18

Palm Dates Value Chain Report

Palm Dates Value Chain Report

Page 2 of 18

PALM DATE VALUE CHAIN

TABLE OF CONTENTS

1. Value Chain characteristics ................................................................................................................................... 3

1.1 Chain actors and recent interventions ................................................................................................................ 7

1.2 Challenges and constraints in the palm dates sector ........................................................................................ 10

2. Vision................................................................................................................................................................... 12

2.1 Scenarios ........................................................................................................................................................... 13

2.2 Needed systemic change .................................................................................................................................. 13

2.3 Proposed strategy and interventions ................................................................................................................ 14

2.4 Gender dynamics .............................................................................................................................................. 17

2.5 Risk analysis ...................................................................................................................................................... 17

Page 3 of 18

PALM DATE VALUE CHAIN

Palm Dates Value Chain

This report provides a description of the actual situation for the palm dates value chain in

the Gaza Strip, a mid-term vision for a more effective and inclusive palm date market

sector, constraints and scenarios that have to be taken into account as well as proposed

strategies to enhance systemic changes in the sector necessary to progress towards the

mentioned vision. Specific attention is given to gender dynamics and risk analysis.

1. Value Chain characteristics This study focuses on palm dates production in Deir Al-Balah, as well as in the eastern

villages of Khan Younis, being the areas most known in the Gaza Strip for their palm

date production. In these areas there are approximately 1.430 palm date producers1, of

whom only 60 are women. The Al-Ahlyia Association for the Development of Palms &

Dates identifies roughly 663 small scale farmers (<20 trees), 572 medium scale farmers

(20-60 trees) and 195 large scale producers (60+ trees). In Deir Al-Balah there are

approximately 70,000 trees, while another 30,000 are found in the villages east of Khan

Younis2.

Table 1 Classification and gender disaggregation of producers

Deir Al-Balah Total Women Men Percentage

Small scale producers 471 18 453 47%

Medium scale producers 371 16 355 37%

Large scale producers 160 8 152 16%

Total 1.002 42 960 100%

Eastern villages of Khan Younis

Total Women Men

Small scale producers 192 10 182 45%

Medium scale producers 201 7 194 47%

Large scale producers 35 1 34 8%

Total 428 18 410 100%

The main variety of trees grown is called Hayani, representing 90% of all palms in Gaza.

Other varieties include the Ameri, Berhi and Almjul. There is one single harvest season

per year and, for mature trees, the average net production per tree is 150kg of dates

(taking into account losses of roughly 10-20%). With 100,000 trees in Deir Al-Balah and

the eastern villages of Khan Younis, this equates to approximately 15,000 tonnes of

dates per year produced in these areas alone. Local dates produce is perceived by

1Al-Ahlyia Palm Data Association data from household survey “Field survey to count the number of palm date trees in the

Deir Al-Balah, as well as in eastern villages of Khan Younis”

2 The statistical data with the palm date association puts the number of trees at around 250,000 in all theGaza strip. The

Ministry of Agriculture places the number of trees in Gaza strip at around 150,000. However, there is some uncertainty

about what trees were counted (eg young trees, single household trees etc).

Page 4 of 18

PALM DATE VALUE CHAIN

the local population and consumers to be a „safe‟ food commodity, as only a very small

amount of pesticides is used in its production, and usually only one time per season.

As for other agricultural goods, demand is largely driven by price. Imported products

(both dates and processed products) tend to be sold for higher prices. For fresh dates

however, supply is available only for a short season (after harvesting), while consumer

demand is spread longer in the year. When there is a glut, supply outstrips demand. At

all other times there is high demand outside peak harvest seasons. Processed can

extend the life of the produce, but is still perceived to be low quality when from Gaza.

For processed products, especially date paste, there is a strong growing local market,

provided products are considered of good quality, are well-branded, packaged and

marketed.

Table 2 Local production and total supply of palm date fruits

Tonnes Percentage of total

Locally produced 5.135 93%

Imported 385 7%

Total supply 5.520 100%

*Source: Ministry of Agriculture 2012. Note, calculating with a production of 150kgs/tree, this

equates to 36,800 local palm trees producing. The difference between this number and the

number of palm date trees cited by MoA in Gaza can be attributed to not all trees being

pollinated, some trees being too young to produce, and some date production being consumed at

the producer household and thus not being counted.

In general, palm date production requires a relatively small amount of inputs (fertilisers

and pesticides), costing some 20NIS per tree. Palm trees do not require a huge amount

of water, approximately 50m3 of water per year, and they are saline tolerant. Roughly 20

trees per dunum can be planted although most often trees are scattered around the

borders of dunums. This makes them a suitable crop for Gaza growing conditions.

