46 | MMI HOLDINGS INTEGRATED REPORT 2017 46 | MMI HOLDINGS INTEGRATED REPORT 2017 Performance We continue to invest in the capabilities we need to succeed in the world envisioned by the Fourth Industrial Revolution.

MMI’s purpose is to enhance the lifetime Financial Wellness of people, their communities and their businesses. This Financial Wellness purpose remains relevant in the current tough economic environment. Slow economic growth, shrinking disposable income and rising unemployment characterised the operating environment in 2017, increasing the financial pressure on consumers.

Although MMI had to deal with the challenges of the tough South African operating environment, we remain committed to our client-centric strategy and our Financial Wellness purpose. The MMI management team acted decisively to implement key strategic focus areas, balancing the investment required for a sustainable long-term future with shorter term priorities to ensure MMI’s core businesses continue to compete in South Africa. In the process we streamlined MMI’s corporate portfolio, reducing our African footprint and increasing the focus on MMI’s large existing businesses in South Africa.

We remain mindful of the exponential technology advances of the Fourth Industrial Revolution and continued to invest in the capabilities we need to succeed in the world envisioned by this revolution. Capabilities like data analytics, machine learning, design thinking, digital marketing and robotics will support our client-centric strategy and help us to build superior relationships with clients in a cost-effective manner.

OVERVIEW OF 2017

Environment and industry

2017 has been another challenging year for the financial services industry in South Africa. Political events impacted negatively on an already weak economy, and all key economic indicators in South Africa confirmed a picture of consumers who experienced more pressure on disposable income than in 2016. Business and consumer confidence indices were at historical low levels, fuelled by South Africa’s sovereign credit downgrade. The negative environment inevitably had a commensurate impact on MMI.

Strategic focus areas

MMI has three strategic focus areas to realise our vision to be the preferred lifetime Financial Wellness partner, with a reputation for innovation and trustworthiness. We define Financial Wellness to be a continuous process to assist people with planning and managing their money so that they can afford their expenses and reach their goals over their lifetime. All strategic activities throughout MMI are aligned to the focus areas of Client Centricity, Growth and Excellence. During 2017, we made good progress to achieve the strategic objectives in respect of all three strategic focus areas.

Nicolaas KrugerGroup chief executive officer

Although MMI had to deal with the challenges of the tough South

African operating environment, we remain committed to our

client-centric strategy and our Financial Wellness purpose.

48 | MMI HOLDINGS INTEGRATED REPORT 2017

Group chief executive officer's overview

Client Centricity

The successful execution of our strategic focus to understand and meet client needs was independently confimed by the latest South African Customer Satisfaction Index (SAcsi), which indicated that South African life insurance clients are the most satisfied with our Metropolitan brand, for the second year in a row. Metropolitan Retail aims to gain a deep understanding of the problems our clients face and then use new technologies to enable relevant solutions for clients, while protecting shareholder interests. For example, interventions that use data analytics shortened Metropolitan’s claims turnaround times from 48 hours to as little as 10 minutes.

To create value for MMI clients, our Multiply Wellness and Rewards programme educates, engages, empowers and encourages members for doing everyday things that ensure a physically and financially healthy lifestyle. Multiply continued its growth path during 2017 and now has over 250 000 clients and created value through improved persistency, higher cross-product holdings and a reduction in claims.

During 2017 we further refined the value propositions for all our South African client segments. We again measured the financial wellness of South African citizens through the Momentum Financial Wellness Index (in partnership with UNISA). The adverse impact of South Africa’s economic challenges on household finances was clear from the results of the Index and we will take account of these findings to enhance our client value propositions.

Growth

Our Health and Wellness joint venture with Aditya Birla in India was launched during November 2016 and we are very pleased with the progress made in the few months since the launch. Aditya Birla Health already received awards in respect of its product range and digital marketing campaigns, while total insured lives exceeded 200 000 by the end of the financial year. We also launched our micro-insurance JV with MTN in Uganda and Ghana during 2017 and we are gaining valuable insights.

Earlier in this overview I referred to the streamlining of MMI’s corporate portfolio outside South Africa. We have decided to significantly scale down our presence in the United Kingdom, and we have announced our plan to exit a number of African countries to improve focus on remaining operations. Our efforts in this regard have enabled more focused investment in our large South African businesses, in the capabilities required for the Fourth Industrial Revolution and in attractive new strategic growth initiatives in South Africa.

