23

Pakistan economy Review and Recommendations

| Date post: | 22-Dec-2015 |

| Category: |

Documents |

| View: | 214 times |

| Download: | 0 times |

Pakistan economy Review and Recommendations

Pakistan ECONOMY: Key Stakeholders perspective

CITIZENS

INVESTORSMULTILATERAL

AGENCIES (IMF/WORLD BANK etc.)

Slide 2

THE CITIZENS PERSPECTIVE

THE CITIZENS PERSPECTIVE

Lack of Employment Opportunities

Crushing Inflation

Source: State Bank of Pakistan

FY-2

000

FY-2

001

FY-2

002

FY-2

003

FY-2

004

FY-2

005

FY-2

006

FY-2

007

FY-2

008

FY-2

009

FY-2

010

FY-2

011*

3.6% 4.4%3.5% 3.1%

4.6%

9.3%7.9% 7.8%

12.0%

20.8%

11.7%

14.6%

Consumer Price Inflation %

* July-DecemberFY

-2000

FY-2

001

FY-2

002

FY-2

003

FY-2

004

FY-2

005

FY-2

006

FY-2

007

FY-2

008

FY-2

009

FY-2

010

FY-2

011*

3.9%

2.5%

3.6%

5.1%

6.4%

8.6%

6.6% 6.8%

3.7%

1.2%

4.1%

2.5%

Real GDP Growth Rate %

* SBP projectionSlide 4

THE CITIZENS PERSPECTIVE (CONT…)

Lack of Economic Justice:

Rich don’t pay fair share of taxes

Government not able to control cartel’s (mafias)

Poor and unequal access to services and opportunities (gas, electricity, education, health etc.)