The main production activities include pruning, trimming, pollination and punch hanging,

and are carried out by men, while women‟s involvement in the production cycle consists

primarily in the harvesting of dates. The production itself does not require intensive

labour as each dunum (1000 square meters)of land cultivated with 20 trees requires 1

man worker and three women engaged in the harvesting (picking up of dates).

Altogether, costs of wages add up to around 50NIS per tree. However, it should be

noted that small-scale producers (<20 trees) and medium-scale producers (20-60 trees)

represent small family farmers who mostly rely on unpaid family labour, thus saving

costs as male family members carry out production activities, while women family

members engage in harvesting. Large scale producers (60+ trees) employ temporary

labour ranging from 2-8 workers for a total period of 2 months (as average per year), the

majority of which are women. Large producers also use family labour to reduce

production costs.

Page 5 of 18

PALM DATE VALUE CHAIN

In terms of marketing, about 50% of total production is short sold by producers to traders

at the beginning of the season. In fact, there is a custom in the Gaza Strip of booking the

palm date tree before the harvesting period (this selling agreement is called a short

selling to traders). Each mature tree (approximately 150kg of dates) can be booked for

approximately 200 NIS.

This short selling is important for many producers because at harvest time there is an

oversupply of local (and possibly also imported) dates on the market making it difficult to

find buyers who give reasonable prices. This method ensures a guaranteed income to

the producers without the risks associated with dumping prices3 coupled to oversupply at

the peak of the harvest season, as harvested ripe dates are subject to spoiling very

quickly after harvesting (1-2 days) unless stored in cold storage facilities. Furthermore,

the limited capacity (as commented below a major problem is lack of fuel for the cold

storage units currently in Gaza with only 5 of 20 currently running) and high cost of cold

storage also affect the marketing chain. Another strategy used by producers is

processing of dates into date paste, syrups or other products.

Around 25% of total production is sold by farmers to wholesalers. The average price is 1

NIS/kg of dates, so the selling price for 1 tree (150kgs) is approximately 150NIS. From

the sale price the farmer bears the cost of a 6% fee of on the total transaction (9

NIS/150kgs) to be paid to the wholesaler. This average price disguises a great deal of

market fluctuations. Typically a farmer does not sell all the produce at once or even

using the same channels or buyers. The farmer will harvest at several moments,

depending on whether the date is ripe or pre-ripe and according to market

flows/demands. The price for 1 kg of dates ranges between 0.5 NIS-3 NIS/kg.

Around 15% of total production is sold directly by farmers to retailers. The average

selling price is 2NIS/ kg, meaning 300NIS per tree (150kgs/tree). Unlike selling to

wholesalers, this transaction does not require the payment of fees. As described above,

seasonal price fluctuations might range from 1.5 – 4 NIS. While this marketing channel

receives higher income, it also comes with higher risk. Indeed due to the low capacity of

storage, buyers have a limited time frame during which they can sell dates before they

spoil and thus invest considerably more efforts to timely negotiate with buyers and hand

the products to them.

Around 10% of total production is sold directly to micro-enterprise processors (many of

which are run by the Al-Ahlyia Association for the Development of Palms & Dates) for

date paste or other food processing products (syrup, jam etc.). The average selling price

is 1.5-2 NIS/kg.

3 At the time of harvesting there is a glut of dates in the market and prices can fall markedly, rising again

near the end of the season.

Page 6 of 18

PALM DATE VALUE CHAIN

Table 3 Income per palm date tree (NIS) for producers selling their fresh produce

Farmer to trader (short

sell)

Farmer to wholesaler

Farmer to

retailer

Farmer to processor

Average price (range) NIS

1.33 1.5 (0.5-3) 2 (1.5-4) 1.5 (1.5-2)

Average Income 200 225 300 225

Fee 0 13.5 (6%) 0 0

Labour 50 50 50 50

Inputs 20 20 20 20

Average profit per tree (~150kgs)

130 141.5 230 155

Average profit per tonne

867 943 1533 1033

In terms of generated income, there are no differences between men and women

producers as the selling price is usually the same.

The processing units run by the Al-Ahlyia Association, mainly involve women in the

processing of date pastes, syrups and jam. There are 120 employees, including 110

women. This processing unit involves women workers in labour-intensive, seasonal, low-

paid work. Women workers are usually employed for a temporary period of time (2-4

months) yearly, earning about 700 NIS per month. The unit is managed by two

supervisors, a woman who is a general supervisor and a man who oversees technical

production during the processing stages. Production quantities are forecast based on

prior product requests from consumers, and are the responsibility of two employees

within the association. Usually the association decides on the packaging, branding and

marketing of products for different channels, namely: the supermarkets, small shops,

local markets and bakeries.

