Page 1

Singapore is one of the leading financial centers of the world and a major distribution hub of

finance in Southeast Asia. No wonder, therefore, that the country has created one of the

most advanced banking system in the world, numbering about 700 local and foreign banks

and financial institutions that provide services ranging from consumer banking and asset

management, to stock exchange, investment banking and specialized insurance services.

At the end of 2004, Singapore’s domestic banking sector consisted of assets / liabilities in

the amount of about 230 billion U.S. dollars. Singapore’s leading banks are ABN AMRO,

Citibank, DBS, HSBC, OCBC, Standard Chartered and UOB. Country’s central bank is the

Monetary Authority of Singapore (MAS), which determines monetary policy, regulates banks

and financial institutions and issues the currency. Despite the current lack of government-

sponsored deposit insurance program, MAS plans to establish such a system in the near

future.

Activities of commercial banks licensed in Singapore and is subject to the Banking Act.

Commercial banks may engage in all possible types of banking activities. In addition to

providing commercial banking services, including deposit-taking, lending and checking

operations, banks may also engage in any other kind of banking business, which is regulated

or permitted by MAS, including consulting services in finance, brokerage services in the field

of insurance and capital market placement services (Section 30 of the Banking Act describes

all the possible types of banking activities).

Commercial banks and their representatives do not necessarily need a separate license for

such activities, but must comply with the code of conduct in its business activities

prescribed in the Act on Financial Advisors (IA) and the Law on Securities and Futures Act

(SFA), respectively. In July 2001, the Banking Act was amended by prohibiting banks from

engaging in non-financial activities. Banks were provided three years, until July 2004, on

completion of their non-financial activities. In August 2003, this grace period was extended

for another two years until July 2006 for those banks which have applied to MAS to request

an extension. Currently in Singapore operate 113 commercial banks. Five of them are

registered at the local level and are owned by three local banking groups. Commercial banks

can operate as banks, providing the full range of services, wholesale banks or offshore

banks.

Banks providing a full range of services

Currently, there are 28 banks, offering the full range of services and operating under the

Banking Act in Singapore. Five of them are registered and owned by the local 3 local

banking groups, and the remaining 23 banks are branches of banks registered abroad. Six of

the 23 branches of foreign banks have the privilege to implement a full range of banking

services. Foreign banks, providing the full range of services and those who use the specified

privilege can only have 15 branches and / or ATMs of which a maximum 10 can be separated

from the branches. These banks can use ATMs in conjunction with each other and are free to

change the location of their offices. From July 1, 2002 privileged banks were allowed to

provide services through EFTPOS (electronic funds transfer)debit network, to offer additional

Page 2

pension package, to use the investment accounts (CPF Investment Scheme accounts) and

take time deposits in the investment scheme with a minimum amount of the deposit.

Wholesale banking

Wholesale banks may engage in the same banking activities that banks offering a full range

of services, except that they do not have the right to provide retail banking services in the

Singapore dollars. They operate in accordance with the Guidelines issued by MAS to work

wholesale banks. In Singapore, there are 37 wholesale banks, and all of them are

subsidiaries of foreign banks.

Offshore banks

Offshore banks have the right to engage in the same activities as banks, providing a full

range of services, as well a activities involving Asian currencies, expressed in units of Asian

currencies (ACU). Units of Asian currencies – is an accounting unit used by banks to account

for all their foreign currency transactions carried out on the Asian market. Banking

operations in Singaporean dollars are accounted separately in the domestic banking unit

(DBU). The volume of transactions carried out in the domestic banking units of offshore

banks a bit more limited in terms of transactions with residents compared with wholesale

banks. Offshore banks operate in accordance with the Guidelines issued by MAS for offshore

banks.

As a part of the liberalization of the banking activities, offshore banks were given greater

leeway in the implementation of wholesale operations with the Singaporean dollar. Limit on

loans in SGD to offshore banks was increased to 500 million now, these banks may transact

“swap” in the Singaporean dollars in relation to the proceeds from the issuance of Singapore

dollar bonds, which are run or released by banks.

In total in Singapore operate 48 offshore banks, and all of them are subsidiaries of foreign

banks.

Merchant banks

In addition to these three categories of commercial banks, there are financial institutions

that can operate as merchant banks. Merchant banks are approved by Monetary Authority in

accordance with the law, and their activity is subject to the directives of the trade banks.

Operations of these banks in terms of Asian currencies also performed in accordance with

the Banking Act. Typically, commercial banks engaged in financing of corporate entities, the

subscription to shares and bonds issued, mergers and merger of companies, investment

portfolio management, management consulting and other reimbursable activities. Most

commercial banks with the permission of MAS work with Asian currencies, through which

they compete with commercial banks in the Asian dollar market. As for DBU, then merchant

banks have no right to demand deposits, savings deposits or borrow from the public.

However, they are allowed to accept deposits or borrow from banks, finance companies,

shareholders and companies controlled by their shareholders. Total in Singapore there are

currently 52 commercial banks.

Page 3

Financial companies

Financial companies concentrate their activities on a small scale financing, including loans to

purchase cars, consumer durables, and extend loans for real estate purchase. Financial

companies are licensed and operated in accordance with the Law on financial companies.

Financial companies are not allowed to open deposit accounts, which allows to withdraw the

funds at the request of checks, promissory notes or payment request. They are not allowed

to provide unsecured loans in excess of 5,000 Singaporean dollars to any person or for any

transaction in foreign currency, gold or other precious metals or acquire shares,

denominated in foreign currencies, equity or debt securities.

However, financial companies with capital of more than 10 million Singapore dollars, may

apply for permission to carry out transactions in foreign currencies, precious metals and

shares denominated in foreign currencies. Such permit shall be issued, provided that at any

time the aggregate amount of credit granted in foreign currency will not exceed 10% of

equity finance company. In Singapore, there are 3 financial company.

Some of major financial institutions operating in Singapore in accordance with a

license to provide a full range of services:

ABN AMRO BANK NV

AMERICAN EXPRESS BANK LTD

BANGKOK BANK PUBLIC COMPANY LIMITED

BANK OF AMERICA, NATIONAL ASSOCIATION

BANK OF CHINA LIMITED

BANK OF EAST ASIA LTD

THE BANK OF INDIA)

BANK OF TOKYO-MITSUBISHI, LTD

BNP PARIBAS

CALYON

CITIBANK SINGAPORE LIMITED

HL BANK

(HONGKONG AND SHANGHAI BANKING CORPORATION LIMITED

THE INDIAN BANK

INDIAN OVERSEAS BANK

JPMORGAN CHASE BANK, N.A.

MALAYAN BANKING BHD)

PT BANK NEGARA INDONESIA (PERSERO) TBK

RHB BANK BERHAD

SOUTHERN BANK BERHAD

STANDARD CHARTERED BANK

SUMITOMO MITSUI BANKING CORPORATION

UCO BANKhttp://sgbanks.com/singapore-banking-system-opening-account-singapore

Page 4

Bisnis.com, NUSA DUA - Berbeda dengan Indonesia, sejumlah negara di Asia telah

memiliki skema perlindungan nasabah terintegrasi.

Sebut saja Korea Selatan yang memiliki perkembangan paling pesat dalam

implementasi skema proteksi terintegrasi.

Begitu juga Singapura, bahkan negara tetangga Malaysia yang sudah memiliki lembaga

independen yang menangani perlindungan nasabah perbankan dan asuransi.

Hayden Hyunseok, Senior Manager International Cooperation Team Korea Deposit

Insurance Corporation (KDIC), memaparkan sejak terjadi krisis finansial di Asia pada

1997, struktur industri finansial di Korea berubah drastis dari semula hanya ada skema

kompensasi terhadap perbankan, sampai akhirnya digagas skema kompensasi

terintegrasi.

Tak hanya industri perbankan, pemerintah Korea juga menjamin perlindungan nasabah

di industri asuransi, pasar modal, dan perkreditan. Batasan dana yang diberikan kepada

nasabah setiap sektor antara lain, masing-masing 20 juta won untuk nasabah

perbankan dan pasar modal, dan masing-masing 10 juta won bagi nasabah merchant,

mutual savings bank, serta nasabah serikat kredit.

