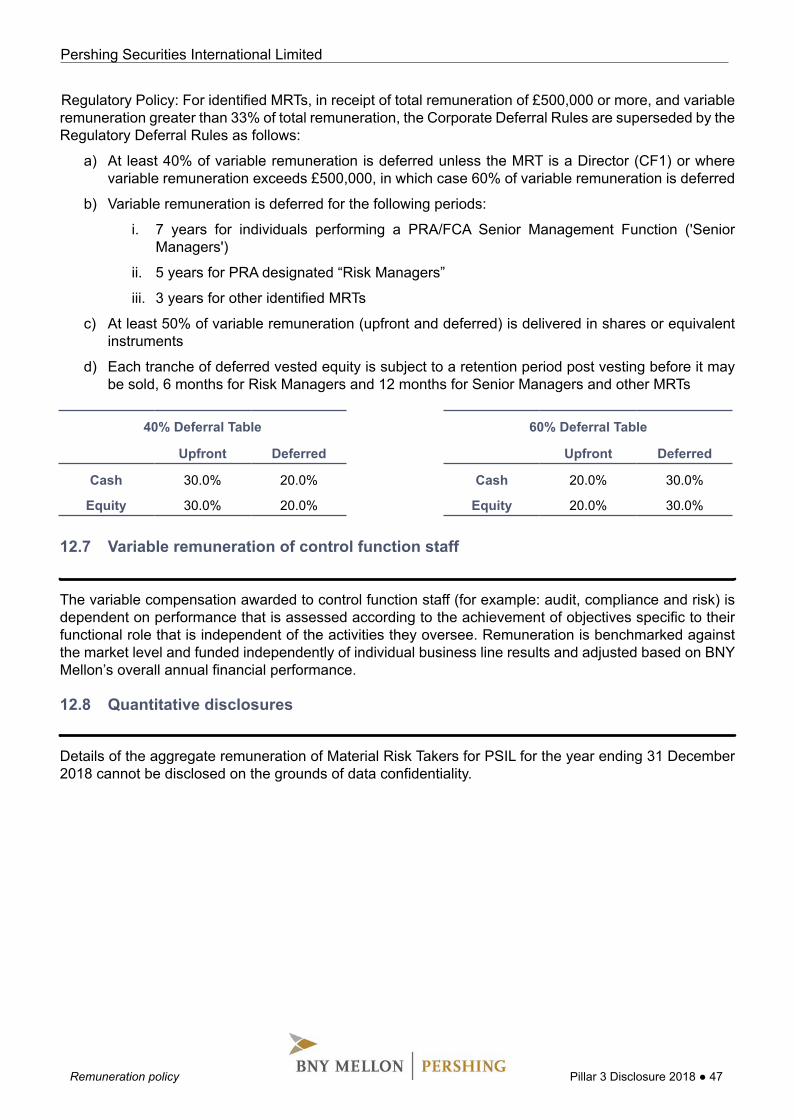

62

Executive summary1 Article 431 CRR - Scope of disclosure requirements ...................................... 61.1 Disclosure policy............................................................................................................... 6

1.2 The Basel III framework.................................................................................................... 7

1.3 Purpose of pillar 3............................................................................................................. 8

1.4 Article 432 CRR - Non-material, proprietary or confidential information........................... 8

1.5 Article 433/434 CRR - Frequency and means of disclosure............................................. 9

1.6 Board approval ................................................................................................................. 9

1.7 Key 2018 and subsequent events .................................................................................... 9

1.8 Key metrics....................................................................................................................... 9

1.9 Article 436 CRR - Scope of application ............................................................................ 11

1.10 Core business lines .......................................................................................................... 12

Capital2 Article 438 CRR - Capital requirements ............................................................ 152.1 Calculating capital requirements ...................................................................................... 16

Risk3 Article 435 CRR - Risk management objectives and policies......................... 173.1 Board of Directors............................................................................................................. 20

3.2 Risk management framework........................................................................................... 22

3.3 Risk appetite..................................................................................................................... 23

3.4 Stress testing.................................................................................................................... 23

4 Article 442 CRR - Credit risk adjustments ........................................................ 244.1 Definition and identification............................................................................................... 25

4.2 Management of credit risk ................................................................................................ 25

4.3 Governance ...................................................................................................................... 26

4.4 Analysis of credit risk........................................................................................................ 26

4.5 Analysis of past due and impaired exposures .................................................................. 28

5 Article 453 CRR - Credit risk mitigation ............................................................ 325.1 Collateral valuation and management .............................................................................. 32

5.2 Wrong-way risk................................................................................................................. 32

5.3 Credit risk concentration................................................................................................... 32

6 Article 444 CRR - External credit rating assessment institutions .................. 34

Pershing Securities International Limited

Pillar 3 Disclosure 2018 ● 2

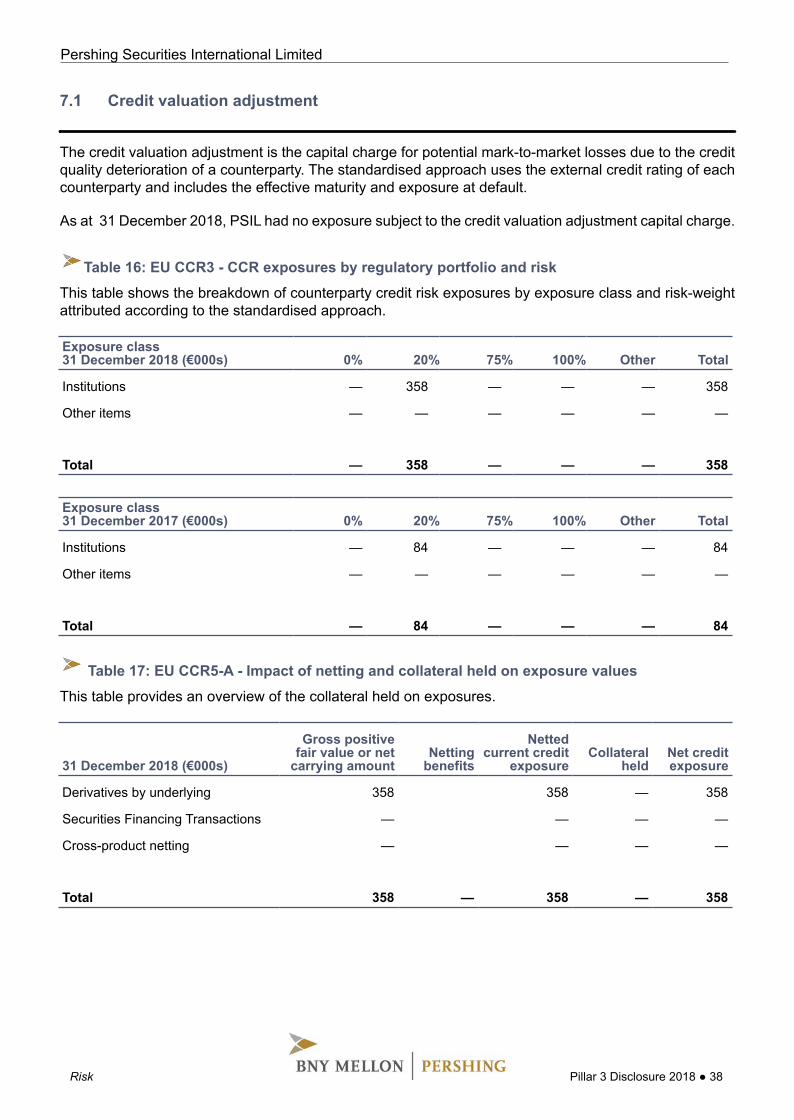

7 Article 439 CRR - Exposure to counterparty credit risk .................................. 377.1 Credit valuation adjustment .............................................................................................. 38

8 Article 443 CRR - Asset encumbrance.............................................................. 399 Article 445 CRR - Exposure to market risk ....................................................... 4110 Article 448 CRR - Interest rate risk in the banking book ................................. 4211 Article 446 CRR - Operational risk .................................................................... 4311.1 Operational risk management framework......................................................................... 43

Human resources12 Article 450 CRR - Remuneration policy ............................................................ 4412.1 Governance ...................................................................................................................... 44

12.2 Aligning pay with performance ......................................................................................... 44

12.3 Fixed remuneration........................................................................................................... 45

12.4 Ratio between fixed and variable pay............................................................................... 45

12.5 Variable compensation funding and risk adjustment ........................................................ 45

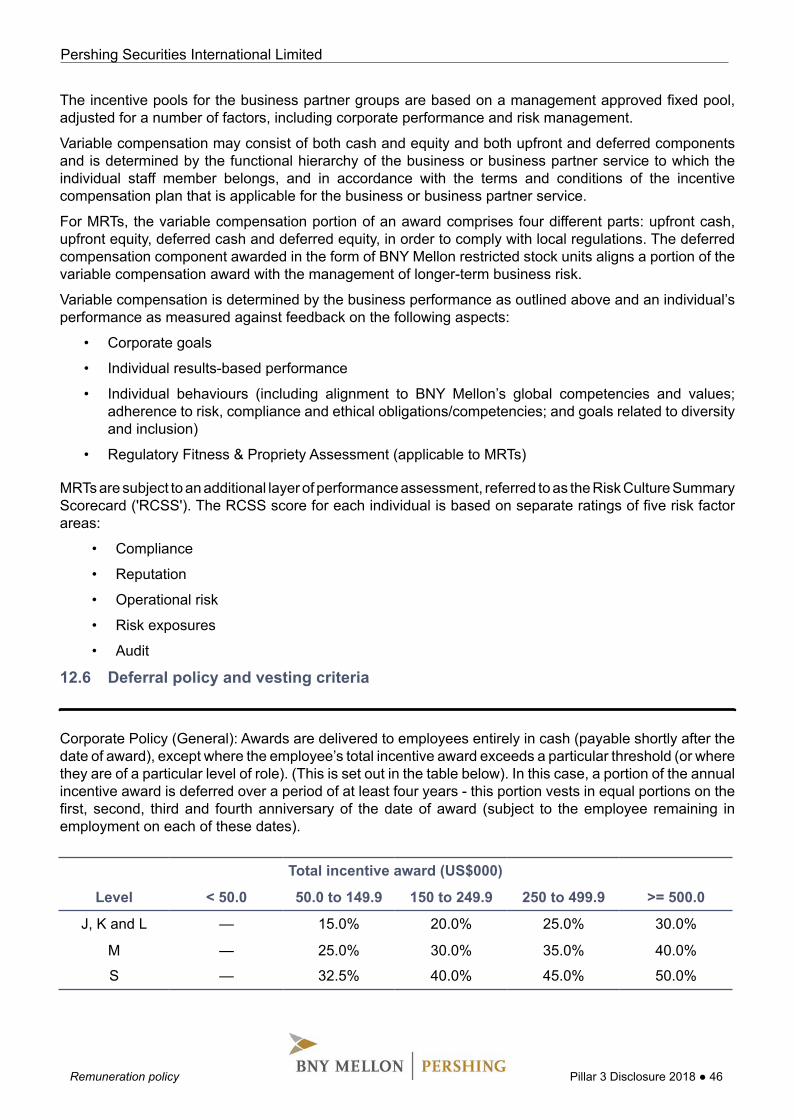

12.6 Deferral policy and vesting criteria ................................................................................... 46

12.7 Variable remuneration of control function staff ................................................................. 47

12.8 Quantitative disclosures ................................................................................................... 47

Pershing Securities International Limited

Pillar 3 Disclosure 2018 ● 3

Any discrepancies between the totals and sums of components within the tables and graphs within this report aredue to rounding.

