Performance information use by politicians and public managers for internal control and external accountability purposes Iris Saliterer *, Sanja Korac Alpen-Adria-Universita ¨t Klagenfurt, Universita ¨tsstraße 65-67, Room E.248, 9020 Klagenfurt, Austria 1. Introduction Under the umbrella of the global NPM movement, governance structures, patterns of responsibility, and modes of control have changed fundamentally as governments externalize or contract out services, sell agencies to the private sector, create quasi-markets and decentralize functions to local authorities, often leading to fragmented public service delivery systems (Hood, 1995; Rhodes et al., 1997). Moreover, boundaries between public, private, and third sector organizations have become blurred as the delivery of public services is increasingly characterized by hybrid forms of organization, variously described as partnerships, collaborations, networks, alliances and, most prominently, as public-private partnerships (Agranoff and McGuire, 2003; Kooiman, 2003; Salamon and Elliott, 2002). These changes in governance structures challenge Critical Perspectives on Accounting 24 (2013) 502–517 A R T I C L E I N F O Article history: Received 9 January 2012 Received in revised form 1 June 2012 Accepted 20 August 2012 Available online 21 August 2013 Mots cle ´s: Gestion des performances Responsabilite ´ Nouvelle gestion publique Gouvernance Palabras clave: Gestio ´n del rendimiento Responsabilidad Nueva gestio ´n pu ´ blica Gobernanza Keywords: Performance management Accountability New Public Management Governance A B S T R A C T Governance structures have changed fundamentally since the beginning of New Public Management inspired reforms. Particularly local public service delivery nowadays can be characterized as diversified and fragmented, leading to internal management and external accountability challenges for politicians as well as public managers. In this context the use of performance information is seen as a crucial element for effectively dealing with both issues. Nevertheless, empirical research considering different actors and contexts within one study is rare. The present paper fills this gap by applying a multi-theoretical perspective and testing hypotheses on the antecedents of performance information use by politicians and public managers for internal management as well as external accountability purposes in small- and medium sized local governments in Austria. The study results show that both groups use performance information to a greater extent within external accountability relationships than for internal management purposes. Results further illustrate that driving factors show similarities for both groups with reference to the latter mentioned purpose, while a more diverse picture is shown regarding factors impacting their use behavior toward citizens and supervisory authorities. ß 2013 Elsevier Ltd. All rights reserved. * Corresponding author. Tel.: +43 0463 2700 4132; fax: +43 0463 2700 4193. E-mail addresses: [email protected](I. Saliterer), [email protected](S. Korac). Contents lists available at ScienceDirect Critical Perspectives on Accounting jo u rn al ho m epag e: ww w.els evier.c o m/lo cat e/cp a 1045-2354/$ – see front matter ß 2013 Elsevier Ltd. All rights reserved. http://dx.doi.org/10.1016/j.cpa.2013.08.001

Transcript

Critical Perspectives on Accounting 24 (2013) 502–517

Contents lists available at ScienceDirect

Critical Perspectives on Accounting

jo u rn al ho m epag e: ww w.els evier .c o m/lo cat e/cp a

Performance information use by politicians and public

managers for internal control and external accountabilitypurposes

Iris Saliterer *, Sanja Korac

Alpen-Adria-Universitat Klagenfurt, Universitatsstraße 65-67, Room E.248, 9020 Klagenfurt, Austria

A R T I C L E I N F O

Article history:

Received 9 January 2012

Received in revised form 1 June 2012

Accepted 20 August 2012

Available online 21 August 2013

Mots cles:

Gestion des performances

Responsabilite

Nouvelle gestion publique

Gouvernance

Palabras clave:

Gestion del rendimiento

Responsabilidad

Nueva gestion publica

Gobernanza

Keywords:

Performance management

Accountability

New Public Management

Governance

A B S T R A C T

Governance structures have changed fundamentally since the beginning of New Public

Management inspired reforms. Particularly local public service delivery nowadays can be

characterized as diversified and fragmented, leading to internal management and external

accountability challenges for politicians as well as public managers. In this context the use of

performance information is seen as a crucial element for effectively dealing with both issues.

Nevertheless, empirical research considering different actors and contexts within one study

is rare. The present paper fills this gap by applying a multi-theoretical perspective and testing

hypotheses on the antecedents of performance information use by politicians and public

managers for internal management as well as external accountability purposes in small- and

medium sized local governments in Austria. The study results show that both groups use

performance information to a greater extent within external accountability relationships

than for internal management purposes. Results further illustrate that driving factors show

similarities for both groups with reference to the latter mentioned purpose, while a more

diverse picture is shown regarding factors impacting their use behavior toward citizens and

supervisory authorities.

� 2013 Elsevier Ltd. All rights reserved.

1. Introduction

Under the umbrella of the global NPM movement, governance structures, patterns of responsibility, and modes of controlhave changed fundamentally as governments externalize or contract out services, sell agencies to the private sector, createquasi-markets and decentralize functions to local authorities, often leading to fragmented public service delivery systems(Hood, 1995; Rhodes et al., 1997). Moreover, boundaries between public, private, and third sector organizations havebecome blurred as the delivery of public services is increasingly characterized by hybrid forms of organization, variouslydescribed as partnerships, collaborations, networks, alliances and, most prominently, as public-private partnerships(Agranoff and McGuire, 2003; Kooiman, 2003; Salamon and Elliott, 2002). These changes in governance structures challenge

I. Saliterer, S. Korac / Critical Perspectives on Accounting 24 (2013) 502–517 503

traditional accountability meanings, mechanisms, and relationships (Pina, 2007), and furthermore foster the shift towardsaccountability based on performance (Heinrich, 2002; Behn, 2003). The re-design of the traditionally cash based budgetingand accounting systems and the introduction of managerial accounting and performance indicators are therefore seen asessential elements in dealing with these accountability challenges and in enhancing the efficiency and effectiveness of publicorganizations (e.g. also De Lancer, 2006; Guthrie et al., 2005; Hood, 1991, 1995; Pollitt, 2006b). In particular, performanceorientation has reached new prominence within NPM-oriented reform processes (Van Dooren, 2008) and still ranks high onthe reform agenda of various countries and in public management research. In recent years, we have observed a shift of focusto the question of whether, and how, ‘newly’ available accounting and performance information is being used by differentstakeholder groups inside and outside public sector organizations (Arnaboldi and Azzone, 2010; Askim, 2007; Ho, 2005;Liguori et al., 2012; Melkers et al., 2000; Van Dooren et al., 2008). Nevertheless there is still a lack of quantitative empiricalevidence, addressing factors driving performance information use (PIU) by local government actors for internal managementand external accountability purposes. In order to enhance research from that point of view, the aim of this paper is toempirically test the impact of different factors on PIU for different purposes in a fragmented local service delivery context, byconsidering two actor groups – politicians with executive power (mayors) and public managers (chief officials). Therefore, itprovides the opportunity to analyze potentially existing trade-offs regarding the universal adoption of performancemeasurement for different purposes, internal performance improvement and external accountability, (Ammons andRivenbark, 2008), as well as for different actor groups. Both issues have mainly been treated separately to date in the area ofquantitative research (Liguori et al., 2012).

The remainder of the article is structured as follows. First, an introduction on the use of performance information, ananalysis of the existing literature, and a critical review of empirical studies dealing with PIU is outlined. In a next stepdifferent theoretical perspectives dealing with the antecedents of PIU are discussed, before hypotheses regarding the impactof different factors on PIU are developed within the third section. A view on the background of Austrian local governments isprovided where it can contribute to the understanding of hypotheses development and context specialities. In the followingsection, the nationwide e-mail triggered survey as well as the operationalization of the variables is illustrated, and thedescriptive figures are presented. Subsequently, findings of the empirical analysis are described and discussed, and in a laststep conclusions are synthesized, and finally, possible implications and limitations of the study are depicted.

2. Literature review, theoretical perspectives

2.1. PIU – what, who and what for?

Based on definitions proposed by other researchers in this field, performance information in this paper context ischaracterized as data and evidence that is produced, collected, and used to judge the performance of an organization (e.g.Guthrie and English, 1997; Pollitt, 2006b; Thiel and Leeuw, 2002). In the public sector, performance is regarded as amultidimensional concept ranging from concerns about increases in efficiency, effectiveness, output quantity and quality,productivity, equity, fairness, responsiveness to service needs, trust, citizen and consumer satisfaction (Lee, 2008; Walkeret al., 2010).