In addition, many women process their pastes, jams, and syrups at home for both

household consumption and trade to neighbours, and local market places, though the

latter is done on a much lower scale and scope (around 10% of total market; mainly for

household consumption and some local petty trade). A small number of large-scale

traders also engage in the processing of dates into date pastes and jams, and rely on

women‟s labour for processing. Labour costs add up to around 150 NIS/150kg to the

total cost of production for these traders. The marketing of processed products is usually

done by small scale producers themselves, with only 10% of women actually

participating in marketing activities, especially female-headed households.

Page 7 of 18

PALM DATE VALUE CHAIN

Table 4- Income per palm date tree (NIS) for producers processing date paste at

the household level

Farmers/traders to consumers Using family labour

for processing

Farmers/traders to consumers

Using hired labour for processing

Average price (range) NIS/kg 10 (9-11) 10 (9-11)

Average Income 525 525

Fee 0 0

Labour 50 200

Inputs 20 50

Average profit per tree (~150kgs) 455 275

Average profit per tonne 3033 1833

Dates are consumed by a wide section of consumers across the Gaza Strip. The

majority of consumers buy fresh dates, with most consumers preferring ripe dates over

pre-ripe dates. Dates are particularly popular during specific seasons like Eid Al Adha

and Ramadan.

Harvested ripe dates are subject to spoiling very quickly after harvesting (1-2 days)

unless stored in cold storage facilities. Some traders (and occasionally large producers)

are able to book cold storage in one of the 5 working cold storage facilities in Gaza

(there are around 20 in total in Gaza but many are not operational largely due to fuel

shortages). Cold storage units have a capacity of 100 tonnes, and to book 1 tonne of

dates for storage costs 200 NIS per month. Storing for one month is usually long enough

for market prices to rise again following the glut. Usually this option is only available to

traders.

Low-income consumer households process their own date paste and jam for household

consumption. Middle- and high-income households tend to purchase processed date

products from retailers. Most consumers buy from central marketplaces due to

freshness, quality and lower prices. Others buy at higher price at supermarkets or from

mobile sellers when in need of smaller quantities.

1.1 Chain actors and recent interventions

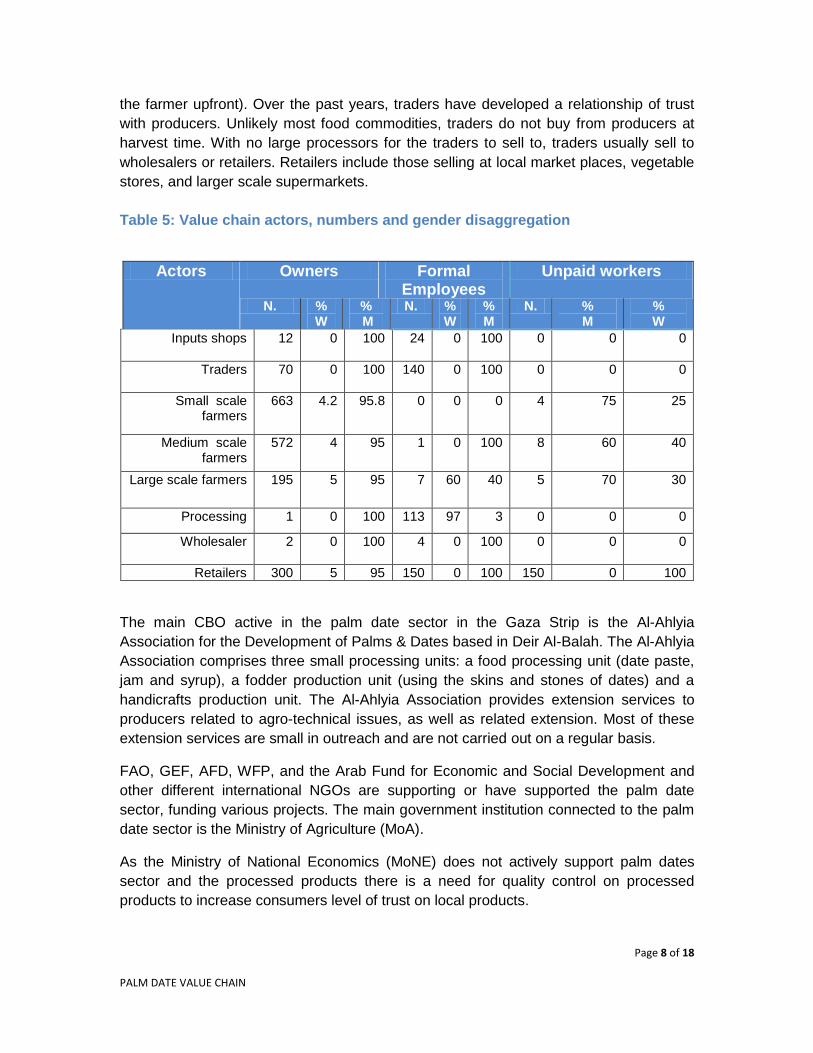

Producers can be categorised as small-scale (<20 trees), medium-scale (20-60 trees)

and large-scale (>60 trees). Input suppliers mainly supply pesticides, seedlings,

fertilisers, and other farm tools. Wholesalers work as intermediaries between

farmers/traders and retailers. Wholesalers sell on an auction basis and the supplier

