A Report to the Operations Evaluation Department Asian Development Bank For the Country Assistance Program Evaluation for Pakistan Pakistan Private Sector Assistance Evaluation, 1985–2004 by Jayyad Malik Lloyd Powell July 2006

Transcript

A Report to the Operations Evaluation Department Asian Development Bank For the Country Assistance Program Evaluation for Pakistan

Pakistan Private Sector Assistance Evaluation, 1985–2004 by Jayyad Malik Lloyd Powell July 2006

CURRENCY EQUIVALENTS (as of 1 November 2005)

Currency Unit – Pakistan rupee/s (PRe/PRs)

PRe1.00 = $0.0167 $1.00 = PRs59.73

ABBREVIATIONS

ADB – Asian Development Bank BCO – Banking Companies Ordinance 1962 CSP – country strategy and program FYP – five-year plan MFI – microfinance institution NBFI – non-bank financial institution NGO – nongovernment organization PCR – project completion report PRM – Pakistan Resident Mission SBP – State Bank of Pakistan SECP – Securities and Exchange Commission of Pakistan SME – small and medium enterprise TA – technical assistance ZTBL – Zarai Tarqiati Bank Limited

NOTES

(i) In this report, “$” refers to US dollars.

CONTENTS EXECUTIVE SUMMARY iii I. INTRODUCTION 1 A. Background 1 B. Scope and Objectives of the Evaluation 2 C. Evaluation Methodology 2 D. Report Content 3 II. PRIVATE SECTOR PERFORMANCE AND CONSTRAINTS 3 A. Private Sector Overview 3 B. Private Sector Constraints 4 III. FINANCE SECTOR PERFORMANCE AND ISSUES 6 A. Introduction 6 B. Banking Sector 6 C. Non-Bank Financial Institutions 15 IV. STRATEGIES AND POLICIES 22 A. Government Strategies and Policies 23 B. ADB’s Country Strategies 25 V. DESCRIPTION OF ADB’S PRIVATE SECTOR OPERATIONS 30 A. Finance Sector Development (Public Sector Loans) 30 B. Private Sector Transactions 34 C. Other Operational Activities 37 VI. CONCLUSIONS AND RECOMMENDATIONS 38 A. Overall Conclusions 38 B. Recommendations 43 APPENDIXES 1. Pakistan Public Sector Loans 1984–2004 45 2. Pakistan Private Sector Loans/Equity 19984–2004 46 3. Securities and Exchange Commission of Pakistan Ordinance 1997 47 4. Individuals Interviewed for Private Sector Evaluation Mission 76

This report is a working paper for the Country Assistance Program Evaluation for Pakistan. OED Working Papers are an informal series to present the findings of work in progress in evaluation. They are circulated to encourage discussion and elicit comment. The views expressed in this report are those of the author(s) and do not necessarily reflect the views and policies of the Asian Development Bank, or its Board of Governors or the governments they represent. The Asian Development Bank does not guarantee the accuracy of the data included in this report and accepts no responsibility for any consequences of their use. Use of the term “country” does not imply any judgment by the author(s) or the Asian Development Bank as to the legal or other status of any territorial entity.

EXECUTIVE SUMMARY This report evaluates 20 years (1985–2004) of Asian Development Bank’s (ADB) support to the private sector in Pakistan. During this timeframe, ADB has formulated five strategy documents to guide its operations in Pakistan (plus two annual updates) and has approved $2,241 million in public and private sector facilities of which around 79% or $1,774 million was for 16 public sector projects.1 The remainder, 21% or $467 million was allocated across 38 private sector facilities.2 Over the same period, ADB approved 18 technical assistance (TA) grants for the finance sector for a total of $7.038 million.

Pakistan has undergone significant economic changes over the last 20 years. These

changes have had (and in many cases continue to have) an immediate and far-reaching impact on the scope as well as scale of private sector activities within the country. Similarly, the nature of support provided by ADB in order to enhance private sector participation has also evolved over the last two decades. Overall, ADB pursued two main strategies for assisting private sector in Pakistan. The first strategy was followed up until the mid-1990s and involved ADB providing much needed capital to private sector entities through its private sector operations window. Under this strategy, ADB approved $467 million for 38 projects. These projects accounted for 21% of the total ADB private sector assistance and involved ADB providing loans to private sector entities and/or taking equity positions in these businesses. Such interventions made sense at the time given the difficulties the private sector faced in their attempts to access financial resources due to a highly regulated and state controlled economy. However, the main drawback with this strategy was that these interventions were not material in the context of the size of the economy and, as such, did not bring about sustainable reforms. Of the total 38 private sector transactions, 13 occurred during the 1980s, 23 during the 1990s, and 2 in 2000s. The spike in the number of transactions coincides with the time (during the 1980s and the 1990s) that Pakistan’s economy was mired in economic problems and ADB decided to step in and provide the much needed financial support directly to the private sector. Overall, these private sector interventions appear to be well intentioned, commercial, and effective.3

In the mid-1990s, after the Government signed up for the most recent Structural

Adjustment Program (macroeconomic stabilization of the International Monetary Fund and the World Bank) and committed to a broad set of reforms, ADB stepped up its efforts and quickly shifted its private sector assistance strategy by working directly with the Government in order to effect meaningful and sustainable financial sector reforms. This strategy shift was co-coordinated with the World Bank and was based on the assumption that a robust financial infrastructure was a prerequisite for establishing a thriving private sector that would enable the country to achieve both its economic growth as well as its poverty alleviation objectives. Under this strategy ADB approved $1,774 million for 16 public sector projects that were geared towards strengthening the country’s financial systems. These finance sector reform projects make up a major portion (79%) of ADB’s private sector assistance activities over the last 20 years.

Some key accomplishments associated with ADB’s private sector assistance include (i)

bringing about policy reform, (ii) developing the country’s capital markets, (iii) kick-starting the country’s microfinance sector, (iv) supporting private sector entities through ADB’s private

1 Details on ADB’s public sector interventions between 1984 and 2004 are provided as Appendix 1. 2 Details on ADB’s private sector interventions between 1984 and 2004 are provided as Appendix 2. 3 Currently, ADB’s Private sector operation is considering investing in an existing mineral sector public private

partnership venture in Balochistan.

iv

sector operations window, (v) delivering TA for conducting critical analysis across a broad range of finance subsectors, and (vi) assisting the Government’s efforts towards restructuring financial institutions (such as Zarai Tarqiati Bank Limited [ZTBL] and SME Bank). However, there are some finance sector development projects that are raising questions and concerns because either they are not delivering anticipated results (e.g., large amounts spent on restructuring public sector organizations—ZTBL and SME Bank), or they are seen to provide an unfair subsidy (e.g., continued ADB funding of Government-sponsored microfinance bank—Khushali Bank).

Private sector transactions undertaken under the first strategy were more effective but

were not able to bring about any meaningful reform primarily due to their (smaller) size and (narrow) focus. On the other hand, finance sector development projects carried out in the second strategy were much larger in scale and scope as well as more sustainable. However, these projects appear to be much less effective due to (i) insufficient understanding of the sector/subsector as witnessed by low levels of TA resource allocation prior to loan approval, (ii) over-reliance on ability to transform (almost bankrupt) public sector agencies into viable commercial entities, and (iii) simultaneously supporting multiple subsectors (e.g., rural finance, microfinance, small and medium enterprise, capital markets, etc.). From an operational standpoint, initial parts of these projects (project planning and approval) went smoothly, but then some projects encountered problems during implementation. These problems were caused by (i) limited capacity within the Pakistan Resident Mission (PRM) to effectively implement projects and/or maintain relationship with key stakeholders, (ii) high staff turnover (both at PRM and headquarters) which raised confusion with regards to accountability, and (iii) Government’s responsiveness in implementing reforms and/or regulatory frameworks.

More recent government plans (such as the Ten-Year Perspective Plan and the Medium

Term Development Framework 2005–2010) indicate that the Government is more confident and is taking the lead in establishing what and how it plans to develop its economy. The following principal recommendations are made:

Recommendations Responsibility For Government Consideration 1. Immediate Action. The Ministry of Finance, for the

Government, should commission an assessment that provides a “gap-analysis” (i.e., what support does the financial sector need to evolve into a mature/developed financial sector) and a series of recommendations based on international financial market standards and a fully-costed and time bound action plan to get there. It is vital that international and local financial market operators are utilized for this assignment.