Different authors have recognized ‘implementation in the sense of use’ of performance information as the most difficult –but crucial – aspect of reforms, as individuals are required to undergo behavioral changes and widen as well as deepen thescope of information to be taken into account (De Lancer and Holzer, 2001; Hatry, 2002; OECD, 2005; Torres et al., 2011; VanDooren, 2008). In their enduringly influential work on the utilization of performance management in public organizations,De Lancer and Holzer (2001) differentiate between the stages of adoption and implementation. Within the adoption stage,the focus lies on building the capacity to act, meaning the development of accurate performance measures, which leads todifferent levels of performance information availability. Actual PIU levels for different purposes, however, represent theimplementation stage of utilization. Many research scholars working in this stream point at the gap between the productionand the use of performance information (e.g. Pollitt, 2006b; Ter Bogt, 2004). De Lancer and Holzer (2001) were at theforefront of authors pointing to the importance of considering and distinguishing between both sides of the coin, the supplyside and demand side of performance management (Askim, 2007, 2009; Ter Bogt, 2003). Hatry (2006) differentiates betweenperformance measurement and performance management, which also seems to reflect the above mentioned two aspects ofutilization, where the latter is concerned with using performance information effectively for a variety of purposes(Moynihan, 2008). According to this, the present study treats PIU as the expression of whether performance management isworth the effort, since the introduction of ‘full blown performance management systems’ is based on the assumption thatindividuals can use the information to make better decisions (Cavalluzzo and Ittner, 2004; Taylor, 2009). As a consequence,this will lead to enhanced performance and a better compliance with external accountability requirements and ultimately toimproved outcomes for society (Torres et al., 2011). This assumption also covers two critical aspects in empirically orientedperformance management research: (1) PIU for better managerial decision-making to enhance performance, and (2) PIU fordemonstrating and/or improving external accountability. Most studies in this field are more or less explicitly founded on adecision-based framework, in which the objective of management control systems is to provide information that is useful foreconomic decisions (Ijiri, 1983). The main focus of these studies therefore lies on exploring the internal use of performanceinformation for budget formulation and resource allocation, employee steering and motivation, setting goals and objectives,evaluation and control, strategic planning, establishing contracts, and for decisions in general (Askim, 2007; Melkers and

I. Saliterer, S. Korac / Critical Perspectives on Accounting 24 (2013) 502–517504

Willoughby, 2005; Moynihan and Pandey, 2010; Taylor, 2009). Also applying a rational perspective, some authors focus onthe economic usefulness or functionality (Poister and Streib, 1999) of available performance information in decision making(Yang and Hsieh, 2007). This primary focus is surprising, as performance measurement is often interpreted as a toolanswering the long history of calls for accountability (De Lancer, 2006; Lee, 2008). This in fact is interpreted as one of thecentral objectives of democratic governments, but is far from being a clear and simple concept (Sinclair, 1995).Categorizations and typologies have been developed and presented in the literature (Behn, 2003; Day and Klein, 1987;Sinclair, 1995) and most authors describe its meaning as complex, evolving, and constantly changing (Pollitt, 2006b;Robinson, 2003), depending on governance styles, the actors involved, and broad or narrow definitions. Given the papercontext, for the accountability purpose, we explicitly focus on ‘accountability for performance’ (Stewart, 1984; Behn, 2001;Lee, 2008; De Lancer, 2006; Robinson, 2003; Carnegie and West, 2005) from a directional perspective. Applying this view,there seems to be a broad consensus synthesized by Ijiri (1983) and Pollitt (2003), that accountability is a relationship inwhich one party, the accountee, recognizes an obligation to explain and justify their conduct to another, the accountor. Inthis relation the objective of performance management may alter, and fairness and adequacy of information flows can beconsidered as important topics (De Lancer, 2006; Ijiri, 1983). Therefore PIU for internal management purposes as well as inaccountability relations with actors outside local governments is included in our study, limiting the focus to communicationprocesses with supervisory authorities at the federal state level, and with citizens. Within these relationships, ‘formerdecision-makers’ change their roles and become suppliers of performance information, while citizens and supervisoryauthorities become its users. In this context, not only possible variances between the influences of factors on PIU for differentpurposes are at the point of interest, but also for different actors groups; specifically, politicians and public managers at thelocal government level. From a classical perspective and also within NPM, a normative division of their roles – althoughchanging – is made and politicians and public managers are thought to be driven by different rationalities, acting in differentand separated spheres (e.g. also Liguori et al., 2011, 2012). Nevertheless, more recent empirical studies challenge theseassumptions (Liguori et al., 2011, 2012; Svara, 1998, 2006). Including both groups therefore further enhances the presentstudy, as research in this field has largely concentrated on PIU by public managers (Heinrich, 2003; Lee, 2008; Moynihan andPandey, 2010; Taylor, 2009; Yang and Hsieh, 2007), while much less attention has been paid to its use by politicians (Askim,2007, 2009; Flury and Schedler, 2006; Ho, 2006; Schedler, 2003).

2.2. Theoretical perspectives on the antecedents of PIU

Various authors aimed to contribute to explaining the introduction of NPM-oriented management control systems, suchas accrual accounting, management accounting, and the introduction of performance measures (e.g. Anessi-Pessina et al.,2010; Berman and Wang, 2000; Lueder, 1992; Luder, 2002; Lueder and Jones, 2003), clearly limiting their focus to theadoption stage or supply side of these systems. Few authors explicitly aimed to contribute to explaining the use ofinformation provided by these systems and therefore addressing the implementation stage or their demand side. In a publicperformance management context some qualitative studies (Askim, 2007, 2009; Torres et al., 2011) and an even smallernumber of quantitative studies attempt to systematically analyze different environmental, organizational, and individualpredictors for PIU (De Lancer and Holzer, 2001; Johansson and Siverbo, 2009; Lægreid et al., 2008; Melkers and Willoughby,2005; Moynihan and Pandey, 2010; Taylor, 2009; Yang and Hsieh, 2007). The latter draw on a variety of theoreticalperspectives, although some studies do not explicitly link their arguments to theoretical bases.

A clearer picture in dealing with the variety of theoretical perspectives, one which possibly enhances theunderstanding of factors driving PIU, can be attained by structuring them into environmental, inter-organizational,intra-organizational, and individual approaches. Contingency theory and new institutional sociology can be consideredas important research streams (Chenhall, 2003; Modell, 2009) within this field, offering insights into the effects ofenvironmental factors and institutions. While contingency theory offers explanations from an economic or rationalperspective and therefore can be considered as a functionalist approach (Chenhall, 2003; Ter Bogt, 2008), newinstitutional sociology deals with characteristics and social processes (e.g. Meyer and Rowan, 1977), wherebymanagement control systems in public organizations are adopted and operated (e.g. for example Brignall and Modell,2000; Ezzamel et al., 2007; Lapsley and Wright, 2004; Ter Bogt and van Helden, 2000). Thus it broadens the concept ofeconomic rationality allowing the inclusion of social as well as other aspects (Ter Bogt, 2003). Applying a morefunctionalist inter-organizational control perspective, based on new institutional economics, Johansson and Siverbo(2006) discuss the impact of outsourcing on the utilization of relative performance evaluations at the local governmentlevel in Sweden. Nevertheless, many studies criticize the neglect of internal processes within new institutionalsociology (Burns and Scapens, 2000; Hengel et al., 2010; Ribeiro and Scapens, 2006), contingency theory (Chenhall,2003) and new institutional economics (Ter Bogt, 2008). Some authors therefore suggest the application of an originalinstitutional economics perspective, dealing with intra-organizational routines and their institutionalizations (Burnsand Scapens, 2000; Ter Bogt, 2008), while Chenhall (2003, p. 157) suggests that ‘advances in contingency-basedresearch will be best served by developing and refining theory within its organizational core’. In this sense, Moynihanand Pandey (2010) treat PIU as organizational behavior, where actors have discretion about whether and the degree towhich they use performance information, although they are influenced by their social context and the formal systems inwhich they work (Moynihan and Pandey, 2010). This approach allows the integration of environmental variables as wellas variables from the organizational core. In addition, from a micro-perspective or individual approach, concepts

I. Saliterer, S. Korac / Critical Perspectives on Accounting 24 (2013) 502–517 505

deriving from organizational psychology contribute to the understanding of PIU, as the consideration of individualcharacteristics can enhance predictions in this field (Askim, 2007; Chenhall, 2003; Moynihan and Pandey, 2010). Someauthors include variables without clearly linking them to theory, as they aim to build and empirically test ‘middle rangetheories’ and therefore apply variables, which emerged as significant factors in former studies (Moynihan and Pandey,2010; Yang and Hsieh, 2007). An increasing number of authors, however, explicitly apply a multi-theoretical approach(Johansson and Siverbo, 2009; Lægreid et al., 2006) considering the weaknesses of single theories in explaining acomplex phenomenon. As the present paper aims to identify factors that can create a satisfactory explanation for thePIU of two actor groups and for different use purposes, we take up this approach and apply a multi-theoreticalperspective, looking upon them as complementary rather than competitive (see Collin et al., 2009; Falkman andTagesson, 2008; Neu and Simmons, 1996).

