15

Pearson LCCI Certificate in Bookkeeping (VRQ) Level 1 (ASE20091) Examiners’ Report November 2016 LCCI Bookkeeping ASE20091 1

Pearson LCCI Certificate in Bookkeeping (VRQ) Level 1 (ASE20091)

Examiners’ Report November 2016

LCCI Bookkeeping ASE20091 1

LCCI Qualifications LCCI qualifications come from Pearson, the world’s leading learning company. We provide a wide range of qualifications including academic, vocational, occupational and specific programmes for employers. For further information, please visit our website at www.lcci.org.uk. Pearson: helping people progress, everywhere Pearson aspires to be the world’s leading learning company. Our aim is to help everyone progress in their lives through education. We believe in every kind of learning, for all kinds of people, wherever they are in the world. We’ve been involved in education for over 150 years, and by working across 70 countries, in 100 languages, we have built an international reputation for our commitment to high standards and raising achievement through innovation in education. Find out more about how we can help you and your students at: www.pearson.com/uk. November 2016 Publication code: 51699_ER All the material in this publication is copyright © Pearson Education Ltd 2016

2 LCCI Bookkeeping ASE20091

Introduction Pearson (LCCI) redeveloped the new specification at Level 1 Certificate in Bookkeeping (VRQ) (ASE20091) in January 2015 as a part of Finance and Quantitative suite of qualifications from Level 1 to Level 4 and assessed first time in November 2015.The purpose of this qualification is to give candidates the essential skills and knowledge of double entry book-keeping. The assessment is of 100 marks comprising of a total of 5 questions. All the questions are compulsory. This assessment covered these topics:

• Preparation of the purchases day book. • Books of original entry. • Double entry bookkeeping. • Updating of the cash book. • Preparation of a bank reconciliation statement. • Preparation of a trial balance from given balances. • Preparation of an income statement for a sole trader. • Identification of errors that do not affect the trial balance. • Preparation of the Journal to correct errors. • Calculation of depreciation and carrying value. • Calculation of net pay and methods of payment.

Question 1 was a 28 mark question which required candidates to complete and total the purchases day book and then tested knowledge of the books of prime entry and the ledgers by requiring candidates to make postings to three supplier accounts, the control account and discount received account. Most candidates correctly prepared the purchases day book including the totalling. The preparation of the ledger accounts was not carried out to a high standard with many candidates losing marks due to incorrect labelling. The preparation of the discount received account was poorly answered and very few candidates were able to provide an explanation as was required for part (c). Question 2 was a 19 mark question which tested the updating of the cash book and the bank reconciliation statement. Very few candidates were able to identify possible reasons why a cheque may be returned or the differences between a standing order and direct debit. Despite the bank reconciliation being examined regularly there were very few fully correct statements produced. As well as using incorrect items candidates often labelled the statement incorrectly. Question 3 was a 23 mark question which required the preparation of the trial balance and income statement from a given list of balances. This question was answered to a high standard by nearly all candidates. There were no common errors in the trial balance and a marked improvement in this area was noted from recent sittings. Most candidates presented the income statement neatly and scored high marks although marks were lost due to the incorrect treatment of carriage in some cases.

LCCI Bookkeeping ASE20091 3

Question 4 was a 20 mark question which tested errors, journal entries and depreciation. Most candidates were able to correctly indicate the type of given error for some of the given errors but few candidates identified all three errors. The journal entries were well prepared but the required explanation of why the trial balance still balanced was poorly answered. The calculations of the depreciation charge and carrying value of the two types of non-current assets were very disappointing. Nearly all candidates failed to account for the acquisitions during the year and relatively few were able to calculate the carrying values as required. Question 5 was a 10 mark question which tested payroll aspects. Part (a) was generally well answered although many candidates failed to convert the given annual salary of Sonia to a monthly amount as was required and were penalised accordingly. The bank transfer was invariably completed correctly but few candidates were able to explain an advantage of a bank transfer over cash. Most candidates demonstrated an acceptable knowledge of a piece rate scheme.