Coordination by Ministry of Finance

For ADB (and Government) Consideration 2. ADB should conduct a review of its finance sector

development projects and develop an action plan for unfinished business, such as, enhancing Securities and Exchange Commission of Pakistan’s (SECP’s) capacity as a regulator, development of the bond market, etc. (as highlighted in this evaluation as well as by findings of “1” above).

South Asia Finance Division and the Pakistan Resident Mission (PRM)

v

Recommendations Responsibility 3. ADB should consider reducing, if possible, the high turnover

of its finance personnel at PRM. In addition, a specialty support unit for supporting ongoing projects/programs and other Government and private sector stakeholders should be created in PRM as soon as possible.

4. ADB should be more stringent in evaluating its ongoing

projects (especially, finance sector development programs) in order to pragmatically assess their ability to achieve their stated objectives.

5. ADB should increase timely TA resource allocation, especially

for finance sector development programs. 6. ADB should maintain strategic focus (applies to both ongoing

and future projects) so as not to “spread itself too thin” by simultaneously supporting a relatively large number of sectors.

7. In the next country strategy and program (CSP),

consideration should be given to increasing the number of transactions developed through ADB’s private sector operations window.

8. In the next CSP, a more selective approach should be

adopted for new finance sector development projects given that private entities already dominate finance sector activities in Pakistan. Large-scale public finance sector development projects will continue to diminish as the financial systems in the country mature.

9. Provision should be made in the next CSP to utilize

innovative financing modalities when developing private sector assistance interventions (such as those offered under ADB’s Innovation and Efficiency Initiative).

10. ADB needs to reassess its existing strategy of supporting

institutions (e.g., ZTBL, SME Bank, Khushali Bank, etc.). If the Government wants to continue with these initiatives, then accountabilities should be documented so that ADB and the Government understand who is carrying what risks.

PRM Country Director/ South Asia Department Operations Evaluations Department/South Asia Finance Division South Asia Finance Division South Asia Finance Division/PRM Private Sector Operation/PRM South Asia Finance Division/PRM/Government South Asia Finance Division/PRM/Government South Asia Finance Division/ Operations Evaluation Department/PRM

I. INTRODUCTION A. Background 1. This report is prepared by the Operations Evaluation Department of the Asian Development Bank (ADB) and presents an evaluation of ADB’s private sector assistance in Pakistan over 1985–2004. This evaluation will contribute in preparation of a Pakistan Country Assistance Program Evaluation, which, in turn, will support the formulation of a new Pakistan Country Strategy and Program (CSP) to be approved in 2006. 2. Pakistan has undergone significant economic changes over the last 20 years. These changes have had (and in many cases continue to have) an immediate and far-reaching impact on the scope as well as scale of private sector activities within the country. Similarly, the nature of support provided by ADB in order to enhance private sector participation has also evolved over the last two decades. During this time, ADB assisted the private sector in Pakistan either by delivering support directly to the private sector (through its private sector operations window), or, by working with the Government to develop large-scale finance sector reform programs. 3. Overall, ADB approved $2,241 million in facilities to assist with the development of private sector enterprise in Pakistan and pursued two main strategies to this end. The first strategy was followed up until the mid-1990s and involved ADB providing much needed capital to private entities through its private sector operations window. Under this strategy, ADB approved $467 million for 38 projects. These projects accounted for 21% of the total ADB private sector assistance and involved ADB providing loans to private sector entities and/or taking equity positions in these businesses. Such interventions made sense at the time given the difficulties the private sector faced in their attempts to access financial resources due to a highly regulated and state controlled economy. The main drawback with this strategy was that these interventions were entity specific and, as such, did not attempt to bring about sustainable reforms.

Figure 1: Pattern of ADB’s Private Sector Assistance

0

100

200

300

400

500

600

1985-89 1990-94 1995-99 2000-04Time Period

$ M

illio

n

Finance Sector Development Programs Private Sector Transactions

4. In the mid-1990s, after the Government signed up for the Structural Adjustment Program and committed to a broad set of reforms, ADB stepped up its efforts and quickly shifted its

2

private sector assistance strategy by working with the Government to catalyze more meaningful and sustainable financial sector reforms. This strategy shift was based on the assumption that a robust financial infrastructure was a prerequisite for establishing a private sector that would enable the country to achieve both its economic growth as well as its poverty alleviation objectives. Under this strategy, ADB approved $1,774 million for 16 public sector projects that were geared towards strengthening Pakistan’s financial systems. Interventions carried out under this strategy constitute a major portion (79%) of ADB’s private sector assistance to Pakistan and for this reason a major portion of this evaluation involves discussion, evaluation, and assessment of the country’s financial systems. B. Scope and Objectives of the Evaluation 5. This report provides an assessment of ADB’s activities in support of private sector assistance in Pakistan over the last two decades. It is hoped that in addition to past and present assistance flow, this report will also aid in developing recommendations for future assistance efforts. In order to develop an assessment of ADB’s support for the private sector in Pakistan, this evaluation will attempt to answer the following set of questions:

(i) How has the private sector evolved over the last 20 years and what are the primary constraints it currently faces?

(ii) What strategies and policies have successive governments pursued? (iii) How has ADB assisted the private sector as per its formal country strategies? (iv) How effective have ADB’s projects been in assisting the private sector in

Pakistan? (v) What strategies were pursued for using ADB resources? (vi) What drove these strategic choices? (vii) What was the quality of ADB’s formal country strategies? (viii) Irrespective of quality, what was the quality and performance of ADB’s program? (ix) Was the program well managed? (x) How did ADB resources contribute to sector outcomes? (xi) Was there effective synergy between ADB resources and those of others? (xii) Did ADB do the right things? (xiii) How can choice selection and decision-making processes be improved in future?

C. Evaluation Methodology 6. This report was developed by following the methodology provided below:

(i) assessment of private sector enterprise in Pakistan; (ii) description and review of finance sector and subsector performance to identify

issues and needs; (iii) description of government strategies and policies, and assessment of their

implementation and achievements; (iv) evaluation of ADB sector strategies within country strategy documents; and (v) ADB’s program was then reviewed to determine the relationship between

strategy and program. 7. In order to understand the effectiveness of ADB’s private sector assistance strategies and programs the following approach was followed:

3

(i) all relevant design and evaluation/review documents for loan and TA projects were reviewed;

(ii) performance of ADB’s strategies, projects, and operations were assessed by interviewing senior officials in the Government and holding discussions with a number of private sector organizations and other development partners;1 and

(iii) performance, strategies, and (current/future) expectations of the Government were assessed by holding discussions with key decision and policy makers in Pakistan.

D. Report Content 8. Subsequent chapters cover private sector performance and constraints; finance sector performance and issues; government strategies and policies; ADB’s strategies and policies; a description and review of ADB’s operations in support of private sector; and conclusions and recommendations.

II. PRIVATE SECTOR PERFORMANCE AND CONSTRAINTS 9. This chapter aims to provide a high-level overview of Pakistan’s economic environment over the last two decades as well as information on key constraints to private sector participation in the country. A. Private Sector Overview 10. For the most part, during the 1980s, a state-led model of industrialization was followed in Pakistan. At the time, the Government was only focused on encouraging development of large scale manufacturing concerns. This fact was apparent from the way in which large firms were allowed to obtain licenses, official exchange rates for imports, and tariff rebates. Such preferential treatment was not extended to smaller firms and these firms found it much harder to secure financing2 and complying with regulatory requirements (e.g., tax regulations, labor laws, licensing and price controls, etc.). 11. During the 1990s, Pakistan committed and signed up for the macroeconomic stabilization and structural adjustment programs of the International Monetary Fund and the World Bank. The Government committed itself to these programs in order to lower macro-instability, remove distortions prevalent in trade and industry structures, and enhance economic growth. For the most part, growth rates slowed across most of the main economic sectors during this decade as the country braced for sweeping reform measures. Political instability was a mainstay and peaked towards the end of this decade when Pakistan conducted nuclear tests. Economic sanctions and other fall out from the country’s nuclear experiments also affected the country’s business climate significantly. 12. Pakistan’s economy has improved in 2000s. In 2004–2005, for the third consecutive year, the country’s economy expanded and registered a real gross domestic product (GDP) growth of 8.4%, surpassing the 6.6% target set for the year and improving upon the GDP growth for the previous year (6.4%).3 There are a number of reasons fueling the country’s economic

1 See Appendix 4 for list of individuals met for the Private Sector Assistance Evaluation Mission. 2 Due to the controlled interest rate environment banks were unable to compensate for the higher transaction costs