(farmer or trader) and buyer (retailers) pay a fee of 6% to the wholesaler. The wholesaler

is an intermediary who does not sell to the public. Traders usually buy from producers on

a short-sell basis (i.e. they book the crop around the start of the season and pay cash to

Page 8 of 18

PALM DATE VALUE CHAIN

the farmer upfront). Over the past years, traders have developed a relationship of trust

with producers. Unlikely most food commodities, traders do not buy from producers at

harvest time. With no large processors for the traders to sell to, traders usually sell to

wholesalers or retailers. Retailers include those selling at local market places, vegetable

stores, and larger scale supermarkets.

Table 5: Value chain actors, numbers and gender disaggregation

Unpaid workers Formal Employees

Owners Actors

% W

% M

N. % M

% W

N. % M

% W

N.

0 0 0 100 0 24 100 0 12 Inputs shops

0 0 0 100 0 140 100 0 70 Traders

25 75 4 0 0 0 95.8 4.2 663 Small scale farmers

40 60 8 100 0 1 95 4 572 Medium scale farmers

30 70 5 40 60 7 95 5 195 Large scale farmers

0 0 0 3 97 113 100 0 1 Processing

0 0 0 100 0 4 100 0 2 Wholesaler

100 0 150 100 0 150 95 5 300 Retailers

The main CBO active in the palm date sector in the Gaza Strip is the Al-Ahlyia

Association for the Development of Palms & Dates based in Deir Al-Balah. The Al-Ahlyia

Association comprises three small processing units: a food processing unit (date paste,

jam and syrup), a fodder production unit (using the skins and stones of dates) and a

handicrafts production unit. The Al-Ahlyia Association provides extension services to

producers related to agro-technical issues, as well as related extension. Most of these

extension services are small in outreach and are not carried out on a regular basis.

FAO, GEF, AFD, WFP, and the Arab Fund for Economic and Social Development and

other different international NGOs are supporting or have supported the palm date

sector, funding various projects. The main government institution connected to the palm

date sector is the Ministry of Agriculture (MoA).

As the Ministry of National Economics (MoNE) does not actively support palm dates

sector and the processed products there is a need for quality control on processed

products to increase consumers level of trust on local products.

Page 9 of 18

PALM DATE VALUE CHAIN

In recent years imported dates have also been available, contributing to 7% of the total

supply of Gaza‟s market. Date fruits are imported to Gaza, mostly from the West Bank

and Israel, while date paste may also be imported from the Emirates and Saudi Arabia.

The imports of date fruit during the harvesting season contribute to an additional

oversupply at that time.

Table 6 Actors involved in the date palm sector and their interventions

Actor Description

Producers Distributed throughout Gaza, but concentrated around

Deir Al-Balah, as well as in eastern villages of Khan

Younis

Input Suppliers (various) Various, supplying pesticides, seedlings, fertilisers, and other farm tools

Traders (various) Procurement of date fruit and marketing to wholesalers, retailers and processors

Retailers (various) Various, from small market stalls to large retailers

Palm dates cluster This is a recent established cluster with currently 15 members of palm date cluster including: 8 dates producers who do processing, 3 women who do handicrafts processing, one fodder processing unit which managed by Al-Ahlyia Association, Al- Awda factories, Al- Ahlyia Association for the Development of Palms & Dates and Palestinian Palm Association for Development. The main objective of the cluster is to strengthen the competitiveness of local companies, and especially SME, in order to increase their market share on local market.

Al- Ahlyia Association for the Development of Palms & Dates

Al-Ahlyia Association the main CBO is implementing various donors funded projects (see below): introducing new Palm tree varieties, providing technical support, extension services to farmers, palm date food processing units, fodder processing, handicrafts processing.

FAO FAO has funded a project on red palm weevil control, which was implemented through the Al-Ahlyia Association. The project was focussing on monitoring insect behaviour through the distribution and the instalment of pheromone traps, as well as awareness raising activities on weevil identification and control mechanisms.