4 LCCI Bookkeeping ASE20091

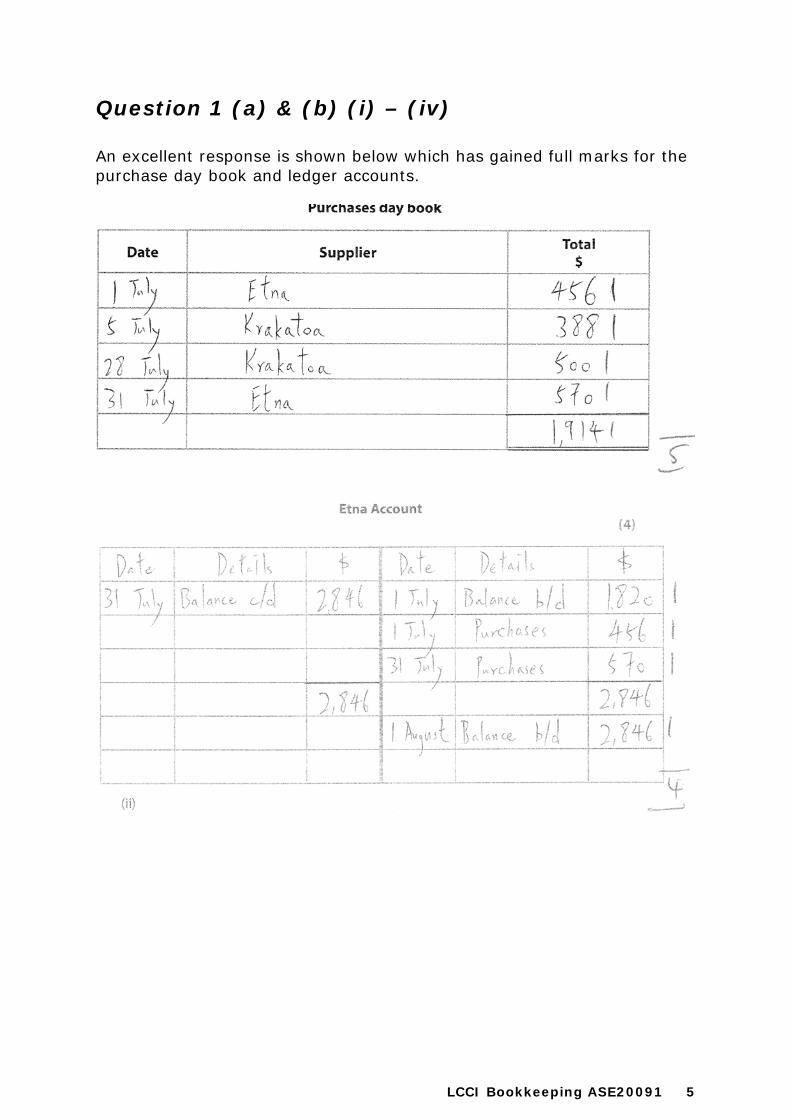

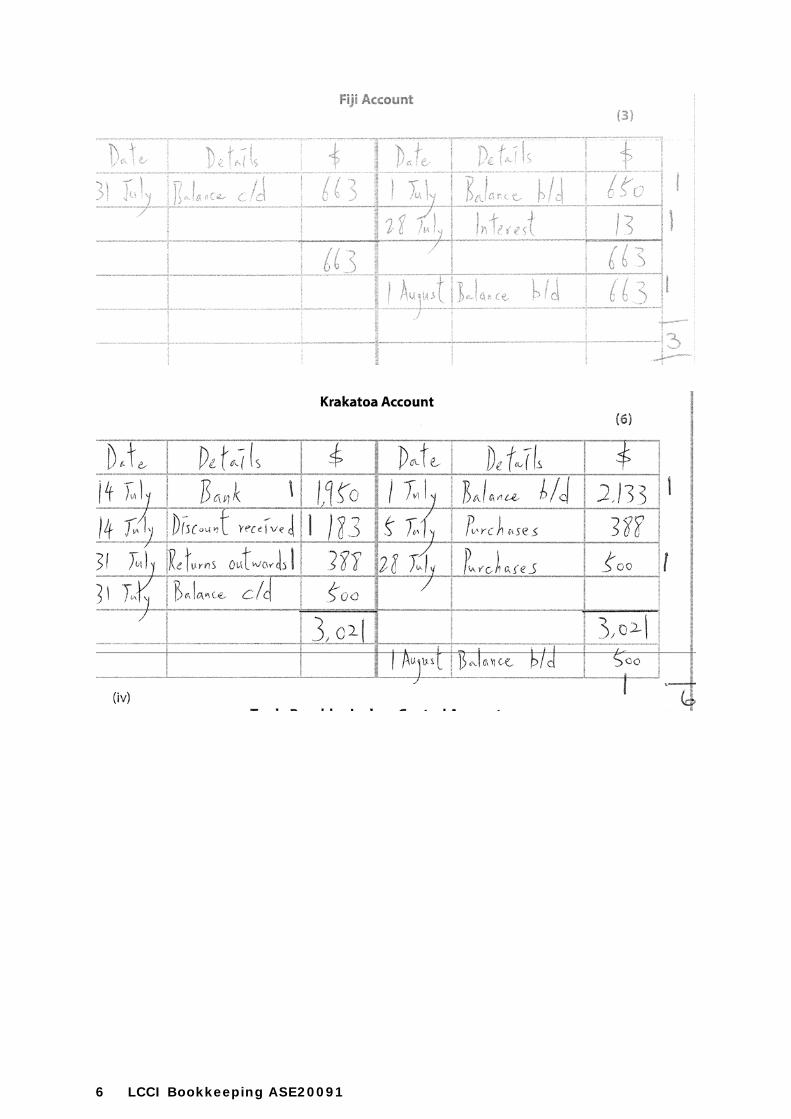

Question 1 (a) & (b) (i) – (iv) An excellent response is shown below which has gained full marks for the purchase day book and ledger accounts.

