20

Pathways to LDC Graduation The Case of Nepal SWARNIM WAGLÉ NATIONAL PLANNING COMMISSION

Pathways to LDC Graduation The Case of Nepal

SWARNIM WAGLÉ N A T I O N A L P L A N N I N G C O M M I S S I O N

Outline

1. LDCs: A Glimpse

2. Graduation and IPoA

3. Where Does Nepal Stand?

4. The Path Ahead

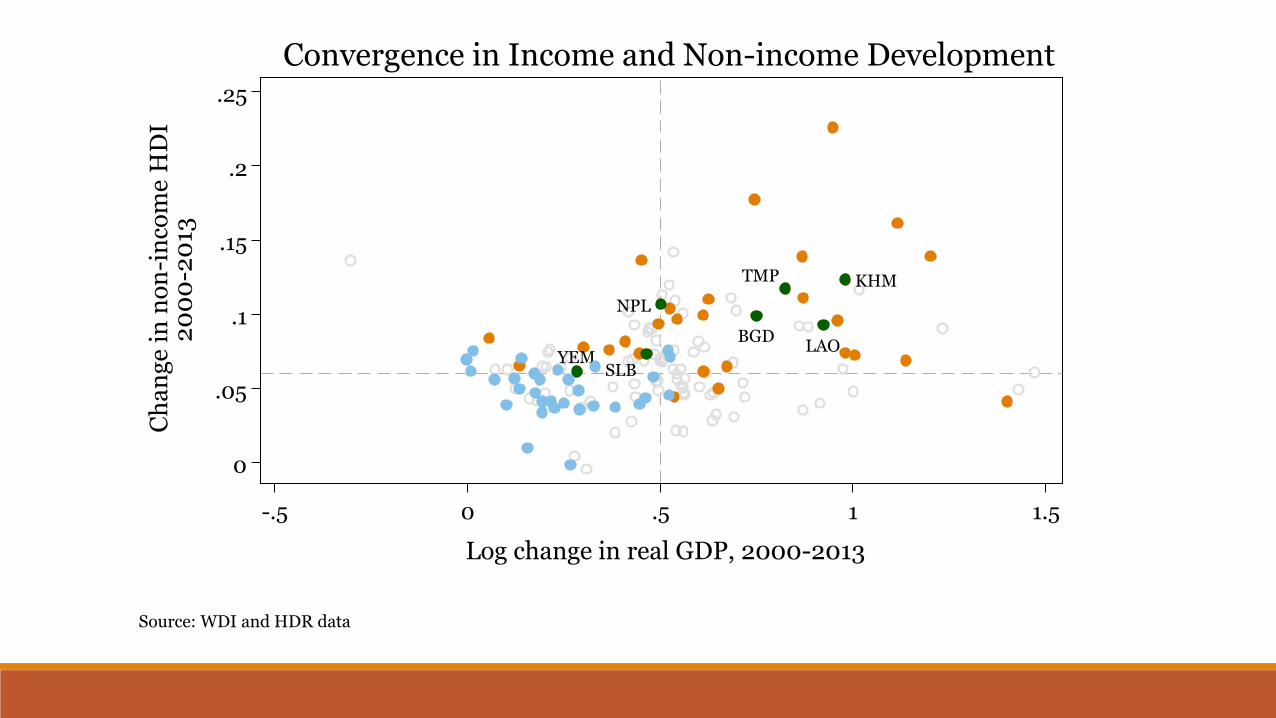

A Glimpse of the Club

1. 48 countries ◦ 13% of world population; 1% of GDP; 1.2% of trade; 2% of FDI inflow

Began with 25 countries (with 3 eligible opting out)

2. A diverse bunch, but shared vulnerabilities ◦ From Bangladesh to Tuvalu; Equatorial Guinea to Malawi

◦ Many are landlocked, remote, undiversified

7 countries account for 3/4 of LDCs’ exports

3. Over 320 million people in 13 LDCs in Asia-Pacific ◦ Third largest in the world if a country (but economy comp. to Greece)

BGD

KHM

LAO

NPL

SLB

TMP

YEM

0

.05

.1

.15

.2

.25

Ch

an

ge

in n

on

-in

com

e H

DI

20

00

-20

13

-.5 0 .5 1 1.5

Log change in real GDP, 2000-2013

Source: WDI and HDR data

Convergence in Income and Non-income Development

BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT BGD

BTN

KIR NPL

VUT

0

15

30

45

60

No

n-m

iner

al

exp

ort

s re

lati

ve

to G

DP

(%

)

6 8.5 11

Log of GDP per capita (PPP)

1995

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

AFG

BTN

KHM

NPL

SLB

VUT

0

15

30

45

60

6 8.5 11

Log of GDP per capita (PPP)