Bagi nasabah lembaga perkreditan diberikan penggantian kerugian maksimal 30 juta

won, sementara itu penggantian untuk nasabah asuransi tercatat paling tinggi yakni

mencapai 50 juta won.

Di Singapura, lembaga perlindungan nasabah terintegrasi bernama Singapore Deposit

Insurance Corporation (SDIC) bahkan sudah memiliki jenis dan bentuk pungutan yang

jelas dan rinci untuk masing-masing produk asuransi.

Chief Executive Officer SDIC Ooi Sin Teik menjelaskan pihaknya memisahkan premi

dan batasan dana kerugian bagi industri asuransi jiwa dan asuransi umum.

Page 5

“Untuk produknya pun memiliki klasifikasi dan batasan tersendiri, ada maksimum

kerugian yang diganti,”paparnya dalam seminar 3rd International Workshop on

Integrated Protection Scheme beberapa waktu lalu.

Tak hanya pemisahan persentase premi dan batasan maksimum dana kerugian,

pemerintah Singapura juga memisahkan dana hasil pengumpulan premi masing-masing

industri agar tidak ada cross subsidize dan menimbulkan kerancuan.

http://finansial.bisnis.com/read/20140316/215/211174/contoh-skema-perlindungan-nasabah-terintegrasi-di-beberapa-negara

Otoritas Moneter Singapura atau Monetary Authority of Singapore (Singkatan: MAS; bahasa

Tionghoa: 新加坡金融管理局; bahasa Malaysia: Penguasa Kewangan Singapura) adalah bank

sentral dan otoritas keuangan di Singapura. Hal ini mengelola berbagai hukum yang terkait dengan

uang, perbankan, asuransi penerbitan, sekuritas dan sektor keuangan pada umumnya, serta mata

uang Singapura.

Daftar isi

[sembunyikan]

1 Sejarah 2 Tanggungjawab

o 2.1 Alat 3 Penerbitan uang kertas dan uang logam 4 Lihat pula 5 Referensi 6 Pranala luar

Sejarah[sunting | sunting sumber]

Otoritas Moneter Singapura didirikan pada tahun 1971 untuk mengawasi fungsi-fungsi keuangan

terkait dengan perbankan dan keuangan. Sebelum pembentukan, fungsi keuangan dilakukan oleh

Departemen pemerintah dan agen.

Sebagai negara berkembang Singapura, klaim dari perbankan semakin kompleks dan lingkungan

keuangan mengharuskan perampingan fungsi untuk memudahkan pengembangan kebijakan yang

lebih dinamis dan koheren tentang hal-hal keuangan. Oleh karena itu pada tahun 1970,Parlemen

Page 6

Singapura melewati hukum Otoritas Moneter Singapura yang mengarah pada pembentukan MAS

pada 1 Januari 1971.

Tanggungjawab[sunting | sunting sumber]

Pada April 1977, Pemerintah memutuskan untuk membawa keseimbangan industri asuransi di

bawah sayap MAS dan pada September 1984 fungsi regulasi bawah Securities Industry Act (1973)

juga dipindahkan ke MAS. Ini berarti bahwa tidak seperti banyak bank sentral yang lain, MAS juga

pihak kuasa keuangan untuk Singapura.

MAS telah diberikan kuasa untuk bertindak sebagai bankir dan agen keuangan Pemerintah. Ini juga

telah dipercayakan untuk memperkenalkan stabilitas keuangan, dan kredit dan kebijakan perubahan

kondusif untuk pertumbuhan ekonomi.

Alat[sunting | sunting sumber]

Namun, tidak seperti banyak bank sentral yang lain seperti Federal Reserve System di Amerika

Serikat atau Bank of England di Britania Raya, MAS tidak mengatur sistem keuangan melalui suku

bunga untuk mempengaruhi likuiditas dalam sistem. Sebaliknya, MAS memilih untuk melakukannya

melalui mekanisme pertukaran asing. MAS melakukannya dengan intervensi di pasar Dolar

Singapura.

Penerbitan uang kertas dan uang logam[sunting | sunting sumber]

Setelah penggabungan dengan Dewan Komisaris Uang pada tanggal 1 Oktober 2002, MAS

diasumsikan fungsi penerbitan mata uang.

MAS memiliki hak eksklusif untuk mengeluarkan uang kertas dan uang logam di Republik

Singapura. Dimensi, desain dan denominasi mereka ditentukan oleh Komite Kebijakan Keuangan

dengan persetujuan Pemerintah. Uang kertas dan uang logam sehingga diterbitkan memiliki status

legal tender di dalam negeri untuk semua transaksi, baik negeri maupun swasta, tidak terbatas.

https://id.wikipedia.org/wiki/Otoritas_Moneter_Singapura

Banking Industry and Major Banks in SingaporeRelated Links

Setting Up a Singapore Company

Page 7

Opening a Singapore Bank Account

Singapore Income Tax

Singapore is a flourishing financial centre of international repute servicing not only

its domestic economy per se but also the entire Asia Pacific region. The banking

industry is a key player in the country’s financial market segment, soon emerging

as one of the strongest in the world. Factors such as a sound economic and political

environment, conducive legal and tax policies, reputation for integrity, and strict

enforcement against crime and money laundering, have contributed to Singapore’s

status as an International Finance Centre – the third largest in Asia, after Japan and

Hong Kong. Today there are as many as 117 foreign banks and 6 local banks that

dominate the banking scene.

Factors that have contributed to the success of the banking industry in Singapore

include:

Liberalisation of the domestic banking market.

Local banks strengthened their regional presence through mergers and

acquisitions.

Expansion of foreign banks, some of which made Singapore a regional or even

global platform for important banking services, which in turn led to increased

competitiveness.

Increased competition spurred the development of innovative products and more

competitive pricing models.

Provision of sophisticated banking services like corporate and investment banking

activities, apart from traditional lending and deposit-taking functions.

Strict banking secrecy laws, tax friendly policies and a suite of wealth

management services created a private banking boom. Swiss giants Credit Suisse

Group and UBS AG have expanded private-banking operations in Singapore to

cater to new demand from Asians and Europeans.

Page 8

Recognising and catering to the needs of Small and Medium Enterprises who

comprise a sizable banking market in Singapore.

This guide provides an overview of the banking industry in Singapore focusing on

the key trends, the major domestic and international players and the services they

offer, the role of the Monetary Authority of Singapore (MAS) and banking regulations

that govern the industry today.

Singapore’s Banking Industry TrendsLiberalisation of banking sector

In May 1999, MAS launched a five-year liberalisation package to strengthen the

banking system and to improve Singapore’s reputation as an international financial

centre. The measures included issuing a new category of full banking licenses

known as Qualifying Full Bank (QFB) licenses to foreign banks, increasing the

number of restricted banks, and giving offshore banks greater flexibility in

Singapore Dollar wholesale business. MAS also set out to improve corporate

governance practices. Furthermore, the 40 percent foreign shareholding limit in

local banks was lifted.

The second phase of liberalisation began in June 2001 during which the restricted

banks were re-classified as wholesale banks to improve competitiveness in retail

banking. QFBs were given more privileges (permission to establish more locations,

provide debt and special account services). Qualifying offshore banks (QOBs) were

given priority to upgrade themselves to wholesale banking status. Consolidation of

local banks was seen as a positive, stabilising move as these banks play a pivotal

role in providing resilience and stability to the banking system, especially during a

financial crisis.

Growth of private banking industry

Singapore has capitalised on the growing number of high net worth individuals in

Asia and other regions like Europe and the Middle East, emerging as a leading

private banking destination for international investors. Singapore has earned the

sobriquet “Switzerland of Asia”, attributable to

Page 9

Strict banking secrecy laws – Section 47 of the Banking Act states that customer

information shall not, in any way, be disclosed by a bank or any of its officers, to

any other person except as expressly provided in the Banking Act.

Non-recognition of the 2005 European Tax Directive – Singapore is one of the few

remaining offshore centres that has not signed up to the EU’s Savings Tax

Directive, whose country members can exchange private information relating to

individuals who bank and invest in these countries.

