Perspectives on the Forest Products Industry CONFIDENTIAL AND PROPRIETARY Any use of this material without specific permission of McKinsey & Company is strictly prohibited Québec City – May 24, 2012 Québec Forest Industry Council

Transcript

Perspectives on the Forest Products Industry

CONFIDENTIAL AND PROPRIETARYAny use of this material without specific permission of McKinsey & Company is strictly prohibited

Québec City – May 24, 2012

Québec Forest Industry Council

McKinsey & Company 1|

Contents

▪ Trends and developments in the

North American and global markets

▪ Competitiveness of the Quebec forest sector

▪ Potential responses and ways forward

McKinsey & Company 2|

Changed consumption patterns▪ Stagnation in developed countries▪ Growth in new economies

Changed production base▪ Production follows consumption

– China/Asia (paper/board)– Other emerging markets– (India)

▪ South America (pulp)

Changed raw material dynamics▪ Fundamental land use issues▪ Biomass for energy▪ Recycled fiber scarcity

Increasing requirements on sustainability and interest in green products

Three fundamental forces drive the most important trends in the forest products industry today

Demographic changes

Fundamental forces General trends Key forest-industry trends

New opportunities for construction wood – Asia & domestic industrialized building

Technology and knowledge development

Experiencing Earth’s limits

Growing healthcare sector

New consumers

Growing public sector

Second agricultural revolution

Increased connection between world economies

Growing infrastructure problems

Urbanization and megacities

Changed economic centers

Accelerating green economy

Changed social values

Increased regulation

McKinsey & Company 3|

90

95

100

105

110

115

120

125

130

135

140

145

40

60

80

100

120

140

160

180

200

220

240

260

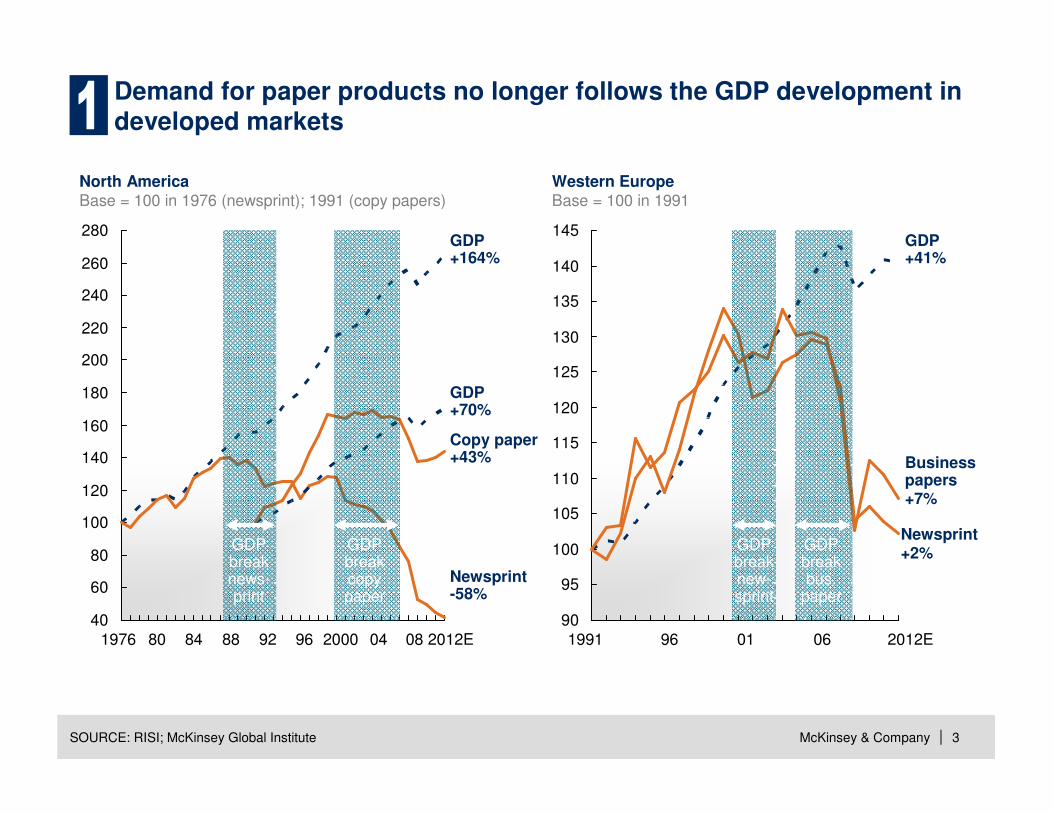

280GDP+164%

GDP+70%

Copy paper+43%

Demand for paper products no longer follows the GDP development in developed markets