3. Conceptualizing PIU in a fragmented local service delivery context

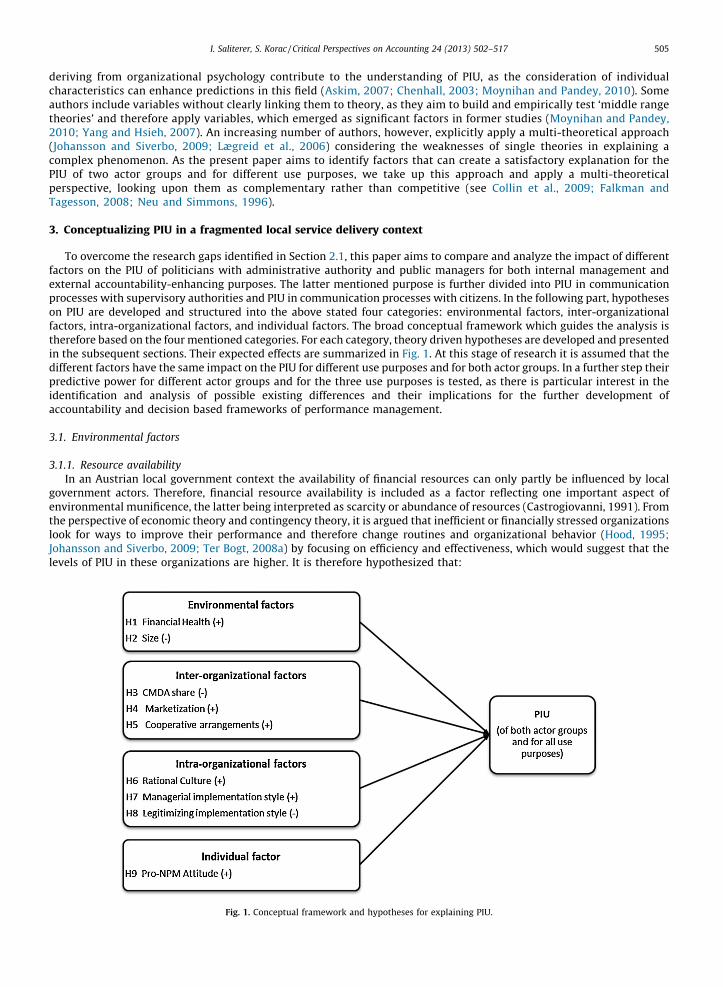

To overcome the research gaps identified in Section 2.1, this paper aims to compare and analyze the impact of differentfactors on the PIU of politicians with administrative authority and public managers for both internal management andexternal accountability-enhancing purposes. The latter mentioned purpose is further divided into PIU in communicationprocesses with supervisory authorities and PIU in communication processes with citizens. In the following part, hypotheseson PIU are developed and structured into the above stated four categories: environmental factors, inter-organizationalfactors, intra-organizational factors, and individual factors. The broad conceptual framework which guides the analysis istherefore based on the four mentioned categories. For each category, theory driven hypotheses are developed and presentedin the subsequent sections. Their expected effects are summarized in Fig. 1. At this stage of research it is assumed that thedifferent factors have the same impact on the PIU for different use purposes and for both actor groups. In a further step theirpredictive power for different actor groups and for the three use purposes is tested, as there is particular interest in theidentification and analysis of possible existing differences and their implications for the further development ofaccountability and decision based frameworks of performance management.

3.1. Environmental factors

3.1.1. Resource availability

In an Austrian local government context the availability of financial resources can only partly be influenced by localgovernment actors. Therefore, financial resource availability is included as a factor reflecting one important aspect ofenvironmental munificence, the latter being interpreted as scarcity or abundance of resources (Castrogiovanni, 1991). Fromthe perspective of economic theory and contingency theory, it is argued that inefficient or financially stressed organizationslook for ways to improve their performance and therefore change routines and organizational behavior (Hood, 1995;Johansson and Siverbo, 2009; Ter Bogt, 2008a) by focusing on efficiency and effectiveness, which would suggest that thelevels of PIU in these organizations are higher. It is therefore hypothesized that:

Fig. 1. Conceptual framework and hypotheses for explaining PIU.

I. Saliterer, S. Korac / Critical Perspectives on Accounting 24 (2013) 502–517506

H1. Greater resource availability has a negative impact on the PIU of both actor groups and for all use purposes

3.1.2. Size

Within their work on accounting innovations, Anessi-Pessina et al. (2010) discuss the factor of size by applying acontingent as well as a new institutionalist perspective and treat this aspect as organizational as well as environmentalfactor. Within the former, size reflects organizational complexity, which may hinder innovations in accounting (Lueder,1992). The above mentioned authors expand Lueders’ (1992) contingency model and consider size as a proxy fororganizational complexity as well as external visibility. Applying a contingency perspective within this paper, size isconsidered as an aspect reflecting environmental complexity as it is assumed that higher population levels also increase thediversity of groups to be provided with local government services (e.g. Dess and Beard, 1984). From this point of view, localgovernment actors demand greater quantities of information, which in turn may foster PIU. By further applying a newinstitutionalist perspective where a larger organization is more visible externally, the expectation is that greater attentionwill be paid to performance information, as this behavior is considered as desirable (Anessi-Pessina et al., 2010). Followingthe described argumentation it is assumed that from both theoretical perspectives:

H2. Larger size has a positive impact on PIU of both actor groups and for all use purposes

3.2. Inter-organizational factors

3.2.1. Governance re-structuring strategies

In most OECD countries, local services are produced and delivered by a variety of actors nowadays. The traditional form oflocal service delivery through departments of municipal core governments (unity of administration) is therefore steadilydecreasing. Researchers in this field are developing typologies to gain a clearer and more accurate picture of this ‘diversifiedand plural institutional landscape’ (Grossi and Reichard, 2008, p. 600), e.g. reflecting the grade of externalization of publicservice provision. Although different forms of externalization to other public sector utilities have always played animportant role in Austria, this field was actuated within the last two decades. Many authors point at the challenges of inter-organizational control resulting from NPM-oriented reform strategies, but only a few empirical studies deal with the impactof changing governance structures on performance management utilization (Cristofoli et al., 2010; Johansson and Siverbo,2009) by applying a functionalist control perspective. From a contingency perspective, fragmented service delivery reflectscomplexity in general and heterogeneity in particular (Khandwalla, 1972). In the present paper, it is defined as localgovernment re-structuring strategies for offering products and services to the population, resulting in diversity and ingeneral a greater demand for performance information. To obtain a clearer picture of changing governance structures at thelocal government level, findings from prior research dealing with new ways of ‘managing, organizing and delivering services’(Walker, 2006, p. 317) are applied and three relevant types of innovation, which have an impact on governance structures atthe local government level, are identified. The different types are discussed within the study context of the local governmentlevel in Austria in the following, as it is essential for ‘understanding similarity and difference, continuity and change’ inpublic management research (Pollitt and Bouckaert, 2009, p. 193).

3.2.2. Corporations with market-determined activities

According to the constitution, every municipality in Austria is an independent economic entity and has the right toestablish commercial enterprises in order to fulfil its tasks in an efficient way. In this context the founding of corporationswith market-determined activities (CMDA) as one possible form of organization has increased. These quasi-corporationsare public law based, without their own legal status but with a special statute as well as a manager. Local governmentactors, like the mayor and the local council, formally remain the key decision-makers and are board members of the CMDA.Besides carrying out market-determined activities, CMDAs must demonstrate economic and financial behavior similar toprivate corporations, and have to generate a turnover which covers more than 50 per cent of the production costs. EveryCMDA has an obligation to record a verification of assets and liabilities and to enclose a capital statement based onrecognizing depreciation according to the income tax law. They are treated as separate accounting entities, but theiraccounting is fully integrated with the budgeting and accounting systems of their local governments. The latter are liablefor all CMDA activities and therefore have both governance and financial interests (Christensen et al., 2002). In this contextit has to be recognized that the establishment of CMDAs is not mainly a result of NPM-inspired movements but has gainedmomentum in view of the need to formally comply with the Maastricht criteria, which became binding for Austria from thetime of its EU membership in 1995. Given the latter argument it is assumed that, although CMDAs are somewhat underpressure to reach the cost criterion, a high share of CMDA revenues has a negative impact on PIU. According to newinstitutional sociology (Meyer and Rowan, 1977, 1991) formally triggered changes probably do not affect internal routinesand processes. From our viewpoint, this governance re-structuring approach can also be regarded as maintaining strategy(Pollitt and Bouckaert, 2004), which means that new (public) management ideas are widely rejected or ignored. Insummary, it is predicted that:

H3. A high share of CMDAs has a negative impact on PIU of both actor groups and for all use purposes