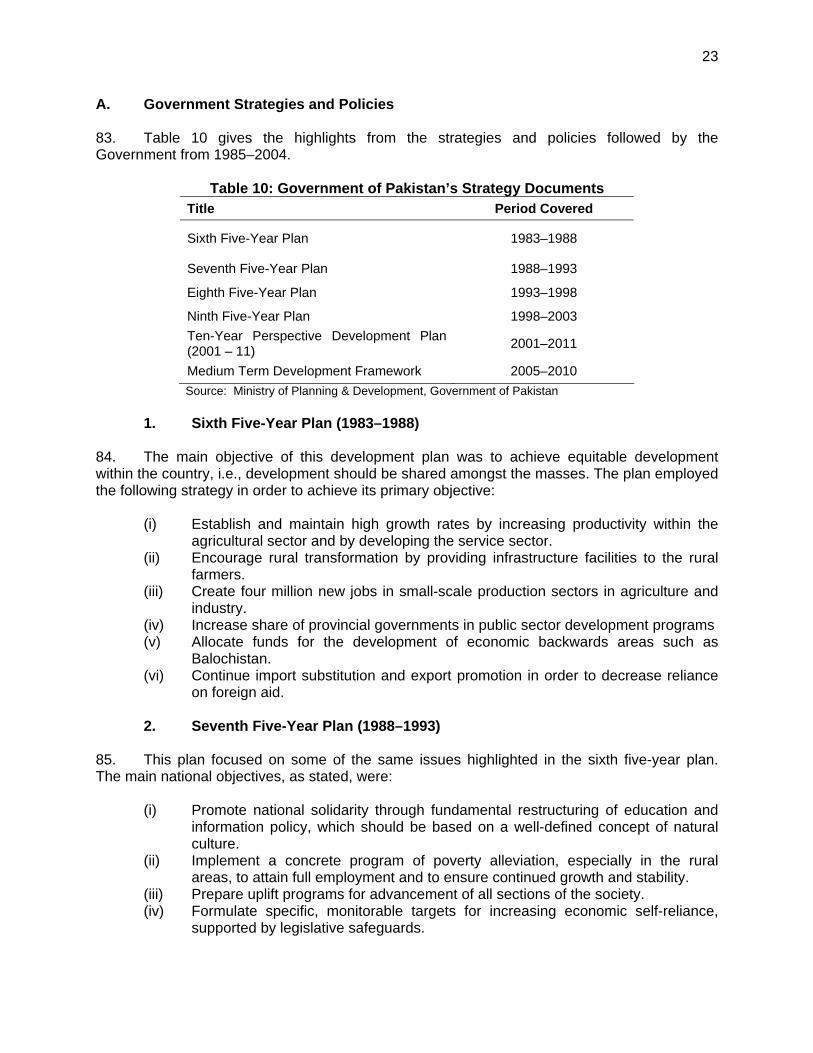

associated with lending to smaller businesses 3 Ministry of Finance. 2005. Economic Survey 2004–2005. Pakistan.

4

recovery, such as, actualization of government reforms aimed at deregulating and liberalizing key sectors of the economy, improvements in country’s infrastructure (physical, financial, and telecommunication), increasing demand for goods and services within the domestic markets, etc. Provided in Table 1 (below) is information on average growth rates that illustrate the trends discussed in this section.

Table 1: Average (Annual) Growth Rates Indicators

1980s 1999–2000

2000–2001

2001–2002

2002– 2003 R

2003–2004 P

GDP 6.45 3.91 1.8 3.1 5.1 6.4 Agriculture 5.44 6.09 -2.2 0.1 4.1 2.6 Manufacturing 8.21 1.53 9.3 4.5 6.9 13.4 Commodity Producing Sector 6.49 3.02 0.5 1.3 4.9 7.7 Services Sector 6.65 4.79 3.1 4.8 5.3 5.2 R = Revised, P = Provisional. GDP = gross domestic product. Source: Ministry of Finance. Economic Survey of Pakistan (various issues). Pakistan. B. Private Sector Constraints 13. Provided below are some of the main issues and challenges that have (and in most cases still continue to) hampered private sector participation in the country’s economic reality.4

1. Financial Constraints 14. Access to finance is one of the main hurdles discouraging increased private sector participation in the country’s economy. Even though opportunities to secure financing have increased over the years, there is still considerable shortfall in demand and supply for credit-related resources and services. Some of the main issues and challenges faced by the private sector in this regard include:

(i) lack of access to credit, (ii) stringent collateral requirements, (iii) procedural delays in loan disbursement, (iv) corrupt system for obtaining credit, (v) high cost for securing credit, and (vi) high interest rates.

15. Detailed analysis for this topic is provided in Chapter III.

2. Regulatory Constraints 16. Uneven and unpredictable enforcement of regulations (tax laws, tariffs, and export regulations) serve as a constraint for private sector participation. 17. Some of the main tax-related constraints include:

(i) high rates of income tax, 4 The constraint-related information is based on the findings of ADB’s Pakistan Resident Mission 2005 report titled

“SME Development in Pakistan, Analyzing the Constraints to Growth.”

5

(ii) high rates of sales tax, (iii) lengthy procedures for submitting income tax statements, (iv) uncertainty with regards to income and sales tax policies, and (v) slow pace and cost associated with resolving tax disputes.

18. Some of the main tariff-related constraints include

(i) high tariff rates on import of raw materials and intermediate goods, and (ii) unpredictable changes in tariff rates.

19. Some of the main export regulation-related constraints include

(i) cost of delay in obtaining duty drawbacks and sales tax refunds, and (ii) uncertainty of sales tax refund.

3. Infrastructure Constraints

20. Lack of adequate infrastructure facilities serve as a major impediment to private sector growth. Main constraints faced by the private sector in the country include

(i) high cost, poor quality of service, and unreliable supply of power; (ii) inefficient, unreliable, and costly transport network; (iii) widespread corruption within utilities providers; and (iv) high cost of establishing back up power.

4. Human Resources Constraints

21. Finding appropriate human resource capacity also serves as a constraint for the private sector. Provided below are the main human resources-related constraints faced by the private sector:

(i) workers are not educated enough; (ii) personnel are not adequately trained; (iii) lower and middle-level personnel lack requisite skills; (iv) even where workers had degrees or certificates, the quality of training and

education they had received was substandard; and (v) there is a significant mismatch between skills required by employers and the

training provided by educational/training institutions.

5. Market Constraints 22. Market constraints refer to issues and challenges faced by the private sector as a direct consequence of high degree of state control and inefficient regulation. Provided below are some of the main market constraints:

(i) lack of trust between suppliers and manufacturers/retailers significantly increase transaction costs,

(ii) high cost of contract repudiation increases cost of doing business for firms, (iii) competition from smuggled goods and the informal economy significantly affects

private sector participation for manufacturer as well as retailers, and (iv) rule of law.

6

III. FINANCE SECTOR PERFORMANCE AND ISSUES A. Introduction 23. ADB’s finance sector reform interventions constitute a major portion (79%) of its private sector assistance to Pakistan over the last 20 years. This emphasis on the financial sector was based on the assumption that a robust financial infrastructure was a prerequisite for establishing a private sector that would enable the country to achieve both its economic growth as well as its poverty alleviation objectives. 24. Pakistan’s finance sector can be broadly rationalized in two main categories—the banking sector and the non-bank financial institutions (NBFIs). The banking sector refers to a number of subsectors, such as commercial and retail banking, rural finance (agricultural and microfinance), and small and medium enterprise (SME) lending. As the name suggests, NBFIs refers to financial institutions other than banks, such as stock markets, leasing companies, insurance companies, etc. The remainder of this chapter provides information and analysis on the country’s key financial sectors and subsectors. B. Banking Sector 25. Information on the regulatory framework as well as the main sub-sectors of the banking sector is provided below.

1. Regulatory Framework 26. The regulator of the banking sector is the State Bank of Pakistan (SBP). Banking Companies Ordinance (BCO) 1962 is the main law governing the establishment and operations of commercial banking institutions and is administered by SBP. This law sets out certain key requirements for those entities interested in developing and/or operating commercial banking entities in Pakistan that include:

(i) Capital and Reserve Requirements. As of December 2004, all scheduled banks operating in Pakistan are required to maintain a minimum paid up capital (net of losses) of PRs1,500 million. This requirement will increase to PRs2,000 million by December 2005. In addition, banks are also required to maintain capital and unencumbered general reserves, the value of which is not less than 8% of their risk weighted assets (on both consolidated as well as stand alone basis)

(ii) Cash Reserves. The banks are required to maintain a cash reserve of a

percentage of their demand and time liabilities excluding the paid up capital, reserves and balance in the profit and loss account with the SBP. This ratio is changed from time to time in accordance with the demands of the monetary policy. No interest and/or profit is paid by SBP on these funds.

