24

Europe’s View Of China -- A Triangular One Comments By J. Paul Horne Independent International Market Economist To Global Interdependence Center Philadelphia, 9 November 2005

| Date post: | 08-Mar-2016 |

| Category: |

Documents |

| Upload: | global-interdependence-center |

| View: | 231 times |

| Download: | 1 times |

Europe’s View Of China -- A Triangular One

Comments By

J. Paul HorneIndependent International Market Economist

To

Global Interdependence CenterPhiladelphia, 9 November 2005

2

China is for Europe aTriangular not Bilateral Problem

• Most Chinese-EU issues involve key U.S. interests and reactions

• Arms, trade, out-sourcing, energy supplies, capital flows, interest rates, FX – have vital implications for all 3

• EU defense, fiscal, labor, social policies increasing influenced by China

• EU’s own problems make dealing with CH difficult, and often earns US enmity

3

Europe … the “Old World”

4

EU’s Medium-Term Challenges• Economic growth of

1.5% to 2.% to 2007• UR stabilizes at 9%• EUR deficit = 3.2%• EUR slips vs USD• Biz confidence up if

Merkel produces• EU budget squabbles• Trade protectionism

sentiment rises

• No new constitution until French vote 07

• Accession talk delay• EU process slows• Politics move right• Anti-immigrant trend

worsens• Disputes with U.S.

grow in number, tone

5

EU vs. Global Economy• EU-25 economy out of “synch” :

–Limited business opportunities, labor constraints, low Rate Of Return on capital =

–FDI outflow to U.S., China developing world = EUR appreciation = slows export growth–EU is No. 1 U.S. trade - investment partner–China-India labor force direct threat to EU = EU policy makers get more protectionist–EU-15 Geezer Land but immigrants unwelcome

6

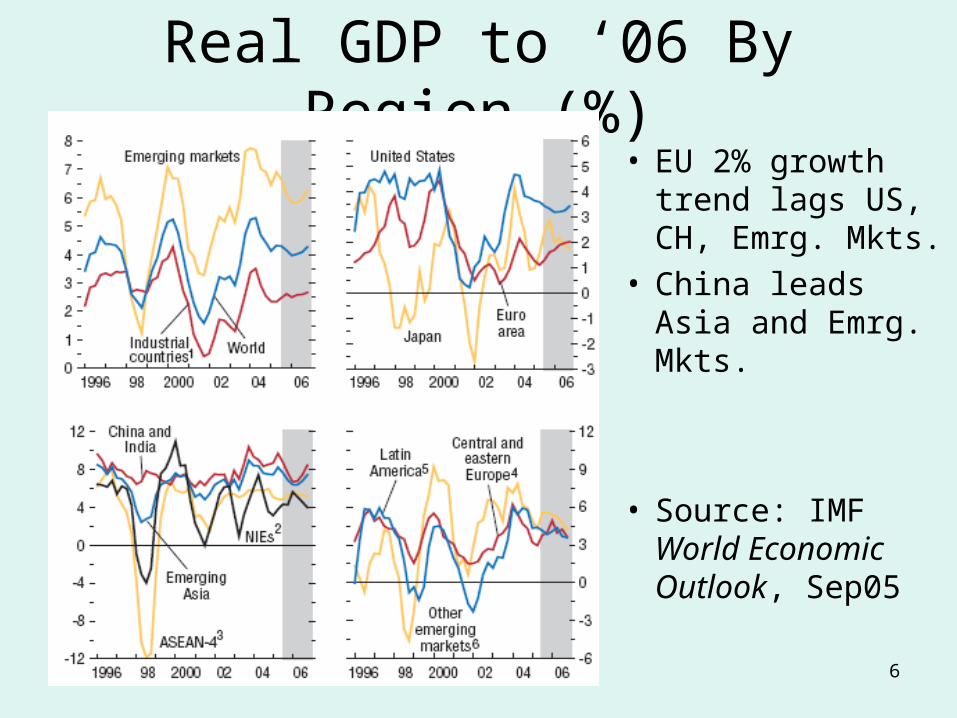

Real GDP to ‘06 By Region (%)• EU 2% growth

trend lags US, CH, Emrg. Mkts.

• China leads Asia and Emrg. Mkts.