Index of tablesTable 1: KM1 - Key metrics ................................................................................................................. 10

Table 2: EU OV1 - Overview of RWAs ................................................................................................ 16

Table 3: EU CRB-B - Total and average net amount of exposures ..................................................... 27

Table 4: EU CRB-C - Geographical breakdown of exposures ............................................................ 27

Table 5: EU CRB-D - Concentration of exposures by counterparty types........................................... 28

Table 6: EU CRB-E - Maturity of exposures........................................................................................ 28

Table 7: EU CR1-A - Credit quality of exposures by exposure class and instrument.......................... 29

Table 8: EU CR1-B - Credit quality of exposures by industry.............................................................. 29

Table 9: EU CR1-C - Credit quality of exposures by geography ......................................................... 30

Table 10: EU CR3 - Credit risk mitigation techniques - overview........................................................ 33

Table 11: Mapping of ECAIs credit assessments to credit quality steps ............................................. 34

Table 12: Credit quality steps and risk-weights ................................................................................... 34

Table 13: EU CR4 - Credit risk exposure and credit risk mitigation ('CRM') effects ............................ 35

Table 14: EU CR5 - Credit risk exposure by risk-weight post CCF and CRM..................................... 35

Table 15: EU CCR1 - Analysis of the counterparty credit risk ('CCR') exposure by approach............ 37

Table 16: EU CCR3 - CCR exposures by regulatory portfolio and risk ............................................... 38

Table 17: EU CCR5-A - Impact of netting and collateral held on exposure values ............................. 38

Table 18: AE-A - Encumbered assets.................................................................................................. 39

Table 19: AE-B - Collateral .................................................................................................................. 39

Table 20: AE-C - Sources of encumbrance ......................................................................................... 40

Table 21: EU MR1 - Market risk .......................................................................................................... 41

Pershing Securities International Limited

Pillar 3 Disclosure 2018 ● 4

AppendicesAppendix 1 - Other risks ................................................................................................... 48Liquidity risk...................................................................................................................................... 48

Group risk ......................................................................................................................................... 48

Business and financial risk ............................................................................................................... 48

Residual risk ..................................................................................................................................... 49

Appendix 2 - Glossary of terms........................................................................................ 50

Appendix 3 - CRD IV reference......................................................................................... 55

Pershing Securities International Limited

Pillar 3 Disclosure 2018 ● 5

Executive summary

1 Article 431 CRR - Scope of disclosure requirements

Pershing Securities International Limited

Executive summary Pillar 3 Disclosure 2018 ● 6

1.1 Disclosure policy

This document comprises the Pershing Securities International Limited ('PSIL' or 'the Company') Pillar 3disclosures on capital and risk management at 31 December 2018. These Pillar 3 disclosures are publishedin accordance with the requirements of the Capital Requirements Regulation ('CRR') and the CapitalRequirements Directive ('CRD') referred to together as CRD IV, which came into effect on 1 January 2014.CRD IV has the effect of implementing the international Basel III reforms of the Basel Committee on BankingSupervision within the European Union. The Pillar 3 disclosure requirements are contained in Part Eightof the CRR, in particular articles 431 to 455.

Pillar 3 disclosures are required for a consolidated group and for those parts of the group covered by CRDIV. When assessing the appropriateness of these disclosures in the application of Article 431(3) of theCRR, PSIL has ensured adherence to the following principles of:

Clarity Meaningfulness

Consistency over time Comparability across institutions

The Basel Committee on Banking Supervision ('BCBS') requires these disclosures to be published at thehighest level of consolidation. PSIL has adopted this approach with information presented at a fullyconsolidated level.

Information in this report has been prepared solely to meet the Pillar 3 disclosure requirements of the entitynoted, and to provide certain specified information about capital and other risks and details about themanagement of those risks, and for no other purpose. These disclosures do not constitute any form offinancial statement of the business nor do they constitute any form of contemporary or forward lookingrecord or opinion of the business.

Unless indicated otherwise, information contained within this document has not been subject to externalaudit.

CET1 ratio = CET1 capital / Pillar 1 RWAs Tier 1 ratio = Tier 1 capital / Pillar 1 RWAs Total capital ratio = Total capital / Pillar 1 RWAs

The following risk metrics present PSIL's risk components as at 31 December 2018. Please seepage 10 for the full comprehensive list capital ratios.

Common Equity Tier 1 ratio 167.3% Ý2017: 157.4%

Tier 1 capital ratio 167.3% Ý2017: 157.4%

Total capital ratio 167.3% Ý2017: 157.4%

Pershing Securities International Limited

Executive summary Pillar 3 Disclosure 2018 ● 7

1.2 The Basel III framework

Basel III is the international banking accord intended to strengthen the measurement and monitoring offinancial institutions’ capital. The Basel III framework was implemented in the European Union through theCapital Requirements Directive ('CRD') and establishes a more risk sensitive approach to capitalmanagement. It is comprised of three pillars

Pillar 1 - Minimum capital requirement:

Establishes rules for the calculation of minimum capital for credit risk, counterparty credit risk,market risk and operational risk

Pillar 2 - Supervisory review process:

Requires firms and supervisors to undertake an internal capital adequacy assessment process todetermine whether the financial institution needs to hold additional capital against risks notadequately covered in Pillar 1 and to take action accordingly

Pillar 3 - Market discipline:

Complements the other two pillars and effects market discipline through public disclosure showingan institution’s risk management policies, approach to capital management, its capital resourcesand an analysis of its credit risk exposures

Wherever possible and relevant, the PSIL Board of Directors ('the Board') will ensure consistency betweenPillar 3 disclosures, Pillar 1 reporting and Pillar 2 Internal Capital Adequacy Assessment Process ('ICAAP')content.

Pershing Securities International Limited

Executive summary Pillar 3 Disclosure 2018 ● 8

1.3 Purpose of pillar 3

Pillar 3 requires the external publication of exposures and associated risk-weighted assets and the approachto calculating capital requirements for the following risk and exposure types:

Credit risk Counterparty credit risk Asset encumbrance Market risk

Interest rate risk Operational risk Leverage

These Pillar 3 disclosures only focus on those risk and exposure types relevant to PSIL.

PSIL includes both quantitative and qualitative disclosures to show the relevant information and describeits approach to capital management, its capital resources and an analysis of its risk exposures. Thedisclosures also include, where appropriate, comparative figures for the prior year and an analysis of themore significant movements to provide greater insight into its approach to risk management.

For completeness, other risks that PSIL is exposed to, but are not covered above, are also discussed inAppendix 1.

1.4 Article 432 CRR - Non-material, proprietary or confidential information

In accordance with CRD IV, the Board may omit one or more disclosures if the information provided is notregarded as material. The criteria for materiality used in these disclosures is that the PSIL will regard asmaterial any information where its omission or misstatement could change or influence the assessment ordecision of a user relying on that information for the purpose of making economic decisions.

Furthermore, the Board may omit one or more disclosures if the information provided is regarded asproprietary or confidential. Information is regarded as proprietary if disclosing it publicly would underminethe company’s competitive position. It may include information on products or systems which, if sharedwith competitors, would render an institution’s investment therein less valuable. In such circumstance, theBoard will state in its disclosures the fact that specific items of information are not disclosed and the reasonfor non-disclosure. In addition it will publish more general information about the subject matter of thedisclosure requirement except where these are to be classified as confidential.

PSIL undertakes no obligation to revise or to update any forward-looking or other statement containedwithin this report regardless of whether or not those statements are affected as a result of new informationor future events.

1.5 Article 433/434 CRR - Frequency and means of disclosure

Disclosure will be made annually based on calendar year end and will be published in conjunction with thepreparation of the Annual Report and Financial Statements. PSIL will reassess the need to publish someor all of the disclosures more frequently than annually in light of any significant change to the relevantcharacteristics of its business including disclosure about capital resources and adequacy, and informationabout risk exposure and other items prone to rapid change. This will be periodically reassessed and updatedin light of market developments associated with Pillar 3.

Disclosures are published on the Pershing and The Bank of New York Mellon Corporation group websiteswhich can be accessed using the link below:

Pershing - Disclosures - Financial & Regulatory Disclosures

BNY Mellon - Investor Relations - Pillar 3 Disclosures

Pershing Securities International Limited

Executive summary Pillar 3 Disclosure 2018 ● 9

1.6 Board approval

These disclosures were approved for publication by the Board on 17 July 2019. The Board has verifiedthat the disclosures are consistent with formal policies adopted regarding production and validation andare satisfied with the adequacy and effectiveness of the risk management arrangements.

1.7 Key 2018 and subsequent events

The Board periodically reviews the strategy of PSIL and the associated products and services it providesto clients. This generally takes place during the first quarter of each year following the yearly refresh of thelegal entity strategy.

Brexit

In relation to the assessment and monitoring of economic, political and regulatory risks, the Company iscontinuing to evaluate the impact of the outcome of the referendum in relation to the UK’s membership ofthe EU on the Company’s business strategy and business risks in the short, medium and long term. In theshort term the Pershing Brexit Programme has determined that there is no significant impact expected onthe Company’s business activities, there will be no immediate change in business strategy, and we havetherefore determined that the going concern position of the Company is not affected. The Company willcontinue to closely monitor developments and will make appropriate changes to the business strategy asthe impact on the UK and European financial services industries becomes clearer.

1.8 Key metrics

The following risk metrics reflect PSIL’s risk profile:

Regulatory capital (€m) Risk-weighted assets (€m)

2018 *2017

31 28

2018 *2017

18.5 18.1

CET1 ratio Total capital ratio

2018 *2017

167.3% 157.4%

2018 *2017

167.3% 157.4%

Pershing Securities International Limited

Executive summary Pillar 3 Disclosure 2018 ● 10

Table 1: KM1 - Key metrics

*2017 figures have been updated to include all final audit adjustments

Own Funds 2018 *2017

Available capital (€000s)

Common Equity Tier 1 ('CET1') capital 30,905 28,457

Tier 1 capital 30,905 28,457

Total capital 30,905 28,457

Risk-weighted assets (€000s)

Total risk-weighted assets ('RWA') 18,473 18,079

Risk-based capital ratios as a percentage of RWA

CET1 ratio 167.3% 157.4%

Tier 1 ratio 167.3% 157.4%

Total capital ratio 167.3% 157.4%

1.9 Article 436 CRR - Scope of application

Pershing Securities International Limited ('PSIL') is a private company incorporated and domiciled in theRepublic of Ireland. PSIL's immediate parent undertaking is Pershing Limited ('PL'), which is, in turn asubsidiary of Pershing Holdings (UK) Limited ('PHUK'). Pershing Holdings (UK) Limited is a holdingcompany for a group of subsidiaries which provide a full range of execution, middle-office and post-tradeservices, investment administration, Self-Invested Personal Pension ('SIPP') operation services and relatedservices. Pershing Holdings (UK) Limited is incorporated in the UK and is a operationally independentsubsidiary of Pershing Group LLC which is, in turn a subsidiary of the Bank of New York Mellon Corporation.

Pershing Group LLC is engaged in broadly the same business activity as PSIL.

BNY Mellon Group ('BNY Mellon') is a global investments company dedicated to helping its clients manageand service their financial assets throughout the investment lifecycle. Whether providing financial servicesfor institutions, corporations or individual investors, BNY Mellon delivers informed investment managementand investment services in 35 countries and more than 100 markets. As of 31 December 2018, BNY Mellonhad $33.1 trillion in assets under custody and/or administration, and $1.7 trillion in assets undermanagement. BNY Mellon can act as a single point of contact for clients looking to create, trade, hold,manage, service, distribute or restructure investments. BNY Mellon is the corporate brand of The Bank ofNew York Mellon Corporation (NYSE: BK). Additional information is available on www.bnymellon.com.Follow us on Twitter @BNYMellon or visit our newsroom at www.bnymellon.com/newsroom for the latestcompany news.

PSIL is a €125k minimum capital investment firm regulated by the Central Bank of Ireland ('CBI'), PSIL isrequired to operate under the CBI’s Basel III implementation rules, which include the disclosures providedin this document.

There is no current or foreseen material or legal impediments to the prompt transfer of capital resourcesor repayment of liabilities among the parent undertaking and its subsidiary undertakings.

The legal entity structure of PSIL is illustrated in Figure 1.

