21

Asset Liability Management performance metrics and risk attribution Charles Gilbert, FSA, FCIA, CFA, CERA

December 4, 2008

Asset Liability Managementperformance metrics and risk attribution

Charles Gilbert, FSA, FCIA, CFA, CERA

Asset Liability Management

Review of traditional approach

Developments in the risk management landscape

Integrating ALM with Enterprise Risk Management

Performance metrics and risk attribution

Performance metrics and risk attribution

2

Leveraged liability cash flow profile

3

2008 2013 2018 2023 2028 2033 2038 2043 2048 2053 2058

Liability Cash Flow Profile

2008 2013 2018 2023 2028 2033 2038 2043 2048 2053 2058

In‐force Asset Cash Flow Profile

Traditional risk metricsMultiple dimensions of risk need to be measured

Probability weighted measures

Static exposure at risk measure provide limited information> Duration/convexity are based on simple premises and may give

false sense of comfort> Partial duration need to be supplement with covariance structure

Probability weighted measures prone to RAROC calculations> Allows quantification of yield curve “bets” within a principled risk

framework> Multi factor interest rate model or Principal Component Analysis

(PCA)Objectives of PCA> Reduce the number of explanatory variables> Find hidden patterns in data and simplify interpretation

Particularly useful in performing risk optimization

5

Traditional approach still prevalentAsset management executed separately

Focus of asset management is on assets> maximize total return> maximize book yield> simple ALM risk metrics

Investment (i.e. asset-only) objectives specified by insurance company / clientAssets managed and performance measured against benchmark> asset-only benchmark> liability-driven benchmark

Attribution performed against benchmark> active asset management decisions not explicitly measured

6

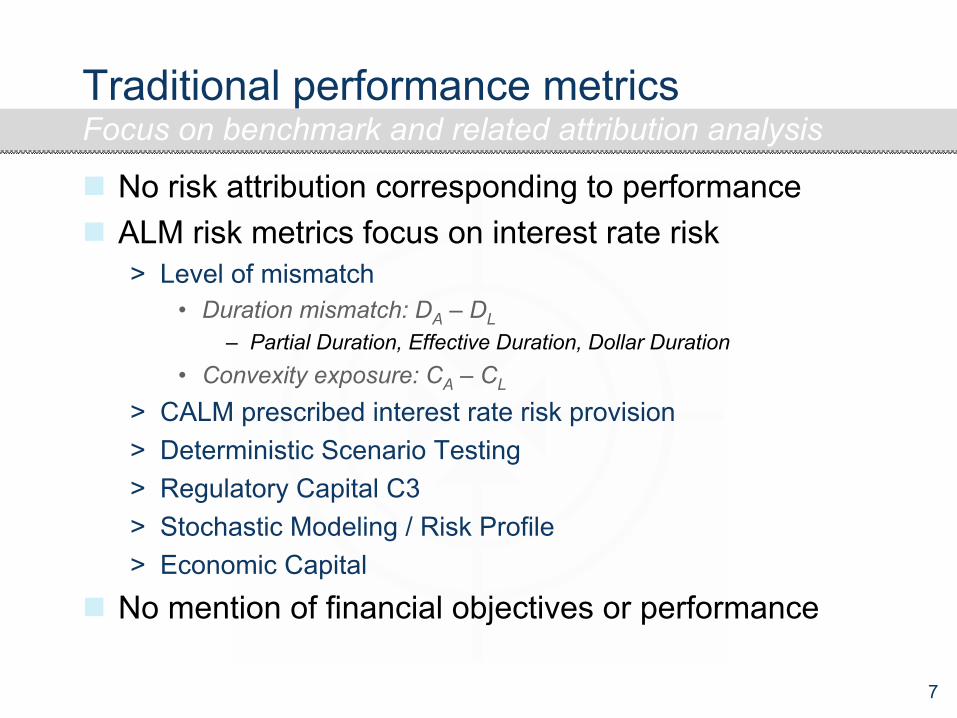

Traditional performance metrics

No risk attribution corresponding to performanceALM risk metrics focus on interest rate risk > Level of mismatch

