46

Performance of the Manufacturing Industries in Hawaii and the U.S. Department of Business, Economic Development and Tourism November 2016

PerformanceoftheManufacturingIndustriesin

HawaiiandtheU.S.

Department of Business, Economic Development and Tourism

November 2016

2|P a g e

Hawaii Department of Business, Economic Development & Tourism

November 2016

P a g e |3

TableofContents

EXECUTIVESUMMARY 4

I. INTRODUCTION 7 ResearchObjectives 8 DataSources 8 Major Industry Groups of the Manufacturing Sector 9

II. COSTSTRUCTUREOFMANUFACTURINGSECTOR 12

III. HISTORICALTRENDSOFTHEMANUFACTURINGSECTOR 14

IV. HAWAII’SMANUFACTURINGSECTORPORTFOLIO 18ManufacturingSectorJobGrowth 18NationalCompetitivenessoftheManufacturingSector 21IndustryConcentration–Hawaii’sManufacturingSpecialties 22PerformanceMapFramework:IdentifyingEmergingManufacturingIndustries23

V. MANUFACTURINGINDUSTRYPERFORMANCEBYCOUNTY 26City&CountyofHonolulu 26HawaiiCounty 27MauiCounty 29KauaiCounty 30

VI. MANUFACTURINGINDUSTRYPERFORMANCEBYMAJORGROUP 32

FoodandBeverageandTobaccoManufacturing 34MiscellaneousManufacturing 35NonmetallicMineralProductManufacturing 36ApparelandLeatherandAlliedProductManufacturing 37PrintingandRelatedSupportActivities 38OtherDurableGoodsManufacturing 39TransportationEquipmentManufacturing 40OtherNondurableGoodsManufacturing 41WoodProductManufacturing 42PetroleumandCoalProductsManufacturing 43FurnitureandRelatedProductManufacturing 44ChemicalManufacturing 45

VII. CONCLUSIONS 46

4|P a g e

EXECUTIVESUMMARY

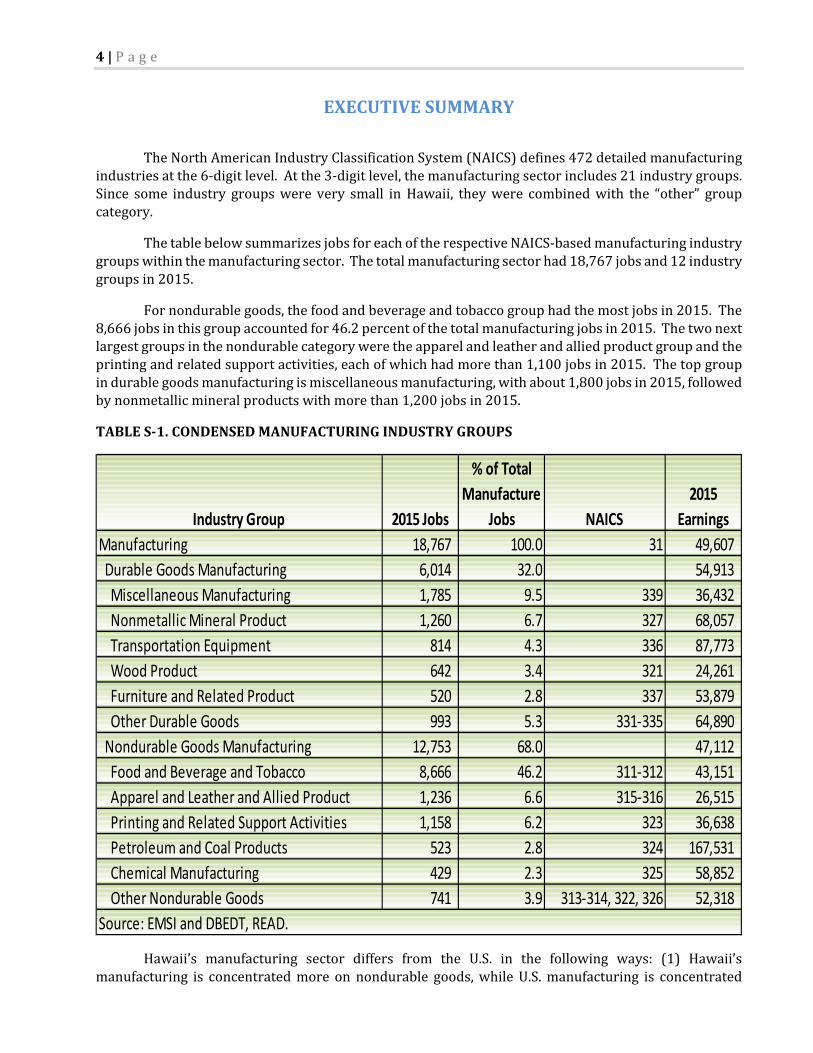

TheNorthAmericanIndustryClassificationSystem(NAICS)defines472detailedmanufacturingindustriesatthe6‐digitlevel.Atthe3‐digitlevel,themanufacturingsectorincludes21industrygroups.Since some industry groupswere very small inHawaii, theywere combinedwith the “other” groupcategory.

ThetablebelowsummarizesjobsforeachoftherespectiveNAICS‐basedmanufacturingindustrygroupswithinthemanufacturingsector.Thetotalmanufacturingsectorhad18,767jobsand12industrygroupsin2015.

Fornondurablegoods,thefoodandbeverageandtobaccogrouphadthemostjobsin2015.The8,666jobsinthisgroupaccountedfor46.2percentofthetotalmanufacturingjobsin2015.Thetwonextlargestgroupsinthenondurablecategoryweretheapparelandleatherandalliedproductgroupandtheprintingandrelatedsupportactivities,eachofwhichhadmorethan1,100jobsin2015.Thetopgroupindurablegoodsmanufacturingismiscellaneousmanufacturing,withabout1,800jobsin2015,followedbynonmetallicmineralproductswithmorethan1,200jobsin2015.

TABLES‐1.CONDENSEDMANUFACTURINGINDUSTRYGROUPS

Hawaii’s manufacturing sector differs from the U.S. in the following ways: (1) Hawaii’smanufacturing is concentratedmore on nondurable goods,whileU.S.manufacturing is concentrated

Industry Group 2015 Jobs

% of Total

Manufacture

Jobs NAICS

2015

Earnings

Manufacturing 18,767 100.0 31 49,607

Durable Goods Manufacturing 6,014 32.0 54,913

Miscellaneous Manufacturing 1,785 9.5 339 36,432

Nonmetallic Mineral Product 1,260 6.7 327 68,057

Transportation Equipment 814 4.3 336 87,773

Wood Product 642 3.4 321 24,261

Furniture and Related Product 520 2.8 337 53,879

Other Durable Goods 993 5.3 331‐335 64,890

Nondurable Goods Manufacturing 12,753 68.0 47,112

Food and Beverage and Tobacco 8,666 46.2 311‐312 43,151

Apparel and Leather and Allied Product 1,236 6.6 315‐316 26,515

Printing and Related Support Activities 1,158 6.2 323 36,638

Petroleum and Coal Products 523 2.8 324 167,531

Chemical Manufacturing 429 2.3 325 58,852

Other Nondurable Goods 741 3.9 313‐314, 322, 326 52,318

Source: EMSI and DBEDT, READ.

P a g e |5

moreondurablegoods.68.0percentofHawaiimanufacturingworkersproducenondurablegoodsand32.0percentoftheworkersproducedurablegoods.Incontrast,amajorityofU.S.manufacturingisindurable goods, with 62.6 percent of U.S. manufacturingworkers producing durable goods and 37.4percentproducingnon‐durablegoods.(2)ManufacturingcomposesagreatershareoftheU.S.economythanthatofHawaii’seconomy. In2015,U.S.manufacturingcontributed12.2percentoftheU.S.GDP,whileHawaii’smanufacturingcontributed1.8percentof thestate’sGDP. (3)TheU.S.manufacturingindustry is more diversified than Hawaii’s manufacturing industry. The main categories for U.S.manufacturing are metal products, machinery, equipment, computers and electronic products, withthesecategoriesaccountingfor65.1percentofU.S.manufacturingrealGDP.PetroleumproductsandprocessedfoodarethemajorcategoriesforHawaii’smanufacturingindustry,accountingfor53.3percentofHawaii’smanufacturingrealGDP.(4)U.S.manufacturersarelargercompanies,withanaverageof38employees per establishment versus 20 employees per establishment for Hawaii. (5) Hawaiimanufactures pay more for materials than their U.S. counterparts. For Hawaii, 83.2 percent ofmanufacturing costs were for materials, while 71.4 percent of U.S. manufacturing costs were formaterials.(6)Onaverage,Hawaii’smanufacturingworkerswerepaidlessthanthenationalaverage.In2015, theaverageearnings forHawaii’smanufacturingworkerswas$49,607versus$76,657 forU.S.manufacturingworkers.

Between2005and2015,Hawaii’smanufacturingindustriesaddedonlyabout200jobs,whileHawaii’stotaleconomyaddedabout67,000jobs.Asaresult,themanufacturingsector’scontributiontoHawaii’semploymentdroppedfrom2.2percentin2005to2.1percentin2015.However,fiveoftheindustrygroupsshowedjobgrowthduringthepastdecade:transportationequipment,petroleumandcoalproducts,foodandbeverageandtobacco,otherdurablegoods,andnonmetallicmineralproduct.

From1998to2015,theshareofmanufacturingjobsintotaljobsdecreasedby0.5percentagepointinHawaii.Thedecreaseintheshareofmanufacturingjobswaspartiallyduetoincreasedlaborproductivity.Inotherwords,thedecreaseinthemanufacturingsector’sshareofrealGDPwaslessthantheshareofthetotaljobdecrease.ThiswastrueforbothHawaiiandthenation,especiallyforthenation.

LaborproductivityinHawaii’smanufacturingsector,especiallydurablegoods,waslowerthanthe overall productivity of all industries combined. However, the growth rate of themanufacturingsector’slaborproductivitywashigherthantheoverallproductivitygrowthrate.From1998to2015,allindustriescombined inHawaii increasedrealGDPper jobby12.0percent, from$70,266to$78,716.However,forHawaii’smanufacturingsector,realGDPperjobincreased24.2percent,from$51,935to$64,513duringthesameperiod.ForHawaii’sdurablegoodsmanufacturing,realGDPperjobincreased44.7percent,from$37,451to$54,194duringthesameperiod.

The next table shows how each of the respective NAICS‐based manufacturing groups was

classifiedonaperformancematrix.Basedonjobgrowthalone,nomanufacturingindustrygroupswerequalifiedashighperformingbase‐growth industriesor transitioning industries for the2005 to2015period. The industry groups in the emerging categorywere composedof transportationequipment,petroleumandcoalproducts(mostlypetroleum),foodandbeverageandtobacco,otherdurablegoods,and nonmetallic mineral product. These groups accounted for about 65.3 percent of the totalmanufacturingsectorjobsin2015.Thesevenmanufacturingindustrygroupsthatlostjobsinthe2005to2015periodfell intothedecliningquadrantoftheperformancemap. Thesegroupsaccountedforabout34.7percentoftotalmanufacturingsectorjobsin2015.Theearningsaverageofthemanufacturingindustrywas$49,607in2015,whichwaslowerthanthestatewideaverageof$52,156.

6|P a g e

TABLES‐2.MANUFACTURINGINDUSTRYGROUPSMAPPEDBYPERFORMANCE,2005‐2015

*NAdenotesnoindustrygroupsinthecategory

GroupChange

in Jobs

Average

EarningsGroup

Change in

Jobs

Average

Earnings

NA NA NA NA NA NA

GroupChange

in Jobs

Average

EarningsGroup

Change in

Jobs

Average

Earnings

Miscellaneous Manufacturing ‐8.5% $36,432 Transportation Equipment 41.9% $87,773

Apparel and Leather and Allied Product ‐14.0% $26,515 Petroleum and Coal Products 20.0% $167,531

Chemical Manufacturing ‐15.8% $58,852 Food and Beverage and Tobacco 17.1% $43,151

Printing and Related Support Activities ‐20.8% $36,638 Other Durable Goods 9.7% $64,890

Other Nondurable Goods ‐23.4% $52,318 Nonmetallic Mineral Product 3.3% $68,057

Wood Product ‐29.5% $24,261

Furniture and Related Product ‐30.2% $53,879

Declining Group: 34.7% of Jobs Emerging Group: 65.3% of Jobs

Total Jobs, 2015: 18,767

Average Annual Earnings, 2015: $49,607

Net Change in Jobs, 2005‐2015: 1.3%

Transitioning Group: 0.0% of Jobs Base‐Growth Group: 0.0% of Jobs

P a g e |7

I. INTRODUCTION

Themanufacturingsectorisadriverforexportactivities,thecreatorofbrandnames,thesourceforinnovation,thetestbedfortechnologyimprovement,andthecontributorforproductivitygrowth.However,manufacturinghasbeenadecliningindustryandthishasledtoeffortsaimedatrevitalizingthe manufacturing industry, both at the national and local levels. In the past few years, HawaiiLegislature introduced many bills with the goal of increasing manufacturing competitiveness andcreatingmorehighpayingjobs.

