105

PETROBRAS AT A GLANCE PETROBRAS AT A GLANCE December, 2011 1

PETROBRAS AT A GLANCEPETROBRAS AT A GLANCE

December, 2011

1

DISCLAIMER

FORWARD-LOOKING STATEMENTS:

DISCLAIMER

The presentation may contain forward-looking statementsb f h h f f

We undertake no obligation to publicly update orabout future events within the meaning of Section 27A ofthe Securities Act of 1933, as amended, and Section 21Eof the Securities Exchange Act of 1934, as amended, thatare not based on historical facts and are not assurances offuture results. Such forward-looking statements merely

fl t th C ’ t i d ti t f

revise any forward-looking statements, whether asa result of new information or future events or forany other reason. Figures for 2011 on areestimates or targets.

reflect the Company’s current views and estimates offuture economic circumstances, industry conditions,company performance and financial results. Such termsas "anticipate", "believe", "expect", "forecast", "intend","plan", "project", "seek", "should", along with similar oranalogous expressions are used to identify such forward

All forward-looking statements are expresslyqualified in their entirety by this cautionarystatement, and you should not place reliance onany forward-looking statement contained in this

t tianalogous expressions, are used to identify such forward-looking statements. Readers are cautioned that thesestatements are only projections and may differ materiallyfrom actual future results or events. Readers are referredto the documents filed by the Company with the SEC,specifically the Company’s most recent Annual Report on

presentation.

NON-SEC COMPLIANT OIL AND GAS RESERVES:

CAUTIONARY STATEMENT FOR US INVESTORSspecifically the Company s most recent Annual Report onForm 20-F, which identify important risk factors that couldcause actual results to differ from those contained in theforward-looking statements, including, among otherthings, risks relating to general economic and businessconditions including crude oil and other commodity

We present certain data in this presentation, suchas oil and gas resources, that we are not permittedto present in documents filed with the UnitedStates Securities and Exchange Commission (SEC)under new Subpart 1200 to Regulation S-K becauseconditions, including crude oil and other commodity

prices, refining margins and prevailing exchange rates,uncertainties inherent in making estimates of our oil andgas reserves including recently discovered oil and gasreserves, international and Brazilian political, economicand social developments, receipt of governmental

under new Subpart 1200 to Regulation S-K becausesuch terms do not qualify as proved, probable orpossible reserves under Rule 4-10(a) of RegulationS-X.

2

and social developments, receipt of governmentalapprovals and licenses and our ability to obtain financing.

OverviewOverview

3

PETROBRAS HISTORYBecoming a major , publicly traded oil company through organic growth

Incorporated in 1953 as governmentmonopoly for all hydrocarbon activities.Little or no reserves, production orrefining.

Brazilian Government (directly andindirectly), owns 48% of Petrobras, andmaintains control with 64% of votingshares.

A history of organic, operated, self fundedgrowth. Transition from a refiner ofimported crude to integrated self

Independent financial structure, withinvestment grade foreign currency ratingsnotched above the sovereign.imported crude to integrated self

sufficiency.

End of monopoly and opening of oil sectorto international participants Petrobras

notched above the sovereign.

Listing on NYSE and SEC registration in2000 Full quarterly disclosure in IFRS andto international participants. Petrobras

status as an operator, without privilegedposition.

2000. Full quarterly disclosure in IFRS andU.S. GAAP. Market cap year‐end 2010 ofUSD 237 billion.

Incorporation in 1953 as government

l

Discovery of shallow water offshore fields Discovery of mega

fields inElimination of Monopoly, Brazil achieves

19531953 19741974 19841984 19951995‐‐88

Listing on NYSE,

20002000 20102010

USD 70 bn

20062006‐‐77

monopoly

Reserves: 16.8 million boe

Production: 2 6 Thous BPD*

Reserves:800 million BOE

Production:177 Thous. BPD

fields in deepwater Campos Basin.

Last refinery completed ‘81

Monopoly, creation of oil law. Full deregulation by 2002.

self sufficiency in oil production

Discovery of Santos Pre‐salt

with market cap of $ 31 billion

1st Investment grade rating

capitalization and acquisition of rights to produce 5 bn BOE

Production: 2MM

4

2.6 Thous. BPD

Refining Cap: 41 Thous. BDP*

Refining Cap: 823 Thous. BDP

Production:467 Thous.BPD

Production:1 MM BPD oil in Brazil in ‘98

Production: 2MM BPD oil in Brazil

* 1954

OWNERSHIPBroad distribution among government, Brazilian, and foreign shareholders

Foreign ShareholdersNon-Voting

32%30%21%

Brazilian Non-Gov’tShareholders

N V ti

Voting

20%

32%

21%

39%

23%

36%

25%

30%

18%45%

Non-VotingVoting

Brazilian Gov’t *48%40%

21%

41%

23%

45%61%55%

Oct/1992 Jul/2000 After Aug/00 After Jul/01 Dec/2009 Dec/2010

Non-VotingVoting

40%41%

Oct/1992 Jul/2000 After Aug/00 offering

After Jul/01 offering

Dec/2009 Dec/2010

Brazilian government by law must maintain control Does so with 64% of voting shareso Brazilian government, by law, must maintain control. Does so with 64% of voting shares.

o Petrobras is the most actively traded ADR on NYSE in three years, and among all stocks, the 8th mostactively traded stock. On Bovespa, Petrobras most actively traded stock, by shares and by volume.

5*Includes: Republic, BNDES, BNDESPAR, Sov. Wealth Fund

BUSINESS MODELOperating as an integrated balanced oil company, dominant in Brazil

Exploration & Production

• Focus on production in deep and ultra‐deep waters;

D

• Licensed blocks guarantee access to reserves and economies of scale;

• New exploratory frontier, adjacent to existing operations.

Downstream

• Dominant position in a growing market, far from other refining centers;

Gas and Power

•Balance and integration between production, refining and demand.

• Gas infrastructure develeped for processand and transfer of gas;Gas infrastructure develeped for processand and transfer of gas;

• Complete flexibility to consume domestic and imported gas.

Biofuels

• High productivitiy of Brazilian ethanol;

• Large areas of available unused agricultural land;

• Large consumer market, with fleet and distribution in place.

6

Large consumer market, with fleet and distribution in place.

LOGISTICAL ADVANTAGESUniquely positioned to integrate upstream and downstream operations

Upstream Operations Downstream OperationsUpstream Operations Downstream Operations

Petrobras

Existing PipelinesRefineriesMarine Terminal

Logistical Synergies Stable Cash FlowsGrowing MarketDominant Position

•Leadership in all segments of •Strong organic demand in one •Main oil producing basins and •Diversified cash flows with

Other CompaniesMarine Terminal In Land Terminal

•Leadership in all segments of the value chain

•Market position ensures economies of scale and efficient business model

•Strong organic demand in one of the fastest growing global markets

•Attractive domestic market opportunities for upstream, d t d th

•Main oil producing basins and refining located in S.E. Brazil, near GDP centers

•Logistical infrastructure fully developed

•Diversified cash flows with several growth drivers

•Reduced volatility of cash flows due to ability to smoothen prices fluctuations i th d ti k t

7

downstream and other energy segments

in the domestic market

BUSINESS SEGMENTSFully integrated across the hydrocarbon chain, dominated by Brazilian production

Adjusted EBITDA US$ 32.6 Billion1 (2010)