SOURCE: RISI; McKinsey Global Institute

North AmericaBase = 100 in 1976 (newsprint); 1991 (copy papers)

Western EuropeBase = 100 in 1991

1991 96 2012E

Newsprint+2%

Business papers+7%

1976 80 84 88 92 96 2000 04 2012E

GDP+41%

Newsprint-58%

08

GDP break news-print

GDP break copy paper

01 06

GDP break bus.

paper

GDP break new-sprint

McKinsey & Company 4|SOURCE: Audit Bureau of Circulations, PaidContent

2.2

2.0

1.8

1.6

1.4

1.2

1.0

0.8

0.6

0.4

0.2

0

2011201020092008

0.60

0.50

0.40

0.30

0.20

0.10

0

2011201020092008

0.05

0.15

0.25

0.35

0.45

0.55

0.65

Print

Digital

Print down 6%

Average Daily Circulation; Daily copies; Millions

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

201008060402001998

Large American newspapers have begun the shift to digital circulation

Print down 25% Print down 31%

McKinsey & Company 5|

3.03.3

3.1

1.6

-1.6%

2015201020001990

Copy paper consumption is expected to decrease –Western Europe example

1 Estimate based on UWF cut-size consumption, actual values slightly higher (estimate 1–3% missing)

SOURCE: EMGE; expert interviews

Apparent consumption of copy paper in Western Europe1; Million tonnes

McKinsey & Company 6|

0

5

10

15

20

25

30

0908 201514131211102007

Tablet penetration is expected to grow rapidly, further impacting graphical papers

1 Installed based/total population

SOURCE: Yankee; Press search; McKinsey analysis

Tablets population penetration1; Percent

Forecast 2012–15

North America

Western Europe

Eastern Europe

McKinsey & Company 7|SOURCE: National Bureaus of Statistics; US Census; Hindustan Unilever investor presentations Sep2008; Freedonia;Euromonitor; McKinsey

In packaging changing consumer demographics and shopping behaviors create positive dynamics

Changing

demographics

Changing shopping

behaviors

Higher “churn”; increasing volumes

Opportunities for

differentiation and higher margins

New

requirements on packaging

New demands on packaged

foods and goods

Substrate

choice and dynamics

Technology development

McKinsey & Company 8|

What’s next?▪ China’s next development step?▪ Will southern hemisphere fiber continue to be low-cost?

Relative production capacity is experiencing significant shifts out of Europe/North America

SOURCE: RISI; McKinsey

Production capacity; Millions tonnes

0

10

20

30

40

50

60

70

80

90

100

20151005001995

0

50

100

150

200

20151005001995

0

10

20

30

40

50

60

70

80

05 10 2015001995

Freesheet (UFS + CFS)1 Containerboard Market pulp

North America

Latin America

Europe

Asia/ Oceania

RoW

1 Woodfree capacity for 1995 to 1999 based on actual production and 2000 utilization rate

Forecast Forecast Forecast

McKinsey & Company 9|

90

Wind

Hydro

2020 scenario

3,030

1,650

380

280

370

350

Biomass and Waste

Biofuels

Sun, Geothermal,Wave, and Tidal

310

2007

1,330

800

30 100

Energy growth from biomass2

850

Growth in other renewables

850

In the European Commission’s scenarios, biomass plays a crucial role

to secure the EU’s RES targets – threat or opportunity?