One of the attractive opportunities we are pursuing is the joint venture between MMI and African Bank. This partnership includes three business lines, comprising lending, insurance business and transactional banking. The lending venture will make it possible for MMI to offer needs-based credit to our

client base through various distribution channels and the insurance opportunity will enable African Bank to provide MMI insurance products to its client base through African Bank distribution channels. The transactional banking capabilities will further enable the MMI Financial Wellness client value proposition. The different components of the joint venture will be rolled out on a phased basis during the 2018 financial year.

In our existing South African businesses, we increased efforts to grow productive face-to-face channels for our Momentum Retail and Metropolitan Retail businesses, aiming to increase MMI’s client base. Good results have been achieved in respect of growth in the membership of the Momentum Health open scheme and growing our Momentum Short-term Insurance client base, where cross-selling and our Multiply Wellness and Rewards programme have been very effective. We also continued to invest in alternative distribution channels to support our omni-channel strategy.

Excellence

A critical initiative within our Excellence strategic focus area is MMI’s expense optimisation project. We are pleased that this project achieved its milestones and remains on track to achieve the 2019 target of R750 million in annual cost savings.

An important aspect of MMI’s client-centric strategy is to have leading Financial Wellness building blocks. There was a particular focus on turning around Momentum Short-term Insurance, which consistently improved from a new business premium, expense and claims ratio perspective. Momentum Short-term Insurance is closely tracking its business plans and aims to achieve sustainable profitability by 2019.

Strategic enablers

Earlier in this CEO overview I referred to our investment in the critical capabilities that will enable MMI to be successful in the new world of the Fourth Industrial Revolution. During 2017 significant headway has been made in respect of strengthening our strategic enablers, to build IT systems fit-for-purpose for the Fourth Industrial Revolution, improve data analytics skills, vest a client-centric culture and increase innovation.

In line with trends towards mobile client engagement, we released a first version of a Momentum mobile application. Momentum Health and Short-term Insurance applications will be included into one holistic Momentum mobile application during the next year, aligned to our Financial Wellness ambition. We also implemented Webchat functionality on all the Multiply pages on the www.momentum.co.za website. Further systems development to prepare MMI for the Fourth Industrial Revolution is underway.

MMI’s client-centric culture, the MMI Way was launched at a country-wide MMI executive (exco) roadshow. Following the MMI exco roadshow, we successfully completed an industrial

MMI HOLDINGS INTEGRATED REPORT 2017 | 49

INTRO

DU

CTION

ABO

UT U

SPERFO

RMA

NCE

GO

VERNA

NCE

REMU

NERATIO

NFIN

AN

CIAL STATEM

ENTS

theatre roadshow throughout the country to practically illustrate the MMI Way to all staff and internalise how to change their behaviours to align with the MMI Way. Our staff reacted very positively to the two roadshows and we will implement further initiatives to fully vest the behaviours and values of our culture.

Our innovation partnership with the United Kingdom venture capital firm Anthemis progressed well. We have evaluated a large number of potential Fintech and Insuretech start-ups in the Financial Wellness space and the first investments have been made. In South Africa our partnership with venture capital firm 4Di Capital has also made good progress and investments have been made on a similar basis. We continuously connect relevant start-ups and new technologies to the existing business of MMI, aiming to take advantage of their skills and capabilities to advance our strategy.

We continued to pursue internal innovation on an agile basis during the year, using design thinking and lean start-up methodologies to advance internal opportunities in a focused manner.

Financial performanceThe results of MMI for the financial year ended 30 June 2017 were impacted by the tough economic environment and the weak investment markets. Core headline earnings remained flat relative to the prior year. New business sales reduced by 6%, while new business margins reduced from 1.6% to 1.3%. We continued to invest in key strategic initiatives and expense management was very satisfactory. MMI’s capital base remains adequate.

For further details on the financial performance, please refer to the group finance director’s report on page 52.

Executive team

The MMI executive committee is a diverse and energised team and we are confident of our ability to lead MMI towards our Financial Wellness purpose.

MMI’s executive committee membership changed during 2017. The chief executive (CE) Momentum Retail business (Etienne de Waal), MMI’s chief operating officer (Danie Botes) and the group executive of brand (Vuyo Lee) resigned during the year. I would like to thank Etienne, Danie and Vuyo for the important contributions they have made to MMI on multiple fronts and wish them all the best.