RTM10% G&P

2010 Proven Reserves (SPE)15.986 billion boe

Sh ll W t4%Distribution3%International6%

Shallow Water(0-300m)9%Deep Water

(300-1,500m)50%

Onshore9%

E&P77%

Ultra-Deep Water(>1,500m)

Our Main Segments: Key Statistics and Market Positions (2010)

Exploration and RTM (incl. Distribution Gas and Power International Biofuels

( 1,500m)32%

Production

• 15.3 Bn boe of 1P(SPE)

• 2.3 mm boed production

98 5% f B ili

Petrochemicals)

• 12 refineries (Brazil)

•2.0 mm bbld refining

Distribution

• 7,306 service stations

•38.8% share of distribution volume

Gas and Power

• 9,239 km of pipelines

• Participation in 20 of the 27 gas discos in

International

• 25 countries

• 0.7 Bn boe of 1P(SPE)

h b d

Biofuels

• 3 new Biodiesel Plants

• Ethanol: Opening•98.5% of Brazilian production

• 20% of global DW and UDW production

capacity

• 11.2 mty materials nominal capacity (2)

distribution volume the 27 gas discos in Brazil

• 5,943 MW of generation capacity

• 245 thous. boed production

• 281 thous. bbl/d refining capacity

•Petrochemicals Gas &

• Ethanol: Opening new markets

• Responsible for 10% of Brazilian ethanol exports

8

•Petrochemicals, Gas & Power activities

Notes: (1) Includes Corporate and Elimination; (2) Through Braskem and Quattor

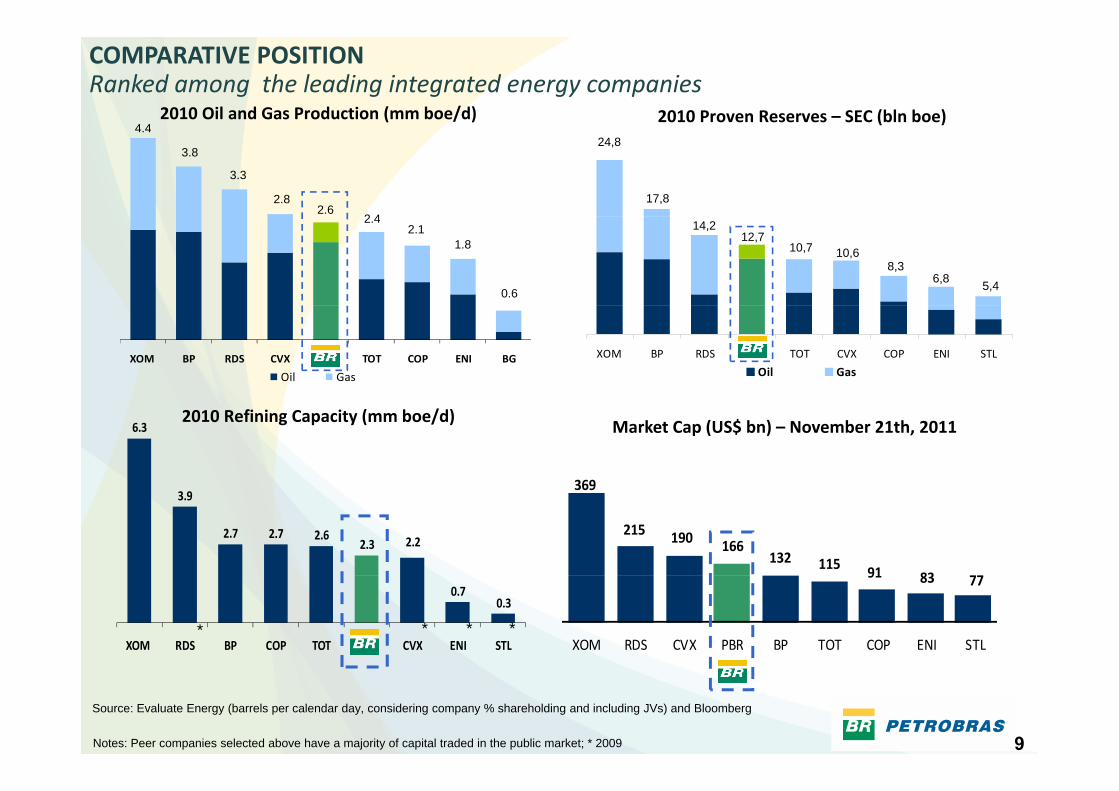

COMPARATIVE POSITIONRanked among the leading integrated energy companies

2010 Proven Reserves – SEC (bln boe)2010 Oil and Gas Production (mm boe/d)4 44.4

3.8

3.3

2.82.6

2 4

24,8

17,8

2.42.1

1.8

0.6

14,212,7

10,78,3

6,8 5,4

10,6

XOM BP RDS CVX BR TOT COP ENI BG

Oil Gas

XOM BP RDS BR TOT CVX COP ENI STL

Oil Gas

6.32010 Refining Capacity (mm boe/d)

Market Cap (US$ bn) – November 21th, 2011

3693.9

2.7 2.7 2.62.3 2.2

369

215 190 166132 115 91 83

0.70.3

XOM RDS BP COP TOT BR CVX ENI STL

91 83 77

XOM RDS CVX PBR BP TOT COP ENI STL* * **

9Notes: Peer companies selected above have a majority of capital traded in the public market; * 2009

Source: Evaluate Energy (barrels per calendar day, considering company % shareholding and including JVs) and Bloomberg

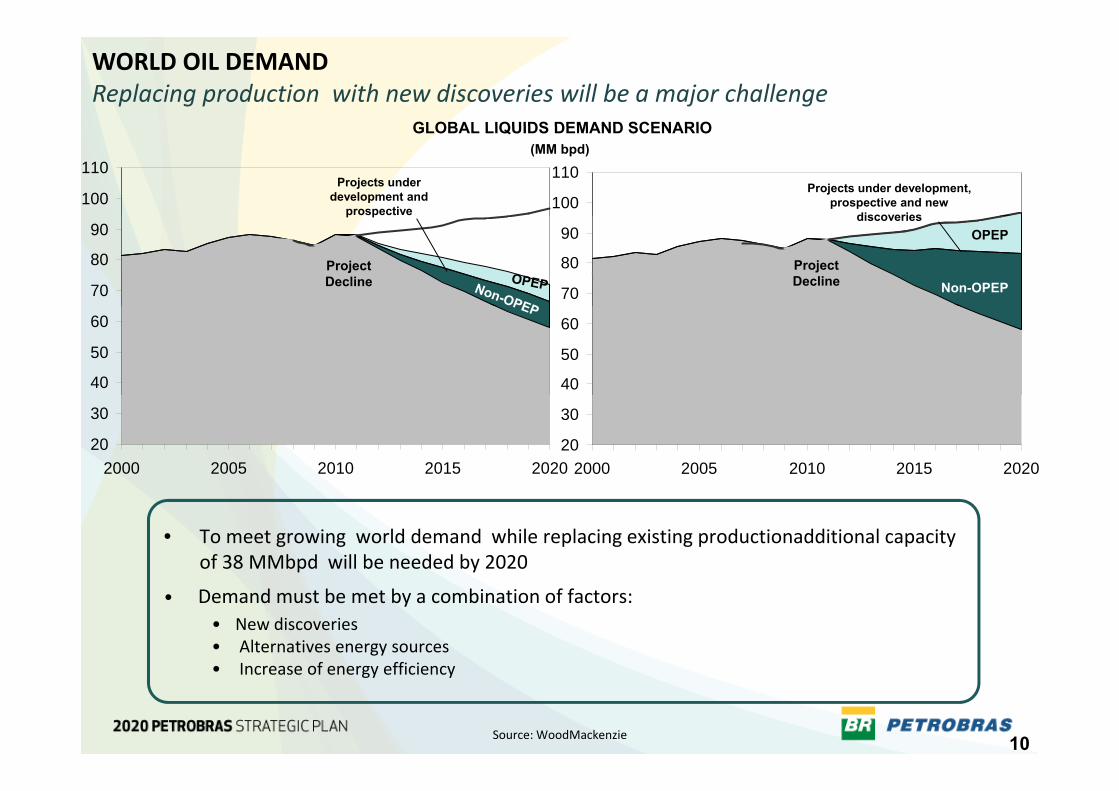

GLOBAL LIQUIDS DEMAND SCENARIO

WORLD OIL DEMANDReplacing production with new discoveries will be a major challenge

