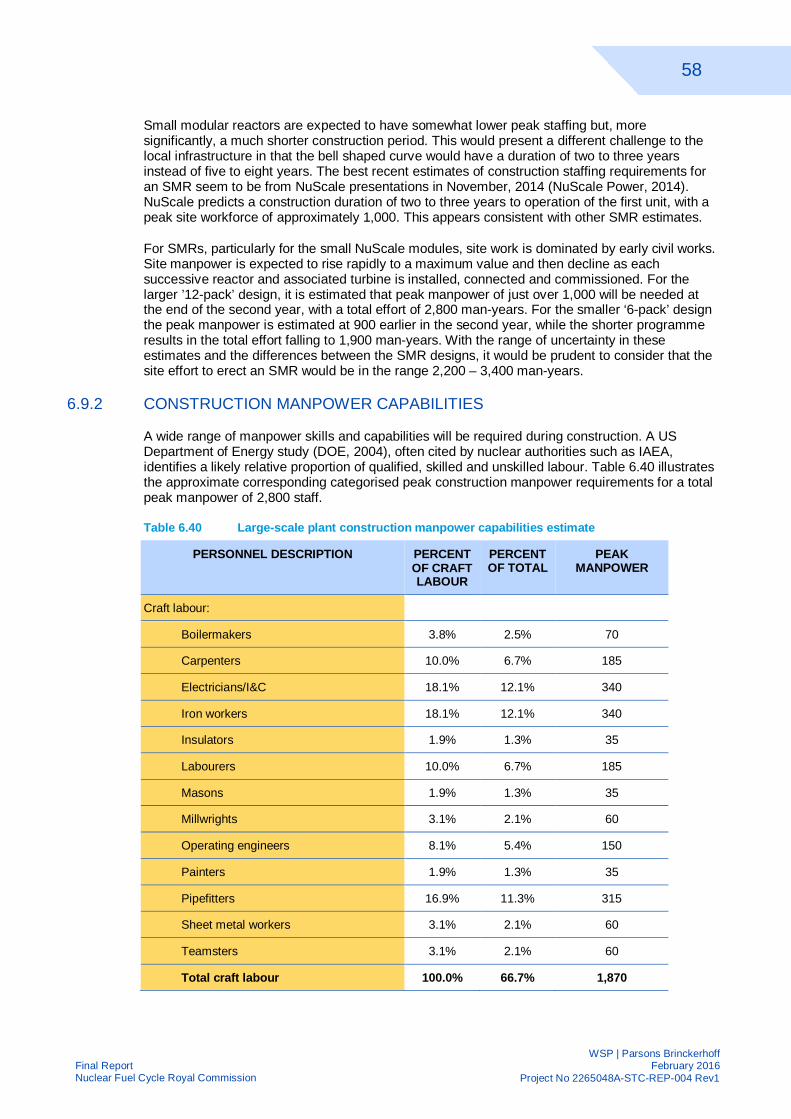

165

NUCLEAR FUEL CYCLE ROYAL COMMISSION FINAL REPORT QUANTITATIVE ANALYSIS AND INITIAL BUSINESS CASE – ESTABLISHING A NUCLEAR POWER PLANT AND SYSTEMS IN SOUTH AUSTRALIA FEBRUARY 2016

NUCLEAR FUEL CYCLE ROYAL COMMISSION

FINAL REPORTQUANTITATIVE ANALYSIS AND INITIALBUSINESS CASE – ESTABLISHING A NUCLEARPOWER PLANT AND SYSTEMS IN SOUTHAUSTRALIA

FEBRUARY 2016

Project no: 2265048A-STC-REP-004 Rev1Date: February 2016

–WSP | Parsons BrinckerhoffLevel 14, 1 King William StreetAdelaide SA 5000GPO Box 398Adelaide SA 5001

Tel: +61 8 8405 4300Fax: +61 8 8405 4301www.wspgroup.comwww.pbworld.com

FINAL REPORTQUANTITATIVE ANALYSIS AND INITIALBUSINESS CASE – ESTABLISHING ANUCLEAR POWER PLANT ANDSYSTEMS IN SOUTH AUSTRALIANuclear Fuel Cycle Royal Commission

Parsons Brinckerhoff Australia Pty LtdABN 47 005 113 468

Level 14, 1 King William StreetAdelaide SA 5000GPO Box 398Adelaide SA 5001

Tel: +61 8 8405 4300Fax: +61 8 8405 4301

www.wspgroup.comwww.pbworld.com

Our ref: 2265048A-STC-REP-004 Rev1

3 February 2016

Ashok KaniyalTechnical Research OfficerNuclear Fuel Cycle Royal CommissionLevel 5, 50 Grenfell StreetADELAIDE SA 5000

Dear Ashok

Detailed Business Case – Quantitative Analysis and Initial Business Case –Establishing a Nuclear Power Plant and Systems in South Australia

We are pleased to submit the final version of our report for the nuclear power plantcomponent of the Nuclear Fuel Cycle Royal Commission’s work.

Yours sincerely

David DowningPrincipal Consultant

cc: WSP | Parsons Brinckerhoff (UK) – Paul WillsonSargent & Lundy Consulting – Kenneth GreenKPMG – Matthew Pearce

Q U A L I T Y M A N A G E M E N TISSUE/REVISION FIRST ISSUE REVISION 1 REVISION 2 REVISION 3

Date 23 December2015 2 February 2016

Prepared by

D Downing,P Willson,P McKay,C Best,V Cantone,E Hobart,M Busby,C Reynolds,M Waters,S Luyks, Sargent& Lundy, KPMG,Aquenta

D Downing

Signature

Reviewed by G Sampson G Kneebone

Signature

Authorised by David Downing David Downing

Signature

Project number 2265048A 2265048A

i

WSP | Parsons BrinckerhoffFebruary 2016

Project No 2265048A-STC-REP-004 Rev1Final ReportNuclear Fuel Cycle Royal Commission

TABLE OF CONTENTS1 INTRODUCTION .............................................................................. 11.1 Nuclear Fuel Cycle Royal Commission ............................................................. 11.2 The brief ............................................................................................................. 11.3 The process ....................................................................................................... 11.4 Disclaimers and limitations ............................................................................... 2

1.4.1 Reliance on information ....................................................................................... 21.4.2 Indemnities and warnings..................................................................................... 21.4.3 Continuing engagement ....................................................................................... 31.4.4 Assumptions ........................................................................................................ 3

2 NUCLEAR GENERATION TECHNOLOGIES ................................. 42.1 Potential technologies ....................................................................................... 42.2 Evolutionary reactor designs ............................................................................ 42.3 Advanced reactor designs ................................................................................ 52.4 Large-scale technologies .................................................................................. 5

2.4.1 Pressurised water reactors ................................................................................... 52.4.2 Boiling water reactors .......................................................................................... 62.4.3 Heavy water reactors ........................................................................................... 7

2.5 Small modular reactors ..................................................................................... 82.6 Supporting infrastructure .................................................................................. 9

3 TECHNOLOGY ASSESSMENT .................................................... 103.1 Methodology .................................................................................................... 103.2 Review of technology status ........................................................................... 10

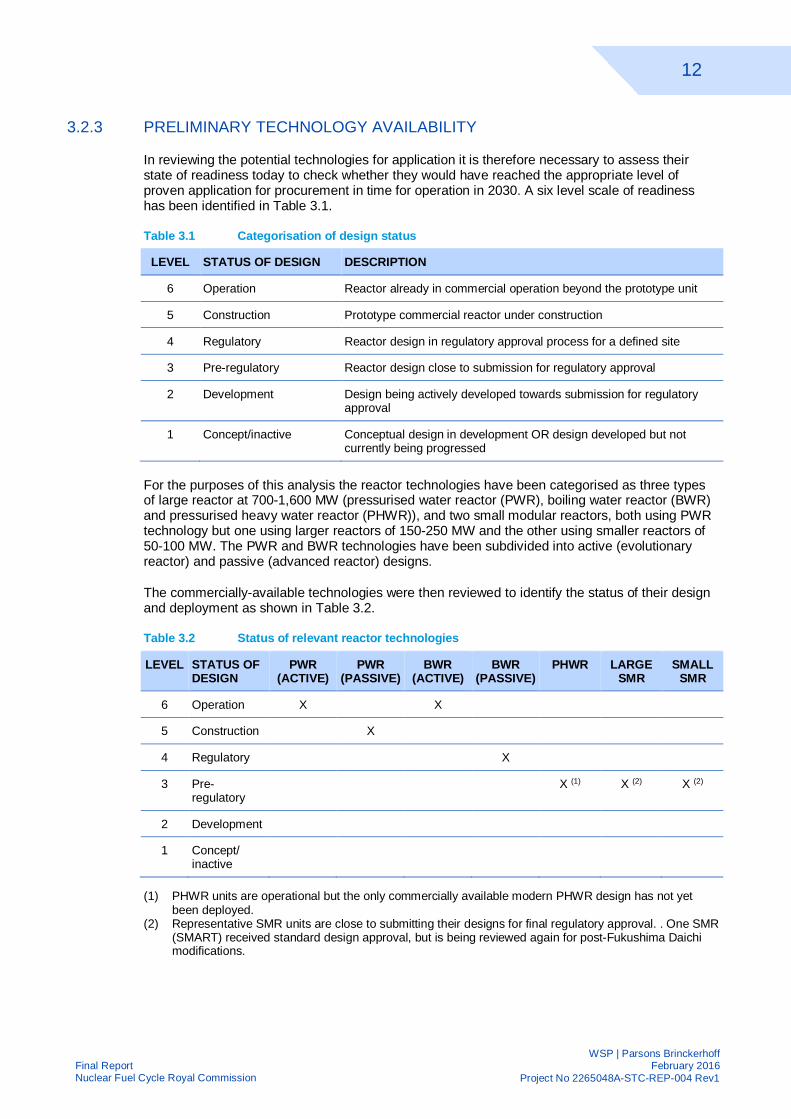

3.2.1 Development status ........................................................................................... 103.2.2 Timescale to 2030.............................................................................................. 113.2.3 Preliminary technology availability ...................................................................... 12

3.3 Limitations for application in South Australia ................................................ 13

3.3.1 Reactor specific limitations ................................................................................. 133.3.2 General site limitations ....................................................................................... 14

3.4 Identification of best-fit technologies ............................................................. 16

4 ALTERNATIVE APPLICATIONS ................................................... 174.1 Storage in electrical generation systems ....................................................... 17

4.1.1 Need for storage ................................................................................................ 174.1.2 Supply characteristics ........................................................................................ 174.1.3 Demand characteristics ...................................................................................... 18

ii

WSP | Parsons BrinckerhoffFebruary 2016

Project No 2265048A-STC-REP-004 Rev1Final ReportNuclear Fuel Cycle Royal Commission

4.1.4 Matching supply and demand............................................................................. 184.1.5 Storage capability .............................................................................................. 184.1.6 Storage options.................................................................................................. 194.1.7 Conclusion ......................................................................................................... 20

4.2 Hydrogen coproduction from nuclear plant ................................................... 204.2.1 Introduction ........................................................................................................ 204.2.2 Hydrogen production techniques ........................................................................ 204.2.3 Review of alternative hydrogen production technologies..................................... 21

4.3 Neutron irradiation services ............................................................................ 224.3.1 Introduction ........................................................................................................ 224.3.2 Production of cobalt-60 ...................................................................................... 224.3.3 Production of molybenum-99 ............................................................................. 224.3.4 Neutron irradiation of silicon ............................................................................... 23

5 REGULATION ................................................................................ 245.1 Existing regulatory environment ..................................................................... 245.2 Legislative barriers .......................................................................................... 265.3 Planning approvals .......................................................................................... 275.4 Community and stakeholder engagement ...................................................... 28

5.4.1 Key principles of engagement to be considered.................................................. 285.4.2 Engagement during environmental assessment and approvals........................... 305.4.3 Key social aspects to be considered .................................................................. 30

