In the ten year period between 1988 and 1998 Pakistan saw itself governed by seven different political administrations ending with a nonviolent coup in 1998. Coupled with long-standing social volatility, this political instability encouraged the worsening of the nation‟s economic condition. Though Pakistan‟s economy averted the financial crises that hit East Asian countries in 1998, it was one seemingly non-economic event that triggered Pakistan‟s Debt Crisis of 1998. On May 28, 1998, Amidst a turbulent domestic political environment and against the international community‟s advice, Pakistan responded to five nuclear arm tests conducted by India with nuclear arms tests of its own – this exacerbated Pakistan‟s already precarious situation and pushed it over the edge into crisis mode.

Written by Lateef Mauricio / [email protected]/ Published on January 5, 2011 at Machete Mag: http://bit.ly/pakistandebtcrisis1998 Page 1 of 12 Written by Lateef Mauricio / [email protected]Published on January 5, 2011 at Machete Mag: http://bit.ly/pakistandebtcrisis1998 Pakistan Debt Crisis of 1998 Introduction In the ten year period between 1988 and 1998 Pakistan saw itself governed by seven different political administrations ending with a nonviolent coup in 1998. Coupled with long-standing social volatility, this political instability encouraged the worsening of the nation‟s economic condition. Though Pakistan‟s economy averted the financial crises that hit East Asian countries in 1998, it was one seemingly non- economic event that triggered Pakistan‟s Debt Crisis of 1998. On May 28, 1998, Amidst a turbulent domestic political environment and against the international community‟s advice, Pakistan responded to five nuclear arm tests conducted by India with nuclear arms tests of its own – this exacerbated Pakistan‟s already precarious situation and pushed it over the edge into crisis mode. As suggested in the Middle East Economic Digest, “Pakistan has put national pride ahead of economic prudence by testing its nuclear devices.” 1 Pre-Crisis Issues and Conditions: Before May 28, 1998 Pakistan consistently displayed signs of a weakening economic condition in the years leading up to 1998; nevertheless, it should be said that a crisis was not imminent – in fact, the nation largely dodged most of the negative effects caused by the East Asian crises of 1998. The factors that were depressing Pakistan‟s economy before 1998 included an unacceptably high fiscal deficit, an ongoing trade deficit, the overwhelming amount of defaulted loans, and political instability. Unacceptably High Fiscal Deficit In the years leading up to 1998 Pakistan‟s revenue base hardly moved from the $5.4bn neighborhood – an exceedingly low figure that doesn‟t even begin to cover the nation‟s expenses. This low revenue base was fundamentally related to the high level of tax evasion – out of a population of 140m people there are less than 1.4m taxpayers. 2 The bulk of the revenue base gets used up almost evenly by defense expenditures and debt servicing. As a result, “the government‟s development and administrative expenditures have [had] to be financed entirely through domestic and international borrowing, leading to unacceptably high fiscal deficits.” 3 In the 97/98 fiscal year (July – June) the 1 Counting the Nuclear Costs, Middle East Economic Digest, June 8 1998. 2 PAKISTAN: IMF Agreement, Oxford Analytica Daily Brief Service, November 26, 1998. 3 No Easy Fix, Business Asia, The Economist Intelligence Unit, January 10, 2000, p. 4.

Transcript

Written by Lateef Mauricio / [email protected] / Published on January 5, 2011 at Machete Mag: http://bit.ly/pakistandebtcrisis1998

Page 1 of 12

Written by Lateef Mauricio / [email protected] Published on January 5, 2011 at Machete Mag: http://bit.ly/pakistandebtcrisis1998

Pakistan Debt Crisis of 1998

Introduction

In the ten year period between 1988 and 1998 Pakistan saw itself governed by seven different political

administrations ending with a nonviolent coup in 1998. Coupled with long-standing social volatility, this

political instability encouraged the worsening of the nation‟s economic condition. Though Pakistan‟s

economy averted the financial crises that hit East Asian countries in 1998, it was one seemingly non-

economic event that triggered Pakistan‟s Debt Crisis of 1998. On May 28, 1998, Amidst a turbulent

domestic political environment and against the international community‟s advice, Pakistan responded to

five nuclear arm tests conducted by India with nuclear arms tests of its own – this exacerbated