Inlookingattheglobaleconomy,alargeshareofmanufacturinghasshiftedfromthedevelopedcountriestothenewlyindustrializedcountriessuchasChina. Asaresult, themanufacturingsector’sshareof the totaleconomyhasdecreasedover timeinboththeU.S.andHawaii. ComparedwiththeoverallU.S.economy,Hawaii’smanufacturingindustryfacesadditionalchallengesincludinghighenergy,land,andmaterialcosts.AnotherchallengeforHawaii’seconomyishighshippingcostscoupledwithalimitedlocalsupplychain.Amajorityofrawmaterialsandpartsusedformanufacturingareimported,addingsubstantialcosttotheendproduct.

Inspiteofthesechallenges,thereareadvantagestodevelopingHawaii’smanufacturingindustryin certain areas. First, many of themanufacturing industry groups have above average wages andsalaries. This is especially true for thepetroleumrefining, transportationequipmentmanufacturing,chemicalmanufacturing,andnonmetallicmanufacturing.

Second,Hawaiihasavery largedefensesector. TheDepartmentofDefensespendsabout$2billion each year on prime contracts and equipment inHawaii. The proximity tomilitary bases andpersonnelisaninherentadvantagethatlocalmanufacturerscanleveragethroughcollaborations,justintimeinventory,andjointresearchanddevelopment.

Finally,perhapsHawaii’sbiggestadvantageformanufacturingisthatithasaglobalmarketof8.5millionpeoplethatvisitthestateeachyear.In2015,Hawaiivisitorsspent$15.2billiondollarsandthereistremendouspotentialforHawaiitomanufacturemoreproductstoservethetourismmarket.

8|P a g e

ResearchObjectives

This report analyzes the recent trend of Hawaii’s manufacturing sector, benchmarks theperformanceoftheindustrieswithinthesector,andidentifiespotentialchallengesandopportunitiesforthemanufacturingsectorgrowthinHawaii.Specifically,thisstudyhasfourresearchobjectives:

1)Tobenchmarkthestate’smanufacturingindustryasawhole.

2)TocompareHawaii’smanufacturing industryagainst theU.S. totalmanufacturing industryperformance. The report will compare the manufacturing’s relative productivity and coststructurebetweentheU.S.andHawaii.

3)Toexaminethemanufacturingindustryperformanceineachofthemanufacturingindustrygroups.

4)ToexaminethemanufacturingindustryperformanceineachofHawaii’sfourcounties.

DataSources

Therearethreemaindatasourcesusedinthisstudy.ThefirstistheU.S.BureauofEconomicAnalysis(BEA).TheBEAprovidesemployment,GDP,andrealGDPdatabythree‐digitNorthAmericanIndustryClassificationSystem(NAICS)codeforallU.S.states. It is importanttonotethattheperiodavailableforanalysisdependsonthetypeofdata.Forsixofthethree‐digitlevelNAICSindustries,theBEAdataareonlyavailableatthecombinedlevelofthreeindustries.TheemploymentdatafromtheBEAarecurrentlyavailablefrom1998to2015.TheGDPbyNAICSindustrydataareavailableatthetwo‐digitlevelfrom1997to2015andavailablefrom1997to2014atthethree‐digitlevel.

ThesecondsourceofdataistheEconomicModelingSpecialists,Inc.(EMSI).EMSIdataconsistprimarilyofjobsandlaborearningsthatareavailableannuallyatthesix‐digitNAICSlevel.1TheEMSIdataareavailableatboththestateandthecountylevel,butonlyavailablesince2001.

ThethirdsourceofdataistheU.S.CensusBureau.The2012EconomicCensus(EC)dataincludesdetailedstatisticsforthemanufactureindustrycosts.

1 The basic data are compiled by EconomicModeling Specialists, Inc. (EMSI) and processed byDBEDT. EMSIsupplementsdatafromtheFederalDepartmentsofLaborandCommercebyincludingestimatesofproprietorsandself‐employedjobs,andbyestimatingdataforverysmallindustriesthatarenotreportedbytheFederalagenciesduetodisclosureissues.

P a g e |9

Major Industry Groups of the Manufacturing Sector

The Manufacturing sector comprises establishments engaged in the mechanical, physical, orchemical transformation of materials, substances, or components into new products. The NorthAmericanIndustryClassificationSystem(NAICS)defines472detailedmanufacturingindustriesatthe6‐digitleveland21availableatthe3‐digitlevel:

311Foodmanufacturing

312Beverageandtobaccoproductmanufacturing

313Textilemills

314Textileproductmills

315Apparelmanufacturing

316Leatherandalliedproductmanufacturing

321Woodproductmanufacturing

322Papermanufacturing

323Printingandrelatedsupportactivities

324Petroleumandcoalproductmanufacturing

325Chemicalmanufacturing

326Plasticsandrubberproductmanufacturing

327Nonmetallicmineralproductmanufacturing

331Primarymetalmanufacturing

332Fabricatedmetalproductmanufacturing

333Machinerymanufacturing

334Computerandelectronicproductmanufacturing

335Electricalequipment,appliance,andcomponentmanufacturing

336Transportationequipmentmanufacturing

337Furnitureandrelatedproductmanufacturing

339Miscellaneousmanufacturing

Theaboveindustriesarefurtherclassifiedasdurablegoodsmanufacturingornondurablegoodsmanufacturing.Adurablegoodisagoodthatdoesnotquicklywearout,ormorespecifically,onethatcanbeusedrepeatedlyovertimeratherthanbeingcompletelyconsumedinoneuse.Nondurablegoodsmaybedefinedeitherasgoodsthatareimmediatelyconsumedinoneuseoronesthathavealifespanoflessthan3years.

10|P a g e

As shown in Table 1, the durable goodsmanufacturing includes 10 industry groups, and thenondurable goods manufacturing includes 8 industry groups. In 2015, the manufacturing sectoremployed 18,767 people in Hawaii, accounting for about 2.1 percent of total jobs. Durable goodsmanufacturinghadabout6,000jobs,accountingforabout0.7percentoftotaljobsinHawaii.Nondurablegoodsmanufacturinghadabout12,800 jobs,accountingforabout1.4percentof total jobs inHawaii.UsingEMSIdata,durableandnondurablegoodsmanufacturingcanbebrokendowninto18industrygroupslistedinTable1.

TABLE1.DETAILEDMANUFACTURINGINDUSTRYGROUPS

Industry Group 2015 Jobs

% in Total

Jobs NAICS

2015

Earnings

All Industry Total Jobs 896,608 100.00 52,156

Manufacturing 18,767 2.09 31 49,607

Durable Goods Manufacturing 6,014 0.67 54,913

Wood Product 642 0.07 321 24,261

Nonmetallic Mineral Product 1,260 0.14 327 68,057

Primary Metal 8 0.00 331 57,887

Fabricated Metal Product 511 0.06 332 66,631

Machinery 133 0.01 333 46,159

Computer and Electronic Product 286 0.03 334 75,739

Electrical Equipment and Appliance 54 0.01 335 41,318

Transportation Equipment 814 0.09 336 87,773

Furniture and Related Product 520 0.06 337 53,879

Miscellaneous Manufacturing 1,785 0.20 339 36,432

Nondurable Goods Manufacturing 12,753 1.42 47,112

Food and Beverage and Tobacco Product 8,666 0.97 311‐312 43,151

Textile Mills and Textile Product Mills 314 0.04 313‐314 41,692

Apparel and Leather and Allied Product 1,236 0.14 315‐316 26,515

Paper 84 0.01 322 68,170

Printing and Related Support Activities 1,158 0.13 323 36,638

Petroleum and Coal Products 523 0.06 324 167,531

Chemical 429 0.05 325 58,852

Plastics and Rubber Products 343 0.04 326 58,162

Source: EMSI and DBEDT, READ.

P a g e |11

Since some industry groups listed in Table 1were very small, theywere combinedwith the“other” group category. The five durable goods industry groups,withNAICS code 331 to 335werecombinedtotheotherdurablegoodsgroup.Thethreenondurablegoodsindustrygroups,withNAICScode313‐314,322,and326werecombinedtotheothernondurablegoodsgroup.AsshowninTable2,theotherdurablegoodscategoryaccountedforonly5.3percentoftotalmanufacturingjobsinHawaiiin2015,whileothernondurablegoodsaccountedforonly3.9percentoftotalmanufacturingjobsinHawaiiin2015.

TABLE2.CONDENSEDMANUFACTURINGINDUSTRYGROUPS

Industry Group 2015 Jobs

% of Total

Manufacture

Jobs NAICS

2015

Earnings

Manufacturing 18,767 100.0 31 49,607

Durable Goods Manufacturing 6,014 32.0 54,913

Miscellaneous Manufacturing 1,785 9.5 339 36,432

Nonmetallic Mineral Product 1,260 6.7 327 68,057

Transportation Equipment 814 4.3 336 87,773

Wood Product 642 3.4 321 24,261

Furniture and Related Product 520 2.8 337 53,879

Other Durable Goods 993 5.3 331‐335 64,890

Nondurable Goods Manufacturing 12,753 68.0 47,112

Food and Beverage and Tobacco 8,666 46.2 311‐312 43,151

Apparel and Leather and Allied Product 1,236 6.6 315‐316 26,515

Printing and Related Support Activities 1,158 6.2 323 36,638

Petroleum and Coal Products 523 2.8 324 167,531

Chemical Manufacturing 429 2.3 325 58,852

Other Nondurable Goods 741 3.9 313‐314, 322, 326 52,318

Source: EMSI and DBEDT, READ.

12|P a g e

II. COSTSTRUCTUREOFMANUFACTURINGSECTOR

Thissectiondescribesthecoststructureofthemanufacturingsector.RevenueandcostdataareonlyavailableeveryfiveyearsfromtheU.S.CensusBureau’sEconomicCensus.2012isthelatestyearwhendataareavailable.Duetothedatadisclosurerules,theCensusBureaudidnotreleasethedataforPetroleumindustryforHawaiisincethereareonlytworefineriesinthestate.

AccordingtoestimatebyDBEDT,about57percentofthesalesinHawaii’smanufacturingsector

in2012weregeneratedinthePetroleumindustry.Thepetroleumindustryimported$4.8billionworthofcrudeoilintothestateinthatyear.ThisbigamountofimportsalonemadeHawaii’smanufacturingsectorheavyrelianceonmaterials,comparedwiththeU.S.average.TheCensusdatarevealthattotalmanufacturingcostwascomposedof83.2percentmaterialcostsinHawaii;whileU.S.averagematerialcostwas71.4percentoftotalmanufacturingcost.

LaborcostinHawaii’smanufacturingsectorwaslowerthanthatoftheU.S.manufacturingsector.

7.4percentofthemanufacturingsector’stotalcostwasforlaborinHawaiiin2012,while16.2percentofthemanufacturingsectorcostwenttolaborfortheU.S.asawhole.ThiswasalsoanindicationthatHawaiimanufacturingworkersweregenerallypaidlessthantheirmainlandcounterparts.InvestmentinthemanufacturingsectorwasalsolowinHawaiiwithonlyabout1.3percentofthetotalmanufacturingcostforcapitalexpendituresinHawaiiversus3.5percentfortheU.S..

DespiteofHawaii’snotoriouslyhighrentalprices,percentageoftotalrentalpaymentsinHawaii’s

manufacturingsectorwasonlyslightlyhigherthanoftheU.S.manufacturingaverage(0.8percentforHawaii,0.7percentforU.S.average).

P a g e |13

TABLE3.COMPARISONOFMANUFACTURINGSECTOR’SCOSTS

HI above U.S.