Generous tax incentives – Capital gains and interest income from outside

Singapore are not taxed here.

Private banks such as UBS, Credit Suisse, Citigroup and Standard Chartered to

name a few, provide

global wealth management services

wealth and lifestyle advisory services

investment strategies

tax and estate planning

asset protection

credit services

Investment banking hub

The investment banking industry opened up as Singapore matured into a key

international debt arranging hub in Asia. The following factors have contributed to

the country’s active and thriving capital market:

Encouraging a steady flow of issuance from the Singapore Government, statutory

boards, supra-nationals and corporates.

Launching the Approved Bond Intermediary Scheme that nurtured bond investors

to sustain the debt market.

Growth of SGX as an International exchange which attracted many foreign

companies, who account for more than a quarter of total listings.

Page 10

High standards to maintain investor confidence led to various initiatives to

enhance disclosure, strengthen market discipline and improve corporate

governance of listed companies. These measures included: the Code of Corporate

Governance, revisions to the SGX listing rules and the introduction of the new civil

penalty regime under the Securities and Futures Act.

Most investment banks in Singapore perform various corporate-finance and

investment related activities like:

Underwriting securities

Acting as an intermediary between an issuer of securities and the investing public

Acting as a broker for institutional clients

Facilitating mergers and acquisitions; and corporate reorganizations

Strengthening of local banking groups

A major move in the local banking sector was the consolidation of the previously 6

local banking groups into the present 3 main local banks (DBS, OCBC and UOB).

This led to strengthening the banks’ capabilities, building their management teams

and enhancing operational effectiveness. They have expanded their range of

business activities and have also improved their business and risk management

capabilities. Today, the local banks are “one stop shops” designed to meet all the

needs of their banking customers. With greater financial strength from the mergers

and increased competition at home, local banks have begun to venture abroad and

develop a regional footprint through overseas acquisitions.

SME Banking Services

Local and foreign banks alike have recognised that SMEs are an important segment

of the market and offer a wide range of financial services tailored to meet their

needs. Deposit products and cash management services, loan products, card

products, insurance products, trade financing services (import/export products) and

investment products are all designed to cater to the needs of these enterprises. In

addition to commercial credit, the Government also has financing schemes to assist

SMEs to upgrade, modernise and expand their operations.

Page 11

Industry Snapshots

With one of the more well-established capital markets in Asia-Pacific, the

Singapore Exchange (SGX) is the preferred listing location for more than 200

global companies.

Singapore has grown to be the largest Real Estate Investment Trust (REITs)

market in Asia ex-Japan and also provides an extensive offering of investments in

business trusts of shipping, aviation and infrastructure assets.

With an extensive range of both Singapore government securities and foreign

corporate bonds available, Singapore offers fixed income investors a wide range

of investment opportunities.

As one of the top 5 most active foreign exchange trading centres in the world,

Singapore is also the second largest over-the-counter derivatives trading centre in

Asia, and a leading commodities derivatives trading hub.

Singapore is recognized as one of the premier asset management location in Asia

with total assets under management around S$1 trillion.

Types of BanksMost banks in Singapore cater to different types of clients – individuals, corporations

or government agencies. These banks provide commercial banking (catering to

businesses and corporations), retail banking (catering to individual members of the

public) and private banking (catering to HNWIs) services. Banks can be classified

into 2 main categories:

Local Banks (6)

Foreign Banks(117) – further sub divided into

o Full Banks (27) – provide the whole range of banking business approved under

the Banking Act. Six of the foreign banks operating in Singapore have been

awarded Qualifying Full Bank (QFB) privileges. These banks include: HSBC,

Citibank, Standard Chartered, Maybank, ABN AMRO and BNP Paribas.

o Wholesale Banks (53) – engage in the same range of banking activities as full

banks, except Singapore Dollar retail banking activities. All wholesale banks in

Page 12

Singapore, operate as branches of foreign banks. Examples: ING bank, National

Australia Bank, Barclays Bank, Deutsche Bank etc.

o Offshore Banks (37) – engage in the same activities as full and wholesale

banks for businesses transacted through their Asian Currency Units (an

accounting unit, which banks use to book all foreign currency transactions

conducted in the Asian Dollar Market). The banks’ Singapore dollar transactions

are separately booked in the Domestic Banking Unit (DBU). All offshore banks in

Singapore, operate as branches of foreign banks. Examples: Korea

Development Bank, Bank of Taiwan, Bank of New Zealand, Canadian Imperial

Bank of Commerce etc.

o Merchant banks (42) – provide corporate finance, underwriting of share and

bond issues, mergers and acquisitions, portfolio investment management,

management consultancy and other fee-based activities. Most merchant banks

have, with MAS’ approval, established ACUs, through which they compete with

commercial banks in the Asian Dollar Market. In their DBU, they may accept

deposits or borrow only from banks, finance companies, shareholders and

companies controlled by their shareholders. Examples: Credit Suisse Singapore

Ltd, Barclays Merchant Bank Singapore Ltd, ANZ Singapore Ltd, Axis Bank Ltd

etc.

Major Banks in SingaporeMajor local banks

1. DBS (Development Bank of Singapore) established in 1968, is considered the

largest bank in Singapore and Southeast Asia, as measured by assets. It is a

leading consumer bank in Singapore and Hong Kong, serving over 4 million and

1 million retail customers respectively. It also has the largest retail network in

Singapore, with 80 branches at present. It ranked 14th in The Banker’s “Top 200

Asian Banks 2008″.

2. OCBC (Oversea Chinese Banking Corporation) established in 1912, is one of the

largest financial institutions in the Singapore-Malaysia market with total assets

of S$184 billion. It ranked 1st in “Top 5 Regional Banks”, Asia Risk End-User

Survey 2008.

Page 13

3. UOB (United Overseas Bank) established in 1935, is a leading bank in Singapore

with a strong presence in the Asia-Pacific region. As at 31 December 2007, the

UOB Group had total assets of S$175.0 billion. It was awarded the “Best Overall

Fund Group in Singapore” during The Edge-Lipper Singapore Fund Awards 2008.

Major foreign banks

1. HSBC – In Singapore, The Hong Kong and Shanghai Banking Corporation Limited

first opened its doors in December 1877. HSBC is an approved Primary Dealer in

the Singapore Government Securities Market and an Approved Bond

Intermediary (ABI). It is a QFB honoured with 33 awards at Global Finance

Awards 2006 by Global Finance.

2. Standard Chartered – Standard Chartered’s Singapore operations began in 1859

and today boasts of a largest branch network (20) among international banks in

the Republic. It is the Group’s second largest consumer banking market and

was awarded a Qualifying Full Bank (QFB) licence in 1999. It is the largest

custodian bank in Singapore for foreign institutions, rated top for the past seven

years in Global Custodian’s Agent Bank Survey.

3. ABN-AMRO Singapore – ABN AMRO is now owned by RBS, Santander and the

Dutch government. Its various businesses around the globe are currently being

separated from ABN AMRO and integrated in line with each owner’s plans.

4. Maybank – Maybank’s presence in Singapore began in 1960 as a full-licensed

commercial bank. Maybank is currently among the top five banks in ASEAN and

is a Qualifying Full Bank in Singapore. As of June 2008, Maybank’s total assets

amounted to S$22.7 billion in Singapore.

5. BNP Paribas – BNP Paribas has been at the forefront of banking in Singapore

since 1968 and was awarded a QFB status in 1999. Today, BNP Paribas

Singapore assumes a prominent presence in the region by acting as the Group’s

regional hub for its business in Corporate and Investment Banking as well as

Private Banking.

6. Citibank – Citibank was the first American bank to set up a branch in Singapore

in 1902. Although a relative latecomer to the retail-banking sector, the bank has

grown into a formidable market player with major market share in key

Page 14

businesses including unsecured lending, deposits and investments and secured

assets. Citibank was among the first four foreign banks to be awarded the

Qualifying Full Bank (QFB) license in 1999.