• Source: IMF World Economic Outlook, Sep05

7

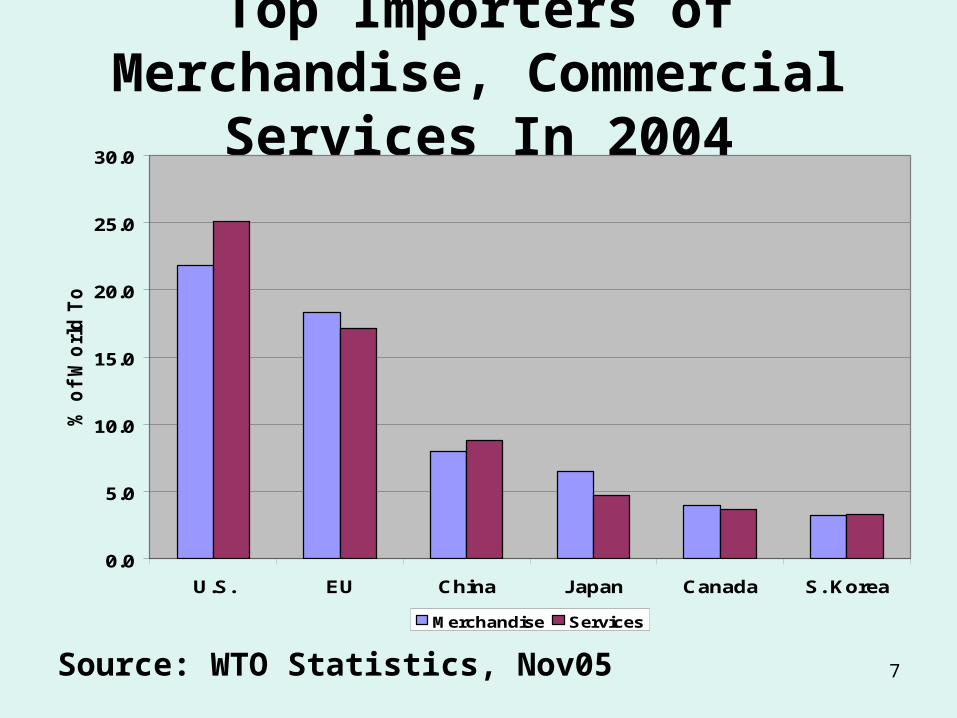

Top Importers of Merchandise, Commercial Services In 2004

Source: WTO Statistics, Nov05

0.0

5.0

10.0

15.0

20.0

25.0

30.0

U.S. EU China Japan Canada S. Korea

% o

f Wor

ld T

otal

Merchandise Services

8

EU-25’s Principal Trading Partners(USD bn in 2004)

• Source: Eurostat, Oct05

0

100

200

300

400

500

600

U.S. China (ex-HK)

Russia Japan Switzerland

Expts.

Impts.