LCCI Bookkeeping ASE20091 5

6 LCCI Bookkeeping ASE20091

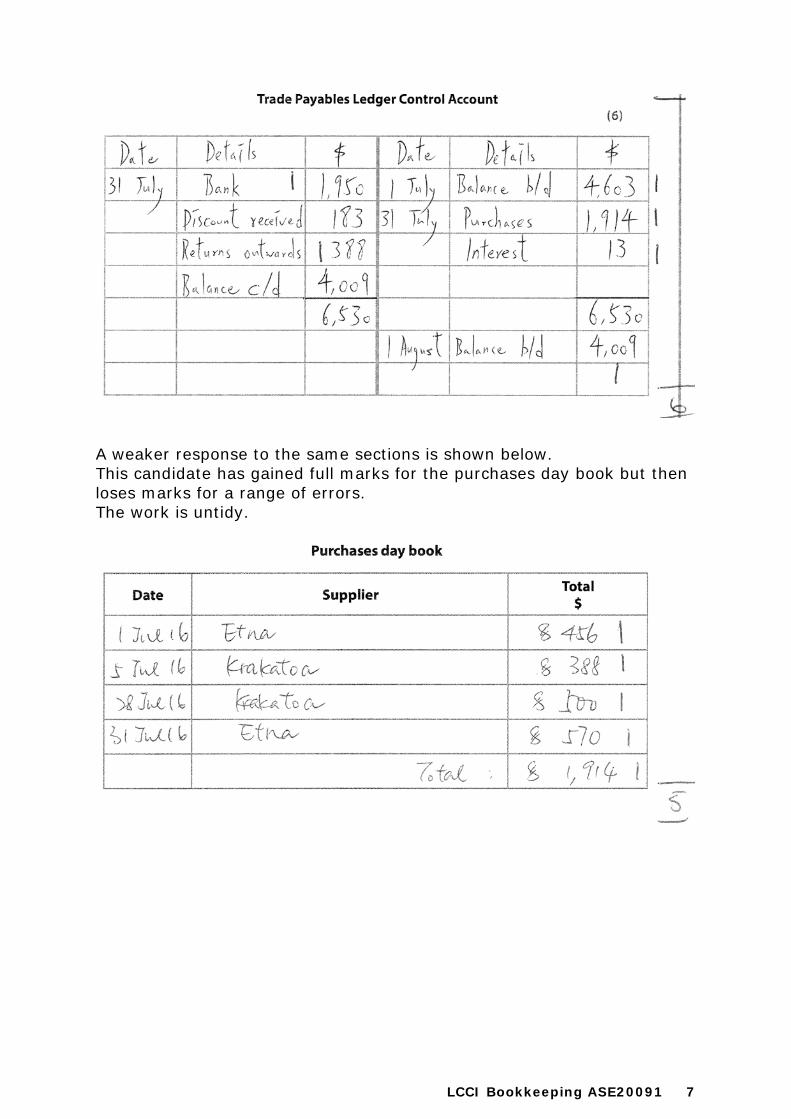

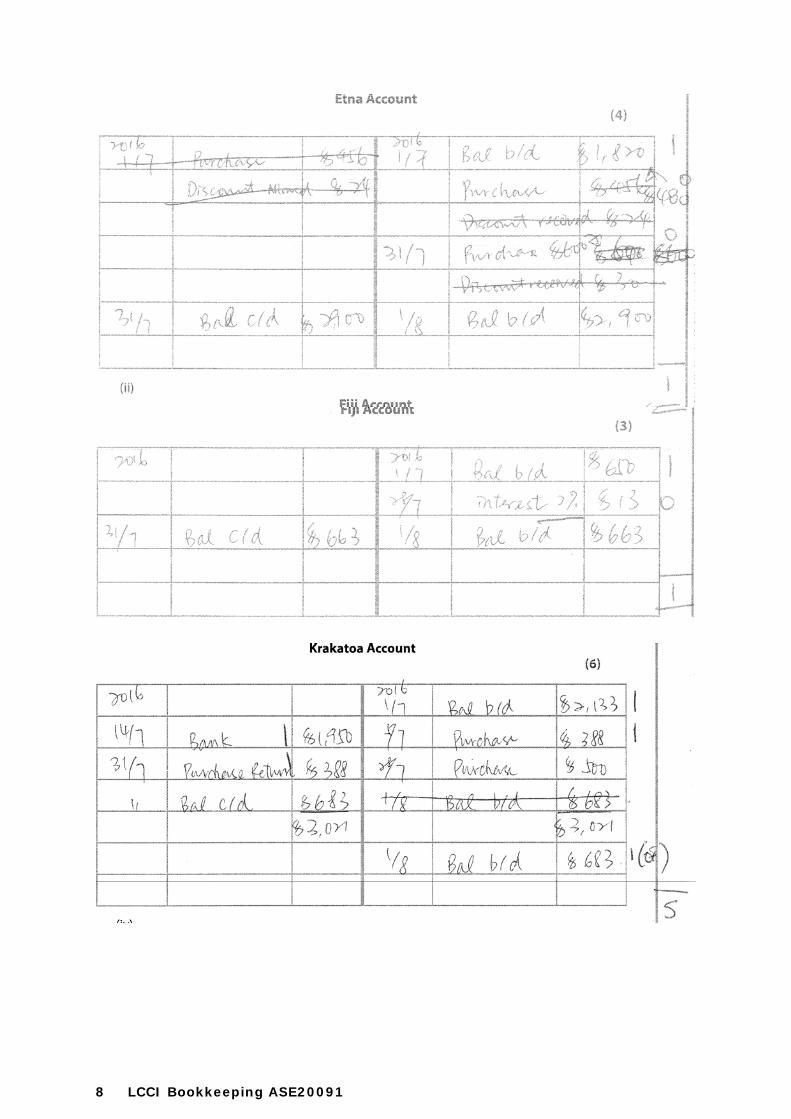

A weaker response to the same sections is shown below. This candidate has gained full marks for the purchases day book but then loses marks for a range of errors. The work is untidy.