Bank Regulations and LegislationIn Singapore, the laws regulating banking are found in the relevant Acts passed by

Parliament (and their related subsidiary legislation), the common law and principles

and rules of equity. The common law and principles and rules of equity are derived

from case law. These legislations not only regulate the banking sector in Singapore,

but also ensure that the legal framework for banking in Singapore keeps pace with

the latest developments in the financial world. The relevant acts pertaining to the

banking industry include:

1. Banking Act – The Banking Act (Cap 19, 2003 Rev Ed) is the legislation that

governs commercial banks in Singapore.

2. Monetary Authority of Singapore Act (Cap 186, 1999 Rev Ed) – governs all

matters related to and connected to MAS and its operations.

3. Anti Money Laundering Regulations

4. Payment & Settlement Systems Guidelines

5. Securities and Futures Act

Role of Monetary Authority of SingaporeIn Singapore, the Monetary Authority of Singapore acts as a defacto central bank. It

was established in 1971 in order to regulate Singapore’s financial industry to aid in

its development as an international financial centre. Its primary function is to

ensure that the financial markets operate in an efficient and smooth manner, in line

with national economic goals. The MAS is responsible for the following:

Implementing monetary policy

Supervisor of the banking systems

Banker to the government

Banker to the banks

Controller of International Reserves

Issuer of currency

Page 15

Issuer of banking licences

Lender of last resort

http://www.guidemesingapore.com/doing-business/finances/singapore-banking-industry-overview

Government Funding and Assistance SchemesRelated Links

Singapore Company Setup Guide

Private Equity Financing Guide

Private Debt Financing Guide

Recognizing that lack of adequate funding is often the most common stumbling

block for start-ups in general. In this regard, the role of the Singapore government

and its associated agencies cannot be overemphasized in contributing to

Singapore’s success as a start-up friendly nation. Enterprise development is on the

top of the government’s agenda. It has consciously crafted a pro-business, and

supportive environment conducive to entrepreneurs who want to start a business

here. Singapore-based start-ups can benefit from an optimal business environment,

excellent infrastructure, low-tax system, lack of bureaucracy, strong legal

environment, a readily available workforce.

The Singapore government has rolled out several initiatives to enable start-ups to

gain access to funding. These funding initiatives include cash grants, government

backed equity financing schemes, business incubator schemes, debt financing

schemes, and tax incentives.

This guide sheds light on the various support programs that have been instituted to

help Singapore start-ups gain access to funding to turn their business ideas into

reality. Start-ups in Singapore have a lot to look forward to in terms of government

Page 16

aided financial assistance schemes. The funding initiatives instituted by various

government agencies for start-ups include the following:

Government-aided equity financing schemes

Cash grants

Business incubator schemes

Debt financing schemes

Tax incentive schemes

Equity Financing SchemesEquity financing is capital that is lent by investors to a business in exchange for a

share of ownership in the company. This form of financing is ideal for start-ups that

need additional capital, especially in their early-stage of development. In addition to

private sources of equity capital, there are certain co-investment equity financing

schemes that have been launched by the Singapore government in order to

catalyze the supply of private capital. In other words, the government co-invests in

start-ups along with a third-party investor. The popular government-backed equity

financing schemes include the following:

SPRING Startup Enterprise Development Scheme (SPRING SEEDS):

SPRING SEEDS is an equity investment scheme where SPRING SEEDS Capital, a

subsidiary of government agency SPRING Singapore, co-invests in commercially

viable Singapore-based start-ups along with independent third-party investor(s),

matching dollar-for-dollar up to a maximum of S$1 million; the first round of

investment is usually limited to S$300,000. SPRING SEEDS Capital and the third-

party investor(s) will take equity stakes in the company in proportion to their

investments. For more details, please visit here.

Business Angels Scheme (BAS): The Business Angels Scheme is an equity

investment scheme where SPRING SEEDS Capital, a subsidiary of government

agency SPRING Singapore, co-invests in growth-oriented, innovative Singapore-

based start-ups along with pre-approved business angels matching dollar-for-

Page 17

dollar up to a maximum of S$1.5 million. SPRING SEEDS Capital and the business

angel group will take equity stakes in the company in proportion to their

investments. For further information, please click here.

Early-Stage Venture Funding Scheme (EVFS): The Early-Stage Venture

Funding Scheme (EVFS), that is administered by the National Research

Foundation (NRF), is a co-funding scheme where selected venture capital firms

who raise at least S$10 million from third-party investors will receive dollar-for-

dollar matching from the NRF up-to a maximum of S$10 million in order to invest

in early-stage technology start-ups. Certain qualifying technology start-ups can

approach the venture capital firms directly in order to seek funding of up-to S$3

million. Click here to find out more.

Cash GrantsOne of the advantages of starting-up in a country like Singapore is that aspiring

entrepreneurs can gain access to business grants disbursed by different

government agencies to fund start-ups across various industries. Each grant has its

set of terms and conditions including qualifying criteria and disbursement method.

Typically, grants only cover a percentage of the finance needed. The business

owner will have to pitch in for the remaining capital. Most grants for start-ups are

designed to encourage investment in innovation, research and development, and

social causes. You are advised to review the terms of the grant prior to making an

application with the appropriate government agency. Some of the popular grants

that are made available to start-ups in Singapore include:

ACE Start-ups Scheme: ACE Start-ups Scheme is a financial assistance scheme

where ACE (Action Community for Entrepreneurship) will match S$7 to every S$3

raised by an entrepreneur for up to S$50,000. In other words, the entrepreneur

will need to raise S$21,429 if (s)he wishes to receive a grant of S$50,000. For

selected ventures, ACE will match S$3 to every S$7 raised by the entrepreneur for

an additional S$50,000. For these ventures, the total grant is capped at

S$100,000. ACE does not take equity in exchange for the financial grant. For more

details, please click here.

Page 18

Technology Enterprise Commercialization Scheme (TECS): The TECS that is

jointly administered by the Infocomm Development Authority (IDA) and SPRING

Singapore spurs the formation of new technology start-ups in Singapore by

addressing their early-stage funding needs towards the commercialization of

proprietary technology ideas. The following grants are offered under the TECS:

o For applicants who wish to develop proprietary ideas at conceptualization stage:

Up-to 100% of qualifying costs for each project up to maximum of S$250,000.

o For applicants who wish to carry out further research and development on a

technology project, including the development of a working prototype: Up to

85% of qualifying costs for each project up to maximum of S$500,000. The

applicant must demonstrate proof of interest from a potential customer or third-

party investor. Click here to find out more.

iSTART:ACE Scheme: The iSTART:ACE (Accelerate & Catalyse Entrepreneurship)

grant scheme that is administered by the Infocomm Development Authority (IDA)

aims to encourage and assist Singapore-based start-ups to accelerate technology

commercialization and catalyze go-to-market activities by leveraging

internationally proven technologies. Under the iStart:ACE scheme, the IDA will

offer funding support to qualifying start-ups by way of a grant that covers up-to

50% of salaries of five technical staff for one year up-to a maximum cap of

S$250,000. For more information, please click here.

iSPRINT: Another project by the IDA, iSPRINT (Increase SME Productivity with

Infocomm Adoption & Transformation) covers improvements through packaged

solutions, such as for accounting and payroll, to more complex customized

solutions for areas such as customer relationship management and supply chain

management. Any customized solutions require that the development must be for

the first-time automation of business functions. In addition, it should be carried

out in Singapore, and must not have started before the grant is approved. iSPRINT

is open to all locally registered or incorporated SMEs. For more information,

see iSprint Scheme Details.

ComCare Enterprise Fund (CEF): The ComCare Enterprise Fund that is

administered by the Ministry of Social and Family Development (MSF; formerly

Page 19

Ministry of Community Development, Youth & Sports) provides seed funding for

social enterprise start-ups (strictly from the social services sector) that train and

employ disadvantaged Singaporeans of up-to 80% of the capital expenditure and

first two years’ operating costs, subject to a maximum of S$300,000. More details

can be found here.

New Initiative Grant (NIG): The New Initiative Grant that is administered by

the National Volunteer and Philanthropy Centre (NVPC) provides seed money for

Singapore-based start-ups with new initiatives that meet community needs in

Singapore and are strong in volunteerism and/or philanthropy. Qualifying start-

ups will receive funding that covers up to 80% of costs (e.g. manpower, rent,

equipment, volunteerism and philanthropy-related costs) in furtherance of the

initiative for one-year subject to a maximum of S$200,000. Click here for more

details.