Pakistan‟s already precarious situation and pushed it over the edge into crisis mode. As suggested in

the Middle East Economic Digest, “Pakistan has put national pride ahead of economic prudence by

testing its nuclear devices.”1

Pre-Crisis Issues and Conditions: Before May 28, 1998

Pakistan consistently displayed signs of a weakening economic condition in the years leading up to

1998; nevertheless, it should be said that a crisis was not imminent – in fact, the nation largely dodged

most of the negative effects caused by the East Asian crises of 1998. The factors that were depressing

Pakistan‟s economy before 1998 included an unacceptably high fiscal deficit, an ongoing trade deficit,

the overwhelming amount of defaulted loans, and political instability.

Unacceptably High Fiscal Deficit

In the years leading up to 1998 Pakistan‟s revenue base hardly moved from the $5.4bn neighborhood –

an exceedingly low figure that doesn‟t even begin to cover the nation‟s expenses. This low revenue

base was fundamentally related to the high level of tax evasion – out of a population of 140m people

there are less than 1.4m taxpayers.2 The bulk of the revenue base gets used up almost evenly by

defense expenditures and debt servicing. As a result, “the government‟s development and

administrative expenditures have [had] to be financed entirely through domestic and international

borrowing, leading to unacceptably high fiscal deficits.”3 In the 97/98 fiscal year (July – June) the

1 Counting the Nuclear Costs, Middle East Economic Digest, June 8 1998.

2 PAKISTAN: IMF Agreement, Oxford Analytica Daily Brief Service, November 26, 1998.

3 No Easy Fix, Business Asia, The Economist Intelligence Unit, January 10, 2000, p. 4.

Written by Lateef Mauricio / [email protected] / Published on January 5, 2011 at Machete Mag: http://bit.ly/pakistandebtcrisis1998

Page 2 of 12

budget deficit was 5.4% of GDP – excessive public-sector borrowing to fund the deficit was one factor

that put upward pressure on consumer price inflation.

Continued Trade Deficit

The 96/97 fiscal year marked an all-time high for Pakistan‟s trade deficit which hit $3.37bn. The East

Asian financial crisis of 1997 didn‟t help matters since “almost one-third of Pakistan‟s exports are bound

for other Asian countries.”4 This deficit has been consistently affected by declining exports – 60% of

which are cotton related. Japan and Hong Kong being the “two main markets for Pakistan‟s yarn

exports” continue to be hindered by a recession while other Pakistani exports have lost competitiveness

to Asian nations whose currencies have “devalued sharply.” However, the record high trade deficit was

partially offset in the latter part of 1997 by “weak domestic demand, slowing investment and low world

prices,” which resulted in a substantial drop in imports – narrowing the deficit to $2.9bn in calendar year

1997.5

Overwhelming Amount of Defaulted Loans

Along the lines of the unbelievable tax evasion (1% of the population pays taxes), is the staggering

amount of defaulted loans that Pakistani citizens owe the nation‟s banks. The total default amount has

been growing exponentially year after year from PKR 10bn in 1985, to PKR 80bn in 1993, to PKR

121bn in August 1996.6 These Non-Performing Loans (NPLs) reached PKR 128bn in June 1998 –

representing about 4% of GDP.7 The NPLs continued amassing, reaching PKR 211bn ($4.06bn) as of

December 1999.8

Political Instability

From 1988 to 1998, seven political administrations took control of Pakistan‟s government – each prime

minister with a different take on handling the nation‟s economic situation. The extreme nature of

political disputes, religious strife, and frequent violent skirmishes with arch-enemy and neighbor India,

made for risky environment for foreign investors and domestic movers of capital alike. Capital flight and

so-called „brain-drain‟ (the emigration of educated people) was on a consistent rise, and so was foreign

direct investment (FDI). Once a very decent $2bn in fiscal year 94/95, FDI dropped drastically to

$436m in 97/98 and continued to drop to $296m in 98/99.