LCCI Bookkeeping ASE20091 7

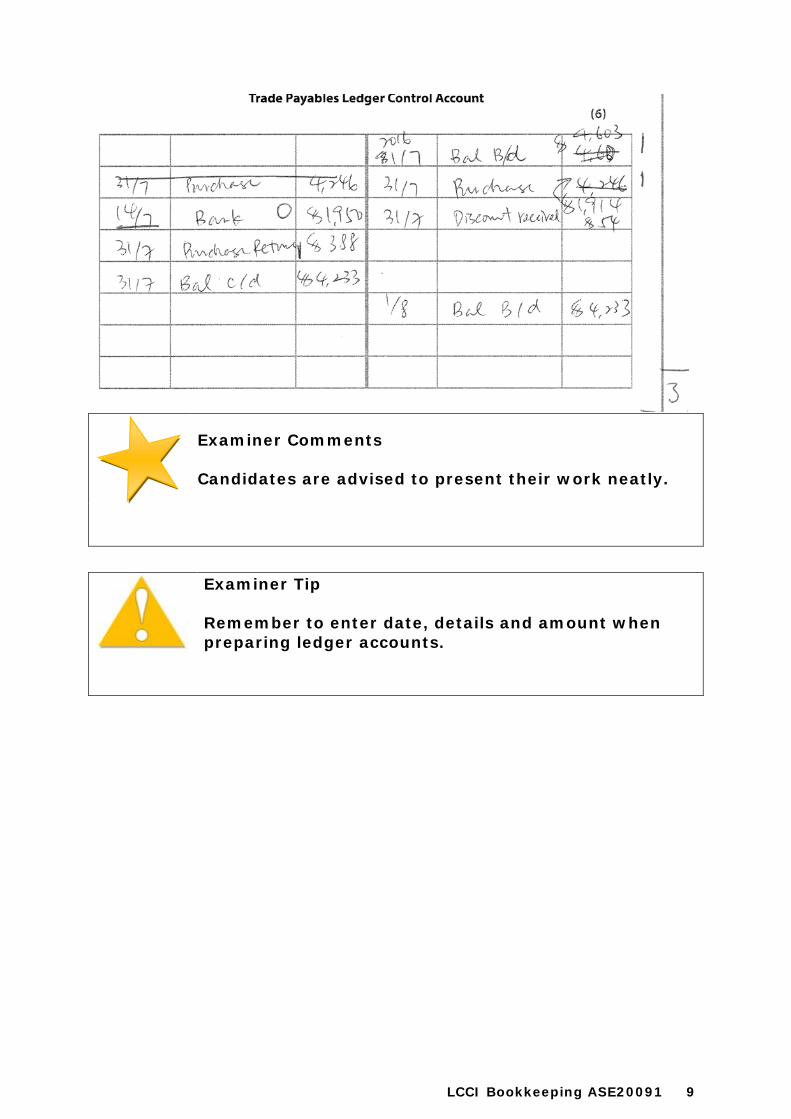

8 LCCI Bookkeeping ASE20091

Examiner Comments Candidates are advised to present their work neatly.

Examiner Tip Remember to enter date, details and amount when preparing ledger accounts.