2012

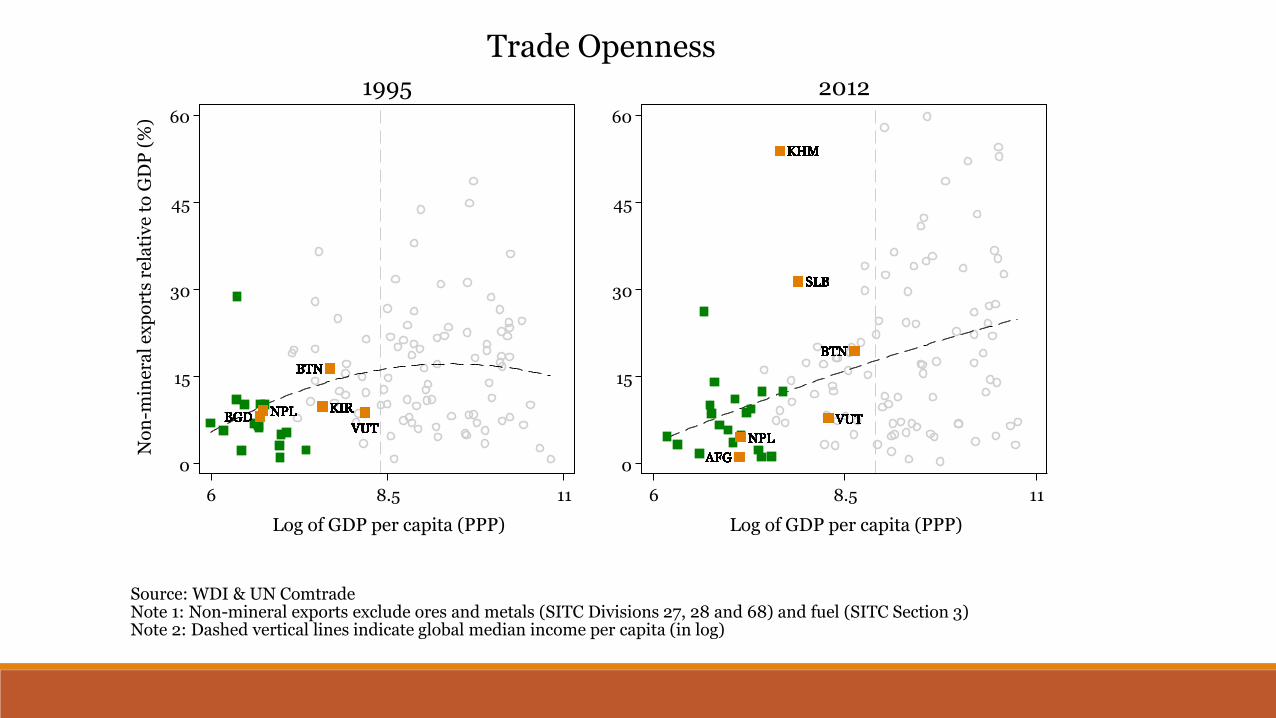

Source: WDI & UN Comtrade Note 1: Non-mineral exports exclude ores and metals (SITC Divisions 27, 28 and 68) and fuel (SITC Section 3) Note 2: Dashed vertical lines indicate global median income per capita (in log)

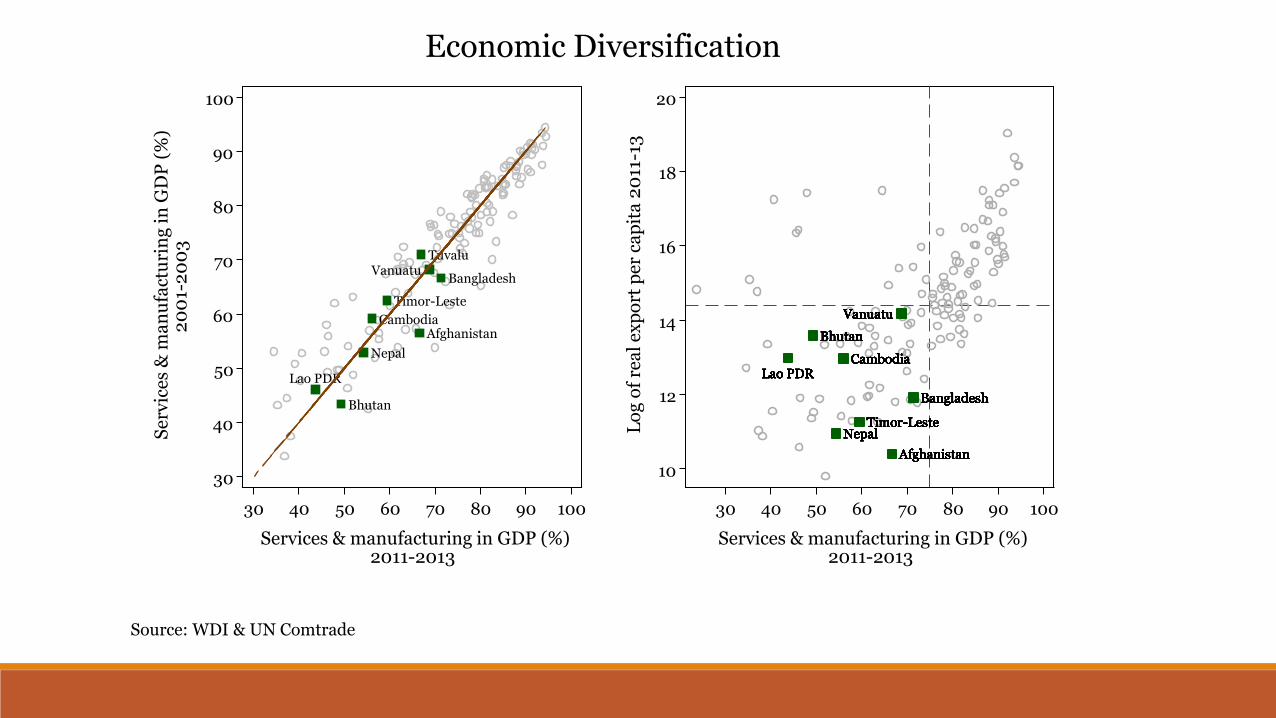

Trade Openness

Afghanistan

Bangladesh

Bhutan

Cambodia

Lao PDR

Nepal

Timor-Leste

Tuvalu Vanuatu

30

40

50

60

70

80

90

100

Ser

vic

es &

ma

nu

fact

uri

ng

in

GD

P (

%)