Pershing Securities International Limited

Executive summary Pillar 3 Disclosure 2018 ● 11

Figure 1: PSIL legal entity structure at 31 December 2018

Basis of consolidation

Entity nameConsolidationbasis Services provided

Pershing SecuritiesInternational Limited ('PSIL')

No subsidiariesfor consolidation

PSIL's principal activities are the provision of execution,middle‑office and post‑trade services, investment administrationand related services.

Pershing Securities International Limited

Executive summary Pillar 3 Disclosure 2018 ● 12

1.10 Core business lines

The principal activities of PSIL include the provision of a full range of clearing and settlement, investmentadministration, global custody and related services. PSIL functionality provides broker-dealers, assetmanagers, intermediary firms and financial institutions with a comprehensive range of services andsolutions, including retail clearing, institutional global clearing, broker services, with execution servicesbeing facilitated through PSL.

The financial strength of PSIL's ultimate parent BNY Mellon, a G-SIFI (Global Systemically ImportantFinancial Institution) is viewed as giving PSIL a competitive advantage in the market place. The PSILbusiness model inherently carries less balance sheet risk than many traditional financial services firms.

PSIL’s business model is split into two main market segments:

Institutional Broker Dealer Services ('IBD')

PSIL provides a broad range of financial business solutions to broker-dealers.

Our multi-asset class solutions combine sophisticated front-end technology with flexible middle and backoffice capabilities. PSIL can manage and help our clients with the full spectrum of post-trade services, fromexecution through to settlement and clearing, specialising in Fixed Income and Equities across 40+ markets.

Our clients recognise us as an industry leader in directing them to operate more efficiently by affordingthem the facility to outsource any, or all, of their trade life-cycle. Our clients leverage upon our technology,strength and global stability and as such we have become a trusted and independent partner to manyfinancial institutions.

We retain our leadership by investing heavily in our technology, so that our customers can be confident inthe knowledge that the functionality and capability of our systems and services will continually meet theirindustry needs, whilst simultaneously addressing the ever changing regulatory landscape, thereby enablingthem to focus on their core business proposition and future proof their corporate positioning.

Wealth and Adviser Solutions ('WAS')

PSIL specialises in providing administration and custody services to wealth management professionals.Many of our clients prefer to outsource back and middle office functions to PSIL so they can focus onserving their existing clients and developing new business. Clients benefit from reduced operational costs,PSIL’s expertise in meeting regulatory requirements and the knowledge of holding their end investorsassets with the world’s largest global custodian.

Clients include wealth managers, advisers and independent financial advisor ('IFA') consolidators thatprovide platform services for smaller IFA firms.

Many wealth management firms are large enough to self-clear their business and most will choose to dothis. However, the increasing rate of technological change, transparency in pricing exerting a downwardpressure on charges, and the increasing cost of regulatory demands can reduce profit margins and sothere is a general industry trend for wealth management firms to consider other ways of working to reducecosts.

Contract basis

Clients contract on a basis appropriate to their business needs, either Model A, Model B, WAS or GlobalClearModel, as outlined below.

Model A

Under Model A client firms contract to outsource their settlement and clearing functions to PSIL. Allsettlement accounts are maintained in the name of the client and PSIL has no settlement obligation to anycounterparty, except where it is providing a General Clearing Member ('GCM') service. Therefore, in allother cases, PSIL is not exposed to any credit and market risk relating to such activity. PSIL does howeverhave credit exposure as a GCM, as it assumes an obligation to deliver cash and stock to the CentralCounterparty ('CCP') and is reliant upon receiving cash or stock from the CCP or client firm.

Model B

The largest portion of PSIL’s business is contracted on a Model B basis where we assume the settlementobligations of clients and it is PSIL’s name not the clients in the market place. The main risk exposure fromthis activity relates to credit risk arising from clients failing to meet their corresponding obligations to PSIL.However the actual exposure is generally limited to any adverse mark to market movement in the underlyingsecurities and is mitigated through various techniques and processes, including credit risk monitoring,rights over retained commissions earned by client firms and cash collateral deposits.

Pershing Securities International Limited

Executive summary Pillar 3 Disclosure 2018 ● 13

WAS Model

The WAS Model is very similar to Model B, but utilises less functionality than is available for Model B clients.Trades are routed exclusively to PSL for execution only where the underlying investor has cash or stockon their accounts. The single execution counterparty for the WAS client is PSL. Also, because tradeinstructions will not be accepted/dealt by PSL unless cash or stock is on the end investors accounts thereis no requirement for a client cash deposit.

GlobalClear

The GlobalClear Model is designed as an intermediate model. The model utilises key Model A componentswhere, for non-GCM trades, PSIL does not assume the settlement obligations of clients as we do underModel B. Clients support these trades on their own balance sheet and PSIL is under no obligation to clearsuch transactions. GlobalClear also utilises key Model B components where the client uses PSIL’s networkfor clearing of GCM trades and PSIL’s settlement network for settlement of GCM and non-GCM transactions.Clients also use PSIL for associated cash and network management.

Pershing Securities International Limited

Executive summary Pillar 3 Disclosure 2018 ● 14

Capital

2 Article 438 CRR - Capital requirements

The following risk metrics present PSIL's risk components as at 31 December 2018.

Total pillar 1 risk exposure amount €18m ó2017: €18m

Total pillar 1 capital requirement €1.48m Ý2017: €1.45m

PSIL has an Internal Capital Adequacy Assessment Process ('ICAAP') which defines the risks that PSILis exposed to, and sets out the associated capital plan which aims to ensure that PSIL holds an appropriateamount of capital to support its business model, through the economic cycle and given a range of plausiblebut severe stress scenarios. The plan is reflective of PSIL’s commitment to a low risk appetite, with noproprietary trading, coupled with a strong capital structure which gives the necessary confidence to ourclients.

Pershing Securities International Limited

Capital Pillar 3 Disclosure 2018 ● 15

2.1 Calculating capital requirements

CRD IV allows for different approaches towards calculating capital requirements. PSIL has chosen to usethe standardised approach where risk weights are based on the exposure class to which the exposure isassigned and its credit quality. These risk-weights used to assess requirements against credit exposuresare consistent across the industry.

For investment firms, in the sense of Article 20(2) of the Capital Requirements Directive 6, the minimumcapital requirement is the higher of the sum of credit risk and market risk or the Fixed Overhead Requirement('FOR').

Pershing Securities International Limited

Capital Pillar 3 Disclosure 2018 ● 16

Table 2: EU OV1 - Overview of RWAs

This table shows the risk-weighted assets using the standardised approach and their respective capitalrequirements

*Standardised approach

PSIL significantly exceeds the minimum capital ratios required to maintain a well-capitalised status and toensure compliance with regulatory requirements at all times. PSIL sets the internal capital target levelshigher than the minimum regulatory requirements to ensure there is a buffer which reflects balance sheetvolatility. These ratios have been determined to be appropriate, sustainable and consistent with the capitalobjectives, business model, risk appetite and capital plan.

Type of risk (€000s)

Risk exposure amount Capital requirements

31-Dec-18 31-Dec-17 31-Dec-18 31-Dec-17

Credit risk* 8,566 11,667 685 933

Counterparty credit risk* 72 17 6 1

Settlement risk* 59 91 5 7

Market risk* 423 564 34 45

of which: Foreign exchange position risk* 423 564 34 45

Total (credit risk and market risk) 9,120 12,339 730 987

Fixed overhead requirement 18,473 18,079 1,478 1,446

Pillar I requirement 18,473 18,079 1,478 1,446

Total capital 30,905 28,457

Surplus capital 29,427 27,010

Risk

3 Article 435 CRR - Risk management objectives and policies

PSIL adopts a prudent approach to all elements of risk to which it is exposed. It is risk averse by natureand manages its business activities in a manner consistent with the tolerances and limits defined within itsrisk appetite quantitative and qualitative measures.

PSIL seeks to manage risk through a collection of complementary processes and methodologies, designedto enable risks to be consistently identified, measured, managed and ultimately reported through itsgovernance structure.

Clients and other market participants need to have confidence that PSIL will remain strong and continueto deliver operational excellence and maintain an uninterrupted service throughout market cycles andespecially during periods of market turbulence. PSIL is committed to maintaining a strong balance sheetand this philosophy is also consistent with PL, PHUK, PGL and BNY Mellon as a whole.

Whilst PSIL assumes less balance sheet risk than most financial services companies due to its focus ontransaction processing, its business model does give rise to some risk as described below. As aconsequence, Pershing has developed a risk management program that is designed to ensure that:

• Risk tolerances (limits) are in place to govern its risk-taking activities across all businesses andrisk types

• Risk appetite principles are incorporated into its strategic decision making processes

Pershing Securities International Limited

Risk Pillar 3 Disclosure 2018 ● 17

• An appropriate risk framework is in place to identify, manage, monitor and report on risk within thegovernance structure

• Monitoring and reporting of key risk metrics to senior management and the Board takes place

• There is a capital planning process based on a stress testing programme

Risk statement

As part of a global investment company, risk is a fundamental characteristic of our business. As such, ourapproach to risk taking and how we consider risk relative to reward directly impacts our success. We have,therefore, established what we consider acceptable risk and set limits on the level and nature of the riskthat we are willing and able to assume in achieving our strategic objectives and business plans. Our RiskAppetite Statement ("RAS") serves this purpose and guides our decision-making processes, including themanner by which we pursue our business strategy and the method by which we manage risk and determinewhether our risk position is within our risk appetite.

The RAS outlined below describes both the nature of, and our tolerance for, the material risks that areinherent in our business. Because reputational risk typically arises as a consequence of another risk event,it is not explicitly described. However, maintaining a strong brand and reputation is fundamental to ourability to attract and retain clients. As such, we consider reputational impact as part of our overall riskmanagement process. Similar to reputational risk, litigation risk is often an outcome of another risk eventand is therefore not individually described. However, the financial services industry continues to faceincreasingly large adverse litigation outcomes that can substantively impact capital position. As such,litigation risk is a key consideration within our overall risk management framework.

The Board adopts a prudent approach to all elements of risk to which it is exposed. It is risk averse bynature and manages its business activities in a manner consistent with the tolerances and limits definedwithin it risk appetite quantitative and qualitative measures. These measures and thresholds are built intoits operating processes and governance structures.

PSIL business model is centered upon the provision of a broad range of financial business solutions tobroker-dealers, wealth managers, financial planners and advisers across EMEA. We provide sophisticatedfront-end technology and flexible middle office capabilities with settlement and custody services. Theseare supported by a robust regulatory and compliance framework with dedicated client asset experienceand expertise.

PSIL’s strategy is to strengthen its digital offering, whilst continuing to concentrate upon the delivery ofservices that are essential to the current marketplace that focuses upon operational and market efficient,advanced technology solutions and fully meets regulatory expectations.

PSIL is faced with complex statutory and regulatory requirements that are evolving and intensifying as newmarket and regulatory reforms are implemented. Select new reforms could impact our business activityand strategy creating both risk and opportunity that we seek to fully mitigate and leverage.

PSIL seeks to maintain a strong liquidity profile by actively managing its liquidity positions and ensuringthat there are sufficient deposits and funding in place to meet timely payment and settlement obligationsunder both normal and stressed conditions.

PSIL seeks to minimise credit and market risk to the amount and type appropriate for it to accept in orderto execute its principal activities. This is achieved through the monitoring and managing of establishedmark-to-market portfolio tolerances, tailored credit limits and collateral management.

Given the nature of the PSIL business, the potential for operational risk is inherent. While we seek tomitigate such risk through the application of a prudent control framework across three lines of defence, werecognise that a moderate degree of residual risk is intrinsic and forms part of our overall appetite.