LCCI Bookkeeping ASE20091 9

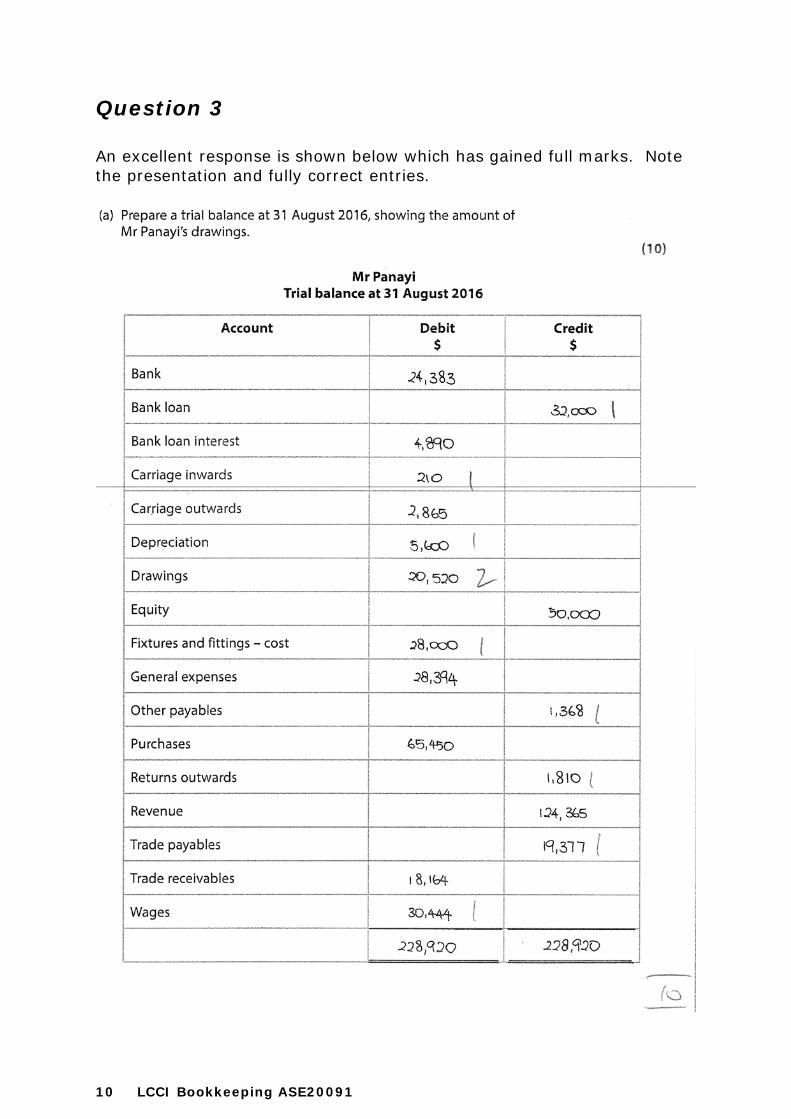

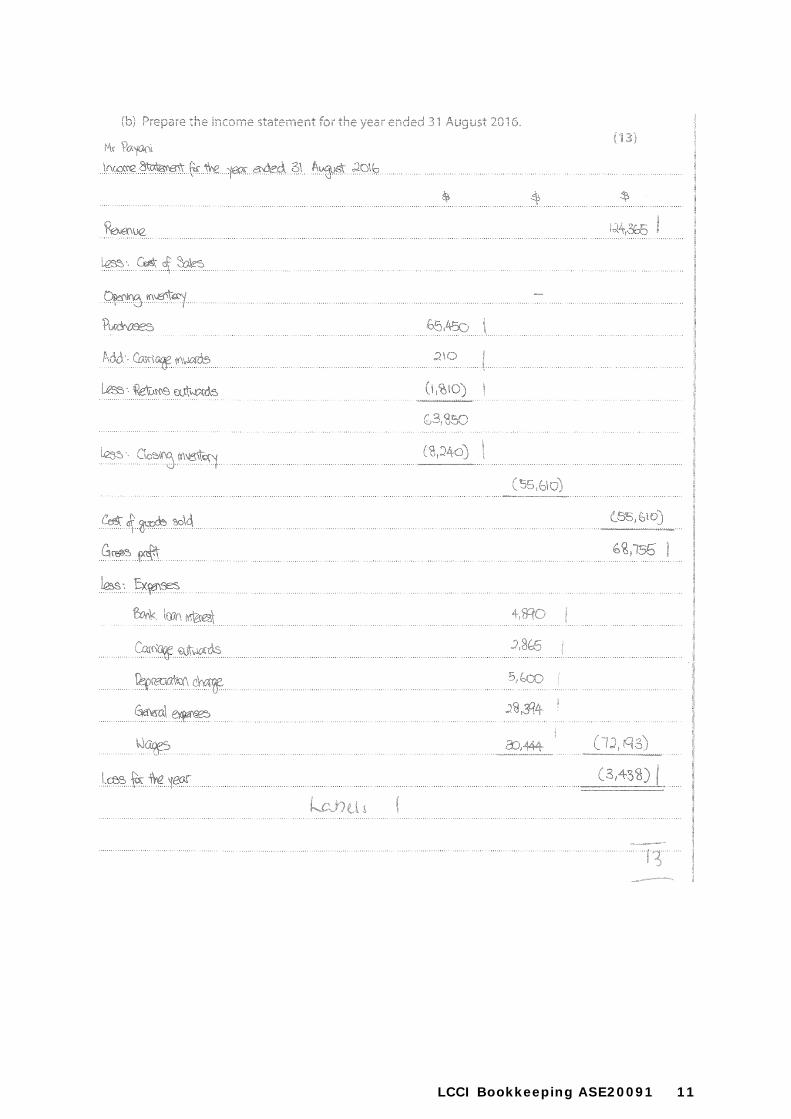

Question 3 An excellent response is shown below which has gained full marks. Note the presentation and fully correct entries.