6 COST AND PERFORMANCE ESTIMATES .................................. 326.1 Pre-construction capital costs ........................................................................ 326.2 Generating plant capital costs ........................................................................ 336.2.1 Pressurised water reactors ................................................................................. 336.2.2 Boiling water reactors ........................................................................................ 356.2.3 Pressurised heavy water reactors ...................................................................... 356.2.4 Small modular reactors ...................................................................................... 356.2.5 Imported vs. Australian content .......................................................................... 366.2.6 Summary ........................................................................................................... 406.2.7 Life extension refurbishment .............................................................................. 40

6.3 Infrastructure Capital costs ............................................................................. 41

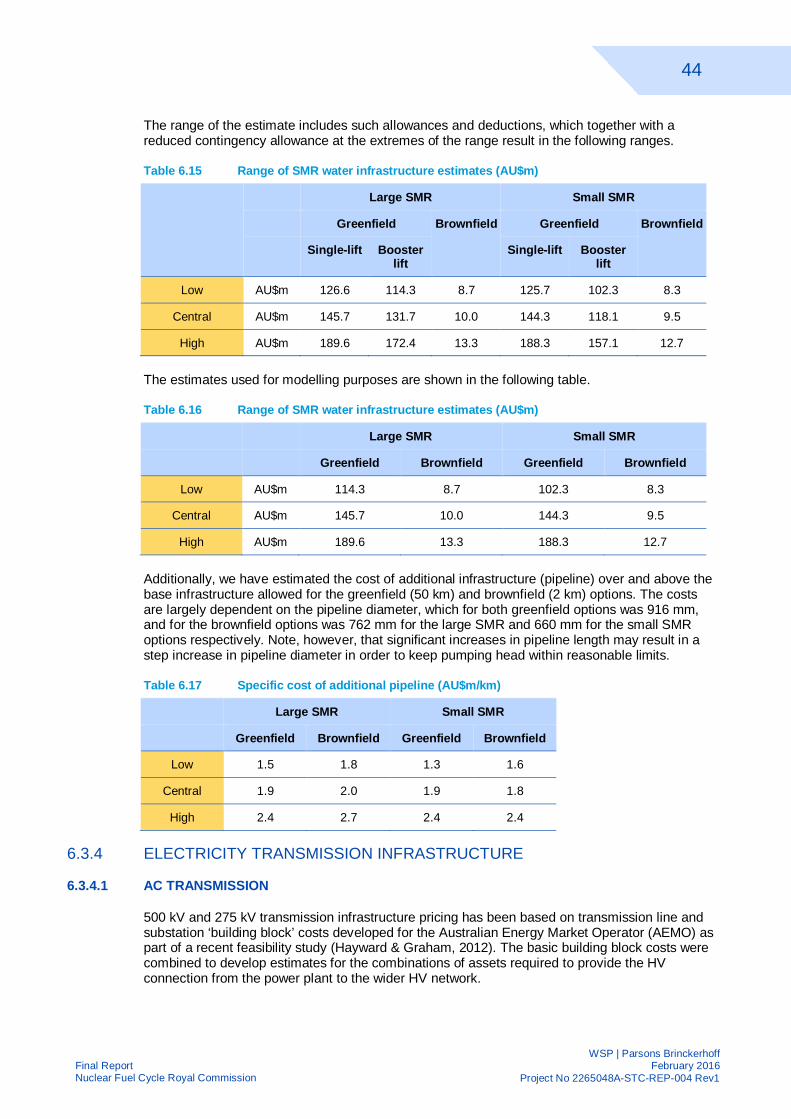

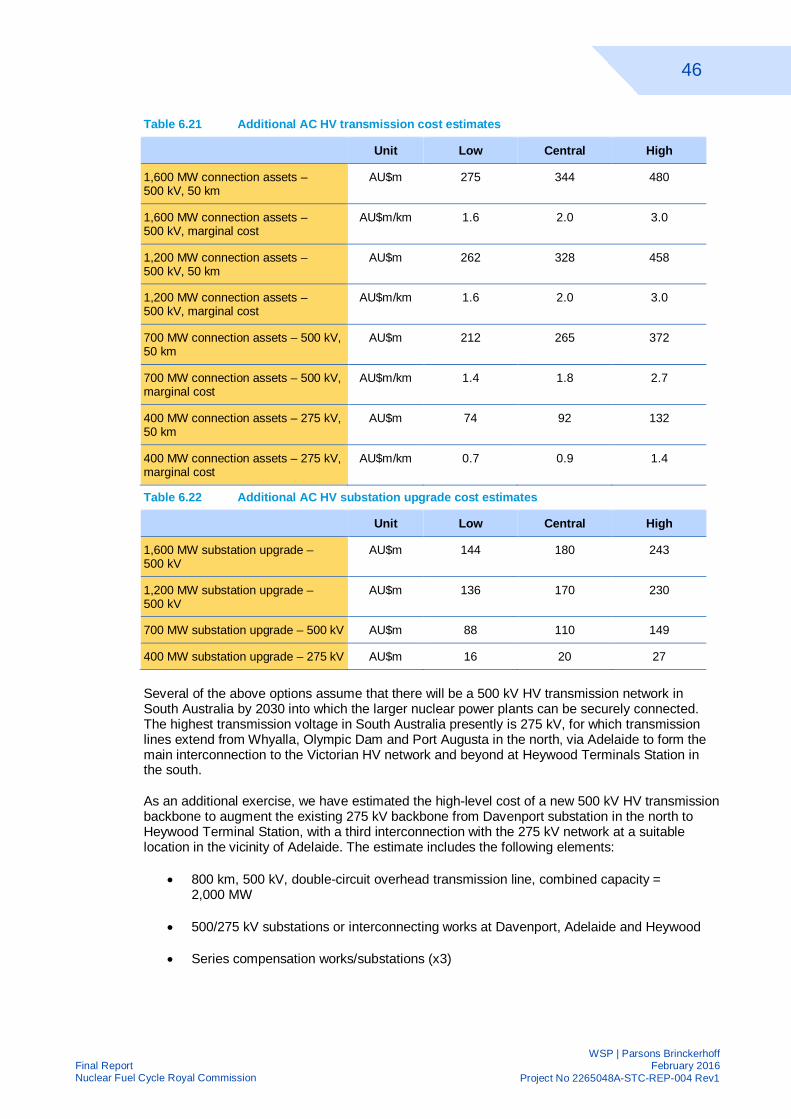

6.3.1 Road infrastructure ............................................................................................ 416.3.2 Rail infrastructure ............................................................................................... 416.3.3 Water supply infrastructure ................................................................................ 426.3.4 Electricity transmission infrastructure ................................................................. 44

6.4 Decommissioning costs .................................................................................. 476.5 Fuel costs ......................................................................................................... 486.6 Spent fuel liability transfer costs .................................................................... 49

iii

WSP | Parsons BrinckerhoffFebruary 2016

Project No 2265048A-STC-REP-004 Rev1Final ReportNuclear Fuel Cycle Royal Commission

6.7 Non-fuel operating costs ................................................................................. 50

6.7.1 Imported vs. Australian content .......................................................................... 516.7.2 Insurance ........................................................................................................... 546.7.3 Transmission use of system (TUoS) & electricity charges ................................... 54

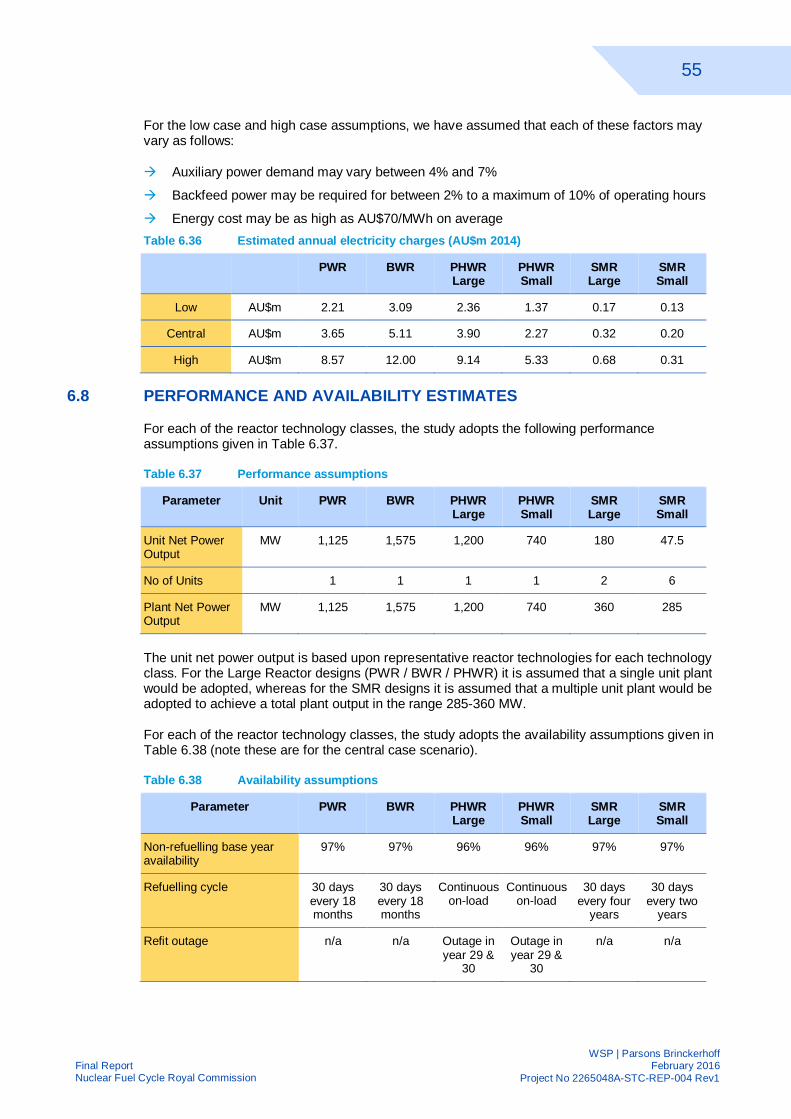

6.8 Performance and availability estimates .......................................................... 556.9 Manpower requirements .................................................................................. 56

6.9.1 Construction manpower ..................................................................................... 576.9.2 Construction Manpower capabilities ................................................................... 586.9.3 Operational manpower ....................................................................................... 59

7 COMMERCIAL ANALYSIS ............................................................ 617.1 Market analysis ................................................................................................ 61

7.1.1 Electricity demand.............................................................................................. 617.1.2 Electricity generation .......................................................................................... 637.1.3 Interconnectors .................................................................................................. 657.1.4 Opportunities for SA nuclear power generation to supply South Australian

market ............................................................................................................... 677.1.5 Opportunities for SA nuclear power generation to supply the Victorian

market ............................................................................................................... 68

7.2 Financing considerations ................................................................................ 707.2.1 Financing challenges ......................................................................................... 707.2.2 Consideration of long-term off-take contracts ..................................................... 737.2.3 International experience in financing of nuclear power ........................................ 747.2.4 Implications for SA Government ......................................................................... 75