9

Europe’s Competitors For Oil

• Source: The Economist, 27aug05

10

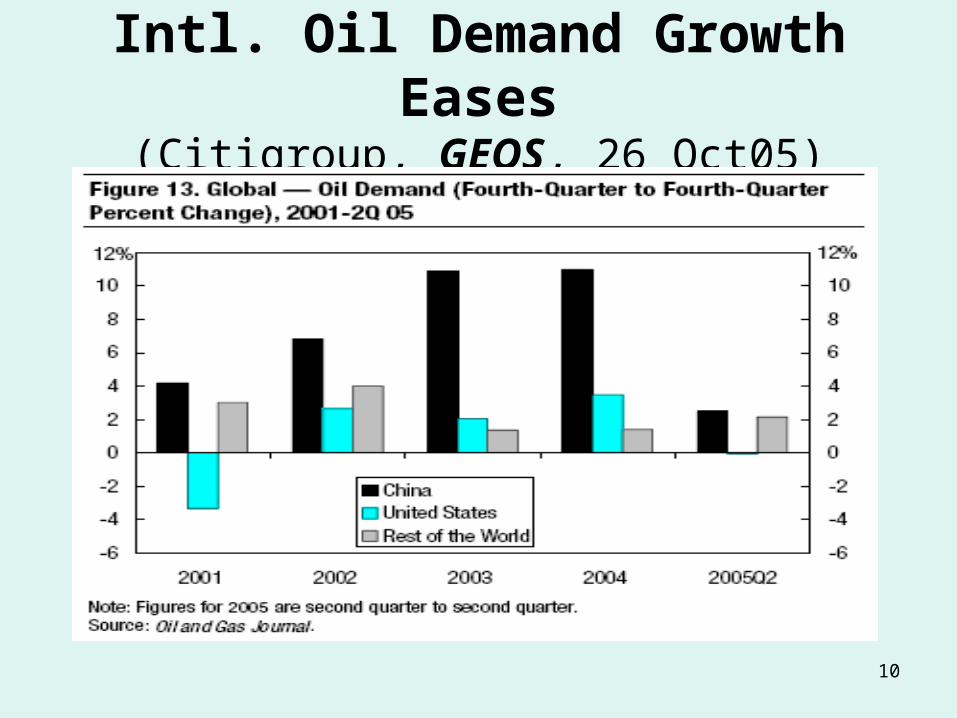

Intl. Oil Demand Growth Eases(Citigroup, GEOS, 26 Oct05)