EU-27 Final energy consumption1; TWh

SOURCE: 2010 report ‘Biomass for heat and power’ by ECF, Södra, Sveaskog, and Vattenfall (Capros et al (2008):Model-based Analysis of the 2008 EU Policy Package on Climate Change and Renewables; IEA)

1 Aveage of ‘EC proposal with RES trading’ and ‘EC proposal with CDM and RES trading’ scenarios2 Varies between 839 and 886 TWh depending on scenario

Direct use

HeatPower

Direct use

Heat/cooling

Power

McKinsey & Company 10|

Increasing biomass trade (due to RES targets) will create new wood-fiber dynamics

SOURCE: Hawkins Wright; WRQ; RISI; Canadian Biomass Magazine; Press search

Planned new large scale (>350 kt/y) wood pellets mills, as of January 2012

Capacity000 t/yCompany Start-up

RWE InnogyGerman PelletsCanadian Bio PelletEnvivaEnvivaPoint EnergyEnviva

Total NA

750500450

450400400350

~3,300

201120122011

2013201220132012

Capacity000 t/yCompany Start-up

Suzano

Suzano

3,000

2,000

2014

2019

Capacity000 t/yCompany Start-up

VyborgskayaCellulose

German Pellets

900

400

2011/12

TBD

NOT EXHAUSTIVE

McKinsey & Company 11|

Global recovered paper supply is tightening, as paper consumption declines and recovery rates reach practical limits in key export regions

Continued increase in demand for RCF in Asia, while reduced ‘production’of RCF in North America/Europe

Expect increased prices for RCF

Opportunity for fresh fiber, particularly long fiber

Potential competition for RCF from bio-energy

Reduced quality of RCF▪ Increasing RCF share in total furnish▪ Next level of sources used

Innovation needed on further reducing fiber share

McKinsey & Company 12|

Sustainability is a ticket to play but its impact is yet unclear

Sustainability increasingly important –must be integral part of product strategy

Impact on volumes unclear

Important to shape individual

situations

‘Sustainability’ often just a way to uncover new opportunities for cost reduction in the value chain

Don’t expect premium for green products – but they can be differentiator to secure business

Innovation needed to ride the wave

McKinsey & Company 13|

There is uncertainty around the timing of the anticipated recovery of annual housing starts

Annual housing startsMillions of units

08070605040302012000

0.4

0.2

0

1.5

201709 151413121110

2.2

2.0

1.8

1.6

1.4

1.2

1.0

0.8

0.6

16

McGraw Hill forecast

Bureau of Census; Moody’s Analytics

Actual

McKinsey & Company 14|

Contents

▪ Trends and developments in the North American and global markets

▪ Competitiveness of the Quebec forest sector

▪ Potential responses and ways forward

McKinsey & Company 15|

-5

0

5

10

15

20

25

30

1992 1996 2000 2004 2008 2012

0

5

10

15

20

25

1990 1995 2000 2005 2010 2015

SOURCE: McKinsey CPAT database

1 Average across ~30 North American paper/board producers

EBIT margin1

PercentROCE1

Percent

North American paper and paperboard producers’ margins and returns have seen a declining trend over the past 10–15 years

McKinsey & Company 16|

-4

-2

0

2

4

6

8

10

4 8 12 16 20 24 28 32 36 40 44

Organic growth outlook trajectory 2011–211

Percent CAGR

Average EBITDA margin 2012–142

PercentTypical margin to cover maintenance and strategic capex and capital cost

Average global paper and board growth

North American and European paper producers are generally not well positioned for future growth

1 Outlook weighted based on each company’s regional production base and product range, measured in volume (Europe seen as one region)2 Based on current earnings estimates

SOURCE: Company reports; RISI; Hawkins Wright; EMGE; Bloomberg; McKinsey analysis

Improve operations to earn the right to grow

Fundamental restructuring

Expand to global champion

Expand beyond regional market

Asia

South America

North America

Europe

NOT EXHAUSTIVE

McKinsey & Company 17|

How Quebec does on major competitive thrusts?