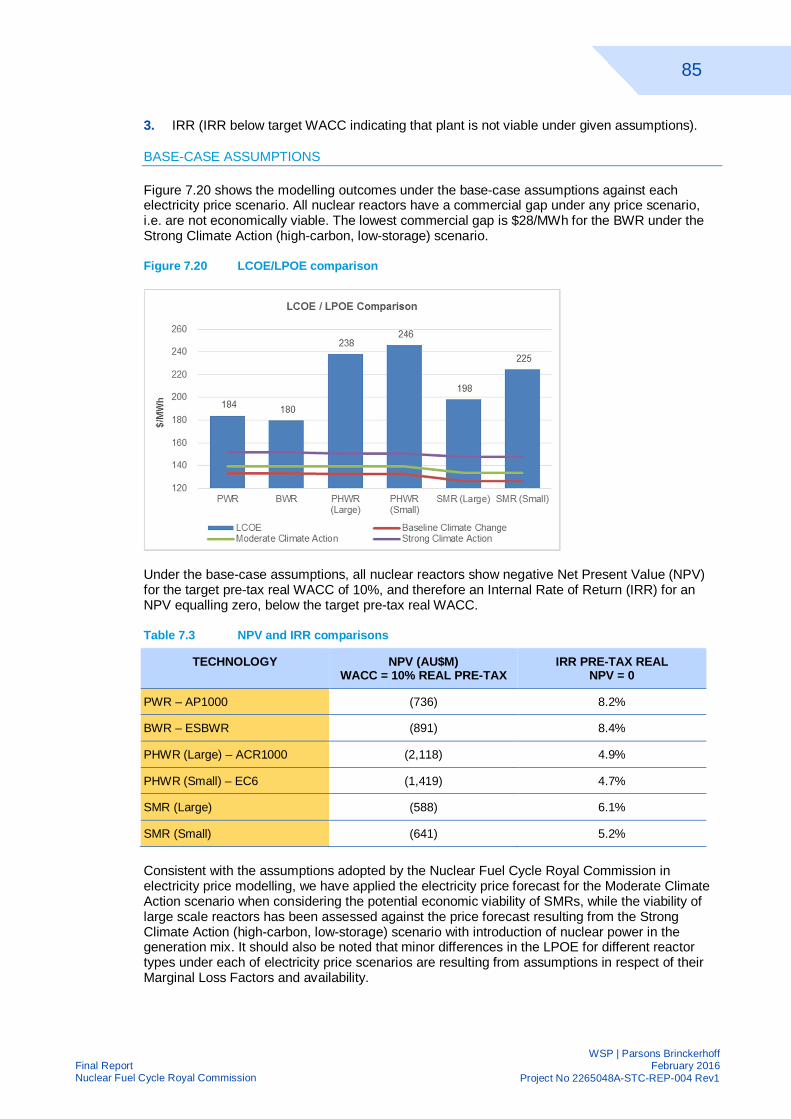

7.3 Economic viability ........................................................................................... 767.3.1 Methodology ...................................................................................................... 767.3.2 Assumptions ...................................................................................................... 797.3.3 Outputs and conclusions .................................................................................... 83

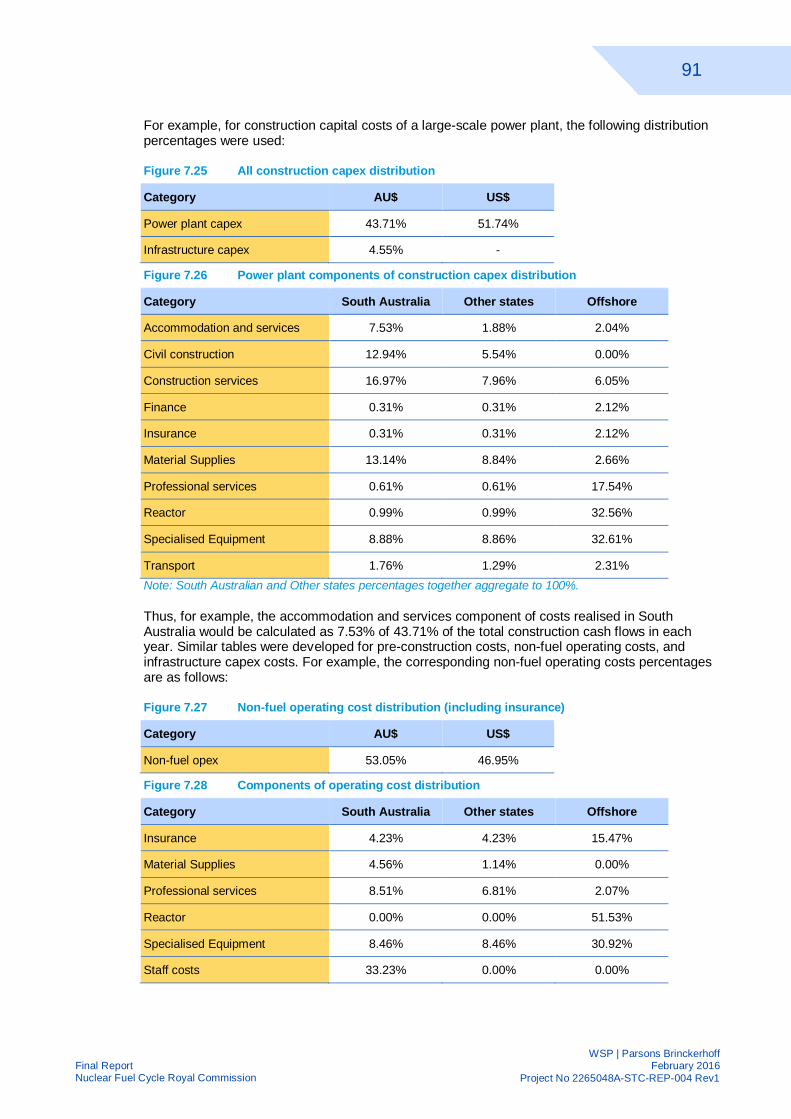

7.4 Cash flow outputs for CGE analysis ............................................................... 897.4.1 CGE data requested .......................................................................................... 897.4.2 CGE data provided ............................................................................................ 90

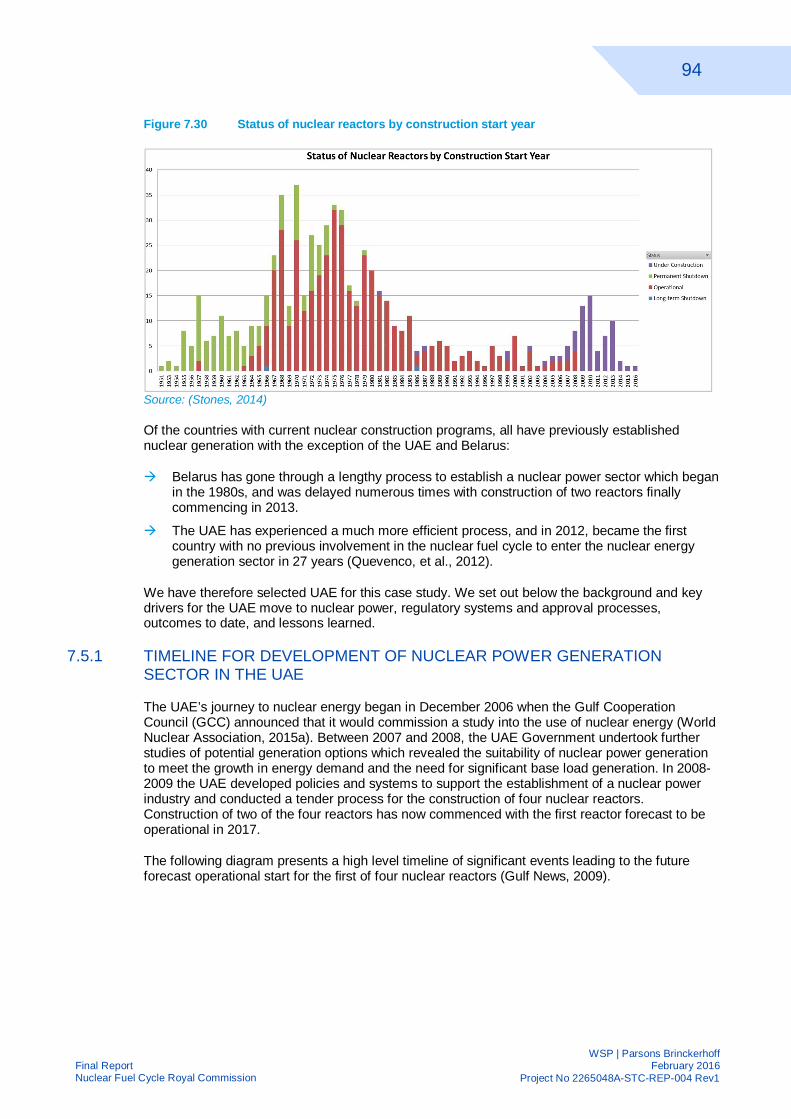

7.5 Case Study: Development of nuclear power generation industry inUnited Arab Emirates....................................................................................... 92

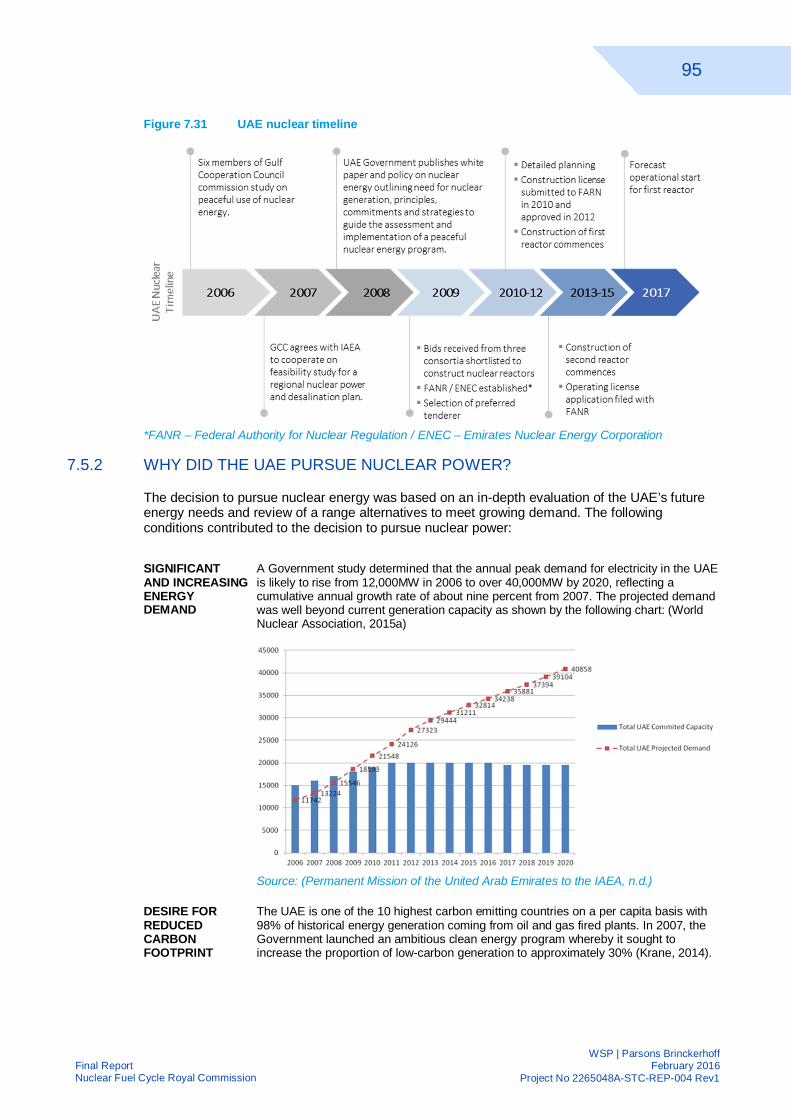

7.5.1 Timeline for development of nuclear power generation sector in the UAE ........... 947.5.2 Why did the UAE pursue nuclear power? ........................................................... 957.5.3 Legislative and regulatory framework ................................................................. 967.5.4 Competitive procurement ................................................................................... 977.5.5 Development approval process .......................................................................... 987.5.6 Project financing ................................................................................................ 997.5.7 Project cost and time variances .......................................................................... 997.5.8 Lessons learned .............................................................................................. 100

iv

WSP | Parsons BrinckerhoffFebruary 2016

Project No 2265048A-STC-REP-004 Rev1Final ReportNuclear Fuel Cycle Royal Commission

8 REFERENCES ............................................................................. 101

L I S T O F T A B L E STable ES.1 Suitability of reactor technologies................................................................ xiiTable ES.2 Pre-construction capital costs ($m 2014) ......................................................... xiiiTable ES.3 Nuclear power plant overnight construction capital costs ($m 2014) ................. xiiiTable ES.4 Life extension refurbishment capital cost (US$m 2014) .................................... xiiiTable ES.5 Supporting infrastructure capital cost (AU$m 2014)......................................... xivTable ES.6 Range of SMR water infrastructure capital cost estimates (AU$m 2014) ......... xivTable ES.7 AC HV greenfield connection asset capital cost estimates (AU$m).................. xivTable ES.8 AC HV brownfield connection asset capital cost estimates (AU$m) ................. xivTable ES.9 Decommissioning cost estimates (US$m, 2014) ............................................. xivTable ES.10 Fuel and spent fuel liability transfer cost estimates (US$/MWh output) ............. xvTable ES.11 Estimated annual non-fuel operating cost ($m 2014)........................................ xvTable ES.12 High-low power plant overnight construction capital costs ($m 2014) .............. xviTable ES.13 High-low annual non-fuel operating cost estimates ($m 2014) ......................... xviTable ES.14 Power plant operational assumptions.............................................................. xvii

