A, the incorporated employee

could reasonably be regarded as an employee of Corporation B, then

• Corporation A will be considered to carry on a “personal services business” in a taxation year, unless

• Corporation A employs more than 5 full-time employees, or• the amount paid or payable for the services provided by

Corporation A to Corporation B is received or receivable from related Corporation C

34

3. Planning Considerations (cont’d)

Personal Services Business cont’d:• Certain exceptions:

– corporation employs more than 5 full-time employees throughout the year; or

– amount paid or payable in the year for services received or receivable from an associated corporation

• “Specified shareholder” generally a taxpayer owning not less than 10% of the issued shares of any class of the capital stock of the corporation or a related corporation, whether directly or indirectly, at any time in a taxation year

35

3. Planning Considerations (cont’d)

Personal Services Business cont’d:• PSB not entitled to small business deduction and limited

deductibility of expenses– See para. 18(1)(p) of the ITA

• Whether found to be operating a PSB a question of fact and involves an examination of factors used to distinguish employeesand independent contractors– i.e. tests established in Wiebe Door Services Ltd. v. M.N.R.,

87 D.T.C. 5025 (FCA); 671122 Ontario Ltd. v. Sagaz Industries Canada Inc., 2001 SCC 59

• Must examine the entire relationship between the parties to determine whether employer-employee relationship existed

36

3. Planning Considerations (cont’d)

Personal Services Business cont’d:• Even if found to be operating a PSB, no longer as

costly as it once was; tax cost varies from province to province

• Weigh costs associated with paying general corporate tax rate on PSB income and paying eligible dividends, as opposed to paying salary

• Obtain deferral of income tax when leave funds in the corporation

37

3. Planning Considerations (cont’d)

($244)Tax cost of using personal services business if dividends paid

($13,944)Personal tax paid on eligible dividend[4]

$70,000Net cash if earned by personal services business

$56,300Net cash if earned directly as individual

$13,700Tax deferral by leaving money in personal services business[3]

($30,000)Corporate tax paid by a personal services business[2]

($43,700)Personal tax paid if income earned directly[1]

$100,000Income of a personal services business

2009

[1] Based on the highest marginal income tax rate in British Columbia of 43.7%[2] Based on top combined federal and British Columbia corporate tax rate of 30%[3] Based on the difference between the highest marginal income tax rate (43.7%) and corporate income tax rate (30%)[4] Based on combined federal and British Columbia rate on eligible dividends of 19.92%

Example: Effect of Earning Income through a PSB in British Columbia

38

4. Cases on Owner-Manager RemunerationReasonableness of Bonuses and Salaries:Safety Boss Ltd. v. The Queen, [2000] 3 C.T.C. 2497 (TCC)• Facts

– Bonuses paid to president of corporate taxpayer (who was also a major shareholder), and non-resident company of the president

– Minister disallowed deduction of bonuses because amounts were unreasonable given that the parties were not dealing at arm’s length

• Issue– Were bonuses unreasonable in light of non-arm’s length relationship?

• Decision– Bonuses paid were fully commensurate with services rendered by the president, given

his exposure to dangerous activity (oil & gas), requiring extraordinary skill, endurance and courage

– Minister’s assessment flawed since it failed to take into account the years the president struggled to keep the company running without any remuneration or compensation

– Amounts paid not arbitrarily determined by the taxpayer• Case Importance

– One of the leading cases on payment of bonuses to owner-managers– Often cited for proposition that corporation can usually deducted an unlimited salary or

bonus paid to owner-manger once its ordinary profits are attributable to the owner-manager’s work for the corporation

39

4. Cases on Owner-Manager Remuneration (cont’d)

Reasonableness of Bonuses and Salaries cont’d:Jastrzebski v. R., 2008 TCC 643 (TCC)• Facts

– Taxpayer was owner of rental property which generated an income of $27,240 in 2004

– $15,000 and $10,000 were paid to his spouse and child for their assistance in maintaining and renovating the properties from 1999-2004

– Minister disallowed portions of rental expenses for 2003 and 2004 taxation years, partially because work of spouse and child not found to have significantly contributed to property

• Issue– Were the amounts paid to the taxpayer’s spouse and child from his rental

property income reasonable business expenses?• Decision

– Relationship between parties was non-arm’s length and due to a lack of sufficient documentary evidence that spouse and child worked in the maintenance of the properties, amounts not reasonably deducted given the gross annual rental income of the property

– In addition, taxpayer had no obligation to pay amounts to spouse and son

40

4. Cases on Owner-Manager Remuneration (cont’d)

Reasonableness of Bonuses and Salaries cont’d:Manchester Chivers & Associates Insurance Brokers Inc. v. R., [2005] 5 C.T.C.