I. Saliterer, S. Korac / Critical Perspectives on Accounting 24 (2013) 502–517 507

3.2.3. Marketization of local service delivery

Within the utility sector, but also within culture and the arts, local governments have transferred service delivery tocorporations, which operate under public or private law and have a legally self-standing status, in contrast to CMDAs. Localgovernments still retain governance and/or financial interest, reflected by their extent of ‘share based participation’ or‘political based participation’ (Krujif, 2011, p. 47). Externalization by contracting out to private sector organizationsconcentrates on service provision in the fields of waste management, social and health care, recreational facilities, andregional development. From an economic perspective, these changes require the development and use of formal, resultsand output oriented control mechanisms (Lapsley and Pallot, 2000; Johansson and Siverbo, 2009, 2011) that allow localgovernments to ‘steer the external entities towards the fulfilment of public interest’ (Cristofoli et al., 2010, p. 351).Regarding the marketization or external autonomization (Ter Bogt, 1999, 2003a) of public service delivery it is thereforepredicted that:

H4. Higher grades of marketization of local services have a positive impact on PIU of both actor groups and for all usepurposes

3.2.4. Cooperative arrangements in local service delivery

Since 1971 the law has offered opportunities for inter-communal cooperation, with inter-communal associations actingas the most prominent organizational form of coordination (Pleschberger, 2003); in other countries these are known asconsortiums (Grossi and Reichard, 2008). In the area of water supply, sewerage disposal, and garbage collection this form iswidely practiced and predominantly mandatory by state law, with the states being responsible for determining the details ofthe institutional settings. According to the trend in other countries, more voluntary forms of inter-communal cooperationhave been re-introduced and public–public partnerships and public–private partnerships have gained increasing popularity.These developments result in shared forms of accountability, leading to challenges with regard to the development ofmeaningful control mechanisms. Partnerships are often set up to solve problems that cannot be solved, or are solvedinefficiently or ineffectively by single organizations (Agranoff and McGuire, 2003), so that the mutual trust of the partnersplays an important role. Given the latter arguments it is assumed that the underlying reasons for the establishment ofpartnerships, e.g. increase in efficiency, effectiveness, or cost reduction, are strong promotors of PIU. As trust can beencouraged with information sharing (Johansson and Siverbo, 2011) it is therefore hypothesized that:

H5. Higher grades of cooperative arrangements have a positive impact on PIU of both actor groups and for all use purposes

3.3. Intra-organizational factors

3.3.1. Organizational culture

Many scholars treat organizational culture as a key variable in developing control systems and interpret efficient controlas a result of fit between culture and the ‘formal’ system in place (Ouchi, 1979; Henri, 2006). Quinn and Rohrbaugh (1983)developed an organizational culture model, which is comprised of two dimensions and allows the identification of fourorganizational culture types, which are more or less dominant in organizations. To our knowledge, an increasing number ofstudies within quantitative public performance measurement research focuses on the influence of a certain type oforganizational culture on PIU (De Lancer and Holzer, 2001; Johansson and Siverbo, 2009; Moynihan and Pandey, 2010). Weexplicitly focus on aspects of rational culture, which describes the attempt to achieve ‘certain ends by choosing appropriatemeans on the basis of the facts of the situation’ (Weber, 1978). As it is associated with control values reflecting an orientationtoward efficiency and the primary emphasis is upon planning, productivity, and goal setting as well as goal clarity (Krakowerand Zammuto, 1991; Quinn and Rohrbaugh, 1993), it is proposed that:

H6. A higher degree of rational culture has a positive impact on PIU of both actor groups and for all use purposes

Authors of the original-institutional-economics stream analyze the processes through which management accountingrules and routines come to be institutionalized in the organization (Burns and Scapens, 2000; Scapens, 1994). From thisperspective, change processes have the most direct and initial effect on formal rules or technical aspects and a more indirector diffuse impact on (management accounting) routines, here interpreted as organizational performance managementimplementation style (Burns and Scapens, 2000). From our viewpoint, the latter is closely connected to and/or influences theattitude toward performance management in general, and therefore is also a reliable predictor for individual PIU. Differentaspects hence are included in the study, reflecting the respondents’ perceived organizational instrumental use andusefulness, as well as the relevance of implemented performance indicators, within their organizational context (Ho, 2006;Melkers and Willoughby, 2005; Taylor, 2009; Walker et al., 2010; Yang and Hsieh, 2007). The identified implementationstyles (see data and method section) presumably have significant but different impacts on PIU:

H7. Managerial implementation style has a positive impact on PIU of both actor groups and for all use purposes

H8. Legitimizing implementation style has a negative impact on PIU of both actor groups and for all use purposes

I. Saliterer, S. Korac / Critical Perspectives on Accounting 24 (2013) 502–517508

3.4. Individual factors

3.4.1. Pro-NPM values

Typical personal characteristics such as age, tenure, or education have been widely explored in a performancemeasurement context, but continue to offer mixed results (Askim, 2008; Melkers and Willoughby, 2005; Moynihan, 2005a).Within this study, the primary focus is on the attitude and belief systems of mayors and chief officials, more precisely theirvalues linked to NPM-inspired movements (Gaebler and Osborne, 1992; Hood, 1991; Schedler, 2007), especially to thedimensions of innovativeness and achievement, which ought to be measured by specific performance indicators (Meiri andVigoda-Gadot, 2008). These values are reflected by the items used in a pro-innovation attitude scale developed byDamanpour and Schneider (2008), which measures managers’ attitudes towards competition and entrepreneurship in apublic service delivery context. The authors found that managers favoring these aspects are more likely to stay withincomplex innovation projects until their successful implementation. In this special issue also English (2013) highlights theimportance of individual values in forming, accepting or resisting accountability regimes. That is why it is predicted that:

H9. Pro-NPM attitudes have a positive impact on PIU of both actor groups and for all use purposes

A synthesis of the developed hypotheses is presented in Fig. 1.

4. Data, methodology, and measurement

Reiterating the aim of the paper, it is to examine the influence of a number of factors on PIU for different purposes of twodifferent actor groups at the top tier level of Austrian local governments. Within this section the survey sample is discussed,followed by the description of the operationalization of dependent and independent variables. The data is analyed by meansof descriptive statistics and factor analysis. In a further step, ordinary least square regression is chosen as statistical methodto test the developed hypotheses and is presented and discussed in the results section.

4.1. Sample and data collection

The primary data source for the empirical part of the paper is a nationwide e-mail triggered online survey of small andmedium-sized local governments (99.9 per cent of all local governments) in Austria. Within the present paper, small andmedium sized local governments are classified according to their population figures, ranging from 1 to 25,000, Regardingtheir annual budget and number of employees, this group of governments can also be compared to small and medium sizedenterprises (SME), their governance structures however show the same complex characteristics as large stock-listedcompanies. Nevertheless, the definitions of small, medium or large local governments strongly depend on the context of thecountry observed. The remaining 17 large local governments were not included because of differences in roles andresponsibilities of the possible informant groups as well as the small number within this size classification, the lattergenerating problems within quantitative analysis. Therefore, this is one of the rare studies which focus on smaller localgovernments, the latter being widely neglected in empirical performance management research (Rivenbark and Kelly, 2006).The informant groups for the survey were mayors and chief officials. Mayors were selected as they are endowed with almosttotal administrative authority for a variety of tasks, including representation of the local government, management of thelocal administrative office, and preparation and execution of the budget – although the latter must be approved by thecouncil. Mayors can therefore be seen as key actors carrying out not only political but also administrative functions(Avellaneda, 2008; Svara, 2006). Most local governments in Austria also have a chief official who supervises departmentchiefs, coordinates departments, prepares the budget and also has a strong advisory function regarding legal, financial, andorganizational issues. The chief official’s influence on local government performance can therefore be considered as high,although it is heavily dependent on the type of mayor-manager interaction (Svara, 2006). Data for the objective measures,financial health and share of CMDA, were collected from the official local government annual financial reports from 2006 to2009. Population figures for the year 2010 were obtained from Statistics Austria.

In a first step, the e-mail addresses for the informant groups were accessed via the 2340 local government homepages, asno central database exists. The lack of direct mail addresses of contact persons, which was a selection criterion, reduced thenumber of respondents in the target population. Thus, on average, the direct e-mail addresses were available in 62 per cent ofall cases for mayors and in 56 per cent for chief officials. These addresses were finally included in the survey. Finally, therespondent rate of 20 per cent for mayors and 26 per cent includes 509 (n) usable instruments for the regression analysis.Some of the non-responding local governments state that the survey is not applicable to them for the following reasons: newin the organization, shared employees with other local governments, the position is vacant, technical problems, no time forsurveys in general or length of survey. As this only affects a small number of cases (17), it has no impact on the study results.A summary of the sample characteristics and the profile of the respondents (Kober et al., 2010) are provided in Table 1.

4.2. Operationalization of the dependent variable

To measure PIU, three dependent variables are applied, questioning mayors’ and chief officials’ perceived intensity of PIU.The latter is operationalized by providing concrete examples for efficiency, effectiveness, internal learning and development

Table 1

Sample characteristics and profile of respondents.