Table 3.1 Categorisation of design status ........................................................................ 12Table 3.2 Status of relevant reactor technologies ............................................................ 12Table 3.3 Indicative technology scores for the candidate technologies ............................. 16Table 5.1 Relevant South Australian legislation ............................................................... 24Table 5.2 Relevant Commonwealth legislation ................................................................ 25Table 5.3 Legislative barriers to the development of nuclear facilities .............................. 27Table 6.1 Pre-construction capital costs ($m 2014) ......................................................... 32Table 6.2 Overnight FOAK capital cost estimates for SMRs – National Nuclear

Laboratory (UK) ............................................................................................... 35Table 6.3 Percentage distribution of overnight capital costs by account ........................... 37Table 6.4 Proportions of each capital cost category attributed to imported and local

content ............................................................................................................ 38Table 6.5 Percentage distribution of capital cost by account and by jurisdiction ............... 39Table 6.6 Nuclear power plant overnight construction capital costs ($/kW 2014) .............. 40Table 6.7 Nuclear power plant overnight construction capital costs ($m 2014) ................. 40Table 6.8 Life extension refurbishment capital cost (US$m 2014) .................................... 41Table 6.9 Roads infrastructure capital cost (AU$m 2014) ................................................ 41Table 6.10 Specific cost of additional road (AU$k/km 2014) .............................................. 41Table 6.11 Rail infrastructure capital cost (AU$m 2014) .................................................... 42Table 6.12 Specific cost of additional rail (AU$k/km 2014) ................................................. 42Table 6.13 SMR water infrastructure parameters............................................................... 43Table 6.14 SMR water infrastructure base estimates (AU$m) ............................................ 43Table 6.15 Range of SMR water infrastructure estimates (AU$m) ..................................... 44Table 6.16 Range of SMR water infrastructure estimates (AU$m) ..................................... 44

v

WSP | Parsons BrinckerhoffFebruary 2016

Project No 2265048A-STC-REP-004 Rev1Final ReportNuclear Fuel Cycle Royal Commission

Table 6.17 Specific cost of additional pipeline (AU$m/km) ................................................. 44Table 6.18 AC HV greenfield connection asset cost estimates (AU$m).............................. 45Table 6.19 AC HV brownfield connection asset cost estimates (AU$m) ............................. 45Table 6.20 AC HV connection asset incremental cost estimates (AU$m) ........................... 45Table 6.21 Additional AC HV transmission cost estimates ................................................. 46Table 6.22 Additional AC HV substation upgrade cost estimates ....................................... 46Table 6.23 Additional AC HV substation upgrade cost estimates ....................................... 47Table 6.24 HVDC transmission cost estimates .................................................................. 47Table 6.25 Decommissioning cost estimates (US$m, 2014) .............................................. 48Table 6.26 Fuel cost estimates (US$/MWh output) ............................................................ 49Table 6.27 Spent fuel liability transfer cost estimates (US$/MWh output) ........................... 50Table 6.28 Bottom-up estimate of fixed O&M costs – large scale ....................................... 51Table 6.29 Bottom-up estimate of fixed O&M costs – large scale ....................................... 52Table 6.30 Categorisation of fixed O&M costs – large scale .............................................. 52Table 6.31 Categorisation of fixed O&M costs – SMR ....................................................... 53Table 6.32 Estimated annual non-fuel operating cost assumptions ($/MW 2014) ............... 53Table 6.33 Estimated annual non-fuel operating cost ($m 2014)........................................ 54Table 6.34 Estimated annual insurance cost assumptions ($/MW 2014) ............................ 54Table 6.35 Estimated annual insurance cost assumptions ($m 2014) ................................ 54Table 6.36 Estimated annual electricity charges (AU$m 2014) .......................................... 55Table 6.37 Performance assumptions ............................................................................... 55Table 6.38 Availability assumptions ................................................................................... 55Table 6.39 Large-scale plant construction manpower estimates – two-unit plant ................ 57Table 6.40 Large-scale plant construction manpower capabilities estimate ........................ 58Table 7.1 Financier checklist ........................................................................................... 71Table 7.2 Financier due diligence requirements............................................................... 72Table 7.3 NPV and IRR comparisons .............................................................................. 85Table 7.4 Cost sensitivity ................................................................................................ 88Table 7.5 WACC sensitivity ............................................................................................. 88Table 7.6 Nuclear reactors under construction by country ............................................... 92

L I S T O F F I G U R E SFigure ES.1 LCOE/LPOE comparison ............................................................................... xviiiFigure ES.2 Composition of LCOE for different reactor types ............................................. xix

Figure 3.1 Development timeline for large reactors / SMR projects ................................... 11Figure 5.1 IAP2 Public Participation Spectrum .................................................................. 29Figure 7.1 Summary of operation consumption by key component in South Australia ....... 62Figure 7.2 Summer 10% POE maximum demand forecast segments for South

Australia .......................................................................................................... 62Figure 7.3 Rooftop PV forecasts for low, medium and high consumption scenarios

in South Australia ............................................................................................ 63

vi

WSP | Parsons BrinckerhoffFebruary 2016

Project No 2265048A-STC-REP-004 Rev1Final ReportNuclear Fuel Cycle Royal Commission

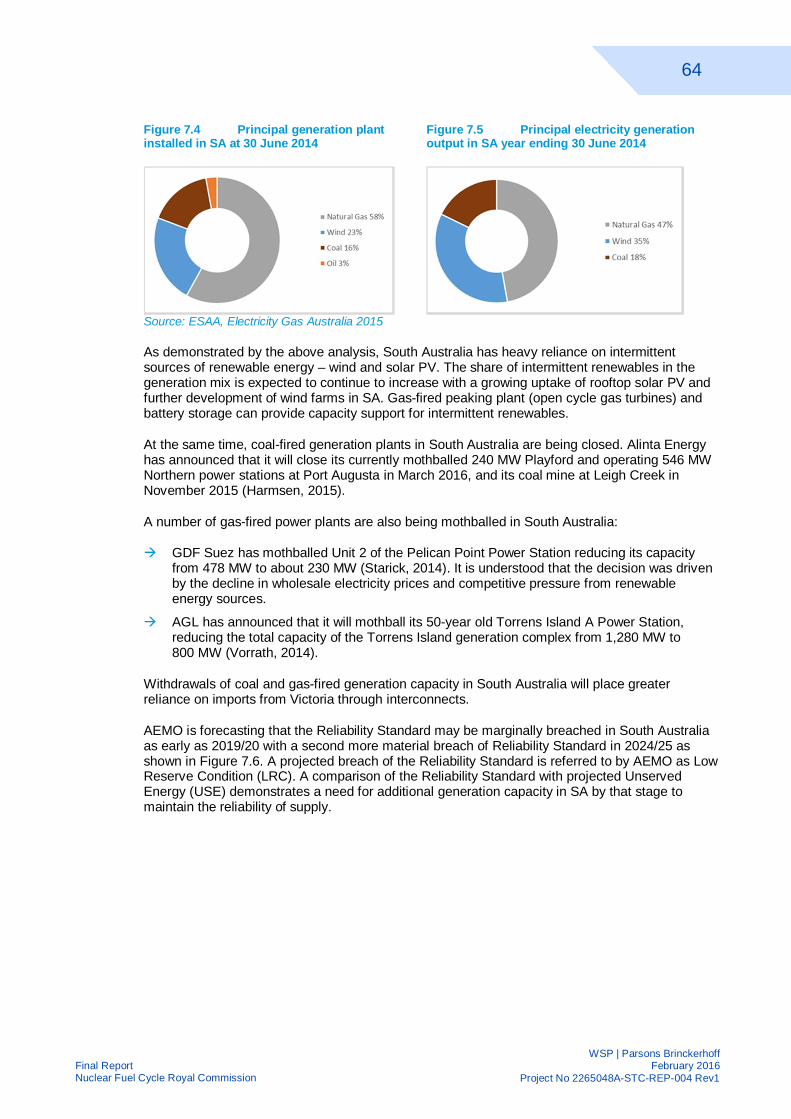

Figure 7.4 Principal generation plant installed in SA at 30 June 2014 ............................... 64Figure 7.5 Principal electricity generation output in SA year ending 30 June 2014 ............ 64Figure 7.6 South Australia supply adequacy (Medium scenario) ....................................... 65Figure 7.7 SA to VIC electricity transmission interconnects ............................................... 66Figure 7.8 Total interconnector imports and exports, South Australia ................................ 66Figure 7.9 Operational consumption by key component in Victoria.................................... 68Figure 7.10 Principal generation plant installed in VIC at 30 June 2014 .............................. 69Figure 7.11 Principal generation output in VIC year ending 30 June 2014 ........................... 69Figure 7.12 Financial model schematic............................................................................... 78Figure 7.13 Timing assumptions ......................................................................................... 79Figure 7.14 Electricity price forecasts ................................................................................. 80Figure 7.15 Comparison of IS3 Large data at 11 November and 30 November 2015 .......... 81Figure 7.16 Comparison of carbon price forecasts .............................................................. 81Figure 7.17 Comparison of carbon price forecasts .............................................................. 82Figure 7.18 US$/AU$ exchange rate forecast ..................................................................... 83Figure 7.19 LCOE cost breakdown ..................................................................................... 84Figure 7.20 LCOE/LPOE comparison ................................................................................. 85Figure 7.21 Low cost LCOE/LPOE comparison .................................................................. 86Figure 7.22 High cost LCOE/LPOE Comparison ................................................................. 86Figure 7.23 Low case WACC (7%) LCOE/LPOE comparison ............................................. 87Figure 7.24 High case WACC (13%) LCOE/LPOE comparison ........................................... 87Figure 7.25 All construction capex distribution .................................................................... 91Figure 7.26 Power plant components of construction capex distribution .............................. 91Figure 7.27 Non-fuel operating cost distribution (including insurance) ................................. 91Figure 7.28 Components of operating cost distribution ....................................................... 91Figure 7.29 Nuclear reactors operational by country ........................................................... 93Figure 7.30 Status of nuclear reactors by construction start year ........................................ 94Figure 7.31 UAE nuclear timeline ....................................................................................... 95Figure 7.32 UAE nuclear regulatory structure ..................................................................... 97Figure 7.33 Barakah Nuclear Power Plant construction timeline ......................................... 99

L I S T O F A P P E N D I C E SAppendix A Technology-based modelling assumptionsAppendix B Weighted Average Cost of Capital CalculationAppendix C Cashflow outputs for CGE Modelling inputs

vii

WSP | Parsons BrinckerhoffFebruary 2016

Project No 2265048A-STC-REP-004 Rev1Final ReportNuclear Fuel Cycle Royal Commission

A B B R E V I AT I O N SABWR advanced boiling water reactor

AC alternating current

AECL Atomic Energy of Canada Limited

AEMO Australian energy market operator

AUDAU$

Australian dollar

BWR boiling water reactor

°C degrees Celsius

CANDU CANada Deuterium Uranium

CCGT combined cycle gas turbine

CFD contract for difference

CGE computable general equilibrium

DC direct current

DECC Department of Energy and Climate Change (UK Government)

EPC Engineering, Procurement, Construction [contract]

EPR evolutionary pressurised reactor

ESAA Electricity Supply Association of Australia

ESBWR economic simplified boiling water reactor

EUR€

euro

EY Ernst & Young

FID final investment decision

FOAK first-of-a-kind

FTE full-time equivalent

GBP£

United Kingdom pound sterling

GCC Gulf Cooperation Council: an intergovernmental political and economicunion comprising Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and theUnited Arab Emirates

viii

WSP | Parsons BrinckerhoffFebruary 2016

Project No 2265048A-STC-REP-004 Rev1Final ReportNuclear Fuel Cycle Royal Commission