2180 (TCC)• Facts

– Corporate taxpayer owned by sole shareholder and employed about 85 employees, including daughter and son of shareholder

– Substantial bonuses paid to shareholder, daughter and son for 1995-1997 taxation years– No other employees paid a bonus– Minister disallowed deduction of bonuses because not incurred for the purpose of gaining or

producing income pursuant to s. 18(1)(a) and not reasonable pursuant to s. 67 of ITA• Issue

– Can bonuses paid to shareholder and two children constitute reasonable business expenses?• Decision

– Yes, bonuses deductible since work performed greatly contributed to the success of the corporation and were for the purpose of gaining or producing income

– Amounts paid to daughter reasonable given her authority to sign corporate cheques, ability to manage labour relations, and implementation of complex collective agreements

– Amounts to son reasonable given his availability 24 hours a day, 7 days a week to look after equipment management, manage crisis situations, and negotiate the sales of businesses

– Amounts to shareholder reasonable given his representation of the corporation relating to complaints made in the purchase of a business, and his efforts in taking care of accounts receivables and settling grievances

41

4. Cases on Owner-Manager Remuneration (cont’d)

Reasonableness of Bonuses and Salaries cont’d:Wedge v. The Queen, [2005] 4 C.T.C. 2204 (TCC)• Facts

– Taxpayer RW and family owned shares of corporate taxpayer, W Ltd.– W Ltd. was the controlling shareholder of a large corporate group of companies,

including EDC Ltd., owned also by Taxpayer RW and family– Minister disallowed deduction for a $119,000 rollover from W Ltd. to RRSP for taxpayer

RW’s retiring allowance in 1998, since it did not appear taxpayer RW actually retired– Minister disallowed deduction of $519,000 made by W Ltd. for the distribution of assets

to its shareholders pursuant to section 67 of the ITA, since it was not reasonable given employees’ duties

• Issue– Were the deductions made reasonable?

• Decision– The $519,000 deduction was reasonable because it was compensation paid to

employees for services rendered in previous years in which they received no remuneration for

– The $119,000 deduction was not reasonable as a deduction for retiring allowance because taxpayer RW continued to hold significant functions of an officer and director after the allowance was paid

42

4. Cases on Owner-Manager Remuneration (cont’d)

Reasonableness of Bonuses and Salaries cont’d:Mépalex Inc. v. The Queen, [2004] 2 C.T.C. 2681 (TCC)• Facts

– Husband and wife of corporate taxpayer were sole shareholders and paid children salaries and bonuses from the profits of the corporation

– Payments to children assessed to be unreasonable and disallowed under s.67 of ITA by the Minister

– Husband and wife agreed with assessment and thus, requested amounts paid to be added to salaries of managing shareholders pursuant to s.56(2) of ITA, to be deducted in order to avoid double taxation

• Main Issue– Can modifications to a corporate tax plan be made retroactively pursuant to s.56(2) of

ITA for the deductibility of payments made to children of shareholders?• Decision

– No, salaries and bonuses initially determined to be unreasonable under s.67 of ITA, cannot be retroactively restructured to be deducted under s.56(2) of ITA

– Salaries and bonuses were unreasonable and part of income-splitting scheme– Children nonetheless entitled to minimal remuneration for their work

• Case Importance– Acknowledges that bonuses could be paid to children, but must be reasonable having

regard for actual services performed

43

4. Cases on Owner-Manager Remuneration (cont’d)

Reasonableness of Management Fees:Nielsen Development Co. v. R. 2009 TCC 160 (TCC)• Facts

– Individual taxpayer J owned 100% of corporate taxpayer K– Corporate taxpayer K owned 100% of corporate taxpayer N– Corporate taxpayer N entered into agreement with ManagementCo owned by taxpayer

J’s wife– Taxpayer J’s wife had responsibilities including purchasing, making accounting

decisions, signing cheques, and budgeting on behalf of ManagementCo– Minister disallowed payments of $275,000 and $300,000 in management fees paid in

2003 and 2004 to taxpayer J’s wife on the basis that her duties were overstated and the amounts paid were therefore unreasonable in the circumstances

• Issue– Were management fees paid to ManagementCo reasonable under s.67 of the ITA?