20

01-

20

03

30 40 50 60 70 80 90 100

Services & manufacturing in GDP (%) 2011-2013

Afghanistan

Bangladesh

Bhutan

Cambodia Lao PDR

Nepal Timor-Leste

Vanuatu

Afghanistan

Bangladesh

Bhutan

Cambodia Lao PDR

Nepal Timor-Leste

Vanuatu

Afghanistan

Bangladesh

Bhutan

Cambodia Lao PDR

Nepal Timor-Leste

Vanuatu

Afghanistan

Bangladesh

Bhutan

Cambodia Lao PDR

Nepal Timor-Leste

Vanuatu

Afghanistan

Bangladesh

Bhutan

Cambodia Lao PDR

Nepal Timor-Leste

Vanuatu

Afghanistan

Bangladesh

Bhutan

Cambodia Lao PDR

Nepal Timor-Leste

Vanuatu

Afghanistan

Bangladesh

Bhutan

Cambodia Lao PDR

Nepal Timor-Leste

Vanuatu

Afghanistan

Bangladesh

Bhutan

Cambodia Lao PDR

Nepal Timor-Leste

Vanuatu

Afghanistan

Bangladesh

Bhutan

Cambodia Lao PDR

Nepal Timor-Leste

Vanuatu

Afghanistan

Bangladesh

Bhutan

Cambodia Lao PDR

Nepal Timor-Leste

Vanuatu

Afghanistan

Bangladesh

Bhutan

Cambodia Lao PDR

Nepal Timor-Leste

Vanuatu

Afghanistan

Bangladesh

Bhutan

Cambodia Lao PDR

Nepal Timor-Leste

Vanuatu

Afghanistan

Bangladesh

Bhutan