• Duration mismatch: DA – DL– Partial Duration, Effective Duration, Dollar Duration

• Convexity exposure: CA – CL

> CALM prescribed interest rate risk provision> Deterministic Scenario Testing> Regulatory Capital C3> Stochastic Modeling / Risk Profile> Economic Capital

No mention of financial objectives or performance

Focus on benchmark and related attribution analysis

7

Shortcomings undermine performanceFinancial objectives are not being achieved

Fundamental flaw:Beating benchmark and/or achieving investment objectives does not necessarily mean financial objectives will be metNo separation of sources of value-added from ALM and active asset management decisionsCapital and risk-adjusted performance cannot be properly factored in> cannot evaluate whether fairly compensated for risks taken

8

Performance measures lack transparencyNot clear where value-added comes from

Active asset management bets not explicitly disclosed ex ante nor measured ex post

Unintended, implicit bets not recognized

Result – may reward a poorly matched position> E.g. interest rate exposure not from a deliberate view on rates

9

Conflicts between ALM and Asset ManagementResistance to moving away from traditional approach

Benchmark may be inappropriate> benchmark and or targets frequently oversimplified for benefit

of asset managerEntire process may cater more to needs of asset manager, not client > asset manager requires specification of investment objectives,

not financial objectives> asset manager requires benchmark and targets that may bear

little resemblance to actual liabilities> value-added ALM strategies may disrupt performance

measurement of asset managerTraditional asset management divorces assets from liabilities for benefit of asset manager

10

Developments in risk managementCompanies starting to execute ALM at strategic level

Rating Agencies and Regulators evaluating quality of risk managementRecent losses and failures drawing greater attention to effectiveness of risk managementGreater recognition of value of executing ERM as a strategic decision-making framework

11

Most companies run ALM at a tactical level Strategic ALM is not necessarily about eliminating risk

12

Integrating ALM with ERMALM conceptual framework consistent with ERM

Replace traditional benchmarks with actual liabilitiesReplace focus on narrow investment objectives with focus on overall financial objectivesChange process so that ALM drives investment decisions

13

ALM Conceptual FrameworkNeeded in order to execute ALM at strategic level

14

ERM defines how performance measuredPerformance metrics based on financial objectives

Performance metrics based on financial objectives> maximize accounting earnings (CGAAP, future earnings)> maximize embedded value (EEV, MCEV)> maximize economic surplus> maximize investment income / total return> minimize economic capital> minimize required regulatory capital

ALM attribution analysis focuses on change in performance metric over the period> quantifies impact on performance metric for each source of risk> most companies focus on change in interest rates for ALM

15

ALM attribution analysisCreates awareness of impact of financial variables

US Treasury Yield Curve

Economic Surplus BOP 111,673 Change due to Yield Curve 2,292 Change due to Liabilities (19,982)Change due to Assets 26,718 Total Change 9,028

Economic Surplus EOP 120,701

Change due to Assets 26,718New Business 14,399 Asset trades 2,244 Change due to aging of cash flows 10,075 Change due to assumptions changes -

Change due to Liabilities (19,982)New Business (12,413)Change due to aging of cash flows (7,569)Change due to assumptions changes -

16

ALM attribution analysisRecognizes sources of value added

Identify value from both ALM and active management > ALM strategies (excluding tactical credit views, security selection,

rate anticipation, etc)Active asset management can adds value on top of ALM optimized portfolio> Any bets (i.e., active positions) are recorded ex ante and

measured ex post – thus fully transparent> Measure actual value added from active management, not just

value against a benchmarkAttribution not restricted to a particular measurement basis > could be change in ES, accounting results or other financial

objective(s)Impact of passive position / prior period decisions / noise

17

Quantifying sources of value added

ALM attribution analysis is a valuable tool to separate the value added from ALM and asset managementALM strategies are on a default-free basisActive asset management can add further value by taking bets within risk limits