Slide 5

THE MULTILATERAL PERSPECTIVE

Source: State Bank of Pakistan

2006 2007 2008 2009 20101,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

0

10

20

30

40

50

60

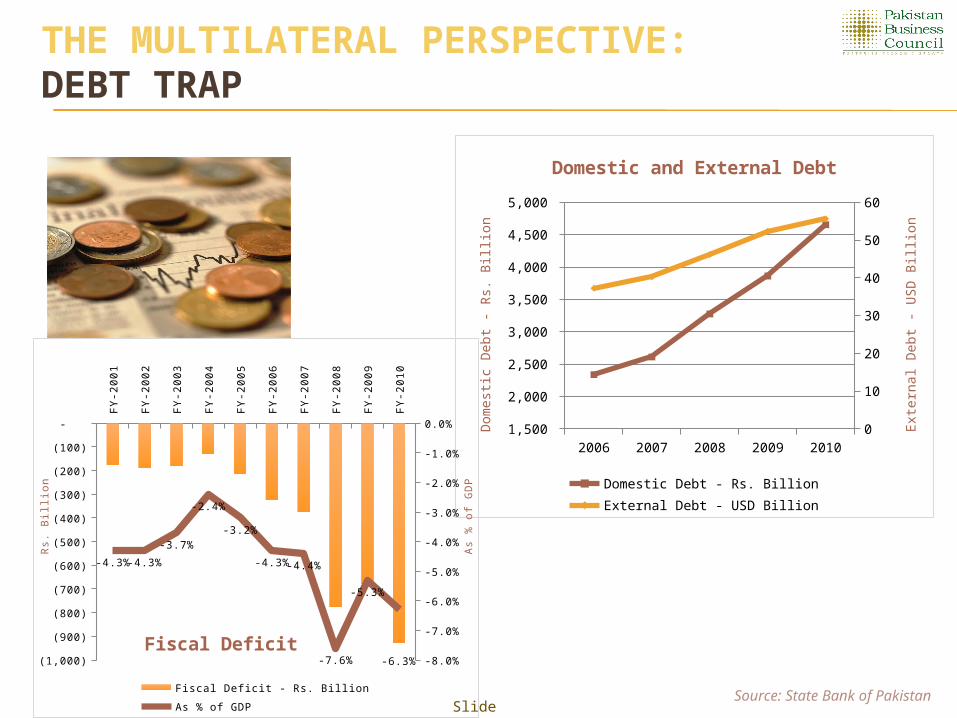

Domestic and External Debt

Domestic Debt - Rs. Billion External Debt - USD Billion

Dom

est

ic D

ebt

- R

s. B

illion

Exte

rnal D

ebt

- U

SD

Billion

FY-2

00

1

FY-2

00

2

FY-2

00

3

FY-2

00

4

FY-2

00

5

FY-2

00

6

FY-2

00

7

FY-2

00

8

FY-2

00

9

FY-2

01

0

(1,000)

(900)

(800)

(700)

(600)

(500)

(400)

(300)

(200)

(100)

-

-8.0%

-7.0%

-6.0%

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

-4.3%-4.3%

-3.7%

-2.4%

-3.2%

-4.3%-4.4%

-7.6%

-5.3%

-6.3%

Fiscal Deficit

Fiscal Deficit - Rs. Billion As % of GDP

Rs.