11

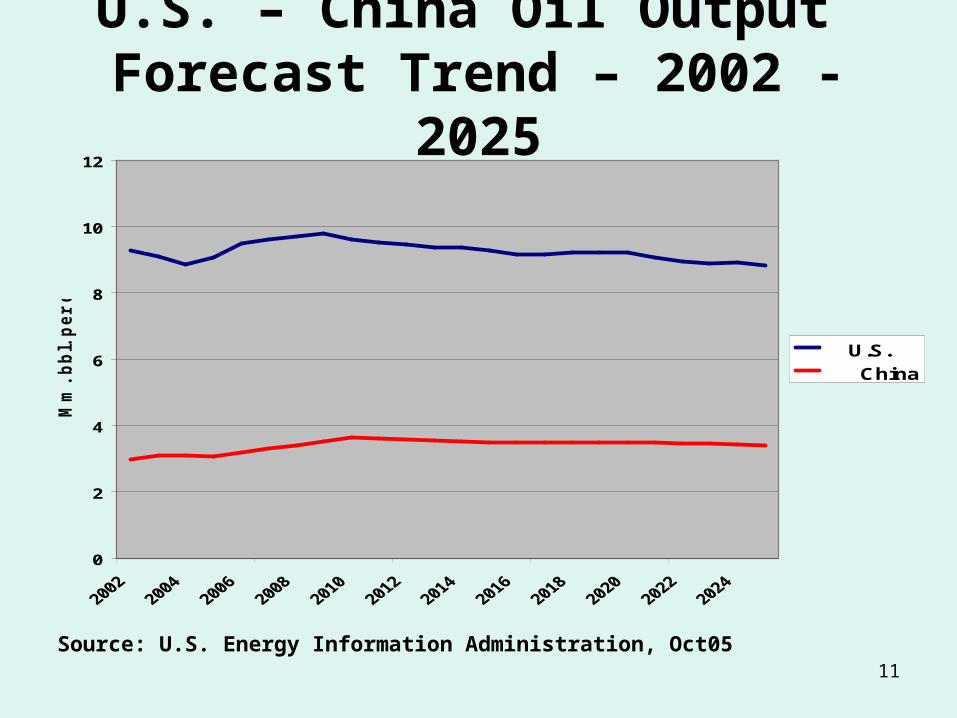

U.S. – China Oil Output Forecast Trend – 2002 - 2025

Source: U.S. Energy Information Administration, Oct05

0

2

4

6

8

10

12

Mm

. bbl

. per

day

U.S. China

12

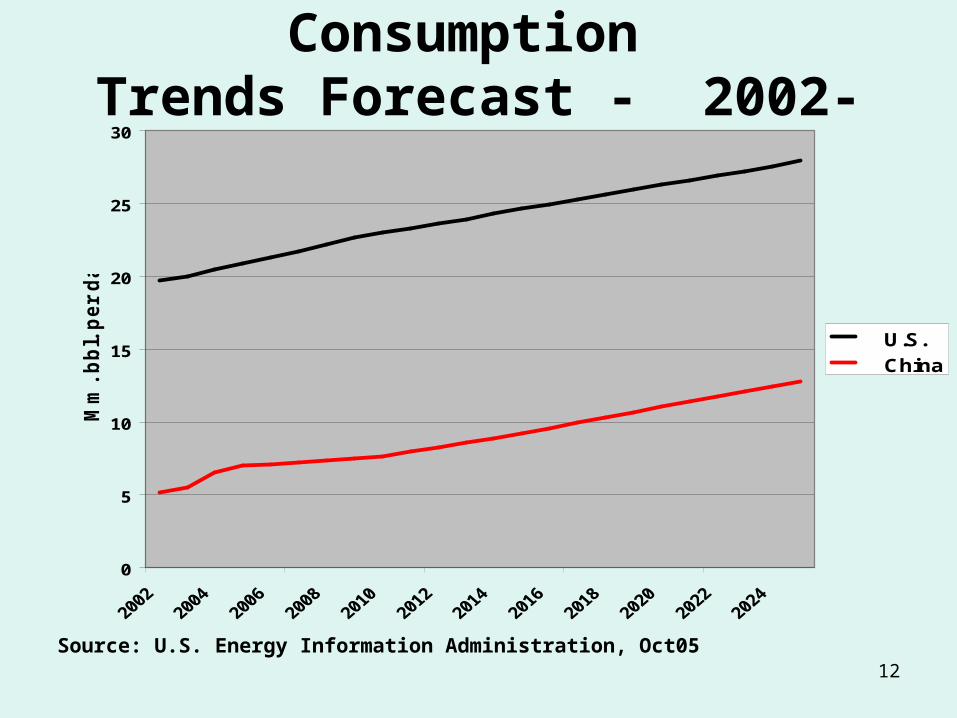

U.S. – China Oil Consumption Trends Forecast - 2002- 2025

Source: U.S. Energy Information Administration, Oct05

0

5

10

15

20

25

30

Mm

. bbl

. per

day

U.S. China

13

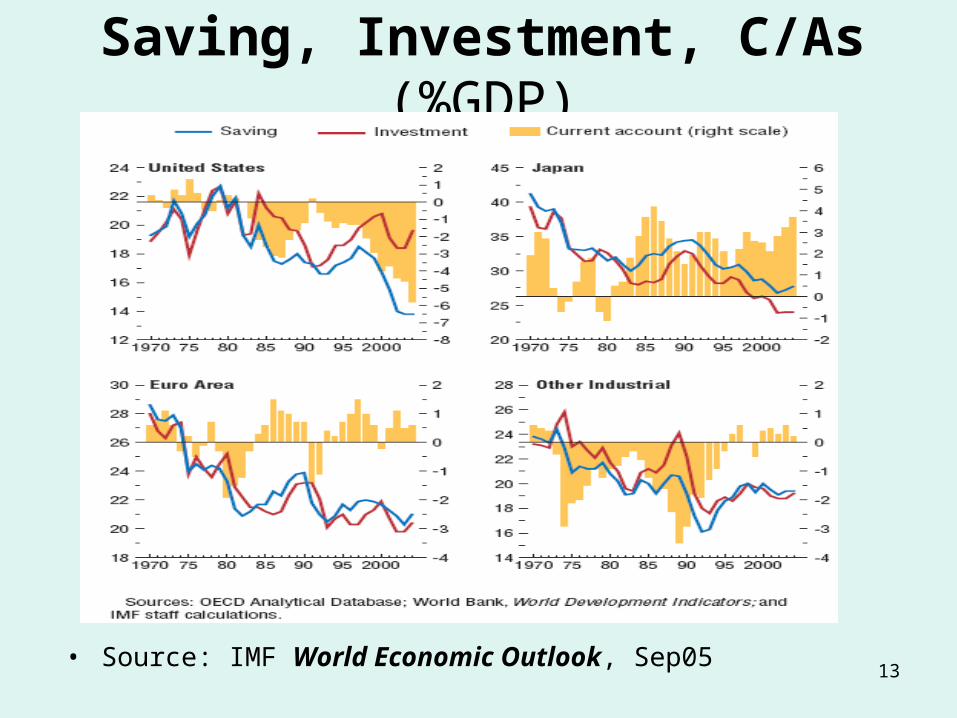

Saving, Investment, C/As (%GDP)

