COMPANY PROFILE Piaggio Vehicle Private Limited is a 100% subsidiary of Piaggio & C. S.p.a,Italy.Piaggio Vehicles Private Limited was incorporat ed on Feb rua ry 17, 1998, as a joi nt ventu re betwe en Piagg io & C. S.p. a Ita ly, Simest Spa, Ital y to manufacture and market world-class diesel 3-wheelers in India. The company acquired the auto unit from Greaves Limited on March 31, 1998, located in Baramati, India. On August 30, 2001; Piaggio& C. SpA Italy acquired the entire shareholding of Greaves Limited consequent to which the Board of Directors passed a resolution to change its name to Piaggio Vehicles Private Limited. The company was incorporated to manufacture and market world-class diesel 3-wheelers & 4-wheelers in India. The company launched its Ape range of multi –utility, diesel 3-wheelers in India on 31 st July 1999. The parent company Piaggio and C.SpA, Italy transports its light weight, diverse product range with sales turn over exceeding $1.00 billion; vespa is one of them which are popular in India for last 20 years. Piaggio & C. Spa Italy is a $1.3 bn. Global Transportation Company in the field of light transport vehicles covering a very diverse product range comprising of 2-wheelers, 3-wheelers and 4-wheelers for cargo as well as passenger mobility. The Ape vehicles, which are, preferred mode of transportation in many countries. The Ape range comprises pick-ups, delivery vans, Drive Away Chassis for various customized applications, and various ‘Special Purpose Vehicles’ optimally designed for specific needs and applications. Piaggio Vehicle Private Limited manufactures the Ape vehicles, as perPiaggio’s international standards of design and manufacturing in Baramati near Pune in Maharashtra state. It had got capacity of 36000 vehicles per annum, which will be 72000 after the expansion.

Piaggio Vehicle Private Limited is a 100% subsidiary of Piaggio & C. S.p.a,Italy.Piaggio Vehicles Private Limited

was incorporated on February 17, 1998, as a joint venture between Piaggio & C. S.p.a Italy, Simest Spa, Italy to

manufacture and market world-class diesel 3-wheelers in India. The company acquired the auto unit from Greaves Limited

on March 31, 1998, located in Baramati, India. On August 30, 2001; Piaggio& C. SpA Italy acquired the entire shareholding

of Greaves Limited consequent to which the Board of Directors passed a resolution to change its name to Piaggio Vehicles

Private Limited.

The company was incorporated to manufacture and market world-class diesel 3-wheelers & 4-wheelers in India. Thecompany launched its Ape range of multi –utility, diesel 3-wheelers in India on 31st July 1999. The parent company Piaggio

and C.SpA, Italy transports its light weight, diverse product range with sales turn over exceeding $1.00 billion; vespa is one

of them which are popular in India for last 20 years.

Piaggio & C. Spa Italy is a $1.3 bn. Global Transportation Company in the field of light transport vehicles covering a

very diverse product range comprising of 2-wheelers, 3-wheelers and 4-wheelers for cargo as well as passenger mobility.

The Ape vehicles, which are, preferred mode of transportation in many countries. The Ape range comprises pick-ups,

delivery vans, Drive Away Chassis for various customized applications, and various ‘Special Purpose Vehicles’ optimally

designed for specific needs and applications. Piaggio Vehicle Private Limited manufactures the Ape vehicles, as per

Piaggio’s international standards of design and manufacturing in Baramati near Pune in Maharashtra state. It had got

capacity of 36000 vehicles per annum, which will be 72000 after the expansion.

1. The cost of an item of fixed asset comprises its purchase price, including import duties and other non-refundable taxes or

levies and any directly attributable cost of bringing the asset to its working condition for its intended use; any trade

discounts and rebates are deducted in arriving at the purchase price. Examples of directly attributable costs are:

(i) Site preparation;

(ii) Initial delivery and handling costs;

(iii) Installation cost, such as special foundations for plant; and

(iv) Professional fees, for example fees of architects and engineers.The cost of a fixed asset may undergo changes subsequent to its acquisition or construction on account of exchange

fluctuations, price adjustments, changes in duties or similar factors.

2. Administration and other general overhead expenses are usually excluded from the cost of fixed assets because they do

not relate to a specific fixed asset. However, in some circumstances, such expenses as are specifically attributable to

construction of a project or to the acquisition of a fixed asset or bringing it to its working condition, may be included as part

of the cost of the construction project or as a part of the cost of the fixed asset.