Pershing Securities International Limited

Risk Pillar 3 Disclosure 2018 ● 18

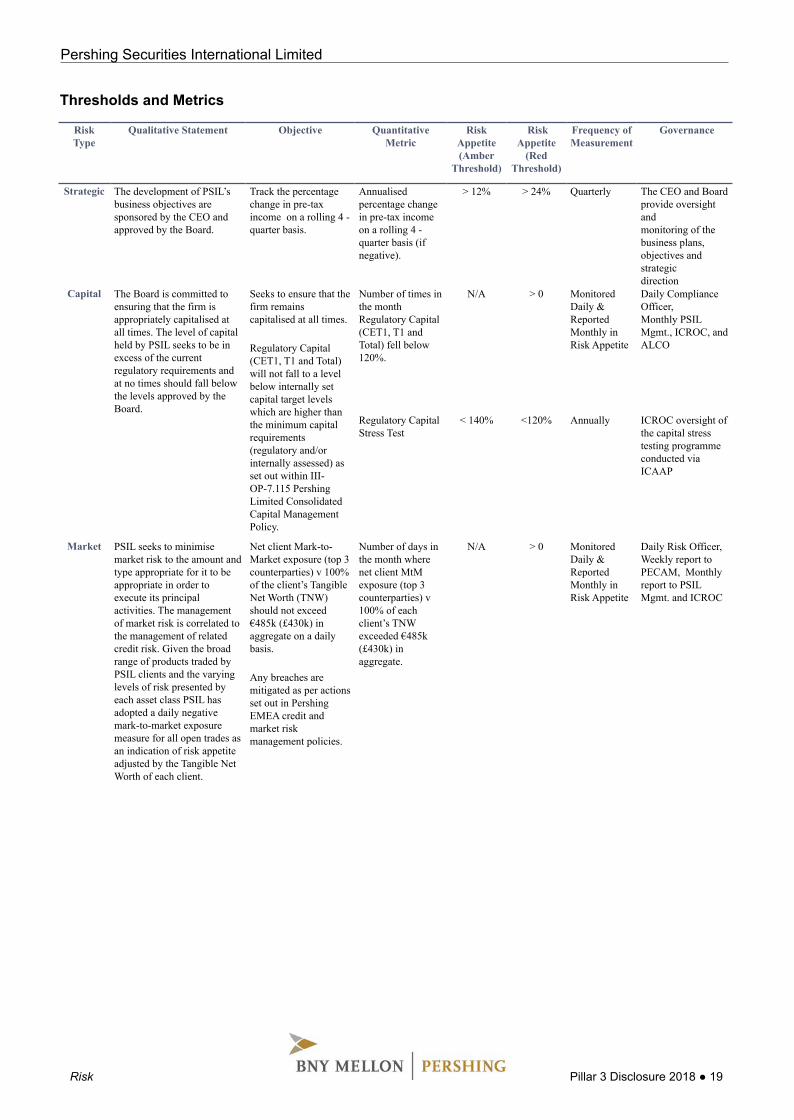

Thresholds and Metrics

RiskType

Qualitative Statement Objective QuantitativeMetric

RiskAppetite(Amber

Threshold)

RiskAppetite

(RedThreshold)

Frequency ofMeasurement

Governance

Strategic The development of PSIL’sbusiness objectives aresponsored by the CEO andapproved by the Board.

Track the percentagechange in pre-taxincome on a rolling 4 -quarter basis.

Annualisedpercentage changein pre-tax incomeon a rolling 4 -quarter basis (ifnegative).

> 12% > 24% Quarterly The CEO and Board provide oversightand monitoring of the business plans, objectives andstrategicdirection

Capital The Board is committed toensuring that the firm isappropriately capitalised atall times. The level of capitalheld by PSIL seeks to be inexcess of the currentregulatory requirements andat no times should fall belowthe levels approved by theBoard.

Seeks to ensure that thefirm remainscapitalised at all times.

Regulatory Capital(CET1, T1 and Total)will not fall to a levelbelow internally setcapital target levelswhich are higher thanthe minimum capitalrequirements(regulatory and/orinternally assessed) asset out within III-OP-7.115 PershingLimited ConsolidatedCapital ManagementPolicy.

Number of times inthe monthRegulatory Capital(CET1, T1 andTotal) fell below120%.

N/A > 0 MonitoredDaily &ReportedMonthly inRisk Appetite

Daily ComplianceOfficer,Monthly PSILMgmt., ICROC, andALCO

Regulatory CapitalStress Test

< 140% <120% Annually ICROC oversight ofthe capital stresstesting programmeconducted viaICAAP

Market PSIL seeks to minimisemarket risk to the amount andtype appropriate for it to beappropriate in order toexecute its principalactivities. The managementof market risk is correlated tothe management of relatedcredit risk. Given the broadrange of products traded byPSIL clients and the varyinglevels of risk presented byeach asset class PSIL hasadopted a daily negativemark-to-market exposuremeasure for all open trades asan indication of risk appetiteadjusted by the Tangible NetWorth of each client.

Net client Mark-to-Market exposure (top 3counterparties) v 100%of the client’s TangibleNet Worth (TNW)should not exceed€485k (£430k) inaggregate on a dailybasis.

Any breaches aremitigated as per actionsset out in PershingEMEA credit andmarket riskmanagement policies.

Number of days inthe month wherenet client MtMexposure (top 3counterparties) v100% of eachclient’s TNWexceeded €485k(£430k) inaggregate.

N/A > 0 MonitoredDaily &ReportedMonthly inRisk Appetite

Daily Risk Officer,Weekly report toPECAM, Monthlyreport to PSILMgmt. and ICROC

Pershing Securities International Limited

Risk Pillar 3 Disclosure 2018 ● 19

RiskType

Qualitative Statement Objective QuantitativeMetric

RiskAppetite(Amber

Threshold)

RiskAppetite

(RedThreshold)

Frequency ofMeasurement

Governance

Credit Collateralised Lending riskPSIL provides a limitedamount of credit facilities inthe form of margin financeand securities finance to asmall number of clients.

Daily oversight of theactive clients’ marginexcess/deficit via theirdaily Margin Statementas uploaded to theclients’ FTP site.

Number of days inthe month theclients MarginStatement was indeficit.

> 1 > 2 MonitoredDaily, Weekly& ReportedMonthly inRisk Appetite

Daily Risk OfficerWeekly reported toPECAM Monthly report toPSIL Mgmt. andICROC

Provision of CreditFacilities riskOther than above, PSIL doesnot actively sell or providecredit facilities to clientsexcept to the extent that thisis required to facilitate thesettlement of trades.

Daily oversight ofactive clients' MtMexposure as % of theirTNW to seek to ensureremains is withinagreed internal limits.

Average number ofactive clientswhose daily MtMexposure (top 3counterparties)exceeded 100% oftheir TNW.

> 0 > 1 MonitoredDaily, Weekly& ReportedMonthly inRisk Appetite

Daily Risk OfficerWeekly reported toPECAM Monthly report toPSIL Mgmt. andICROC

Counterparty risk PSIL seeks to minimise itsbank counterparty riskthrough selective andconservative placementprocess. PSIL seeks to minimise itscounterparty credit riskthrough its prudent approvalprocess and monitoring.

Establish and monitorclient free money bankdeposits and seek toensure compliance withpolicy, risk appetiteand regulatoryrequirement.

The number ofPSIL Client MoneyBank Accountsbreaches of thePSIL Bank andCustodian ReviewPolicy (III-OP-7.061).

N/A > 0 MonitoredDaily, Weekly& ReportedMonthly inRisk Appetite

Daily Risk OfficerWeekly reported toPECAM Monthly report toPSIL Mgmt. andICROC

Pershing Securities International Limited

Risk Pillar 3 Disclosure 2018 ● 20

3.1 Board of Directors

The main duty and responsibility of the Board is to define the strategy of PSIL and to supervise themanagement of PSIL. Whilst acting autonomously and in accordance with its legal and regulatoryrequirements, the Board also aligns PSIL’s strategy to that of its primary shareholder, Pershing Limited.The Board has overall responsibility for the establishment and maintenance of PSIL’s risk appetiteframework and for the approval of the risk appetite statement. The Board ensures that strategic businessplans are consistent with the approved risk appetite.

The Board is also responsible for both the management and the oversight of risks, together with the qualityand effectiveness of internal controls, but delegates risk management oversight to general management,supported by the risk management committees. It is also responsible for reviewing, challenging andapproving all risk management processes including risk identification and assessment, stress testing andcapital adequacy. The various control functions provide further support for the management of risk withinthe business.

The Board meets at least quarterly and the directors who served during 2018 were:

Boardmember Function at PSIL

Name of the othercompany in which anexternal function isexercised

Location(country)

Type ofactivities

Listedcompany(Y/N)

Externalmandate(title)

Capitalconnectionwith PSIL(Y/N)

J Duffy Non-executiveDirector

N Harrington Chief ExecutiveOfficer

Note: All Board members have no material interest of more than 1% in the share capital of the ultimate holdingcompany or its subsidiaries Note: E Canning appointed as director effective from April 25, 2018

Boardmember Function at PSIL

Name of the othercompany in which anexternal function isexercised

Location(country)

Type ofactivities

Listedcompany(Y/N)

Externalmandate(title)

Capitalconnectionwith PSIL(Y/N)

K MolonyChair andIndependentNon-executiveDirector

G Towers ExecutiveDirector

J Wheatley Non-executiveDirector

E Canning ExecutiveDirector Providence Row United

KingdomSocial workactivities,housing

NChair oftheTrustees

N

Pershing Securities International Limited

Risk Pillar 3 Disclosure 2018 ● 21

3.1.1 Risk committees

PSIL Risk Governance

The PSIL Board is the senior strategic and decision making body. The Board delegates day to dayresponsibility for managing the business to the Executive Committee of Pershing Limited ('ExCo') accordingto approved plans, policies and risk appetite.

ExCo further delegates specific responsibilities to various committees and councils to provide an appropriateoversight and direction to various risk and regulatory processes and activities, including:

Pershing Risk Committee

The Pershing Risk Committee ('PRC') provides a senior management oversight to the overall risk frameworkand identified risk types that could potentially impact PL entities including PSIL. The PRC reports to ExCoand forms a central point for the oversight and management of risk and the escalation of significant riskissues and events to PSIL Senior Management, ICROC and the PSIL Board. Subsidiary risk committeesand councils report to the PRC to ensure a consistent and effective reporting of risks and these includethe Credit and Market Risk Committee, the Business Acceptance Committee, Asset and Liability Committee,and the Client Assets Council. PRC is chaired by the Chief Risk Officer.

Credit and Market Risk Committee

The Credit and Market Risk Committee ('PECAM') oversees the review of all credit and market risk issuesassociated with and impacting on business undertaken by PL entities including PSIL. The committee’sprincipal credit risk responsibility is to achieve and maintain an acceptable credit exposure to PSIL’s clients,as well as to market makers, custodians and banks. PECAM is chaired by the Director of Credit and MarketRisk.

Asset and Liability Committee

The Asset and Liability Committee ('ALCO') is responsible for overseeing the asset and liability managementactivities of the balance sheet of PL entities including PSIL, and for ensuring compliance with all treasuryrelated regulatory requirements.

ALCO is responsible for ensuring that the policy and guidance set through the BNY Mellon’s Global ALCOand EMEA ALCO is understood and executed locally. This includes the strategy related to the investment

portfolio, placements, interest rate risk, capital management and liquidity risk. ALCO is chaired by theChief Financial Officer.

Irish Compliance, Risk and Oversight Committee

The Irish Compliance, Risk and Oversight Committee ('ICROC') assist the Board of PSIL and ExCo inoverseeing PSIL's compliance with its regulatory, risk and legal obligations including adherence toapplicable Irish laws, guidelines and notices effecting its operations and regulatory requirements andguidelines issued by the Central Bank of Ireland and with PL's compliance, risk and oversight policies.ICROC is chaired by PSIL Chief Executive Office.

Business Acceptance Committee

The Business Acceptance Committee ('BAC') is an integral part of the new business process and isresponsible for the review and approval of all new clients, products/services and material changes to existingprocesses before they are executed or implemented and includes responsibility for the pricing of new clientactivity, products and services for all PL entities including PSIL. It is chaired by the PL Chief ExecutiveOfficer and includes representatives of all of the risk and control functions, as well as line support functions.