4 PAKISTAN: East Asian Fallout, Oxford Analytica Daily Brief Service, December 2, 1997.

5 Country Report: Pakistan, Afghanistan, EIU Country Report, The Economist Intelligence Unit, 1998, p. 11.

6 Haque, Mohammed Zahirul, Loan Default (non-payment of bank loans in Pakistan), Economic Review, September 1, 1996.

7 Rising to the Challenge in Asia: A Study of Financial Markets, Volume 9: Pakistan, Asian Development Bank, 1999, p. 38.

8 Bokhari, Farhan, General Appeal, The Banker, Financial Times Business Limited, December 1, 1999, p. 1.

Written by Lateef Mauricio / [email protected] / Published on January 5, 2011 at Machete Mag: http://bit.ly/pakistandebtcrisis1998

Page 3 of 12

High-profile government disputes with Independent Power Producers (IPPs) further affected Pakistan‟s

image as a location for sound investment. The Nawaz Sharif administration that took over after the

Benazir Bhutto government (in power from 1994-1996) took exception to the exceeding debt Pakistan‟s

state-owned Water & Power Development Authority (WAPDA) owed to the IPPs. The Sharif

administration put a hold on many payments from WAPDA to IPPs and initiated high-profile public

hearings of involved parties, accusing the Bhutto administration of corrupt practices that allowed the

IPPs to charge the government unjustifiably high prices. WAPDA faced a $1.6bn bill from IPPs in 1998,

and at the time was projected to owe $3.4bn in 2001.9

Pre-Crisis Reform Efforts

The seven administrations leading up to 1998 weren‟t oblivious to the poor state of affairs in Pakistan –

they undertook several efforts to alleviate the nation‟s ills. Unfortunately, the political instability,

coupled with a general international economic slowdown and a worsening domestic financial situation

doomed the reforms to failure.

Self-(In)correcting Reforms

In response to the incredibly low revenue base the government “increased taxation on a shrinking tax

base” that led to increased tax evasion and “the expansion of the underground economy, and resulted

in further tax hikes.”10 In January, 1998 the finance ministry announced the establishment of “a new tax

collecting entity called the Pakistan Revenue Service (PRS)” to replace the existing tax authority and

enhance tax collection. 11 To alleviate private sector unemployment the government “partly

compensated by over-staffing in the public sector, which further reduced its efficiency. Double-digit

inflation created the need for nominal depreciation, which fed back into inflation.”12 The Pakistani

government also helped to ensure disintermediation of domestic deposits in two ways, by imposing

high reserve requirements and increasing its direct borrowing to finance the fiscal deficit. This

contributed to lower returns on bank deposits, dropping saver confidence, which led to a continued

decline in bank profitability that already existed thanks to “increasing dollarization of the economy as

confidence in the rupee weaken[ed].”13

9 Pakistan Risks All in Clash with IPPs, Middle East Economic Digest, May 25, 1998.

10 Rising to the Challenge in Asia: A Study of Financial Markets, Volume 9: Pakistan, Asian Development Bank, 1999, p. 5.

11 PAKISTAN: IMF Agreement, Oxford Analytica Daily Brief Service, November 26, 1998.

12 Rising to the Challenge in Asia: A Study of Financial Markets, Volume 9: Pakistan, Asian Development Bank, 1999, p. 5.

13 Rising to the Challenge in Asia: A Study of Financial Markets, Volume 9: Pakistan, Asian Development Bank, 1999, p. 46.

Written by Lateef Mauricio / [email protected] / Published on January 5, 2011 at Machete Mag: http://bit.ly/pakistandebtcrisis1998

Page 4 of 12

One outlier reform stands out as an effort that didn‟t backfire economically, though it was politically

detrimental to the Nawaz Sharif administration. The administration set a deadline of July 10, 1998 for

loan “defaulters to begin repaying loans.”14 Since the non-performing loans (NPLs) are largely held by

high-profile, influential businesspeople, previous administrations have been reluctant to take action that

would inevitably lead to political suicide – this tough action helped to motivate banks and increase

saver confidence in the Pakistani banking system.