100

110

100

110(MM bpd)

GLOBAL LIQUIDS DEMAND SCENARIO

Projects underdevelopment and

prospective

Projects under development, prospective and new

discoveries

70

80

90

70

80

90p p

Project Decline

Project Decline Non-OPEP

OPEP discoveries

40

50

60

40

50

60

20

30

2000 2005 2010 2015 202020

30

2000 2005 2010 2015 2020

• To meet growing world demand while replacing existing productionadditional capacity of 38 MMbpd will be needed by 2020

• Demand must be met by a combination of factors: • New discoveries• Alternatives energy sources

I f ffi i

10

• Increase of energy efficiency

Source: WoodMackenzie

BRAZIL LEADERSHIP IN RECENT DISCOVERIESDeep‐water discoveries in Brazil represent 1/3 of the worldwide discoveries in the last 5 years

New Discoveries 2005‐2010

(33,989 million bbl) Deep‐Water Discoveries

62%38% BrasilBrazil62%

OutrosOther

Other Discoveries Deep-Waters

• In the last 5 years, more than 50% of the new discoveries (worldwide) were made in deep waters

• The development of these reserves will demand additional capacity from the supply chain

• Expansion of the oil and gas chain in Brazil is in line with this perspective

Petrobras expects to double its proved reserves until 2020, keeping the discovery cost around US$2/boe

11Source: PFC Energy

COMPETIVE ADVANTAGEReserves in ultra‐deep water in Brazil benefit from comparatively low break‐even

Expected Costs of Production

140

D t d

S$/bbl‐200

8)

80

100

120Deepwater and Ultra‐deep water

Oil Shales

Gas to liquids

Coal to liquids

uction

costs (U

40

60

80

CO₂ ‐

EOR

EOR Arctic

Heavy oil and

bitumen

Shales liquids liquids

Prod

u

20 Produced MENA

Other convention

al oilPetrobras expected maximum break‐even cost

Reserves (bn bbls)

1000 2000 3000 4000 5000 6000 7000 8000 9000 100000

12Source: IEA – Outlook 2008

DEEPWATER LEADERSHIPA history of developing technology and know‐how in Brazilian waters

1977Enchova410ft125m

1988Marimbá1 610ft1,610ft491m

1994Marlim3,370ft1,027m

1997Marlim Sul5,600ft1,707m

2003Roncador6,180ft

2009Lula

7,125ft2,172m

45Petrobras

1,707m ,1,884m

2,172m

Deepwater Production2010 Gross Global Operated¹

Offshore Production Facilities

12

13

15

15

45

BP

ExxonMobil

StatoilHydro

Shell

Petrobras

8

8

9

10

12

C Philli

CNOOC

Total

Anadarko

Chevron

100

5

8

0 20 40 60 80 100

Others

ENI/Agip

ConocoPhillips

FPSO Semi Spar TLP Other

13

FPSO Semi Spar TLP Other

Source: PFC Energy Note: (1) These 15 operators account for 98% of global deepwater production in 2010. Minimum water depth is 1,000 feet (about 300 meters)

OIL PRODUCTIONWith access to abundant reserves, Petrobras can more than double production

1 120

246142

6,418

618

1.120

180

125

3,993

2,772+ 35 Systems

2 575

321 317 334 435

618

111 132 14414199 96

93 962,386 2,516

oe/day

2,772

845Transfer of Rights

+10 Post‐Salt Projects

+8 Pre‐Salt Projects

+1 Transfer of Rights

2,575

3,070

4,910

1.855 1.971 2.004 2.100

2008 2009 2010 2011 2015 2020

1,148543

Pre-Salt’000

b Transfer of Rights13

Added Capacity

Oil: 2,300,000 bpd

2008 2009 2010 2011 2015 2020

Oil Production‐ Brazil Natural Gas Production ‐ Brazil Oil Production ‐ International Natural Gas Production ‐ International

• Pre‐salt and Transfer of Rights will represent 69% of the additional capacity up to 2020;

• Pre‐Salt participation in the total production will enhance from the current 2% to 18% in 2015 and 40.5% in 2020.

14Note: Does not include Non‐Consolidated International Production.

2010 TOTAL OIL CONSUMPTION* (MM BPD)

GROWING MARKETBrazil is the world’s seventh largest oil consumer and growing fast