Chief officials Mayors

Sample information

Initial sample 1318 1460

Less: survey returned as wrong addresses 45 109

Less: other reasons 9 8

Final sample 1264 1343

Responses received 335 274

Responses perceived % 27 20

Profile of the respondents

Average age 45–50 yrs 50–55 yrs

Male 83% 92%

Female 17% 8%

Private sector experience 63% 82%

I. Saliterer, S. Korac / Critical Perspectives on Accounting 24 (2013) 502–517 509

and citizen satisfaction measures, for internal management purposes and within two external accountability relationships.Taking into account the results from previous studies, only the above mentioned higher-order measures are included, as simpleoutput or workload measures do not adequately reflect the performance of organizations (Ammons and Rivenbark, 2008).

For internal management purposes (management model), PIU is measured by constructing a summative indicator of twoitems – controlling for results and monitoring/steering employees – with a Cronbach Alpha of .77 for mayors and .70 for chiefofficials. External accountability is measured by applying two variables, PIU in communication processes with citizens(citizen model), and communication with supervisory authorities (audit model) outside of the local governments. Bothvariables are single-item measures. Although there is some criticism of single-item measures’ reliability in representingconstructs based on different facets or measuring psychological constructs, utilization of these in measurements of self-reported facts or perception is a commonly accepted practice (e.g. Bergkvist and Rossiter, 2007; Moynihan and Pandey, 2010;Wanous et al., 1997). For the purpose of the presented study, one-item measures used to measure self-reported facts aretherefore considered as a marginal reliability problem. All items are based on a seven point Likert scale. The descriptiveresults for the two actor groups are presented in Table 4 at the beginning of the results and discussion section.

4.3. Operationalization of independent variables and measures

4.3.1. Environmental factors

Financial health consists of three measures, namely own-revenue share, current balance or operating ratio, and debtrepayment time, which are considered as valid and reliable predictors for local governments’ resource capacity (Kloha et al.,2005b). The measures were calculated from official local governments reports for the years 2006 to 2009, and resulted in adichotomous construct of below average (0), and above average (1), each. The summative measure ranged on a scale frombad (0) to good condition (3). Size is operationalized using the logarithm of population figures from 2010.

4.3.2. Inter-organizational factors

Governance factors are depicted by three variables, the degree of CMDA, marketization, and partnership. Tooperationalize the CMDA degree, an index variable was developed and calculated from local government reports for the years2006–2009, reflecting the ratio of CMDA revenues to total local government revenues. Regarding the other governancevariables, the respondents were asked to rate the degree (on a 1–5 Likert scale) to which the specific types of innovations hadbeen at the forefront of their local government reform strategies during recent years. Authors of previous studiesdifferentiate between marketization and ancillary innovations (e.g. Walker, 2006), and apply three to four measures forthese constructs. Marketization innovations herein include two items, externalization of local services to other public sectororganizations and contracting out services to the private sector. With .70 for mayors and .71 for chief officials, the Cronbach’sAlpha reaches a sufficient level (Nunnally and Bernstein, 1994), this being comparable to the results obtained by Walker(2006). The ancillary innovation category is also considered as a single-item measure, meaning the development of strategiclocal and regional partnerships (Walker, 2006).

4.3.3. Intra-organizational factors

In the model presented here, three organizational factors are included, all comprised of multiple items. Rational culture ismeasured by using three adapted items from Krakower and Zammuto (1991). Respondents had to state to what extent theyagreed to the following: ‘‘my local government considers efficiency and effectiveness as guiding principles’’, ‘‘my localgovernment is highly production and goal oriented’’, ‘‘my local government has a strong focus on continuous improvementin our service’’. A seven point Likert scale is used and an aggregated index is computed using the scale point values for eachitem. A Cronbach’s Alpha of .80 for mayors and .75 for chief officials indicates good internal reliability.

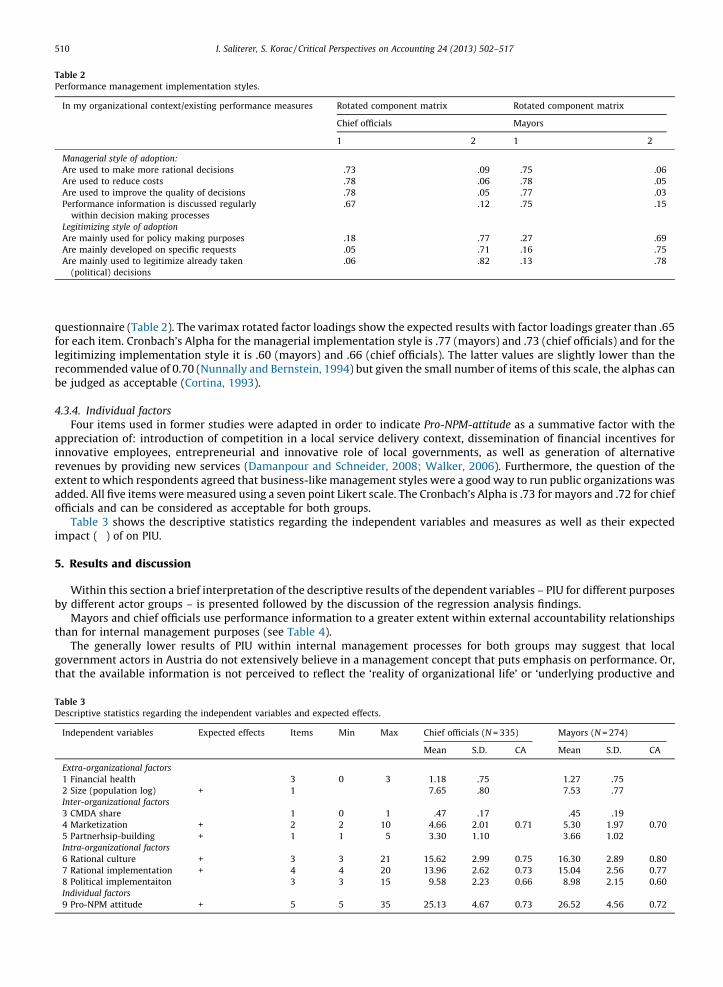

Two composite measures for performance management implementation styles – managerial implementation style andlegitimizing implementation style – are created and tested by applying an explorative factor analysis to seven items of the

Table 2

Performance management implementation styles.

In my organizational context/existing performance measures Rotated component matrix Rotated component matrix

Chief officials Mayors

1 2 1 2

Managerial style of adoption:

Are used to make more rational decisions .73 �.09 .75 �.06

Are used to reduce costs .78 �.06 .78 �.05

Are used to improve the quality of decisions .78 .05 .77 �.03

Performance information is discussed regularly

within decision making processes

.67 �.12 .75 �.15

Legitimizing style of adoption

Are mainly used for policy making purposes �.18 .77 �.27 .69

Are mainly developed on specific requests .05 .71 .16 .75

Are mainly used to legitimize already taken

(political) decisions

�.06 .82 �.13 .78

I. Saliterer, S. Korac / Critical Perspectives on Accounting 24 (2013) 502–517510

questionnaire (Table 2). The varimax rotated factor loadings show the expected results with factor loadings greater than .65for each item. Cronbach’s Alpha for the managerial implementation style is .77 (mayors) and .73 (chief officials) and for thelegitimizing implementation style it is .60 (mayors) and .66 (chief officials). The latter values are slightly lower than therecommended value of 0.70 (Nunnally and Bernstein, 1994) but given the small number of items of this scale, the alphas canbe judged as acceptable (Cortina, 1993).

4.3.4. Individual factors

Four items used in former studies were adapted in order to indicate Pro-NPM-attitude as a summative factor with theappreciation of: introduction of competition in a local service delivery context, dissemination of financial incentives forinnovative employees, entrepreneurial and innovative role of local governments, as well as generation of alternativerevenues by providing new services (Damanpour and Schneider, 2008; Walker, 2006). Furthermore, the question of theextent to which respondents agreed that business-like management styles were a good way to run public organizations wasadded. All five items were measured using a seven point Likert scale. The Cronbach’s Alpha is .73 for mayors and .72 for chiefofficials and can be considered as acceptable for both groups.

Table 3 shows the descriptive statistics regarding the independent variables and measures as well as their expectedimpact (�) of on PIU.

5. Results and discussion

Within this section a brief interpretation of the descriptive results of the dependent variables – PIU for different purposesby different actor groups – is presented followed by the discussion of the regression analysis findings.

Mayors and chief officials use performance information to a greater extent within external accountability relationshipsthan for internal management purposes (see Table 4).

The generally lower results of PIU within internal management processes for both groups may suggest that localgovernment actors in Austria do not extensively believe in a management concept that puts emphasis on performance. Or,that the available information is not perceived to reflect the ‘reality of organizational life’ or ‘underlying productive and

Table 3

Descriptive statistics regarding the independent variables and expected effects.