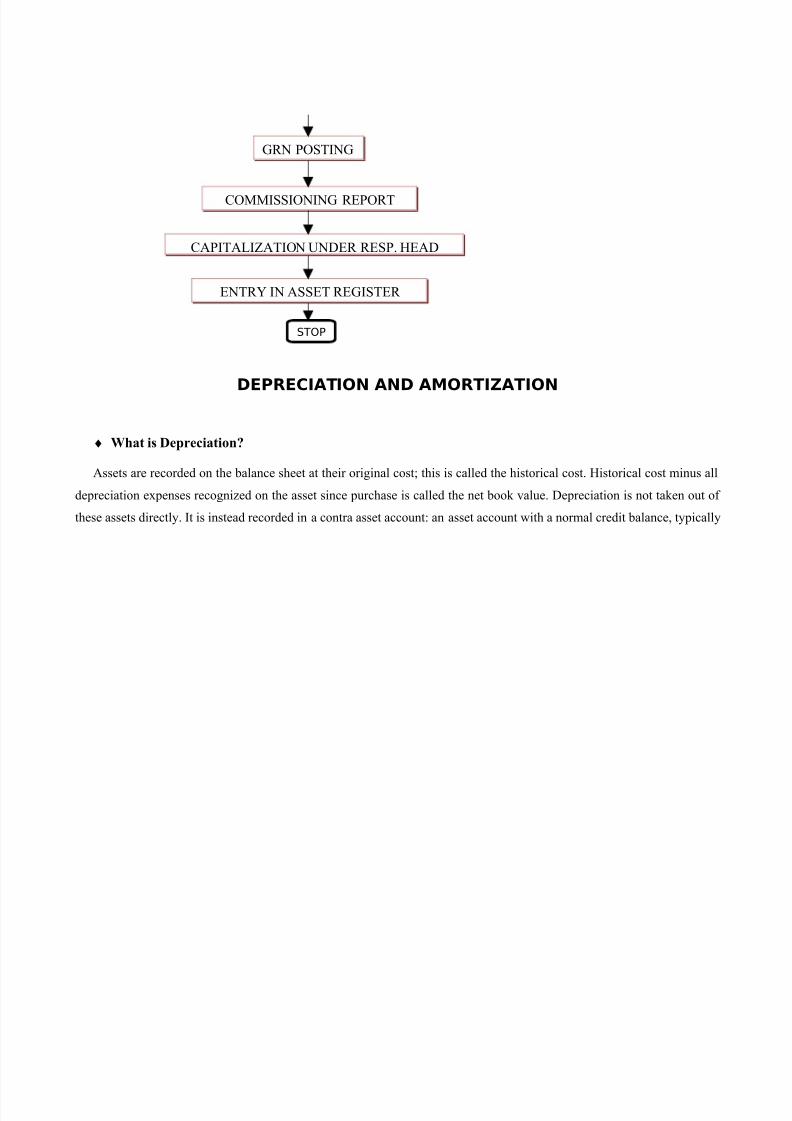

3. The expenditure incurred on start-up and commissioning of the project, including the expenditure incurred on test runs

and experimental production, is usually capitalized as an indirect element of the construction cost. However, the expenditure

incurred after the plant has begun commercial production, i.e., production intended for sale or captive consumption, is not

Companies (Auditor's Report) Order, 2003PUBLISHED IN THE GAZETTE OF INDIA EXTRAORDINARY PART II, SECTION 3 - SUB - SECTION(i)

MINISTRY OF FINANCE

(DEPARTMENT OF COMPANY AFFAIRS)

1. Definitions. In this Order, unless the context otherwise requires,-

(a) Act means the Companies Act, 1956 (1 of 1956);

(b) chit fund company, nidhi company or mutual benefit company means a company engaged in the business

of managing, conducting or supervising as a foreman or agent of any transaction or arrangement by which it

enters into an agreement with a number of subscribers that every one of them shall subscribe to a certain sumof installments for a definite period and that each subscriber, in his turn, as determined by lot or by auction or

by tender or in such other manner as may be provided for in the agreement, shall be entitled to a prize amount,

and includes companies whose principal business is accepting fixed deposits from, and lending money to,

looking at all of its machinery), and consistently employed. However, there is no expectation that each individual item

declines in value by the same amount, primarily because the recognition of depreciation is based upon the allocation of

historical costs and not current market prices.

Accounting standards bodies have detailed rules on which methods of depreciation are acceptable, and auditors should

express a view if they believe the assumptions underlying the estimates do not give a true and fair view.