(iii) Liquid Assets. Banks are required to maintain liquid assets of not less than 80%

of the total time and demand liabilities in Pakistan.

(iv) Annual Accounts and Audits. As per the BCO, a bank is required to maintain the calendar year as its financial year, and its financial statements are required to be audited in accordance with 2nd Schedule of the BCO. Under this ordinance,

7

each bank will submit to the SBP, its audited accounts and the auditor’s report within 3 months of the financial yearend.

(v) Remittance of Profit. Foreign banks operating in Pakistan are allowed to remit

their net profit earned in Pakistan, subject to approval of SBP.

(vi) Number of Branches. As per SBP’s branch licensing policy there is no limitation on the number of branches that a bank can open in Pakistan, subject to fulfillment of SBP criteria. This policy requires that each bank will submit its annual branch expansion plan, 30 days before commencement of each calendar year during which it plans to open new branches.

27. In addition, SBP has also introduced Prudential Regulations for Corporate/Commercial Banks, SMEs, and Microfinance Institutions. These regulations are discussed in the next few sections.

2. Commercial/Retail Banking 28. The country’s banking sector has undergone a tremendous change over the last few years. The impetus for this change came about as a direct consequence of the severe financial strain Pakistan’s economy was going through in the eighties and nineties. During this time, there was a growing realization within the Government that private sector participation in the country’s financial markets would only happen once the Government started deregulating and privatizing these markets.5 29. In 1990, the country’s banking system was dominated by five commercial banks, which were all state-owned. The 1990 amendments to the BCO launched the process of financial sector reforms by allowing privatization of these state-owned banks. During the first round of reform, between 1991 and 1993, two of the state-owned banks (Muslim Commercial Bank and Allied Bank) were privatized. The reforms process was subsequently delayed for several years and resumed in early 2000s. With the privatization of the third large bank, United Bank Limited the domination of state-owned banks ended. After privatization in February 2004 of Habib Bank Limited, the share of banking system assets held by public sector commercial banks decreased to less than 25%.6 However, the privatization process is still not complete as the largest bank in the country, National Bank of Pakistan, with a market share of approximately 20%, remains state-owned and its privatization prospects are uncertain at this stage, although the Government divested approximately 25% of its capital in 2001–2003 (footnote 6). 30. The privatization of state-owned banks has been accompanied by a liberalization of the financial system and a significant increase in the number of local and foreign banks operating in the country. Worried by the health and soundness of the larger number of, and in some cases newer, banks SBP imposed a moratorium on the establishment of new banks in 1995, which still remains in force.

5 These deregulation and privatization reforms were a mandatory requirement stipulated by the International

Monetary Fund for assisting the Government out of its economic problems. 6 Technical Note: Condition of the Banking System in Pakistan. Joint IMF and World Bank Financial Sector

Assessment Paper, October 2004.

8

31. Up until the recent past, the retail banks were primarily focused on delivering financial services and support to the corporate sector and the needs of the households typically went unmet. Lending to individuals was mostly done in the form of fully secured loans against tangible liquid securities (usually, government securities, bank deposits, etc.). Consumer financing was untapped until a few years ago when surplus liquidity and slow credit growth from the corporate sector forced the retail banks to seek other avenues to enhance their asset base and profitability. 32. As shown in Table 2, consumer finance has been growing at a rapid pace. The “Others” category, which accounts for the largest share of consumer finance consists of personal loans (both secured and unsecured) as well as financing for consumer durables. Auto financing accounts for the second largest share in consumer financing followed in third place by credit cards. Mortgages have not gained a foothold in Pakistan’s financial markets and it is an area that will experience significant expansion in the short to medium term.7 This rapid expansion in demand for consumer finance has resulted in banks actively entering into other financial markets, such as leasing, etc.8

Table 2: Consumer Finance (PRs Billion)

Source: State Bank of Pakistan. 2003. Pakistan Financial Sector Assessment 2003. Research Department: Pakistan.

Item Jun-03 Sep-03 Dec-03 Mar-04 Jun-04 Credit Cards 6.7 8.0 8.9 9.7 11.2 House Loans 3.8 3.4 4.1 5.5 8.3 Auto Loans 15.8 16.9 22.2 27.6 33.1 Others 18.7 25.6 30.3 40.2 50.0 Total Consumer Finance 45.0 53.9 65.5 83.0 202.6 Growth Rate (%) 69.8 19.8 21.5 26.7 23.6 Total Loans 1,043.1 1,040.2 1,152.0 1,205.4 1,350.9 Consumer Finance as % of Total 4.3 5.2 5.7 6.9 7.6

33. Another interesting development in the country’s banking system has been the rising popularity of Islamic banking. In 2002, SBP exempted Islamic commercial banks from the moratorium on the establishment of new banks, and the first full-fledged Islamic bank, Meezan Bank, was licensed. Since then, several conventional banks have also opened branches that provide only Islamic financial services. The size of these Islamic banking institutions remains very small.9 Given the present administration’s and SBP’s commitment towards encouraging Islamic mode of financing, there is likely to be a rise in the number and type of Islamic financial institutions and services in the coming few years. 34. In order to provide the required regulatory support for consumer finance, SBP has developed and put in place regulations that provide for

(i) facilities to related persons, (ii) exposure against total consumer financing, (iii) total financing facilities to be commensurate with income, (iv) general reserve against consumer finance,

7 Problems with land title records are a major hurdle that needs to be overcome in order to realize increases in

mortgage transactions in the country. 8 Existing leasing companies were of the opinion that commercial banks entering the leasing market have created a

non-level playing field because they (banks) are not subject to the same (stringent) capital adequacy requirements as are the leasing companies.

9 According to SBP estimates Islamic banking assets account for around one percent of the total bank assets.

9

(v) bar on transfer of facilities from one category to another to avoid classification, (vi) margin requirements, and (vii) credit cards.

35. Additional detailed regulations have also been issued by SBP for auto loans, housing finance, and personal loans including loans for purchase of durables.

3. Rural Finance and Microfinance 36. There is widespread acceptance among decision and policy makers as to the need for developing credit products tailored for meeting the needs of the poor in Pakistan. Driving this is the fact that despite favorable macroeconomic circumstances within the country—poverty and inequality have been on the rise. For instance, 80% of the 14.3 million rural households earned less than $1 a day during 1998–1999.10 Moreover, the head count for rural and urban poverty for the same time period was 36.3% and 24.3%, respectively (footnote 13). 37. During the year ended June 2001, the formal sources jointly disbursed a total of 786,000 loans amounting to PRs56 billion ($0.94 billion), i.e., an average loan size of PRs71,246 or $1192.8 (footnote 13). Nongovernment organizations (NGOs) have disbursed about 100,000 loans. The nominal interest rates charged ranged between 13% and 22%. The outreach is merely 6% of the total rural households and the amount disbursed is 21% of the estimated demand (footnote 13). These numbers clearly suggest that the demand for micro/rural finance was not met and that a sustainable solution would need to be developed. 38. The SBP established a Rural Finance Committee (RFC) that, among other things, was tasked with coming up with a definition for rural finance. In their report, the RFC defined rural finance as

(i) credit requirements for agricultural activities, (ii) mobilization of rural savings, (iii) access to insurance services for risk mitigation, and (iv) payment systems that will allow flow of funds to and from the rural areas.

39. Realizing the importance of developing capacity to deliver rural finance support, over the last few years, the Government has been following a two-pronged strategy. The two main components of this strategy are:

a. Easing access to agricultural credit 40. According to the Government’s current development framework—the Medium Term Development Framework 2005–2010 (MTDF)—over the next 5 years, i.e., up until 2010, the agricultural credit requirements in the country has been estimated to reach PRs1,665 billion ($27.88 billion). Table 3 shows the distribution of the agricultural credit requirement.

10 ADB. 2000. Report and Recommendation of the President to the Board of Directors on Proposed Loans to the

Islamic Republic of Pakistan for the Microfinance Sector Development Program. Manila.