Cambodia Lao PDR

Nepal Timor-Leste

Vanuatu

10

12

14

16

18

20

Lo

g o

f re

al

exp

ort

pe

r ca

pit

a 2

011

-13

30 40 50 60 70 80 90 100

Services & manufacturing in GDP (%) 2011-2013

Source: WDI & UN Comtrade

Economic Diversification

Criteria

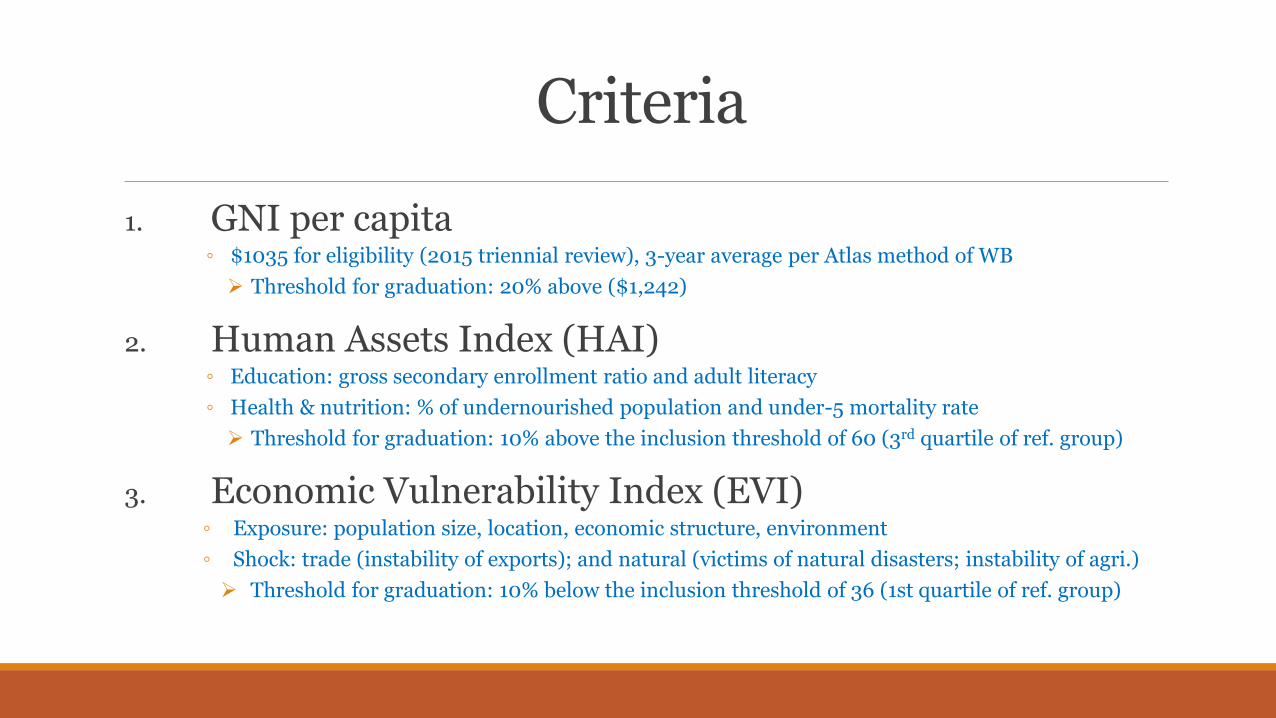

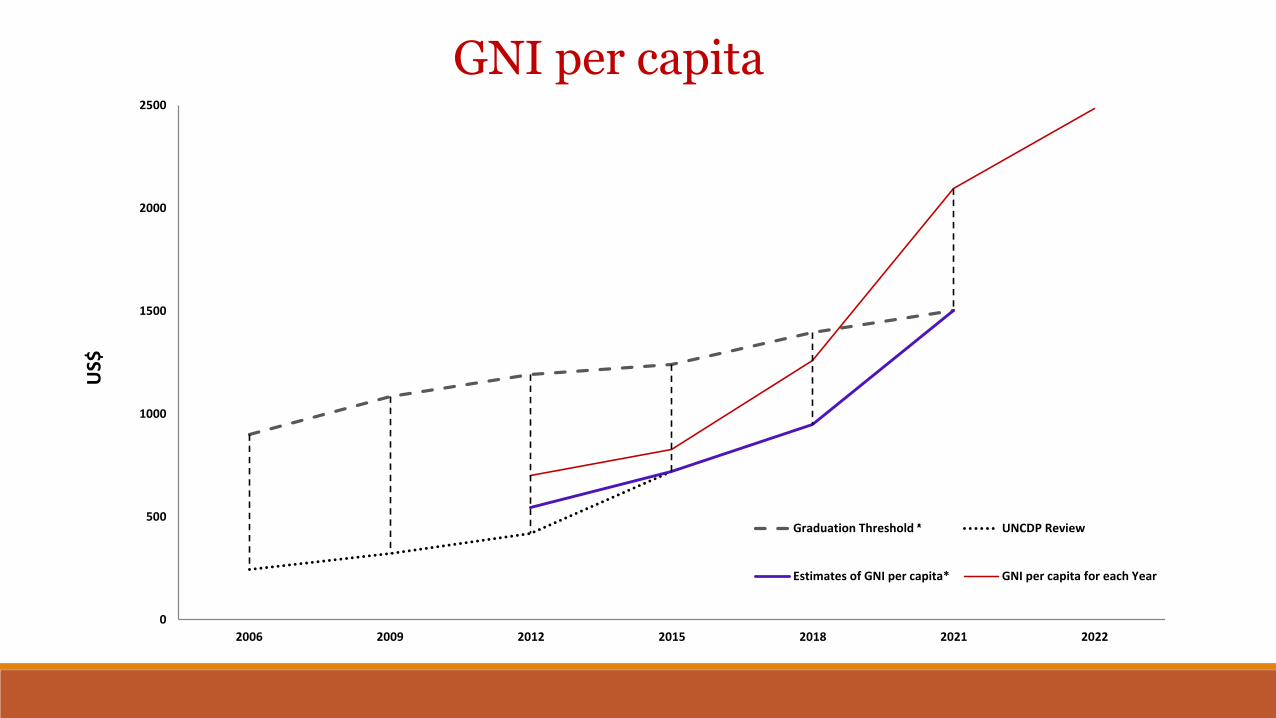

1. GNI per capita ◦ $1035 for eligibility (2015 triennial review), 3-year average per Atlas method of WB

Threshold for graduation: 20% above ($1,242)

2. Human Assets Index (HAI) ◦ Education: gross secondary enrollment ratio and adult literacy

◦ Health & nutrition: % of undernourished population and under-5 mortality rate

Threshold for graduation: 10% above the inclusion threshold of 60 (3rd quartile of ref. group)

3. Economic Vulnerability Index (EVI) ◦ Exposure: population size, location, economic structure, environment

◦ Shock: trade (instability of exports); and natural (victims of natural disasters; instability of agri.)

Threshold for graduation: 10% below the inclusion threshold of 36 (1st quartile of ref. group)