• Decision– Yes, the management fees paid were reasonable given the wide range of responsibilities

taxpayer J’s wife took on, which were above and beyond what was expected of an average general manager (who had subordinate role to taxpayer J’s wife)

– In fact, if a different management company was hired, fees for similar services would have been much greater

44

4. Cases on Owner-Manager Remuneration (cont’d)

Reasonableness of Management Fees cont’d:Bertomeu v. R., 2006 TCC 85 (TCC)• Facts

– Taxpayer was a sole shareholder of a consulting company who provided personnel, administrative and management services to the architect company he worked for

– Agreement provided that the company’s costs and expenses would be billed to taxpayer and his associates at cost plus 15%

– Agreement provided for an additional payment of 3% of all professional fees billed by architect company

– Minister disallowed the additional 3% payment to be deducted because the work already reimbursed for in the former fee at cost plus 15%

• Issue– Were the additional fees paid for services rendered by the related consulting company

reasonable?• Decision

– Yes, the additional fees paid for services rendered were reasonable – Consulting company assumed significant financial risks in the hiring of staff, and the

purchase of equipment necessary to provide services to the taxpayer– Manner in which income allocated between taxpayer and consulting company justified

• Case Importance– Demonstrates that more than a 15% mark-up may be reasonable in the context of

management fees

45

4. Cases on Owner-Manager Remuneration (cont’d)

Reasonableness of Management Fees cont’d:Welton v. Canada, [2005] T.C.J. No. 251 (TCC)• Facts

– Real estate agent taxpayer had husband showing homes, attracting potential customers, and offering expertise for her business

– Management fee of $32,000 paid to husband – Minister claimed fee not deductible because fee was not an obligation as

required by wording of s.18(1)(a) of ITA• Issue

– Was an expense for management fee to taxpayer’s husband truly anobligation and thus, deductible for income tax purposes?

• Decision– No, the expense for management fee paid was not deductible because there

was no evidence that the taxpayer had an obligation to pay her husband– Payment was nothing more than a domestic arrangement– Calculation of fee not supported by any valid documentation

46

5. Technical Interpretations on Owner-Manager RemunerationPersonal Services Business:Technical Interpretation 2008-0270981I7• Complex corporate structure involving individual (“A”) owning

100% of Holdco (management corporation), which had minority interest in Opco and a 98% interest in Partnership, of which A and spouse each held a 1% interest

• A provided services to Opco on behalf of P (A did not provide services to P on behalf of Opco)

• Tax avoidance element to entire corporate structure• CRA expressed concerns that A was trying to avoid the

application of the PSB rules• In addition, A trying to avoid application of source deductions by

providing services to Opco on P’s account, and trying to claim the small business deduction for Holdco

• Would be suitable situation for apply of GAAR in s. 245 of the ITA

47

5. Technical Interpretations on Owner-Manager Remuneration (cont’d)

Owner-Manager Remuneration:Technical Interpretation 2006-0168181E5• Concerned bonus declared and paid by CCPC to deceased shareholder-

manager (active in business operations) after death• CCPC had established practice of declaring and paying bonuses to

shareholder-managers• CCPC had year-end of July 31, 2005• Individual died on May 31, 2005; bonus declared on July 31, 2005 and

paid to estate of the deceased in January, 2006• CRA stated that its policy did not necessarily apply in such a situation,

and it reserved the right to challenge the reasonableness of the amount paid, pursuant to s. 67

• An employer may be able to deduct such a bonus paid to a deceased shareholder-manager in circumstances where the deceased had either an “enforceable claim” (subs. 70(2)) or a right in contract (subs. 70(1)) as at the date of death

48

5. Technical Interpretations on Owner-Manager Remuneration (cont’d)

Summary of some CRA Technical Interpretations:Technical Interpretation 2006-0172051E5• Policy does not apply to bonus paid to principal shareholder of Holdco

out of proceeds from sale of shares in Opco• But see Technical Interpretation 2004-0086191R3, where remuneration

paid to shareholder-managers out of income triggered from proceeds of sale of a business was deductible

Technical Interpretation 2004-0072741R3• Bonus paid to shareholder-manager paid for purposes of creating a non-

capital loss• Non-capital loss carried back to previous years in order to reduce active

business income to the small business limit• Bonus found to be within scope of CRA’s policy and would be deductible

by corporationTechnical Interpretation 2004-0070121E5• Management fees paid by Opco to PSB do not fall within the scope of

CRA’s administrative policy

49

5. Technical Interpretations on Owner-Manager Remuneration (cont’d)

Summary of some CRA Technical Interpretations cont’d:Technical Interpretation 2001-0114993• Inter-corporate management fees paid by Opcos to Holdcos and

then paid to shareholders of Holdcos not within scope of policyTechnical Interpretation 2000-0013085• Normal test of reasonableness applies where bonuses paid by

CCPC owned by corporations that are owned by trusts whose beneficiaries include individuals providing services to CCPC; requires consideration of:- duties performed by individuals;- time spent in carrying out duties;- remuneration paid to employees performing similar functions for

similar-sized corporation in similar circumstances

50

Questions?