Product momentum

Asset competitiveness

▪ Wood costs

▪ Other costs

– Energy price

– Energy usage

– Labour productivity

McKinsey & Company 18|

1 Demand growth in North America for QC, Canada and US, global demand growth for market pulp

Inherent growth by world regionWeighted average annual demand growth1, 2011–16e; %

4.1

3.1

0.60.50.2

-1.6

AsiaRest of World

EuropeRest of Canada

USQC

Quebec’s asset base is skewed towards segments with poor growth

McKinsey & Company 19|

Rest of Canada lumber exportsCAD billion

Quebec lumber exportsCAD billion

SOURCE: Statistics Canada

2.4

2.2

2.0

1.8

1.6

1.4

1.2

1.0

0.8

0.6

0.4

0.2

0

-72%

111009080706050403020100 03020100

10

9

8

7

6

5

4

3

2

1

0

-53%

1110090807060504

Other

Europe

Asia

USQC and Canada lumber exports collapsed with US housing crisis – other provinces have been more successful developing new markets

McKinsey & Company 20|

Canadian wood costs are mid-range in an international comparison; but high in a North American comparisonAverage delivered prices for pulpwood logs, US dollar per dry tonne

71

84

90

97

100

106

107

107

109

151

162

163

166

176

185

US South

Chile

Russia, NW

NZ

Australia

Brazil

Spain

Canada West

US NW

France

Canada East

Germany

Finland

Sweden

Norway

55

58

69

72

82

93

98

110

119

130

131

134

135

161

253

Brazil, cost1Russia, NW

US South

US NW

Chile

Canada East

Indonesia

France

Brazil

Australia

Finland

Sweden

Spain

Germany

China

1 Integrated cash costs of forestry, harvesting and transport for company with own forests – much lower than prices on the (limited) open market

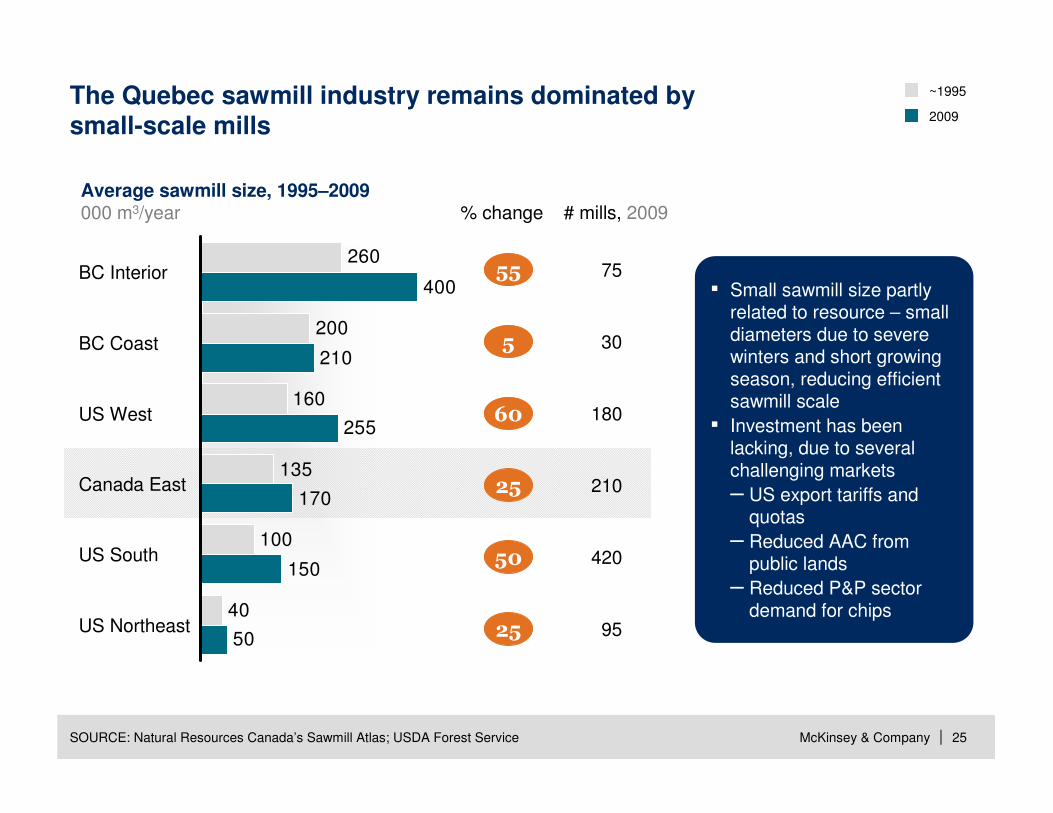

▪ Small sawmill size partly related to resource – small diameters due to severe winters and short growing season, reducing efficient sawmill scale