10 LCCI Bookkeeping ASE20091

LCCI Bookkeeping ASE20091 11

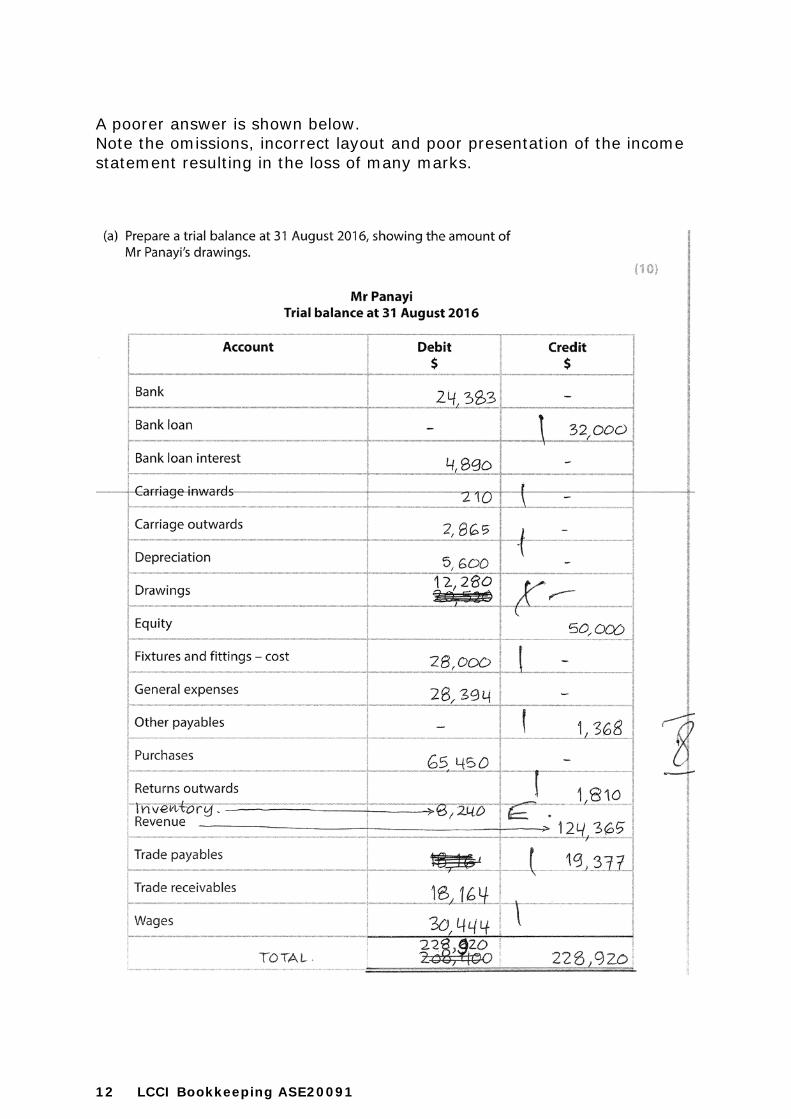

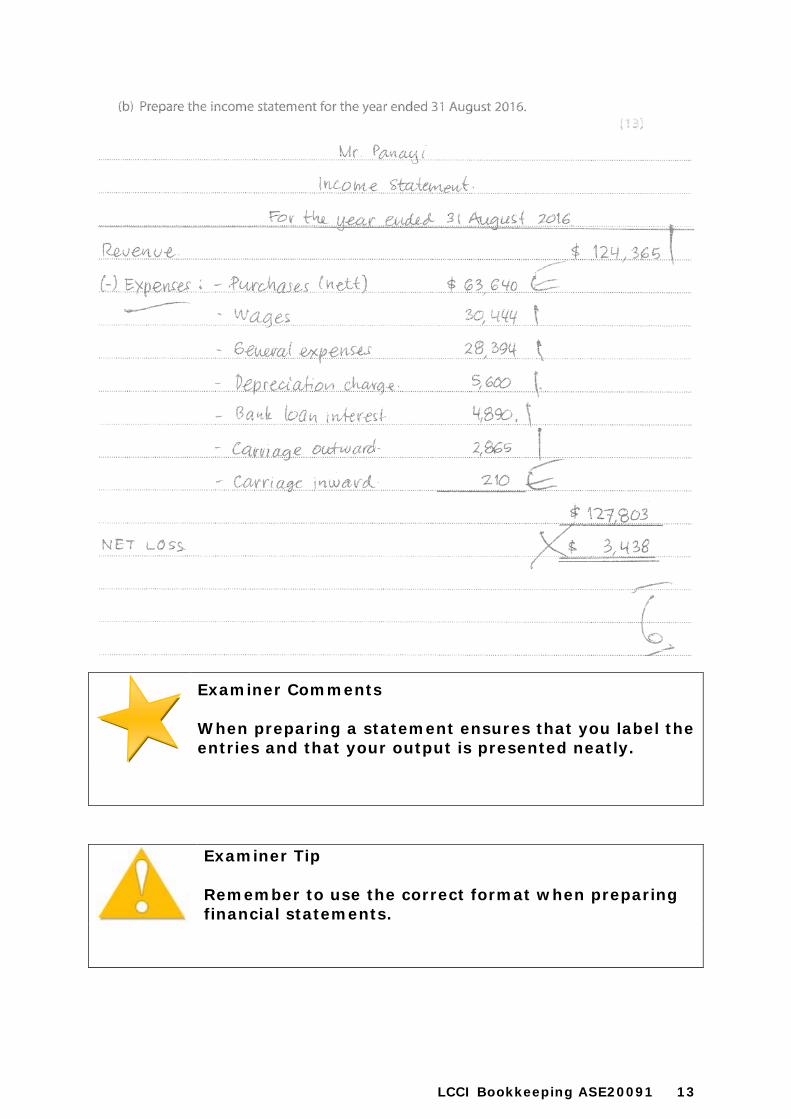

A poorer answer is shown below. Note the omissions, incorrect layout and poor presentation of the income statement resulting in the loss of many marks.

12 LCCI Bookkeeping ASE20091

Examiner Comments When preparing a statement ensures that you label the entries and that your output is presented neatly.

Examiner Tip Remember to use the correct format when preparing financial statements.

LCCI Bookkeeping ASE20091 13

Paper Summary

Candidates should:

• Ensure that they are fully prepared. • Read the paper before starting to answer. • Write neatly. • Show workings where appropriate. • Manage their time efficiently.

• Practice using selected assessment materials.

14 LCCI Bookkeeping ASE20091

Grade Boundaries Grade boundaries for this, and all other papers, can be found on the website on this link: http://qualifications.pearson.com/en/support/support-topics/results-certification/grade-boundaries.html

LCCI Bookkeeping ASE20091 15