GW gigawatt

GWd gigawatt-day

GWh gigawatt-hour

HVDC high voltage direct current

IRR internal rate of return

km kilometre

kV kilovolt

kW kilowatt

LCC load commutated converter

LCOE levelised cost of electricity

LWR light water reactor

L/s litres per second

MW megawatt

MWe megawatts electric

MWh megawatt-hour

m³/sec cubic metres per second

NEM National Electricity Market

NFCRC Nuclear Fuel Cycle Royal Commission

NOAK nth-of-a-kind

NPP nuclear power plant

NPV net present value

PHWR pressurised heavy water reactor

POE probability of exceedence

PPA Power purchase agreement

PWR pressurised water reactor

SMR small modular reactors

t tonnes

t/hr tonnes per hour

ix

WSP | Parsons BrinckerhoffFebruary 2016

Project No 2265048A-STC-REP-004 Rev1Final ReportNuclear Fuel Cycle Royal Commission

t/y tonnes per year

TRL technical readiness level

TUoS transmission use of system

UAE United Arab Emirates

UK United Kingdom

US United States

USNRC United States Nuclear Regulatory Commission

US DOE United States Department of Energy

USDUS$

United States dollar

WACC weighted average cost of capital

x

WSP | Parsons BrinckerhoffFebruary 2016

Project No 2265048A-STC-REP-004 Rev1Final ReportNuclear Fuel Cycle Royal Commission

E X E C U T I V E S U M M A RYKEY OBJECTIVES/PURPOSE

WSP | Parsons Brinckerhoff has partnered with KPMG, Sargent & Lundy and Aquenta to investigatethe third of the four main aspects of the nuclear fuel cycle, namely the use of nuclear fuels forelectricity generation in a nuclear power plant that would be planned to enter commercial operationIn South Australia around 2030. The objectives are to:

à estimate the capital and operating costs necessary for the development of commercially-basednuclear power plants in South Australia for commencement of operation by 2030;

à identify contingency and risk factors that will affect these costs;

à calculate the levelised cost of electricity (LCOE) under a range of commercial discount rates;

à identify a checklist of considerations to be satisfied in order to secure project finance.

METHODOLOGY

Having reviewed the reactor types that would be likely to be commercially available by 2030, andhaving identified those that would be most representative of the classes of technology to which theybelong, WSP | Parsons Brinckerhoff estimated the capital and operating costs by a combination oftop-down and bottom-up methodologies, depending on the availability and the reliability of existingcost data. The reactor types selected as representative of their technology class were:

Pressurised water reactor (PWR) Westinghouse AP1000

Boiling water reactor (BWR) GE Hitachi ESBWR – Economicsimplified BWR

Pressurised heavy water reactor (PHWR) – large AECL ACR-1000

Pressurised heavy water reactor – small AECL EC6

Small modular reactor (SMR) – large B&WBechtel

mPower

Small modular reactor – small NuScale Power NuScale

Nuclear power plant construction is an internationally competitive market, so Engineering,Procurement and Construction (EPC) contract costs can vary according to the market’s appetite forthe available technologies or manufacturers’ products. The estimates developed for the nuclearpower plants themselves therefore are based on a top-down approach including verifiable reportingof recent market experience for established technologies, and of forecast costs for maturingtechnologies. Plants under construction in the US (Vogtle and VC Summer), with mandatory publicreporting requirements, serve as ideal reference plants against which to benchmark cost estimatesof large-scale plants. There are no reference plants based on small modular reactor (SMR)technologies for which benchmark cost data can be verified. However, there have been severalinvestigations performed in other jurisdictions which can be used to benchmark likely SMRconstruction costs.

Estimates of the cost of supporting infrastructure, such as roads, transmission connections, etc., arebased on a bottom-up approach in which high-level scopes of supply were developed and costedaccording to published unit prices and building block costs. Supporting infrastructure estimateswere based on the following assumptions made for the siting of a nuclear power plant in South

xi

WSP | Parsons BrinckerhoffFebruary 2016

Project No 2265048A-STC-REP-004 Rev1Final ReportNuclear Fuel Cycle Royal Commission

Australia, namely that a generic brownfield site is assumed to be adjacent or very close to existinginfrastructure, and a generic greenfield site is assumed to be located approximately 50 km fromexisting infrastructure.

Historical costs of the provision of nuclear fuel and forecast costs for the disposal of spent nuclearfuel enabled life-cycle fuel-related costs to be estimated from unit rates. Non-fuel operating costswere estimated from data reported to regulatory agencies by long-term experienced operators ofnuclear generating facilities.

KEY FINDINGS/ CONCLUSIONS

CANDIDATE REACTOR TECHNOLOGIES

Nuclear power has been used for power generation for over 60 years during which time manynuclear reactor concepts have developed and been constructed. Although development continueswith new concepts and possibilities, there are limited nuclear technologies which havedemonstrated safe, reliable and economic operation. The leading technology internationally is thepressurised water reactor (PWR), representing over 275 of the world fleet of 440 operationalreactors. The next most widely adopted technology is the boiling water reactor (BWR) representinga further 80 units. Of the remaining units the pressurised heavy water reactor (PHWR) is the mostsignificant with 32 units.

This study has reviewed the available solutions in each of these categories which fit the potentialapplication in South Australia at a capacity in the region of 1,000 MW, in the event ranging fromabout 700 MW to 1,600 MW. The history and current commercial availability of these technologieshas been considered along with the potential for up-coming simplified and smaller scale versions ofthe same technologies – small modular reactors – which may better fit the limitations of theelectrical network in South Australia.

TECHNICAL ASSESSMENT CRITERIA

Three criteria are identified for the technical assessment: availability of the technology for possibleapplication on a proven basis in 2030, minimum limitations for connection to the electricity networkand minimum constraints on siting of a reactor in South Australia.

Despite the three dominant nuclear technologies having a long history, the commercial availabilityof the current designs is important. Proven pressurised water reactor designs at a scale of1,100-1,400 MW and boiling water reactors at 1,350-1,600 MW are most suitable for the proposedrequirement. The more extensive regulatory and construction cycle required for the currentpressurised heavy water reactor design means that it is considered likely to be available on aproven basis only some years after 2030. The new SMR designs – all small scale PWRs – arecurrently believed to be close to submission for regulatory approval which would allow them to beavailable on a proven basis by 2030 if the vendors can maintain their development schedules.

The scale of the larger reactors of any technology will require substantial uprating of the electricitytransmission network and demand changes in operation of the electricity system to maintainreliability of supply. However, growth in renewable generation is likely to necessitate major networkdevelopment by 2030 which should overcome many such limitations. SMR technologies arecomparable to or smaller than existing generating units in South Australia and present no suchissues for their application.

Siting constraints including the requirement for access to cooling water for the larger reactorsrequire their siting on, or close to, an ocean coast. Such sites could be a suitable greenfield locationor potentially on a brownfield site, subject to consideration of all environmental requirements.Particular requirements include access to road and rail links for construction and operational traffic

xii

WSP | Parsons BrinckerhoffFebruary 2016

Project No 2265048A-STC-REP-004 Rev1Final ReportNuclear Fuel Cycle Royal Commission

with adequate fresh water supplies for process and service use. Access to large volumes of coolingwater is preferred, although the use of cooling towers would be feasible subject to a larger supply offresh water to maintain conditions in the cooling water circulation. Siting constraints for SMRs areless restrictive, allowing them to be applied at a remote inland site with limited water supply,although their capacity would be reduced.

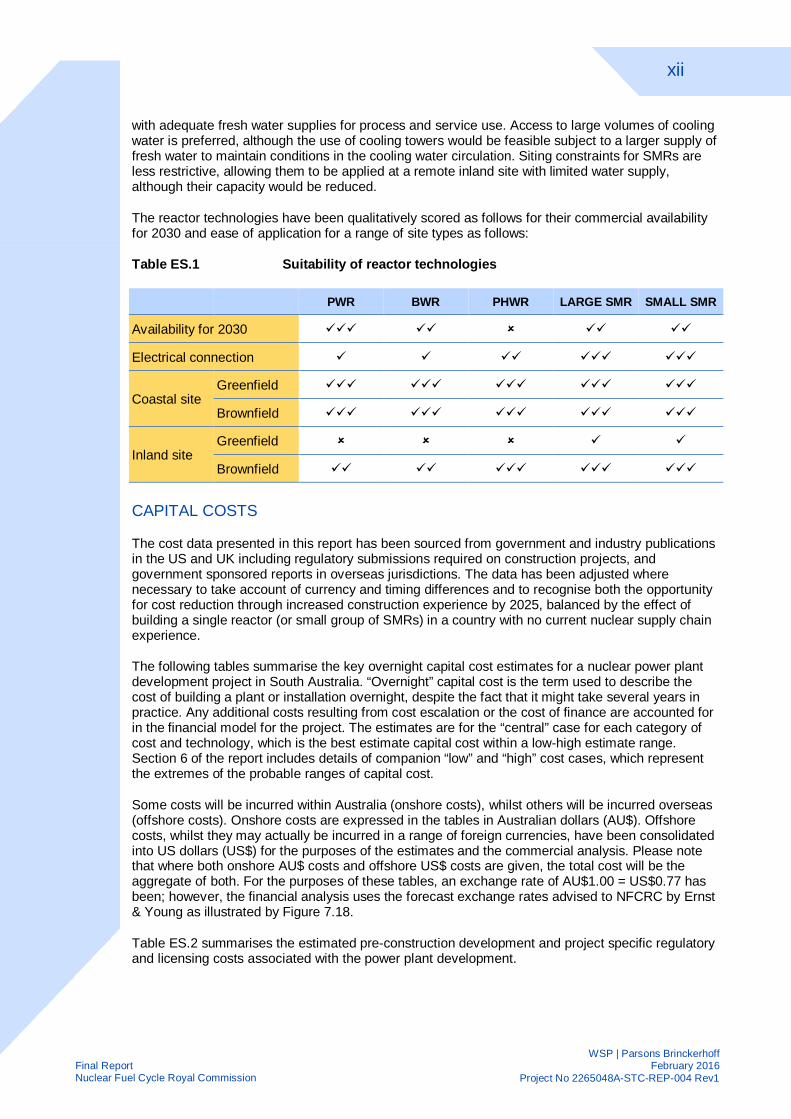

The reactor technologies have been qualitatively scored as follows for their commercial availabilityfor 2030 and ease of application for a range of site types as follows:

Table ES.1 Suitability of reactor technologies

PWR BWR PHWR LARGE SMR SMALL SMR

Availability for 2030 üüü üü û üü üü

Electrical connection ü ü üü üüü üüü

Coastal siteGreenfield üüü üüü üüü üüü üüü

Brownfield üüü üüü üüü üüü üüü

Inland siteGreenfield û û û ü ü

Brownfield üü üü üüü üüü üüü

CAPITAL COSTS

The cost data presented in this report has been sourced from government and industry publicationsin the US and UK including regulatory submissions required on construction projects, andgovernment sponsored reports in overseas jurisdictions. The data has been adjusted wherenecessary to take account of currency and timing differences and to recognise both the opportunityfor cost reduction through increased construction experience by 2025, balanced by the effect ofbuilding a single reactor (or small group of SMRs) in a country with no current nuclear supply chainexperience.

The following tables summarise the key overnight capital cost estimates for a nuclear power plantdevelopment project in South Australia. “Overnight” capital cost is the term used to describe thecost of building a plant or installation overnight, despite the fact that it might take several years inpractice. Any additional costs resulting from cost escalation or the cost of finance are accounted forin the financial model for the project. The estimates are for the “central” case for each category ofcost and technology, which is the best estimate capital cost within a low-high estimate range.Section 6 of the report includes details of companion “low” and “high” cost cases, which representthe extremes of the probable ranges of capital cost.