Bill

ion

As

% o

f G

DP

THE MULTILATERAL PERSPECTIVE: DEBT TRAP

Slide 7

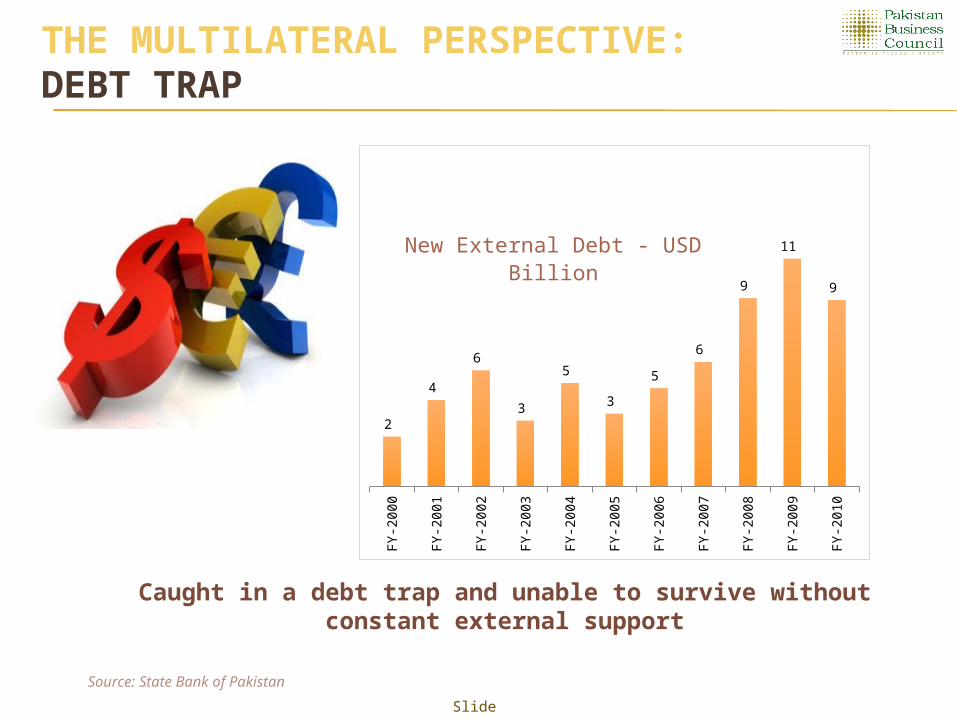

THE MULTILATERAL PERSPECTIVE: DEBT TRAP

Caught in a debt trap and unable to survive without constant external support

Source: State Bank of Pakistan

FY-2

000

FY-2

001

FY-2

002

FY-2

003

FY-2

004

FY-2

005

FY-2

006

FY-2

007

FY-2

008

FY-2

009

FY-2

010

2

4

6

3

5

3

5

6

9

11

9

New External Debt - USD Billion

Slide 8

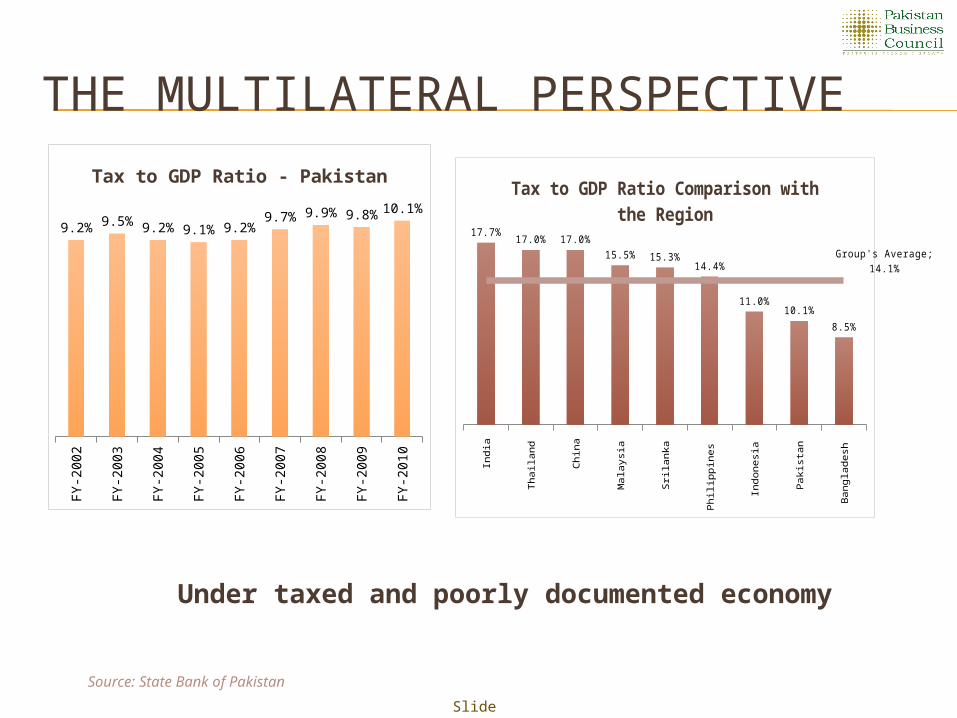

THE MULTILATERAL PERSPECTIVE

Under taxed and poorly documented economy

FY-2

002

FY-2

003

FY-2

004

FY-2

005

FY-2

006

FY-2

007

FY-2

008

FY-2

009

FY-2

010

9.2% 9.5% 9.2% 9.1% 9.2%9.7% 9.9% 9.8% 10.1%

Tax to GDP Ratio - Pakistan

Ind

ia

Th

aila

nd

Ch

ina

Ma

lay

sia

Sri

lan

ka

Ph

ilip

pin

es

Ind

on

esi

a

Pa

kist

an

Ba

ng

lad

esh

17.7%17.0% 17.0%

15.5% 15.3%14.4%

11.0%10.1%

8.5%

Group's Average; 14.1%

Tax to GDP Ratio Comparison with the Region

Source: State Bank of Pakistan

Slide 9

THE MULTILATERAL PERSPECTIVE

Weak trade competitiveness: Lowest regional trade integration in the

world Poorly educated, low skill workforce

Source: Promoting Economic Cooperation in South Asia, World Bank, 2010

27%

16%

6% 5%3%

1%

Intraregional Trade as a share of GDP - %

Slide 10

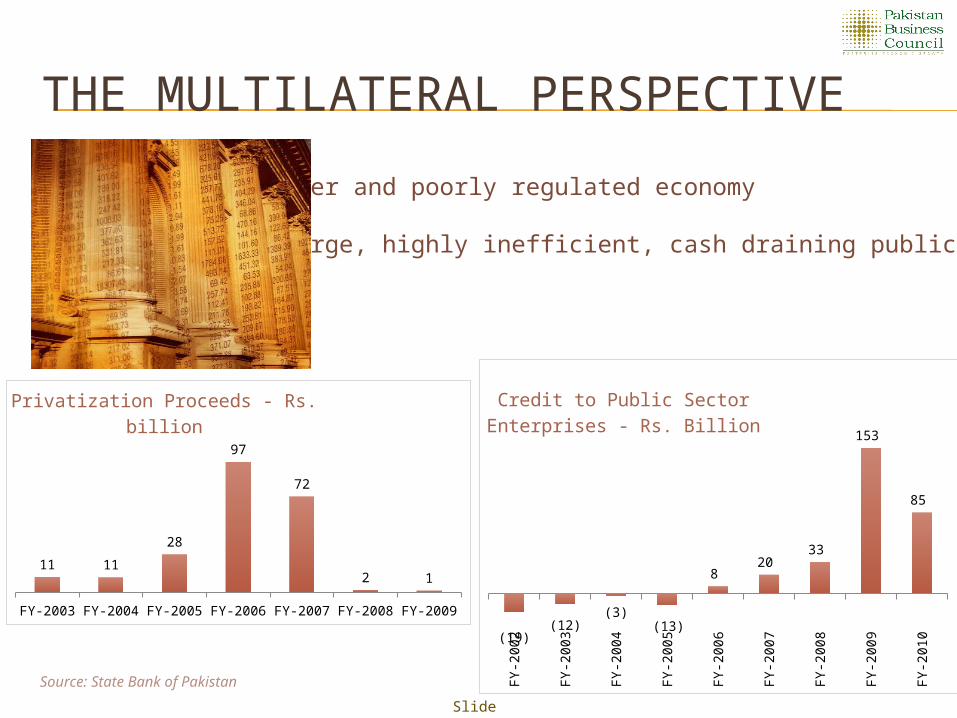

THE MULTILATERAL PERSPECTIVE

Source: State Bank of Pakistan

Over and poorly regulated economy

Large, highly inefficient, cash draining public sector

FY-2

002

FY-2

003

FY-2

004

