Hermanto Siregar Dept. Ilmu Ekonomi – FEM, IPB “PERSPEKTIF PERHEPI”, diselenggara- kan oleh PERHEPI & ISEI BOGOR RAYA BPATP-Kementan, Bogor, 28/4/2016 MASALAH TINGGINYA SUKU BUNGA DAN IMPLIKASINYA BAGI EKONOMI PERTANIAN

Transcript

Hermanto Siregar

Dept. Ilmu Ekonomi – FEM, IPB

“PERSPEKTIF PERHEPI”, diselenggara-kan oleh PERHEPI & ISEI BOGOR RAYA

BPATP-Kementan, Bogor, 28/4/2016

MASALAH TINGGINYA SUKU BUNGA DAN IMPLIKASINYA BAGI EKONOMI PERTANIAN

TEORI-TEORI SUKU BUNGA

Apa fungsi suku bunga?

• The interest rate helps guarantee that current savings will

flow into investment to promote economic growth.

• It rations the available supply of credit, generally providing loanable funds to those investment projects with the highest return.

• It brings the supply of money into balance with the public’s demand for money.

• The interest rate serves as an important tool for government policy through its influence on the volume of savings and investment.

1

2

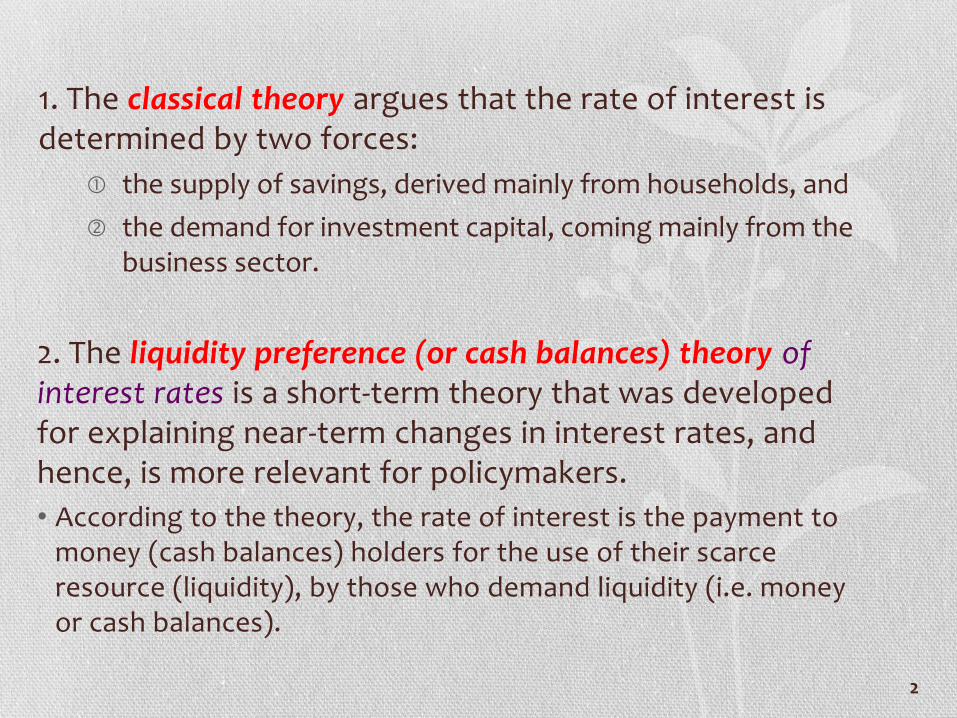

1. The classical theory argues that the rate of interest is determined by two forces:

the supply of savings, derived mainly from households, and

the demand for investment capital, coming mainly from the business sector.

2. The liquidity preference (or cash balances) theory of interest rates is a short-term theory that was developed for explaining near-term changes in interest rates, and hence, is more relevant for policymakers.

• According to the theory, the rate of interest is the payment to money (cash balances) holders for the use of their scarce resource (liquidity), by those who demand liquidity (i.e. money or cash balances).

3

3. The popular loanable funds theory argues that the risk-free interest rate is determined by the interplay of two forces:

the demand for credit (loanable funds) by domestic businesses, consumers, and governments, as well as foreign borrowers

the supply of loanable funds from domestic savings, dishoarding of money balances, money creation by the banking system, as well as foreign lending

Interest rates will be stable only when the economy, money market, loanable funds market, and foreign currency markets are simultaneously in equilibrium.

4. The rational expectations theory builds on a growing body of research evidence that the money and capital markets are highly efficient in digesting new information that affects interest rates and security prices.