10

Table 3: Agricultural Credit Requirement Year Production Development Total (PRs billion)

Source: Planning Commission. May 2005. Medium Term Development Framework 2005–2010. Pakistan.

41. According to SBP, the total agriculture credit disbursement during 2003 was PRs58.9 billion ($.99 billion) to a total of 814,737 individual borrowers. It can be inferred from the information provided here that a major portion of agricultural credit requirement demand goes unmet, especially given that amount disbursed during 2003 is less than 22% of the projected demand for agricultural credit in 2005–2006 (Table 3). More information in this regard is provided in Tables 4 and 5.

Table 4: Credit to Agriculture Sector, Disbursements (PRs billion)

Source: State Bank of Pakistan. February 2004. Financial Sector Reforms and Pro-Poor Growth: Case Study of Pakistan. Pakistan.

42. In order to address the growing demand for agricultural credit, the Government in its MTDF commits to enhancing agricultural productivity by taking the following measures:

(i) In addition to ZTBL and provincial cooperative banks, major commercial and private banks will also provide agricultural credit.

11

(ii) Mark-up rates on agricultural credit will be reviewed by banks and reduced reasonably on the basis of market mechanisms.

(iii) One-window operation facilities will be further enhanced to make it more effective in meeting the farmer’s needs.

(iv) Special trainings will be developed for farmers and will be delivered by banks to create awareness and knowledge amongst them (farmers).

(v) Institutional credit will also be extended to rural non-farm sector including rural poor, tenants, agricultural artisans, women, and other disadvantaged groups by organizing rural communities.

43. It appears that one of the more tangible measures undertaken by the Government (and ADB) to address the shortfall in agricultural credit is the revitalization of ZTBL. The Government’s plans for ZTBL, previously known as the Agricultural Development Bank of Pakistan, involve cleaning up its balance sheet (high nonperforming loans portfolio) as well as its operations (commercializing the public sector organization) and then privatizing the institution. It appears that the Government’s continued support for ZTBL stems from its belief that ZTBL is ideally suited for serving as the key supplier of credit to the rural communities. The Government has invested quite heavily in trying to turn this organization around and the results have been mixed at best.11

b. Development of the Microfinance Industry 44. The second component of the Government’s strategy for addressing the shortfall in the country’s rural finance demand is by encouraging microfinance lending. The Government’s enthusiasm towards developing the microfinance industry lies in its belief that microfinance is a viable means for directly linking finance with poverty reduction. Currently, there are two specialized microfinance banks operating in the country (First Micro Finance Bank Limited and Khushali Bank). According to SBP, two other microfinance banks have been granted licenses and they became operational in 2005. Table 5 provides information on the microfinance sector in Pakistan. 11 ZTBL Chairman indicated that the organization was facing a number of serious problems, some of which are

discussed below: (i) ZTBL Board. As per the restructuring plan, ZTBL’s Board would be from the private sector. However, at the

moment, three members of the seven-member Board are secretaries from the federal government. Two of the remaining four are presidents of competing banks. The Chairman suggested that this situation, at the very least, poses as a conflict of interest.

(ii) Lending Rate Cap. ZTBL secures funds from SBP at 8% and it has a lending rate cap (announced by the President of Pakistan) of 8.5%. Chairman of ZTBL said that the bank will need at least a 6.5% spread in order to turn a profit.

(iii) Operational Issues. The bank faces formidable challenges such as, human resource capacity, operational inefficiency, technology, etc., and there is very little that has been done to address any of these issues.

12

Table 5: Micro Finance Sector in Pakistan (in PRs millions)

KB = Khushali Bank, FMFB = First Micro Finance Bank.

Item Sep-02 Dec-02 Mar-03 Jun-03 Sep-03 Advances Net of Provision KB 413.8 475.5 565.8 662.2 778.9 FMFB 4.38 17.61 31.0 49.8 58.2 Total Advances 418.2 493.1 596.8 712.0 837.1 % Change 17.9 21.0 19.3 17.6 Number of Borrowers KB 45,930 56,324 69,584 83,109 100,228 FMFB 169 713 1657 2,608 3,112 Total Advances 46,099 57,037 71,241 85,717 103,340 % Change 23.7 24.9 20.3 20.6 Number of New Borrowers During Quarter KB 16,827 10,394 13,260 13,525 17,119 FMFB 101 544 944 951 504 Total Advances 16,928 10,938 14,204 14,476 17,623 % Change -35.4 29.9 1.9 21.7 Average Loan Size KB 10,786.2 8,795.7 8,471.4 8,300.1 8,183.6 FMFB 25,662.7 24,697.1 20,304.8 19,406.1 16,263.2 Number of Branches KB 27 31 31 35 35 FMFB 3 8 9 10 11 Total No. of Branches 30 39 40 45 46

Source: State Bank of Pakistan. February 2004. Financial Sector Reforms and Pro-Poor Growth: Case Study of Pakistan. Pakistan.

45. In order to provide the required regulatory support to microfinance institutions (MFIs), SBP has developed and put in place legislations that provide for

(i) minimum capital requirements, (ii) exposure against contingent liabilities, (iii) maintenance of cash reserves and liquidity, (iv) statutory reserves, (v) depositor’s protection fund, (vi) restriction on certain types of transactions, (vii) maximum loan size, (viii) maximum exposure of a borrower from MFIs/other financial institutions/NGOs, (ix) rescheduling/restructuring of loans, (x) writing off of nonperforming loans, (xi) pricing of microfinance products and services, (xii) investment in shares of any body corporate, (xiii) undertaking of cash payments outside the MFI’s authorized place of business, (xiv) prevention of criminal use of MFI channels for the purposes of money laundering

and other unlawful management trade, (xv) audit and submission of accounts, (xvi) internal audit, (xvii) operational policies, and (xviii) restriction on election and appointment of directors.

46. Government’s efforts towards developing the country’s microfinance industry have yielded promising results. Initially, ADB assisted the Government in establishing the Khushali Bank—the first microfinance bank in Pakistan. Since then, microfinance has been gaining

13

ground in the country and a number of new players have started providing microfinance services. Unlike in the past when most institutions geared towards delivering rural finance relief were government owned and/or controlled, for the first time a new business model was utilized that was committed to establishing microfinance banks as commercially viable entities. However, since the microfinance industry has taken off, the Government’s (and ADB’s) continued support (financial and otherwise) for Khushali Bank is questioned and criticized by other microfinance providers.12 So far, it remains unclear whether or not developing a commercially viable microfinance business model is a sustainable proposition or not.13

4. Small and Medium Enterprise Finance 47. SME refers to those business organizations that employ no more than 250 persons or 50 persons depending on whether the organization is a manufacturing concern or a trading/service concern, respectively.14 In addition, the organization in question will also need to fulfill the following conditions:

(i) A manufacturing concern with total assets (excluding land) valued up to PRs100 million ($1.67 million) and net sales not exceeding PRs300 million ($5.02 million) as per the latest financial statement

(ii) A trading/service concern with total assets (excluding land) valued up to PRs50 million ($0.84 million) and net sales not exceeding PRs300 million ($5.02 million) as per the latest financial statement

48. Table 6 (below) provides additional information on how small and medium enterprises are defined.

Table 6: Definition of SMEs

Factor Small Enterprise Medium Enterprise Number of Employeesa

Up to 50 for manufacturing 36–99 for manufacturing

Up to 20 for services

21–50 for services

Total Asset Valueb PRs2–20 million for manufacturing Rs21–100 million for manufacturing PRs2–10 million for services

Rs11–50 million for services

Gross Salesc PRs2–20 million for manufacturing Rs21–100 million for manufacturing PRs2–10 million for services Rs11–50 million for services a Fulltime employees with at least six months employment prior to evaluation. b As per latest evaluations, and includes building and technical non-physical capital. c As per latest financial statements . Source: Medium Term Development Framework 2005–2010. 49. SMEs play a vital role in the economic reality of Pakistan as they constitute 99% of the nearly 2.3 million enterprises in the country and contribute 30% to the manufacturing sector and generate 25% of manufactured exports.15 Importance of SMEs in Pakistan is also driven by the

12 The continued support for Khushali Bank is viewed as an unfair advantage. It is interesting to note that Khushali

Bank is not a member of the apex microfinance organization in Pakistan, i.e., The Micro Finance Network. 13 According to the President of Khushali Bank results to date were on track. However, the bank needed to establish

a track record of commercial viability in the medium term. 14 SME Bank website (www.smebank.org) 15 Source: Planning Commission. May 2005. Medium Term Development Framework 2005–2010. Pakistan.