9,06

2010 TOTAL OIL CONSUMPTION (MM BPD)*Includes ethanol and biodiesel

>3 MM bpd 2-3 MM bpd <2 MM bpd19,15

4,45

3,32 3,20 2,81 2,60 2,44 2,38 2,28 1 99, 2,28 1,99 1,80 1,74 1,59

27 1 1980Barrels per year

PER CAPITA OIL CONSUMPTION

15,314,8

27,1

12,4

16,0

25,0

9 912,8

22,3

2010

2000

1980

0,63,7 1,4

4,52,5

4,9

9,9

15Sources: BP Statistical Review / Petrobras estimates

OECD

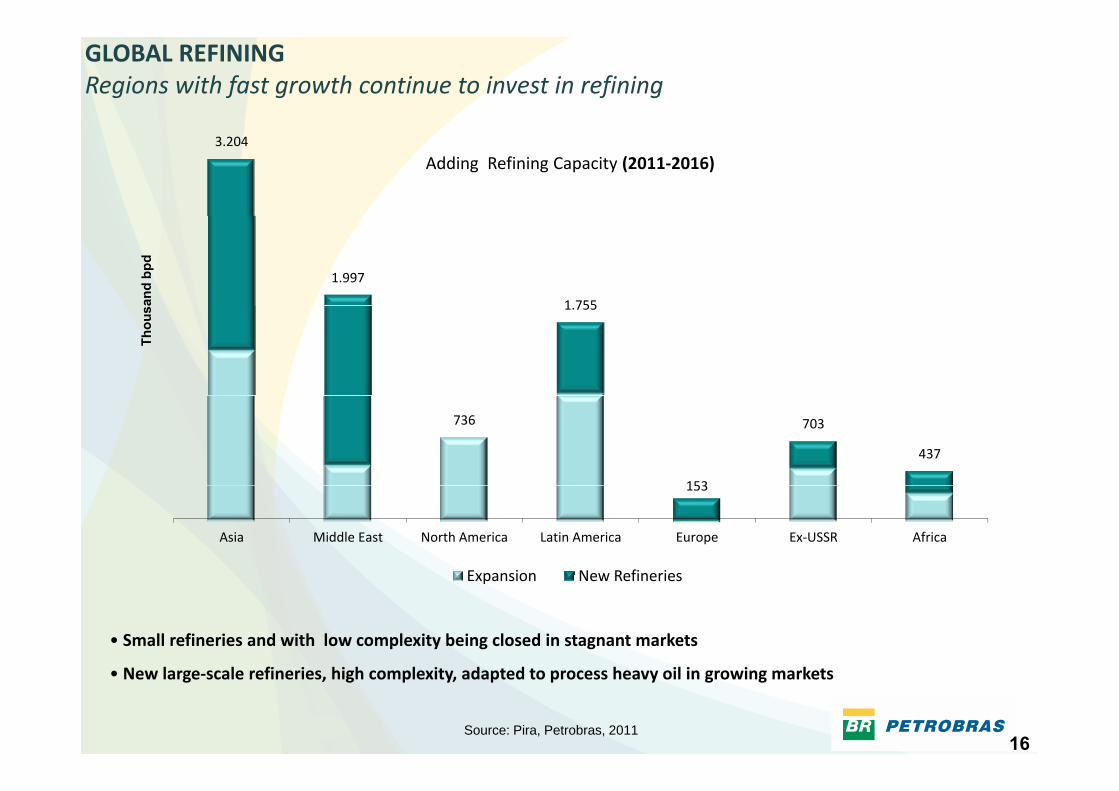

GLOBAL REFININGRegions with fast growth continue to invest in refining

3.204

Adding Refining Capacity (2011‐2016)

1.997

1 755and

bpd

1.755

Thou

s

736

153

703

437

153

Asia Middle East North America Latin America Europe Ex‐USSR Africa

Expansion New Refineries

• Small refineries and with low complexity being closed in stagnant markets

Expansion New Refineries

16

• New large‐scale refineries, high complexity, adapted to process heavy oil in growing markets

Source: Pira, Petrobras, 2011

PRODUCT PRICING Free market follows international prices in the long term

140

160 US$/bbl2002-2011

Average Realization Price ‐ Brazil

Average Realization Price ‐ USA

80

100

120

40

60

20

2011201020092008200720062005200420032002

• Petrobras policy lags the international oil market when prices increase or decrease, leading to more stable cash flows

I N b 10% i i li 2% i i di l i

17

• In November, 10% increase in gasoline, 2% increase in diesel prices

Exploration & ProductionExploration & Production

18

E&P STRATEGYSustainable development of hydrocarbon reserves

Increase oil and gas reserves and production, in a sustainable manner, and be recognized for its excellence in E&P operations, placing the Company among the world’s

five largest oil producers

2011‐15 Business Plan Highlights:

• 65% of Capex allocated to production development.

• 19 large projects, adding capacity of 2.3 million bpd.19 large projects, adding capacity of 2.3 million bpd.

• Drilling of more than 1,000 offshore wells, of these 40% is exploratory and 60% is production developmentdevelopment.

• In 2020, the pre‐salt production will correspond to 40.5% of the oil production in Brazil.

19

Proved Reserves – SPE criteria

RESERVES AND RECOVERABLE VOLUMESRapid growth in reserves from discoveries in deep waters

30.000

Million boe

25.000

15 000

20.000

Whales Park

Pre‐salt: Lula and Cernambi 15,28 Bi boe

10.000

15.000

Roncador

Whales Park, Mexilhão

5.000Garoupa

Namorado

Marlim

Guaricema

0

pCarmópolis

20

Onshore 0‐300 m 300‐1500 m > 1500 m Pre‐salt's Recoverable Volume Transfer of Rights

* Lula/Cernambi, Iara, Guará and Whales Park, ranging from 8.1 to 9.6 Billion boe

*

RESERVE PROFILEProved reserves consist largely of offshore oil that is relatively heavy

Proven Reserves as of Dec/2010 (SPE/ANP)(15.28 billion boe)

Oil + Condensate

< 22º API(heavy) 22 – 31 º API

84%

34%45%

(heavy)(intermediate)

5%11%Associated Gas

15% 6%

Gas > 31 º API (light)

Non‐Associated Gas

( g )

39%DevelopedProven Reserves

UndevelopedProven Reserves

39% 61%

21

BRAZILIAN BASINSOffshore brazil is a vast area, still underexplored

USAUSA

22t

PRODUCTIONPetrobras history is to grow production by expanding into new frontiers

2500 Deep water

Shallow water 2.004

ThousandThousand bpdbpd

2000Onshore

1500

1601

1.271

1000

42

749653

500

211 230 21475

400 292 189

42

181

0

1980 1990 2000 2010

106 211 230 214

23

Onshore Shallow water Deep water Deep and ultra‐deep water

Pre‐salt

Campos Basin Santos Basin

OFFSHORE GEOLOGYProducing from pre‐salt reservoirs will drive future investment

Campos Basin Santos Basin

EastWest

PostPost--salt turbidites:salt turbidites:current productioncurrent production

Albian carbonates

Pre-salt carbonatesPre-salt carbonates:Supergiants oil fields

Near term prod ction increase Mid and long term prod ction increase

24

Geological cross section in Santos Basin used to explain petroleum systems of Santos and Campos basins

Near-term production increase Mid and long-term production increase

E&P FOCUSMaintain and expand traditional areas, while transitioning to new reservoirs

Tertiary and Upper

E&P portfolio has around 3,000 projectsE&P portfolio has around 3,000 projects

1 • Maintain production:

• Implement full development of the main production 1

Tertiary and Upper CretaceousTurbidites

concessions.

• Decrease decline in existing fields.

• Operational maintenance in existing Production Systems.

Albian carbonates

Salt

• Continuous exploration effort.2

Pre‐salt carbonates

SantosCampos

2 • Explore, appraise and start production mostly in existing Production Systems (inside existing ring fences).3 4

3 • Explore, appraise and start production mostly in existing Production Systems (inside existing ring fences).

4 • Explore & appraise. Extended Well Tests in main discoveries. Start production of pilot projects. Declare commerciality. Reduction of the project implementation time: equipments standardization,

25

y p j p q parrival of new drilling rigs, replicante FPSOs.