Economic Indicators: Hardly improving

Two economic indicators seemed to improve with little resistance – mostly due to drastic changes

across Pakistan‟s trading partners that were all unwilling participants in the world-wide economic

slowdown at the time. In 1997 inflation went down from the preceding year‟s 11.4% to 6.2% according

to official figures – while inflation was pushed down in some part by “soft world dollar prices for key

imports;” nevertheless, “independent analysts say that the real inflation rate is running at more than

double the official rate.” “Food-production shortfalls, increased electricity and fuel charges, the higher

cost of key imports and a depreciating currency are among the reasons for the persistence of upward

pressure.”15 Also in 1997, reserves grew to $1.2bn largely in part to the “sharp increase in the inflow of

resident” foreign currency deposits.16

14

Foreign Exchange Falls as Loan Defaulters Arrested, Middle East Economic Digest, August 3, 1998. 15

Pakistan, EIU Country Profile, The Economist Intelligence Unit, 1998, p. 15. 16

Rising to the Challenge in Asia: A Study of Financial Markets, Volume 9: Pakistan, Asian Development Bank, 1999, p. 7.

Written by Lateef Mauricio / [email protected] / Published on January 5, 2011 at Machete Mag: http://bit.ly/pakistandebtcrisis1998

Page 5 of 12

The Tipping Point (Crisis Begins)

On May 28, 1998 “Pakistan […] put national pride ahead of economic prudence by testing its nuclear

devices.” Responding to five nuclear tests conducted by neighbor, and long-time foe, India, the Nawaz

Sharif administration conducted its own nuclear tests, insisting that it has the right to develop its own

nuclear defense posture. The United States and Japan had warned Pakistan against the nuclear tests,

and threatened the nation with sanctions. Foreseeing international reprisal Nawaz Sharif established

the National Self-Reliance fund to receive donations from resident and non-resident Pakistanis,

emphasizing in a statement made on June 2, 1998 that it is time to “‟[…] live as a proud nation rather

than live in fear.”17

The international community condemned the nuclear tests and the “IMF, Asian Development Bank and

Export-Import Bank of Japan […] stopped all aid to Islamabad.”18 On June 11 Pakistan declared a

unilateral moratorium on nuclear tests hoping to get back in good graces – the sanctions and loss of

promised funding would be devastating to the already unstable nation.

Crisis Management Round 1: Panic Mode

The first series of official responses to the crisis were hasty and served to exacerbate the crisis that

followed the nuclear tests – perhaps event assuring a full-blown crisis that may have otherwise blown

over with less economic impact.

Foreign Currency Deposits

On May 28, 1998 – the day after the nuclear tests – the State Bank of Pakistan (SBP) placed an

indefinite freeze on foreign-exchange deposits, bank swaps and profit repatriation. This froze $13bn of

resident and non-resident foreign currency deposits, which made up 1/3rd of total external debt.19

Consequences of Panic Reforms

The immediate lock-down on foreign currency deposits displayed anti-liberalization policies that

furthered the case for the withdrawal and halting of previously obligated foreign aid funds – not to

mention, dissuaded any foreign investment in the nation.

Foreign Currency Deposits

17

Counting the Nuclear Costs, Middle East Economic Digest, June 8 1998. 18

Moratorium on Nuclear Tests, Middle East Economic Digest, June 22, 1998. 19

Counting the Nuclear Costs, Middle East Economic Digest, June 8 1998.

Written by Lateef Mauricio / [email protected] / Published on January 5, 2011 at Machete Mag: http://bit.ly/pakistandebtcrisis1998

Page 6 of 12

“Foreign currency deposits had grown rapidly to $11 billion by July 1997” from $3bn in the early 1990s,

becoming an important pillar of Pakistan‟s economy that accounted “for half of bank deposits in

Pakistan.”20 The freeze served to discourage future capital inflows and encourage immediate capital

flight through parallel channels. This pushed people to non-official methods of currency exchange and

worsened the vulnerable external financing position.