HI U.S. HI U.S. Percentage Point

Total selected cost ($M) 8,102 4,740,301 100.0 100.0 0.0

Labor cost 603 769,610 7.4 16.2 ‐8.8

Total annual payroll 465 590,084 5.7 12.4 ‐6.7

Total fringe benefits 138 179,526 1.7 3.8 ‐2.1

Employer's cost for health insurance 52 71,262 0.6 1.5 ‐0.9

Employer's cost for defined benefit pension plans 16 16,106 0.2 0.3 ‐0.1

Employer's cost for defined contribution plans 13 18,825 0.2 0.4 ‐0.2

Employer's cost for other fringe benefits 56 73,333 0.7 1.5 ‐0.9

Total cost of materials 6,741 3,384,339 83.2 71.4 11.8

Materials, parts, containers, packaging, etc. used 5,975 3,076,382 73.7 64.9 8.8

Cost of resales 571 166,185 7.0 3.5 3.5

Cost of purchased fuels 121 34,556 1.5 0.7 0.8

Purchased electricity 44 50,587 0.5 1.1 ‐0.5

Contract work 30 56,628 0.4 1.2 ‐0.8

Changes in inventories 244 20,873 3.0 0.4 2.6

Total capital expenditures (new and used) 108 166,458 1.3 3.5 ‐2.2

Capital expenditures on buildings and other structures 13 33,065 0.2 0.7 ‐0.5

Capital expenditures on machinery and equipment 96 133,393 1.2 2.8 ‐1.6

On automobiles, trucks, etc. for highway use 6 3,347 0.1 0.1 0.0

On computers and peripheral data processing equ. 6 5,758 0.1 0.1 ‐0.1

On all other machinery and equipment 84 124,289 1.0 2.6 ‐1.6

Total rental payments 61 33,530 0.8 0.7 0.0

Buildings and other structures 47 23,392 0.6 0.5 0.1

Machinery and equipment 14 10,138 0.2 0.2 0.0

Total other expenses 346 365,491 4.3 7.7 ‐3.4

Temporary staff and leased employee expenses 21 30,931 0.3 0.7 ‐0.4

Expensed computer hardware and other equipment 1 3,658 0.0 0.1 ‐0.1

Expensed purchases of software 1 2,835 0.0 0.1 0.0

Data processing and other purchased computer services 6 6,288 0.1 0.1 ‐0.1

Communication services 3 4,344 0.0 0.1 ‐0.1

Repair and maintenance services of buildings & machinery 63 44,244 0.8 0.9 ‐0.2

Refuse removal (including hazardous waste) services 13 13,438 0.2 0.3 ‐0.1

Advertising and promotional services 13 13,265 0.2 0.3 ‐0.1

Purchased professional and technical services 15 29,713 0.2 0.6 ‐0.4

Taxes and license fees 28 17,129 0.3 0.4 0.0

All other expenses 182 199,645 2.2 4.2 ‐2.0

Source: U.S. Census Bureau and DBEDT, READ.

2012 % of Cost

14|P a g e

III. HISTORICALTRENDSOFTHEMANUFACTURINGSECTOR

Due to changes in the economic structure and labor productivity, themanufacturing sector’sshareofjobstototaljobsdecreasedovertimeinboththeU.S.andinHawaii.AsshowninFigure1,from1998to2015,themanufacturingsector’sshareoftotaljobsdecreasedabout4.5percentagepoints,from11.4 percent to 6.9 percent for the nation. Nationally, the share of durable goods manufacturingdecreased 2.8 percentage points and the share of nondurable goods manufacturing decreased 1.7percentagepoint.InlookingatHawaii,themanufacturingsector’sshareoftotaljobsdecreasedabout0.5ofapercentagepoint.TheshareofdurablegoodsmanufacturinginHawaiidecreasedabout0.1ofapercentage point, while the share of nondurable goods manufacturing decreased about 0.4 of apercentagepoint.

WhiletheroleofthemanufacturingsectorinHawaiiissignificantlylessthanthatofthenation,especiallyfordurablegoods,thegaphasbeendecreasing.

FIGURE1

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Manufacturing Percentage of Total Jobs, 1998‐2015

HI Manufacturing HI Durable HI Nondurable

US Manufacturing US Durable US Nondurable

P a g e |15

Thedecreasedshareofmanufacturing jobswaspartiallydue to increased laborproductivity.ComparedwiththeU.S.productivity,improvementsinHawaii’smanufacturingsectorweresmaller.AsshowninFigure2,from1998to2015,themanufacturingsector’sshareofU.S.realGDPdecreased0.4ofa percentagepoint from12.3 percent to 11.9 percent; the share ofU.S. durable goods increased 1.1percentagepointsfrom5.8percentto6.9percent,andtheshareofU.S.nondurablegoodsdecreased1.7percentagepointsfrom6.8percentto5.1percent.

In looking at Hawaii, from 1998 to 2015, themanufacturing sector’s share of total real GDP

decreased0.22ofapercentagepointfrom1.9percentto1.7percent.Hawaii’sshareofdurablegoodsincreased0.04ofapercentagepointandtheshareofnondurablegoodsdecreased0.26ofapercentagepoint.

FIGURE2

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Manufacturing Percentage of Total Real GDP, 1998‐2015

HI Manufacturing HI Durable HI Nondurable

US Manufacturing US Durable US Nondurable

16|P a g e

LaborproductivityinHawaii’smanufacturingsector,especiallydurablegoods,waslowerthantheproductivityofallHawaii’s industriescombined. However, thegrowthrateof themanufacturingsector’slaborproductivitywashigherthantheoverallproductivitygrowth.Figure3comparesHawaii’srealGDPperjobfrom1998to2015.ForallindustriesinHawaii,realGDPperjobincreased12.0percentfrom$70,266to$78,716.However,forHawaii’smanufacturingsector,realGDPperjobincreased24.2percent from $51,935 to $64,513. Real GDPper job for durable goods increased 44.7 percent from$37,451to$54,194andrealGDPperjobfornondurablegoodsincreased18.4percent,from$58,425to$69,162.

In2015,Hawaii’smanufacturingsectorrealGDPperjobwasabout18.0percentbelowthatof

thetotalindustryaverage.Durablegoodswasabout31.2percentandthenondurablegoodswasabout12.1percentbelowthetotalindustryaverage.Additionally,thelaborproductivityforthemanufacturingsector, especiallynondurable goodsmanufacturing,wasmore volatile than that of the total industryaverageovertime.

FIGURE3

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Hawaii Real GDP Per Job, 1998‐2015

HI Total HI Manufacturing

HI Durable HI Nondurable

P a g e |17

FortheU.S.,however,laborproductivityforthemanufacturingsectorwassignificantlyhigherthantheproductivityfortheaverageofallindustries.Furthermore,thegrowthrateofthemanufacturingsector’slaborproductivity,especiallydurablegoods,washigherthantheoverallproductivitygrowth.Figure4compares theU.S. realGDPper job from1998to2015. Forall industries, realGDPper jobincreased 15.0 percent from $73,243 to $84,246. For the manufacturing sector, real GDP per jobincreased84.7percentfrom$79,029to$145,984.RealGDPperjobfordurablegoodsincreased125.3percentfrom$59,982to$135,121andrealGDPperjobfornondurablegoodsincreased44.3percentfrom $115,369 to $166,458. The gap between durable goods and nondurable goods decreasedsignificantly.

In2015,theU.S.manufacturingsector’srealGDPperjobwasabout73.3percentabovethatof

thetotalindustryaverage.Thedurablegoodscategorywasabout60.4percentandthenondurablegoodscategorywasabout97.6percentabovethetotalindustryaverage.Forthetotalindustryaverage,theU.S.real GDP per jobwas only about 7.0 percent higher than that of Hawaii in 2015. However, for themanufacturingsector,theU.S.realGDPperjobwasabout126.3percenthigherthanthatofHawaii.

FIGURE4

30,000

50,000

70,000

90,000

110,000

130,000

150,000

170,000

190,000

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

U.S. Real GDP Per Job, 1998‐2015

All Industry Manufacturing Durable Nondurable

18|P a g e

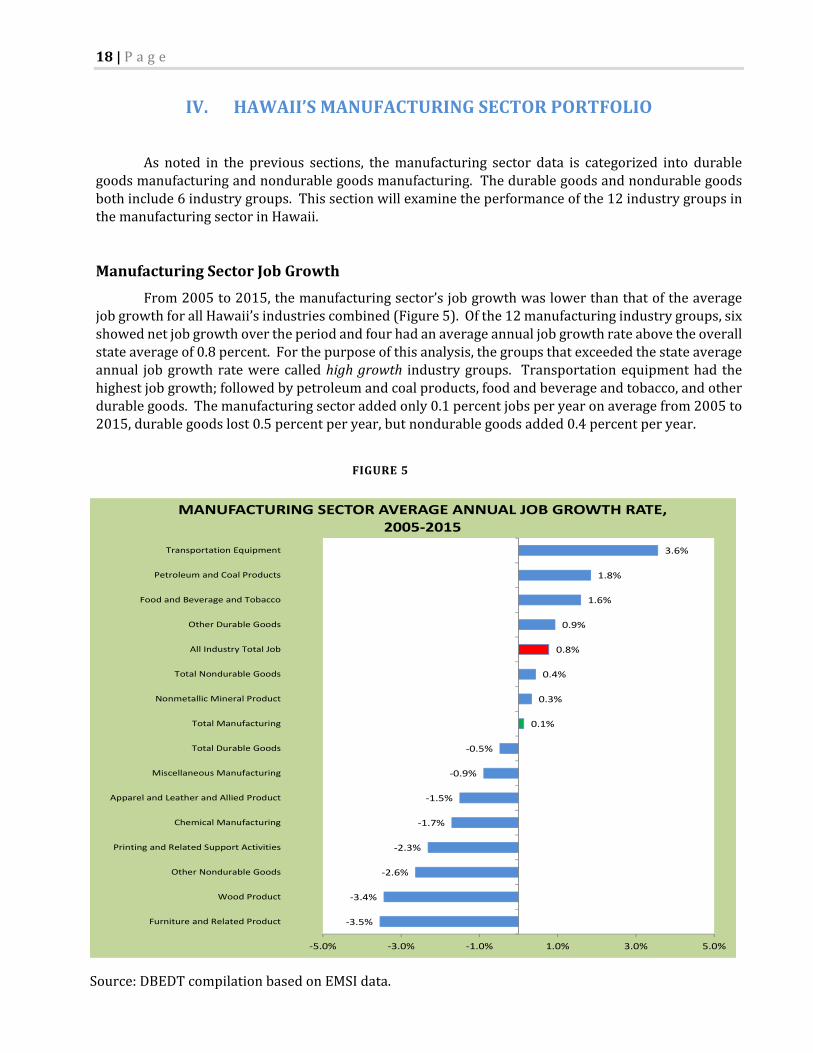

IV. HAWAII’SMANUFACTURINGSECTORPORTFOLIO

As noted in the previous sections, themanufacturing sector data is categorized into durable

goodsmanufacturingandnondurablegoodsmanufacturing.Thedurablegoodsandnondurablegoodsbothinclude6industrygroups.Thissectionwillexaminetheperformanceofthe12industrygroupsinthemanufacturingsectorinHawaii.

ManufacturingSectorJobGrowth

From2005to2015,themanufacturingsector’sjobgrowthwaslowerthanthatoftheaveragejobgrowthforallHawaii’sindustriescombined(Figure5).Ofthe12manufacturingindustrygroups,sixshowednetjobgrowthovertheperiodandfourhadanaverageannualjobgrowthrateabovetheoverallstateaverageof0.8percent.Forthepurposeofthisanalysis,thegroupsthatexceededthestateaverageannual jobgrowthratewerecalledhighgrowth industrygroups. Transportationequipmenthad thehighestjobgrowth;followedbypetroleumandcoalproducts,foodandbeverageandtobacco,andotherdurablegoods.Themanufacturingsectoraddedonly0.1percentjobsperyearonaveragefrom2005to2015,durablegoodslost0.5percentperyear,butnondurablegoodsadded0.4percentperyear.

Source:DBEDTcompilationbasedonEMSIdata.

‐3.5%

‐3.4%

‐2.6%

‐2.3%

‐1.7%

‐1.5%

‐0.9%

‐0.5%

0.1%

0.3%

0.4%

0.8%

0.9%

1.6%

1.8%

3.6%

‐5.0% ‐3.0% ‐1.0% 1.0% 3.0% 5.0%

Furniture and Related Product

Wood Product

Other Nondurable Goods

Printing and Related Support Activities

Chemical Manufacturing

Apparel and Leather and Allied Product

Miscellaneous Manufacturing

Total Durable Goods

Total Manufacturing

Nonmetallic Mineral Product

Total Nondurable Goods

All Industry Total Job

Other Durable Goods

Food and Beverage and Tobacco

Petroleum and Coal Products

Transportation Equipment

MANUFACTURING SECTOR AVERAGE ANNUAL JOB GROWTH RATE, 2005‐2015

FIGURE5

P a g e |19

Whilethisstudyfocusesmoreon long‐termtrends, it is importanttoexaminehowjobs inthemanufacturing sector have been impacted by the recession. The manufacturing sector experiencedseverejoblossesfromtherecessionthatbeganinlate2007.Onlyfivemanufacturingindustrygroupshadpositivejobgrowthduringthe2007‐2015period.Thestrongestperformersduringthisperiodwerethefoodandbeverageandtobaccogroupandthetransportationequipmentgroup.