*Currently on hiatus till July 2015.

Need help with incorporation? Find out how we can

help!Need help with incorporation? Find out how we can

help!Business Incubation SchemesBusiness incubators are an invaluable resource for start-up entrepreneurs who are

not only looking for funding but are also keen on getting guidance and know-how for

their venture. In general, business incubators offer a physical space for the new

business to operate along with access to cost-effective shared services, business

guidance, and financial assistance during their early-stage of development. It is

ideal for start-ups that are looking for regular support, mentoring, funding and

networking along with low-start up costs. The current incubation schemes that are

available to start-ups in Singapore include:

i.Jam Micro Funding Scheme: The IDM (Interactive Digital Media) Jump-start

And Mentor (i.JAM) scheme that is administered by the Media Development

Page 20

Authority’s inter-agency, Interactive Digital Media Programme Officeappoints

incubators to identify, nurture, and administer funding to technically competent

start-ups. More specifically, the incubators will advise start-ups on the uniqueness

of their ideas, aggregate start-ups with similar ideas, offer networks, and provide

guidance on securing additional funding. Incubators will invest 10% to 25% of the

qualifying project costs of the start-up. In addition, start-ups will receive a grant

up-to a maximum of S$50,000 of the project’s qualifying costs. Incubators will

take equity stakes in the company in proportion to their investment. The grant

will be disbursed to the start-up on a reimbursement basis. To find out more,

please click here.

NRF Technology Incubation Scheme: The National Research Foundation has

selected fifteen technology incubators to nurture high-tech Singapore start-ups by

way of mentorship as well as funding. The NRF will offer up-to 85% co-funding in

each start-up company in the incubator, up to a maximum of S$500,000. The

incubator will be required to invest the remaining amount of at least 15%. NRF

and the incubator will take equity stakes in the company in proportion to their

investments. Click here for more information.

Incubator Development Program: The Incubator Development Program that is

administered by SPRING Singaporeprovides up-to 70% grant support to incubators

and venture accelerators who actively introduce programs that help nurture start-

ups including cost of hiring mentors, expenses incurred to market

services/events, hire incubator managers, train staff, provide shared

services/equipment for start-ups, etc. Innovative startups can benefit from the

programmes offered by the various incubators and venture accelerators

supported under the Incubator Development Program. To find out more, please

click here.

Incubator for Disruptive Enterprises and Start-ups (IDEAS) Fund: The

IDEAS Fund that was launched by Innosight Ventures Pte. Ltd. a Singapore-based

venture capital firm and the National Research Foundation (NRF) is an incubator

fund for early-stage start-up companies. Start-ups with disruptive innovation

potential will be identified and offered guidance during their early-stages

Page 21

including funding investment to the tune of up-to S$500,000-S$600,000. The NRF

supports the incubator with 85% co-funding. For additional information, please

click here.

Fast-Track Environmental and Water Technologies Incubator Scheme

(Fast-Tech): The Fast-Tech scheme that is administered by the Economic

Development Board offers start-ups in the environmental and water technology

sector funding assistance of up-to S$300,000 or up to 85% support level,

whichever is lower, over two years. In addition, the start-ups will be housed in

water-technology incubators who will offer mentorship and guidance. The

designated incubator will take an equity stake in the company. The grant will be

disbursed to the start-up on a reimbursement basis. To know more, please

click here.

Debt-Financing SchemesDebt-financing is a viable start-up funding option for entrepreneurs who wish to

raise capital without having to give up a share of their profits. The only downside is

that loan repayments have to be made on time and that borrowers are indebted to

lenders, irrespective of whether the start-up is generating profits or not. Traditional

sources of debt financing are “friendship loans” from family and friends as well as

private debt-financing schemes. However, there are a significant number of

government debt-financing schemes that have been designed for SMEs in

Singapore. Start-ups that meet the qualifying criteria can also avail of these

schemes. The various government debt-financing schemes in Singapore include:

Micro-Loan Program: Under the Micro-Loan Program, participating banks and

financial institutions will lend eligible Singapore companies loans of up-to

S$100,000 for their daily operations or for automating and upgrading factory and

equipment. The SMEs will have to pay a minimum 5.75% interest rate for a less

than four years loan tenure. For details, click here.

Loan Insurance Scheme (LIS): The Loan Insurance Scheme insures loans

against default risks. The government will co-share the insurance premium with

the start-up enterprise. The LIS supports both domestic trade and overseas trade

Page 22

facilities. There is no maximum loan quantum for the LIS. The premium rate,

interest rate, and loan tenure will be determined by the insurer based on the risk

profile of borrower. The government provides premium support of 50%. The

repayment structures and collateral requirements will be determined by the

participating financial institutions. Further information can be found here.

Local Enterprise Finance Scheme (LEFS): Under the LEFS, participating banks

and financial institutions will lend eligible Singapore companies loans of up-to

S$15 million for automating and upgrading factory and equipment/construction

equipment/heavy vehicles, and/or purchasing factory and business premises. The

SMEs will have to pay a minimum 4.75% interest rate for a less-than-four-years

loan tenure and 5.25% interest rate for a loan tenure of more than 4 years. To

know more, please click here.

Tax Incentive SchemesOne of the very prudent and noteworthy initiatives of the government has been the

introduction of several tax benefits for start-ups. Tax breaks act an incentive for

entrepreneurs to build more companies and generate more jobs for the economy.

Listed below are the various tax incentives that are made available to start-ups and

SMEs in Singapore.

Tax Exemption for Start-ups: Singapore startups that meet certain qualifying

criteria can avail of a full tax exemption on a certain amount of their taxable

income for the each of their first three consecutive years. A newly incorporated

Singapore company that satisfies the qualifying conditions (viz. be incorporated in

Singapore, be a tax resident of Singapore and has no more than 20 shareholders

of which at least one is an individual shareholder holding at least 10% of shares)

will be taxed as follows:

o For each of its first three consecutive tax years – corporate tax rate of 0% on

the first S$100,000 of taxable income and 8.5% (partial exemption) tax rate on

the next S$200,000 of taxable income. The taxable income above S$300,000

will be charged at the normal headline corporate tax rate of 17%.

Page 23

o From the fourth tax year onwards – 8.5% tax rate on taxable income of upto

S$300,000 per annum. The taxable income above S$300,000 will be charged at

the normal headline corporate tax rate of 17%. For more information, please

refer to our Singapore Corporate Tax guide.

Development and Expansion Incentive (DEI): The DEI encourages Singapore-

based companies to move into high value-addition business activities, expand

their operations in the country, and procure advanced machinery and equipment

by offering a reduced tax in the range of 5%-10% on incremental income derived

from qualifying activities.

Investment Allowance: Companies may claim capital allowance on plant and

equipment used in connection with their trade or business, subject to meeting

certain conditions. Budget 2012 saw the introduction of a new Integrated

Investment Allowance Scheme that will provide an additional allowance on fixed

capital expenditure incurred for productive equipment placed overseas on

approved projects with effect from YA 2013.

Pioneer Incentive Scheme: Companies from the manufacturing or services

sector that engage in activities that raise overall industry standards may be

eligible for full corporate tax exemption on qualifying profits for up to 15 years.

Productivity and Innovation Credit (PIC) Scheme: The PIC scheme is a tax

benefit scheme that was first introduced in 2010 to encourage companies to

engage in innovative and productive activities. Under the scheme, businesses can

enjoy up-to 400% deduction or allowances on up to $400,000 of expenditure

incurred in each of the following qualifying innovative activities. The qualifying

activities include Research & Development; Intellectual Property registration;

Intellectual Property acquisition; Design activities, Automation through technology

or software; and training of employees. Note businesses will be allowed to

combine the $400,000 expenditure cap per year for YA 2013 to YA 2015 into a

new ceiling of $1,200,000 over the three years. Businesses with a low taxable

income, can choose to convert up to S$300,000 of the tax deductions and

allowances credited to them into a cash grant, up to a maximum of S$21,000

each year. Businesses can also exercise an option to convert upto S$100,000 of

Page 24

their expenditure into a non-taxable cash payout at a conversion rate of 30%. The

cash payout rate will be increased from 30% to 60% for up to S$100,000 of

qualifying expenditure from YA 2013 to YA 2015. Earlier the PIC benefits were

applicable only to R&D activities performed in Singapore. However, effective YA

2011 PIC benefits will also extend to R&D done overseas.

Industry-specific tax incentives: In addition to the above-mentioned tax

incentives, there are various industry-specific tax incentives for Singapore-based

SMEs, including start-ups. For a comprehensive overview of these incentives,

please refer to our guide on Industry-specific Tax Incentives in Singapore.