Graduands

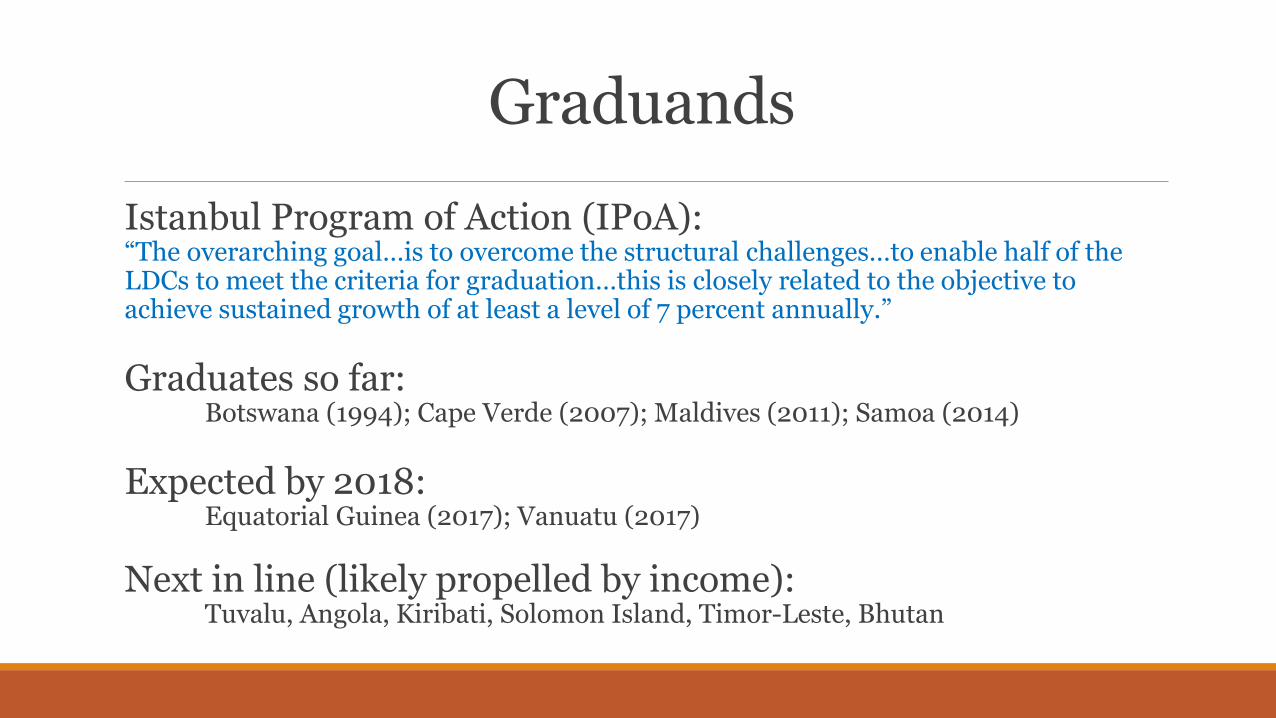

Istanbul Program of Action (IPoA): “The overarching goal…is to overcome the structural challenges…to enable half of the LDCs to meet the criteria for graduation…this is closely related to the objective to achieve sustained growth of at least a level of 7 percent annually.”

Graduates so far: Botswana (1994); Cape Verde (2007); Maldives (2011); Samoa (2014)

Expected by 2018: Equatorial Guinea (2017); Vanuatu (2017)

Next in line (likely propelled by income): Tuvalu, Angola, Kiribati, Solomon Island, Timor-Leste, Bhutan

Where does Nepal stand?

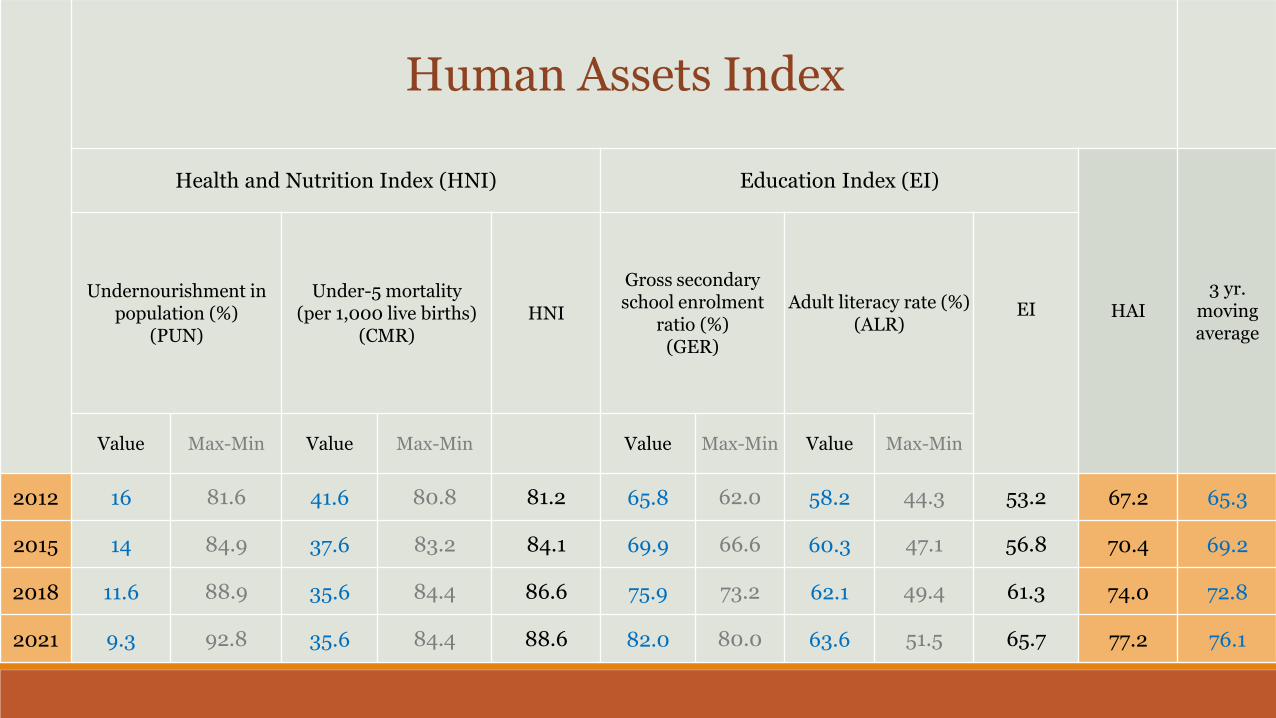

Human Assets Index

Health and Nutrition Index (HNI) Education Index (EI)

HAI 3 yr.

moving average

Undernourishment in population (%)

(PUN)

Under-5 mortality (per 1,000 live births)

(CMR) HNI

Gross secondary school enrolment

ratio (%) (GER)

Adult literacy rate (%) (ALR)