Incremental value added from active asset management

Impact of ALM StrategiesChange in ES Before Rebalance (5,045)Change in ES After Rebalance 9,028

Total 14,073

Impact of Active Asset ManagementChange in ES due to rate anticipation 1,213Change in ES due to credit selection 750

Total 1,963

18

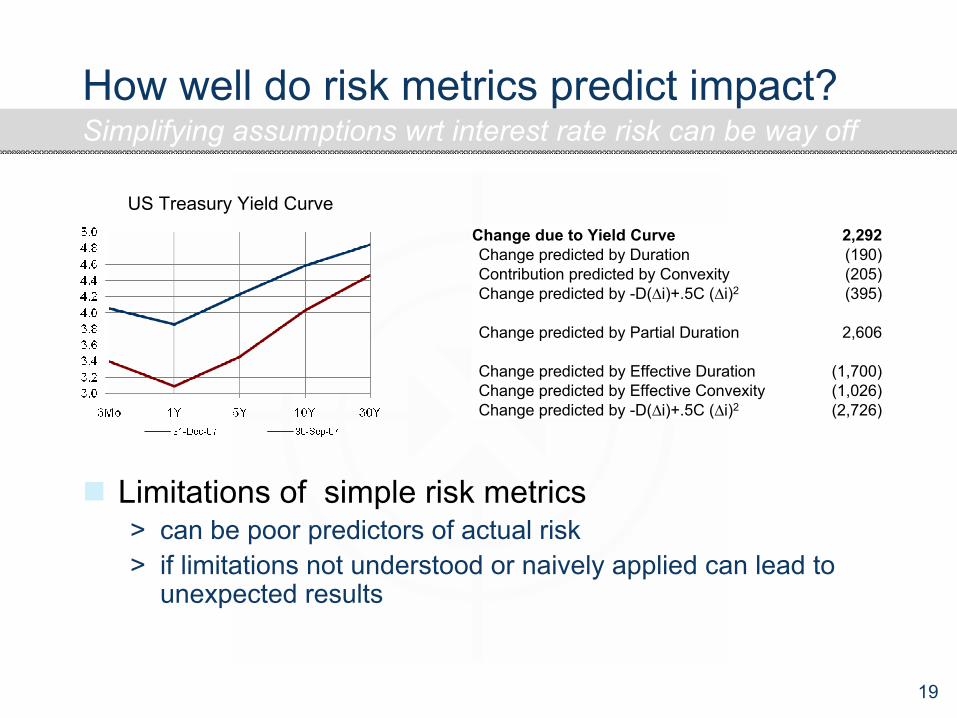

How well do risk metrics predict impact?

Change due to Yield Curve 2,292 Change predicted by Duration (190)Contribution predicted by Convexity (205)Change predicted by -D(∆i)+.5C (∆i)2 (395)

Change predicted by Partial Duration 2,606

Change predicted by Effective Duration (1,700)Change predicted by Effective Convexity (1,026)Change predicted by -D(∆i)+.5C (∆i)2 (2,726)

Simplifying assumptions wrt interest rate risk can be way off

US Treasury Yield Curve

Limitations of simple risk metrics > can be poor predictors of actual risk > if limitations not understood or naively applied can lead to

unexpected results

19

Attribution gives greater insight

Impact on financial objectives broken down by sourceBets are made explicit> duration or rate anticipation> credit selection> backing fixed income liabilities with non-fixed income assets

Value added by asset manager is transparentPerformance measurement is more meaningful but difficult to implement in practiceSome companies feel that performance measurement of asset management is less important than successful execution of ALM

Valuable tool to manage assets and liabilities

20

Thank You!

Contact info:Charles L. Gilbert, FSA, FCIA, CFA, CERANexus Risk Management+ 1 416 593 [email protected]

21