• Source: IMF World Economic Outlook, Sep05

14

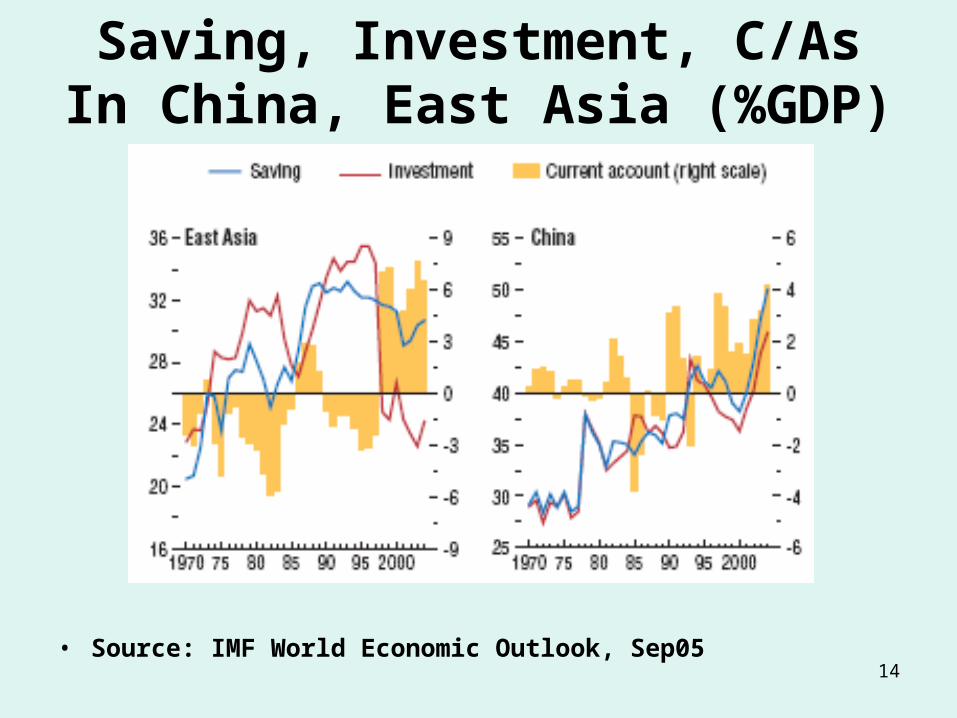

Saving, Investment, C/As In China, East Asia (%GDP)

• Source: IMF World Economic Outlook, Sep05

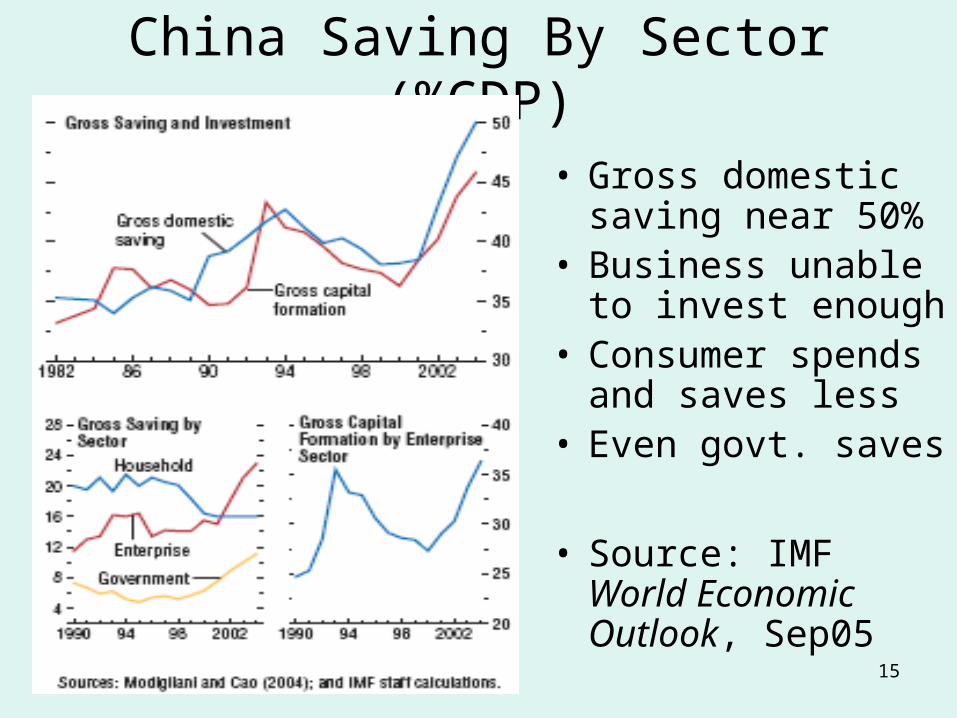

15

China Saving By Sector (%GDP)