Audit Oversight Review Council

The Audit Oversight Review Council provides review, discussion and challenge of control related issueswithin all PL entities including PSIL. The Council’s responsibilities include discussing emerging controlrisks, thematic control concerns or weaknesses and considering possible means to monitor, control ormitigate such exposures.

Client Asset Council

The Client Asset Council is responsible for the oversight and governance of all PL entities including PSILand ensuring PSIL adherence to the CBI custody and client money rules. The council reports to the PRCto confirm the adequacy of systems and controls in place to ensure that the seven client asset core principlesare fully adhered to in accordance with regulatory rules.

Pershing Securities International Limited

Risk Pillar 3 Disclosure 2018 ● 22

3.2 Risk management framework

Suitable policies and procedures have been adopted by PSIL in order to ensure an appropriate level ofrisk management is directed at the relevant element of the business. In line with global policy, PSIL hasadopted the ‘Three Lines of Defense’ model in deploying its risk management framework (figure 2 below).

Figure 2: Managing Three Lines of Defense

Pershing Securities International Limited

Risk Pillar 3 Disclosure 2018 ● 23

3.3 Risk appetite

The Board adopts a prudent approach to all elements of risk to which it is exposed. It is risk averse bynature and manages its business activities in a manner consistent with the tolerances and limits definedwithin its risk appetite quantitative and qualitative measures. These measures and thresholds are built intoits operating processes and governance structures. The risk appetite statement describes both the natureof, and tolerance for, the material risks that are inherent in PSIL’s business.

3.4 Stress testing

Capital Stress testing is undertaken at PSIL to monitor and quantify risk exposures and capital requirementsto ascertain whether or not there are sufficient capital resources on a forward-looking basis. The processinvolves developing stressed scenarios that identify an appropriate range of adverse circumstances ofvarying nature, severity and duration relevant to PSIL’s risk profile and business activities. Scenarios arederived from current, emerging, and plausible future risks and strategy, and reviewed, discussed and agreedby ICROC, PRC, ExCo and the Board.

4 Article 442 CRR - Credit risk adjustments

The following risk metrics present PSIL's risk components as at 31 December 2018.

Standardised net credit exposure amount €39m Ý2017: €29m

Total on and off-balance sheet exposures €39m Ý2017: €29m

Standardised credit exposure by Standardised credit exposure by country at 31 December 2018 country at 31 December 2017

UK

Belgium Ireland

US

FranceOther

France

Ireland

Belgium

UK

USOther

Standardised net credit exposure by Standardised net credit exposure by counterparty at 31 December 2018 counterparty at 31 December 2017

Corporates

Institutions

Other items Corporates

Institutions

Other items

Pershing Securities International Limited

Risk Pillar 3 Disclosure 2018 ● 24

4.1 Definition and identification

Credit risk is the risk of loss in the event that a client, underlying investor or counterparty fails to meet itscontractual obligations to PSIL.

On-balance sheet credit risk covers default risk for loans, commitments, securities, receivables and otherassets where the realisation of the value of the asset is dependent on the counterparty’s ability andwillingness to repay its contractual obligations.

The nature of PSIL’s business as a provider of clearing and settlement services results in credit risk mainlyarising from the risk of loss in the event that a client, underlying client or market counterparty fails to meetits contractual obligations to pay for a trade, or to deliver securities for sale. However, the legal structureof the clearing agreements provides PSIL with the right to set-off any indebtedness of underlying clientsagainst any credit balance in the name of the same underlying client. PSIL also has recourse to securitiesand cash as collateral and indemnities from client firms in respect of any underlying clients. Consequently,the residual credit risk (i.e. post-mitigation) will devolve to market risk, as the exposure in such cases isthe movement in the underlying financial instruments and foreign currency prices. In addition, PSIL alsorequires most clients to place a security deposit with PSIL to cover this potential mark to market exposure.

Credit risk also arises from the non-payment of other receivables, cash at bank, loans to third parties,investment securities and outstanding client invoices and loans to third parties.

Pershing Securities International Limited

Risk Pillar 3 Disclosure 2018 ● 25

4.2 Management of credit risk

PSIL manages credit risk exposure by a two-stage process:

1) Setting minimum thresholds for the type of client acceptable to PSIL in terms of tangible net worthand business profile, including:

• The type of business to be conducted through PSIL (e.g. retail vs. institutional; agency/matched principal vs. proprietary trading / market making)

• Markets and financial instruments in which the client can trade

• Any special conditions clients are subject to (e.g. cash on account)

Obtaining credit approval for a particular client is the primary responsibility of the business as thefirst line of defence alongside guidance and oversight from Credit Risk as the second line of defence.Any new relationship requires approval from the Business Acceptance Committee.

2) Monitoring all exposure (both pre- and post-settlement) on a daily basis against various limits forits clients, as follows:

• Trade limit (set per client following analysis of the financial strength, management expertise,nature of business and expected or historical peak and average exposure levels)

• Gross exposure limit (calculated with reference to the security deposit and tangible net worthof the client and utilised as the higher of total purchases or total sales)

• Negative mark-to-market exposure

Breaches are reported to senior management which may lead to management action such asrequesting additional collateral, or requiring the client to inject additional capital into the business.

4.3 Governance

Governance of credit risk oversight as a second line of defence function is described and controlled throughcredit risk policies and day-to-day procedures as follows:

• Credit Risk Policy for each legal entity describes the outsourcing of credit risk tasks, defines rolesand responsibilities and requires reporting to be carried out to each business line and entity thatthe policy applies to. Any deviation from approved policy requires either senior business or seniorlegal entity approval depending on the type of event

• Approvals for excesses are controlled using a matrix of credit risk approval authorities held withinthe Credit Risk Policy, each Credit Risk Officer has his/her own individual delegated approvalauthority granted by the Director of Credit and Market Risk. He/she must act within those limitswhen making approvals. If an excess is beyond the officer’s approval limit, it is escalated to a moresenior officer as per the applicable Credit Risk Policy. The outsourcing of credit responsibility toCredit Risk is through the Board approved Credit Risk Policy

• Daily exposure reports are reviewed and signed by a senior member of the Credit Risk Department.The Credit & Market Risk Committee reviews the top exposure items for each client and counterpartyweekly; monthly reports are reviewed by ICROC and PRC within the overall framework set by thePSIL Risk Appetite Statement. At each of these monitoring and review stages action points arerecorded to follow up on breaches.

Pershing Securities International Limited

Risk Pillar 3 Disclosure 2018 ● 26

4.4 Analysis of credit risk

Total net exposures at 31 December 2018 Average net exposures over 2018

Corporates

Institutions

Other items Corporates

Institutions

Other items

PSIL’s minimum credit risk capital requirement is calculated using the standardised approach and isexpressed as 8% of risk-weighted exposures. Where available, issuer ratings from External Credit RatingAssessment Institutions ('ECAI') are used in the determination of the relevant risk-weighting across allexposure classes. Where ECAI ratings differ, the more conservative rating is applied.

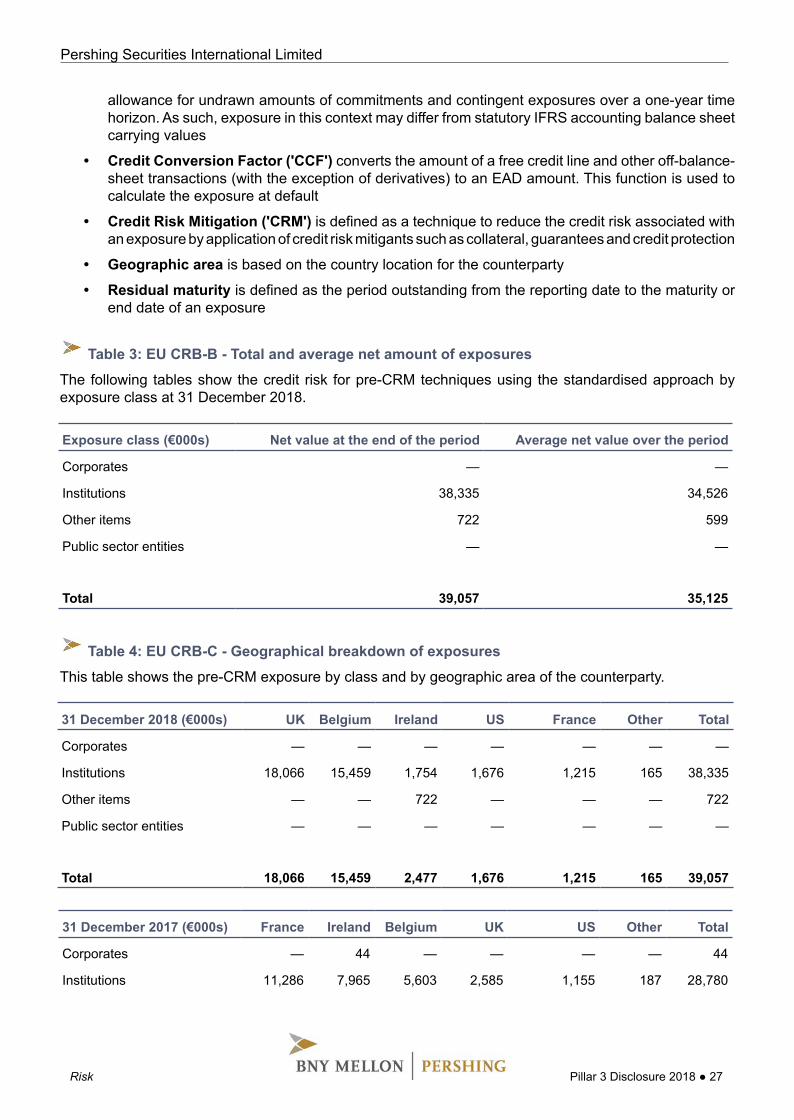

The definitions below are used in the following tables:

• Exposure at Default ('EAD') is defined as the amount expected to be outstanding, after any creditrisk mitigation, if and when a counterparty defaults. Exposure reflects drawn balances as well as

allowance for undrawn amounts of commitments and contingent exposures over a one-year timehorizon. As such, exposure in this context may differ from statutory IFRS accounting balance sheetcarrying values

• Credit Conversion Factor ('CCF') converts the amount of a free credit line and other off-balance-sheet transactions (with the exception of derivatives) to an EAD amount. This function is used tocalculate the exposure at default

• Credit Risk Mitigation ('CRM') is defined as a technique to reduce the credit risk associated withan exposure by application of credit risk mitigants such as collateral, guarantees and credit protection

• Geographic area is based on the country location for the counterparty

• Residual maturity is defined as the period outstanding from the reporting date to the maturity orend date of an exposure

Pershing Securities International Limited

Risk Pillar 3 Disclosure 2018 ● 27

Table 3: EU CRB-B - Total and average net amount of exposures

The following tables show the credit risk for pre-CRM techniques using the standardised approach byexposure class at 31 December 2018.

Exposure class (€000s) Net value at the end of the period Average net value over the period

Corporates — —

Institutions 38,335 34,526

Other items 722 599

Public sector entities — —

Total 39,057 35,125

Table 4: EU CRB-C - Geographical breakdown of exposures

This table shows the pre-CRM exposure by class and by geographic area of the counterparty.

31 December 2017 (€000s) France Ireland Belgium UK US Other Total

Corporates — 44 — — — — 44

Institutions 11,286 7,965 5,603 2,585 1,155 187 28,780

31 December 2018 (€000s) UK Belgium Ireland US France Other Total

Corporates — — — — — — —

Institutions 18,066 15,459 1,754 1,676 1,215 165 38,335

Other items — — 722 — — — 722

Public sector entities — — — — — — —

Total 18,066 15,459 2,477 1,676 1,215 165 39,057

31 December 2017 (€000s) France Ireland Belgium UK US Other Total

Other items — 363 — — — — 363

Public sector entities — — — — — — —

Total 11,286 8,372 5,603 2,585 1,155 187 29,187

Pershing Securities International Limited

Risk Pillar 3 Disclosure 2018 ● 28

Table 5: EU CRB-D - Concentration of exposures by counterparty types

This table shows the credit exposure pre-CRM classified by class and by counterparty type.