EI

Value Max-Min Value Max-Min Value Max-Min Value Max-Min

2012 16 81.6 41.6 80.8 81.2 65.8 62.0 58.2 44.3 53.2 67.2 65.3

2015 14 84.9 37.6 83.2 84.1 69.9 66.6 60.3 47.1 56.8 70.4 69.2

2018 11.6 88.9 35.6 84.4 86.6 75.9 73.2 62.1 49.4 61.3 74.0 72.8

2021 9.3 92.8 35.6 84.4 88.6 82.0 80.0 63.6 51.5 65.7 77.2 76.1

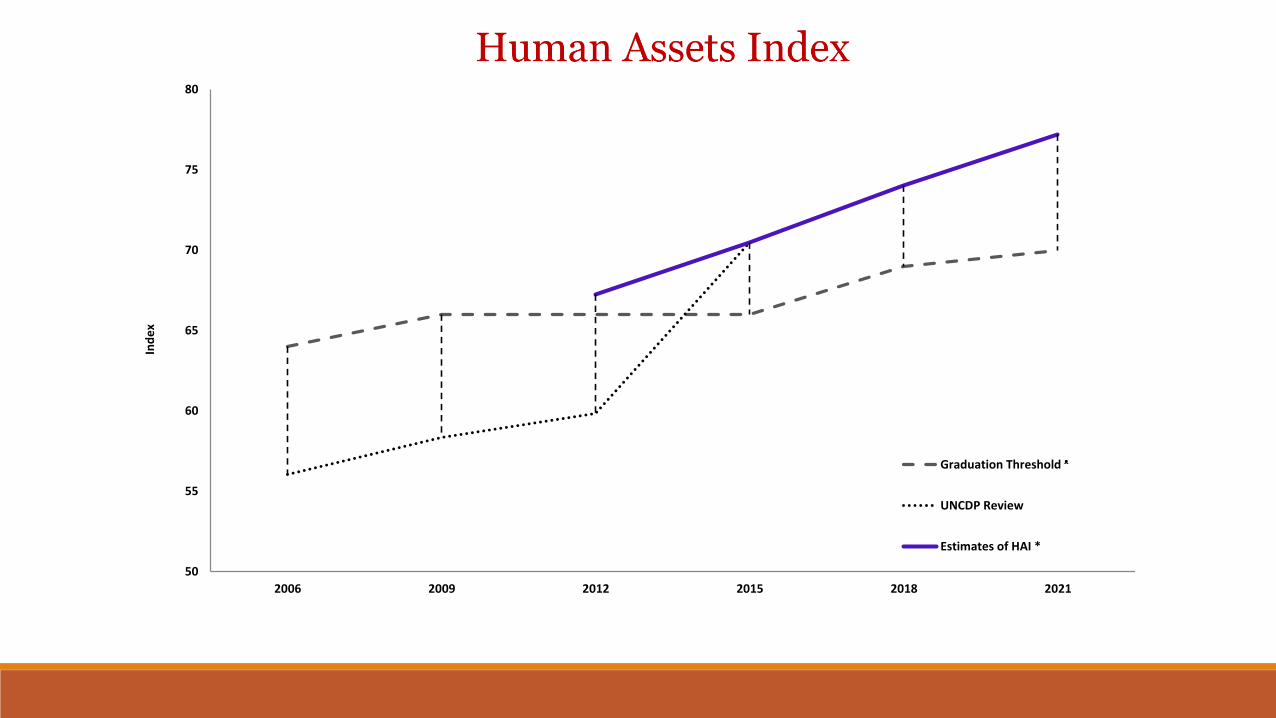

50

55

60

65

70

75

80

2006 2009 2012 2015 2018 2021

Ind

ex

Graduation Threshold ᵜ

UNCDP Review

Estimates of HAI *

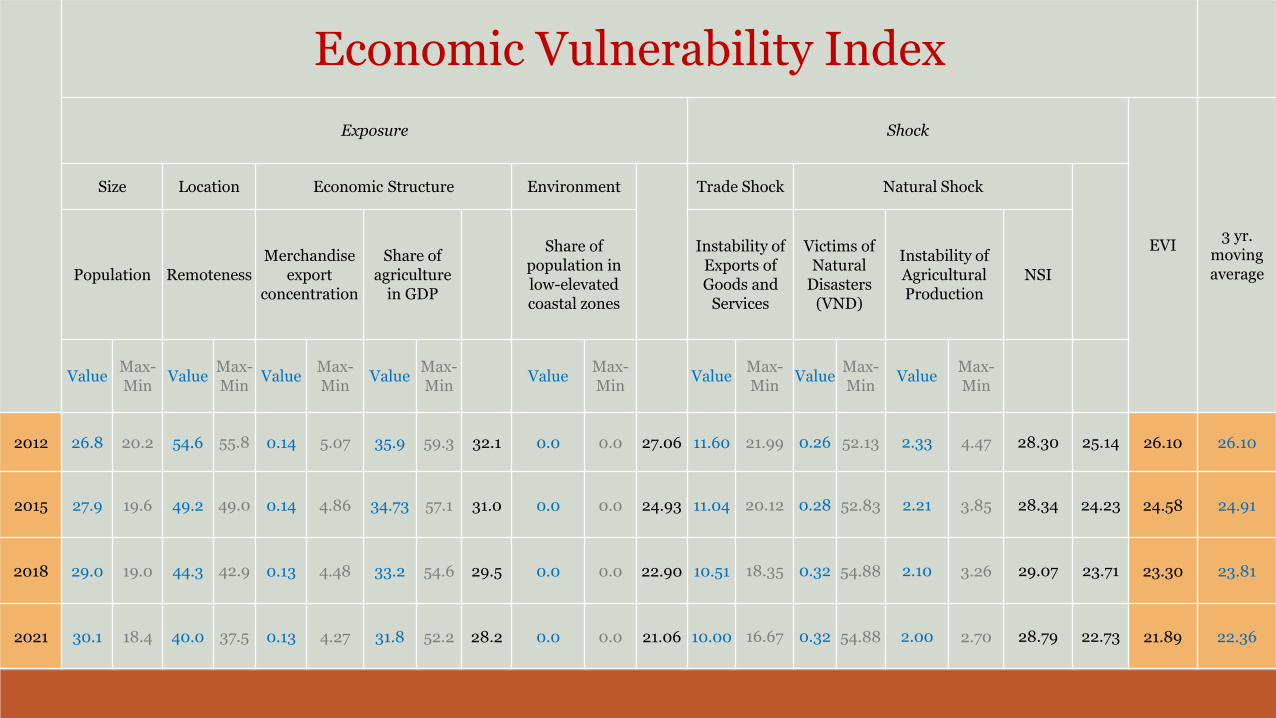

Economic Vulnerability Index

Exposure Shock

EVI

3 yr. moving average

Size Location Economic Structure Environment Trade Shock Natural Shock

Population Remoteness Merchandise

export concentration

Share of agriculture

in GDP

Share of population in low-elevated coastal zones

Instability of Exports of Goods and

Services

Victims of Natural

Disasters (VND)

Instability of Agricultural Production

NSI

Value Max-Min

Value Max-Min

Value Max-Min

Value Max-Min

Value Max-Min

Value Max-Min

Value Max-Min

Value Max-Min

2012 26.8 20.2 54.6 55.8 0.14 5.07 35.9 59.3 32.1 0.0 0.0 27.06 11.60 21.99 0.26 52.13 2.33 4.47 28.30 25.14 26.10 26.10

2015 27.9 19.6 49.2 49.0 0.14 4.86 34.73 57.1 31.0 0.0 0.0 24.93 11.04 20.12 0.28 52.83 2.21 3.85 28.34 24.23 24.58 24.91

2018 29.0 19.0 44.3 42.9 0.13 4.48 33.2 54.6 29.5 0.0 0.0 22.90 10.51 18.35 0.32 54.88 2.10 3.26 29.07 23.71 23.30 23.81

2021 30.1 18.4 40.0 37.5 0.13 4.27 31.8 52.2 28.2 0.0 0.0 21.06 10.00 16.67 0.32 54.88 2.00 2.70 28.79 22.73 21.89 22.36