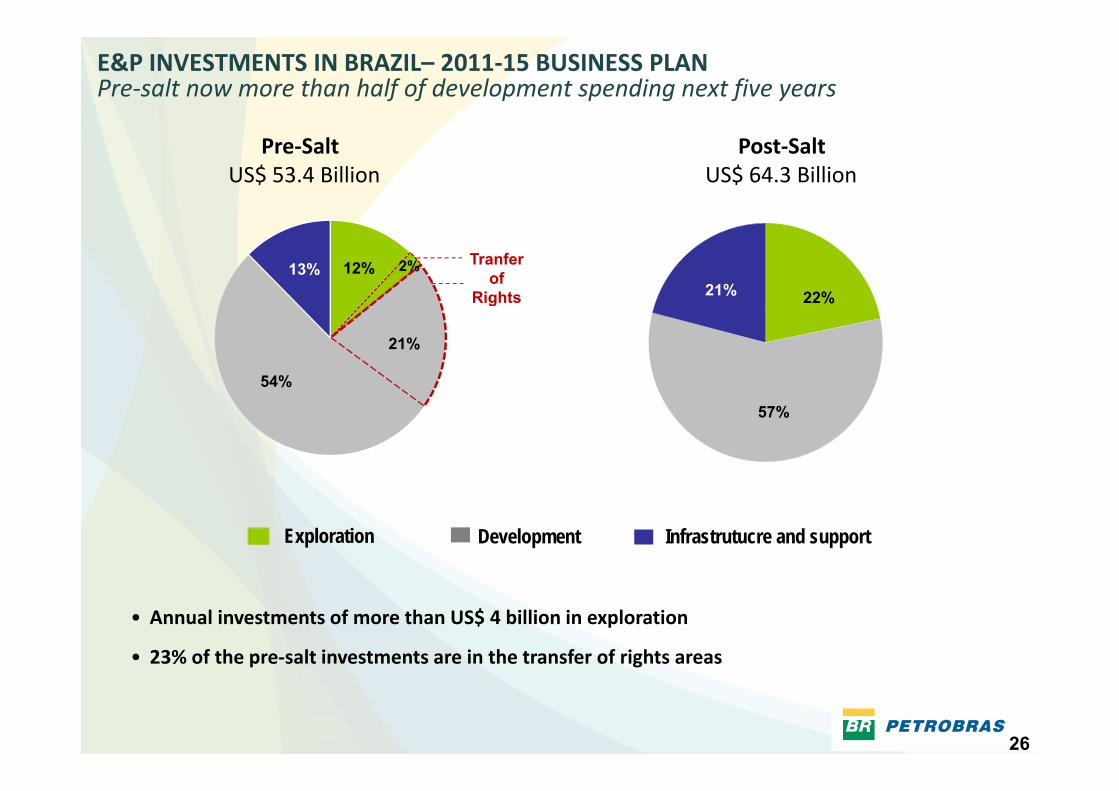

E&P INVESTMENTS IN BRAZIL– 2011‐15 BUSINESS PLANPre‐salt now more than half of development spending next five years

Pre‐SaltUS$ 53.4 Billion

Post‐SaltUS$ 64.3 Billion

22%21%12% 2%13% Tranfer

ofRights

54%

21%

g

57%

Exploration Development Infrastrutucre and support

• Annual investments of more than US$ 4 billion in exploration

• 23% of the pre‐salt investments are in the transfer of rights areas

26

p g

66 OFFSHORE EXPLORATORY WELLS EXPECTED IN 2012

F dF d

Mar Mediterrâneo CearáCeará

TacutuPará-

MaranhãoPará-

Maranhão

Foz doAmazonas

Foz doAmazonas

BarreirinhasBarreirinhas

3

4

PotiguarPotiguar

Solimões

Amazonas

Paraíba PernambucoParaíba Pernambuco

ParnaíbaAlto Tapajós

Marajó 3

Sergipe/AlagoasSergipe/AlagoasParecis

Paraíba-PernambucoParaíba-PernambucoAlto TapajósAcre

BananalCamamuC

JacuipeJacuipe

Tucano

Jatobá

9

PantanalCumuruxatibaCumuruxatibaJequitinhonhaJequitinhonhaAlmadaAlmadaCamamuCamamu

MucuriMucuri

pS. Francisco

5

Espírito SantoEspírito SantoParaná

CamposCampos16

11Brazilian Sedimentary

B i

lh500km

SantosSantos

PelotasPelotas

1618

Basins

27

Mar VermelhoPelotasPelotas

MAIN PROJECTSLarge projects sustain production increases Pre‐Salt and Transfer of

Rights Projects

NG Projects

P S l P j

Lula PilotFPSO BW Cidade Angra dos Reis100.000 bpd Lula NE

Juruá GNA

F 1

EWTs

Post‐Salt Projects

p

Cachalote andBaleia Franca FPSO Capixaba100.000 bpd

Guará (North) FPSO Cidade de

IlhabelaParque das Baleias

FPSO P 58

MexilhãoJaquetaHG

Guará Pilot 2FPSO Cidade de

São Paulo120.000 bpd

FPSO Cidade de Paraty

120.000 bpd

FPSO P‐67 Replicant 2Tambaú

Franco 1 Transfer of Rights

FPSO P‐74 150.000 bpd

3.070Mil bpd

Marlim Sulmodule 3

Baleia AzulFPSO Cidade de

Anchieta100.000 bpd

Papa‐Terra TLWP P‐61 &FPSO P‐63

Ilhabela150.000 bpd

FPSO P‐58180.000 bpdUruguá

FPSO Cidade de Santos

35.000 bpd

120.000 bpd

Cernambi SouthFPSO Cidade de Mangaratiba150 000 bpd

Replicant 2150.000 bpdLula Central

Tambaú FPSO Cidade de

SantosNG

2.004 2.100

2000

2500

3000module 3SS P‐56

100.000 bpd

JubarteFPSO P‐57180.000 bpd

(FPSO Espadarte reallocation)

RoncadorRoncador

150.000 bpd150.000 bpd

FPSO P‐66Replicant 1150.000 bpdLula Alto

Baleia AzulFPSO

1000

1500

2000 Roncador Módule 4 FPSO P‐62180.000 bpd

Roncador module 3SS P‐55

180.000 bpd

Tiro/SidonFPSO Cidade de

Tiro PilotSS‐11

Atlantic Zephir30.000 bpd ESP/MarimbáAruanã

FPSO

MarombaFPSO

100.000 bpdSiri

Jaqueta e FPSO

FPSO60.000 bpd

EWTs Lula NE e Cernambi

FPSO BW Cidade São Vicente30.000 bpd

0

500

1000 Itajaí80.000 bpdEWT Guará

FPSO DynamicProducer30.000 bpd

FPSO 40.000 bpd

FPSO 100.000 bpd

50.000 bpd

4 EWTsPre‐salt

EWT Carioca FPSO Dynamic

Producer30.000 bpd

3 EWTsPre‐salt

5 EWTsPre‐salt

5 EWTsPre‐salt

28

0

2010 2011 2012 2013 2014 2015

NEW PRODUCTION UNITS 2012Production capacity growth above 400 thousand bpd during the period

Development ProjectCapacity

(thousd. bpd)Petrobras % Forecast

Tambaú Natural Gas 100% PBR 1Q 2012

Pilot Baleia Azul (Pre salt) 100 100% PBR 3Q 2012Pilot Baleia Azul (Pre‐salt) 100 100% PBR 3Q 2012

Tiro Sidon 80 100% PBR 3Q2012

Roncador mod. 3 SS P‐55 180 100% PBR 4Q 2012

Pilot Guará (Pre‐salt) 120 45% PBR 4Q 2012

Additional Total Capacity ‐ Petrobras: 414 thousand bpd

o 8 ultra deepwater rigs have arrived during 2011. 15 more contracted to arrive by end of 2012.

o Additional rigs will accelerate ramp‐up of new systems.