At 31 December 2018(€000s)

Generalgovernments

Creditinstitutions

Other financialcorporations

Various balancesheet Items Total

Corporates — — — — —

Institutions — 38,335 — — 38,335

Other items — — — 722 722

Public sector entities — — — — —

Total — 38,335 — 722 39,057

Table 6: EU CRB-E - Maturity of exposures

This table shows the exposure pre-credit risk mitigation, classified by credit exposure class and residualmaturity.

At 31 December 2018 (€000s)On

demand <= 1 year> 1 year

<= 5 years > 5 yearsNo stated

maturity Total

Corporates — — — — — —

Institutions 38,335 — — — — 38,335

Other items 722 — — — — 722

Public sector entities — — — — — —

Total 39,057 — — — — 39,057

4.5 Analysis of past due and impaired exposures

An aspect of credit risk management relates to problem debt management, which entails early problemidentification through to litigation and recovery of cash where there is no realistic potential for rehabilitation.

The following tables provide an analysis of past due and impaired exposures using the following definitions:

• Past due exposure is when a counterparty has failed to make a payment when contractually due

• Impaired exposure is when the entity does not expect to collect all the contractual cash flows whenthey are due

As at 31 December 2018, PSIL had no material impaired assets for which a specific or general provisionwas required. There were no material assets past due greater than 90 days. PSIL did not incur any materialwrite-offs of bad debts or make any recovery of amounts previously written off during the year.

Pershing Securities International Limited

Risk Pillar 3 Disclosure 2018 ● 29

Table 7: EU CR1-A - Credit quality of exposures by exposure class and instrument

This table provides a comprehensive picture of the credit quality of on- and off-balance sheet exposures.

31 December 2018(€000s)

ExposuresCredit risk

adjustmentsAccumulated

write-offs

Credit riskadjustmentcharges ofthe period

NetvaluesDefaulted

Non-defaulted Specific General

General governments — — — — — — —

Credit institutions — 38,335 — — — — 38,335

Other financialcorporations — — — — — — —

Various balance sheetItems — 722 — — — — 722

Total — 39,057 — — — — 39,057

31 December 2017(€000s)

ExposuresCredit risk

adjustmentsAccumulated

write-offs

Credit riskadjustmentcharges ofthe period

NetvaluesDefaulted

Non-defaulted Specific General

General governments — — — — — — —

Credit institutions — 28,780 — — — — 28,780Other financialcorporations — 44 — — — — 44Various balance sheetItems — 363 — — — — 363

Total — 29,187 — — — — 29,187

Table 8: EU CR1-B - Credit quality of exposures by industry

This table provides a comprehensive picture of the credit quality of on- and off-balance sheet exposuresby industry type.

31 December 2017(€000s)

ExposuresCredit risk

adjustmentsAccumulated

write-offs

Credit riskadjustmentcharges ofthe period

NetvaluesDefaulted

Non-defaulted Specific General

Financial and insuranceactivities — 29,187 — — — — 29,187

Total — 29,187 — — — — 29,187

31 December 2018(€000s)

ExposuresCredit risk

adjustmentsAccumulated

write-offs

Credit riskadjustmentcharges ofthe period

NetvaluesDefaulted

Non-defaulted Specific General

Financial and insuranceactivities — 39,057 — — — — 39,057

Total — 39,057 — — — — 39,057

Pershing Securities International Limited

Risk Pillar 3 Disclosure 2018 ● 30

Table 9: EU CR1-C - Credit quality of exposures by geography

This table shows an analysis of past due, impaired exposures and allowances by country using the IFRSmethodology.

31 December 2017(€000s)

ExposuresCredit risk

adjustmentsAccumulated

write-offs

Credit riskadjustmentcharges ofthe period

NetvaluesDefaulted

Non-defaulted Specific General

France — 11,286 — — — — 11,286

Ireland — 8,456 — — — — 8,456

Belgium — 5,603 — — — — 5,603

United Kingdom — 2,585 — — — — 2,585

United States — 1,155 — — — — 1,155

31 December 2018(€000s)

ExposuresCredit risk

adjustmentsAccumulated

write-offs

Credit riskadjustmentcharges ofthe period

NetvaluesDefaulted

Non-defaulted Specific General

United Kingdom — 18,066 — — — — 18,066

Belgium — 15,459 — — — — 15,459

Ireland — 2,477 — — — — 2,477

United States — 1,676 — — — — 1,676

France — 1,215 — — — — 1,215

Other — 165 — — — — 165

Total — 39,057 — — — — 39,057

31 December 2017(€000s)

ExposuresCredit risk

adjustmentsAccumulated

write-offs

Credit riskadjustmentcharges ofthe period

NetvaluesDefaulted

Non-defaulted Specific General

Other — 103 — — — — 103

Total — 29,187 — — — — 29,187

Pershing Securities International Limited

Risk Pillar 3 Disclosure 2018 ● 31

5 Article 453 CRR - Credit risk mitigation

The following risk metrics present PSIL's risk components as at 31 December 2018.

Total exposure unsecured €39m Ý2017: €29m

Total exposure secured €0m ó2017: €0m

PSIL mitigates credit risk through a variety of strategies including obtaining cash collateral.

Pershing Securities International Limited

Risk Pillar 3 Disclosure 2018 ● 32

5.1 Collateral valuation and management

PSIL can receive collateral from clients which can include guarantees, cash or eligible debt securities andhas the ability to call on this collateral in the event of a default by the client.

Collateral amounts are adjusted on a daily basis to reflect market activity to ensure they continue to achievean appropriate mitigation of risk value. Securities are marked-to-market daily and haircuts are applied toprotect PSIL in the event of the value of the collateral suddenly reducing in value due to adverse marketconditions. Customer agreements can include requirements for the provision of additional collateral shouldvaluations decline.

5.2 Wrong-way risk

PSIL takes particular care to ensure that wrong-way risk between collateral and exposures does not exist.Wrong-way risk results when the exposure to the client or market counterparty increases when thecounterparty’s credit quality deteriorates.

5.3 Credit risk concentration

PSIL is exposed to credit risk concentration through exchanges and central counterparties, correspondentbanks and issuers of securities. These risks are managed and mitigated through the establishment ofvarious limits, on-going monitoring of exposure, collateral and contractual obligations upon the client,including margin calls.

Ongoing assessments of credit concentration risk are performed as part of the Pillar 2 risk assessmentprocess.

The number of counterparties PSIL is willing to place funds with is limited and hence, concentration riskcan arise from cash balances placed with a relatively small number of counterparties. To mitigate this,

exposures are only placed on a very short-term basis, generally overnight (maximum of 180 days), ensuringability to withdraw funds in a timely manner.

Pershing Securities International Limited

Risk Pillar 3 Disclosure 2018 ● 33

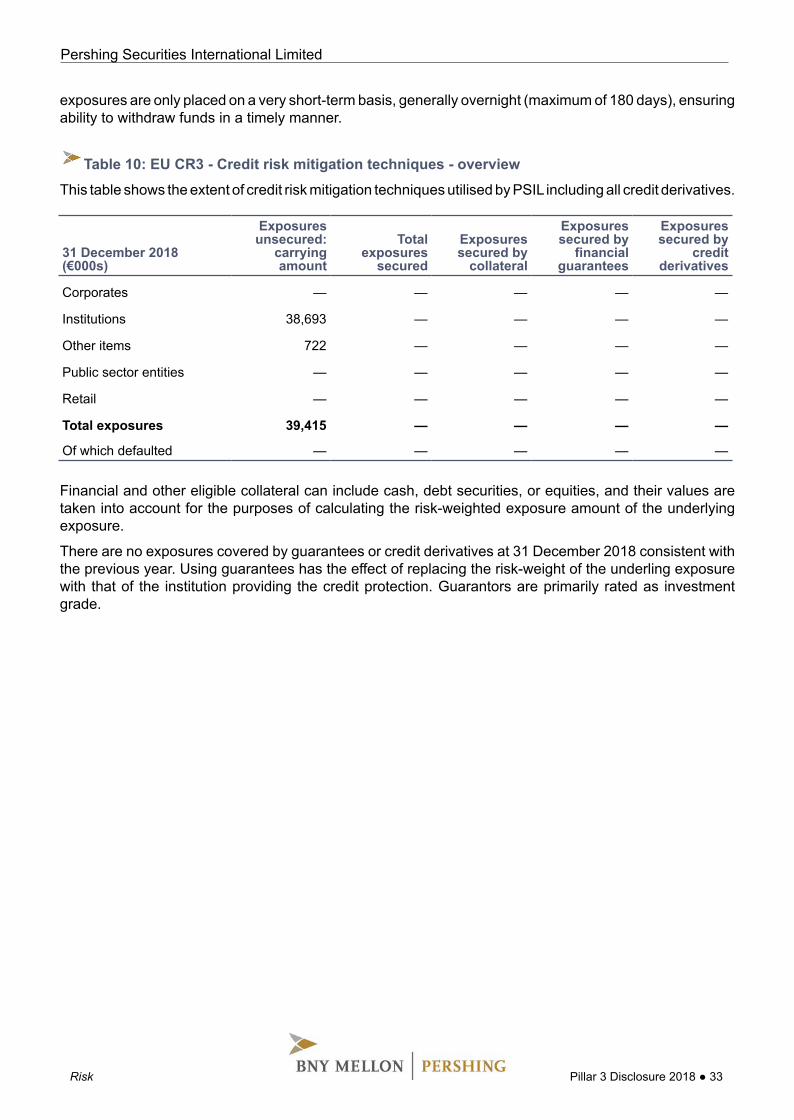

Table 10: EU CR3 - Credit risk mitigation techniques - overview

This table shows the extent of credit risk mitigation techniques utilised by PSIL including all credit derivatives.

Financial and other eligible collateral can include cash, debt securities, or equities, and their values aretaken into account for the purposes of calculating the risk-weighted exposure amount of the underlyingexposure.

There are no exposures covered by guarantees or credit derivatives at 31 December 2018 consistent withthe previous year. Using guarantees has the effect of replacing the risk-weight of the underling exposurewith that of the institution providing the credit protection. Guarantors are primarily rated as investmentgrade.

