14

PERSONAL FINANCE MBF3C Lesson #8: Credit Cards

| Date post: | 27-Dec-2015 |

| Category: |

Documents |

| Upload: | andra-lambert |

| View: | 246 times |

| Download: | 3 times |

PERSONAL FINANCE

MBF3C

Lesson #8: Credit Cards

Good, bad, convenient, dangerous, safer than cash, scary, and expensive are common words that people use when describing their relationship with credit cards. All of the adjectives are right—depending on how the cards are used. In this section, you will begin to discover the good, the bad, and the ugly of using a credit card.

QUESTIONS TO ANSWER WHEN COMPARING

1. Is there an annual fee for holding the card? If so, how much is the annual fee?

2. What annual interest rate is charged on an overdue balance?

3. How often is the interest compounded?

4. How many days after the monthly statement is issued is the payment due?

5. How much interest is charged if the balance is paid in full by the due date?

6. Are there any incentives or rewards associated with being a cardholder?

Comparing Cards

Choose two credit cards: one issued by a bank or other financial institution and one offered by a retailer (for example, an electronics store, a furniture retailer, or a gasoline retailer). Gather the following information about each card. Record your findings in a table or chart

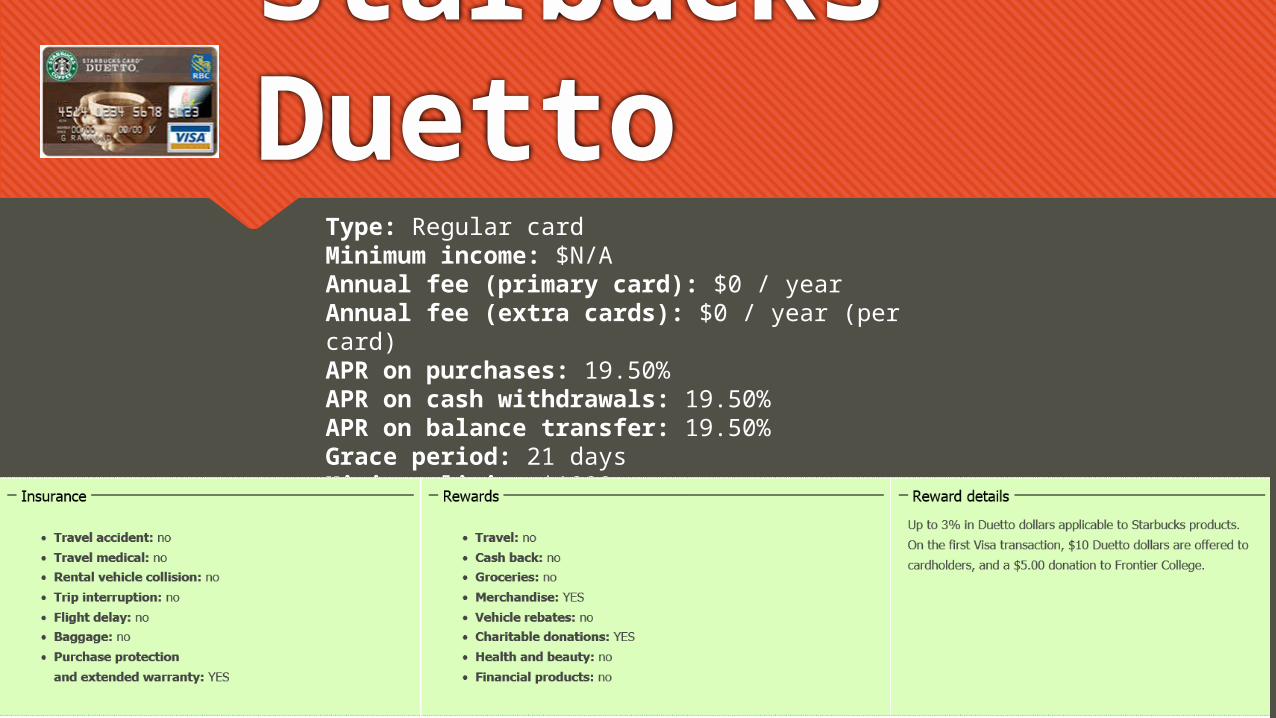

Starbucks Duetto

Type: Regular cardMinimum income: $N/AAnnual fee (primary card): $0 / yearAnnual fee (extra cards): $0 / year (per card)APR on purchases: 19.50%APR on cash withdrawals: 19.50%APR on balance transfer: 19.50%Grace period: 21 daysMinimum limit: $1000

RBC Gold Card•Type: Gold card•Minimum income: $35,000•Annual fee (primary card): $0 / year•Annual fee (extra cards): $0 / year (per card)•APR on purchases: 19.50%•APR on cash withdrawals: 19.50%•APR on balance transfer: 19.50%•Grace period: 21 days•Minimum limit: $5000