FY-2

005

FY-2

006

FY-2

007

FY-2

008

FY-2

009

FY-2

010(19)

(12)(3)

(13)

8 20

33

153

85

Credit to Public Sector Enterprises - Rs. Billion

FY-2003 FY-2004 FY-2005 FY-2006 FY-2007 FY-2008 FY-2009

11 11

28

97

72

2 1

Privatization Proceeds - Rs. billion

Slide 11

The Investors Perspective

Private & Public Sector Borrowings

The Investors Perspective: Out of control Public Spending

Heavy borrowing by the government has resulted in classic crowding out effect on borrowing , reducing private investments & driving down private demand for credit.

2005-2007 2008-2010

768

132 207

1,169

Private Sector Borrowing

Government Borrowing

Source: State Bank of PakistanFY-2006 FY-2007 FY-2008 FY-2009 FY-2010

15.7% 15.4% 15.0% 12.7% 10.7%

4.8% 5.5% 5.4%

4.6%

4.3%

Public & Private Sector Investment as % of GDP

Private Sector Investment as % of GDP

Public Sector Investment as % of GDP

2005-2007 2008-2010 Spot *

8.5%

12.5%13.7%6 Months T-Bill Rate

* Feb, 2011

20.5%

20.9%

20.4%

17.3%

15%

Slide 13

B- B- B- B B B+ B+ B+ B+ CCC+ B- B-1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

B-

B

B-

B+

CCC+

The Investors Perspective

Badly deteriorated credit standing

Pakistan's Credit Rating by Standard & Poor’s (S&P)

Source: Bloomberg Slide 14

THE SOLUTION

THE SOLUTIONOn a war footing address the severe energy crisis by taking critical reform decisions which tackle pricing distortions, production and distribution inefficiencies, remove bottlenecks for urgently needed imports and develop the indigenous energy resources.