Thecategoryoffurnitureandrelatedproductexperiencedthemostsignificantjobslossduringthisperiod,followedbyothernondurablegoods,printingandrelatedsupportingactivity,woodproduct,miscellaneousmanufacturing,apparelandleatherandalliedproduct,nonmetallicmineralproduct,andchemicalmanufacturing.

Source:DBEDTcompilationbasedonEMSIdata.

‐5.1%

‐2.8%

‐2.6%

‐2.6%

‐2.4%

‐1.8%

‐1.5%

‐0.8%

‐0.8%

‐0.3%

0.3%

0.4%

0.7%

0.7%

1.4%

1.6%

‐6.5% ‐4.5% ‐2.5% ‐0.5% 1.5%

Furniture and Related Product

Other Nondurable Goods

Printing and Related Support Activities

Wood Product

Miscellaneous Manufacturing

Apparel and Leather and Allied Product

Total Durable Goods

Nonmetallic Mineral Product

Chemical Manufacturing

Total Manufacturing

All Industry Total Job

Total Nondurable Goods

Other Durable Goods

Petroleum and Coal Products

Transportation Equipment

Food and Beverage and Tobacco

MANUFACTURING SECTOR AVERAGE ANNUAL JOB GROWTH RATE, 2007‐2015

FIGURE6

20|P a g e

TABLE4.STATEOFHAWAIIMANUFACTURINGINDUSTRYJOBS

Source:DBEDTcompilationbasedonEMSIdata.

2005 2007 2014 2015 2005‐2007 2007‐2015 2014‐2015 2005‐2015

Transportation Equipment Emerging 574 731 760 814 12.9% 1.4% 7.1% 3.6%

Nonmetallic Mineral Product Emerging 1,219 1,347 1,212 1,260 5.1% ‐0.8% 4.0% 0.3%

Petroleum and Coal Products Emerging 436 494 493 523 6.4% 0.7% 6.1% 1.8%

Other Durable Goods Emerging 905 941 963 993 2.0% 0.7% 3.1% 0.9%

Food and Beverage and Tobacco Emerging 7,403 7,641 8,488 8,666 1.6% 1.6% 2.1% 1.6%

Miscellaneous Manufacturing Declining 1,951 2,170 1,830 1,785 5.5% ‐2.4% ‐2.4% ‐0.9%

Apparel and Leather and Allied Product Declining 1,437 1,431 1,209 1,236 ‐0.2% ‐1.8% 2.2% ‐1.5%

Chemical Manufacturing Declining 509 456 482 429 ‐5.4% ‐0.8% ‐11.1% ‐1.7%

Printing and Related Support Activities Declining 1,463 1,435 1,182 1,158 ‐0.9% ‐2.6% ‐2.1% ‐2.3%

Other Nondurable Goods Declining 967 929 697 741 ‐2.0% ‐2.8% 6.4% ‐2.6%

Wood Product Declining 911 792 622 642 ‐6.7% ‐2.6% 3.2% ‐3.4%

Furniture and Related Product Declining 745 791 519 520 3.1% ‐5.1% 0.1% ‐3.5%

Total Manufacturing Emerging 18,519 19,158 18,457 18,767 1.7% ‐0.3% 1.7% 0.1%

Industry GroupPerformance Class

Jobs Average Annual Job Growth (%)

P a g e |21

NationalCompetitivenessoftheManufacturingSector

Another measure that can help shed light on the manufacturing sector is the performancecomparedwiththenationalindustryaverageforeachgroup.IfaHawaiimanufacturingindustrygrouphasanaverageannualgrowthratethatishigherthanthenationalaverageforthesamegroup,thentheHawaiigroupiseffectivelyincreasingitscompetitiveshareofthetotalnationalindustry.Conversely,ifHawaii’sgrowthrateforarespectiveindustrygroupislessthanthenationalaverage,thentheHawaiigroupiseffectivelydecreasingitscompetitiveshareofthetotalnationalindustry.Figure7showshowmuchmoreorlessHawaii’smanufacturingindustriesgrewperyearonaveragecomparedwiththesameindustriesnationally.Forinstance,overthe2005to2015period,jobsinthetransportationequipmentindustrygroupgrewat anaverageannual rate thatwas4.6percenthigher inHawaii than the sameindustrynationwide.Thus,Hawaii’stransportationequipmentindustrygroupincreaseditscompetitivenationalindustryshare.Ontheotherhand,chemicalmanufacturinglostnationalindustryshareduetoanaverageannualgrowthratethatwas1.1percentbelowthenationalindustrygrowthrate.

Source:DBEDTcompilationbasedonEMSIdata.

‐1.1%

‐0.6%

‐0.1%

0.0%

0.1%

0.2%

0.6%

0.8%

1.3%

1.8%

2.0%

2.1%

2.4%

4.6%

‐2.0% ‐1.0% 0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0%

Chemical Manufacturing

Miscellaneous Manufacturing

All Industry Total

Other Nondurable Goods

Wood Product

Furniture and Related Product

Printing and Related Support Activities

Food and Beverage and Tobacco

Total Manufacturing

Other Durable Goods

Petroleum and Coal Products

Apparel and Leather and Allied Product

Nonmetallic Mineral Product

Transportation Equipment

GAIN OR LOSS OF NATIONAL COMPETITIVE INDUSTRY SHARE, 2005‐2015

Gaining national competitive share

Losing national competitive share

FIGURE7

22|P a g e

Of the 12 industry groups in the manufacturing sector, only three groups lost nationalcompetitive shareover the2005‐2015period. Industries thathavebothpositive jobgrowthandanincreaseincompetitivenationalindustryshare,representthebestperformingindustrygroupsoveragivenperiodoftime.Industrygroupswiththehighercompetitivesharemetricareprobablyshowingahighercomparativeadvantagecomparedwith thenational industry. InHawaii, thesegroups includetransportationequipment,nonmetallicmineralproduct,petroleummanufacturing,otherdurablegoods,andfoodandbeverageandtobacco.

IndustryConcentration–Hawaii’sManufacturingSpecialties

Athirdperformancemetricthathelpsintheevaluationofthemanufacturingindustryportfolioisindustry job concentration (Figure8). This is ameasureof the state’s levelof specialization in eachrespectiveindustryandhelpsshedlightontheindustries’exportpotential.

Source:DBEDTcompilationbasedonEMSIdata.

FIGURE8

P a g e |23

Export activity brings newmoney into the state and is a basis for long‐term industry growth.Unfortunately,estimatesofindustryexportsarenotpartofstandardindustrydataprograms.Thus,itisnotclearhowmuchoutputinagivenmanufacturingindustryisexported.

However,itispossibletoidentifyindustriesthatarelikelyexportbymeasuringtheconcentrationof their employment in the state’s economy. As explained above, an industry that employs ahigherproportionofjobsinHawaiithanthesameindustrynationally,isrelativelymoreconcentratedandismorelikelytobeexportingsomeofitsoutput.

IndustryconcentrationismeasuredbyametriccalledtheLocationQuotientorLQforshort.TheLQforanindustryatthestatelevelthatisequaltotheU.S.levelis1.0. HawaiiindustrieswithanLQmeasureofmorethan1.0aremoreconcentratedinthestateeconomythanthesameindustryfortheU.S.asawhole.Conversely,thoseindustriesthatarebelow1.0arelessconcentratedinstateeconomythantheU.S.aswhole.

Of the12 industrygroups in themanufacturingsector,only theappareland leatherandalliedproductindustrygrouphadaconcentrationlevelinHawaii’seconomythatwashigherthanthesameindustrynationally.IndustriesthatarelessconcentratedinHawaiimayalsobeexportingsomeoftheiroutput.However,amajorityoftheoutputisprobablyservinglocaldemand.

PerformanceMapFramework:IdentifyingEmergingManufacturingIndustries

Aframeworktobetterunderstandtheoverallimplicationsofthesekeyperformancemetricsisthe performance map adapted from the industry life cycle model. The performance map breaksindustriesintheeconomyintofourgeneralizedstagesoflife,startingwithanemergingphase,movingtoabase‐growthindustryphase,followedbyamatureortransitioningphaseandfinallyadecliningphase.Ofcourse,notallindustriesfitnicelyintothisnotion,especiallyovershortperiodsoftime.However,with some qualifications, this notion of development stages can help us evaluate the status of themanufacturingindustryportfolio.

UsingthethreeperformancemetricsfromFigures5,7and8,themanufacturingindustrygroupscan be placed into one of four life‐cycle quadrants according to the criteria shown in Table 5 anddescribedbelow.

TABLE5.PERFORMANCEMAPCRITERIA

TRANSITIONING BASE‐GROWTH

Positivejobgrowth Positivejobgrowth

Losingcompetitivenationalindustryshare Highlyconcentratedintheeconomy

Increasingcompetitivenationalindustryshare

DECLINING EMERGING

Positivejobgrowth

Currentlowconcentrationintheeconomy

Increasingcompetitivenationalindustryshare

Losingjobsoverperiod

24|P a g e

EmergingQuadrant:Theseareindustriesthatarepotentiallyintheearly,take‐offstage. Theyhavebeenperformingwell by showingboth job growthandan increase in their competitive shareof thenationalindustry.However,theseindustrieshaveyettoachieveaconcentrationinthestate’seconomyequaltothesameindustryfortheU.S.asawhole.Anemergingmanufacturingindustryisonethathasfoundacompetitivenicheintheeconomyandisgainingincompetitivenationalindustryshare.Atsomepoint, if the process continues, the industry’s concentration will exceed the national level and theemergingindustrywillgraduatetoabase‐growthindustryinthestate’seconomy.

Base‐GrowthQuadrant:Theseareindustriesthathavebecomepotentialeconomicdrivers.Theyaregrowingtheirjobcountsandareincreasingtheircompetitivenationalindustryshare.Moreover,theyhaveexceededthenationallevelofindustryconcentrationintheeconomyandareprobablyexportingatleastaproportionoftheiroutput.

TransitioningQuadrant:Transitioningmanufacturingindustriesarestillmaintainingorgrowingtheirworkforce,howevertheyarelosingcompetitivenationalindustryshare(growingmoreslowlythanthesameindustrynationally).Thisistypicalofmatureindustriesthatarestillimportanttotheeconomybutarehavingdifficultymaintainingnationalmarketshare.Theyareconsideredtransitioningbecausethey could either continue to lose industry share and eventually fall into decline, or reinvigoratethemselves andbegin to regain industry share and continue growing. Also in this quadrantmaybeformeremergingindustriesthatneverreachedbase‐growthstatusbeforelosingcompetitivenationalindustryshareandsomepreviouslydecliningindustriesthatarefightingbackintocompetitiveness.

DecliningQuadrant: Thedecliningquadrant contains industry groups showing job losses over theperiod. Allof thesemanufacturing industrygroupshave lost jobs tosomeextentbetween2005and2015.Mostindustriesthatarelosingjobsarealsolosingcompetitivenationalindustryshare.However,whiletheyaredeclininginjobsfortheperiod,theseindustriesarenotnecessarilydyingindustries.AnumberoftemporarycircumstancesmayhaveputsomeofHawaii’smanufacturingindustriesintothedecliningquadrantfortheperiodstudied.Theirappearanceinthedecliningquadrantisaredflagthatwarrantsmorecarefulanalysistounderstandtheproblem.

Itshouldbeemphasizedthattheperformancemapframeworkismoreofaguidetounderstandanindustry’ssituationratherthanaconclusionaboutthevalueoftheindustrytothestate.Itprovidesastartingpointforassessingthestrengthsandweaknessesoftheindustriesintheportfolio.Also,itisimportanttonotethat,withinindustriesthatareexperiencingmixedorpoorperformance,theremaybepocketsofverysuccessfulfirms.

P a g e |25

Table6showshoweachoftherespectiveNAICS‐basedmanufacturingindustrygroupsfellontheperformancemapbasedon the2005 to2015performancemeasures. Combined, themanufacturingindustrygroupsaccountedforabout18,767jobsinHawaii’seconomyin2015.

Source:DBEDTcompilationbasedonEMSIdata.*NAdenotesnoindustrygroupsinthecategory

Overall,themanufacturingindustrygroupsadded247jobsbetween2005and2015inHawaii.Thisamountedtoa1.3percentincreaseinjobs.Incontrast,totaljobsinHawaiiincreased8.0percentduringthesameperiod.Basedonjobgrowthalone,theleadingperformersofthemanufacturinggroupswere transportation equipment, petroleumand coal products, food andbeverage and tobacco, otherdurablegoods,andnonmetallicmineralproductgroups. Theearningsaverageof themanufacturingindustryportfoliowas$49,607in2015,whichwaslowerthanthestatewideaverageof$52,156.