♦ Recording depreciation

For historical cost purposes, assets are recorded on the balance sheet at their original cost; this is called the historical

cost. Historical cost minus all depreciation expenses recognized on the asset since purchase is called the book value.Depreciation is not taken out of these assets directly. It is instead recorded in a contra asset account: an asset account with a

normal credit balance, typically called "accumulated depreciation". Balancing an asset account with its corresponding

accumulated depreciation account will result in the net book value. The net book value will never fall below the salvage

value, meaning that once an asset is fully depreciated, no further expenses will be taken during its life. Salvage value is the

estimated value of the asset at the end of its useful life. In this way, total depreciation for an asset will never exceed the

estimated total cash outlay (depreciable basis) for the asset. The exception to this is in many price-regulated industries

(public utilities) where salvage is estimated net of the cost of physically removing the asset from service. (Decommissioning

a nuclear power plant is a nontrivial expense.) If the expected cost of removal exceeds the expected raw (or gross) salvage,

then the net of the two (called net salvage) may be negative. In this case, the depreciation recorded on the regulated books

may exceed the depreciable basis. Companies have no obligation to dispose of depreciated assets, of course, and many fully

Sum-of-Years' Digits is a depreciation method that results in a more accelerated write-off than straight line,

but less than declining-balance method. Under this method annual depreciation is determined by multiplying the

Depreciable Cost by a schedule of fractions.

♦ Units-of-Production Depreciation Method

Under the Units-of-Production method, useful life of the asset is expressed in terms of the total number of

units expected to be produced. Annual depreciation is computed in three steps.

First, a Depreciable Cost is computed.

Second, Depreciation per Unit is computed. Depreciation charge per unit is computed by dividing Depreciable Cost byTotal Units, expected to be produced during the useful life of the asset.

Depreciable Cost = Original Cost - Salvage Value

Book Value = Original Cost - Accumulated Depreciation

Depreciation per Unit = Depreciable Cost / Total Units of production

When a company spends money for a service or anything else that is short-lived, this expenditure is usually

immediately tax deductible in some countries, and the company enjoys an immediate tax benefit.

To be eligible for depreciation, an asset must have two features:

1. it has a useful life beyond the taxable year (essentially why it was capitalized in the first place), and

2. it wears out, decays, declines in value due to natural causes, or is subject to exhaustion or obsolescence.

Therefore, when a company buys an asset that will last longer than one year, like a computer, car, or building, the

company cannot immediately deduct the cost and enjoy an immediate large tax benefit. Instead, the company must

depreciate the cost over the useful life of the asset, taking a tax deduction for a part of the cost each year. Eventually the

company does get to deduct the full cost of the asset, but this happens over several years. In the jurisdictions accounting

depreciation and tax depreciation are almost always significantly different numbers, as in many instances a form of "accelerated depreciation" can be used for tax purposes to lower (taxable) net income in a given period (or, in some

instances, a fixed asset may be allowed to be expensed for tax purposes; Section 179 of the Internal Revenue Code allows

for this treatment in some circumstances). Technically, these are not considered "tax reductions" but tax deferrals lowering

taxable income now by increasing expenses should increase future taxable income (and taxes) at a later date.

Importantly, no depreciation deduction is allowed for inventories or other property held for sale to customers in the ordinary

course of business. Land is also not depreciable. However, improvements to land, including landscaping, are usually

depreciable.

There are generally five variables that a taxpayer must take into account when computing the correct depreciation

deduction:

1. The depreciation base (the asset’s cost basis),

2. The asset’s class life (estimated life expectancy of the asset),

3. The applicable recovery period (the number of years the taxpayer can claim depreciation deductions),

4. The applicable depreciation method (see double declining balance method or straight-line method), and

5. The applicable convention (§ 168(d)(4) of the code—generally the half-year convention).

National accounts

In national accounts, depreciation represents the decline in the aggregate capital stock arising from the use of capitalin production, also referred to as consumption of fixed capital. Hence, depreciation is equal to the difference between

aggregate (gross) investment and net investment or between Gross National Product and Net National Product. Unlike

depreciation in business accounting, depreciation in national accounts is, in principle, not a method of allocating the costs of

I.BUILDING1. Building which are used mainly for residential purposes

except hotels and boarding houses.2. Building other than those used mainly for residential purposes

and not covered by sub-items (1) above & (3) below.3.Building acquired on or after the 1st day of sep, 2002 for

installing P&M forming part of water supply project or water treatment system and which is put to use for the purpose of businessof providing infrastructure facilities under (i) of sub-section (4 ) of sec 80-IA.

4. Purely temporary erections such as wooden structures

5

10

100

100

II.FURNITURE AND FIXTURE10

III.PLANT & MACHINERY

1. P&M other than those covered by sub-items (2 ),(3 ) & (8 ) below:

2. Motors cars, other than those used in a business running themon hire, acquired or put to use on or after the 1 st day of Apr,1990.