EXAMPLE 1:

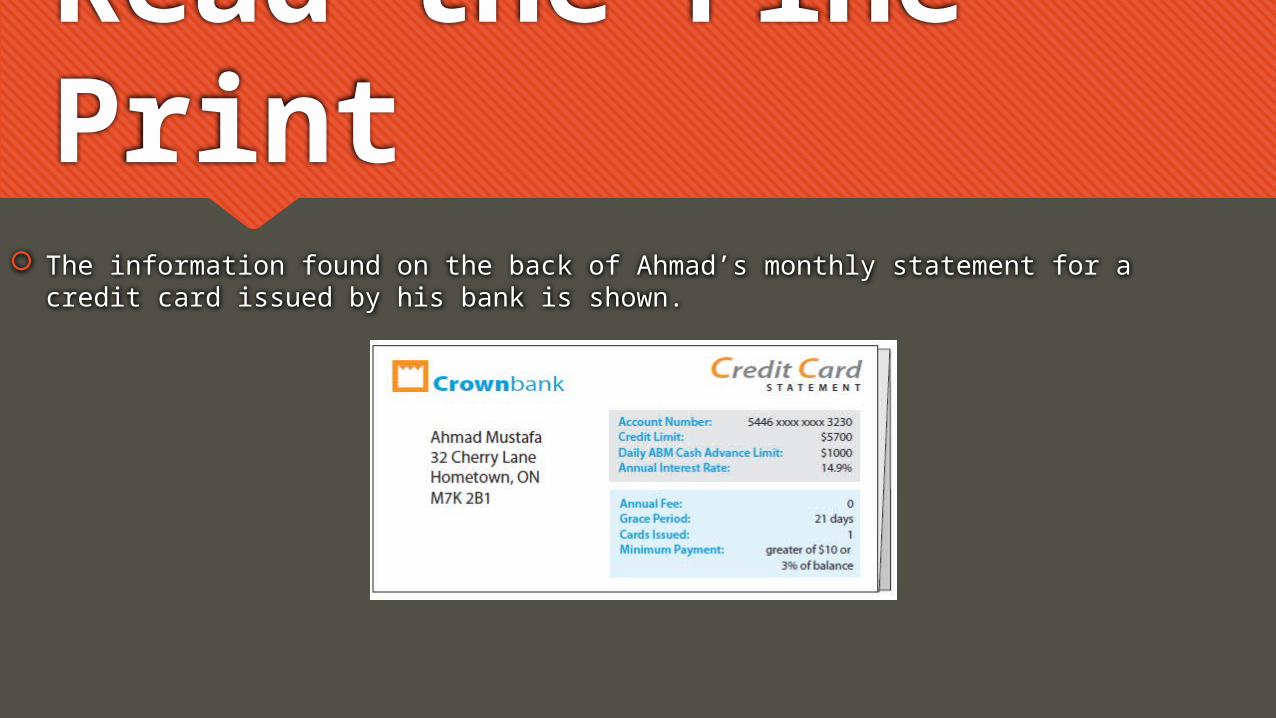

Read the Fine Print

The information found on the back of Ahmad’s monthly statement for a credit card issued by his bank is shown.

EXAMPLE 1:

Read the Fine Print

a) A statement is issued to Ahmad on the 8th of each month. On what date will the payment be due? The payment will be due on the 29th of each month.

b) On September’s statement, Ahmad has a balance of $86.36. Determine his minimum payment. 3% of $86.36 is $2.59, so the minimum payment due is $10.00.

c) On October’s statement, Ahmad has a balance of $462.18. Determine his minimum payment. 3% of $462.18 is $13.87, so the minimum payment due is $13.87.

EXAMPLE 1:

Read the Fine Print d) If it takes three days to process his payment, what is the latest date that

Ahmad can pay October’s bill and not be overdue?

ANSWER: The bill should be paid no If the balance is paid in full on or before the due date, no interest is

charged. later than the 26th of the month.

EXAMPLE 1:

Read the Fine Print

e) If interest is calculated and compounded daily, determine the daily interest rate. Round your answer to 4 decimal places.

EXAMPLE 1:

Read the Fine Print

f) Calculate the interest charged on October’s bill if it is paid in full five days after the due date. Ahmad paid his September bill in full. He made one new purchase for $462.18 on September 15.

EXAMPLE 1:

Read the Fine Print

Key Concepts

Interest rates charged on credit card accounts are often much greater than the interest rates paid on savings accounts.

Most credit cards compound interest daily on overdue accounts.

If the balance is paid in full, then no interest is charged during the grace period.

Some credit card companies offer incentives or rewards to customers for using the card to make purchases.

IN-CLASS & HOMEWORK

Page 479-481, #1-7, 9-10