There were no manufacturing industry groups that qualified as base‐growth industries ortransitioningindustriesforthe2005to2015period.Theindustrygroupsintheemergingcategorywerecomposed of transportation equipment, petroleum and coal products (mostly petroleum), food andbeverageandtobacco,otherdurablegoods,andnonmetallicmineralproduct.Thesegroupsaccountedforabout65.3percentofthetotalmanufacturingsectorjobsin2015.Thesevenmanufacturingindustrygroupsthatlostjobsinthe2005to2015periodfellintothedecliningquadrantoftheperformancemap.Thesegroupsaccountedforabout34.7percentoftotalmanufacturingsectorjobsin2015.

GroupChange

in Jobs

Average

EarningsGroup

Change in

Jobs

Average

Earnings

NA NA NA NA NA NA

GroupChange

in Jobs

Average

EarningsGroup

Change in

Jobs

Average

Earnings

Miscellaneous Manufacturing ‐8.5% $36,432 Transportation Equipment 41.9% $87,773

Apparel and Leather and Allied Product ‐14.0% $26,515 Petroleum and Coal Products 20.0% $167,531

Chemical Manufacturing ‐15.8% $58,852 Food and Beverage and Tobacco 17.1% $43,151

Printing and Related Support Activities ‐20.8% $36,638 Other Durable Goods 9.7% $64,890

Other Nondurable Goods ‐23.4% $52,318 Nonmetallic Mineral Product 3.3% $68,057

Wood Product ‐29.5% $24,261

Furniture and Related Product ‐30.2% $53,879

Declining Group: 34.7% of Jobs Emerging Group: 65.3% of Jobs

Total Jobs, 2015: 18,767

Average Annual Earnings, 2015: $49,607

Net Change in Jobs, 2005‐2015: 1.3%

Transitioning Group: 0.0% of Jobs Base‐Growth Group: 0.0% of Jobs

TABLE6.MANUFACTURINGINDUSTRYGROUPSMAPPEDBYPERFORMANCE,2005‐2015

26|P a g e

V. MANUFACTURINGINDUSTRYPERFORMANCEBYCOUNTYThe following tables summarize the 2005 to 2015 county performance of the statewide

manufacturing industries (paid employment and self‐employed/sole proprietors). Performance hasbeenorganizedbyBestPerformingTargets(registeringasbase‐growth&emergingindustrygroups)andOtherTargetedIndustryPerformance(thosethatfellintothetransitioninganddecliningcategories).

City&CountyofHonolulu

Honoluluaccountedfor13,870ofthestate’smanufacturingindustryjobsin2015,a0.1percentaverageannualgrowthfrom2005to2015.Theaverageannualjobgrowthratewas1.4percentfrom2005to2007,andwasnegative0.2percentfrom2007to2015.AsshowninTable7,fivemanufacturingindustry groups were in the high performing quadrant in the 2005 to 2015 period. These highperforminggroupsnotonlygrewjobsduringtheperiod,butalsoincreasedtheircompetitiveshareoftheactivitybyexceedingthenationalgrowthratefortheindustry.Theseincludedpetroleumandcoalproducts,foodandbeverageandtobacco,nonmetallicmineralproduct,transportationequipment,andotherdurablegoods.SevenmanufacturingindustrygroupslostjobsinHonoluluCountyoverthe2005to2015period. Apparelandleatherandalliedproductlostthemostjobs,followedbymiscellaneousmanufacturing,printingandrelatedsupportactivities,furnitureandrelatedproducts,othernondurablegoods,woodproduct,andchemicalmanufacturing.

TABLE7.MANUFACTURINGINDUSTRYJOBS,HONOLULU

Source:DBEDTcompilationbasedonEMSIdata.

2005 2007 2014 2015 2005‐2007 2007‐2015 2014‐2015 2005‐2015

Petroleum and Coal Products Base‐Growth 434 494 491 517 6.7% 0.6% 5.2% 1.8%

Food and Beverage and Tobacco Emerging 5,194 5,315 6,198 6,296 1.2% 2.1% 1.6% 1.9%

Nonmetallic Mineral Product Emerging 718 789 719 745 4.8% ‐0.7% 3.7% 0.4%

Transportation Equipment Emerging 537 697 746 796 13.9% 1.7% 6.8% 4.0%

Other Durable Goods Emerging 698 728 757 775 2.1% 0.8% 2.4% 1.0%

Chemical Manufacturing Declining 291 273 246 276 ‐3.2% 0.1% 12.4% ‐0.5%

Miscellaneous Manufacturing Declining 1,544 1,625 1,308 1,267 2.6% ‐3.1% ‐3.1% ‐2.0%

Apparel and Leather and Allied Product Declining 1,314 1,277 1,012 1,036 ‐1.4% ‐2.6% 2.4% ‐2.3%

Printing and Related Support Activities Declining 1,157 1,146 907 884 ‐0.5% ‐3.2% ‐2.6% ‐2.7%

Other Nondurable Goods Declining 874 842 625 663 ‐1.8% ‐2.9% 6.2% ‐2.7%

Wood Product Declining 446 425 286 294 ‐2.4% ‐4.5% 3.0% ‐4.1%

Furniture and Related Product Declining 542 533 320 319 ‐0.8% ‐6.2% ‐0.5% ‐5.2%

Total Manufacturing Emerging 13,749 14,144 13,614 13,870 1.4% ‐0.2% 1.9% 0.1%

Industry Group Performance

Class

Jobs Average Annual Job Growth (%)

P a g e |27

ThecomparisonsofHonoluluCounty’smanufacturingindustryjobsandearningsgrowthwiththestateandnationarelistedinTable8.Forjobgrowth,HonoluluCounty’s0.1percentannualgrowthratewasthesameasthestate’sgrowthratebutwasbetterthanthenationalaverageofnegative1.2percent.Foraverageearnings,HonoluluCountywashigherthanthestate,butlowerthanthenationalaverage.

TABLE8.HONOLULUCOUNTYMANUFACTURINGINDUSTRYPERFORMANCECOMPAREDWITHSTATEANDNATION,2005‐2015

Source:DBEDTcompilationbasedonEMSIdata.

HawaiiCounty

Hawaii County accounted for 2,143 of the state’smanufacturing jobs in 2015, a 0.1 percentaverageannualincreasefrom2005to2015.Theaverageannualjobgrowthratewas7.0percentfrom2005 to 2007. However, since the recession began at the end of 2007, manufacturing job growthdeclined.Ofthe12manufacturingindustrygroupsdefined,only11groupshadjobsinHawaiiCountyin2015.AsshowninTable9,fivemanufacturingindustrygroupswerehighperforminginHawaiiCountyduringthe2005to2015period.Theseincludedfoodandbeverageandtobacco,apparelandleatherandallied product, printing and related support activities, miscellaneous manufacturing, and othernondurablegoods. Sixmanufacturing industrygroups lost jobs inHawaiiCountyduringthe2005to2015period. Woodproducts lost themost jobs, followed bynonmetallicmineral product, chemicalmanufacturing,furnitureandrelatedproduct,transportationequipment,andotherdurablegoods.

Average Annual Job Growth (%)

County State U.S. County State U.S.

Petroleum and Coal Products Base‐Growth 83 1.8% 1.8% ‐0.2% 168,564 167,531 165,867

Food and Beverage and Tobacco Emerging 1,102 1.9% 1.6% 0.8% 114,937 43,151 56,365

Nonmetallic Mineral Product Emerging 27 0.4% 0.3% ‐2.0% 72,999 68,057 63,814

Transportation Equipment Emerging 259 4.0% 3.6% ‐1.0% 88,598 87,773 88,081

Other Durable Goods Emerging 76 1.0% 0.9% ‐0.9% 69,686 64,890 85,680

Chemical Manufacturing Declining ‐15 ‐0.5% ‐1.7% ‐0.6% 61,576 58,852 118,964

Miscellaneous Manufacturing Declining ‐277 ‐2.0% ‐0.9% ‐0.3% 40,217 36,432 75,037

Apparel and Leather and Allied Product Declining ‐278 ‐2.3% ‐1.5% ‐3.6% 54,686 26,515 41,710

Printing and Related Support Activities Declining ‐273 ‐2.7% ‐2.3% ‐2.9% 39,296 36,638 51,809

Other Nondurable Goods Declining ‐211 ‐2.7% ‐2.6% ‐2.6% 52,945 52,318 64,075

Wood Product Declining ‐152 ‐4.1% ‐3.4% ‐3.5% 25,085 24,261 48,255

Furniture and Related Product Declining ‐223 ‐5.2% ‐3.5% ‐3.8% 55,361 53,879 48,572

Total Manufacturing Emerging 121 0.1% 0.1% ‐1.2% 52,730 49,607 76,657

Job Change

2005‐2015

Avg. Annual Earnings (2015)Industry Group Performance

Class

28|P a g e

TABLE9.MANUFACTURINGINDUSTRYJOBS,HAWAIICOUNTY

Source:DBEDTcompilationbasedonEMSIdata.

ThecomparisonofHawaiiCounty’smanufacturingindustryjobsandearningsgrowthwiththestateandnationarelistedinTable10.Forjobgrowth,HawaiiCounty’s0.1percentannualgrowthratewasthesameas thestate’sgrowthrateandabovethenationalaverageofnegative1.2percent. Foraverageearnings,HawaiiCountywaslowerthanthestateandmuchlowerthanthenationalaverage.

TABLE10.HAWAIICOUNTYMANUFACTURINGINDUSTRYPERFORMANCECOMPAREDWITHSTATEANDNATION,2005‐2015

Source:DBEDTcompilationbasedonEMSIdata.

2005 2007 2014 2015 2005‐2007 2007‐2015 2014‐2015 2005‐2015

Food and Beverage and Tobacco Base‐Growth 952 1,134 1,044 1,105 9.2% ‐0.3% 5.8% 1.5%

Apparel and Leather and Allied Product Emerging 57 71 76 73 11.7% 0.4% ‐3.8% 2.6%

Printing and Related Support Activities Emerging 125 133 133 136 3.1% 0.2% 1.7% 0.8%

Miscellaneous Manufacturing Emerging 141 229 183 178 27.4% ‐3.1% ‐2.4% 2.4%

Other Nondurable Goods Emerging 39 34 44 44 ‐5.9% 3.2% 0.3% 1.3%

Other Durable Goods Declining 102 126 87 98 10.9% ‐3.1% 12.1% ‐0.4%

Nonmetallic Mineral Product Declining 235 259 195 198 4.8% ‐3.3% 1.8% ‐1.7%

Furniture and Related Product Declining 115 144 94 87 11.9% ‐6.1% ‐7.3% ‐2.7%

Chemical Manufacturing Declining 94 88 141 63 ‐3.4% ‐4.2% ‐55.4% ‐4.0%

Wood Product Declining 238 199 150 151 ‐8.5% ‐3.4% 0.2% ‐4.5%

Transportation Equipment Declining 27 18 5 10 ‐18.9% ‐6.5% 104.9% ‐9.2%

Total Manufacturing Emerging 2,125 2,434 2,153 2,143 7.0% ‐1.6% ‐0.5% 0.1%

Industry Group Performance

Class

Jobs Average Annual Job Growth (%)

Average Annual Job Growth (%)

County State U.S. County State U.S.

Food and Beverage and Tobacco Base‐Growth 152 1.5% 1.6% 0.8% 42,296 43,151 56,365

Apparel and Leather and Allied Product Emerging 17 2.6% ‐1.5% ‐3.6% 20,292 26,515 41,710

Printing and Related Support Activities Emerging 10 0.8% ‐2.3% ‐2.9% 21,339 36,638 51,809

Miscellaneous Manufacturing Emerging 37 2.4% ‐0.9% ‐0.3% 23,882 36,432 75,037

Other Nondurable Goods Emerging 6 1.3% ‐2.6% ‐2.6% 28,542 52,318 64,075

Other Durable Goods Declining ‐4 ‐0.4% 0.9% ‐0.9% 41,649 64,890 85,680

Nonmetallic Mineral Product Declining ‐37 ‐1.7% 0.3% ‐2.0% 57,952 68,057 63,814

Furniture and Related Product Declining ‐28 ‐2.7% ‐3.5% ‐3.8% 54,333 53,879 48,572

Chemical Manufacturing Declining ‐32 ‐4.0% ‐1.7% ‐0.6% 58,324 58,852 118,964

Wood Product Declining ‐87 ‐4.5% ‐3.4% ‐3.5% 20,209 24,261 48,255

Transportation Equipment Declining ‐17 ‐9.2% 3.6% ‐1.0% 70,508 87,773 88,081

Total Manufacturing Emerging 18 0.1% 0.1% ‐1.2% 39,334 49,607 76,657

Job Change

2005‐2015

Avg. Annual Earnings (2015)Industry Group Performance

Class

P a g e |29

MauiCounty

Ofthe12condensedmanufacturingindustrygroupsdefinedinthisstudy,only11groupshadjobsin2015forMauiCounty.Thesegroupsaccountedfor2,010ofthestate’smanufacturingindustryjobsin2015,anegative0.1percentaverageannualdecreasefrom2005to2015.Theaverageannualjobgrowthwasanegative2.2percentfrom2005to2007andapositive0.4percentfrom2007to2015.AsshowninTable11,sixmanufacturingindustrygroupswerehighperforminginMauiCountyinthe2005to2015period. Theseincludednonmetallicmineralproduct,apparelandleatherandalliedproduct,miscellaneous manufacturing, furniture and related product, and other durable goods. Fivemanufacturing industry groups lost jobs in Maui County over the 2005 to 2015 period. Food andbeverage and tobacco lost the most jobs, followed by printing and related support activities, othernondurablegoods,woodproduct,andchemicalmanufacturing.