Some costs will be incurred within Australia (onshore costs), whilst others will be incurred overseas(offshore costs). Onshore costs are expressed in the tables in Australian dollars (AU$). Offshorecosts, whilst they may actually be incurred in a range of foreign currencies, have been consolidatedinto US dollars (US$) for the purposes of the estimates and the commercial analysis. Please notethat where both onshore AU$ costs and offshore US$ costs are given, the total cost will be theaggregate of both. For the purposes of these tables, an exchange rate of AU$1.00 = US$0.77 hasbeen; however, the financial analysis uses the forecast exchange rates advised to NFCRC by Ernst& Young as illustrated by Figure 7.18.

Table ES.2 summarises the estimated pre-construction development and project specific regulatoryand licensing costs associated with the power plant development.

xiii

WSP | Parsons BrinckerhoffFebruary 2016

Project No 2265048A-STC-REP-004 Rev1Final ReportNuclear Fuel Cycle Royal Commission

Table ES.2 Pre-construction capital costs ($m 2014)

Project Development Regulatory/Licensing

Pre-construction costs

AU$m 311 44

US$m 63 16

Total AU$mequivalent 393 65

Table ES.3 summarises the overnight capital cost estimates by currency for the representativepower plants of the different technology classes being studied.

Table ES.3 Nuclear power plant overnight construction capital costs ($m 2014)

PWR BWR PHWRLarge

PHWRSmall

SMRLarge

SMRSmall

Net capacity MW 1,125 1,575 1,200 740 360 285

NPPconstruction

costs

AU$m 3,814 5,339 4,500 2,775 1,102 960

US$m 3,476 4,867 4,092 2,523 1,310 1,143

TotalAU$m

equivalent8,328 11,660 9,814 6,052 2,803 2,444

Given the availability of good quality data from regulatory reporting submissions on recent PWRconstruction projects, we are confident that the PWR cost estimate (based on AP1000 rectortechnology) in Table ES.3 is fundamentally sound. Long-term experience has shown that therelative costs of PWR and BWR projects are reasonably consistent, so we are also quite confidentthat the BWR estimate is reasonably sound, though we are concerned that the capacity of the BWRtechnology considered (GE-Hitachi ABWR) is likely to be too large for the South Australian system.We are less confident of the PHWR estimates owing to the lack of recent projects with publishedout-turn costs. However, given that we believe that the availability of Generation III/III+ PWHRtechnology by 2030 will be very low, the low level of confidence is not material to our overallfindings.

There are no SMR projects yet implemented to serve as cost benchmarks. However, there is aconsiderable amount of SMR manufacturers’ literature available, and independent studies in otherjurisdictions that have looked at the SMR market in considerable detail. Therefore, given the degreeof independent analysis by others, we are quite confident that both the SMR cost estimates arebasically sound.

Table ES.4 summarises the estimated capital cost of the life extension refurbishment associatedwith PHWR CANDU-type reactors after approximately 30 years’ service.

Table ES.4 Life extension refurbishment capital cost (US$m 2014)

PHWR Large PHWR Small

PHWR life extensioncost

US$m 2,000 1,450

Table ES.5 summarises the estimated capital cost of road, rail and marine supporting infrastructureassociated with the power plants located in generic brownfield and greenfield locations.

xiv

WSP | Parsons BrinckerhoffFebruary 2016

Project No 2265048A-STC-REP-004 Rev1Final ReportNuclear Fuel Cycle Royal Commission

Table ES.5 Supporting infrastructure capital cost (AU$m 2014)

Brownfield Greenfield

Supporting infrastructurecost

AU$m 9.184 193.180

The cost of water supply infrastructure for the coastal large-scale plants has been included in theoverall capital cost of the plants. Water supply infrastructure costs for the SMR-based plants locatedaway from the coast are shown in Table ES.6.

Table ES.6 Range of SMR water infrastructure capital cost estimates (AU$m 2014)

Large SMR Small SMR

Greenfield Brownfield Greenfield Brownfield

SMR water supplyinfrastructure cost

AU$m 145.7 10.0 144.3 9.5

Table ES.7 and Table ES.8 summarise the estimated capital cost of high voltage AC transmissioninfrastructure to connect the power plants to existing electricity transmission networks in genericgreenfield and brownfield locations respectively.

Table ES.7 AC HV greenfield connection asset capital cost estimates (AU$m)

PWR BWR PHWRLarge

PHWRSmall

SMRLarge

SMRSmall

Transmission Voltage, kV 500 500 500 500 275 275

Greenfield transmissionconnection assets cost AU$m 344 344 344 265 92 92

Table ES.8 AC HV brownfield connection asset capital cost estimates (AU$m)

PWR BWR PHWRLarge

PHWRSmall

SMRLarge

SMRSmall

Transmission Voltage, kV 500 500 500 500 275 275

Brownfield transmissionconnection assets cost AU$m 167 183 167 112 22 22

DECOMMISSIONING COSTS

Decommissioning of the power plant and remediation of the site will be funded by annualcontributions to a decommissioning reserve that, with investment in low-risk instruments, willaccumulate to provide future funds upon completion of the operating life of the plant equivalent tothe escalated value of the FY2014 estimates in Table ES.9.

Table ES.9 Decommissioning cost estimates (US$m, 2014)

PWR BWR PHWRLarge

PHWRSmall

SMRLarge

SMRSmall

Decommissioning cost US$m 500 575 500 250

xv

WSP | Parsons BrinckerhoffFebruary 2016

Project No 2265048A-STC-REP-004 Rev1Final ReportNuclear Fuel Cycle Royal Commission

OPERATING COSTS

The following tables summarise the “central” case key operating cost estimate components for anuclear power plant development project. Details of the companion “low” and “high” cost cases aregiven in section 6, as are comparatively minor costs such as insurance and connection charges. Aswith the capital cost estimate, some costs will have both onshore and offshore components,denoted in AU$ and US$ respectively. In such cases, the total cost is again the aggregate of both.

Table ES.10 summarises the estimated cost of fuel, and the estimated cost of transferring theliability for long-term storage of spent fuel to the long-term storage facility.

Table ES.10 Fuel and spent fuel liability transfer cost estimates (US$/MWh output)

PWR BWR PHWRLarge

PHWRSmall

SMRLarge

SMRSmall

Fuel cost US$/MWh 7.60 9.10

Spent fuel liabilitytransfer cost US$m/MWh 3.75 27.00 4.50

Table ES.11 summarises the estimated annual non-fuel operating cost excluding insurance.

Table ES.11 Estimated annual non-fuel operating cost ($m 2014)

PWR BWR PHWRLarge

PHWRSmall

SMRLarge

SMRSmall

Net capacity MW 1,125 1,575 1,200 740 360 285

Non-fuel operating cost

AU$m 108.1 151.4 115.3 71.1 37.9 30.0

US$m 63.0 88.2 67.2 41.4 17.6 13.9

TotalAU$m

equivalent189.9 265.9 202.6 124.9 60.8 48.1

CENTRAL ESTIMATE RISKS AND LIMITATIONS

In addition to the “central” case cost estimates summarised here, section 6 of this report considersthe likely range of cost estimates that might be expected. There are several main factors thatintroduce risks and uncertainties to the estimates, a few of which key factors are descried here.

Nuclear power plant construction projects are subject to market forces. An EPC contract value maybe influenced by several market factors at the time a contract is tendered and placed, such as:

à Contractors’ workloads – contractors with low forward workloads may offer better deals thanthose with full order books.

à Market penetration – manufacturers offering particular generation technologies may offer betterdeals to increase their market penetration – this may be particularly prevalent in the SMRmarket as more technologies come to market.

à Jurisdictional penetration – manufacturers seeking to enter new country markets may offerbetter deals to be the first to market.

xvi

WSP | Parsons BrinckerhoffFebruary 2016

Project No 2265048A-STC-REP-004 Rev1Final ReportNuclear Fuel Cycle Royal Commission

Whilst there may be advantages to owners from each of these possibilities, there may also bemarket risks arising from, for example, construction contractors or manufacturers of “popular”nuclear generation technologies becoming more expensive. Ultimately, it will only be possible tojudge the optimum technological and commercial solution following a comprehensive tenderingprocess.

The total equivalent Australian dollar high and low case capital cost estimates shown in TableES.12 also make allowance for the possibility of construction schedule and cost under- or over-runs. Recent project experience has shown that there is a distinct risk of construction scheduleslippage. Whilst under a fixed-price EPC contract, there should be minimal direct impact to the EPCconstruction cost, there will be indirect impacts that would have to be borne by the project owner.Furthermore, it is increasingly likely that EPC contractors will attempt to increase the constructionrisk allowances into their future proposals, although this would be tempered by a downwardpressure resulting from a need to remain competitive in the nuclear construction market. The high-case estimates include some provision for such behaviour.

Table ES.12 High-low power plant overnight construction capital costs ($m 2014)

PWR BWR PHWRLarge

PHWRSmall

SMRLarge

SMRSmall

Low TotalAU$m 7,738 10,831 8,253 5,089 2,385 2,073

High TotalAU$m 9,201 12,881 11,376 7,015 3,368 2,922

Operational costs will also be subject to market forces. The cost of fuel, for example, will depend onthe future demand for uranium and fabricated nuclear fuel and the capacity of the world’s uraniummines and fuel processing facilities to meet it.

A particular issue for the establishment of a nuclear power plant in South Australia will be the lack ofawareness, expertise and experience in nuclear generating facilities among the existing labourforce. In the short-term and in key areas of expertise, the shortfall might be met by the recruitmentof appropriately qualified staff from overseas, but given that there is expected to be a world-wideincrease in demand developing for nuclear-qualified expertise, the cost of such expertise might behigh. The long-term sustainable solution to South Australia’s skills gap will be to transfer nuclearknowledge and expertise under a planned programme of education and retraining to upskill theexisting workforce.

The total equivalent Australian dollar high-low operational cost estimates in Table ES.13 includeprovision for various operational and staffing risks.

Table ES.13 High-low annual non-fuel operating cost estimates ($m 2014)

PWR BWR PHWRLarge

PHWRSmall

SMRLarge

SMRSmall

Net capacity MW 1,125 1,575 1,200 740 360 285

LowTotal

AU$mequivalent

151.9 212.7 162.1 99.9 48.6 38.4

HighTotal

AU$mequivalent

227.9 319.0 243.1 149.8 72.9 57.8

xvii

WSP | Parsons BrinckerhoffFebruary 2016

Project No 2265048A-STC-REP-004 Rev1Final ReportNuclear Fuel Cycle Royal Commission

OPERATIONAL ASSUMPTIONS

Table ES.14 summarises the central case power plant output and availability estimates. Higher andlower range average capacity factors incorporating (respectively) longer and shorter refuellingoutages have also been estimated.

Table ES.14 Power plant operational assumptions

Parameter PWR BWR PHWRLarge

PHWRSmall

SMRLarge

SMRSmall

Unit Net PowerOutput

MW 1,125 1,575 1,200 740 180 47.5

No of Units 1 1 1 1 2 6

Plant Net PowerOutput

MW 1,125 1,575 1,200 740 360 285

Non-refuellingbase yearavailability

% 97 97 96 96 97 97

Refuelling cycle 30 daysevery 18months

30 daysevery 18months

Continuouson-load

Continuouson-load

30 daysevery four

years

30 daysevery two

years

Refit outage n/a n/a Outage inyear 29 &

30

Outage inyear 29 &

30

n/a n/a

Overallavailability profile:Year 1

Year 2

Year 3

Year 4

Year 5

Year 29 and 30(PHWR)

Year 31 (PHWR)

%

%

%

%

%

%

97.00%

89.03%

89.03%

Y1-3repeats

…

97.00%

89.03%

89.03%

Y1-3repeats

…

96.00%

96.00%

85.48%

Y1-3repeats

…

0%

Y1-3repeats

96.00%

96.00%

85.48%

Y1-3repeats

…

0%

Y1-3repeats

96.99%

96.99%

93.01%

93.01%

Y1-4repeats

…

93%

Annually

INPUTS/ASSUMPTIONS

In addition to the cost estimates and siting assumptions described above, WSP | ParsonsBrinckerhoff adopted macro-economic assumptions, in common with other technology study teams,as required by the Royal Commission, which were based on advice from the Royal Commissionand its other advisers.