14

fact that increasing the number of SMEs can increase employment more than growth in large-scale firms.16 There is a growing realization in Pakistan that SMEs can play a vital role in enabling the country’s drive towards sustainable development. Among the many issues that constrain growth of SMEs (as discussed in Chapter III) by far the greatest impediment faced by these organizations is lack of financing.17 In order to provide financing support to the SME community, the Government in its MTDF plans to facilitate SME financing by:

(i) Encouraging venture capital for new SME start-ups (especially for those engaged in export oriented contract-manufacturing and designing, or electronic services).

(ii) Offering incentive schemes in order to streamline taxation and business registration for SMEs.

(iii) Improving weightage for skill levels, technology and export potential, and linkages with prime contractor, in addition to the usual evaluation schemes that are based upon physical assets and turnover.

50. Since January 2004, SBP has enforced SME-friendly regulations so as to provide better financing opportunities and options for such entities. According to these regulations, banks do not have to require collateral and instead can take into consideration asset conversion cycle and cash flow generation as the basis for loan approval. 51. ADB has been supporting the development of the SME sector in Pakistan through its SME Sector Development program. In addition to providing capacity building support to the SME sector, this program is also providing financing for the establishment and restructuring of the SME Bank (discussed below). 52. In 2002, the SME Bank was established and its primary purpose was stated as facilitation of credit to SMEs. This bank was created by combining two state-owned DFIs that were on the brink of collapse due to exceptionally high nonperforming loans portfolios. Since its creation, the SME Bank has been primarily preoccupied with cleaning up its books and operations. It is also in the process of developing prototypes for a range of SME banking functions, such as, lending programs, credit appraisals and delivery methodologies, standardized documentation, monitoring mechanisms, etc. The next step is for the SME Bank to be privatized—however, the timing, terms, and mode of this privatization remain unclear.18

5. Other a. Human Capital

53. Availability of appropriate human capital resources is a prerequisite for establishment of mature financial markets in Pakistan. Requirements for human resources differ significantly across the different banking subsectors. Provided below is a discussion on the various aspects of the human resources situation across different aspects of Pakistan’s banking system.

16 SME Financing: Issues & Strategies. Welcome address given at the SME Conference by the Governor State Bank

of Pakistan in Lahore on 10 May 2005. 17 According to a recently conducted World Business Environment Survey that covered 4,000 firms in 54 countries

found that SMEs cited inadequate access to financing as their primary constraint to growth. 18 The President of SME Bank and the Governor of the State Bank of Pakistan were not sure when this entity would

be privatized. They both talked about 2006 but with vagueness about “what” was going to be privatized. When pressed they talked about the banking license and the Mission team got the impression that the turn around and SME Bank’s penetration into the SME sector to meet the MTDF 2005–2010 intentions was less of a focus for them.

15

(i) Regulatory. SBP enjoys a high level of confidence within the banking sector. In addition to attracting and retaining the right skill mix to carry out its regulatory responsibilities, SBP has also instituted training programs for young professionals. So far, according to Governor SBP, the organization has trained 400 Graduate students who are then either absorbed by SBP itself or else seconded to other financial institution.19

(ii) Commercial Banks. There do not appear to be any issues associated with the commercial banks sourcing talent from the local markets.

(iii) Microfinance/Rural Finance/SME. Both SME and microfinance banking are commercially untested models. These organizations are investing heavily in technology and hiring/training fresh graduates for their respective market segments.20 ZTBL, too, is investing heavily in technology; however, the organization does not appear to have a coherent strategy towards addressing all of its human resources related issues.21

C. Non-Bank Financial Institutions

1. Regulatory Framework 54. The Securities and Exchange Commission of Pakistan (SECP) Act 1997 dissolved the old corporate sector regulator the Corporate Law Authority (CLA), which was a department within the Ministry of Finance, and replaced it with the SECP. On 1 January 1999, through a gazette notification, the Securities and Exchange Commission Act was enforced making the SECP fully operational. 55. In accordance with the requirements of the SECP Act, a commission and a board (the Securities and Exchange Policy Board) were established within the SECP. The Commission consists of commissioners some of whom are appointed by the federal government. However, a majority of them are from the private sector. Likewise, the Board consists of seven members, of which four are appointed by the federal government and the rest from the private sector. 56. Power to make regulations is shared between the Board and the Commission. Whereas the Board can make regulations on its own, the Commission can only "recommend" proposed regulations to the Board for their approval. All the powers and functions previously enjoyed by

19 The Governor SBP indicated that some of these graduates had been deputed to fill human capacity gaps at other

institutions such as the SECP and ZTBL. 20 Khushali Bank has put in place an aggressive recruitment strategy whereby the organization trains Graduate

students. According to the Bank the only downside is the high rate of turnover of these new recruits. 21 Correcting its human resources problems provides an interesting window into the broader issues faced by ZTBL,

some of these are detailed below: 1. Golden Hand Shake Scheme (GHS). As part of its restructuring efforts, ZTBL implemented a GHS Scheme

before it developed an understanding of what the organization’s human resource-related needs were. The obvious unintended outcome of this exercise was that most of the competent employees left the organization. Whereas in the past, one ZTBL field officer was required to cater to 300 clients—now, after the GHS, one field officer is required to meet the demands of 1,200 clients.

2. Technology. According to ZTBL’s Chairman, there are no computers in any of the organization’s field offices. In order to correct this deficiency the organization is investing substantially in developing technologies it can use; however, it remains unclear whether the organization has thought about how its personnel will be able to utilize these technologies.

3. Management and Culture. ZTBL is having problems in recruiting a management team that can help turn this organization around. One of the main issues that the new management will grapple with is the organization-wide operational inefficiency and lack of motivation.

16

CLA were transferred to the Commission with the exception of the powers to create regulations. Provided below are some of SECP’s main responsibilities:

(i) regulating issue of securities; (ii) regulating business in stock exchanges and any other securities markets; (iii) registering and regulating workings of stock brokers, sub-brokers, share transfer

agents, bankers to an issue, trustees of trust deeds, registrars to an issue, underwriters, portfolio managers, investment advisers and such other intermediaries who may be associated with the securities markets in any manner;

(iv) proposing regulations for the registration and workings of collective investment schemes, including unit trust schemes;

(v) promoting and regulating self-regulatory organizations in the securities industry and related fields such as stock exchanges and associations of mutual funds, leasing companies and other non bank financial institutions;

(vi) prohibiting fraudulent and unfair trade practices relating to securities markets; and

(vii) regulating substantial acquisition of shares and the merger and takeover of companies.

57. SECP Act clearly states that the Commission will regulate the NBFIs, which include development finance institutions, insurance companies, leasing companies, housing finance companies and investment banks. Certain activities of the NBFIs are, however, regulated by the SBP. There is no clear distinction in Pakistan with regard to the scope of activity of the investment and commercial banks with the result that the investment banks can perform almost all the functions of a commercial bank and vice versa. Full text of the SECP Act 1997 is provided as Appendix 3.

2. Stock Exchanges 58. The three registered stock exchanges in Pakistan are located in Karachi, Lahore, and Islamabad. Karachi Stock Exchange (KSE) is the biggest and most liquid stock exchange in the country. As of 31 October 2004, 661 companies were listed with a market capitalization of PRs1,478.6 billion ($24.75 billion) and with a listed capital of PRs396.4 billion ($6.64 billion).22

59. Membership of KSE is capped at 200 and the only way to secure membership is to purchase a seat from an existing member. Since June 1990, corporate entities can also become members of KSE and currently there are 106 such corporate members (nine of which are publicly traded companies).23 KSE is run by a 10-member board of directors that consists of five elected directors (elected from amongst the 200 members of KSE), four non-member directors (elected from various trade and/or professional bodies), and the Managing Director of the stock exchange. The Chairman is elected by the Board from amongst the elected directors. The operational and administrative activities of the stock exchange are managed by the Managing Director who also is the full time Chief Executive of the exchange. 60. According to the KSE classification, stock market consists of 34 sectors. In terms of market capitalization, oil and gas exploration, communication, commercial banks, and oil and gas generation and distribution are the largest sectors investment-wise that between them

22 Information secured from Karachi Stock Exchange. 23 Corporate members are required to satisfy certain minimum requirements, such as minimum paid up capital of

these entities should be PRs20 million.