TABLE11.MANUFACTURINGINDUSTRYJOBS,MAUICOUNTY

Source:DBEDTcompilationbasedonEMSIdata.

ThecomparisonsofMauiCounty’smanufacturing industry jobsandearningsgrowthwith thestateandnationarelistedinTable12.Forjobgrowth,MauiCounty’snegative0.1percentaverageannualgrowthdeclinewasbelowthestate’spositive0.1percent,butabovethenationalaverageofnegative1.2percent.Foraverageearnings,MauiCountywaslowerthanthestateandmuchlowerthanthenationalaverage.

2005 2007 2014 2015 2005‐2007 2007‐2015 2014‐2015 2005‐2015

Nonmetallic Mineral Product Base‐Growth 188 233 226 244 11.2% 0.6% 7.7% 2.6%

Apparel and Leather and Allied Product Emerging 48 53 78 86 5.7% 6.2% 10.3% 6.1%

Miscellaneous Manufacturing Emerging 196 233 264 265 9.1% 1.6% 0.2% 3.0%

Furniture and Related Product Emerging 57 74 76 94 13.5% 3.2% 24.6% 5.2%

Other Durable Goods Emerging 86 71 89 87 ‐8.8% 2.5% ‐3.1% 0.1%

Transportation Equipment Emerging 5 12 5 5 55.8% ‐10.5% 0.0% 0.0%

Food and Beverage and Tobacco Declining 1,033 932 931 927 ‐5.0% ‐0.1% ‐0.3% ‐1.1%

Wood Product Declining 135 107 109 112 ‐10.8% 0.5% 2.9% ‐1.9%

Chemical Manufacturing Declining 105 74 85 81 ‐15.7% 1.1% ‐4.5% ‐2.5%

Printing and Related Support Activities Declining 131 110 95 94 ‐8.3% ‐2.0% ‐1.1% ‐3.3%

Other Nondurable Goods Declining 48 45 14 15 ‐3.5% ‐12.7% 7.8% ‐11.0%

Total Manufacturing Declining 2,031 1,944 1,972 2,010 ‐2.2% 0.4% 1.9% ‐0.1%

Industry Group Performance

Class

Jobs Average Annual Job Growth (%)

30|P a g e

TABLE12.MAUICOUNTYMANUFACTURINGINDUSTRYPERFORMANCECOMPAREDWITHSTATEANDNATION,2005‐2015

Source:DBEDTcompilationbasedonEMSIdata.

Kauai County

Ofthe12condensedmanufacturingindustrygroupsdefinedinthisstudy,only11groupshadjobsin2015forKauaiCounty.Thesegroupsaccountedfor730ofthestate’smanufacturingindustryjobsin2015,a1.8percentaverageannualincreasefrom2005to2015.Theaverageannualjobgrowthwas1.1 percent from2005 to 2007 and1.9 percent from2007 to 2015. As shown inTable 13, sixmanufacturingindustrygroupsqualifiedashighperforminginKauaiCountyduringthe2005to2015period.Theseincludedotherdurablegoods,apparelandleatherandalliedproduct,othernondurablegoods,foodandbeverageandtobacco,andmiscellaneousmanufacturing.FivemanufacturingindustrygroupslostjobsinKauaiCountyoverthe2005to2015period.

Average Annual Job Growth (%)

County State U.S. County State U.S.

Nonmetallic Mineral Product Base‐Growth 55 2.6% 0.3% ‐2.0% 68,871 68,057 63,814

Apparel and Leather and Allied Product Emerging 39 6.1% ‐1.5% ‐3.6% 10,924 26,515 41,710

Miscellaneous Manufacturing Emerging 69 3.0% ‐0.9% ‐0.3% 26,627 36,432 75,037

Furniture and Related Product Emerging 37 5.2% ‐3.5% ‐3.8% 48,186 53,879 48,572

Other Durable Goods Emerging 1 0.1% 0.9% ‐0.9% 61,678 64,890 85,680

Transportation Equipment Emerging 0 0.0% 3.6% ‐1.0% 71,000 87,773 88,081

Food and Beverage and Tobacco Declining ‐105 ‐1.1% 1.6% 0.8% 43,933 43,151 56,365

Wood Product Declining ‐23 ‐1.9% ‐3.4% ‐3.5% 25,216 24,261 48,255

Chemical Manufacturing Declining ‐23 ‐2.5% ‐1.7% ‐0.6% 54,245 58,852 118,964

Printing and Related Support Activities Declining ‐37 ‐3.3% ‐2.3% ‐2.9% 40,801 36,638 51,809

Other Nondurable Goods Declining ‐33 ‐11.0% ‐2.6% ‐2.6% 47,490 52,318 64,075

Total Manufacturing Declining ‐21 ‐0.1% 0.1% ‐1.2% 43,478 49,607 76,657

Job Change

2005‐2015

Avg. Annual Earnings (2015)Industry Group Performance

Class

P a g e |31

TABLE13.MANUFACTURINGINDUSTRYJOBS,KAUAICOUNTY

Source:DBEDTcompilationbasedonEMSIdata.

ThecomparisonsofKauaiCounty’smanufacturing industry jobsandearningsgrowthwiththestateandnationarelistedinTable14.Forjobgrowth,KauaiCounty’s1.8percentaverageannualgrowthratewasbetterthanthestate’s0.1percentandbetterthanthenationalaverageofanegative1.2percent.Foraverageearnings,KauaiCountywaslowerthanthestateandmuchlowerthanthenationalaverage.

TABLE14.KAUAICOUNTYMANUFACTURINGINDUSTRYPERFORMANCECOMPAREDWITHSTATEANDNATION,2005‐2015

Source:DBEDTcompilationbasedonEMSIdata.

2005 2007 2014 2015 2005‐2007 2007‐2015 2014‐2015 2005‐2015

Other Durable Goods Emerging 15 14 32 38 ‐3.4% 13.2% 17.1% 9.7%

Apparel and Leather and Allied Product Emerging 22 29 40 42 13.8% 5.0% 5.2% 6.7%

Other Nondurable Goods Emerging 9 3 8 15 ‐42.3% 22.3% 87.5% 5.2%

Food and Beverage and Tobacco Emerging 224 259 306 328 7.5% 3.0% 7.5% 3.9%

Miscellaneous Manufacturing Emerging 70 83 74 74 8.9% ‐1.5% ‐0.7% 0.5%

Transportation Equipment Emerging 5 5 5 5 0.0% 0.0% 0.0% 0.0%

Nonmetallic Mineral Product Declining 77 66 72 72 ‐7.3% 1.1% 0.7% ‐0.6%

Wood Product Declining 91 60 78 86 ‐18.9% 4.5% 10.0% ‐0.7%

Printing and Related Support Activities Declining 50 46 47 45 ‐3.6% ‐0.5% ‐5.1% ‐1.2%

Furniture and Related Product Declining 32 41 29 19 14.2% ‐8.9% ‐33.2% ‐4.7%

Chemical Manufacturing Declining 18 20 10 6 3.7% ‐13.9% ‐41.5% ‐10.6%

Total Manufacturing Emerging 614 627 702 730 1.1% 1.9% 4.1% 1.8%

Industry Group Performance

Class

Jobs Average Annual Job Growth (%)

Average Annual Job Growth (%)

County State U.S. County State U.S.

Other Durable Goods Emerging 23 9.7% 0.9% ‐0.9% 34,734 64,890 85,680

Apparel and Leather and Allied Product Emerging 20 6.7% ‐1.5% ‐3.6% 19,571 26,515 41,710

Other Nondurable Goods Emerging 6 5.2% ‐2.6% ‐2.6% 24,000 52,318 64,075

Food and Beverage and Tobacco Emerging 104 3.9% 1.6% 0.8% 40,269 43,151 56,365

Miscellaneous Manufacturing Emerging 4 0.5% ‐0.9% ‐0.3% 36,757 36,432 75,037

Transportation Equipment Emerging 0 0.0% 3.6% ‐1.0% 70,000 87,773 88,081

Nonmetallic Mineral Product Declining ‐5 ‐0.6% 0.3% ‐2.0% 42,116 68,057 63,814

Wood Product Declining ‐6 ‐0.7% ‐3.4% ‐3.5% 27,308 24,261 48,255

Printing and Related Support Activities Declining ‐5 ‐1.2% ‐2.3% ‐2.9% 21,681 36,638 51,809

Furniture and Related Product Declining ‐12 ‐4.7% ‐3.5% ‐3.8% 55,195 53,879 48,572

Chemical Manufacturing Declining ‐12 ‐10.6% ‐1.7% ‐0.6% 58,000 58,852 118,964

Total Manufacturing Emerging 116 1.8% 0.1% ‐1.2% 37,481 49,607 76,657

Job Change

2005‐2015

Avg. Annual Earnings (2015)Industry Group Performance

Class

32|P a g e

VI. MANUFACTURINGINDUSTRYPERFORMANCEBYMAJORGROUPS

This section takesacloser lookat theperformance foreachrespective industrygroup in themanufacturingsector’sportfolio.Asdiscussedearlier,themanufacturingsectorincludedabout18,767jobsin12industrygroupsin2015. Intermsof jobs,these12groupswerecomposedofthetopfivegroups fordurable goods, the top five groups fornondurable goods, one group for all otherdurablegoods,andonegroupforallothernondurablegoods.Theaverageannualearningsforthemanufacturingsectorwas$49,607in2015.Table15showsthemajorindustrygroupsofthemanufacturingsectorandtheirprimaryperformancemetrics.

Amongthenondurablegoodsmanufacturinggroups,thefoodandbeverageandtobaccogrouphad the most jobs in 2015. The 8,666 jobs in this group accounted for 46.2 percent of the totalmanufacturingjobsin2015.Inthenondurablegoodsgroups,boththeapparelandleatherandalliedproductgroupandtheprintingandrelatedsupportactivitieshadmorethan1,100jobsin2015.Thetopgroupindurablegoodsmanufacturingwasmiscellaneousmanufacturing,whichhadabout1,800jobsin2015.Nonmetallicmineralproductinthedurablegoodsgroupsalsohadmorethan1,000jobsin2015.

TABLE15.EMPLOYMENTANDGROWTHINHAWAII’SMANUFACTURINGINDUSTRY

Source:DBEDTcompilationbasedonEMSIdata.

Table 16 compares the U.S. and Hawaii’s real GDP growth rates from 2005 to 2014 for themanufacturingsectorgroupsbasedonBEAdata. For the total, includingall industries, therealGDPannualgrowth rate inHawaiiwasbelow thenational averageby0.2of apercentagepoint. For themanufacturing sector,Hawaii’s negative 0.7 percent annual growth ratewas significantly below thepositive0.7percentannualgrowthforthenation. TherealGDPgrowthratesfordurablegoodsandnondurablegoodsinHawaiiwerebothbelowthenationalaverage.Amongthe12manufacturingsectorgroups,sevengroupsinHawaiiperformedbetterthanthenationintermsofrealGDPgrowthfrom2005to2014.

2005 2015 Hawaii U.S. Hawaii U.S.