29

New Units in Campos B i 2011 15

New UnitsFPSO

FPSO Espadarte

P‐58

201120122013Basin: 2011-15 2011

P‐56 – 100.000 bpd

2012

FPSO Espadarte

20142015

P‐62

P‐55

P‐55 – 180.000 bpd

FPSO Espadarte – 100.000 bpd

2013P‐58 – 150.000 bpd

P‐61 – 150.000 bpd

P‐62 – 180.000 bpd

P 63 150 000 bpd

P‐56FPSO

P‐63 – 150.000 bpd

FPSO (Marimbá) – 40.000 bpd

FPSO (Aruana) – 100.000 bpd

2014FPSO (Baleia Azul) – 60.000 bpdFPSO

20152015FPSO (Maromba) – 100.000 bpd

30

FPSO

P‐61

P‐63

2010

PRODUCTION SYSTEMS7 new systems until 2015, having already hired six

Lula Pilot

FPSO Cidade Angra dos Reis – 100.000 bpd

The 1st production well in Lula Pilot reached 36,000 boed (28,000 bpd of oil), being the36,000 boed (28,000 bpd of oil), being the most prolific well from Petrobras

2012Guará Pilot

2013

Guará Pilot

FPSO Cidade de São Paulo – 120.000 bpd

Lula Northeast

FPSO Cidade Paraty – 120.000 bpd

2014Guará North

FPSO – 150.000 bpd

Cernambi

FPSO – 150.000 bpd

2015Lula Central

FPSO – 150.000 bpd

Franco – Transfer ofRights

31

Lula High

FPSO – 150.000 bpd

FPSO – 150.000 bpd

VARREDURA PROJECTTechnological development and exploratory optimization in existing concessions

• Additional recoverable volume from discoveries:

Varredura ProjectDescobertas do Pr é-sal na Bacia de Campos2009/10 (VARREDURA)

Discoveries in Pre‐salt Campos Basin 2009/10 (Varredura)

• Post‐salt: Marimbá, Marlim Sul and Pampo:1,105 MM boe;

• Pre‐salt: Barracuda, Caratinga, Marlim, MarlimLeste, Albacora and Albacora Leste: 1,130 MMboe*.

•Well productivity exceeds 20,000 bpd

67 exploratory wells will be drilled between 2011 and 2015 in production areas in

Campos basin

32*No volumes have been announced regarding the Marlim Leste and Albacora Leste discoveries.

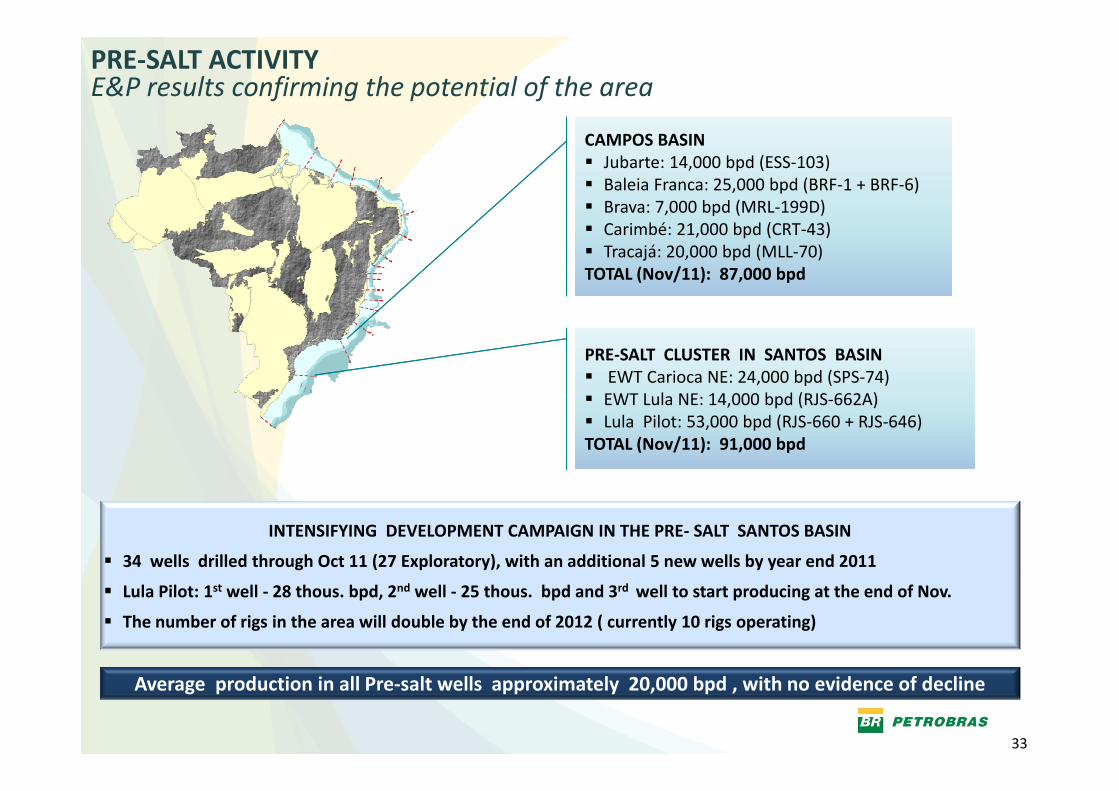

E&P results confirming the potential of the areaPRE‐SALT ACTIVITY

CAMPOS BASIN Jubarte: 14,000 bpd (ESS‐103) Baleia Franca: 25,000 bpd (BRF‐1 + BRF‐6) Brava: 7,000 bpd (MRL‐199D) Carimbé: 21,000 bpd (CRT‐43) Tracajá: 20,000 bpd (MLL‐70)TOTAL (Nov/11): 87,000 bpd

PRE‐SALT CLUSTER IN SANTOS BASIN EWT Carioca NE: 24,000 bpd (SPS‐74)

EWT L l NE 14 000 b d (RJS 662A) EWT Lula NE: 14,000 bpd (RJS‐662A) Lula Pilot: 53,000 bpd (RJS‐660 + RJS‐646)TOTAL (Nov/11): 91,000 bpd

INTENSIFYING DEVELOPMENT CAMPAIGN IN THE PRE‐ SALT SANTOS BASIN

34 wells drilled through Oct 11 (27 Exploratory), with an additional 5 new wells by year end 2011

Lula Pilot: 1st well ‐ 28 thous. bpd, 2nd well ‐ 25 thous. bpd and 3rd well to start producing at the end of Nov.

The number of rigs in the area will double by the end of 2012 ( currently 10 rigs operating)

33

Average production in all Pre‐salt wells approximately 20,000 bpd , with no evidence of decline

NEW TECHNOLOGIESPetrobras is implementing cutting‐edge technologies

OIL/WATER SUBSEA SEPARATION

‐ Resolves limitations from growing

RAW WATERINJECTION

‐ Increases production in existingResolves limitations from growingwater production

‐ Separates water and oil under the sea, reinjecting water and relieving h i f h f i

Increases production in existingsystems

‐ 3 subsea systems for pumping raw water (with little treatment) to

i h i i ithe size of the surface equipment on the platform

‐ Field: Marlim (Nov/2011)

pressurize the reservoir, increasing recovery factor without increasing surface systems. Pioneer in the world in such water depth

34

‐ Field: Albacora (Dec/2011)

bbl/d

PRODUCTION BEHAVIORReservoirs and equipments set production over time

bbl/d

Potential1

Natural decline of reservoir *Possible causes:‐ decrease in reservoir pressure

Production1 Potential2

Production2

‐ increase jn water production

* Assuming 100% efficiency of the equipment installed

2

Actual production, a combination of:‐ Natural decline of the reservoir and ‐ Equipment efficiency- problems with lift;hydrate formation in the collection line;compression failures;power outages;t t

Time power outages;equipment failures;scheduled and unscheduled maintenanceetc...

t1 t2

o 2011 production decline in some fields above historical rates was due to reducedequipment efficiency, not geology.

35

oOn average, reservoir decline was below expected.

PRODUCTION ‐ 2011Production below target mostly explained by unplanned maintenance

l d i

25.000Unprogrammed Stoppages

Production loss due to operational causes – effect on annual production

bpd

)

Unplanned maintenance and additional time for

planned maintenance in the 9M11 lowered production

15.000

20.000 Programmed Stoppages

(tho

usd.