Three new executives joined the MMI exco team, Linda Mthenjane as group executive of Human Capital, Ashlene van der Colff as head of group operations and Risto Ketola as chief financial officer. Our group finance director, Mary Vilakazi has accepted the responsibility of deputy CEO and Khanyi Nzukuma (previously CE of Metropolitan Retail) has accepted the responsibility to become CE of Momentum Retail.

Transformation

We remain committed to creating sustainable transformation in the South African economy and have maintained our Level 2 Contributor status. The new B-BBEE certificate was issued during May 2017 and I am very pleased with the score of 93.37 (125% B-BBEE recognition level). Transformation remains a critical building block to achieve our objective of enhancing Financial Wellness for all.

Looking aheadThe current challenging environment for both consumers and businesses is likely to prevail for some time, and technology advances will continue to change the business world. MMI’s client-centric strategy and investment in capabilities to succeed in the new world will position us to compete in the future. In the short term, MMI and our industry peers will remain subject to a tough and uncertain environment. Our strategic choices to streamline MMI’s corporate portfolio and focus on strengthening the large existing businesses in South Africa will help us to successfully navigate through this short-term cycle successfully, while setting MMI up for future success.

ThanksI would like to thank everyone involved with MMI for their contributions during the year. We appreciate the ongoing strategic guidance provided by the MMI board. We also appreciate the ongoing commitment and resilience of our executive management team and our MMI employees. I would also like to thank our shareholders and clients for their continued support. We look forward to journey with all of you on the way to a new world and Financial Wellness.

NICOLAAS KRUGERGroup chief executive officer

50 | MMI HOLDINGS INTEGRATED REPORT 2017

Group chief executive officer's overview (continued)

MMI HOLDINGS INTEGRATED REPORT 2017 | 51

INTRO

DU

CTION

ABO

UT U

SPERFO

RMA

NCE

GO

VERNA

NCE

REMU

NERATIO

NFIN

AN

CIAL STATEM

ENTS

IntroductionThis review provides a high-level overview of the group results. Additional financial disclosure can be found in the annual financial statements and additional operating performance information can be found in the segmental reports.

The results of MMI for the financial year ended 30 June 2017 reflect a difficult operating environment with the main financial metrics being under pressure. The following themes impacted on the financial results of the group:

• The balance sheet of the group is highly geared towards equity markets. Muted equity market growth over the past three years have impacted the level of asset based fees and discretionary margin releases, resulting in flat earnings year-on-year.

• Lower than expected underwriting profits remain a feature in the corporate group disability business. The underwriting results of the rest of the life insurance book recovered well from the previous financial year.

• The group’s International short-term insurance and health businesses continued to face headwinds, resulting in decisions taken to exit numerous businesses outside of South Africa to preserve the group’s capital resources going forward.

• The return on embedded value (ROEV) was impacted by negative investment variances resulting from weak market returns, lower than expected value of new business and the write down of asset valuations following the decisions to exit certain business lines and countries.

• Reasonable new business volumes given the tough economic environment but with new business margins under pressure.

The group’s various strategic initiatives are on track and are discussed in the CEO report.

Group performance scorecardMMI assesses its operational performance against a set of key performance indicators that are annually reviewed and approved by the group’s Remuneration Committee. The set of indicators include both short-term and long-term objectives.

Short-term deliverables are measured over a period of 12 months and are reviewed on an annual basis. The group set stretching targets for F2017 in line with the aspirational ROEV targets. For the financial year ended 30 June 2017, the following set of short-term deliverables applied to the group as a whole:

The group continued to experience tough operating conditions over the

past year that manifested in lower than expected earnings. Despite the

challenging conditions the group was able to secure solid new business

flows albeit at lower margins, while keeping a strong control

over expense growth.

Mary VilakaziDeputy chief executive officer and group finance director

Performance scorecard 2017Weight F2017 target Actual Achieved

Return on embedded value¹ 20% 12.2% 8.9% ↓Core headline earnings 20% 13% growth 0% ↓Value of new business 15% R801m R547m ↓Optimisation and expense savings programme 10% R200m R219m ↑Strategic initiatives 35% Exco assessment 3.4 (max 5.0) ↑

1 For the short term performance scorecard ROEV is measured excluding the impact of investment variances

52 | MMI HOLDINGS INTEGRATED REPORT 2017

Group finance director's report

The above scorecard relates to group-wide targets and deliverables. In addition specific targets are set for individual business units. This report only discusses the financial metrics of the group performance scorecard. The progress on key strategic initiatives is discussed in the group CEO’s overview.