On A Final NoteToday, Singapore has emerged as a premier destination to do business. The World

Bank has consistently ranked Singapore as the best place to do business for the last

six consecutive years. It has also been ranked as Asia’s most entrepreneurial

economy and the best country to nurture start-ups for expats. Singapore has

emerged as a hub for first-time entrepreneurs and the city has witnessed the

mushrooming of several start-ups over the past few years. Start-ups, defined as

companies employing at least one employee and less than 5 years old, have

increased from 27,000 in 2002 to more than 36,000 in 2009 in Singapore. These

start-ups have employed more than 300,000 workers and generating more than

S$166 billion in turnover.

The Singapore government has taken cognizance of the key role played by new

businesses in spurring economic growth and has consequently spent considerable

amount of money, time and effort in devising a support ecosystem for start-ups in

Singapore.

http://www.guidemesingapore.com/doing-business/finances/singapore-government-schemes-for-startups

Venture Funding Options for Singapore CompaniesRelated Links

Page 25

Singapore Company Registration Guide

Private Debt Financing Guide

Government Assistance Schemes Guide

In equity financing, you sell partial ownership of your company in exchange for

cash. The investors assume all the risk i.e. if the company fails, they lose their

money. But if it succeeds, they typically make much greater return on their

investment than interest rates. Compared to debt financing, equity financing is far

more expensive if your company is successful, but far less expensive if it isn’t.

The rise of Asia is rapidly spurring the birth of new startups and private equity

players in Singapore. In recent times, the Singapore government has been actively

encouraging more private investors to invest in the country’s numerous start-ups by

introducing timely tax incentive schemes. According to a news report, Singapore

accounted for almost 52% of all private equity investments in Southeast Asia

between 2005 and 2010. The country is also considered to be the fourth attractive

market for venture capital and private equity firms. This spells good news for start-

ups that are looking to raise capital through equity financing.

This guide provides an overview of the private equity financing options for start-ups

in Singapore.

What is Private Equity Financing?One of the major challenges that start-ups face in their early stage is access to

capital. Many new business ventures are funded with informal capital often sourced

from the founders, or their family and friends. However, often to fund their growth

or to build out their infrastructure, informal sources of funding no longer suffice.

This is where private equity financing can play a role in addressing the gap.

Private equity financing refers to capital from private investors who are looking at

capital gains and possibly dividend returns in return for their investment in a firm.

Private funding is an attractive source of start-up funding especially for businesses

that do not have sufficient collateral for traditional loans. In order to have a good

chance of securing equity capital in Singapore, you need to have a comprehensive

Page 26

business plan, a clear exit strategy, reasonable financial projections, an experienced

management team, and strong growth potential. Determining the stage of your

business life cycle is key to finding the right investor. Venture capitalists and

business angels are the two major sources of private equity capital. Other sources

of private equity capital include banks, investment companies and financial

institutions.

Angel investors are wealthy individuals who generally invest in high risk, early

stage business ventures in exchange for a share of the business. In other words,

business angels are private investors who invest their business skills and capital

in start-ups and early-stage businesses in exchange for equity in the investee

company. Business angels can operate independently or can be part of an angel

network. They are usually interested in investing in start-ups that have high

growth potential and that belong to business sectors that they are familiar with.

Some business angels play an active role in the business in offering guidance, and

mentor-ship to start-ups while some act as sleeping partners. The best source of

private equity capital for start-ups in the seed or early-stage are business angels.

Venture capitalists are professional investors who play a very active role in

your business. Like most business angels, venture capitalists not only offer

funding, but also advise you on how you can enhance the profitability of your

business. Venture capitalists look for a higher rate of return from the company

they invest in, usually 25% and above. Most venture capitalists prefer to invest in

start-ups that are at advanced stage and are in high growth sectors such as

biotechnology, nanotechnology, or IT.

Private funds are the third source of equity financing for startups. Banks,

financial institutions, and investment companies are the main sources of private

funds. Managers of private funds are not interested in playing an active role in

managing the business. Their main purpose is to receive an attractive return on

their investment. Such funds are only suitable for those businesses that are

already established, are generating revenue, and have a high growth potential

and not start-ups in the early-stage of growth.

Page 27

Angel Investment Scene in Singapore Angel investment is a significant source of raising capital in Singapore.

Angel investors are typically successful businessmen with an appetite for start-up

companies with higher risk.

Usually, business angels offer early-stage investment to start-ups.

Angel investors tend to invest in start-ups that have a certain competitive

advantage in the market. This could include innovative technology, exclusive

marketing and distribution relationships or a strong brand or access to scarce raw

material, etc. The business idea should demonstrate that it will generate returns

for the investors.

Start-ups that have a high growth potential win the favor of most business angels.

Angel investors not only provide funding but also offer mentorship and strategic

guidance to the companies they invest in.

According to research conducted by the National University of Singapore,

business angels in Singapore tend to invest in the retail, hospitality and business

services sectors.

Typically, individual business angels invest anywhere between S$25,000-

S$100,000, while angel groups invest much larger sums in the range of

S$250,000-S$750,000.

Angel investors often form angel networks or groups in order to pool their

resources and capital. Angel networks are often a good source of capital for those

seeking early-stage or seed funding. The networks help match entrepreneurs with

appropriate business angels. Some of the popular angel investment networks in

Singapore are listed below in the article.

Venture Capital Industry in Singapore The venture capital industry in Singapore is relatively new and small as compared

to the US and Europe.

Page 28

The Singapore government plays an active role in attracting foreign venture

capital firms to set up their regional base in the country. Today, there are more

than 100 venture capital firms in Singapore.

Venture capitalists in Singapore not only provide financing but also offer

mentoring to start-up companies. Most entrepreneurs turn to venture capitalists

for both financing as well as to gain access to professional management skills and

expertise.

It must be noted that most venture capital firms in Singapore tend to focus on

“late-stage expansion financing” and investment in late-stage startups or mature

companies, rather than early-stage financing in new start-ups. Certain venture

capitalists prefer to invest in companies that are already making profits rather

than investing in a potentially profitable start-up. However, some firms do offer

financing for start-ups in their early stages.

There are different types of venture capital firms in Singapore ranging from

independent limited partnership venture capital firms to corporate backed

venture capital firms. Due to attractive tax incentives and other beneficial

government policies a number or cash-rich large corporations, government

boards and high net worth individuals have setup venture capital funds in

Singapore.

Venture capitalists in Singapore pay a great deal of attention to the services

industry, manufacturing industry, and the high-tech industry. In recent years a

significant portion of venture capital investments were directed towards high-

return sectors such as biotechnology, medicine, genetic engineering, etc.

On an average, venture capitalists invest up to four to five times the net earnings

of a company.

Generally, venture capital investments last between 2-5 years.

Businesses that are likely to turn into multi-million dollar companies in due course

are most favored by venture capitalists.

Page 29

Venture capitalists expect an ROI of at least 25%-30% for each year of

investment.

Venture capitalists look for the following factors while investing in seed stage

start-ups: A brilliant business idea that will have a competitive edge in the market

such as a scientific breakthrough or IP; a top-notch team; business model

innovations; and the economic and market benefits of the business plan/idea.

The business team plays a key role in securing the favor of venture capitalists.

More specifically, venture capitalists will look at how qualified the team is, what is

the role of each team member, what are the technical skills they possess, etc.

Venture capitalists assess the milestones that have been set for the business and

how much capital will be required to achieve them.

Venture capitalists assess the team’s understanding of the current market and

competition.