9M11 lowered production by an average of 44

thousand bpd in the year

0

5.000

10.000

01Q 2Q 3Q

Other factors that reduced production relative to targets

o Delays in the completion and connection of wells, due to the late arrival of new rigs fromo Delays in the completion and connection of wells, due to the late arrival of new rigs frominternational shipyards.

o Logistical and market restrictions reduced production of natural gas, in turn reducing oilproduction by 20 thousand. Bpd during 9M11 (Uruguá: 10 thousd. bpd; Lula: 10 thousd. bpd)

36

production by 20 thousand. Bpd during 9M11 (Uruguá: 10 thousd. bpd; Lula: 10 thousd. bpd)

LIFTING COSTSCosts pressured by a combination of factors during first nine months of 2011

$$ US$/barrilR$/barril

104.97

117.36113.46

175.30

187.78 186.07

76.86

86.48

30.48 31.25

24 67 25 58

35.0050.66

54.11

42.72 43.47

55.14134.51

147.02

24.26 26.1331.66

34.21 31.80

14.07 15.2919.10

21.8817.88

24.67 25.58

18.46 17.34 19.00 20.93 22.3110.60 10.29 11.38 13.12 13.37

3Q10 4Q10 1Q11 2Q11 3Q11 3Q10 4Q10 1Q11 2Q11 3Q11

Lifting costBrent Government take

o In 3Q11 lifting costs increased by provisioning for 2011 Collective Bargaining Agreement, under negotiation.

37

o Increasing lifting cost trend in 2011 as a result of start‐up of new production systems, increase in planned andunplanned stoppages and higher oil prices affecting service and energy costs.

E&P PROFITABILITY IN BRAZIL

E&P Net Income ($/boe)l

Profitability of oil Production in Brazil fully exposed to oil pricesE&P Net Income ($/boe)

20

25

Brent vs. E&P Net income per Barrel

10

15

20

per B

arrel (US$)

0

5

10

Peer RangePetrobrasPeers

Net income

60%E&P ROCE

02005 2006 2007 2008 2009 2010

Brent (Average in dollars)

30%

40%

50%• E&P profitability strongly correlated to oil price

• Production in Brazil: 86% oil and 14% gas

• Higher net profit per barrel yields better return

10%

20%

30%

Peer Range

g p p ythan its peers

• Stable regulatory environment allows for capturing the benefits of the increase in oil prices Petrobras

Peers

38

0%2005 2006 2007 2008 2009 2010

Peers: BP, CVX, XOM,RDS, TOTSource: PFC Energy

PROFITABILITYNew E&P projects generate attractive returns

40,0%

45,0%

Key Assumptions:

30,0%

35,0% • 150,000 bpd FPSOs

• Production of 500 MM barrels

• Ramp‐up in line with industry

15,0%

20,0%

25,0% • Ramp‐up in line with industry

• Historic decline rate

• Oil value = 95% Brent

5,0%

10,0%

15,0%• Does not include exploration and acquisition costs

0,0%60 70 80 90 100 110

Case 1 – US$12/boe Capex / US$5/boe Opex

Case 2 US$15/boe Capex / US$7/boe Opex

(expected scenario)

US$/ bbl

h h ill h b fi i f d d d i

Case 3 – US$12/boe Capex / US$5/boe Opex without Special Interest (such as Transfer of Rights)

Case 2 – US$15/boe Capex / US$7/boe Opex

39

• The graph illustrates the cost‐benefit ratio of a standard productiondevelopment in Brazil, using assumptions based on previous experiences

DISTRIBUTION OF UPSTREAM REVENUESIn higher oil price environment, net income per BOE benefits from concession terms

Distribution of the Realization Price of a Barrel of Domestically Produced Oil

$ per Barrel Realization Price % Share of Realization Price

80,0%

100,0%

$70,00

$90,00

60,0%

80,0%

$50,00

20,0%

40,0%$30,00

0,0%

2003 2004 2005 2006 2007 2008 2009 2010 1S11$(10,00)

$10,00

2003 2004 2005 2006 2007 2008 2009 2010 1S11

Other COGS DD&A Income TaxLifting Other

-20,0%( )

40

Net Income R&DSG&A Exploratory Costs Government Take

WHAT IS PRE‐SALT?

Located in a remote area, up to 300 km offshore

CorcovadoWater depths that canexceed 2,000 meters

Total depth from5,000 to 7,000 meters

Salt layer more than 2,000 t thi k

Post‐Salt LayerFocus up to 2006

meters thick.

Pre‐Salt LayerNew Exploratory Frontier

Large Oil CarbonaticReservoirs

41

PRE‐SALT Pre‐salt represent a large and relativly unexplored area

42

SANTOS PRE‐SALT MASTER PLAN HIGHLIGHTSFrom 2006 to 2010...

Infraestructure

Pipeline Tupi‐Mexilhão

FPSO

s/nitive Systems

Pipeline Tupi Mexilhão

Defin

Piloto de Lula (AR)

EWTs

FPSO

s/E

Tupi (CSV) Guará (DP)

W Polaris Cajun (SS76)

New

Rigs

W Emminence (SS69)

W Polaris (NS28)Clipper

(NS21)

Louisiana (SS51)

W Taurus (SS68)

Stena (NS25)*

Victoria (SS70)W Orion (SS78)

Ocean Valor (SS77)Cajun (SS76)

Goldstar (SS73)Dave Beard (SS71)

Deepwater Expedition(NS20)*

Paul Wolf (SS53)

Pré‐Sal/Parati

TupiDiscoveries Carioca

Bem‐Te‐ViGuará

Iara

Caramba

Júpiter

Franco

Goldstar (SS73)

Iracema

43

2006 2008 2009 2010... 2007

* Sondas que não estão mais sob contrato com a Petrobras ou consórcios operados pela Cia.

SANTOS PRE‐SALT MASTER PLAN HIGHLIGHTS... 2011 and onwards

frastructure

ROTA 2 ROTA 3stem

s

Guará N t

Inf

LulaAlto

FPSO

s/Definitive Sys

Piloto Guará

Piloto Lula NE

Norte

Cernambi Sul

LulaCentral

Franco1

Os/EW

Ts

Lula NE (CSV)

Cernambi (CSV / 2S 2011) 4 EWTs 3 EWTs 5 EWTs 5 EWTs

sFPSO Carioca

(DP / 2S 2011)

Vitoria 10000

New

Rigs

2013 20142012

7 drilling rigsVitoria 10000

(NS‐30)

+ 3 rigs

Drilling Rigs to be contracted(includes up to 28 rigs to be constructed in Brazil)

44

2011 2013 2014 2015... 2012 2016

DEVELOPMENT OF PRE‐SALTAll first‐phase units under construction or being contracted

2 FPSOs performing EWTs

Contracted(start‐up in 2012 and 2013)

Contracted (start‐up in 2014)

Significant production increase

Phase 1b

Production > 1 MM bbl in 2017

Phase 1aPhase 0

Acquisition of information

After 20172013/2017

• Guará Pilot

2008/2013

• Appraisal wells • Accelerated innovation • Lula NE Pilot

• Guará N

• Cernambi S

• Extended well tests

• Lula Pilot• Intensive use of new technologies specifically developed for pre‐salt conditions

• 8 definitive production systems (replicant)

• 4 production units in the Transfer of Rights area

Operating (only 4years after discovery)

Hulls already contracted (conversion in the Inhaúma shipyard)

45

Under construction (hulls being built in the Rio Grande shipyard) +

topsides under bid

SANTOS BASIN PRE‐SALT UPDATEDrilling campaign continues to accelerate

High exploration success ratio continues

High productivity in producing wells

C t d ti f 91 000 b d Current production of 91,000 bpdin 3 wells.