Global Environment Facility (GEF)

GEF has funded a project on red palm weevil ( infest) control, which was implemented through the Al-Ahlyia Association . The project also focussed on monitoring insect behaviour through the distribution and the instalment of pheromone traps, awareness raising activities, a field survey of 30,000 palm trees, and providing the necessary treatment for the infected trees. GEF funded also a project to provide support for the

development of palm date processing industries (namely

Page 10 of 18

PALM DATE VALUE CHAIN

food processing, handicrafts, and fodder processing),

implemented by Al-Ahlyia. The project was focusing on

building the capacity of the date processing units,

through providing equipment, tools and related inputs for

processing .

AgenceFrançaise de Développement (AFD)

AFD has funded a project for the rehabilitation of agriculture lands, and the expansion of palm tree cultivation, through introducing new varieties (with NPA, NDC).This project was also implemented by Al-Ahlyia

Association. AFD recently gave financial support for the development of palm dates cluster, injunction with the Palestinian Authority and Chamber of Commerce.

Norwegian People's Aid (NPA)

NPA has also funded a project for the rehabilitation of agriculture lands, and the expansion of palm tree cultivation, through introducing new varieties (with AFD, NDC). Moreover NPA has funded a project to provide technical capacity support through supplying new processing equipment to food processing unit and fodder processing unit , which are managed by Al- Ahlyia Association.

The NGO Development Center (NDC)

NDC has also has funded a project for the rehabilitation of agriculture lands, and the expansion of palm tree cultivation, through introducing new varieties (with AFD, NPA).

Welfare Association Supported the original establishment of small food processing units, at Al- Ahlyia Association around 2007 and provided basic technical training for women on dates food processing.

Arab fund for Economic and Social Development

Implemented a project through the Al-Ahlyia Association

to support fodder processing from the dates waste, and

distributing the fodder for livestock breeders.

Ministry of Agriculture (MOA) Provides extension on the red palm weevil control.

Ministry of National Economics (MoNE)

Agricultural Fund provides loans supporting producers, set standards of specifications for production, do quality monitoring of all products.

1.2 Challenges and constraints in the palm date sector The figure below presents a problem tree analysis highlighting the key challenges and

constraints encountered in the Gaza Strip palm date production and processing industry,

detailing underlying causes and effects on Palestinian male and female farmers and

other actors in the olive value chain. This problem tree was made by the participants to a

workshop of the Gaza UPA Platform held on March 20th 2014 in Gaza City. Participants

are representatives of the 30 organisations that are playing a key role in the Urban and

Peri-urban Agricultural sector.

Page 11 of 18

PALM DATE VALUE CHAIN

Diagram 1 Problem Tree Analysis for the Palm Date Sector in the Gaza Strip

The main challenges are related to over-supply and related low market prices at gut

periods, low palm tree productivity and low competitiveness of processed date products

on the local market.

The main causes for the low productivity of palm date trees are:

1. The main challenges facing the production of palm dates mainly relate to the

weakness of the productive capacity due to the lack of good pollen and low

productivity of cultivated varieties compared to other varieties.

2. Over the last five years, one of the major threats to the cultivation of date palm

trees has been the now widespread red palm weevil

"Rhynchophorusferrugineus". This kind of insect probably arrived from Egypt

through the tunnels. Weevil larvae can excavate holes in the trunk of palm

trees up to a meter long, thereby weakening and eventually killing the host plant.

The Red Palm Weevil‟s holes are slowly killing trees. About 20% of the trees

cultivated in the Gaza Strip are affected and need to be treated chemically.

3. As for other agricultural sectors, agricultural extension and applied research

provided either by government agencies or NGOs is weak, with low geographical

coverage.

Low income of Palm date producers and processors

Livelihood conditions of palm date producers and processors are deteriorated

Palm date sector contribution to agricultural total value has diminished

Low productivity of palm date trees

Low competitiveness of local processed products

Over supply and low prices at glut periods

1.Bad quality of pollen

2.Low quality of cultivated palm trees variety 3.Poor research and extension services (insufficient capacity; only as response strategy to problems) 4.Palm date diseases and insects

1. Low diversity of palm date products 2.Consumers donot trust the local product/lack of quality control 3.Poor packaging and storage 4. Lack of protection and enabling policies for producers and processors

1. Lack of cold storage and processing

2. Imports at times of local over supply 3.Low capacity of existing factories and processing units

Page 12 of 18

PALM DATE VALUE CHAIN

The main causes for over supply and low market prices at glut periods are:

1. The biggest challenge for the palm date sector is the large volume of dates that

arrive at the same time on the market around harvest time, resulting in low

prices.

2. There is very little capacity in Gaza for (cold) storing dates, which would allow

producers to wait for higher prices.

3. Processing of palm dates would be one way to deal with the market glut of dates.

However, existing processing capacity is relatively low and is limited to some

micro-enterprises run by women through the Al-Ahlyia Association.