Venture capitalists are not interested in knowing long-term financial projections,

unrealistic claims about how the company will grow and acquire a large customer-

base in the short or long term, businesses that are solely seeking for funds

without any guidance from venture capitalists.

Private Equity Fund Industry in Singapore Private equity funds are setup by financial institutions, banks, or investment

companies.

Usually, private equity funds do not invest in early-stage or developing start-ups.

Established start-ups that are already in operation and demonstrate high growth

potential are preferred by private equity funds.

Private equity funds do not offer management and technical expertise; they only

provide funding.

There are different types of private funds such as:

o Independent funds: Such funds are typically setup by wealthy individuals, cash-

rich companies or families.

Page 30

o Institutional funds: Such funds are setup by banks and financial institutions.

o Corporate funds: Large companies setup a separate fund in order to invest in

smaller companies.

List of Private Funding Resources in SingaporeThere are several networks in Singapore that help match start-ups with business

angels and venture capitalists. The country also boasts of investment funds that

invest in innovative companies. Some of these networks and firms include:

Business Angel Network Southeast Asia (BANSEA): Matches start-ups in the seed

stage of enterprise formation with business angels. BANSEA invests in companies

that offer exceptional opportunities for high returns on investment. This usually

implies early stage ventures with the potential to achieve high growth, strong

market position and sustainable advantages. BANSEA invests in companies that

have the potential to grow to more than S$50 million in annual revenue within

five years. This should be either in a developing market or in an existing market

with international scope.

Deal Flow Connection: Deal Flow Connection assists enterprises that are at

different phases of their growth and from different industry sectors to gain access

to intermediaries and various sources of funds such as banks, finance houses,

venture capital firms and investors. Start-ups can expect to raise capital of

S$50,000 or more.

Angel Capital Network: Invests in entrepreneurs and companies in a variety of

industries and stages of development.

Business Angels Pty Ltd: Refers businesses to angel investors.

Draper Fisher Jurvetson: DFJ invests in emerging technologies, from the Internet

and life sciences to clean energy and nanotechnology.

ENDEAVOR: Invests in all stages with a preference for late-stage expansion, joint

venture and distressed investments.

K1 Ventures Ltd: Invests across diverse industry sectors.

Page 31

Sirius Capital Holdings Pte Ltd: Is a boutique venture capital and entrepreneurial

finance firm, focused on small and medium-sized companies in Singapore and

overseas.

Upstream Ventures: Focuses on early-stage venture creation by providing

funding, expertise and networks to emerging companies

Singapore Investment Network: Provides access to one of Singapore’s largest

databases of angel investors who are regular investors in various industries

across Singapore.

Angels Den: A UK based angel network that has recently set up shop in Singapore.

Business Angels primarily look for a profitable return on their investment within

three to five years.

3V Source One Capital: Focuses on growth to late-stage companies with an Asian

link or growth strategy.

Extream Ventures: Is an early-stage venture fund focused on Asia-based

technology driven companies in the areas of Internet (enterprise, consumer,

retail), IDM (interactive digital media), mobile & wireless (applications & services),

security & biometrics, and semiconductors (fabless design) It typically targets

Singapore-based early stage companies with significant regional market

opportunities. Extream Ventures assumes the role of lead investor in early stage

companies, typically investing up to a maximum of S$3M per company as part of

a Startup or Series A round of funding.

Bio Veda: Invests in health-care companies in the developmental or expansion

stage.

Walden International: An international venture capital firm that provides seed and

startup funds for emerging growth companies, as well as capital for expansion

financing and acquisitions.

Nanostart Asia: Invests in young, up-and-coming companies in Singapore which

seek to commercialize a highly promising nanotechnology-based product or

process and who are approaching market launch.

Raffles Venture Partners: Invests in innovative start-up companies.

Page 32

OWW Capital Partners: Invests in service providers in infocomm technology,

logistics, education/training, healthcare, financial services and consumer services

sectors.

BAF Spectrum: Focuses on Asia-based (preferably Singapore), early stage

technology startups within digital media, internet and mobile consumer portals as

well as R&D-intensive information technology.

Azione Capital: An early stage venture capital investment company and startup

business incubator that focuses on digital media, mobile communications

(inclusive of the full spectrum of wireless technologies), energy and maritime

industry startups that operate primarily within Asia.

Enspire Capital: Invests at various stages of a company’s development, with a

typical initial investment of US$1 million to US$3 million across a wide range of

high tech industries, in Technology, Media and Telecommunications (TMT) and

Internet.

Springboard Harper: Invests in technology businesses that are in various stages of

development.

The Carlyle Group: Invests up-to US$25 million in early stage companies.

Adam Street Partners: Invests US$5-20 million in companies seeking venture

capital or growth equity to accelerate their businesses.

Fortune Venture: Focuses in high-tech investments, specifically in software,

information technology, and the Internet, areas which Singapore companies have

strong domain knowledge and core competency

GIZA Venture Capital: Invests in seed and early-stage technology companies

across industries such as ICT, cleantech, and life sciences.

Grove International Partners: Invests in companies whose underlying assets and

businesses are real estate or real estate related.

McLean Watson: Invests in a wide range of technology companies that address

large, changing or expanding new markets.

Tembusu Partners: Invests in entrepreneur-driven companies that exhibit strong

growth potential through scalability and the ownership of proprietary rights.

Page 33

Focuses on industry sectors such as education, green technology, oil & gas,

resources and healthcare

Vertex Venture Holdings: Invests in companies at various stages of development,

be it seed or mezzanine investments, with deal size ranging from US$1 million to

US$30 million.

Singtel Innov8: SingTel Innov8 (Innov8), a wholly-owned subsidiary of the SingTel

Group, is a corporate venture capital fund that invests in companies in all stages

of development, from seed to early growth. SingTel Innov8 invests in ideas,

technologies, products and services that are related to the Group’s business

including those in adjacent spaces such as internet applications and new digital

media.

Some of the private financial institutions in Singapore include:

Citibank

Standard Chartered Bank

Hong Kong and Shanghai Banking Corporation

Development Bank of Singapore

Oversea Chinese Banking Corporation

United Overseas Bank

GE Commercial Financing Singapore

IFS Capital Limited

Hong Leong Finance Limited

Sing Investments and Finance Limited

Singapura Finance Limited

ON A FINAL NOTEPrivate investors are increasingly turning their attention towards the Asia-Pacific

and are relocating their offices, investing capital, and executing transactions in the

region. With Singapore’s ascendancy as Asia’s entrepreneurial hub, more and more

private equity investors are heading to the country in search of growth rates and

opportunities that are currently hard to come by in more developed economies.

Singapore government hopes to bring in angel investments to the tune of S$600

Page 34

million by 2015. This is undoubtedly an advantage to start-ups that choose

Singapore as their operational base.

http://www.guidemesingapore.com/doing-business/finances/private-equity-financing-for-singapore-startups

Debt Financing Options for Singapore CompaniesRelated Links

Singapore Company Incorporation Guide

Private Equity Financing Guide

Government Assistance Schemes Guide

Debt financing is one of the options for first-time entrepreneurs who are looking for

small business loans or start-up capital in order to jump-start their business.

Unlike equity financing where investors take up equity stakes in the company, debt

financing helps entrepreneurs retail full control over their business including the

profits generated. In debt financing, you borrow the money and agree to pay it back

in a particular time frame at a set interest rate. You owe the money whether your

venture succeeds or not. Compared to equity financing, debt financing is far less

expensive if your company is successful, but far more expensive if it isn’t.

The primary source of debt financing for most start-up entrepreneurs is the close-

knit circle of their friends and family. However, capital loaned from personal sources

many not always suffice for a high-growth or capital intensive business. This is

where banks and finance companies can help. In recent times, Singapore banks

have witnessed a strong interest in their start-up loan offerings. According to a

news report, OCBC Bank said that its loans for start-ups rose 10% in the Q3 2011 as

compared the Q2 2011. Most banks and finance companies in Singapore offer

products and services that have been customized to meet the needs of small

enterprises. These range from working capital loans, factoring loans, to hire

purchase loans.