Take urgent & concrete steps to sharply reduce public finance deficits.• Overhaul the tax & tariff structure and bring all sectors

into a uniform documented tax net.• Reform and restructure public sector enterprises, starting

with the transparent appointment of capable / professional top management and boards which are empowered to take the necessary actions.

• Eliminate waste in Govt. expenditure.• Phase out broad based non targeted subsidies which

unnecessarily benefit the well off also.

Significantly increase education, health and income support expenditures (targeted subsidies) for the most vulnerable segments of the Society.

Strengthen intra-regional trade linkagesSlide 16

ADDRESS THE SEVERE ENERGY CRISIS

Expedite LNG imports

Eliminate pricing distortions between different fuels / sectors created by GoP taxation / pricing decisions.

Accelerate development of Thar Coal

Revamp obsolete power generation / distribution / transmission facilities

Deregulate the sector to bring in innovation and allow market to allocate molecules

Accelerate gas exploration through political initiatives by settling high prospective zones in Baluchistan & KP - offer high incentives, which are consistent with global prices, for offshore drilling

Slide 17

IMPROVEMENT OF PUBLIC FINANCE: OVERHAUL THE TAX STRUCTURE

Same rate of tax regardless of source of income. Bring all exempted/severely under taxed sectors in the tax net

Lower the tax rate and remove all exemptions.

Document the Economy

Revamp FBR. Deploy technology

Carry out strategic review of tariff structure to create level playing field for local manufacturing

Check abuse/misuse – Afghan Transit Trade/ under invoicing / smuggling

Pakist

an*

Indi

a

Thailand

Chin

a

Indo

nesia

Malay

sia

Viet

nam

Turk

ey

35.00% 33.99%

30.00%

25.00% 25.00% 25.00% 25.00%

20.00%

Corporate Tax Rate

* Exclusive of 7% levies (WWF, WPPF)

Source: State Bank of PakistanSlide 18

IMPROVEMENT OF PUBLIC FINANCE: REFORM, RESTRUCTURE AND DEREGULATE

Reform and restructure public sector enterprises

• Create a "supra board" which overseas the restructuring program of all these PSE's

• Take these PSE's out of control of line ministries and have the "supra board" report to a parliamentary committee for restructuring.

• Appoint capable/professional top management and boards which are empowered and accountable.

• Mandate to reform and restructure these PSE's within two years.

Focused and integrated deregulation of key sectors like energy and agricultural commodities

Strengthen regulatory agencies (CCP, OGRA, NEPRA, SECP) by building capacity and ensuring independence.

Slide 19

IMPROVEMENT OF PUBLIC FINANCE: ELIMINATION OF WASTE

Reduce size of Govt. structure by eliminating ministries and subordinated institutions which add little or no value

Introduce stronger parliamentary oversight over Govt. expenditure, including defense expenditure, by strengthening parliamentary committees

Make Freedom of Information Act operational and provide citizens access to Govt. expenditure, particularly by using information technology

Slide 20

INCREASE EDUCATION, HEALTH AND INCOME SUPPORT EXPENDITURE

Significantly enhance resources for education, health and social protection

Instead of broad based subsidies use targeted income support programs

Use innovative strategies to provide education and health coverage

Enhance citizens engagement and oversight over public education and health programs

Slide 21

REPRIORITIZING EXPENDITURE PHASED OVER THREE YEARS

5% Improvement by increasing Tax to GDP

Ratio by 5%

2% Improvement by 10% Reduction in Expenditure

2% Improvement by elimination of PSEs Losses

Total Improvement:9%

3.3% Reduction in Fiscal Deficit

5.7% Increase in Education, Health and

Income Support

expenditure

Slide 22

INTRA-REGIONAL TRADE LINKAGES

Revisit Afghan transit treaty to take care of Pakistani business concerns and address trade opportunities with Afghanistan and Central Asia

Increase trade linkages with Iran with specific emphasis on energy

Work for creation of a fully integrated South/Central/ West Asia energy grid

Expand trade linkages with India

Slide 23