Halted Credit/Funding

With official credit accounting for over “80% of Pakistan‟s $30,000m of medium and long-term external

debt finance,” the nation was placed in a dangerous financial situation.21 In fact, a general consensus

amongst international ratings agencies and analysts predicted that sovereign default was a possibility

within three months of July 1998.22 SBP reserves, though increased from the preceding year to $2bn,

only represented about 1/3rd of foreign capital requirements for 98/99, which stood around $5.8bn –

increasing the nation‟s external vulnerability, especially given that a larger amount in expected foreign

loans was immediately put at risk on May 28. Foreign loans and assistance were expected to provide

somewhere between $2.5-3bn in funding from 1998-1999, of which $1.5bn were blocked by sanctions.

In response to funding blocks, Pakistan‟s finance ministry publicly stated that it might be forced to

declare a moratorium on its foreign debt totaling over $30bn.

Specific funding issues:

International Monetary Fund (IMF) – Halted $226m that represented 3rd tranche of $1.6bn relief

package

US Export-Import Bank – Stopped $293m

US Defense Licenses for commercial exports to Pakistan – Stopped $143m

Asian Development Bank (ADB) – Halted $2.bn pledged throughout 1998 – 2000

20

Rising to the Challenge in Asia: A Study of Financial Markets, Volume 9: Pakistan, Asian Development Bank, 1999, p. 46. 21

Counting the Nuclear Costs, Middle East Economic Digest, June 8 1998. 22

PAKISTAN – Debt Default Looms, Middle East Economic Digest, July 20, 1998.

Written by Lateef Mauricio / [email protected] / Published on January 5, 2011 at Machete Mag: http://bit.ly/pakistandebtcrisis1998

Page 7 of 12

Support from Islamic Nations

Between July and August of 1998, Islamic nations pitched in to help Pakistan‟s financial situation. The

Islamic Development Bank provided $700m package to finance imports and encourage exports while

Kuwait provided a $250m loan.

Losing International Credibility

Standard & Poor‟s (S&P) credit ratings for Pakistan immediately dropped in response to the nuclear

tests; a pattern that continued to worsen throughout the fiscal year of 98/99. In July 1998 S&P dropped

the long-term foreign currency issuer credit rating to Triple C from Single B-; and, short-term foreign

currency issuer credit rating to Single C. Almost one year later, in April 1999, both ratings stood at SD

– Selective Default, assigned to nations that fail to pay on or more of their financial obligations when

they become due.

Worsening Fundamentals

Exchange Rates

In the early 1990s Pakistan liberalized its foreign exchange system substantially – setting its exchange

rate as a managed float based on a trade-weight basket that was adjusted frequently to contain

inflationary pressures. Immediately after conducting the nuclear tests Pakistan put a total stop to all

foreign exchange withdrawals. As of June 30, 1998 the SBP attempted to defend its currency by

devaluing the Pakistani rupee by 4.4%, pushing it up from PKR 44/$1 to PKR 46/$1 – many analysts

viewed this devaluation as a last ditch measure to avoid a debt moratorium.23 The official exchange

rate was at PKR 46/$1 on May 28, 1998 and weakened more than 30% to PKR 60/$1 on the open

market in late-July, 1998.

Reserves and Balance of Payments Crisis

On May 21, 1998 liquid foreign exchange reserves were about $1.4bn – they fell precipitously to an

estimated $700m on July 8, 1998.24 Reserves continued to drop to $541m in late-July, 1998. With

debt repayments estimated at $5bn over the one-year period that followed the nuclear tests, the

reserves were clearly not going to be enough to cover obligations.

23

Pakistan Devalues Currency by 4.4%, New York Times, June 30, 1998. 24

PAKISTAN – Debt Default Looms, Middle East Economic Digest, July 20, 1998.

Written by Lateef Mauricio / [email protected] / Published on January 5, 2011 at Machete Mag: http://bit.ly/pakistandebtcrisis1998

Page 8 of 12

Figure 1 below shows a general worsening of major economic indicators, except for the inflation rate

which, as mentioned above in “Economic Indicators: Hardly Improving,” did not represent the real

inflation rate that has actually risen to double the inflation rate listed in Figure 1.