The main causes for low competitiveness of processed palm dates products on the

local market are:

1. Consumers prefer imported processed dates products (syrup, jam) due to their

higher (perceived) quality and safety. Such negative perception is particularly

disadvantageous to women as most processing is done by them and their

organisations. The challenge is to improve the market share of locally processed

products through better processing and marketing practices that can position

women further.

2. Date paste, syrups and jams are not marketed effectively (poor packaging,

branding) and cannot compete with imported Israeli and Turkish products.

However, date paste is better marketed and more trusted by consumers in Gaza.

3. In terms of processed dates (syrup, jam, paste, etc.), local products are

perceived by Gaza consumers to be of lower quality compared to imported

products. Quality needs to be improved to increase local market share.

4. Even Al-Ahlyia Association, that runs the only palm date processing unit, faces

challenges such as poor access of the processed products to markets; need for

improved working conditions (including place, lack of safety equipment, etc.);

limited processing capacity of the processing unit, and high prices of packaging

and branding materials. Women workers have very limited knowledge and

experience in food processing, marketing and quality assurance and control.

5. There is general lack in the Gaza Strip of knowledge on quality standards and

poor access to quality certification. Safety processing standards are not followed

with regards to quality improvement.

2. Vision, scenarios and proposed interventions

2.1 Vision

The following vision was developed by a large number of local actors actively involved in the Gaza palm date sector in a workshop facilitated by the project of the Gaza Platform for Urban and Peri-urban Agriculture (March 20th, 2014)

“All men and women producers and workers in the palm date sector, both men and

women, enjoy a decent standard of living, which brings them food security and

Page 13 of 18

PALM DATE VALUE CHAIN

contributes to make the palm date sector in the Gaza Strip a strategic, protected,

developed sector capable of competing with imported products.

2.2 Scenarios Two possible scenarios are here discussed, representing the projected political and

economic context that could affect the way the palm date sector may grow in the future.

First scenario: Political stability. A political stable environment will reflect

positively on the overall economic condition and growth in the country. Political

stability will also entail the establishment of a national unity government,

accompanied with a full national reconciliation. This situation will eventually reflect

positively on all other life dimensions, improve relations with neighbouring countries,

accelerate development and growth, as well as increase funding opportunities and

external support. Both increased employment opportunities and increased labour

productivity are envisaged, enhancing consequently the living standard of both

Palestinian men and women.

Second scenario: Political instability and deteriorating household economy:

Foreseen political instability entails the continuation of political disagreement and

reluctance towards national reconciliation. This situation will further deteriorate the

economic and living standards of households involved in palm date production,

processing and marketing. External funding and support for development activities

will continue to be limited. With the lack of national stability, poverty levels and

unemployment rates are not expected to decrease, and external investments in the

various productive sectors will remain at a low level.

In view of the unlikelihood of the first scenario to materialise, strategies and interventions

for the palm date sector in the Gaza Strip will work under the assumption of the second

and current scenario. Resultant strategies to achieve the vision formulated in section 2.1

will take into account the constraints posed by this scenario and work notably on

systemic changes that encompass the independence of external inputs, that promote

better palm tree management and harvesting, improve storage, processing and

packaging and work on creating higher value products for the local market. Section 2.6

below will assess the risks that are related to working under this scenario.

2.3 Needed systemic change

In view of the vision above, the analysis of the current context for the palm date sector,

the challenges and constraints mentioned in section 1, and the scenario under which

strengthening of the palm date sector in the Gaza Strip has to be achieved, the project

Consortium recommends that the following systemic changes are facilitated by the

project and operated by the local actors involved in the sector.

Where most of the here recommended systemic changes in the palm date value chain

would be necessary under both scenarios (more and less political stability), they become

Page 14 of 18

PALM DATE VALUE CHAIN

critical for the survival of the palm date sector in the Gaza Strip under the second

scenario. The following three systemic changes are considered essential to pursue in

the palm date sector:

1. Reducing over supply and glut periods by facilitating better use of cold storage

and the processing of higher quality products (paste, syrups, jams) for a local

market.

2. Increase in quality control and consumer perception of local products. This will

require that necessary improvements are made in processing, packaging and

storage. This also requires strengthening capacities of control and extension

agencies and coordination among actors in the chain.

3. A deliberate focus on women as future key players in an innovative technology

process for diversifying and increasing quality of palm date related products and

their marketing.