Competitive

Share 2005‐

2015

Location

Quotient

(LQ), 2015

Change in

LQ, 2005‐

2015

Total Manufacturing 18,519 18,767 0.1% ‐1.2% 49,607 76,657 1.3% 0.30 0.04

Food and Beverage and Tobacco 7,403 8,666 1.6% 0.8% 43,151 56,365 0.8% 0.97 0.09

Miscellaneous Manufacturing 1,951 1,785 ‐0.9% ‐0.3% 36,432 75,037 ‐0.6% 0.53 ‐0.03

Nonmetallic Mineral Product 1,219 1,260 0.3% ‐2.0% 68,057 63,814 2.4% 0.62 0.14

Apparel and Leather and Allied Product 1,437 1,236 ‐1.5% ‐3.6% 26,515 41,710 2.1% 1.14 0.23

Printing and Related Support Activities 1,463 1,158 ‐2.3% ‐2.9% 36,638 51,809 0.6% 0.47 0.03

Other Durable Goods 905 993 0.9% ‐0.9% 64,890 85,680 1.8% 0.05 0.01

Transportation Equipment 574 814 3.6% ‐1.0% 87,773 88,081 4.6% 0.11 0.04

Other Nondurable Goods 967 741 ‐2.6% ‐2.6% 52,318 64,075 0.0% 0.12 0.00

Wood Product 911 642 ‐3.4% ‐3.5% 24,261 48,255 0.1% 0.31 0.01

Petroleum and Coal Products 436 523 1.8% ‐0.2% 167,531 165,867 2.0% 0.98 0.19

Furniture and Related Product 745 520 ‐3.5% ‐3.8% 53,879 48,572 0.2% 0.26 0.01

Chemical Manufacturing 509 429 ‐1.7% ‐0.6% 58,852 118,964 ‐1.1% 0.11 ‐0.01

Group & Industry

Hawaii Jobs

Avg. Job

Growth Rate,

2005‐2015

Annual Earnings

2015Performance Metrics

P a g e |33

Amongthenondurablegoodsmanufacturinggroups,thefoodandbeverageandtobaccogroupalsoaccountedforthelargestportionofthemanufacturingsector’srealGDPin2014.The$355millionrealGDPinthisgroupaccountedfor31.2percentofthetotalmanufacturingsector’srealGDPin2014.Although this sharewas below this group’s share of totalmanufacturing jobs (46.0 percent), itwassignificantlyhigherthanthesameshareforthenation(11.6percent).ThesecondlargestgroupforrealGDPispetroleumandcoalproducts(mostlypetroleumrefinery). Althoughitonlyaccountedfor2.7percentofthemanufacturingsectorjobsin2014,itsshareofthemanufacturingsector’srealGDPwas22.1percentin2014.Thisvaluewasalsosignificantlyhigherthanthesameshareforthenationat5.3percent.

For durable goods, the top two groupswere nonmetallicmineral product and other durablegoods. Theyaccounted forabout9.7percentand6.3percentofHawaii’smanufacturingrealGDP in2014,respectively.

TABLE16.REALGDPINHAWAIIANDU.S.MANUFACTURINGINDUSTRY

Source:DBEDTcompilationbasedonBEAdata.

Mostofthe12industrygroupsarecomposedofsmallersubgroupsandjobnumbersandaverageearnings data are available for these subgroups. However, GDP data is only available at the largerindustry level and not the subgroup level. Job numbers and average earnings data for the smallerindustrylevelareshownindetailinthefollowingsections.

2005 2014 2005 2014 Hawaii U.S.U.S. Above

HawaiiHawaii U.S.

All Industry Total 64,365 69,662 14,211,385 15,653,000 0.9% 1.1% 0.2%

Manufacturing 1,212 1,139 1,776,685 1,886,153 ‐0.7% 0.7% 1.4% 100.0% 100.0%

Durable Goods Manufacturing 323 321 930,148 1,095,908 ‐0.1% 1.8% 1.9% 28.2% 58.1%

Miscellaneous Manufacturing 44 56 68,049 77,083 2.7% 1.4% ‐1.3% 4.9% 4.1%

Nonmetallic Mineral Product 119 111 55,078 43,007 ‐0.8% ‐2.7% ‐1.9% 9.7% 2.3%

Transportation Equipment 48 56 228,151 261,531 1.7% 1.5% ‐0.2% 4.9% 13.9%

Wood Product 14 8 26,093 21,590 ‐6.0% ‐2.1% 3.9% 0.7% 1.1%

Furniture and Related Product 39 21 39,554 25,124 ‐6.6% ‐4.9% 1.7% 1.8% 1.3%

Other Durable Goods 61 72 531,784 672,264 1.9% 2.6% 0.8% 6.3% 35.6%

Nondurable Goods Manufacturing 891 817 850,561 801,934 ‐1.0% ‐0.7% 0.3% 71.7% 42.5%

Food and Beverage and Tobacco 387 355 212,102 218,906 ‐1.0% 0.4% 1.3% 31.2% 11.6%

Apparel and Leather and Allied Product 23 24 13,281 10,892 0.5% ‐2.2% ‐2.7% 2.1% 0.6%

Printing and Related Support Activities 57 70 44,588 40,720 2.3% ‐1.0% ‐3.3% 6.1% 2.2%

Petroleum and Coal Products 320 252 127,465 99,393 ‐2.6% ‐2.7% ‐0.1% 22.1% 5.3%

Chemical Manufacturing 64 87 284,749 293,876 3.5% 0.4% ‐3.1% 7.6% 15.6%

Other Nondurable Goods 57 40 163,044 137,613 ‐3.9% ‐1.9% 2.0% 3.5% 7.3%

Group & Industry

% of 2014

Manufacture Real

GDP

Hawaii Real GDP U.S. Real GDP Real GDP Annual Growth

34|P a g e

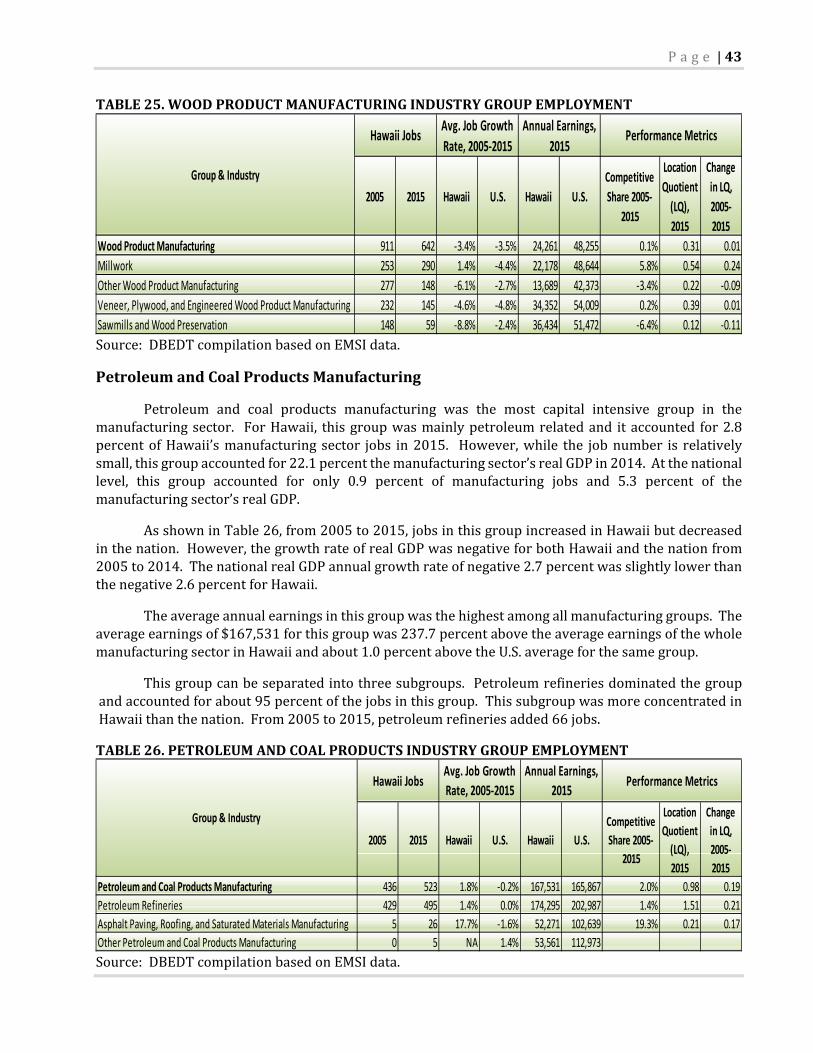

FoodandBeverageandTobaccoManufacturing

Hawaii has no tobacco manufacturing, so this group included only food and beveragemanufacturing.ItwasthelargestgroupforHawaii’smanufacturingsector,bothintermsofjobsandrealGDP.Withabout8,700employees,includingself‐employedworkers,itaccountedforabout46.2percentoftotalmanufacturingjobsin2015.However,theaverageearningsofthisgroupwasonly$43,151in2015,about13.0percentbelowtheaverageearningsforthetotalmanufacturingsectorinHawaii.Theaverageearningsfigurewasabout23.4percentbelowtheU.S.averageforthesamegroup.From2005to2015,jobsinthisgroupincreasedatanaverageannualrateof1.6percent,higherthanthe0.8percentaverageannualgrowthforthenation.

Thisgroupincludestwelvesmallerindustrysubgroups. Nineofthemarefoodmanufacturingrelatedandtheyaccountedforabout88.7percentofjobsinthefoodandbeveragegroup.Thesubgroupswiththemostjobsalsohadthelowestearnings.AsshowninTable17,thelargestsubgroupwasbakeriesandtortilla,whichhadabout2,900jobsandaccountedforabout33.5percentofthejobsinthisgroup.Thesecondlargestsubgroupwasperishablepreparedfood,withabout1,200jobs.Thesetwosubgroupsalsoaddedthemostjobs(877jobsand204jobs,respectively)from2005to2015.Withabout$33,400inannualearnings,thebakeriesandtortillasubgroupwasthelowestinthefoodandbeveragegroup.Theaverageearningsoftheperishablepreparedfoodsubgroupwas$36,166,thethirdlowestannualearningsinthisgroup.

ThesetwosubgroupsaremoreconcentratedinHawaiithanthenation,withLQvaluesin2015equalto1.79and5.07,respectively.Thisisprobablyduetothefactthatasignificantquantityoftheirproductswereeitherconsumedbyvisitorsorexported.OthermoreconcentratedsubgroupsinHawaiiincludesugarandconfectioneryproduct,coffeeandtea,snackfood,softdrink,andbottledwater.Softdrinkmanufacturing,whichhad445jobsin2015,hasthehighestaverageearnings($83,425),followedbydairyproduct($59,186),bottledwater($57,843),andotherbeverageproduct($54,676).From2005to2015,fruitandvegetablepreservingandspecialtyfoodlostthemostjobs(lost188jobs),followedbyanimalslaughteringandprocessing(lost130jobs),andsnackfood(lost45jobs).

P a g e |35

TABLE17.FOODANDBEVERAGEANDTOBACCOINDUSTRYGROUPEMPLOYMENT

Source:DBEDTcompilationbasedonEMSIdata.

MiscellaneousManufacturing

Withabout1,800jobsin2015,orabout9.5percentoftotaljobsinthemanufacturingsector,themiscellaneousmanufacturinggroupwasthelargestgroupfordurablegoodsmanufacturing.However,sincethisgroup’sGDPper jobwasrelatively low, itonlyaccountedforabout4.9percentofthetotalmanufacturingsector’srealGDPin2014,whichwasslightlyabovethe4.1percentfigureforthenation.Theaverageearningsof thisgroupwasonly$36,432 in2015,about26.6percentbelowtheaverageearningsofthetotalmanufacturingsectorinHawaiiandabout51.4percentbelowtheU.S.averageforthesamegroup.From2005to2015,jobsinthisgroupdecreased0.9percentperyearonaverageforHawaii.Incontrast,jobsinthisgroupdecreasedatanaverageannualrateof0.3percentnationally.ThisgroupwaslessconcentratedinHawaii,indicatingthatHawaiiislikelytobeanetimporterforthisgroup.

Thisgroupincludesfiveindustrysubgroups.Jewelryandsilverwaremanufacturinghadthemostjobs(604jobs),withtheotherfoursubgroupseachhavingabout200‐400jobsin2015.AsshowninTable18,medicalequipmentandsupplies,whichmainlyincludeddentallaboratories,hadthehighestaverageannualearnings ($53,487) in thisgroup, followedby sportingandathleticgoods ($44,157),other miscellaneous manufacturing ($36,892), sign manufacturing ($35,231), and jewelry andsilverware($27,177).

Twosubgroups,jewelryandsilverwareandsportingandathleticgoodsweremoreconcentratedinHawaiithanthenation,with2015LQvaluesof3.07and1.16,respectively.Thiswasprobablyduetothefactthatasignificantportionoftheirproductswereeitherconsumedbyvisitorsorexported.

From2005to2015,twoofthesubgroupsaddedjobs.Othermiscellaneousmanufacturingaddedthemost jobs (24 jobs), followedby sporting and athletic goods (18 jobs). Medical equipment andsupplieslost127jobsandjewelryandsilverwaremanufacturinglost76jobs.

2005 2015 Hawaii U.S. Hawaii U.S.