Pre-Crisis: 1997 vs 1998

FIGURE 1: PRE-CRISIS ECONOMIC INDICATORS 1997 VS 1998

Crisis Management Round 2: Cooler Heads

Rosy-colored Glasses at Finance Ministry

Finance Minister Sartaj Aziz acknowledged the dangerous economic situation Pakistan was in – he

emphasized that sanctions were not the way to deal with this situation as they would not only hurt

Pakistan, but also its trade partners if the nation was forced to declare a moratorium on its foreign debt

valued over $30bn. Aziz also highlighted the country‟s fiscal year 97/98 progress in three key

indicators of macroeconomic stability:

The current account deficit was down to 2.3% of gross domestic product (GDP) from 6%,

inflation was down to 8% from 12% and growth rate went up to 5.5%.25

25

Mian, Yawar, Gulf States Primed to Give Financial Support, Middle East Economic Digest, June 15, 1998

Written by Lateef Mauricio / [email protected] / Published on January 5, 2011 at Machete Mag: http://bit.ly/pakistandebtcrisis1998

Page 9 of 12

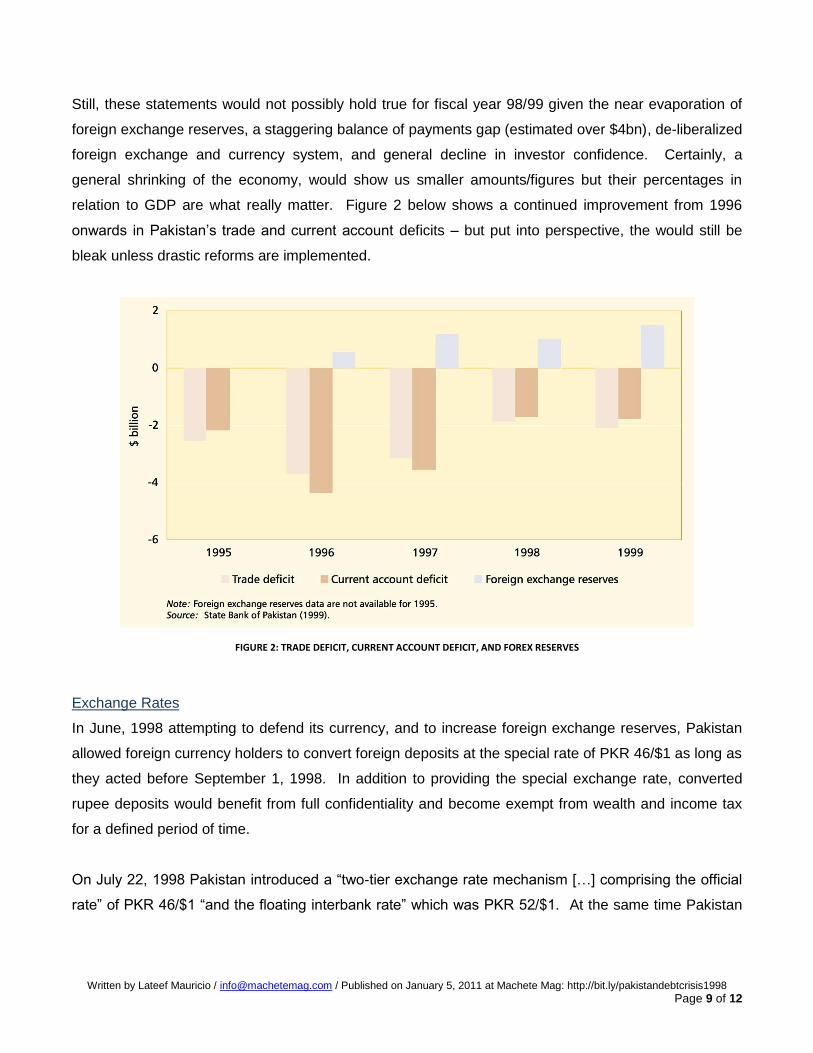

Still, these statements would not possibly hold true for fiscal year 98/99 given the near evaporation of

foreign exchange reserves, a staggering balance of payments gap (estimated over $4bn), de-liberalized

foreign exchange and currency system, and general decline in investor confidence. Certainly, a

general shrinking of the economy, would show us smaller amounts/figures but their percentages in

relation to GDP are what really matter. Figure 2 below shows a continued improvement from 1996

onwards in Pakistan‟s trade and current account deficits – but put into perspective, the would still be

bleak unless drastic reforms are implemented.