4

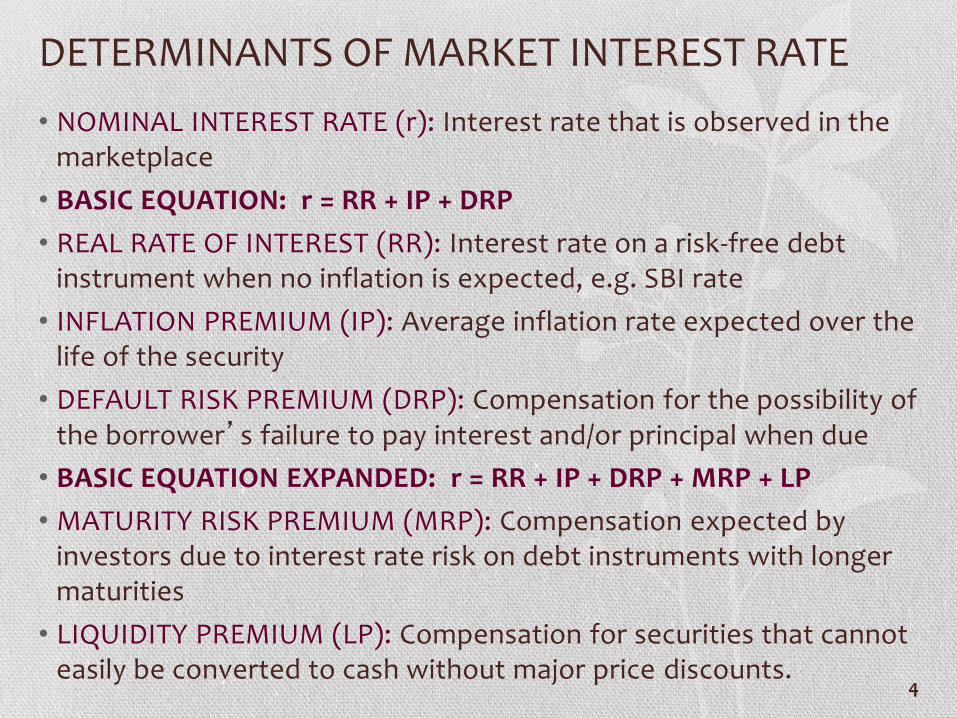

DETERMINANTS OF MARKET INTEREST RATE

• NOMINAL INTEREST RATE (r): Interest rate that is observed in the marketplace

• BASIC EQUATION: r = RR + IP + DRP

• REAL RATE OF INTEREST (RR): Interest rate on a risk-free debt instrument when no inflation is expected, e.g. SBI rate

• INFLATION PREMIUM (IP): Average inflation rate expected over the life of the security

• DEFAULT RISK PREMIUM (DRP): Compensation for the possibility of the borrower’s failure to pay interest and/or principal when due

• BASIC EQUATION EXPANDED: r = RR + IP + DRP + MRP + LP

• MATURITY RISK PREMIUM (MRP): Compensation expected by investors due to interest rate risk on debt instruments with longer maturities

• LIQUIDITY PREMIUM (LP): Compensation for securities that cannot easily be converted to cash without major price discounts.

5

In addition, normally there is also provisions charged by the banks.

Types of Inflation:

• COST-PUSH INFLATION: Occurs when prices are raised to cover rising production costs, such as wages, transport costs

• DEMAND-PULL INFLATION: Occurs during economic expansions when demand for goods and services is greater than supply

• SPECULATIVE INFLATION: Caused by the expectation that prices will continue to rise, resulting in increased buying to avoid even higher future prices

• ADMINISTRATIVE INFLATION: The tendency of prices, aided by union-corporation contracts, to rise wages (UMR) during economic expansion and to resist declines during recessions

Jika suku bunga nominal ingin diturunkan, maka inflasi dan determinan2 lainnya tsb harus juga diturunkan.