The group delivered a muted ROEV of 8.9% (excluding investment variances) well below the group’s target ROEV of Risk Free + 3% (12.2% based on 10-year RFR at start of year). ROEV inclusive of investment variances was 4.7% for the year.

The group saw a decline in overall new business growth of 6% on a present value of premiums (PVP) basis and 3% on an annual premium equivalent (APE) basis. The value of new business (VNB) declined sharply by 23% as a result of lower volumes as well as lower margins at product level.

The flat core headline earnings were satisfactory in difficult operating circumstances. Improved group risk results were offset by an increase in lapse rates in the Metropolitan Retail market as well as the ongoing impact of flat equity markets on our asset based fees and discretionary margin releases.

Expense management was good with the group achieving R219 million in savings against a target of R226 million for the 2017 financial year. Note that these savings are part of the cost efficiency program to take out R750 million of operating expenses by the 2019 financial year.

The group’s performance in terms of each of the key financial metrics in the scorecard is discussed below.

Return on embedded value (ROEV)

The graph below shows an attribution between the ROEV of the current and previous financial year:

The diluted embedded value of the MMI group amounts to R42 523 million (R26.51 per share) as at 30 June 2017. Adding back the payment of dividends and other capital movements (R2 495 million) the overall return on embedded value (ROEV) amounts to R2 029 million, an annualised return of 4.7% on the opening embedded value. This is below the targeted return on embedded value of 12.2% for the year to 30 June 2017.

Significant items impacting negatively on the ROEV include flat equity markets leading to negative investment variances. The impact of weak investment markets is visible in the ROEV contributions from both our life business and our asset management operations. In addition poor underwriting results in the corporate disability and International short-term and life insurance businesses continued. We continue to increase premium rates on our corporate disability business in order to return to acceptable underwriting margins and we have initiated exits from some of the underperforming International operations. We thus expect underwriting results to improve in F2018.

MMI HOLDINGS INTEGRATED REPORT 2017 | 53

INTRO

DU

CTION

ABO

UT U

SPERFO

RMA

NCE

GO

VERNA

NCE

REMU

NERATIO

NFIN

AN

CIAL STATEM

ENTS

Value of new business (VNB)The graph below shows an attribution between the VNB of the current and previous financial year:

Value of new business per segment June 2017

RmJune 2016

Rm1 year change

%PVP margin

%

Momentum Retail 228 251 (9) 1.0

Metropolitan Retail 178 191 (7) 3.4Corporate and Public Sector 68 199 (66) 0.6International 73 71 3 2.9Total 547 712 (23)New business margin (PVP) 1.3% 1.6%

The Momentum Retail VNB deteriorated due to the reduction in the more profitable business during the current financial year. This is particularly the case on single premium products where the sales mix migrated to lower margin solutions. Metropolitan Retail’s VNB decreased largely due to acquisition costs increasing faster than sales volumes. Market conditions remains highly competitive in the Corporate and Public Sector market and our sales channels experienced some disruptions during the current financial year. This resulted in significant pressure on sales volumes for traditional large corporate business and a weak VNB number. The International VNB was positively impacted by a slight increase in sales in Namibia and in Botswana.

The overall value of new business (VNB) for the 12 months to June 2017 amounts to R547m at a PVP margin of 1.3%, compared with a margin of 1.6% for the prior year. The decline in VNB from the prior year comparative is largely attributable to the negative impact of the decrease in sales volumes (R199m impact).