FIGURE 2: TRADE DEFICIT, CURRENT ACCOUNT DEFICIT, AND FOREX RESERVES

Exchange Rates

In June, 1998 attempting to defend its currency, and to increase foreign exchange reserves, Pakistan

allowed foreign currency holders to convert foreign deposits at the special rate of PKR 46/$1 as long as

they acted before September 1, 1998. In addition to providing the special exchange rate, converted

rupee deposits would benefit from full confidentiality and become exempt from wealth and income tax

for a defined period of time.

On July 22, 1998 Pakistan introduced a “two-tier exchange rate mechanism […] comprising the official

rate” of PKR 46/$1 “and the floating interbank rate” which was PKR 52/$1. At the same time Pakistan

Written by Lateef Mauricio / [email protected] / Published on January 5, 2011 at Machete Mag: http://bit.ly/pakistandebtcrisis1998

Page 10 of 12

removed the SBP band that was previously fixed at PKR 46/$1 for spot buying and PKR 46/$1 for spot

selling.26

Averting Sovereign Default

Given the multi-billion dollar balance of payments gap (estimated to be $7.2bn in 98/99) and the

dangerously low level of reserves (dropped to $541m in late-July), Pakistan was on the path to

imminent sovereign default, all things held constant.27 Thankfully, things weren‟t held constant and

negotiations with the Paris and London clubs of creditors proved to be the nation‟s saving grace. In

August 1998, Pakistan was able to reschedule $4bn in debt payments – this stopped the rapid drain on

foreign exchange reserves and marked the crisis‟ turnaround. As a result of this new breathing space,

foreign currency and foreign-exchange transaction restrictions would likely begin to be reversed, thus

re-instilling confidence into the people and businesses that would typically pump money into the nation.

The debt rescheduling was critical, but one policy touch assured the aversion of sovereign default – the

forcible curtailment of imports. Concerted efforts by the finance ministry in early June, 1998 included

“plans to cut imports by $700m and increase exports by 15% to $1.3bn.”28

Rescue from IMF and World Bank

In January, 1999, after witnessing the improvement of Pakistan‟s economy in relation to Washington

Consensus principles the IMF and World Bank were able to lend money to Pakistan to help the nation

gain stable footing. The IMF provided an Enhanced Structural Adjustment Facility (ESAF) of $575m

towards the improvement of key macroeconomic indicators, social indicators, and financial reforms.

The World Bank provided a $350m loan for reforms in banking, tax administration, public utilities

improvement, and public expenditure. Later on, in July 1999, the IMF once again suspended funding

due to a lack of progress in tax reform efforts and persistent problems with independent power

producers (IPPs).

Military Coup, Another Administration…

On October 12, 1999, General Pervez Musharraf took power of the country in a bloodless military coup.

The economic situation inherited by Musharraf was bleak as there was still a lot of work to be done in

terms of reforms to re-start much needed IMF funding that was suspended in July 1999. Key economic

26

Rising to the Challenge in Asia: A Study of Financial Markets, Volume 9: Pakistan, Asian Development Bank, 1999, p. 25. 27

No Easy Fix, Business Asia, The Economist Intelligence Unit, January 10, 2000, p. 4. 28

Mian, Yawar, Gulf States Primed to Give Financial Support, Middle East Economic Digest, June 15, 1998

Written by Lateef Mauricio / [email protected] / Published on January 5, 2011 at Machete Mag: http://bit.ly/pakistandebtcrisis1998

Page 11 of 12

indicators proved the nation‟s precarious position: GDP growth in 98/99 was 3.1% (6% was projected),

national savings rate fell to 12% (from 14% in 97/98), exports declined by 10% (projected to increase

by 15%), the national debt rose by 8% (amounting to 97% of GDP), and liquid foreign-exchange

reserves were stifled at $930m by the end of 97/98.29

The military ruler announced a package of reforms that were to begin being rolled out immediately.