• Gross domestic saving near 50%

• Business unable to invest enough

• Consumer spends and saves less

• Even govt. saves

• Source: IMF World Economic Outlook, Sep05

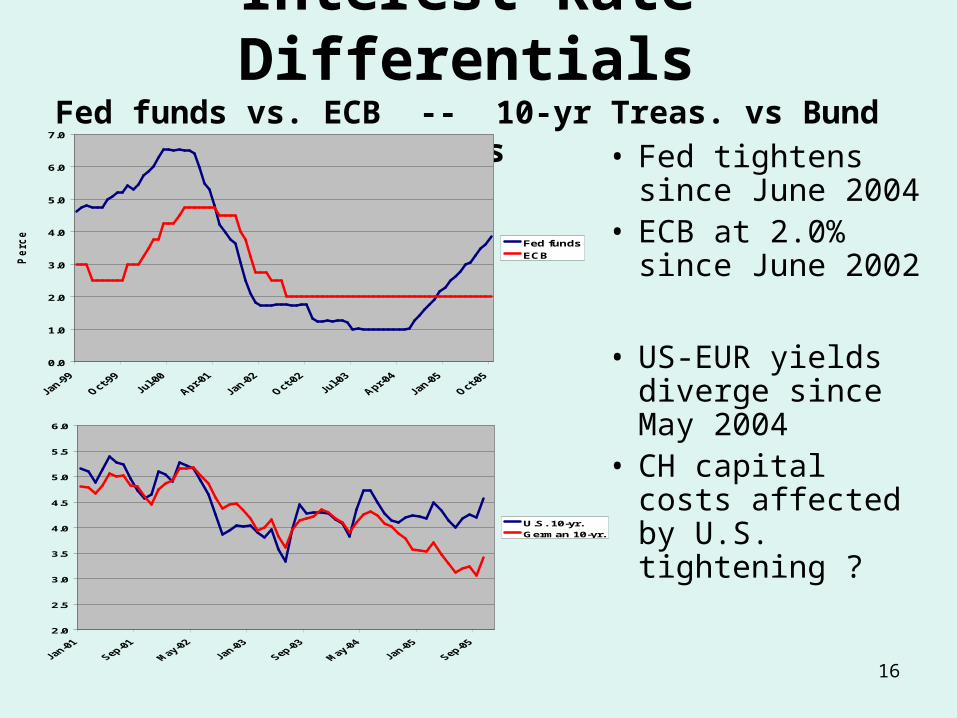

16

Interest Rate DifferentialsFed funds vs. ECB -- 10-yr Treas. vs Bund Ylds

• Fed tightens since June 2004

• ECB at 2.0% since June 2002

• US-EUR yields diverge since May 2004

• CH capital costs affected by U.S. tightening ?

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Perc

ent

Fed fundsECB

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

U.S. 10-yr.German 10-yr.

17

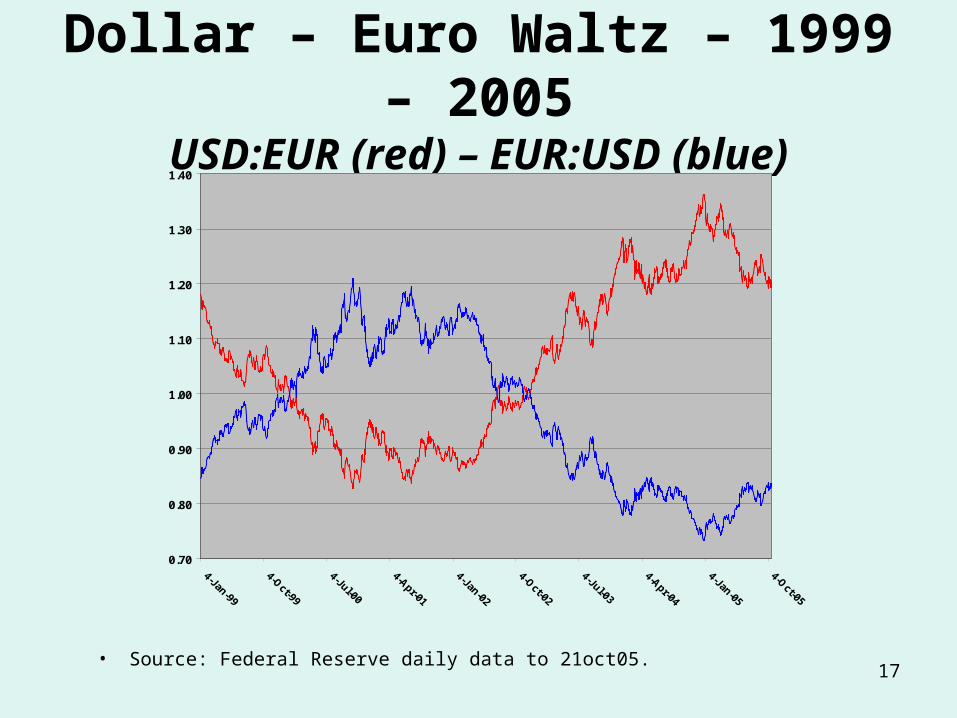

Dollar – Euro Waltz – 1999 – 2005USD:EUR (red) – EUR:USD (blue)

• Source: Federal Reserve daily data to 21oct05.