Independent variables Expected effects Items Min Max Chief officials (N = 335) Mayors (N = 274)

I. Saliterer, S. Korac / Critical Perspectives on Accounting 24 (2013) 502–517 511

interpersonal processes’ and is therefore neglected (Ahrens, 1996, p. 153; Roberts and Scapens, 1985, p. 453). To ourknowledge, until now only one empirical study dealt with the perceived usefulness of performance measurement of mayorswith administrative authority. It concludes that the main benefits lie in an improved citizen-oriented communication andenhanced accountability (Ho, 2005), which somewhat supports our findings. It is remarkable that the results for chiefofficials in all use categories are significantly lower than those for mayors and therefore stand in contradiction to the resultsfrom a scant number of studies, which found that politicians rarely use performance information within decision-makingcontexts (Askim, 2007; Flury and Schedler, 2006; Ho, 2005; Moynihan, 2005a; Ter Bogt, 2003). However, these studies,except for that by Moynihan (2005a) and Ho (2005), deal with PIU for internal management purposes, and focus onpoliticians without administrative authority. Another possible explanation may be that chief officials are not that involved incitizen communication and internal management processes or have a more realistic view, while mayors tend to overstatePIU in their local government context.

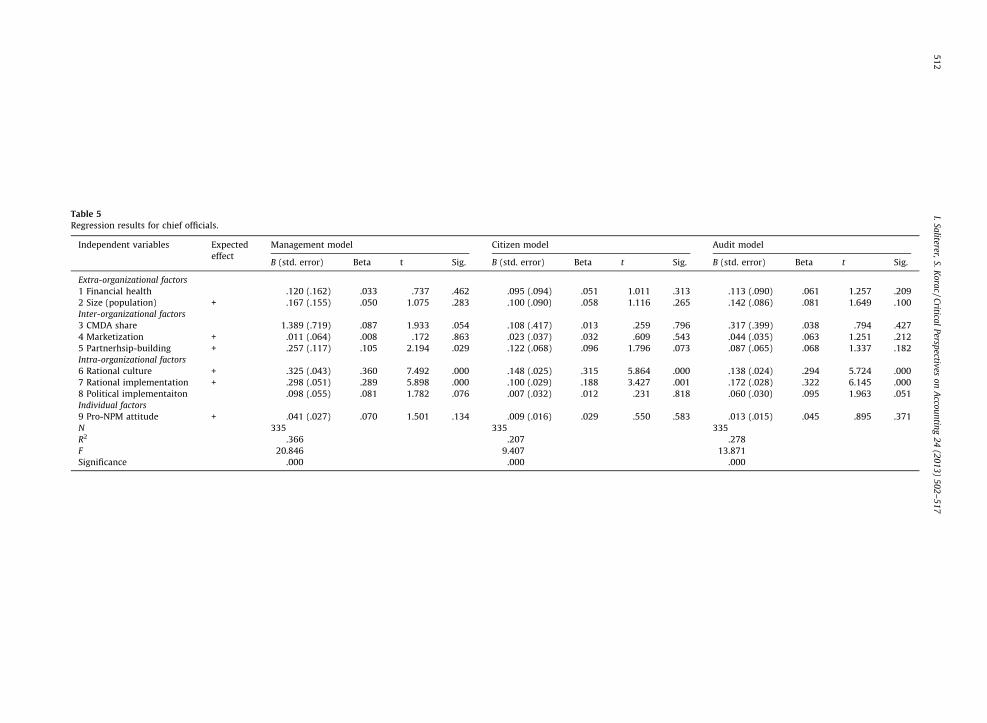

To further examine the influence of the previously described factors on PIU for both respondent groups, six regressionmodels are developed and tested, reflecting the different purposes of PIU mentioned earlier. To determine whether OrdinaryLeast Square was appropriate, data was examined for heteroscedasticity and multicollinearity, both returning satisfyingresults. All models achieve good rates for multicollinearity and no Variance Inflation Factor (VIF) higher than 1.47 wasreported in the models. The results of the six multiple regressions are presented in Tables 5 and 6.

The management models provide the highest explanatory power, with an adjusted R2 of .33 for mayors and .35 for chiefofficials. The explained variance in the citizen and audit models ranges from .17 to .27, and their explanatory level can beinterpreted as moderate within empirical performance management research. A quick glance across all models revealsrational culture to be the most consistent and effective predictor factor, while environmental factors play no significant role.A detailed and structured interpretation of the results will be at the centre of the following sections, in line with the order ofthe developed hypotheses.

5.1. Environmental factors

Environmental factors such as fiscal stress show the expected but non-significant impact on PIU of mayors and chiefofficials in five out of six regression models and turned out to be significant in the audit model of mayors. Size showed anunexpected negative but non-significant impact in nearly all models. Within the audit model of mayors and chief officialsthis impact turned out to be significant, meaning that in larger local government organizations, both groups are usingperformance information to a lesser extent within this relationship. The hypothesis regarding size, based on new-institutional sociology and contingency theory, therefore has to be rejected in a PIU context at the local government level inAustria. The significant negative impact may be better explained by the expanding capacity of mayors and chief officials inlarger local governments in Austria. In this case, they are supported by a greater number of staff, the latter being responsiblefor the communication with supervisory authorities or their greater power and independence with regard to supervisorybodies of federal states. Moreover, the roles and responsibilities of actors at the top tier level of local governments probablychange with increasing size, leading to lower PIU levels.

5.2. Inter-organizational factors

Governance factors had no significant impact on PIU (H3–H5), although they sometimes showed effects in an unexpecteddirection. A high share of corporations with market-determined activities (CMDAs) only showed the significant expectedeffect in the citizen model of mayors. One possible interpretation may lie in the mainly ‘formal’ reasons for the founding ofCMDAs, with the aim to reduce the budget deficit in order to comply with the Maastricht criteria. From a control perspective,this result seems to be problematic, as it indicates that mayors may not feel responsible for the performance of these quasi-corporations, even though they are affiliated with local governments. This situation points to possible negative effects onaccountability, as the mean share of CMDA is about 45% of total income regarding the provision of own local services andthese organizations are based on diffuse regulations allowing a great deal of room for interpretation. Nevertheless, due to itslow significance, hypothesis 3 had to be rejected in all other models although mainly pointing in the expected direction.Higher grades of externalization and contracting-out of local services showed an expected and positive significant effect on

Table 5

Regression results for chief officials.

Independent variables Expected

effect

Management model Citizen model Audit model

B (std. error) Beta t Sig. B (std. error) Beta t Sig. B (std. error) Beta t Sig.

I. Saliterer, S. Korac / Critical Perspectives on Accounting 24 (2013) 502–517514

PIU (H4) by mayors for internal management purposes, but had no impact in all chief official models. The influence ofpartnership building shows a diverse picture for mayors and chief officials. Higher grades of cooperative arrangements areshown to lead to lower PIU by mayors for internal management purposes as well as in both accountability contexts, whichcontradicts H5, while for chief officials it shows the expected positive effect in all models. These results can probably bepartly explained by the different roles of politicians and public managers in collaboration contexts. It is possible that chiefofficials have a different understanding of and focus on partnerships, which are built to provide tangible local services. At thesame time, mayors probably focus on more strategic and informal forms with the aim of improving regional or localdevelopment. The first mentioned are often built to reach higher levels of efficiency and effectiveness and thereforearguments concerning these performance dimensions may play a significant role within an internal management as well asexternal accountability context. Strategic partnerships are often more outcome-oriented and diffuse, therefore going wellbeyond organizational borders. As performance measures within this dimension are generally rare, this would be anexplanation for the negative impact on PIU levels of mayors. However, these lines of argument can only remain best guessesin the context of this quantitative study, but can provide a starting point for further in-depth qualitative surveys.

5.3. Intra-organizational factors

Intra-organizational factors such as rational culture show the expected positive effects on PIU (H7) by mayors for internalmanagement purposes and in the accountability relationship with citizens, while this is an important PIU fostering factor forchief officials in all models. Therefore the results largely confirm the findings from previous studies (De Lancer and Holzer,2001; Moynihan and Pandey, 2010). The impact of implementation styles shows a highly diverse picture, where themanagerial style of implementation is a clearly significant factor in enhancing PIU by chief officials in all models (H8), butshows a slightly different picture for mayors. Here, it significantly fosters the PIU for internal management purposes andwithin the accountability relationship to supervisory bodies, but not in communication processes with citizens. Resultsregarding the positive impact of the perceived managerial value of organizational performance information use thereforelargely support the assumption described and contribute to the further validation of this aspect (Askim, 2007; Melkers andWilloughby, 2005; Taylor, 2009). The findings also show that chief officials who think that performance measures are mainlyused for policy-making purposes or to legitimize political decisions in their organizational context (H9) tend to useperformance information to a significantly lesser extent for internal management purposes. The results in the managementmodel of mayors point in the same direction, although they are not significant. The unexpected significant positive impact ofthe legitimizing implementation style of chief officials on PIU within the supervisory accountability relationship isnoteworthy. It indicates some sort of dysfunctional behavior based on distortion of information, like gaming, filtering orsmoothing, as this relationship is based on a more diagnostic or mandated use of performance measurement (Brignall andModell, 2000; Henri, 2006, Habersam et al., 2013).