17

account for over PRs100 billion ($1.67 billion). Also counted among the largest sectors are power generation and fertilizers. Table 7 provides more detailed information on KSE market activity. 61. The other major stock exchange is the Lahore Stock Exchange, which accounts for around twenty percent of the transactional volume but appears to be more technologically savvy and innovative than the KSE.24

62. Regulation of the stock market and securities business in Pakistan is principally governed by the Securities and Exchange Ordinance 1969, and the rules prescribed pursuant to it. The regulatory body entrusted with the powers conferred on the government under this law is the SECP. The SECP is responsible for supervising stock exchanges and their members. It also licenses investment advisers, regulates the contents of the prospectuses and enforces legislation pertaining to companies and corporate securities. Stock exchanges are also expected to self-regulate and to establish standards for listing and dealing in securities, regulating the conduct of stock exchange members, and organizing the smooth clearing and settlement of trades executed.

24 According to LSE management they have plans to open stock exchange field offices in various major cities of

Punjab. They believe that having access to trading floors will go along way in winning over investors from those cities to invest and trade on the LSE.

Table 7: Karachi Stock Exchange Market Activity

18

Year Ended 31 December 5 August Item 2000 20022001 2003 2004 2005

Cumulative Increase/Decrease Since 2001 n.a. n.a. 1,194 2,964 4,711 5,817

Dividend Yield of KSE – 100 Index Companies 7 15 9 6 6 5 Price Earnings Ratio of KSE – 100 Index Companies 10 7 13 11 12 11 KSE All Share Indexb 946 820 1,671 2,833 4,105 4,811Year-Wise Increase 71 (125) 851 1,162 1,272 707 Cumulative Increase/Decrease Since 2001 Total Number of Listed Companies 762 747 711 701 661 659 Total Listed Capital 236,459 235,683 291,241 313,267 405,646 447,150 Total Market Capitalization 382,730 296,144

595,206

951,447

1,723,454

2,082,660

New Companies Listed During the Year 3 3 4 6 17 10 Listed Capital of New Companies 2,035 2,885 6,318 4,563 66,837 17,783Number of Companies Listed Under: Voluntary Delisting and Buy Back of Shares 3 5 9 8 15 8 Due to Merger 1 7 16 8 39 3 Involuntary Delisting 2 7 15 0 3 1 New Debt Instruments Listed During the Year 3 5 16 6 5 6 Listed Capital of New Debt Instruments 648 5,658 8,656 2,749 4,775 8,125

Average Daily Turnover (T+3) YTDc 187 97 171 309 344 387Average Value of Daily Turnover (YTD) 7,130 3,134 5,963 15,686 17,409 35,557

Average Daily Turnover (Future) YTDd n.a. 15 35 54 70 129Average Value of Daily Turnover (YTD) n.a.

314

1,721

3,907

4,914

17,440

n.a. = not available, KSE = Karachi Stock Exchange, YTD = year-to-date. a The KSE Exchange was rolled out in November 1991. b KSE All Share was introduced in September 1995. c Includes March 2005 T+3 average turnover of 513 million shares with average trade value of PRs53,265 million (excluding which the average daily T+3 turnover

is 365 million shares and average trade value of PRs32,402 million). d Includes March 2005 Future average turnover of 315 million shares with average trade value of PRs50,749 million (excluding which the average daily Future

turnover is 96 million shares with the average trade value of PRs11,624 million).

19

3. Insurance 63. Pakistan’s insurance industry is relatively small as compared with the insurance markets of other countries with more developed and/or mature financial markets. As is the case in the insurance markets of other developing countries, Pakistan’s insurance industry is small in proportion to its gross domestic product (Table 8).

Table 8: Cross-Country Comparison of Insurance Sectors (% Insurance Contributions to GDP)

Countries Non-Life Life Total

USA 4.3 4.5 8.8 Brazil 1.8 0.4 2.2 Mexico 0.9 0.9 1.8 UK 3.1 12.7 15.8 China 0.7 1.1 1.8 India 0.6 1.7 2.3 Malaysia 1.6 2.1 3.7 Indonesia 0.6 0.6 1.2 Nigeria 0.6 0.1 0.7 Kenya 1.9 0.7 2.6 Pakistan 0.3 0.2 0.5

Source: Pakistan Financial Sector Assessment 2003, State Bank of Pakistan. 64. The largest influence and activities generated within Pakistan’s insurance market (both life and non-life) are by the state-owned companies. The state-owned companies National Insurance Company Limited (NICL), Pakistan Reinsurance Company Limited (PRCL) and State Life Insurance Company (SLIC) are, like private sector insurers, subject to the provisions of the Insurance Ordinance and therefore to the jurisdiction of the SECP. 65. The insurance sector in Pakistan can broadly be rationalized into two main classes—life insurance and non-life insurance. The country only has one reinsurance company that carries out reinsurance activity. Details for the two main classes are provided below.

4. The Life Insurance Sector

66. Life insurance sector activity in Pakistan currently accounts for approximately 0.2% of GDP, which is far below any expected saturation level, and appears to have great scope for expansion. 67. Even though a major portion—i.e., 76% of the premium income—of the sector is dominated by the state owned/run SLIC there are also four private sector companies.28 In addition, life insurance is also provided by Postal Life, a service under the control of the Ministry of Communications, and short term life insurance may be offered by non-life companies.

28 Ernst & Young. 2005. Pakistan Insurance Sector—A Report to the Asian Development Bank under TA 4033-PAK.

United Kingdom.

20

68. According to the Insurance Ordinance, effective 31 December 2004, the minimum paid-up capital requirement for life insurance providers was set at PRs150 million ($2.51 million). Failure of any insurer in complying with these requirements would lead to the insurer in question being prevented from operating in this sector. 69. The overall structure of this sector is such that the activities appear to be concentrated within the public sector. There appears to be a significant role that the private sector can play in shaping the future of this market, considering that there are plans to privatize the state owned corporations, such as SLIC, etc.

5. The Non-Life Insurance Sector

70. The non-life insurance sector activity in Pakistan currently represents 0.3% of the country’s GDP. This represents a level of penetration that is, as for life insurance, well below levels that would be considered as saturation; this has been estimated at approximately 5% (footnote 32). 71. An increasing popularity of leased motor vehicles explains this sector’s dependence on motor insurance—this type of insurance accounted for 35% of net premium revenue in 2002 and 42% in 2003 (footnote 32). However, this class of business generated underwriting losses in both years. Profit was mostly generated in the two other largest classes (after motor insurance), such as fire and marine, and aviation and transport (mostly marine cargo) business. 72. An important aspect of the sector to consider involves the difficulties faced by market participants due to the aftermath of 11 September 2001. The reinsurance rates increased as a consequence of these events and in some cases terrorism cover was only available on a selective basis.29

73. Overall, the non-life sector has undergone significant growth and consolidation over the past few years. Consolidation has been driven in part by the increased capital requirements introduced by the Insurance Ordinance, which reached their most recent minimum equity level of PRs80 million ($1.34 million) with effect from 31 December 2004. Further important developments within this sector involve aggressive strategies by banks to provide these insurance services. Such strategies can involve banks either acquiring insurance companies or establishing separate in-house departments. Some examples of this trend include Adamjee Insurance being acquired by Muslim Commercial Bank, and Agha Khan Foundation for Economic Development, the owner of New Jubilee Insurance and New Jubilee Life, has acquired Habib Bank Limited. Another established retailer, Pakistan Industrial Credit & Investment Corporation, has established a non-life insurer and is in the process of trying to set up a life insurance company.

6. Leasing 74. Since the creation of the first leasing company in Pakistan in the mid-80s, leasing has remained an important segment within the country’s financial markets. As was the case with retail banks, initially, the focus of these leasing companies was on catering to the needs of the 29 Under the Financial (Non-Bank) Markets and Governance Programme Loan, ADB will provide a political risk

guarantee with counter-guarantee from the Government of Pakistan for political violence related risks (including terrorism and sabotage) for which insurance in Pakistan is not readily available. The counter guarantee has yet to be signed by the Government.

21

corporate sector. However, slow economic growth and a slump in profitability forced these leasing organizations to broaden their business focus and offer services to individual consumers. 75. As of December 2003, the leasing industry was made up of 27 companies and their total assets stood at PRs45.8 billion ($0.77 billion). Table 9 provides a breakdown of the leasing industry assets in 2003.