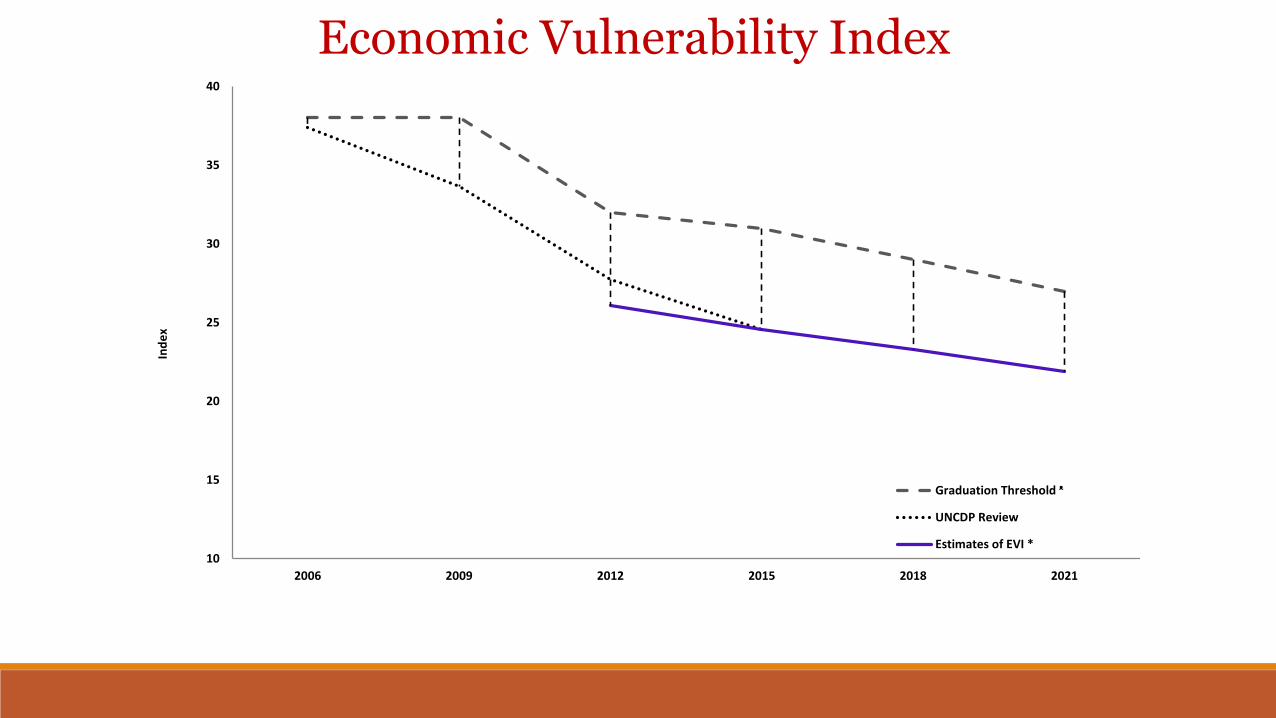

10

15

20

25

30

35

40

2006 2009 2012 2015 2018 2021

Ind

ex

Economic Vulnerability Index

Graduation Threshold ᵜ

UNCDP Review

Estimates of EVI *

0

500

1000

1500

2000

2500

2006 2009 2012 2015 2018 2021 2022

US$

GNI per capita

Graduation Threshold ᵜ UNCDP Review

Estimates of GNI per capita* GNI per capita for each Year

0

5000

10000

15000

20000

25000

30000

177

5

178

5

179

5

180

5

1815

182

5

183

5

184

5

185

5

186

5

187

5

188

5

189

5

190

5

1915

192

5

193

5

194

5

195

5

196

5

197

5

198

5

199

5

20

05

20

15

Nepal USA South Korea Malaysia

India China Japan Argentina

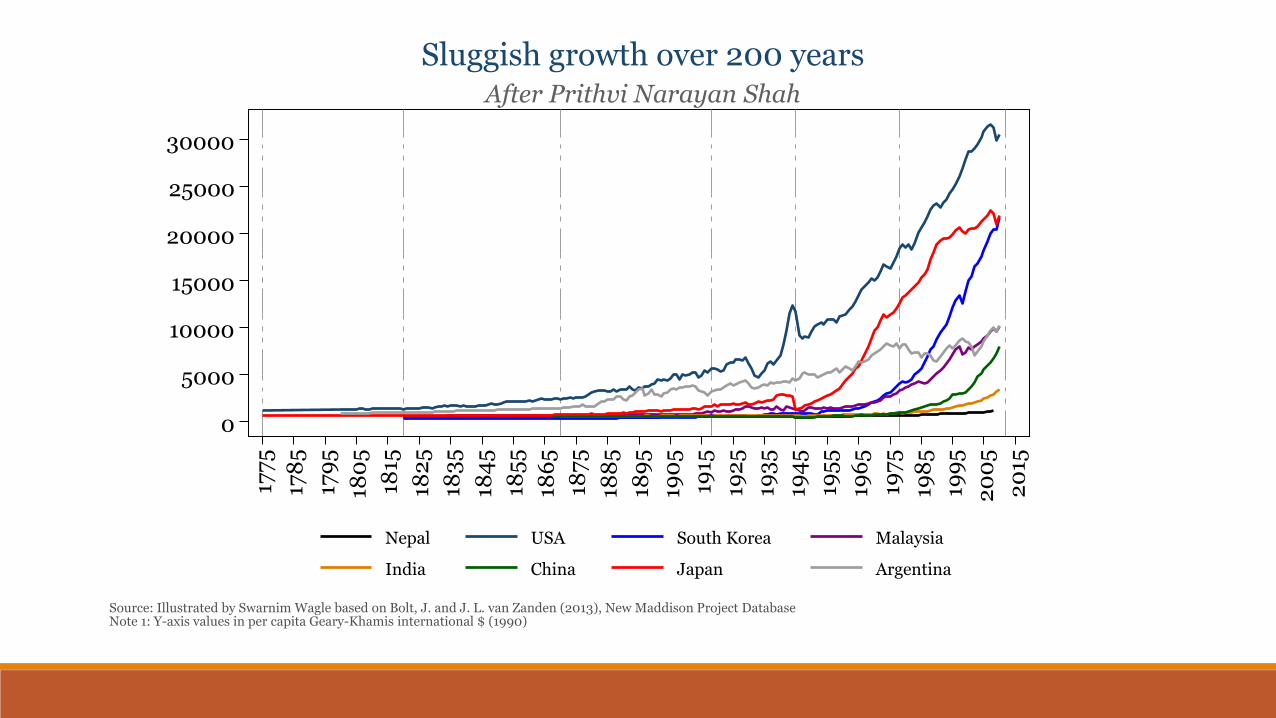

Source: Illustrated by Swarnim Wagle based on Bolt, J. and J. L. van Zanden (2013), New Maddison Project Database Note 1: Y-axis values in per capita Geary-Khamis international $ (1990)

After Prithvi Narayan Shah

Sluggish growth over 200 years

The Path Ahead

Augmenting human capabilities

Efficacy of budgetary allocation in education and health

Evidence-driven management of systems and professionals ◦ Low attendance and absenteeism

◦ Matching of inputs (medicine, textbook) with other (performance) incentives

◦ Teaching at the right level

Enforcing accountability; widening access; and coordinating better

Well-regulated private initiatives, including PPP

The imperative of sustained high growth

Massive investments esp. in clean energy, transport and other infrastructure that constrain growth

Enhanced productive capacities; revival of manufacturing; niche agriculture and modern tradable services (including tourism)

Regional growth poles in India and China; global value chains

Youth bulge and the remittance economy

“At a time of our choosing”

Mainstream and pursue the three pillars for graduation

◦ Graduation Strategy, Periodic Plans, NHDRs

Engage in CDP review of eligibility in 2015, 2018

◦ Take the parliament on board

◦ Prepare vulnerability profile and impact assessments

◦ Work on a smooth transition strategy

Meet technical criteria -- but not seek to graduate formally? ◦ Income base ought to be much stronger; and

◦ Implications for aid, market access, S&DT and international obligations clearer

The End