31 December 2018(€000s)

Exposuresunsecured:

carryingamount

Totalexposures

secured

Exposuressecured by

collateral

Exposuressecured by

financialguarantees

Exposuressecured by

creditderivatives

Corporates — — — — —

Institutions 38,693 — — — —

Other items 722 — — — —

Public sector entities — — — — —

Retail — — — — —

Total exposures 39,415 — — — —

Of which defaulted — — — — —

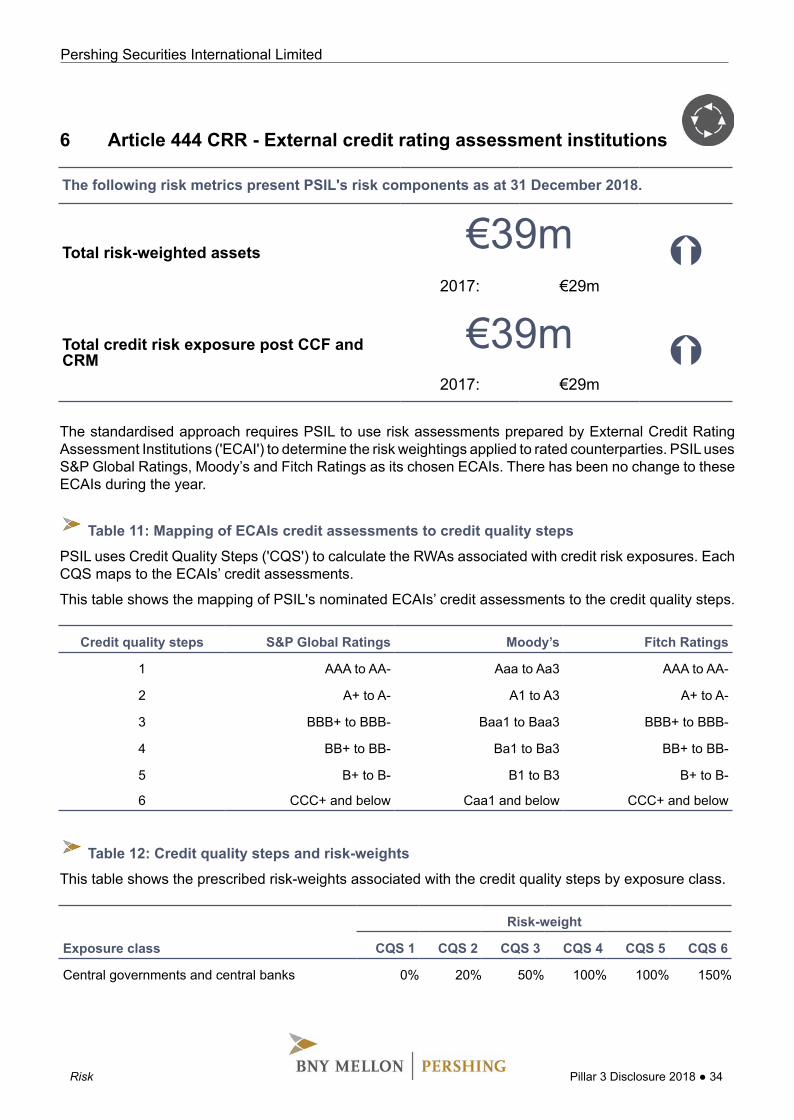

6 Article 444 CRR - External credit rating assessment institutions

The standardised approach requires PSIL to use risk assessments prepared by External Credit RatingAssessment Institutions ('ECAI') to determine the risk weightings applied to rated counterparties. PSIL usesS&P Global Ratings, Moody’s and Fitch Ratings as its chosen ECAIs. There has been no change to theseECAIs during the year.

The following risk metrics present PSIL's risk components as at 31 December 2018.

Total risk-weighted assets €39m Ý2017: €29m

Total credit risk exposure post CCF andCRM

€39m Ý2017: €29m

Pershing Securities International Limited

Risk Pillar 3 Disclosure 2018 ● 34

Table 11: Mapping of ECAIs credit assessments to credit quality steps

PSIL uses Credit Quality Steps ('CQS') to calculate the RWAs associated with credit risk exposures. EachCQS maps to the ECAIs’ credit assessments.

This table shows the mapping of PSIL's nominated ECAIs’ credit assessments to the credit quality steps.

Credit quality steps S&P Global Ratings Moody’s Fitch Ratings

1 AAA to AA- Aaa to Aa3 AAA to AA-

2 A+ to A- A1 to A3 A+ to A-

3 BBB+ to BBB- Baa1 to Baa3 BBB+ to BBB-

4 BB+ to BB- Ba1 to Ba3 BB+ to BB-

5 B+ to B- B1 to B3 B+ to B-

6 CCC+ and below Caa1 and below CCC+ and below

Table 12: Credit quality steps and risk-weights

This table shows the prescribed risk-weights associated with the credit quality steps by exposure class.

Exposure class

Risk-weight

CQS 1 CQS 2 CQS 3 CQS 4 CQS 5 CQS 6

Central governments and central banks 0% 20% 50% 100% 100% 150%

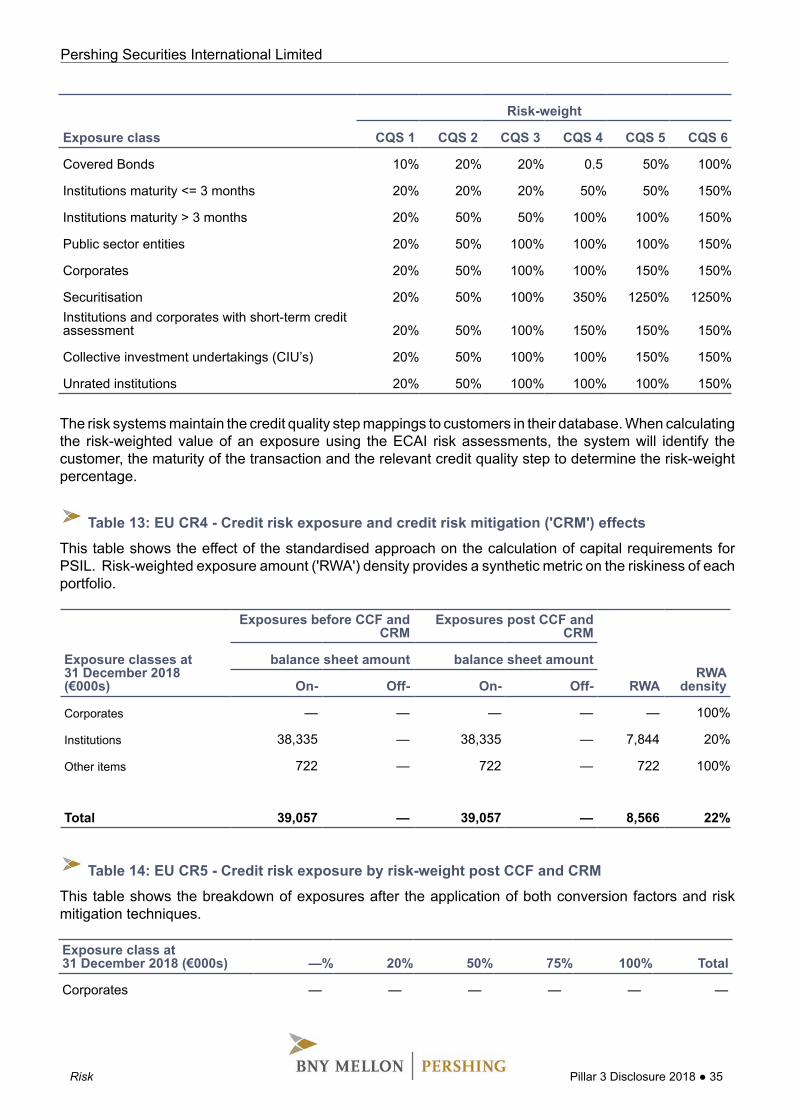

The risk systems maintain the credit quality step mappings to customers in their database. When calculatingthe risk-weighted value of an exposure using the ECAI risk assessments, the system will identify thecustomer, the maturity of the transaction and the relevant credit quality step to determine the risk-weightpercentage.

Exposure class

Risk-weight

CQS 1 CQS 2 CQS 3 CQS 4 CQS 5 CQS 6

Covered Bonds 10% 20% 20% 0.5 50% 100%

Institutions maturity <= 3 months 20% 20% 20% 50% 50% 150%

Institutions maturity > 3 months 20% 50% 50% 100% 100% 150%

Public sector entities 20% 50% 100% 100% 100% 150%

Corporates 20% 50% 100% 100% 150% 150%

Securitisation 20% 50% 100% 350% 1250% 1250%Institutions and corporates with short-term creditassessment 20% 50% 100% 150% 150% 150%

Collective investment undertakings (CIU’s) 20% 50% 100% 100% 150% 150%

Unrated institutions 20% 50% 100% 100% 100% 150%

Pershing Securities International Limited

Risk Pillar 3 Disclosure 2018 ● 35

Table 13: EU CR4 - Credit risk exposure and credit risk mitigation ('CRM') effects

This table shows the effect of the standardised approach on the calculation of capital requirements forPSIL. Risk-weighted exposure amount ('RWA') density provides a synthetic metric on the riskiness of eachportfolio.

Exposure classes at31 December 2018(€000s)

Exposures before CCF andCRM

Exposures post CCF andCRM

RWARWA

density

balance sheet amount balance sheet amount

On- Off- On- Off-

Corporates — — — — — 100%

Institutions 38,335 — 38,335 — 7,844 20%

Other items 722 — 722 — 722 100%

Total 39,057 — 39,057 — 8,566 22%

Table 14: EU CR5 - Credit risk exposure by risk-weight post CCF and CRM

This table shows the breakdown of exposures after the application of both conversion factors and riskmitigation techniques.

Exposure class at31 December 2018 (€000s) —% 20% 50% 75% 100% Total

Corporates — — — — — —

Exposure class at31 December 2018 (€000s) —% 20% 50% 75% 100% Total

Institutions — 37,738 580 — 17 38,335

Other items — — — — 722 722

Total — 37,738 580 — 739 39,057

Exposure class at31 December 2017 (€000s) —% 20% 50% 75% 100% Total

Corporates — — — — 44 44

Institutions — 20,414 2,378 — 5,988 28,780

Other items — — — — 363 363

Public sector entities — — — — — —

Total — 20,414 2,378 — 6,395 29,187

Pershing Securities International Limited

Risk Pillar 3 Disclosure 2018 ● 36

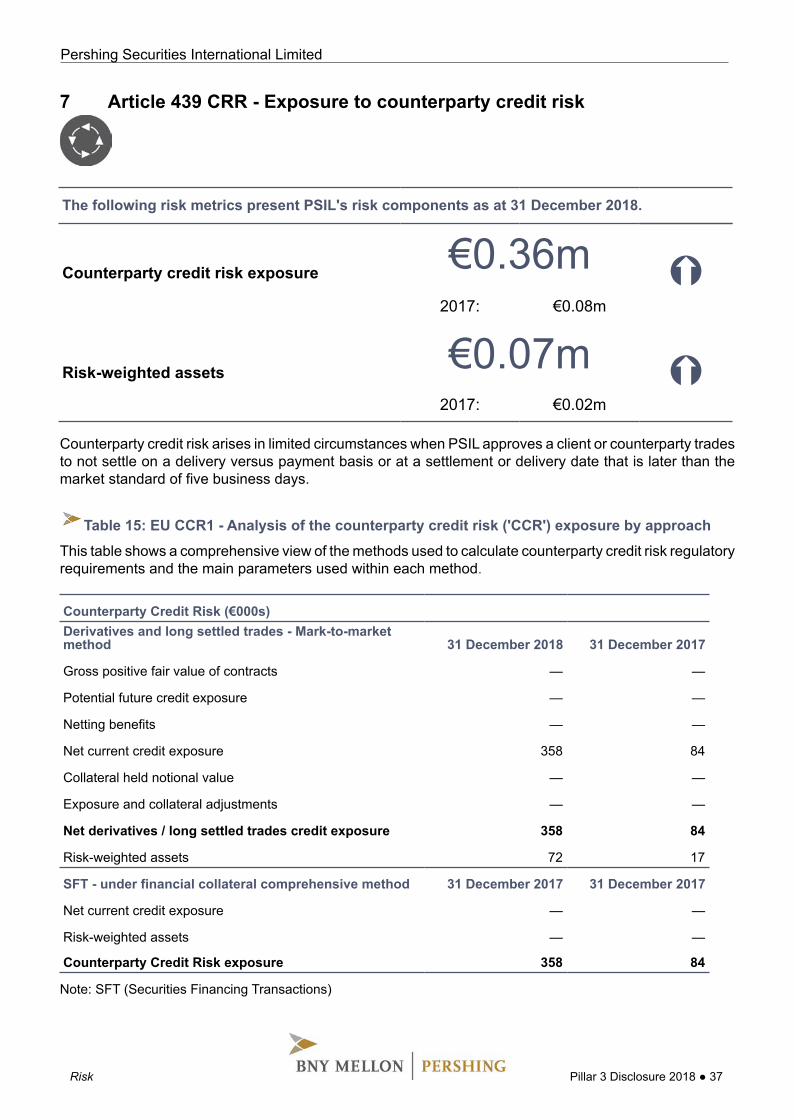

7 Article 439 CRR - Exposure to counterparty credit risk

Counterparty credit risk arises in limited circumstances when PSIL approves a client or counterparty tradesto not settle on a delivery versus payment basis or at a settlement or delivery date that is later than themarket standard of five business days.