6

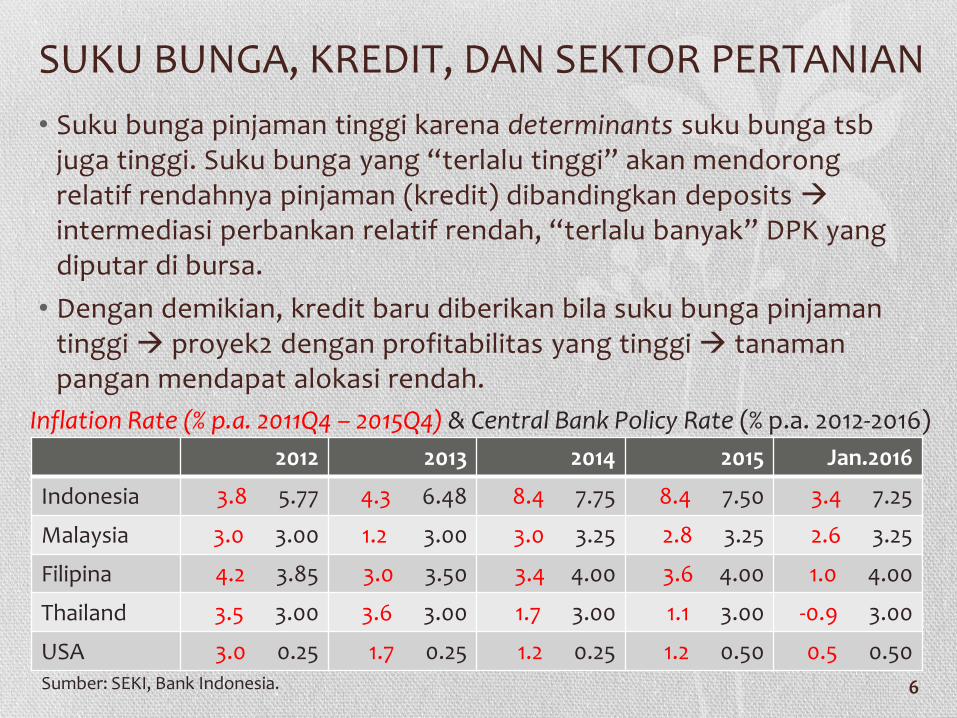

SUKU BUNGA, KREDIT, DAN SEKTOR PERTANIAN

• Suku bunga pinjaman tinggi karena determinants suku bunga tsb juga tinggi. Suku bunga yang “terlalu tinggi” akan mendorong relatif rendahnya pinjaman (kredit) dibandingkan deposits intermediasi perbankan relatif rendah, “terlalu banyak” DPK yang diputar di bursa.

• Dengan demikian, kredit baru diberikan bila suku bunga pinjaman tinggi proyek2 dengan profitabilitas yang tinggi tanaman pangan mendapat alokasi rendah.

Inflation Rate (% p.a. 2011Q4 – 2015Q4) & Central Bank Policy Rate (% p.a. 2012-2016)

7

• Manakah yang lebih penting: akses petani terhadap kredit atau suku bunga yang rendah?

• Dalam kasus absennya pasar kredit formal di pedesaan, akses kredit lebih penting sekalipun dengan suku bunga relatif tinggi—mengingat suku bunga pinjaman informal eksisting jauh lebih tinggi

• Dalam kasus pasar kredit formal sudah ada, maka baik akses maupun tingkat suku bunga sama pentingnya

• KUR yang saat ini dengan suku bunga 9% p.a. merupakan kebijakan kredit bersuku bunga relatif rendah (karena disubsidi oleh pemerintah kepada perbankan) dan membuka akses debitur/produsen relatif lebar karena adanya penjaminan.

• Namun demikian, alokasi KUR utk sektor pertanian masih sangat rendah yaitu sekitar 8% (tahun 2013), khusus di BRI 16% (tahun 2015). Ke depan, alokasi KUR terhadap sektor pertanian perlu diperluas—hal ini lebih crucial daripada menekan lebih jauh suku bunga KUR.

8

KESIMPULAN DAN IMPLIKASI

• Suku bunga dipengaruhi oleh banyak faktor dan kaitan antar faktor2 tsb sangat kompleks, sehingga menurunkan suku bunga bukan merupakan hal yang mudah, namun sangat diperlukan.

• Inflasi merupakan determinan penting suku bunga, dan di Indonesia sifatnya adalah costs push. Sehingga, perbaikan2 sisi supply perekonomian perlu diseriusi utamanya infrastruktur. Selain itu, efisiensi perbankan juga perlu ditingkatkan.

• Suku bunga perbankan yang tinggi bukan satu2nya faktor penyebab rendahnya kredit pertanian. Masalah yg lebih penting ialah akses terhadap kredit. Untuk itu, KUR yang membuka akses dan menerapkan suku bunga rendah perlu ditingkatkan terutama kepada sektor pertanian skala mikro dan kecil.

• Mengingat karakteristik komoditas pertanian yang beragam, maka KUR pertanian disarankan untuk dikembangkan dengan skema yang sesuai dengan karakteristik budidaya tanaman tsb.