▪ Investment has been lacking, due to several challenging markets

– US export tariffs and quotas

– Reduced AAC from public lands

– Reduced P&P sector demand for chips

25

50

25

210

420

95

McKinsey & Company 26|

Canadian mills tend to be less labor and energy efficient

LaborTonne/employee

1,700

1,600

1,500

1,400

1,300

0.38

1,200

0

Energy (fuel and purchased power)Tonne/MWh

0.480.460.440.420.400.360.340.320

New Zealand

Austria

Russia

Germany

US

Chile

SwedenCanada

Average BSKP1 production efficiency, 2011

SOURCE: Fisher International; McKinsey analysis

0.5m tonnes/yr

2.0m tonnes/yr

1 Including fluff pulp

McKinsey & Company 27|

But labor productivity has improved over the last decade

SOURCE: Statistics Canada; Coal Association Canada; FAO; RISI

-2.3

-1.6-1.2

-0.2

1.4

3.4

4.04.2

Chemicals Oil and gasLoggingAluminumP&PSawmills CementCoal

Development of production per employee, Canadian basic materials sectorsAnnual percentage change, 1999–2010

McKinsey & Company 28|

Contents

▪ Trends and developments in the North American and global markets

▪ Competitiveness of the Quebec forest sector

▪ Potential responses and ways forward

McKinsey & Company 29|

Four potential elements of an industry-wide transformation

There is no silver bullet!

Structural changesInevitable! But consolidation per se not certain to help

Productivity and functional excellence

Cost will continue to be king!

New S-curve for markets – new and old

Enthusiasm and realism; focus on what you are good at

Business environmentValue creation drives jobs –not the other way around

McKinsey & Company 30|

The Canadian newsprint industry has made great efforts to balance the market by closing capacity – but we need to expect more is to come