A general inflation rate of 2.5% was used, with operating and maintenance costs escalating at anadditional 1.05% in real terms. Ernst & Young advised forecast US$/AU$ foreign exchange ratesuntil 2050 (see Figure 7.18), in addition to forecast wholesale electricity prices for four differentclimate action scenarios over the same period.

xviii

WSP | Parsons BrinckerhoffFebruary 2016

Project No 2265048A-STC-REP-004 Rev1Final ReportNuclear Fuel Cycle Royal Commission

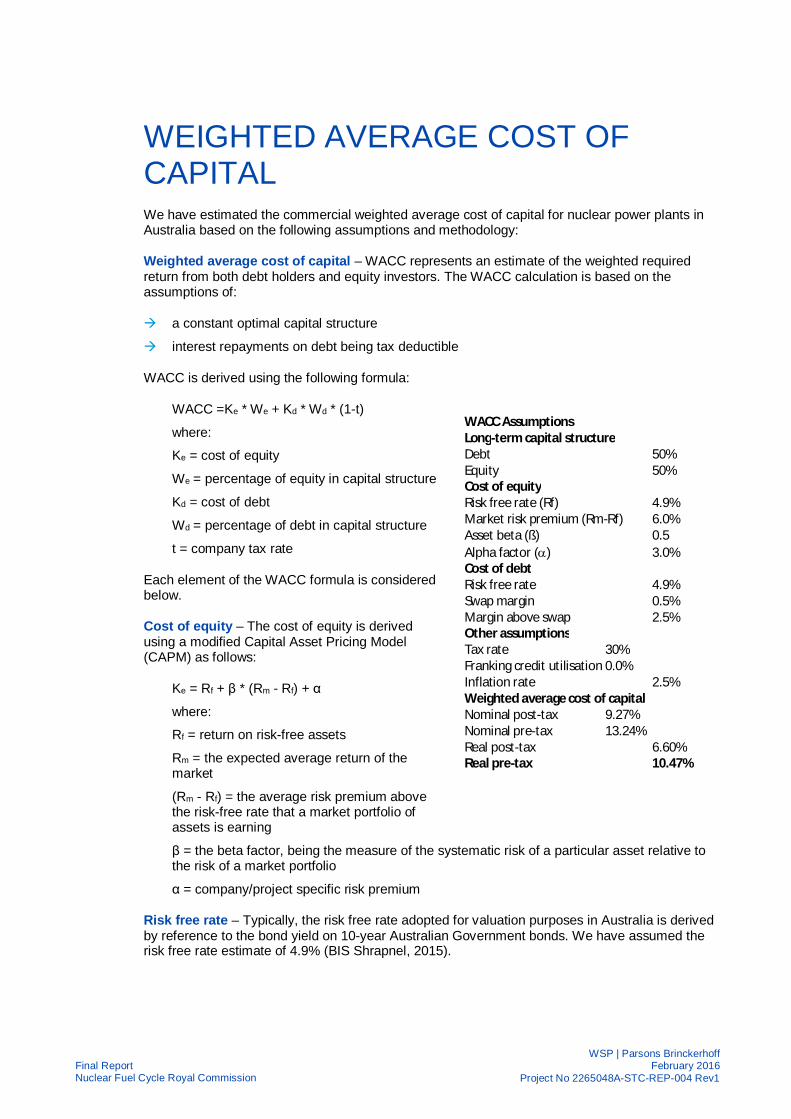

WSP | Parsons Brinckerhoff analysed a likely financing structure for a nuclear generating businessin South Australia, and estimated the real pre-tax weighted average cost of capital to be about10.47%, which was within the range of 10-11% that had been expected based on a review of earlierstudies. For the purposes of the financial analysis, a real pre-tax WACC of 10% was used as aproxy for the discount rate in net present value (NPV) calculations.

LEVELISED COST OF ELECTRICITY

Figure ES.1 illustrates for the central case assumptions of each technology type being studied, thelevelised cost of electricity (LCOE) assuming a weighted average cost of capital (on a real, pre-taxbasis) of 10%. Figure ES.1 also illustrates the levelised price of electricity (LPOE) for the wholesaleelectricity price projections forecasted by Ernst & Young as of 11 November 2015. The figure clearlyillustrates the commercial gap that exists for all reactor types under central case cost assumptions.

Figure ES.1 LCOE/LPOE comparison

KEY SENSITIVITIES

The composition of LCOE in Figure ES.2 shows that all nuclear power technologies arecharacterised by high fixed costs and relatively low variable costs. Capital cost recovery, and fixedoperation and maintenance costs account for about 90% of LCOE of nuclear power plants. Capitalcost of plant construction is by far the largest component of the LCOE. The cost of fuel supply tonuclear power plants is a relatively minor component of their LCOE. The PHWR technologies haveproportionately higher costs as a result of estimated spent fuel disposal costs which areapproximately six times greater than other reactor types.

xix

WSP | Parsons BrinckerhoffFebruary 2016

Project No 2265048A-STC-REP-004 Rev1Final ReportNuclear Fuel Cycle Royal Commission

Figure ES.2 Composition of LCOE for different reactor types

Sensitivity analysis shows that LCOE of nuclear power plants is most sensitive to capital cost andWACC assumptions. Under all central case assumptions, the internal rate of return for eachtechnology is less than the base-case WACC assumption, indicating a commercial gap or deficit asopposed to a surplus. However, a small commercial surplus can be calculated if cost estimates atthe extreme low end of the ranges is assumed in combination with plant performance (i.e. capacityfactors) at the high end of the ranges.

Similarly, a commercial surplus can be realised if the project can be financed more cheaply. Ananalysis using a real pre-tax WACC of 7%, which is below the commercial rate of return normallyexpected by project developers, returned a surplus in the analysis for all the large-scalerepresentative technologies analysed.

ECONOMIC ANALYSIS CONCLUSIONS

Analysis of the economic viability measures for the scenarios under consideration suggests thatnuclear power plants in South Australia are not likely to be economically viable, unless:

à capital and operating costs of nuclear power plants are reduced to or below the lowest extremeof the plausible range of costs considered by this study; and/or

à the cost of capital (debt and equity) is reduced to a level that is unlikely to be commerciallyavailable from the open market; and

à electricity prices increase dramatically as a result of strong climate action, such as 100%reduction in emissions relative to 2000 levels by 2040 to 2050.

FINANCING CHALLENGES

Analysis of recent international experience in the development and financing of nuclear powerplants demonstrates that:

à developers require long-term revenue certainty to commit to investment and be able to raiseproject financing and often require Government guarantees of project debt; and

à Governments continue to play a key role in facilitating the development of nuclear power (evenin countries that have a long history in the nuclear power generation industry) through a wide

xx

WSP | Parsons BrinckerhoffFebruary 2016

Project No 2265048A-STC-REP-004 Rev1Final ReportNuclear Fuel Cycle Royal Commission

range of mechanisms, such as long-term Power Purchase Agreements (PPAs), Contracts forDifference (CFDs) guaranteeing a strike price, loan guarantees, and export credit.

Our hypothesis for the financing of nuclear power plants in South Australia is that:

à nuclear power plants would require long-term revenue certainty in order to attract interest ofprivate sector equity investors and debt financiers; and

à the SA Government would need to provide significant support through revenue underwriting,loan guarantees, and/or in other forms in order to attract private sector developers andfinanciers of nuclear power generation.

There are very few precedents in the Australian energy market for PPAs or electricity hedgingcontracts with the very long contract durations that would be required to underpin financing of anuclear power plant, and most of these precedents involved a State Government as a contractcounterparty. If private sector players in the National Electricity Market are not willing to enter intoelectricity hedging contracts with nuclear power stations for a sufficiently long term to underpinproject financing, the SA Government would have to provide revenue certainty to a nuclear powerplant developer through a CFD or another revenue support mechanism.

Depending on the perception of risks associated with nuclear power by project financiers, the SAGovernment may also be required to provide loan guarantees in addition to revenue support. Thishas been the experience in recent nuclear power plants developments – the Vogtle plant in the USAand the Hinkley Point C plant in the UK.

1

WSP | Parsons BrinckerhoffFebruary 2016

Project No 2265048A-STC-REP-004 Rev1Final ReportNuclear Fuel Cycle Royal Commission

1 INTRODUCTION1.1 NUCLEAR FUEL CYCLE ROYAL COMMISSION

The Nuclear Fuel Cycle Royal Commission (NFCRC) was established by the Government ofSouth Australia to investigate South Australia’s participation in the four main aspects of thenuclear fuel cycle:

à exploration and extraction of mineralsà processing of minerals and manufacture of materials containing radioactive substancesà use of nuclear fuels for electricity generation; andà the storage and disposal of radioactive and nuclear waste materials.

Established in March 2015, the Royal Commission has set a strict timetable of work that willenable it to submit its report to the government by 6 May 2016.

1.2 THE BRIEF

WSP | Parsons Brinckerhoff in partnership with KPMG, Sargent & Lundy and Aquenta wasappointed by the NFCRC to investigate the third of these aspects, namely the use of nuclear fuelsfor electricity generation. WSP | Parsons Brinckerhoff is required to quantify the whole-of-life costsentailed in the development, construction, operation and decommissioning of three principal typesof nuclear power plant and their associated systems and infrastructure, taking account of costdatabases and indices appropriate to South Australia.

The assignment is to be conducted in stages, with deliverables to be provided to the NFCRC ateach stage. This report is the final deliverable in response to the scope of work.

This report presents the detailed business case and cost assumptions for a range of nucleargeneration technologies that might be possibilities for the establishment of a nuclear power plantin South Australia.

The brief required the consideration of commercially available Generation III and Generation III+reactor technologies, and how they might be implemented within the South Australian context,assuming a date for the commencement of commercial operation in 2030.

1.3 THE PROCESS

The first stage in the development of any business case is to define what drives the need that theselected solution is designed to satisfy. In this case, the need is driven by the RoyalCommission’s remit to investigate the possibilities for expanding the state’s involvement in allaspects of the nuclear fuel cycle, including the generation of electrical energy from nuclear fuel.Whilst other studies are looking into the possible expansion of mining and exploration, mineralprocessing, and waste storage and disposal; this study is considering the use of products from theexpanded uranium mining and processing industries to generate electricity for use within both thelocal South Australian market and for export to other regions of the National Electricity Market.

In identifying the parameters for the study, NFCRC proposed that several technologies might beappropriate for consideration, broadly separated into large-scale technologies, typically havingreactor outputs of greater than 1000 MW, and small-scale technologies, which are commonlyreferred to as small modular reactors, with reactor outputs of less than 300 MW. WSP | ParsonsBrinckerhoff and Sargent & Lundy nuclear power plant specialists have joined forces to pool theirknowledge and experience of nuclear power plant projects and developments in order to identify

2

WSP | Parsons BrinckerhoffFebruary 2016

Project No 2265048A-STC-REP-004 Rev1Final ReportNuclear Fuel Cycle Royal Commission

and assess the available nuclear power plant technologies that meet the need. The range ofavailable technologies were reduced to a short-list of six categories of plants that either alreadyare, or are expected to be, mature commercially available technologies by 2030.

Establishment of a nuclear power plant necessitates consideration of other impacts including theprovision of new or augmented infrastructure to support the nuclear power plant. The NFCRCproposed that such infrastructure be identified for generic brownfield and greenfield locations,where a brownfield location is defined as one in which there is established connectivity tosupporting infrastructure, and a greenfield site is defined as one in which existing infrastructure islocated 50 km from the site. Together with the nuclear power plant specialists, WSP | ParsonsBrinckerhoff specialists have identified the functional requirements for the supportinginfrastructure, and have identified the new and augmented infrastructure required to support eachpower plant option.