Table 9: Breakout of Lease Finance

Asset Type 2002 2003 Plant and Machinery 54% 54% Vehicles 32% 35% Equipment 10% 8% Other 4% 3% Total 100% 100% Source: State Bank of Pakistan.

76. The comparison for the 2 years (Table 9) suggests that the asset composition over this time frame remained largely unchanged. Plant and machinery was unchanged and accounted for the largest share of the leasing industry assets. The 3% rise in vehicles can be attributed to the intense competition between commercial banks and leasing companies to deliver leasing services for vehicles.30 77. Since the development of the SECP, leasing companies have been categorized as non-bank financial companies and are regulated by the SECP in accordance with the 2003 Non-Banking Finance (Establishment and Regulations) Rules. Last 3 years have witnessed increased consolidation across the industry as smaller companies merge their resources in order to satisfy the increased minimum paid-up capital requirements prescribed by the SECP.

7. Other 78. Provided in this section are important issues as they relate to the development of the NBFI sector.

a. Badla Phaseout 79. “Badla” is a facility for financing share purchases and is extended by brokerages and banks, which allows buyers to obtain highly leveraged positions in the market. The extent of leverage through such non-bank financing is not transparent and underlying security transactions are typically speculative. This directly results in market manipulation and increases systemic risk. The need to phase out Badla is obvious and is seen as a growing pain that many other financial markets in different countries have also had to overcome in order to realize mature and well-functioning capital markets. However, so far SECP failed in its efforts to phase

30 The leasing companies interviewed during the Evaluation Mission stated that provision of leasing services by

commercial banks was a major cause for concern for them as it gave the commercial banks an unfair advantage, stemming from the fact that leasing companies, as non-bank financial intermediaries, have to comply with more stringent requirements of the SECP; whereas, the commercial banks are regulated by the State Bank of Pakistan and are not subject to any such restrictive requirements.

22

out Badla trading.31 The drop in liquidity that occurred as a result of the proposed phase out served as the deterrent for the regulator (SECP) and it quickly reversed its decision.32 The unavailability of a viable alternative to replace Badla has been identified as the primary deficiency of the failed phaseout plan.33 The Badla debacle contains interesting insight into the effectiveness of SECP as the regulator for the NBFI market.

b. Futures and Commodities Market 80. Developing the futures and commodities markets in Pakistan appear to be a prerequisite for the Badla phase out, as well as for broadening and deepening the country’s financial markets. Progress in developing these markets has so far been limited. Currently, the only solution available for futures trading is a 30-day forward contract. On the other hand, the development of the commodities market in Pakistan is currently on hold pending the drafting and implementation of the Futures Act. According to the National Commodities Exchange Limited, the company has been ready to go live since mid-2004; however, it has been told to wait till the Futures Act is instituted.34

8. Human Capital 81. Unlike the banking sector institutions, the non-bank side of the financial industry faces an uphill task as it tries to develop its human resource capacity. This matter is further complicated by the fact that most of these institutions are relatively new and they have to constantly adjust to the changing regulatory and other requirements of a growing market. This appears to ring true for both the regulator as well as the market players. There is broad-based consensus in the market that SECP is finding it hard to effectively regulate the NBFI market. Many attribute SECP’s deficiency in enforcement powers to it (SECP) not having the breadth of expertise that an effective regulator is required to have. On the other hand, market players suggested that it would be useful to develop certification and training modules that will educate market players and investors about the risks associated with their investments.

IV. STRATEGIES AND POLICIES 82. This chapter discusses Government and ADB strategies and policies that were geared towards enhancing private sector participation in the country’s economy.35

31 According to the SECP Chairman, he had worked on the proposed Badla phase out for over a year and had

secured agreement from all the key stakeholders. 32 India has also undergone a similar exercise whereby plans to phase out speculative trading were rolled back and

then later implemented. 33 Stock Market Review Task Force. June 2005. Report on the Review of Stock Market Situation, March 2005.

Pakistan. 34 According to the Managing Director of the National Commodities Exchange Limited, instead of drafting and

implementing a new Futures Act, a more effective option would be to modify and/or amend the existing Securities Act and pointed to efforts in India, where an existing Securities Act was modified and implemented. He also added that Pakistan’s rural farmers would benefit much like the farmers in India, where the farmers can get indicative prices for their commodities off of monitors placed in rural post offices.

35 As is the case with most public sector planning documents, the Governments’ planning documents represent political aspirations more than the operational realities. The articulated “what” is planned tends to be tuned to current political and donor themes while the “how” is most often not stated.

23

A. Government Strategies and Policies 83. Table 10 gives the highlights from the strategies and policies followed by the Government from 1985–2004.

Table 10: Government of Pakistan’s Strategy Documents Title Period Covered

Sixth Five-Year Plan 1983–1988

Seventh Five-Year Plan 1988–1993

Eighth Five-Year Plan 1993–1998

Ninth Five-Year Plan 1998–2003 Ten-Year Perspective Development Plan (2001 – 11) 2001–2011

Medium Term Development Framework 2005–2010 Source: Ministry of Planning & Development, Government of Pakistan

1. Sixth Five-Year Plan (1983–1988)

84. The main objective of this development plan was to achieve equitable development within the country, i.e., development should be shared amongst the masses. The plan employed the following strategy in order to achieve its primary objective:

(i) Establish and maintain high growth rates by increasing productivity within the

agricultural sector and by developing the service sector. (ii) Encourage rural transformation by providing infrastructure facilities to the rural

farmers. (iii) Create four million new jobs in small-scale production sectors in agriculture and

industry. (iv) Increase share of provincial governments in public sector development programs (v) Allocate funds for the development of economic backwards areas such as

Balochistan. (vi) Continue import substitution and export promotion in order to decrease reliance

on foreign aid.

2. Seventh Five-Year Plan (1988–1993) 85. This plan focused on some of the same issues highlighted in the sixth five-year plan. The main national objectives, as stated, were:

(i) Promote national solidarity through fundamental restructuring of education and information policy, which should be based on a well-defined concept of natural culture.

(ii) Implement a concrete program of poverty alleviation, especially in the rural areas, to attain full employment and to ensure continued growth and stability.

(iii) Prepare uplift programs for advancement of all sections of the society. (iv) Formulate specific, monitorable targets for increasing economic self-reliance,

supported by legislative safeguards.

24

86. An interesting development that took place during this plan period was that sectors that used to be reserved for the public sector were opened to the private sector. During this plan period two banks and 63 industrial units were privatized.

3. Eighth Five-Year Plan (1993–1998) 87. This plan was released by the Government in June 1994. Unlike the previous plans, this plan outlined private sector led investment as a priority. Provided below are some of the main objectives as stated in this plan.

(i) Improve enabling environment by a. providing adequate services and physical infrastructure, b. providing education and training, c. providing better health coverage, d. strengthening capital markets, and e. deregulation and privatization.

(ii) Develop supportive policies for fiscal, monetary, foreign exchange, and trade

regimes. 88. The development and articulation of a private sector led investment agenda by the Government constituted an important milestone in the Government’s planning process. Also, this signaled the public sectors continued commitment to deregulating and liberalizing the country’s financial sector.

4. Ninth Five-Year Plan (1998–2003) 89. This plan was not officially announced and/or implemented by the Government. The reason for this was because the Government was dealing with the fallout from its nuclear testing (e.g., international sanctions, etc.). During this timeframe, the Government was mostly concentrating on achieving short term economic stabilization by tightening its fiscal and monetary policies.

5. Ten-Year Perspective Development Plan (2001–2011) 90. This plan laid out Government’s intentions to bolster the country’s financial sector by articulating a wide variety of measures. Provided below is information on the Government’s stated intentions as per this plan.

(i) New financial products will be introduced in order to cater to the varying needs of depositors.

(ii) Continue to auction investment bonds for those institutional investors who are interested in investing in government securities.

(iii) Forge ahead with privatization plans for commercial banks, and Corporate Industrial Restructuring Corporation was set up to deal with nonperforming loans.

(iv) Promulgate bankruptcy laws in order to streamline dispute resolution mechanism.

(v) Strengthen capital markets by supporting development of regulatory frameworks for different financial products (such as pensions) by the SECP.

25

(vi) Microfinance initiatives, such as Khushali Bank, would encourage savings at the grassroots level (i.e., microfinance banks would only lend if the applicant has already been saving).

(vii) Special measures were being taken to extend credit to SMEs—credit of PRs2 billion ($0.03 billion) would be made available for development of SMEs in priority sectors.