The following risk metrics present PSIL's risk components as at 31 December 2018.

Counterparty credit risk exposure €0.36m Ý2017: €0.08m

Risk-weighted assets €0.07m Ý2017: €0.02m

Pershing Securities International Limited

Risk Pillar 3 Disclosure 2018 ● 37

Table 15: EU CCR1 - Analysis of the counterparty credit risk ('CCR') exposure by approach

This table shows a comprehensive view of the methods used to calculate counterparty credit risk regulatoryrequirements and the main parameters used within each method.

Note: SFT (Securities Financing Transactions)

Counterparty Credit Risk (€000s)Derivatives and long settled trades - Mark-to-marketmethod 31 December 2018 31 December 2017

Gross positive fair value of contracts — —

Potential future credit exposure — —

Netting benefits — —

Net current credit exposure 358 84

Collateral held notional value — —

Exposure and collateral adjustments — —

Net derivatives / long settled trades credit exposure 358 84

Risk-weighted assets 72 17

SFT - under financial collateral comprehensive method 31 December 2017 31 December 2017

Net current credit exposure — —

Risk-weighted assets — —

Counterparty Credit Risk exposure 358 84

7.1 Credit valuation adjustment

The credit valuation adjustment is the capital charge for potential mark-to-market losses due to the creditquality deterioration of a counterparty. The standardised approach uses the external credit rating of eachcounterparty and includes the effective maturity and exposure at default.

As at 31 December 2018, PSIL had no exposure subject to the credit valuation adjustment capital charge.

Pershing Securities International Limited

Risk Pillar 3 Disclosure 2018 ● 38

Table 16: EU CCR3 - CCR exposures by regulatory portfolio and risk

This table shows the breakdown of counterparty credit risk exposures by exposure class and risk-weightattributed according to the standardised approach.

Exposure class 31 December 2017 (€000s) 0% 20% 75% 100% Other Total

Institutions — 84 — — — 84

Other items — — — — — —

Total — 84 — — — 84

Exposure class31 December 2018 (€000s) 0% 20% 75% 100% Other Total

Institutions — 358 — — — 358

Other items — — — — — —

Total — 358 — — — 358

Table 17: EU CCR5-A - Impact of netting and collateral held on exposure values

This table provides an overview of the collateral held on exposures.

31 December 2018 (€000s)

Gross positivefair value or net

carrying amountNetting

benefits

Nettedcurrent credit

exposureCollateral

heldNet creditexposure

Derivatives by underlying 358 358 — 358

Securities Financing Transactions — — — —

Cross-product netting — — — —

Total 358 — 358 — 358

8 Article 443 CRR - Asset encumbrance

The following risk metrics present PSIL's risk components as at 31 December 2018.

Carrying amount - encumbered assets €0.05m Þ2017: €0.10m

Carrying amount - unencumbered assets €19.4m Þ2017: €39.1m

Pershing Securities International Limited

Risk Pillar 3 Disclosure 2018 ● 39

Table 18: AE-A - Encumbered assets

The carrying and fair value of encumbered assets by type, based on median values in 2018, are as follows:

Note: HQLA (High Quality Liquid Assets) / EHQLA (Extremely High Quality Liquid Assets)

31 December 2018(€000s)

Encumbered assets Unencumbered assets

Carryingamount

of whichnotionally

eligibleEHQLA

and HQLAFair

value

of whichnotionally

eligibleEHQLA

and HQLACarryingamount

of whichEHQLA

andHQLA

Fairvalue

of whichEHQLA

andHQLA

Assets of the reportinginstitution 50 — 19,443 —

Other assets 50 — 19,443 —

Table 19: AE-B - Collateral

The reportable encumbered collateral received, or available for encumbrance based on median valuesare presented below:

31 December 2018 (€000s)

Fair value of encumberedcollateral received or own

debt securities issued

UnencumberedFair value of collateral received or own

debt securities issued available forencumbrance

of which notionallyelligible EHQLA

and HQLAof which EHQLA

and HQLA

Total assets, collateral received &own debt securities issued 50 —

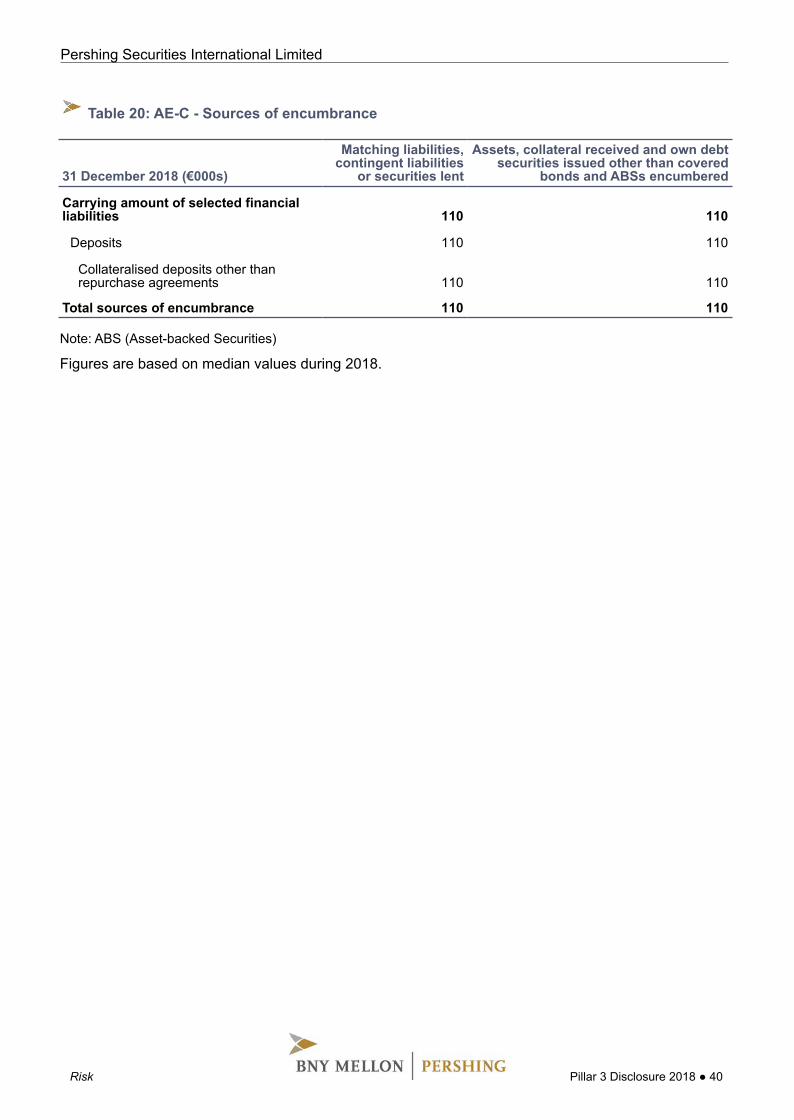

Table 20: AE-C - Sources of encumbrance

Note: ABS (Asset-backed Securities)

Figures are based on median values during 2018.

31 December 2018 (€000s)

Matching liabilities,contingent liabilities

or securities lent

Assets, collateral received and own debtsecurities issued other than covered

bonds and ABSs encumbered

Carrying amount of selected financialliabilities 110 110

Deposits 110 110

Collateralised deposits other thanrepurchase agreements 110 110

Total sources of encumbrance 110 110

Pershing Securities International Limited

Risk Pillar 3 Disclosure 2018 ● 40

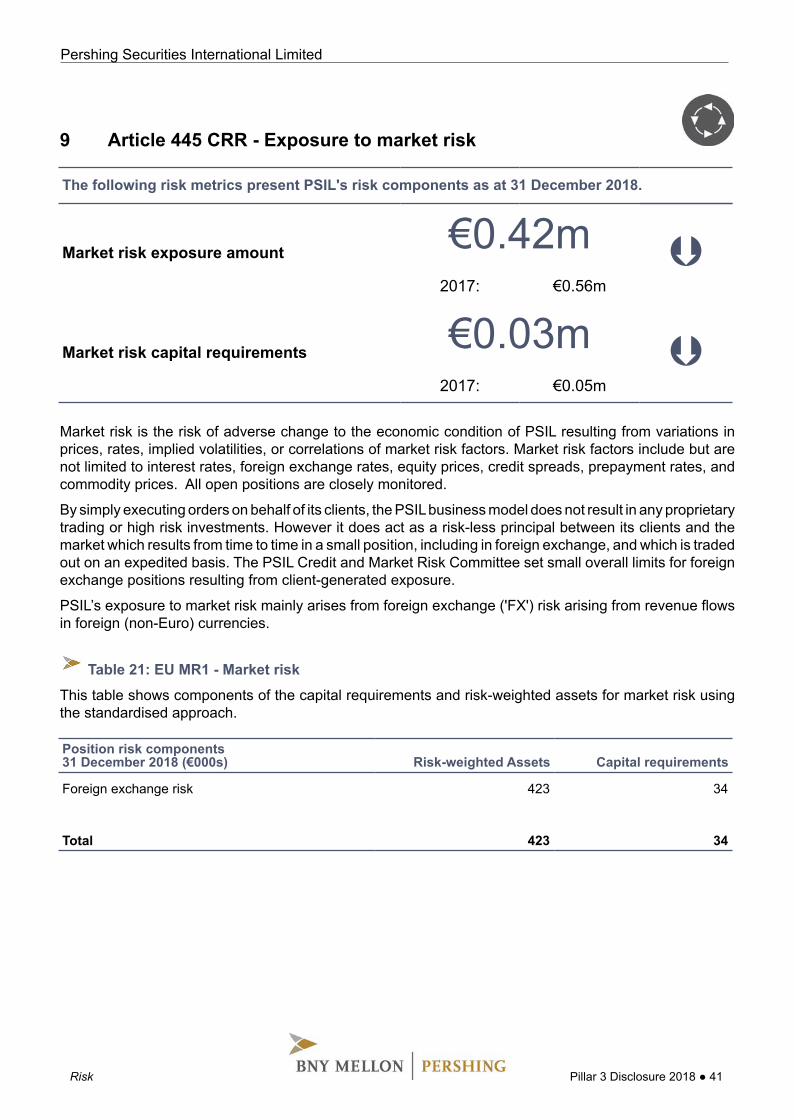

9 Article 445 CRR - Exposure to market risk

The following risk metrics present PSIL's risk components as at 31 December 2018.

Market risk exposure amount €0.42m Þ2017: €0.56m

Market risk capital requirements €0.03m Þ2017: €0.05m

Market risk is the risk of adverse change to the economic condition of PSIL resulting from variations inprices, rates, implied volatilities, or correlations of market risk factors. Market risk factors include but arenot limited to interest rates, foreign exchange rates, equity prices, credit spreads, prepayment rates, andcommodity prices. All open positions are closely monitored.

By simply executing orders on behalf of its clients, the PSIL business model does not result in any proprietarytrading or high risk investments. However it does act as a risk-less principal between its clients and themarket which results from time to time in a small position, including in foreign exchange, and which is tradedout on an expedited basis. The PSIL Credit and Market Risk Committee set small overall limits for foreignexchange positions resulting from client-generated exposure.

PSIL’s exposure to market risk mainly arises from foreign exchange ('FX') risk arising from revenue flowsin foreign (non-Euro) currencies.

Pershing Securities International Limited

Risk Pillar 3 Disclosure 2018 ● 41

Table 21: EU MR1 - Market risk

This table shows components of the capital requirements and risk-weighted assets for market risk usingthe standardised approach.

Position risk components31 December 2018 (€000s) Risk-weighted Assets Capital requirements

Foreign exchange risk 423 34

Total 423 34

10 Article 448 CRR - Interest rate risk in the banking book