54 | MMI HOLDINGS INTEGRATED REPORT 2017

Group finance director's report (continued)

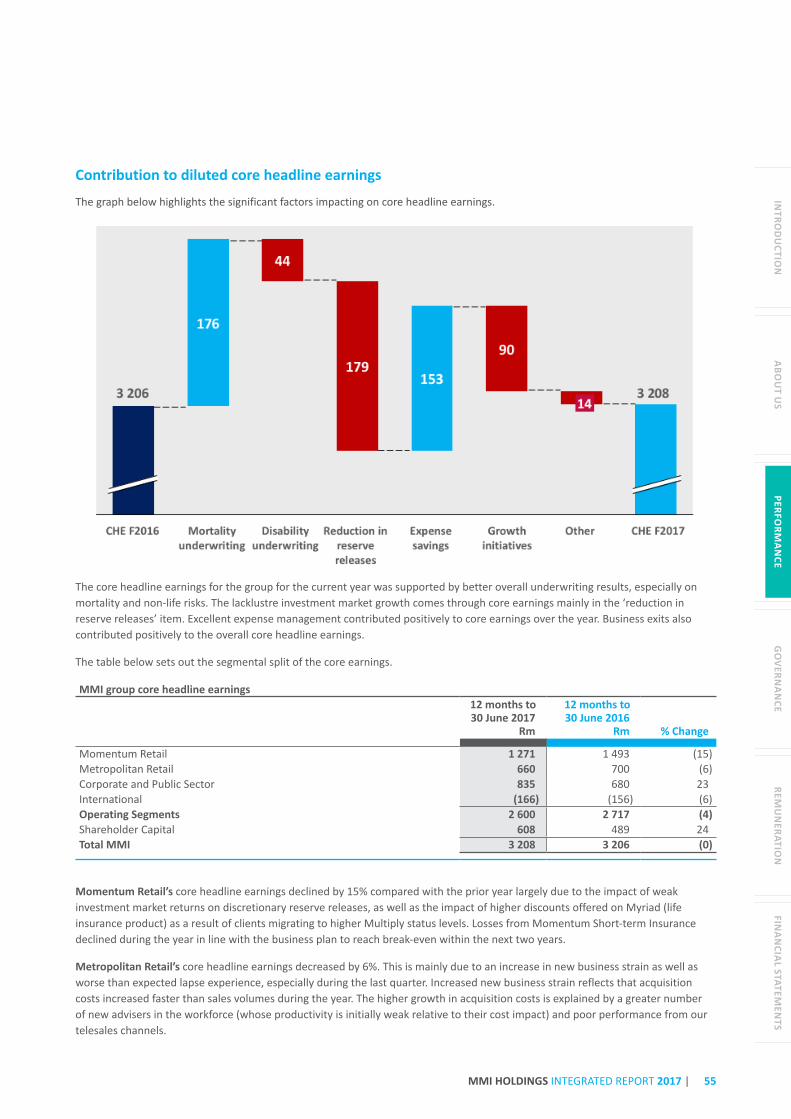

Contribution to diluted core headline earnings

The graph below highlights the significant factors impacting on core headline earnings.

The core headline earnings for the group for the current year was supported by better overall underwriting results, especially on mortality and non-life risks. The lacklustre investment market growth comes through core earnings mainly in the ‘reduction in reserve releases’ item. Excellent expense management contributed positively to core earnings over the year. Business exits also contributed positively to the overall core headline earnings.

The table below sets out the segmental split of the core earnings.

MMI group core headline earnings 12 months to 30 June 2017

Momentum Retail’s core headline earnings declined by 15% compared with the prior year largely due to the impact of weak investment market returns on discretionary reserve releases, as well as the impact of higher discounts offered on Myriad (life insurance product) as a result of clients migrating to higher Multiply status levels. Losses from Momentum Short-term Insurance declined during the year in line with the business plan to reach break-even within the next two years.

Metropolitan Retail’s core headline earnings decreased by 6%. This is mainly due to an increase in new business strain as well as worse than expected lapse experience, especially during the last quarter. Increased new business strain reflects that acquisition costs increased faster than sales volumes during the year. The higher growth in acquisition costs is explained by a greater number of new advisers in the workforce (whose productivity is initially weak relative to their cost impact) and poor performance from our telesales channels.

MMI HOLDINGS INTEGRATED REPORT 2017 | 55

INTRO

DU

CTION

ABO

UT U

SPERFO

RMA

NCE

GO

VERNA

NCE

REMU

NERATIO

NFIN

AN

CIAL STATEM

ENTS

The Corporate and Public Sector core headline earnings, which increased by 23% compared to the prior year, was positively impacted by an improvement in group risk experience profits in the current financial year, and the positive impact of efficiency savings in the Health business. Disability underwriting profits remains under pressure given the poor economic climate and a very competitive market. The segment continues to monitor this closely, increasing rates where appropriate. Premiums have also started to harden over the past 12 months. Guardrisk also contributed positively to the pleasing increase in earnings.