2.4 Proposed strategy and interventions The proposed interventions will be carried out under the current scenario, where there is

no political stability and weak economic incomes at the household level. In the not so

near future, the political instability will possibly continue with negative influence on the

economic situation of the GS that will remain weak. Therefore, under this scenario the

poor living conditions of many of the poorer households in the GS risk to remain

unchanged in the future. Moreover, there will be limited external development support ,

while no important shifts from emergency to development approach are foreseen in

internationally funded projects. Therefore poverty and unemployment rates risk to

increase while private sector investments risk to contract. In spite of these bleak

perspectives there is scope for a better reality even within these hard economic

conditions. As mentioned above important systemic change in a number of domains is

necessary to shift economic dynamics in a more positive sense.

The vision for the palm date sector is to work on achieving increased income and a good

standard of living for palm date producers and those involved in the processing and

marketing of dates and date products. This can be through improved storage and more

staggered marketing and improvement of processing practices, so that quality of

products increases and can fetch higher consumer demand and prices.

This requires increasing and improving quality control, extension and training; enhancing

access to finance, certification of product quality and consumer marketing.

The following are proposed intervention ideas by local value chain actors. Activities will

be focused around the producing areas of Deir al-Balah and the Eastern villages of Khan

Younis. The project will build on and coordinate with the efforts started by the palm date

cluster to facilitate the establishment of a broader palm date platform to coordinate

between all actors in the palm dates sector. The Al-Ahlyia Association for the

Page 15 of 18

PALM DATE VALUE CHAIN

Development of Palms & Dates, a well-known CBO respected by different market actors,

could be the local platform coordinator.

Proposed interventions to improve processing, product quality and marketing:

1. Training/capacity building of women working in Al-Ahlyia Association processing

units. Staff would be trained in processing techniques to improve efficiency and

quality and to produce on a larger scale. In addition, staff will be capacitated in

post processing quality assurance and control, better marketing and accessibility

to market and improving quality standards and quality certification. Training

would be provided by local training institutes (MoA), as Al-Ahlyia has current

limited capacity to do this themselves. Capacity building would include food

safety, packaging, storage, labelling and branding and developing marketing

channels for processed goods to ensure more sustainable employment

opportunities for women workers. Furthermore, improving women workers

working conditions, especially through ensuring a safe working environment.

Other interventions would involve to facilitate their access to a co-investment

fund to cover processing costs, especially raw materials, and equipment.

2. The Association on its turn could be capacitated and trained in in processing--

related extension for more outreach to individual households and women in

particular. The Al-Ahlyia Association can share and bring its extension expertise

to women who engage in processing at the household level to improve their

processing quality, improve packaging and branding, and better access markets

(possibly by clustering households for joint marketing and by introducing cold

storage at household level).

3. Support development of new (solar based) cold storage equipment and

infrastructure at household level and in form of larger storage units. At the same

time, small scale producers could be supported to organise sharing the costs of

leasing cold storage space in the presently functioning cold storage units that are

operating in Gaza, each with a capacity of around 100 tonnes. Storage costs per

tonne are 200 NIS per month. This means that if 1 tonne of dates is sold on

average for 2000 NIS, then the cost of storage is 10% of this value. Hence, by

storing the produce for one month, the market price only needs to increase by

10% of this cost to be recovered, which is virtually certain to occur after the peak

supply glut. A co-investment will be available to finance farmers to put dates in

cold storage.

4. Facilitate linkages between research institutions, including the Faculty of

Agriculture of al-Azhar University and Faculty of Science of the Islamic University

with producers and other chain actors, through promoting the use of applied

scientific research methods to improve processing quality and develop new

processing and storage techniques. Also build relationships with input/service

providers to introduce new processing and packaging technologies and

techniques

Page 16 of 18

PALM DATE VALUE CHAIN

5. Facilitate initiating of local consumers campaign, which will be set up to promote

a “buy-local” products in order to enhance consumers‟ trust in local produce.

Government institutions, private sector organizations, namely Pal Trade and the

Chamber of Commerce and other stakeholders might be encouraged to launch

targeted marketing campaigns. In addition, processing unit produce could be

linked to new potential consumers/customers through current food voucher

distribution programs implemented by (WFP, UNRWA and other organization.

6. Facilitate a co-investment fund, linked to available finance and micro-finance

facilities. At the level of the local value chain platforms, the co-investment fund

might be used as a guarantee fund to attract financial institutions to innovate in

their service provisions in this area. Alternatively the co-investment fund could

help address initial problems with money flows in the chain (for example, when

cold storage is improved to increase marketing options, money flows will be

delayed and should be looked at in coordination with any changes in the

warehouse system).