5.4. Individual factors

A pro-NPM-attitude shows the positive significant effect on PIU only in external accountability relationships of mayors,while the hypothesis has to be rejected in all other models. The strong influence of NPM-values on PIU in the citizen modelmay indicate that mayors who tend to be more entrepreneurial and market-oriented are more actively engaged in usingperformance information, exploiting information as evidence for their claims (Moynihan, 2008). This conclusion is alsosupported by the irrelevance of both implementation styles in the citizen model of mayors.

6. Conclusion

This study empirically investigated the impact of different factors on the PIU of politicians with administrative authorityand public managers for different, internal management as well as accountability enhancing purposes. Although focusing onsmall and medium sized local governments in Austria, some general conclusions regarding the theoretical contributions andpractical implications can be derived from our results.

By comparing the results for politicians and managers from a more general perspective, it can be observed that PIU forinternal management purposes is mainly driven by the same intra-organizational factors for both groups. Moreover, in thisregard all intra-organizational factors show an impact in the expected direction. This picture changes fundamentally andbecomes fuzzy, when looking at the results regarding the impact of intra-organizational factors on PIU withinaccountability relationships for both groups. The differences between the factors driving PIU for internal managementpurposes and PIU for external accountability purposes in the mayor models are noteworthy, as both performancemanagement implementation styles turned out to be non-significant in the accountability towards citizens model. Theresults for chief officials also show a diverse picture, particularly with reference to the contradicting results regarding theimpact of the legitimizing implementation style on PIU for internal management purposes, and in communicationprocesses with supervisory authorities. It is reasonable to conclude that an original institutional economics perspective,which offers the theoretical basis for the hypotheses on the impact of different implementation styles in our study, clearlyhas the potential to advance the understanding in this field of research, although the results discussed differ with regard tothe use purpose.

I. Saliterer, S. Korac / Critical Perspectives on Accounting 24 (2013) 502–517 515

Organizational culture turned out to be an omnipresent driving factor within all models. Going back to the theoreticalassumptions we can therefore conclude that the inclusion of organizational culture seems to be a promising avenue forrefined contingency based research in this field (Chenhall, 2003; Henri, 2006). Nevertheless, the contingency and newinstitutional theory based hypotheses regarding the impact of environmental factors on PIU have not been confirmed.These results may indicate that a complex behavioral phenomenon like PIU cannot be broadly explained by theories that donot reach as far as the organizational core or by factors which are too unspecific for the field of interest (Van Helden, 2000).The inter-organizational hypotheses are mainly based on contingency (complexity) and economic (control) theory.Partnership building, albeit a significant driving factor, showed contradicting results for mayors and chief officials, and alsothe hypotheses on the two other externalization strategies have only been partly confirmed. The results can therefore beconsidered as diffuse and indicate that the impact of (changing) governance structures needs greater attention andattention of a different kind in future research aiming at explaining PIU (Ter Bogt, 2003; Cristofoli et al., 2010; Caker andSiverbo, 2011; Johansson and Siverbo, 2011). Nevertheless, the impact of inter-organizational factors shows the mostcoherent picture within the internal management models for both groups, which may indicate that changing governancestructures have stronger implications for managerial decision making than for accountability enhancing purposes.Individual factors, herein represented by the pro-NPM values of informants, show a significant positive impact only forexternal accountability purposes for mayors. The significant positive impact of a pro-NPM attitude and the non-significance of implementation styles within communication processes with citizens indicate that PIU of politicians withinexternal accountability relationships are presumably driven by different personal values and characteristics; aspectswhich needs attention in future investigations. In this special issue, Mutiganda (2013) used a promising approach forenhancing knowledge in this field. The author extends the old institutional economics perspective by using critical realismand discuss the role of the accountability identity of accountees for their behavior in accountability relationships. Insummary, it seems reasonable to conclude that the underlying theoretical assumptions concerning inter-organizationaland intra-organizational factors fit better into a ‘‘decision-based-framework’’ than an ‘‘accountability-based-framework’’of PIU. This conclusion is further supported by the results regarding the positive impact of the legitimizing implementationstyle on PIU of chief officials within communication processes with supervisory authorities. Also, it indicates a limitation ofthe study with reference to causality problems of some factors (Van Helden, 2000). The results should also be interpreted inthe context of the following study limitations. As previously stated, like most studies which try to predict different factorson a dependent variable, it suffers from a ‘causality issue’ regarding some variables. In future studies this problem can bepartially solved by using longitudinal designs based on panel data and time-lagged correlations to more adequatelyaddress causality (Kim, 2004).

In general, although the hypotheses are built on theories from different fields and the results offer promising findings,there is a need for further development. Moreover, as this study concentrates on small and medium sized local governmentsin Austria, where local government actors face the challenge of a mainly voluntary and unguided implementation of publicmanagement reforms, it would be interesting to test the different factors, particularly different styles of implementation andthe impact of changing governance structures, in other (country) contexts to draw more general conclusions.

References

Agranoff R, McGuire M. Collaborative public management: new strategies for local governments. Washington: Georgetown University Press; 2003.Ahrens T. Styles of accountability. Account Org Soc 1996;21(2–3):139–73.Ammons DN, Rivenbark WC. Factors influencing the use of performance data to improve municipal services: evidence from the North Carolina benchmarking

project. Public Admin Rev 2008;68:304–18.Anessi-Pessina E, Nasi G, Steccolini I. Accounting innovations: a contingent view on Italian LGs. J Public Budget Account Finan Manage 2010;22(1/2).Arnaboldi M, Azzone G. Critical perspectives on accounting constructing performance measurement in the public sector. Crit Perspect Account 2010;21:266–82.Askim J. Local government by numbers: who makes use of performance information, when, and for what purposes?. Oslo: Unipub; 2007. PhD thesis.Askim J. Determinants of performance information utilization in political decision making. In: van Dooren W, van de Walle ST, editors. Performance information in

the public sector. How it is used. Basingstoke: Palgrave Macmillan; 2008. p. 125–39.Askim J. The demand side of performance measurement: explaining councillors’ utilization of performance information in policymaking. Int Public Manage J

2009;12(1):24–47.Avellaneda CN. Municipal performance: does mayoral quality matter? J Public Admin Res Theory 2008;19(2):285–312.Behn B. Rethinking democratic accountability. Washington, DC: Brookings; 2001.Behn R. Why measure performance? Different purposes require different measures Public Admin Rev 2003;63(5):586–606.Bergkvist L, Rossiter JR. The predictive validity of multiple-item versus single-item measures of the same constructs. J Market Res 2007;44:175–84.Berman E, Wang X. Performance measurement in US counties: capacity for reform. Public Admin Rev 2000;60(5):409–20.Brignall S, Modell S. An institutional perspective on performance measurement and management in the ‘new public sector’. Manage Account Res 2000;11:

281–306.Burns J, Scapens RW. Conceptualizing management accounting change: an institutional framework. Manage Account Res 2000;11:3–25.Carnegie GD, West BP. Making accounting accountable in the public sector. Crit Perspect Account 2005;16(7):905–28.Cavalluzzo KS, Ittner CD. Implementing performance measurement innovations: evidence from government. Account Org Soc 2004;29:243–67.Caker M, Siverbo S. Management control in public sector joint ventures. Manage Account Res 2011;22(4):330–48.Chenhall RH. Management control systems design within its organizational context: findings from contingency-based research and directions for the future.

Account Org Soc 2003;28:127–68.Christensen T, Laegreid P, Wise LR. Transforming administrative policy. Public Admin 2002;80(1):153–78.Collin SO, Tagesson T, Andersson A, Cato J, Hansson K. Explaining the choice of accounting standards in municipal corporations. Crit Perspect Account

2009;20(2):141–74.Cortina JM. What is coefficient alpha? An examination of theory and applications J Appl Psychol 1993;78:98–104.Cristofoli D, Ditillo A, Liguori M, Sicilia M, Steccolini I. Do environmental and task characteristics matter in the control of externalized local public services?

Unveiling the relevance of party characteristics and citizens’ offstage voice Account Audit Account J 2010;23(2):350–72.

I. Saliterer, S. Korac / Critical Perspectives on Accounting 24 (2013) 502–517516

Damanpour F, Schneider M. Characteristics of innovation and innovation adoption in public organizations: assessing the role of managers. J Public Admin ResTheory 2008;19(3):495–522.