Page 35

This guide provides an overview of the various private debt financing options for

start-ups in Singapore.

Sources of Private-Debt Finance: Commercial loansTypes of Loans

Most banks and finance companies in Singapore offer small business loans to start-

up enterprises. Small business finance is offered by way of business revolving lines

of credit, business overdrafts, factoring loans, etc. The most common types of small

business loans that most banks and financial institutions offer in Singapore include

the following:

Working Capital Loans: A working capital loan is short-term loan that is

typically used to finance the everyday business operations of a company. Working

capital loans usually help businesses to stay afloat until they begin generating

revenue. Working capital loans can either be secured (i.e loans on the basis of

collateral) or unsecured (no placement of collateral). Unsecured loans charge

higher rates of interest as compared to secured loans and are often granted to

only low-risk borrowers. Start-ups fall under the high-risk category and are

therefore more likely to obtain secured working capital loans. Working capital

loans serve to fund only short-term financing needs and are not suitable for long-

term projects. Working capital loans can take the form of:

o Factoring loans: Factoring loans refers to money this is lent on the basis of

trade debts. In other words it is the financing of account receivables. In effect,

you are selling the account receivables to the factoring agent i.e. the bank. The

bank will loan you an advance on the basis of the account receivables and your

customer will have to directly make the settlement with the bank. There is no

other collateral involved.Typically, banks offer loans of up-to 90% of the

accounts receivables or billed invoices. However, it must be noted that the bank

will charge a fee in the range of 1-15% of the gross invoice value or an annual

interest rate of 5-8%. The advantage of factoring loans is that you can get

immediate access to cash as soon as you issue an invoice. Moreover, you do not

have to follow up with customers for payments. The downside is that you do not

Page 36

get 100% of the invoice value from the bank and some of your customers may

be averse to dealing with the banks directly.

o Short-term loans: Short-term loans are those that have a short maturity

period of one year or less. Some banks may require you to put up collateral

against the loan. Short-term loans are usually used for buying inventory, to

even out cash-flow, to pay bills or payroll, etc. Start-ups can avail of short-term

loans but will have to provide projected financial statements and demonstrate

their ability to pay up the loans.

o Overdraft: Overdraft is an instant extension of credit from a bank. By signing

up for an overdraft facility, businesses can overdraw their current account up to

a maximum amount agreed with the bank. Interest is paid only on what is

overdrawn and is usually charged at 1-2% above the bank’s prime rate. The

amount of credit allowed will depend upon the limit that has been set with the

bank. The advantage of the overdraft facility is that it is form of short-term

financing that allows for instant access to cash especially for activities such as

stock turnover or payment to creditors. Overdraft facility can either be secured

(on the basis of collateral) or unsecured (no collateral).

Hire Purchase Loans: Hire-purchase is a method of purchasing goods by making

installment payments over a fixed period of time. Hire purchase loans is an

arrangement where the bank finances the purchase of equipment, machinery, or

commercial vehicles for business operations. Hire purchase loans are usually used

to purchase assets that are non-cash convertible. Under hire purchase loans, the

bank will retain legal title to the financed asset, until the last installment is fully

paid-up. In other words, the buyer (hirer) purchases the goods (assets) by paying

a deposit and borrows a loan to make monthly installment payments to the seller

over a predetermined fixed financing period. The interest rate of such loans is

normally offered on a flat-rate basis (i.e a fixed rate on the full amount financed

for the entire hire purchase term). The financing period usually ranges between 4-

8 years depending upon whether the machinery/equipment purchased is new or

used. Usually, the loan amount is up-to 80-90% of the purchase price or market

value, whichever is lower.

Page 37

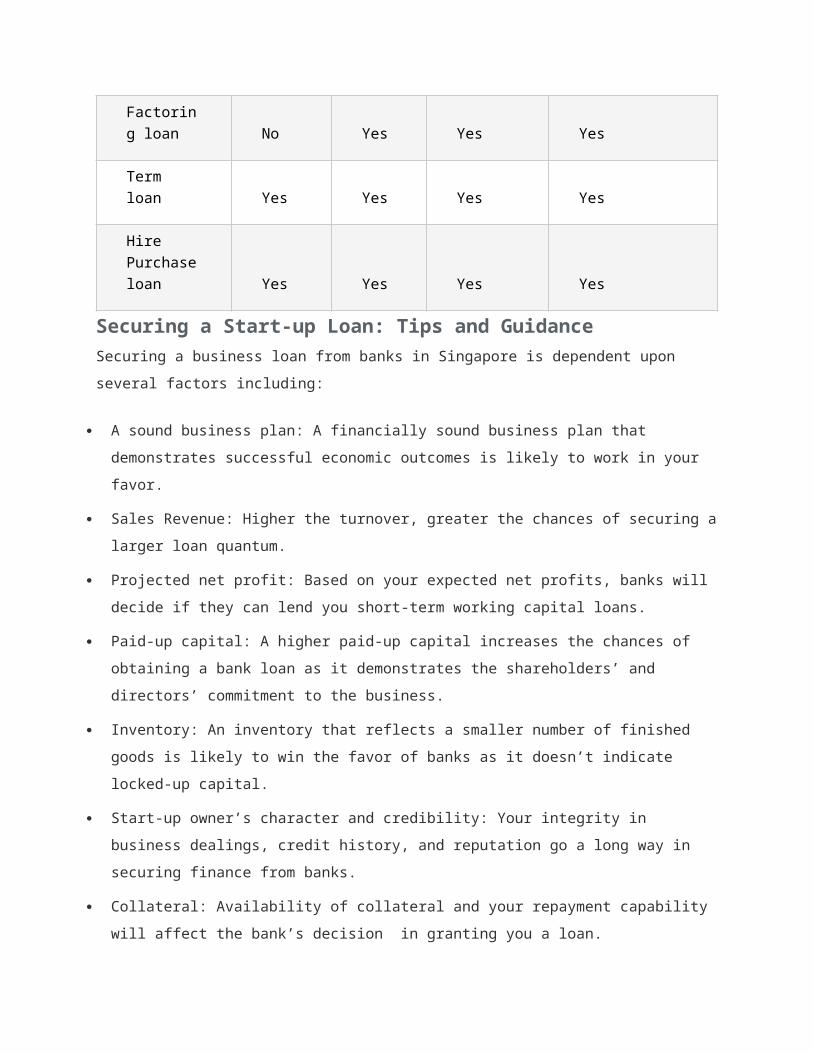

Debt-Financing Products of Financial Institutions in Singapore

For this article we have chosen four major sources of debt financing for start-ups

(overdraft, factoring loan, term-loan, and hire purchase loan) and compared their

availability across three key local banks viz. Development Bank of Singapore (DBS),

United Overseas Bank (UOB) and Oversea Chinese Banking Corporation (OCBC);

three major international banks viz. Standard Chartered Bank, HSBC and Citibank;

and four major finance companies.

Debt-financing products offered by banks

DBS UOB OCBC SCB HSBC CITI

Overdraft

Yes

Yes

Yes

Yes Yes

Yes

Factoring loan

Yes

Yes

Yes

Yes Yes

Yes

Term loan

Yes

Yes

Yes

Yes Yes

Yes

Hire-Purchase loan

Yes

Yes

Yes

Yes

Yes* No

* Commercial auto loans only

Debt-financing products offered by finance companies

ORIX LEASING

IFS CAPITAL

HONG LEONG FINANCE

SING INVESTMENTS & FINANCE

Overdraft No No No No

Factoring loan No Yes Yes Yes

Term loan Yes Yes Yes Yes

Page 38

Hire Purchase loan Yes Yes Yes Yes

Securing a Start-up Loan: Tips and Guidance

Securing a business loan from banks in Singapore is dependent upon several factors

including:

A sound business plan: A financially sound business plan that demonstrates

successful economic outcomes is likely to work in your favor.

Sales Revenue: Higher the turnover, greater the chances of securing a larger loan

quantum.

Projected net profit: Based on your expected net profits, banks will decide if they

can lend you short-term working capital loans.

Paid-up capital: A higher paid-up capital increases the chances of obtaining a

bank loan as it demonstrates the shareholders’ and directors’ commitment to the

business.