The reforms were geared towards increasing the revenue base by simplifying the tax structure (greater

reliance on transparent self-assessment schemes); encourage exports by subsidizing the price of

wheat to PKR 300 per bag (up from PKR 280) and refraining from rising power and gas rates (inputs);

stopping the increasing dollarization of the economy by discontinuing foreign exchange bearer

certificates; development of low-income areas and populations in the form of a PKR 20bn fund; cutting

the fiscal deficit by reducing defense expenditures by PKR 7bn; encourage a higher national savings

rate and savers confidence by cutting interest rates by 2% on government bonds and saving schemes.

Another notable reform effort was based on the controversial topic regarding non-performing loans –

still weighing down the nation‟s economy at a total of $4.06bn in defaulted loans. On October 16, 1999

Musharraf gave the loan defaulters one month (until November 16, 1999) “to repay a portion of their

debt” and agree on a settlement plan with their respective banks.30

Lessons Learned

Nuclear or Not, Sound Economics Prevail

The biggest mistake Pakistan made was to test its nuclear devices – the nation was immediately

sanctioned and billions of dollars in expected foreign aid/loans/credits were halted – along with a

deteriorating economic condition this nuclear test event pushed Pakistan into a full-on crisis. As a

result, many analysts would argue that the main lesson learned here is not to go up against the

international community – I believe this is a moot point, as a nuclear test was imminent in response to

arch-rival India‟s display of military force. It‟s also very clear that any economic reforms require proper

follow-through to ensure their efficacy and success – economic control by seven different

administrations in just ten years almost made this sort of prudence impossible. There are a few

takeaways, political adjustments aside, that one can learn from this case and possibly apply towards

the aversion of a debt crisis similar to Pakistan‟s in 1998.

Securing Inflows

Since foreign direct investment is amongst the most stable and desirable type of inflow it seems that

Pakistan should have placed more emphasis on protecting FDI mechanisms than shutting them down.

29

No Easy Fix, Business Asia, The Economist Intelligence Unit, January 10, 2000, p. 3. 30

Bokhari, Farhan, General Appeal, The Banker, Financial Times Business Limited, December 1, 1999, p. 1.

Written by Lateef Mauricio / [email protected] / Published on January 5, 2011 at Machete Mag: http://bit.ly/pakistandebtcrisis1998

Page 12 of 12

The foreign currency deposit freeze locked up $13bn in money belonging to Pakistanis and foreigners

alike – this amount represented about 1/3rd of the nation‟s debt obligation and doomed it to be at the

mercy of international aid organizations – which were not going to support the nation with funds

anyway. Even in crisis mode, FDI brings benefits other than money that are important to maintain

economic progress, i.e. foreign technology and skills transfers).

The freeze on foreign currency deposits wasn‟t the only thing that restricted capital inflows from

alleviating the crisis. Remittances have been on a consistent decline since 88/89 when they were at

$2.5bn, dropping down to $1.1bn in 98/99.31 This decline certainly sharpened after the crisis in May

1998 – but it was also a result of a failing banking system – where banks were forced to charge

excessive rates in order to cover its own reserve requirements. Thus, banking system reform was long

overdue in Pakistan, not just to secure domestic savings confidence, but also to encourage foreign

capital inflows.

Pre-emptive Exchange Rate Activity

Pakistan did devalue its currency slightly before the crisis, and then by a larger percentage after the

crisis occurred – perhaps it would have been sound economics to have depreciated the currency much

sooner, at least several months before the crisis to have had any crisis softening effect. The

depreciation of the real exchange rate would have served to decrease imports thus improving “the

current account balance of the balance of payments” and having “an expansionary rather than a

contractionary effect on economic performance.” This “depreciation of the domestic currency in

combination with increased real domestic interest rates” would lead to inflows in foreign capital – thus

contributing to good overall economic performance.”32

31

No Easy Fix, Business Asia, The Economist Intelligence Unit, January 10, 2000, p. 4. 32

Iqbal, Zafar, Jeffrey James, and Graham Pyatt, Three-Gap Analysis of Structural Adjustement in Pakistan, Journal of Policy Modeling, 22 no. 1, January 2000, p. 135.