Canadian newsprint closures1

Thousand tonnesCanadian newsprint demand and operating rates

Thousand tonnes

Percent

Total

5540

2010-2011

1258

2008-2009

1509

2006-2007

977

2004-2005

1168

2002-2003

628

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

0

10

20

30

40

50

60

70

80

90

100

2012E10864201998

Exports

Demand

Operating rate

1 Including closures of indefinitely idled machines

SOURCE: RISI; McKinsey analysis

Canada,non QC

QC

McKinsey & Company 31|

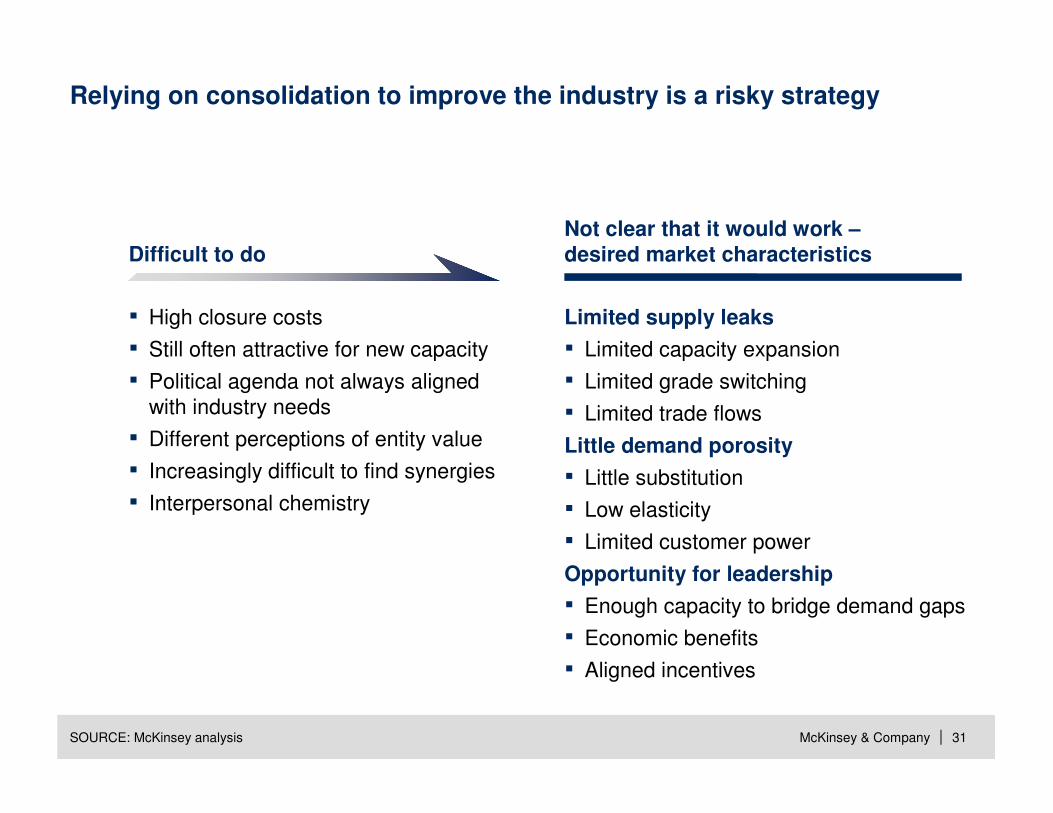

Relying on consolidation to improve the industry is a risky strategy

SOURCE: McKinsey analysis

Difficult to do

▪ High closure costs

▪ Still often attractive for new capacity

▪ Political agenda not always aligned with industry needs

▪ Different perceptions of entity value

▪ Increasingly difficult to find synergies

▪ Interpersonal chemistry

Not clear that it would work –desired market characteristics

Limited supply leaks

▪ Limited capacity expansion

▪ Limited grade switching

▪ Limited trade flows

Little demand porosity

▪ Little substitution

▪ Low elasticity

▪ Limited customer power

Opportunity for leadership

▪ Enough capacity to bridge demand gaps

▪ Economic benefits

▪ Aligned incentives

McKinsey & Company 32|

Potential cash

cost reduction

5–10%

Source: RISI; McKinsey analysis

550

500

450

400

350

300

250

12108765

150

100

50

0

0

200

Introducing the ‘Lean Mill’ can yield significant cost reductions

CapacityMillion metric tonnes

NewsprintEUR/tonne, delivered

Mill starting position

Mill potential position

Typical improvement experience

Productivity/lean

▪ ~5% increased production at same marginal contribution

▪ Variable cost decrease of 2–5%

Fixed cost reduction

▪ 15–20% reduction (production, maintenance, support functions

Procurement

▪ 2–5% reduction on fiber and energy categories and 10–20% on others

SG&A

▪ 25% reduction of SG&A cost

McKinsey & Company 33|

Industry sector

Achieved savings in percent of total energy costs with payback <3 years

0 10 20 30 40 50

Steel

Chemical

Pulp and paper

Consumer goods

Automotive and assembly

Retail

Category

Impact achieved

Min Max

SOURCE: McKinsey

Mining

▪ Integrated upstream

▪ Electric arc furnace

▪ Downstream processing

▪ Continuous processing

▪ Paper production

▪ Packaging

▪ Machining lines

▪ Mechanical/plant engineering

▪ Warehouses

▪ Shops

▪ Liquid goods fabrication

▪ High intensity

▪ Dry goods fabrication

▪ Assembly serial production

▪ Batch processing

▪ Beneficiation plant

Our experience indicates energy efficiency can be improved by 10–15% across all industry sectors, including P&PPercent

McKinsey & Company 34|

Productivity is fundamental even in forest activities (e.g., harvesting)

SOURCE: McKinsey

From… …to

Technical systems

Formal structure and organization

Leadership and mindsets

▪ Standardized, well trained methodology where each harvester reaches ‘best practice’ productivity

▪ Precise and regular control/follow-up with correcting actions taken ‘here and now’