MMI International’s decrease in core headline earnings is largely due to the worse than expected short-term and life insurance results, especially in Kenya. The group continues with its plans to improve focus by exiting certain loss-making business lines and by fully disposing of some operations.

The Shareholder Capital core headline earnings increased by 24% as a result of better investment performance on shareholder capital and lower shareholder expenses.

Capital management The table below sets out the group’s capital position at 30 June 2017:

Rbn

Net asset value as per embedded value statement 16.3Qualifying debt 3.6Less: net asset value of strategic subsidiaries (3.6)Less: required capital (10.1)Capital before deployment 6.2

Deployed (2.5)Final dividend (1.5)Committed capital – strategic initiatives (1.0)

Capital buffer after deployment 3.7

At 30 June 2017, the solvency position of MMI Holdings remained satisfactory with a capital buffer of R3.7bn after allowing for deployment for strategic initiatives. The above position is on the current Statutory Valuation Method (SVM) basis, but group Balance Sheet Management continued with the focus on preparing for Solvency Assesment and Management (SAM) implementation during the year. The results of the investigations indicated that a targeted range of 1.3 to 1.6 times the Solvency Capital Ratio (SCR) for MMI Holdings would be appropriate. The target range for the solo insurance entity (Momentum Group Ltd) will be higher than for MMI Holdings.

DividendDespite the ongoing earnings pressure experienced during the year, the current capital position of the group, in addition to management’s confidence in MMI’s longer-term earnings generating capacity and the decision to exit certain loss-making businesses, supports MMI’s ability to declare an unchanged final dividend compared to the prior year. The final dividend of 92 cents per share results in a total dividend for the year of 157 cents per share. The group plans to revert to its target dividend cover ratio of 1.5 to 1.7 times core headline earnings in due course.

The table below shows the groups dividend declarations over the last three years.

The group continued to experience difficult operating conditions over the past year that manifested in lower than expected earnings. Despite the challenging conditions the group was able to secure solid new business flows albeit at lower margins, while keeping a strong control over expense growth.

The group has made good progress on some key growth initiatives. The Indian health insurance joint venture with Aditya Birla is one deserving of a special mention. Early top line growth has exceeded business plans and we remain excited about this opportunity. We are also optimistic about the prospects of our lending and insurance joint venture with African Bank that will become operational during F2018.

However, tough operating conditions are likely to persist for the more mature domestic life insurance operations and revenue is likely to remain under pressure in the near term. Despite the modest revenue outlook we plan to invest selectively in expanding our distribution presence in the SA retail market and we also continue to invest in client engagement solutions to

56 | MMI HOLDINGS INTEGRATED REPORT 2017

Group finance director's report (continued)

ensure that we have differentiated client solutions. We believe that these investments will enable us to capture increased share of the market and to position us to generate attractive returns once the economic conditions improve.

MARY VILAKAZI Deputy chief executive officer and group finance director

MMI HOLDINGS INTEGRATED REPORT 2017 | 57

INTRO

DU

CTION

ABO

UT U

SPERFO

RMA

NCE

GO

VERNA

NCE

REMU

NERATIO

NFIN

AN

CIAL STATEM

ENTS

INTRODUCTION

MMI’s risk philosophy recognises that managing risk is an integral part of generating shareholder value and enhancing stakeholder interests. It also recognises that an appropriate balance should be struck between entrepreneurial endeavour and sound risk management practice.

Management and the boardRisk management enables management to deal effectively with uncertainty and its associated risks and opportunities, enhancing the capacity to build value.

The MMI board is ultimately responsible for the end-to-end process of risk management, and for assessing its effectiveness. Management is accountable to the board for designing, implementing and monitoring the risk management process and for integrating it into the day-to-day activities of the group.

The board discharges these responsibilities by means of frameworks and policies approved and adopted by the board and its designated committees, which direct the implementation and maintenance of adequate processes for corporate governance, compliance, and risk management. The risk management framework applies to all segments, centres of excellence and group-wide functions.

The chief risk officer (CRO) of MMI is the head of the risk function in the business, who is supported by individual risk type heads, segmental risk management teams and their CROs. The head of the actuarial function provides assurance to the board on the accuracy of calculations and appropriateness of the assumptions underlying the technical provisions and capital requirements, both from a regulatory and economic balance sheet perspective.