The nuclear power plant specialists used their expertise and contacts to identify sources oftechnical and commercial data that have been used to populate an assumptions book, which isused by KPMG in the modelling of whole-of-life costs for each nuclear power plant option. Theinfrastructure specialists together with Aquenta have identified the infrastructure costs for eachpower plant option. KPMG has combined the technical and commercial assumptions with financialand agreed macro-economic assumptions to develop whole-of-life cost and levelised cost ofenergy outputs for the nuclear power plant options.

1.4 DISCLAIMERS AND LIMITATIONS

1.4.1 RELIANCE ON INFORMATION

To prepare this report we have relied upon macroeconomic assumptions and wholesale pricingforecasts provided in November 2015 by Ernst and Young as NFCRC’s computational generalequilibrium modelling adviser, as well as publically available information and data and whereappropriate WSP | Parsons Brinckerhoff’s, Sargent & Lundy’s, KPMG’s, and Aquenta’s internalsources that we believe to be reliable and accurate. We have no reason to believe that anymaterial facts (that a reasonable person would expect to be disclosed) have been withheld fromus, and we have taken no steps to audit or verify the accuracy, completeness or fairness of thatdata provided.

Our procedures and enquires do not include verification work, nor constitute either an audit orreview.

The sources of information that we have relied upon in providing this report have been outlinedthroughout the body of the document.

1.4.2 INDEMNITIES AND WARNINGS

Our opinions are based upon the basis of information made available to us, and the conditionsand circumstances in place at the time of writing, both of which can change on short noticewithout warning. Accordingly, if the basis of the information provided to us, or the conditions ofcircumstances in place have changed subsequent to the release of our report, our conclusionsmay no longer be relevant. In providing this report, WSP | Parsons Brinckerhoff has no obligationto update this document for such changes, subsequent to its date.

Our report has been prepared for the express purposes outline above, and for the benefit of anduse by the Nuclear Fuel Cycle Royal Commission. No reference to, statement of reliance upon,copy, reprint or image our report can be released to any party other than the Nuclear Fuel CycleRoyal Commission without the prior written consent of WSP | Parsons Brinckerhoff as to the formand content of that release.

3

WSP | Parsons BrinckerhoffFebruary 2016

Project No 2265048A-STC-REP-004 Rev1Final ReportNuclear Fuel Cycle Royal Commission

In relying on our report, the document should always be considered in its entirety.

1.4.3 CONTINUING ENGAGEMENT

This reports on our findings in relation to a business case for the development of a nuclear powerplant in South Australia. As such it is subject to further work before finalisation of the report,including final internal review and approval.

1.4.4 ASSUMPTIONS

In completing the brief, we note that we have relied on the following assumptions:

à Our brief did not extend to undertaking site specific analysis; on the contrary, it was requiredto consider only generic locations for the siting of the candidate nuclear power planttechnologies, and we have outlined appropriate assumptions within the report accordingly.

à We have assumed that each of the power plant options will be operated as a base-loadpower plant, and have detailed corresponding assumptions of power plantavailability/average capacity factor accordingly. The levelised costs of energy resulting fromthe modelling are therefore dependent on this assumption. We understand that otheradvisers to NFCRC are examining the role that a nuclear power plant might play in theNational Electricity Market of the future, including part-load operation and load-followingcapabilities. Such changes to the plant operating profiles would result in changes to thelevelised costs of energy resulting from the modelling.

à We have calculated power plant revenues based on wholesale electricity price forecasts,which have been advised by NFCRC based on market modelling and forecasting performedby Ernst and Young as of 15 November 2015. We note that any later revisions to thewholesale price assumptions may have a material effect on our opinions regarding thecommercial outcomes of the study.

à In order to provide consistency with the other studies being performed for NFCRC, we havebeen advised macroeconomic assumptions by NFCRC, including assumptions for forecastinflation of costs. We understand that this and other macroeconomic assumptions, such asforeign exchange rates have been provided to NFCRC by Ernst & Young, and may yet besubject to further revision.

4

WSP | Parsons BrinckerhoffFebruary 2016

Project No 2265048A-STC-REP-004 Rev1Final ReportNuclear Fuel Cycle Royal Commission

2 NUCLEAR GENERATIONTECHNOLOGIES

2.1 POTENTIAL TECHNOLOGIES

Identification of the nuclear plant options that will be available for proposed commercial operationin the 2030 time frame requires some speculation. There are potentially attractive optionsavailable today which may not continue to be offered in the international marketplace in a fewyears and there are promising new alternatives that are not yet commercially available and may ormay not be viable in the future depending on economic and technical developments.

Nuclear reactors are popularly characterised by their “Generation” (i.e. Generation II, GenerationIII or III+, Generation IV). There is a grey area associated with defining the characteristics thatplace a reactor in one generation or another, but for the purpose of this study all the reactors ofinterest are Generation III or III+. Generation II reactors include most of the currently operatingplants in the world but are no longer offered by the reactor vendors as a commercial product fornew plants. Generation III and III+ designs include both “evolutionary” designs, some of which dohave operating examples as well as ones under construction and “advanced” designs includingenhanced safety features. None of the “advanced” designs are operating but some are underconstruction.

In addition to the larger Generation III and III+ reactors, there are also a set of smaller advanceddesigns termed as Small Modular Reactors (SMR) which are passive designs on a smaller scale,and which allow offsite assembly line type construction.

Generation IV designs, which often have innovative features to deal with nuclear waste or to usealternative fuels, are at an earlier stage of development and are not judged to be likely to be aproven alternative within the time frame under study. However, by 2030, Generation IV designsmay be sufficiently developed to offer new opportunities for the fuel cycle. These might particularlyaffect the disposal costs of spent fuel if spent fuel becomes a resource rather than a waste.

2.2 EVOLUTIONARY REACTOR DESIGNS

Generation III evolutionary designs are enhanced versions of the Generation II operating reactors.Although these plants still require active safety systems (systems which utilise pumps and otherpowered components to remove the core heat and hence avoid excessive fuel temperatures),they have modified the designs to eliminate some of the more probable failure modes. As a result,the risk of radioactive release after an accident has been reduced by one or two orders ofmagnitude from the already low risk of the previous generation of operating units. There have alsobeen design changes included to reduce the construction and operating costs. One of thesechanges is a general increase in the size of the units to take advantage of economies of scalenow practical to implement.

There are a number of evolutionary designs available, but five designs are mature and active inthe market. These are the General Electric/Hitachi ABWR, the Korean APR-1400, the AREVAEPR, the CANDU EC6, and the ATMEA 1100 reactor. The first three are in operation or underconstruction whilst the last two have mature designs with some potential for near term projects. Inaddition some Russian and Chinese designs fall into this category, but the available informationon the technical content, pricing and marketing of these units is limited. As a result they will not beaddressed here except to note their potential existence.

In addition to the domestically developed Russian and Chinese designs, other evolutionarydesigns exist but do not appear to be strong market contenders at the present time. Mitsubishi

5

WSP | Parsons BrinckerhoffFebruary 2016

Project No 2265048A-STC-REP-004 Rev1Final ReportNuclear Fuel Cycle Royal Commission

has developed a 1,700 MWe PWR which gained some interest in Japan and the US for a periodof time, but there appear to be no active projects using this design at present. In spite of thesignificant success of Westinghouse PWR plants among operating units, Westinghouse haschosen to focus on passive Advanced Reactor and Small Modular Reactor designs.Westinghouse offerings are addressed below in the Advanced Reactor discussion.

The Enhanced CANDU 6 (EC6) pressurised heavy water reactor is an evolutionary reactor designbut differs from the others because it is smaller (740 MWe). This design has not yet been built orcontracted for but some potential exists for two units to be added to an existing site in Romania.The available information indicates it would have cost characteristics similar to the CANDU ACR-1000 which is considered an Advanced Reactor while the EC6 would be of interest primarilybecause of the smaller capacity of the unit.

The critical question to be answered about the active safety evolutionary designs is whether theywill continue to be attractive alternatives if the passive safety advanced designs prove to be theirequal commercially. Currently the evolutionary designs appear to offer a small cost advantageresulting from longer experience with these plant designs and their larger size which allowseconomy of scale. However, we believe that the reduced complexity of the passive designs willreduce or eliminate the cost differential in the future such that costs of evolutionary and advancedreactors will converge for plants scheduled to enter operation around 2030.

2.3 ADVANCED REACTOR DESIGNS

Generation III+ advanced reactors are functionally similar to Generation II and evolutionaryGeneration III reactors, but have more passive safety systems. This means that operation ofactive components that require electric power is not required for at least several days after theoccurrence of an event requiring or causing a rapid reactor shutdown. On previous reactordesigns, the failure of offsite power and onsite emergency power supplies has always been amajor contributor to accident risk. Removal of this potential failure provides an additional reductionin risk of significant release of radioactivity. These designs incorporate features that allow heat tobe removed by natural convection and heat transfer mechanisms without requiring activecomponents to operate. The extent to which the safety systems are passive, and the delay timebefore active functions are required eventually to come into operation vary between the designs.

Reactor designs in this category include the Westinghouse AP1000 (1,100 MWe PWR), theGeneral Electric/Hitachi ESBWR (1,500 MWe BWR) and the CANDU ACR1000 (1,200 MWePressurised Heavy Water Reactor PHWR). Domestically developed Russian and Chinesedesigns may also exist in this category, but again, little is known about their designs or cost.

Each of these three Advanced Reactor designs is analysed separately. From availableinformation, many of the costs and characteristics of projects using any of these options would besimilar, as one would expect in a competitive market.

2.4 LARGE-SCALE TECHNOLOGIES

The following identifies and briefly describes available reactor technologies and manufacturersaccording to broad headings below.

2.4.1 PRESSURISED WATER REACTORS

2.4.1.1 EVOLUTIONARY DESIGNS

PWR designs have been the most widely utilised reactor technology with over 275 operating unitsworldwide.

6

WSP | Parsons BrinckerhoffFebruary 2016

Project No 2265048A-STC-REP-004 Rev1Final ReportNuclear Fuel Cycle Royal Commission

The Korean APR-1400 is a larger version of a 1000 MWe pressurised water reactor (PWR)Korean plant which incorporated advanced safety features into a previous standard design. Nineof the 1000 MWe versions are operating. Four APR-1400 units are under construction in Koreaand four more are under construction in United Arab Emirates (UAE). The units in Korea areslightly delayed and slightly over budget. The UAE units were sold as a fixed price project andappear to be on schedule. Additional units are planned in Korea and it is likely the design will beaggressively marketed internationally as successful operational experience accumulates. It shouldbe noted that the Korean 1000 MWe design could probably be marketed internationally but wouldhave a higher cost per unit of capacity than the APR-1400.

The AREVA EPR is a 1600 MWe evolutionary design. Single unit examples are underconstruction in Finland and France and two units are under construction in China. All theseprojects have a troubled history with very large cost increases and schedule delays, the Europeanprojects more than the Chinese projects. Some of this resulted from licensing complications butthe more significant issues seem to be fabrication and construction problems. The EPR wasproposed for several US sites but the USNRC design certification effort has been suspended andthe proposed projects are inactive. The EPR has also been proposed for the Hinkley Point Cproject in the UK but that has also been delayed.

AREVA has teamed with Mitsubishi to develop the ATMEA, a 1,100 MWe PWR design,apparently in response to the construction and market challenges of the EPR, but there are noprojects under construction using this design. The ATMEA design was chosen for a project nowunder development in Turkey and is being considered for other locations such as Vietnam.

The size of both the APR-1400 and the EPR would be a significant challenge to integrate into theSouth Australian network. The ATMEA design would be easier but it is very questionable whetherthe design would be proven in a time frame to support operation in 2030 in South Australia.

2.4.1.2 ADVANCED DESIGNS

The AP1000 is clearly the most successful advanced reactor design to date. The reactor hasbeen design certified by the USNRC, approved in China and is under review in UK and othercountries. Four units of the AP1000 are under construction in the US (two at each of two sites)and similarly a further four units are under construction at two sites in China. At least eight moreUS units are in the licensing process and China has announced ambitious plans to build 20 ormore additional units. Other international projects are in the development phase. The US andChinese projects have experienced some First Of A Kind (FOAK) problems leading to costincreases and schedule delays, but these have not resulted in serious concerns about the viabilityof the projects.