3. (i) Aeroplanes – Aeroengines(ii) Motor buses, motor lorries and motor taxis used in a

business of running them on hire(iii) commercial vehicle which is acquired by the assessee on

or after the 1st

day of Oct, 1998, but before the 1st

day of Apr,1999 & is put to use for any period before the 1st day of Apr,1999 for the purposes of business in accordance with the 3rd

provision to clause (ii ) of sub-sec (1) of sec 32.(iv) New commercial vehicle which is acquired on or after the1st day of Oct, 1998, but before the 1st day of Apr, 1999 inreplacement of condemned vehicle of over 15 years of age &is put to use for any period before the 1st day of Apr, 1999 for the purposes of business in accordance with the 3rd proviso to

clause (ii) of sub-sec (1) of sec 32.(v) New commercial vehicle which is acquired on or after the1st day of Apr, 1999, but before the 1st day of Apr, 2000 in

replacement of condemned vehicle of over 15 years of age &is put to use for any period before the 1st day of Apr, 2000 for the purposes of business in accordance with the 3rd proviso toclause (ii) of sub-sec (1) of sec 32.(vi) New commercial vehicle which is acquired on or after the1st day of Apr, 2001 but before the 1st day of Apr, 2002 & is

put to use for any period before the 1st day of Apr, 2002 for the purposes of business.(vii) Moulds used in rubber & plastic goods factories(viii) Air pollution control equipment(ix) Water pollution control equipment

(x) Solidwaste control equipment.(xi) P&M, used in semi-conductor industry covering allintegrated circuits (ICS) ranging from SSI to LSI.(xia) Life saving medical equipment

4. Containers made of glass or plastic used as re-fills5. Computer including computer software6. P&M, used in weaving, processing & garment sector of textile

industry, which is purchased under TUFS on or after the 1st

day of Apr, 2001 but before the 1 st day of Apr, 2004 & is putto use before the 1st day of Apr, 2004.

7. P&M, acquired & installed on or after the 1st day of Sep,

2002 in a water supply project or a water treatment system &which is put to use for the purpose of business of providinginfrastructure facility under clause (i) of sub-sec (4) of sec 80-IA.

8. (i) Wooden parts used in artificial silk manufacturingmachinery(ii) Cinematograph films – bulbs of studio lights(iii) Match factories – wooden match frames(iv) Mines & quarries

1. "buildings" include roads, bridges, culverts, wells & tube-wells.

2. "factory buildings" does not include offices, godowns, officers & employees' quarters, roads, bridges, culverts, wells &

tube-wells.

3. "speed boat" means a motor boat driven by a high speed internal combustion engine capable of propelling the boat at a

speed exceeding 24 Kilometers per hour in still water & so designed that when running at a speed it will plane, i.e., its bow

will rise from the water.

4. Where, during any financial year, any addition has been made to any asset, or where any asset has been sold, discarded,

demolished or destroyed, the depreciation on such assets shall be calculated on a pro rata basis from the date of suchaddition or, as the case may be, up to the date on which such asset has been sold, discarded, demolished or destroyed.

5. The following information should also be disclosed in the accounts:

(i) depreciation methods used; &

(ii) depreciation rates or the useful lives of the assets, if they are different from the principal rates specified in the Schedule.

6. The calculations of the extra depreciation for double shift working & for triple shift working shall be made separately in

the proportion which the number of days for which the concern worked double shift or triple shift, as the case may be, bears

to the normal number of working days during the year. For this purpose, the normal number of working days during the

year shall be deemed to be -

(a) in the case of a seasonal factory or concern, the number of days on which the factory or concern actually worked during

(b) in any other case, the number of days on which the factory or concern actually worked during the year or 240 days,

whichever is greater.

The extra shift depreciation shall not be charged in respect of any item of machinery or plant which has been specifically,

excepted by inscription of the letters "N.E.S.D." (meaning "No Extra Shift Depreciation") against it in sub-items above &

also in respect of the following items of machinery & plant to which the general rate of depreciation of 13.91 per cent

applies-

(1) Accounting machines.

(2) Air-conditioning machinery including room air-conditioners.

(3) Building contractor's machinery.

(4) Calculating machines.

(5) Electrical machinery

(6) Hydraulic works, pipelines & sluices

(7) Mineral oil concerns - field operations.

7. "Continuous process plant" means a plant which is required & designed to operate 24 hours a day.

8. Notwithstanding anything mentioned in this Schedule depreciation on assets, whose actual cost does not exceed fivethousand & rupees, shall be provided depreciation at the rate of hundred per cent:

Provided that where the aggregate actual cost of individual items of plant & machinery costing Rs. 5,000 or less constitutes

more than 10 per cent of the total actual cost of plant & machinery, rates of depreciation applicable to such items shall be

the rates as specified in Item II of the Schedule.