Risk appetiteMMI’s risk appetite is formulated by the group executive committee and approved by the Board Risk, Capital and Compliance Committee, and expresses the level and type of risk which MMI is prepared to seek, accept or tolerate in pursuit of its strategic objectives.

The risk appetite includes quantitative boundaries on risk exposure and the group’s economic capital requirements, supported by a detailed risk strategy. The risk strategy, which is also approved by the Board Risk, Capital and Compliance Committee, provides a qualitative specification of MMI’s appetite for exposure to the different types and sources of risk.

The setting of risk appetite is fundamentally driven by the dual, and at times conflicting, objectives of creating shareholder value through risk taking, while providing financial security for customers through appropriate maintenance of the group’s ongoing solvency. MMI’s appetite for exposure to the different types and sources of risk is aligned with the strategic vision of MMI to be the preferred lifetime Financial Wellness partner of our clients, with a reputation for innovation and trustworthiness.

RISK MANAGEMENT STRATEGYMMI's key risk management strategies are to:

• Understand the nature of the risks MMI is exposed to, the range of outcomes under different scenarios, and the capital required for assuming these risks.

• Manage shareholder value by generating a long-term sustainable return on the capital required to back the risks assumed.• Ensure the protection of client interests by maintaining adequate solvency levels.• Ensure that capital and resources are strategically focused on activities that generate the greatest value on a

risk-adjusted basis.• Create a competitive long-term advantage in the management of the business with greater responsibility to all stakeholders.

58 | MMI HOLDINGS INTEGRATED REPORT 2017

Risk management report

RISK TAXONOMY

BUSINESS AND STRATEGIC RISK

Business and strategic risks for MMI are risks that can adversely affect the fulfilment of business and strategic objectives to the extent that the viability of a business is compromised. This includes reputational risks and the impact of the macroeconomic and business operating environment.

LIFE INSURANCE RISK

Life insurance risk for MMI is the risk that future claims and expenses will cause an adverse change in the value of long-term life insurance contracts. This can be through the realisation of a loss, or the change in insurance liabilities. The value of life insurance contracts is the expectation in the pricing and/or liability of the underlying contract where insurance liabilities are determined using an economic boundary. It therefore relates to the following risk exposures: mortality, morbidity/disability, retrenchment, longevity, life catastrophes, lapse and persistency, expenses and business volumes.

NON-LIFE INSURANCE RISK

For short-term insurance, it is defined as the risk of unexpected underwriting losses in respect of existing business as well as new business expected to be written over the following twelve months. Underwriting losses could result from adverse claims, increased expenses, insufficient pricing, inadequate reserving, or through inefficient mitigation strategies like inadequate or non-adherence to underwriting guidelines. It covers premium, reserve, lapse and catastrophe risk exposures.

CREDIT RISK

Credit risk for MMI is the risk of losses arising from the potential that a counterparty will fail to meet its obligations in accordance with agreed terms. It arises from investment activities but also non-investment activities, for example reinsurance credit risk, amounts due from intermediaries, policy loans and script lending. MMI accepts credit risk on behalf of its policyholders and shareholders.

MARKET RISK

Market risk for MMI is defined as the risk of losses arising from adverse movements in the level and/or volatility of financial market prices and rates. This includes exposure to equities, interest rates, credit spreads, property, price inflation and currencies.

LIQUIDITY RISK

Liquidity risk for MMI is the risk that, though solvent, the organisation has inadequate cash resources to meet its financial obligations when due, or MMI can only secure these resources at excessive cost. MMI differentiates between funding liquidity risk (the risk of losses arising from difficulty in raising funding to meet obligations when they become due) and market liquidity risk (the risk of losses arising when engaging in financial instrument transactions due to inadequate market depth or market disruptions).

OPERATIONAL RISK

Operational risk for MMI is the risk of losses resulting from inadequate or failed internal processes, people and systems or from external events. This definition includes legal risk but excludes strategic and reputational risk.

COMPLIANCE RISK

Compliance risk for MMI is the risk of legal or regulatory sanctions, material financial loss or loss to reputation that the entity may suffer as a result of its failure to comply with legislation, regulation, rules, related self-regulatory organisation standards or codes of conduct applicable to the activities of the entity.