Day P, Klein R. Accountabilities: five public services. London: Tavistock; 1987.De Lancer JP. Performance measurement: an effective tool for government accountability? The debate goes on Evaluation 2006;12(2):219–35.De Lancer JP, Holzer M. Promoting the utilization of performance measures in public organizations: an empirical study of factors affecting adoption and

implementation. Public Admin Rev 2001;61:693–708.English L. The impact of an independent inspectorate on penal governance, performance and accountability: pressure points and conflict ‘‘in the pursuit of an ideal

of perfection’’. Crit Perspect Account 2013.Ezzamel M, Hyndman N, Johnsen A, Lapsley I, Pallot J. Experiencing institutionalization: the development of new budgets in the UK devolved bodies. Account

Audit Account J 2007;20(1):11–40.Falkman P, Tagesson T. Accrual accounting does not necessarily mean accrual accounting: factors that counteract compliance with accounting standards in

Swedish municipal accounting. Scand J Manage 2008;24(3):271–83.Flury R, Schedler K. Political versus managerial use of cost and performance accounting. Public Money Manage 2006;26(4):229–34.Gaebler T, Osborne D. Reinventing government: how the entrepreneurial spirit is transforming the public sector. New York: Plume; 1992.Grossi G, Reichard CH. Municipal corporatization in Germany and Italy. Public Manage Rev 2008;10(5):597–617.Guthrie J, English L. Performance information and programme evaluation in the Australian public sector. Int J Public Sector Manage 1997;10(3):154–64.Guthrie J, Petty RM, Ricceri F. External intellectual capital reporting: contemporary evidence from Hong Kong and Australia. J Intell Capital 2005;6(4):510–27.Habersam M, Piber M, Skoog M. Knowledge balance sheets in Austrian universities: the implementation, use, and re-shaping of measurement and management

practices. Crit Perspect Account 2013.Hatry HP. Performance measurement: fashions and fallacies. Public Perform Manage Rev 2002;25(4):352–435.Hatry HP. Performance measurement: getting results. Washington: Urban Institute; 2006.Heinrich CJ. Outcomes-based performance management in the public sector: implications for government accountability and effectiveness. Public Admin Rev

2002;62(6):712–25.Heinrich CJ. Measuring public sector performance and effectiveness. In: Peters BG, Pierre J, editors. The handbook of public administration. London: Sage; 2003. p.

25–37.Hengel HV, Tjerk BT, Tom G. Different use of performance indicators between hierarchical levels in Dutch municipalities – an institutional approach; 2010.Henri JF. Management control systems and strategy: a resource-based perspective. Society 2006;31:529–58.Ho ATK. Accounting for the value of performance measurement from the perspective of midwestern mayors. J Public Admin Res Theory 2005;16:217–37.Ho ATK. Accounting for the value of performance measurement from the perspective of city mayors. J Public Admin Res Theory 2006;16:217–37.Hood C. A public management for all seasons. Public Admin 1991;69:3–19.Hood C. The ‘‘new public management’’ in the 1980s: variations on the theme. Account Org Soc 1995;20(2–3):93–109.Ijiri Y. On the accountability-based conceptual framework of accounting. J Account Public Policy 1983;2(2):75–81.Johansson T, Siverbo S. Governing cooperation hazards of outsourced municipal low contractibility transactions: an exploratory configuration approach. Manage

Account Res 2011;22(4):292–312.Johansson T, Siverbo S. Explaining the utilization of relative performance evaluation in local government: a multi-theoretical study using data from Sweden. Finan

Account Manage 2009;25(2):197–224.Khandwalla PN. The effect of different types of competition on the use of management controls. J Account Res 1972;275–85.Kim S. Individual-level factors and organizational performance in government organizations. J Public Admin Res Theory 2004;15(2):245–326.Kloha P, Weissert CS, Kleine R. Someone to watch over me. State monitoring of local fiscal conditions. Am Rev Public Admin 2005b;35(3):313–23.Kober R, Lee J, Ng J. Mind your accruals: perceived usefulness of financial information in the Australian public sector under different accounting systems. Finan

Account Manage 2010;26(3):267–98.Kooiman J. Governing as governance. Thousand Oaks, CA: Sage; 2003.Krakower JY, Zammuto RF. Quantitative and qualitative studies of organizational culture. Res Org Change Dev 1991;5:83–114.Kruijf JMD. Controlling externally autonomised entities by Dutch local governments. Int J Product Perform Manage 2011;60(1):41–58.Lægreid P, Roness PG, Rubecksen K. Performance management in practice: the Norwegian way. Finan Account Manage 2006;22(3):251–70.Lægreid P, Roness PG, Rubecksen K. Performance information and performance steering: integrated system or loose coupling. In: van Dooren W, van de Walle ST,

editors. Performance information in the public sector. How it is used. Houndmills: Palgrave Macmillan; 2008.Lapsley I, Pallot J. Accounting, management and organizational change: a comparative study of local government. Manage Account Res 2000;11:213–29.Lapsley I, Wright E. The diffusion of management accounting innovations in the public sector: a research agenda. Manage Account Res 2004;355–74.Lee J. Preparing performance information in the public sector: an Australian perspective. Finan Account Manage 2008;24(2):117–49.Liguori M, Sicilia M, Steccolini I. Politicians and administrators: two characters in search for a role. In: International Research Society for Public Management.

2011.Liguori M, Sicilia M, Steccolini I. Some like it non-financial. politicians’ and managers’ views on the importance of accounting information. Public Manage Rev

2012.Lueder K. Contingency model of governmental accounting innovations in the political administrative environment. Res Gov Nonprof Account 1992;7:99–127.Luder K. Research in comparative governmental accounting over the last decade: achievements and problems. In: Montesinos V, Vela JM, editors. Innovations in

governmental accounting. Boston: Kluwer Academic Publishers; 2002. p. 1–21.Lueder K, Jones R. Reforming governmental accounting and budgeting in Europe. Frankfurt am Main: Fachverlag Moderne Wirtschaft; 2003.Meiri S, Vigoda-Gadot E. New public management values and person-organization fit: a socio-psychological approach and empirical examination among public

sector personnel. Public Admin 2008;86(1):111–32.Melkers JE, Willoughby KG, Implementing PBB. Conflicting views of success. Public Budget Finan 2000;20(1):105–20.Melkers JE, Willoughby KG. Models of performance-measurement use in local governments: understanding budgeting, communication, and lasting effects. Public

Admin Rev 2005;65(2):180–91.Meyer JW, Rowan B. Institutionalized organizations: formal structure as myth and ceremony. Am J Sociol 1977;83(2):340–63.Modell S. Institutional research on performance measurement and management in the public sector accounting literature: a review and assessment. Finan

Account Manage 2009;25(3):277–304.Moynihan DP. Why and how do state governments adopt and implement ‘managing for results’ reforms? J Public Admin Res Theory 2005a;15(2):219–43.Moynihan DP. Advocacy and learning: an interactive-dialogue approach to performance information use. In: van Dooren W, van de Walle ST, editors. Performance

information in the public sector. How it is used. Houndmills: Palgrave Macmillan; 2008.Moynihan DP, Pandey SK. The big question for performance management: why do managers use performance information? J Public Admin Res Theory

2010;20(4):849–66.Mutiganda JC. Budgetary governance and accountability in public organisations: an institutional and critical realism approach. Crit Perspect Account 2013.Neu D, Simmons C. Reconsidering the ‘‘social’’ in positive accounting theory: the case of site restoration costs. Crit Perspect Account 1996;7(4):409–35.Nunnally JC, Bernstein IH. Psychometric theory. New York: McGraw-Hill; 1994.OECD. Modernising government: the way forward. Paris: OECD; 2005.Ouchi WG. A conceptual framework for the design of organizational control mechanisms. Manage Sci 1979;25(9):833–48.Pina V. Are ICTs improving transparency and accountability in the EU regional and local governments? An empirical study Public Admin 2007;12(9):277–472.Pleschberger W. Cities and municipalities in the Austrian political system since the 1990s. New developments between ‘efficiency’ and ‘democracy’. In: Kersting

N, Vetter A, editors. Urban research international: reforming local government in Europe. Opladen: Leske & Budrick; 2003. p. 113–36.Poister TH, Streib G. Performance measurement in municipal government: assessing the state of the practice. Public Admin Rev 1999;59(4):325–35.

I. Saliterer, S. Korac / Critical Perspectives on Accounting 24 (2013) 502–517 517

Pollitt C. Joined-up government: a survey. Polit Stud Rev 2003;1:34–49.Pollitt C. Performance management in practice: a comparative study of executive agencies. J Public Admin Res Theory 2006b;16(1):25–44.Pollitt CH, Bouckaert G. Continuity and change in public policy and management. Cheltenham, UK/Northampton, MA: Edward Elgar; 2009.Quinn RE, Rohrbaugh J. A spatial model of effectiveness criteria: towards a competing values approach to organizational analysis. Manage Sci 1983;29:363–77.Rhodes RAW. Understanding governance. Policy networks, governance, reflexivity and accountability. Maidenhead: Open University Press; 1997.Ribeiro JA, Scapens RW. Institutional theories in management accounting change: contributions, issues and paths for development. Qual Res Account Manage

2006;3:94–111.Roberts J, Scapens R. Accounting systems and systems of accountability - understanding accounting practices in their organisational contexts. Account Org Soc