0.70

0.80

0.90

1.00

1.10

1.20

1.30

1.40

18

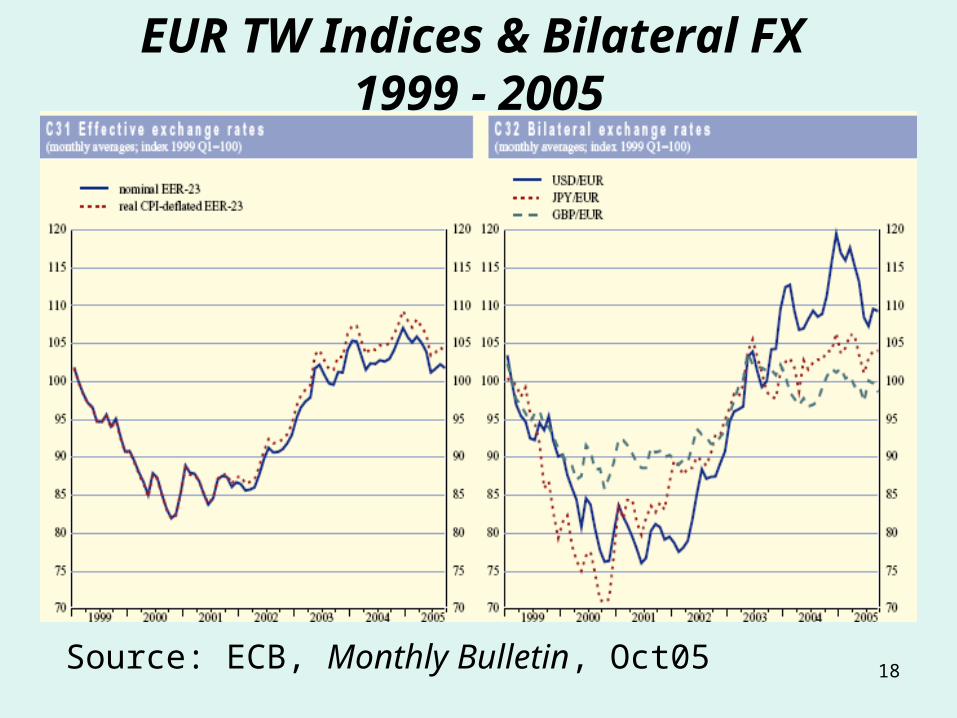

EUR TW Indices & Bilateral FX 1999 - 2005

Source: ECB, Monthly Bulletin, Oct05

19

As long as they focus on each other…

• Source: Financial Times, 28sep05

20

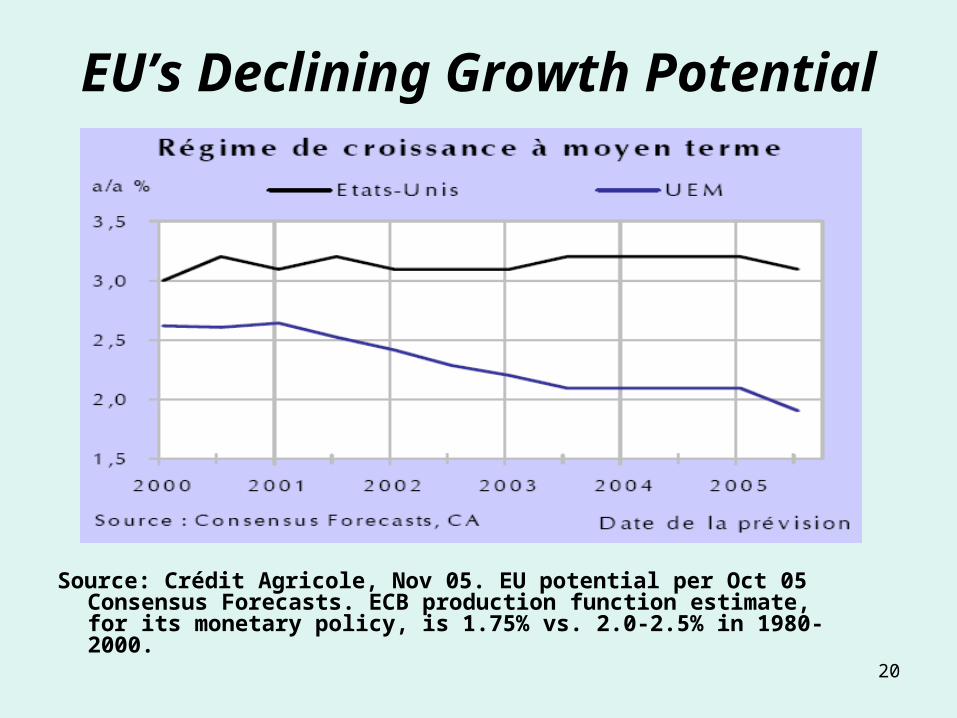

EU’s Declining Growth Potential

Source: Crédit Agricole, Nov 05. EU potential per Oct 05 Consensus Forecasts. ECB production function estimate, for its monetary policy, is 1.75% vs. 2.0-2.5% in 1980-2000.

21

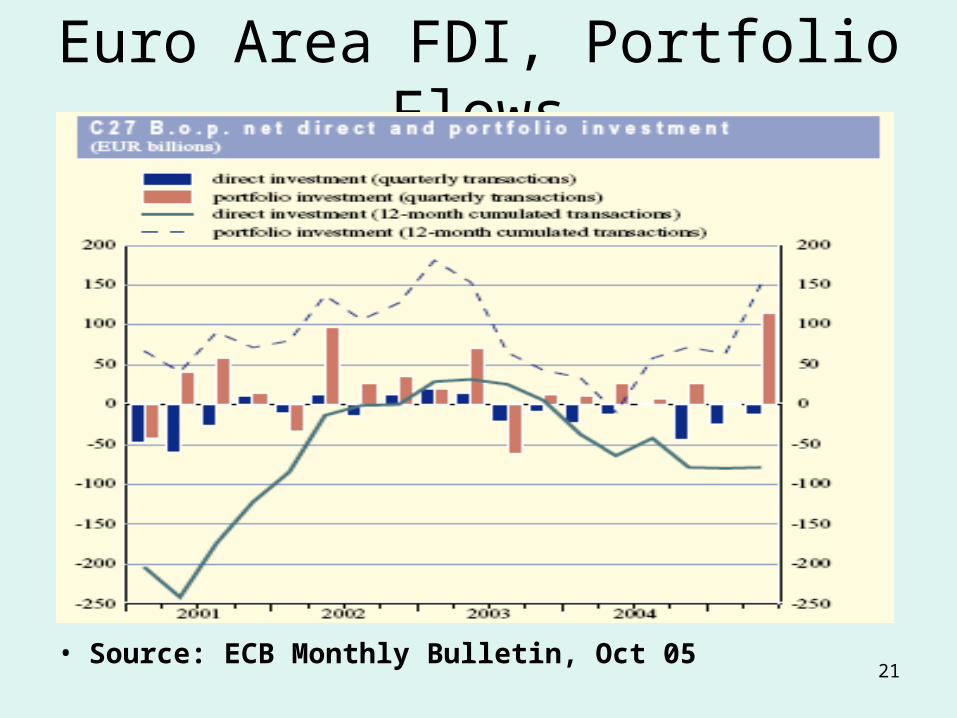

Euro Area FDI, Portfolio Flows

• Source: ECB Monthly Bulletin, Oct 05

22

Current EU – CH Issues:• Trade (textiles, arms), capital flows and FX• Energy & metal supplies – CH competes• World labor force with China + India =

structural changes forced on Europe• China lowers EU prices = disinflationary,

slowing economic and job growth• FDI: CH may rival US as future pot of gold• Security issues: arm sales vs. cordon

23

Special EU – US - CH Issues• H5N1 – do CH farmers get paid to cull ?• Counterfeiting = patents, copyrights ?• Corporate, tax and property law ?• Human rights … for 1.4 billion ?• Environmental issues … for everybody ?• Demography – EU grays, US ages, CH ? • China’s competitors tomorrow : India,

Burma and … TN ?

24

Do Euro-Leaders have a clue ?

• Source: Internet, late 2004