In addition the palm date cluster/platform and G/UPA might address specific

interventions to improve productivity of palm trees:

1. Capacity building of extension institutions, including the staff of local extension

departments of the MoA and the Al-Ahlyia Association and other NGOs to update

their extension services for more efficient outreach. Capacities of such extension

staff need to be built to better (more effectively, larger coverage, more permanent

support) support producers and promote good agricultural management, pest

and disease management using participatory training approaches (PTD, UPA

producers‟ learning and action field schools). As there is not any training capacity

in such approaches in the Gaza Strip, nor in the West Bank, the project will

engage in a PTD/farmer school capacity building process in a learning-by-doing

mode involving both producers as well as staff of NGOs and MoA.

2. Improving productivity through the cultivation of new higher economic yield

varieties. At present most trees are of the Hayani variety (90%). The Ministry of

Agriculture believes that the introduction of new varieties (Ameri and Berhi), in

conjunction with good pollination techniques would boost production for tree

owners. This would be an intervention for the medium/long term due to the time it

takes for the trees to mature (5+ years).

3. Facilitate the establishment of a national palm plant nursery, a pollen collection

center, and a tissue culture laboratory in coordination with the Ministry of

Agriculture and research institutions to develop better, shorter and productive

varieties.

4. Facilitate linkages between research institutions, including the Faculty of

Agriculture of al-Azhar University and Faculty of Science of the Islamic University

with producers and other chain actors, through promoting the use of applied

scientific research methods to provide updated information and knowledge on the

Page 17 of 18

PALM DATE VALUE CHAIN

possibility of introducing new potential varieties and improve practices with

regard to red palm weevil control.

5. Build relationships with input/service providers to supply red palm weevil

detection devices, to introduce automated pollination mechanisms, and industrial

maturation equipment.

Of these proposed interventions, the project will concentrate on interventions 1 (capacity

building of training and extension institutes) and 4 and 5 through the building of a local

date palm platform. Interventions 2 and 3 will be further discussed in the local platform

and Gaza Wide UPA Platform for possible action by the actors involved.

2.5 Gender dynamics Women, in comparison with other chains, are only involved to a limited extent in the date

palm sector. They are mainly present and responsible for processing, both at household

level and at the level of the processing unit set up by Al-Ahlyia Association. They have

more difficulties in accessing information and training as they have poor communication

and coordination with other market actors (ex. extension and training services; retailers).

They do not have access to finance are not able to purchase the needed equipment and

inputs (such as storage and packaging equipment and materials). Coupled to lack of

knowledge and skills in processing, their production is low and of irregular quality. It is

for these reasons that in its focus on processing, the project will make specific efforts to

work with women, both at household level as well as at the level of the Association.

2.6 Risk analysis As in the case of the Olive Value Chain, also in the palm date value chain risks are less

closely related to the blockade of the Gaza strip described under Scenario 2, as

compared to other urban agricultural sectors. The intervention strategy is targeting

foremost the local market as demand for fresh and processed dates is not met, while

locally produced high quality date products are almost non-existent in the local market.

The main impediment created by a continuing closure of the Gaza Strip is in obtaining

modern processing and solar-based storage equipment from outside (new or second-

hand from abroad or the West Bank), although this is less critical than for the olive

sector.

The main risks as related to development of a viable palm date chain are the following:

1. The zero distribution approach : Actors in Gaza are not familiar with this

approach. As most palm date projects were implemented with a „free distribution‟

approach, the project needs to face a number of expectations. This requires

honest discussions from the start and a clear explanation of why this approach

can work sustainably.

2. Willingness of actors to engage and broaden the palm date cluster into a wider

platform: Date interventions in Gaza up to now have usually focussed on a single

value chain actor at a time. The idea of a value chain approach, bringing together

actors from across the market system is unfamiliar to most actors. Therefore, it

Page 18 of 18

PALM DATE VALUE CHAIN

may be a challenge to engage their interest at first if they do not immediately

understand what is in it for them. Also the current palm date cluster might feel

threatened in its functioning and be hesitant to open up to involvement of more

and other actors.

3. Red palm weevil cannot be well controlled: If there is a larger outbreak, this could

affect the palm date sector seriously, leaving producers with losses of trees that

take at least 5 years to begin producing again.

4. Seasonal price fluctuations: Each season there is a glut date supply at harvest

time. This is an ever-present risk to producers that they may struggle to sell their

dates at decent prices, affecting profitability and livelihoods.

5. Competition from imports: Despite the border for imports being usually closed, in

recent years imported dates have still amounted to around 7% of total supply in

the Gaza market. If borders are opened for more dates from outside Gaza this

can be expected to contribute to over-supply and lower prices at peak harvest

times. This will be a challenge for local producers to be competitive. A side effect

of more open borders could also bring other imported fruits into competition with

local dates. Date paste produced in Gaza is regarded as being of good quality

when compared with that imported from Israel and Turkey, however it is a little

more expensive. However, jams and syrups produced locally are considered

inferior to the imports preferred by Gaza consumers.