Competitive

Share 2005‐

2015

Location

Quotient

(LQ), 2015

Change in

LQ, 2005‐

2015

Food and Beverage and Tobacco Product 7,403 8,666 1.6% 0.8% 43,151 56,365 0.8% 0.97 0.09

Bakeries and Tortilla 2,025 2,901 3.7% 1.3% 33,378 43,329 2.4% 1.79 0.38

Perishable Prepared Food 988 1,192 1.9% 4.2% 36,166 41,385 ‐2.3% 5.07 ‐1.19

Sugar and Confectionery Product 875 893 0.2% ‐0.1% 49,743 56,996 0.3% 2.37 0.08

Fruit and Vegetable Preserving and Specialty Food 720 533 ‐3.0% 0.0% 35,278 56,538 ‐3.0% 0.61 ‐0.21

Coffee and Tea 407 499 2.0% 5.7% 50,852 59,794 ‐3.6% 3.97 ‐1.61

Soft Drink Manufacturing 442 445 0.1% ‐0.5% 83,425 73,766 0.6% 1.27 0.09

Animal Slaughtering and Processing 570 440 ‐2.6% ‐0.3% 49,843 45,194 ‐2.2% 0.19 ‐0.05

Other Food Manufacturing 285 415 3.8% 0.9% 36,172 75,178 2.9% 0.34 0.09

Dairy Product 356 414 1.5% 0.4% 59,186 69,695 1.1% 0.62 0.07

Snack Food 443 398 ‐1.1% 2.2% 42,124 58,417 ‐3.2% 1.43 ‐0.53

Other Beverage Product Manufacturing 146 298 7.4% 3.7% 54,676 70,808 3.7% 0.40 0.12

Bottled Water Manufacturing 146 240 5.1% ‐0.9% 57,843 69,591 6.0% 3.39 1.52

Hawaii JobsAvg. Job Growth

Rate, 2005‐2015

Annual Earnings,

2015Performance Metrics

Group & Industry

36|P a g e

TABLE18.MISCELLANEOUSMANUFACTURINGINDUSTRYGROUPEMPLOYMENT

Source:DBEDTcompilationbasedonEMSIdata.

NonmetallicMineralProductManufacturing

Thenonmetallicmineralproductmanufacturinggroupwasthesecondlargestgroupfordurablegoodsmanufacturingin2015,withmorethan1,200jobsorabout6.7percentoftotalmanufacturingjobs.Sincethisgroup’sGDPperjobwashigherthantheaverageofthemanufacturingsector,itaccountedforabout9.7percentof thetotalmanufacturingsector’srealGDPin2014. Atthenational level, thisgroupaccountedforonly3.3percentofthemanufacturingjobsand2.3percentofrealGDP.

Theaverageannualearningsinthisgroupwasrelativelyhigh,withaverageannualearningsof$68,057in2015.Theaverageearningsofthisgroupwas37.2percentabovetheaverageearningsofthewholemanufacturingsectorinHawaiiandabout6.6percentabovetheU.S.averageforthesamegroup.From2005to2015,jobsinthisgroupincreasedatanaverageannualrate0.3percentinHawaii,whichwas a sharp contrast to the 2.0 percent average annual decrease for the nation. This group is lessconcentratedinHawaiithanthenation,indicatingthatHawaiiislikelytobeanetimporterforthisgroup.

This group can be separated into four subgroups, but their products aremostly used in theconstructionsector.Cementandconcreteproductmanufacturinghadthemostjobs(773jobs)andtheotherthreesubgroupseachhadabout100‐200jobsin2015.AsshowninTable19,cementandconcreteproductmanufacturinghadthehighestaverageannualearnings($91,006)inthisgroup,followedbyother nonmetallicmineral product ($64,552), glass and glass product ($36,041). Clay product andrefractorymanufacturinghasthelowestaverageearnings($5,704).

AllsubgroupsarelessconcentratedinHawaiiwitha2015LQvaluelessthan1.0.ThisprobablywasduetothefactthatasignificantquantityofconstructionmaterialswasimportedtoHawaii.

From 2005 to 2015, the cement and concrete product subgroup lost 74 jobs, and the othernonmetallic mineral product subgroup lost 54 jobs. Jobs increased the most in clay product andrefractorymanufacturing(135jobs),followedbyglassandglassproduct(54jobs).

Three subgroups, except the other nonmetallicmineral product subgroup, outperformed thenationalaverageintermsofjobgrowthfromthe2005to2015period.TheU.S.lostjobsinallthefoursubgroups.ThejoblossinthecementandconcreteproductsubgroupwasmoresevereatthenationallevelthaninHawaii.

2005 2015 Hawaii U.S. Hawaii U.S.

Competitive

Share 2005‐

2015

Location

Quotient

(LQ),

2015

Change

in LQ,

2005‐

2015

Miscellaneous Manufacturing 1,951 1,785 ‐0.9% ‐0.3% 36,432 75,037 ‐0.6% 0.53 ‐0.03

Jewelry and Silverware 680 604 ‐1.2% ‐2.5% 27,177 51,429 1.3% 3.07 0.42

Other Miscellaneous Manufacturing 334 358 0.7% ‐1.2% 36,892 63,450 1.9% 0.42 0.08

Sign Manufacturing 324 319 ‐0.2% 0.9% 35,231 51,216 ‐1.0% 0.60 ‐0.06

Sporting and Athletic Goods 281 299 0.6% ‐1.3% 44,157 63,281 1.9% 1.16 0.22

Medical Equipment and Supplies 332 205 ‐4.7% 0.3% 53,487 94,764 ‐5.0% 0.13 ‐0.09

Performance Metrics

Group & Industry

Hawaii JobsAvg. Job Growth

Rate, 2005‐2015

Annual Earnings,

2015

P a g e |37

TABLE19.NONMETALLICMINERALPRODUCTINDUSTRYGROUPEMPLOYMENT

Source:DBEDTcompilationbasedonEMSIdata.

ApparelandLeatherandAlliedProductManufacturing

Withmore than1,200 jobs in2015or about6.6percentof the totalmanufacturing jobs, theapparel and leather and allied product group was the second largest group for nondurable goodsmanufacturinginHawaii.Sincethisgroup’sGDPperjobwasrelativelylow,itonlyaccountedforabout2.1percentofthemanufacturingsector’srealGDPin2014.Forthenation,thisgrouponlyaccountedfor1.7percentoftotalmanufacturingjobsand0.6percentofmanufacturingrealGDP.

Duetoincreasedinternationalcompetition,thisgroupdeclinedsignificantlyinboththeU.S.andHawaii. From2005to2015, jobsinthisgroupdecreasedatanaverageannualrateof1.5percent inHawaii,anddecreased3.6percentforthenation. ComparedwiththeU.S.,thisgroupisslightlymoreconcentratedinHawaii.

Theaverageannualearningsofthisgroupwasthesecondlowestamongall12manufacturinggroups inHawaii. Theaverageearningsof$26,515 for thisgroupwasabout46.5percentbelowtheaverage earnings of the totalmanufacturing sector inHawaii and about 36.4 percent below theU.S.averageforthesamegroup.

This group includes three industry subgroups. The cut and sew apparel manufacturingdominatedthegroupandaccountedfor1,047jobsor84.7percentofthejobsinthegroup.Leatherandalliedproducthad116jobsandotherapparelmanufacturinghad73jobsin2015.AsshowninTable20,cutandsewapparelmanufacturinghadthehighestaverageannualearnings($28,044),followedbyleather and allied product ($22,003) and other apparelmanufacturing ($11,702). The cut and sewapparelmanufacturingismoreconcentratedinHawaiithanthenation,witha2015LQvalueof1.50.

From2005to2015,thecutandsewapparelmanufacturingsubgrouplost308jobs,theleatherandalliedproductadded61jobs,andtheotherapparelmanufacturingadded46jobs.

2005 2015 Hawaii U.S. Hawaii U.S.

Competitive

Share 2005‐

2015

Location

Quotient

(LQ),

2015

Change

in LQ,

2005‐

2015

Nonmetallic Mineral Product 1,219 1,260 0.3% ‐2.0% 68,057 63,814 2.4% 0.62 0.14

Cement and Concrete Product 847 773 ‐0.9% ‐2.5% 91,006 65,831 1.6% 0.86 0.13

Clay Product and Refractory 77 211 10.7% ‐3.4% 5,704 53,796 14.1% 0.91 0.68

Other Nonmetallic Mineral Product 203 149 ‐3.1% ‐0.4% 64,552 65,002 ‐2.6% 0.33 ‐0.10

Glass and Glass Product 93 126 3.2% ‐1.9% 36,041 63,775 5.0% 0.28 0.11

Performance Metrics

Group & Industry

Hawaii JobsAvg. Job Growth

Rate, 2005‐2015

Annual Earnings,

2015

38|P a g e

TABLE20.APPARELANDLEATHERANDALLIEDPRODUCTINDUSTRYGROUPEMPLOYMENT

Source:DBEDTcompilationbasedonEMSIdata.

PrintingandRelatedSupportActivities

With 1,158 jobs in 2015 or about 6.2 percent of total jobs in themanufacturing sector, theprinting and related support activities group was the third largest group for nondurable goodsmanufacturinginHawaii.Itaccountedforabout6.1percentofthetotalmanufacturingsector’srealGDPin2014.Nationally,thisgroupaccountedfor4.0percentofthetotalmanufacturingjobsand2.2percentofthemanufacturingsector’srealGDP.

JobsinthisgroupdecreasedinbothHawaiiandthenation.Thistrendcanpartiallybeattributedtoanincreaseindigitalmediaconsumptionattheexpenseofprintmediaconsumption.From2005to2015,jobsinthisgroupdecreasedatanannualaveragerateof2.3percentinHawaiianddecreased2.9percentnationally.From2005to2014,realGDPinthisgroupincreasedatanaverageannualrateof2.3percentinHawaiianddecreased1.0percentforthenation.ComparedwiththeU.S.,thisgroupislessconcentratedinHawaiithanthenation.

Theaverageannualearningsof$36,638wasabout26.1percentlowerthantheaverageearningsofHawaii’stotalmanufacturingsectorandabout29.3percentbelowtheU.S.averageforthesamegroup.

Thisgroupcanbeseparatedintofoursubgroups.Onlythreesubgroupshadjobsin2015andthesupportactivitiesforprintingsubgrouponlyhadafewjobsin2015.AsshowninTable21,commercialprintinghadthehighestaverageannualearnings($41,212), followedbycommercialscreenprinting($28,111).

From2005to2015,jobsdecreasedinallthesubgroups.Commercialprintingexperiencedthegreatestjobloss(172jobs),followedbycommercialscreenprinting(93jobs),andsupportactivitiesforprinting(41jobs).

2005 2015 Hawaii U.S. Hawaii U.S.

Competitive

Share 2005‐

2015

Location

Quotient

(LQ), 2015

Change

in LQ,

2005‐

2015

Apparel and Leather and Allied Product 1,437 1,236 ‐1.5% ‐3.6% 26,515 41,710 2.1% 1.14 0.23

Cut and Sew Apparel Manufacturing 1,355 1,047 ‐2.5% ‐3.9% 28,044 42,255 1.3% 1.50 0.20

Leather and Allied Product 55 116 7.7% 0.0% 22,003 42,688 7.6% 0.54 0.28

Other Apparel Manufacturing 27 73 10.5% ‐6.0% 11,702 38,119 16.4% 0.44 0.35

Performance Metrics

Group & Industry

Hawaii JobsAvg. Job Growth

Rate, 2005‐2015

Annual Earnings,

2015

P a g e |39

TABLE21.PRINTINGANDRELATEDSUPPORTINDUSTRYGROUPEMPLOYMENT

Source:DBEDTcompilationbasedonEMSIdata.

OtherDurableGoodsManufacturing

Theotherdurablegoodsgroupwasthethirdlargestgroupfordurablegoodsmanufacturing,withabout1,000jobsin2015orabout5.3percentofthetotaljobsinthemanufacturingsector.Sincethisgroup’sGDPperjobwashigherthantheaverageofthemanufacturingsector,itaccountedfor6.3percentofHawaii’stotalmanufacturingsector’srealGDPin2014.Atthenationallevel,theroleofthisgroupwassignificantlyhigherthanHawaii,accountingforabout35.1percentofallmanufacturingjobsand35.6percentofthemanufacturingsector’srealGDP.

TheaverageannualearningsinthisgroupwasrelativelyhighcomparedwithothergroupsinHawaii.However,itwasrelativelylowcomparedwiththeaverageannualearningsforthenationoverall.Withanaverageearningsof$64,890in2015,thisgroupwas30.8percentabovetheaverageearningsofthetotalmanufacturingsectorinHawaii,but24.3percentbelowtheU.S.averageforthesamegroup.From2005 to2015, jobs in this group increasedat anaverageannual rateof0.9percent inHawaii,compared with the negative 0.9 percent average annual growth for the nation. This group is lessconcentratedinHawaiithanthenation,indicatingthatHawaiiislikelytobeanetimporterforthisgroup.