▪ Harvesting groups working towards same target, with same methodology and with leaders that are present and act as role models

McKinsey & Company 35|

Marketing and sales are generally not focus areas of excellence in the forest products industry but can have substantial impact

Enablers

▪ Organization and pivotal roles▪ Talent and skills, mindsets and behaviors▪ Performance management▪ Information and analytical tools

Capabilities

Typical potential▪ 2–3% ROS▪ 2–10% growth

above market

▪ Strategic marketing and go-to-market model

▪ Innovation in products and services▪ Product management▪ Pricing and contract management▪ Customer management▪ Channel management▪ Field sales force management

▪ Tactical optimization of sales and supply

Marketing

Sales

McKinsey & Company 36|

Swedish steel companies survived crisis of the 70’s through specialization

SOURCE: Jernkontoret; McKinsey

▪ Crisis in Swedish steel industry in the 1970s

– Disappearance of the Swedish ship building industry

– Decline of Swedish construction sector

▪ Strong market competition due to liberal Swedish trade policy –leading to an increase in imports

▪ Steel companies pressured to increase profitability in order to survive

Catalyst

▪ Many companies chose specialization to avoid tough price competition in bulk products

▪ Chose to cultivate image of high-quality, expert producers within their respective segments

▪ Close cooperation with end customers enabled R&D to create new products and adjust metallurgical processes to stay in the lead

Bio-refineries to maximize the value of a tree holds a lot of promise –much research still needed before generally attractive

Chips

Glucose Extractives Hemicellulose Lignin

Cellulose Pulp Paper

Gasification

SOURCE: Adapted from P. Axegård, STFI-Packforsk (Innventia), PIRA Energy Management Conference, October 2006

Bark and harvest residues

▪ Methanol▪ DME▪ Bio diesel

▪ Ethanol▪ Butanol

▪ Fatty acids▪ Tannin▪ Anti-oxidizers

▪ Film/barriers▪ Hydrogels▪ Base

chemicals▪ Bio-polymers

▪ Pellets▪ Active carbon▪ Phenols▪ Carbon fiber▪ Emulsifiers

▪ ‘Value-added’ often equals ‘cost-added’ – not necessarily the same as ‘value creating’▪ There is no ‘new economy’ – supply-and-demand laws still apply▪ Other industries are moving too – wood is not the only biomass feedstock

McKinsey & Company 38|

In paper and forest products, value is often created in the upstream and downstream parts of the value chain

X (Y-Z) = Average (min – max)

Position in value chain

Level ofprofitability

1 Average of 8 companies2 Average of 25 companies3 Average of 14 companies4 Average of 15 companies

SOURCE: CPAT; McKinsey analysis; Odin; Company websites; McKinsey

In Sweden, an emerging trend towards more industrialized wood construction is leading to increased penetration in the building market

Type of constructionWood market share%

1 Includes smaller pedestrian bridges

SOURCE: Svenskt Trä (Swedish Wood)

Residential – 1 storey >90

Residential – 2 storey >50

Residential – 3-8 storeys >15

Sports arenas etc >30

Bridges1 >20

McKinsey & Company 41|

Still many obstacles to increased industrialization of wood construction

Few national/international agreements or targets

Small and fragmented wood-product actors (with small voices)

Complex building codes that make standardization difficult

Risk-averse, conservative customers

Lack of knowledge among policy- and decision makers

Increasing competition from other building products

McKinsey & Company 42|

In summary

A paradigm shift▪ Fundamental shifts in consumption patterns, industry

structure, and raw materials dynamics

Quebec/Canada

in challenging position

▪ Western world demand stagnating for many traditional paper products (brighter for wood products)

▪ Quebec in challenged starting position e.g., regarding product portfolio, cost base, and assets; but raw material (virgin fiber) could see revival of fortunes

Actions on several

fronts needed

▪ No silver bullet – combination of restructuring, productivity increases, demand stimulation, and new products required

▪ Possibility to build competitive edge in new products based on virgin fiber – requires sustained efforts and challenges should not be underestimated

▪ Now is the time to bring all stakeholders together