‘EWTLula NE

EWTCarioca NE

34 ll d ill d till O t/2011 (27

Lula Pilot

34 wells drilled till Oct/2011 (27exploratory wells)

10 drilling rigs operating in Santos Basin,from a total of 23 rigs that operates in ultradeep water.

4646

Expectation to double the number of rigsoperating in the Santos Pre‐salt by end of2012.

Wells undergoing drilling, completion or appraisal

CAPITAL COSTS: PRE‐SALT VS. CAMPOS Similar equipment and processes: Principal difference is drilling and completion

PrePre--salt salt CAPEX DISTRIBUTIONCAPEX DISTRIBUTION

20%27%

53%

Gathering Completion + Drilling Units

Deepwater Projects in Campos Basin*Deepwater Projects in Campos Basin*CAPEX DISTRIBUTIONCAPEX DISTRIBUTION

Gathering Completion Drilling Units

33.3%33.3%o Additional drilling and completion cost

in the pre-salt compared with an

33.3%

in the pre salt compared with angeneric deepwater project in Camposbasin can be partially or fully offset byhigher quality and quantity of oil that isexpected in the pre-salt area.

47

Gathering Completion + Drilling Units

* Generic example, considering that these rates can change among the different existing projects in Campos Basin

expected in the pre salt area.

PRE‐SALT RESULTSReduced drilling time and exceptional reservoir behavior lead to growing optimism

Constant production

Results obtained during EWTsAverage drilling time of the wells completed during the year

(versus combined average time for 2006/7)

Constant production

Restriction due to gas burning limitation

Good behavior of the reservoirs

5 wells

4 wells

Good lateral communication

No issues regarding flow guarantee

5 wells

6 wells

EWT Schedule

41

4

1

34

35 5

48

2011 2012 2013 2014 2015

TLD ‐ Pré‐Sal e Cessão Onerosa TLD ‐ Outras áreasEWT – Pre-Salt and Transfer of Rights

EWT – Other areas

SANTOS PRE‐SALT ECONOMICSIncreasing knowledge lowers expected investment, increasing NPV for Master Plan

200%

‐45%

100%

150%nvestm

ent

‐32%

100%81%

55%

0%

50%

PLANSAL 2008 (2008‐2030) PLANSAL 2009 (2008‐2030) PLANSAL 2010 (2008‐2030)

In

200%

152%

100%

150%

esen

t Va

lue

100%118%

152%

0%

50%

PLANSAL 2008 (2008‐2030) PLANSAL 2009 (2008‐2030) PLANSAL 2010 (2008‐2030)

Net Pre

49

PLANSAL 2008 (2008 2030) PLANSAL 2009 (2008 2030) PLANSAL 2010 (2008 2030)

NATURAL GAS FLOW

50

DECLARATION OF COMMERCIALITY Deadlines for the declaration of commerciality influences development plans

2012 2013 2014 201620152011

BM‐S‐8 Bem‐Te‐Vi(12/31/2012)

G ará

Parati(04/12/2012)

Carioca(12/31/2013)

BM‐S‐9

BM‐S‐10

Guará(12/29/2011)

(04/12/2012)BM S 10

BM‐S‐11 Iara(12/31/2013)

BM‐S‐21 Caramba(04/30/2015)

BM‐S‐24 Júpiter(02/28/2016)

51

TRANSFER OF RIGHTS5 billion BOE in contiguous and adjacent areas, adding scale and repeatability

Transfer of Righs Aquisition

Volume 5,0 billion boeVolume 5,0 billion boe

Concession Area

3,865 km2 in 7 blocks

Average Price US$ 8,51 / boe

Initial Value US$ 42.5 billion / R$ 74.8 billion

Duration40 years, extendable for additional 5 years. 4 year

exploration periodexploration period

D&M Assumptions for Franco:*

110,000

Forecast ‐ Accumulated Cash Flow from Franco’s field (2C)(US$ MM)

• 2C Contingent Resource

• Total Potential Oil and Condensate Quantities:

1,632 MM boe

D&M Assumptions for Franco:

70,000

90,000

, (US$ MM)

• Total Potential Sales‐Gas Quantities:

1,664 Bn ft3

• Brent Price: US$ 79.23 bbl

$ 310,000

30,000

50,000

Beginning of Production

Positive Cash Flow

52

• Gas Price: US$ 4.27 thousand ft3

• 3 FPSOs, with 150 thousand BOPD processing capacity

(10,000) tt+

2t+

4t+

6t+

8t+

10t+

12t+

14t+

16t+

18t+

20t+

22t+

24t+

26t+

28t+

30t+

32

* Nominal values

TRANSFER OF RIGHTS Development of the areas fully under way

Declaration of Commerciality

Exploration Production

Development

Duration: 4 yearsExtendable for 2 more years

Variable, according to Development PlanExtendable for 2 more years Development Plan

Total Duration: 40 years, extendable for 5 more years according to specific criteria

Area 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Franco

l di

Resources already available for: First 4lara surroundings

Florim

NE f T i

for:

• 7 Exploratory wells• 1 contingent Exploratory well

First 4

production

units

undergoing

New technologies and definition of

NE of Tupi

South of Guará

S th f T i

well• 1 EWT• 2 contingent EWTs• 3D Seismic

undergoing

contracting

(*)

resource allocation

53

South of Tupi

* Conversion at the Inhaúma shipyard

D illi RiDrilling Rigs,Critical Resources and

Local Content

54

OFFSHORE CAPACITY GROWTH WILL KEEP STRONG Brazil is the main country to contribute with the increase in DW and UDW

Net Changes in Non‐OPEC Productive Capacity Non OPEC Major Capacity Outlook* Between Now and 2030 for Non‐OPEC Countries

Extra‐Heavy Oil

Non‐OPEC Major Capacity Outlook*r d

ay

y

UDW (>750 m)October 2010 Outlook

on barrels per

barrels pe

r da

Onshore

Shelf (< 200 m)Milli

Million

Deepwater Productive Capacity(% f Gl b l Li id C it )

2011 2012 20152014 20162013* Does not include NGLs, CTL/GTL, biofuels, or shale oil projects

7%

9% 8%

per day

(% of Global Liquids Capacity)

Others

3%

6%

Million barrels

Angola

Nigeria

Brazil

552004 2009 2015 2020 2030

M

United States (Gulf of Mexico)

Source: IHS CERA

TECHNOLOGICAL LEADERSHIPIntegration with suppliers, research centers and other oil companies

International Research Centers

Other operators

Suppliers

Brazilian Universities Brazilian Universities and Research Centersand Research Centers

Expenditures (investments and funding): US$1.3 billion / year

• Four R&D centers of Petrobras’ suppliers under construction;• In order to meet local content requirements, several companies will develop technological centers

56

in the country.

NEW VESSELS AND EQUIPMENTSResources required for production growth

Critical Resources Current Situation(Dec/10)

Delivery Plan (to be contracted)Accumulated Value

By 2013 By 2015 By 2020

Drilling Rigs Water Depth Above 2 000 m 15 39 37 (1) 65 (2)Drilling Rigs Water Depth Above 2.000 m 15 39 37 (1) 65 (2)

Supply and Special Vessel 287 423 479 568

Production Platforms SS e FPSO 44 54 61 94Production Platforms SS e FPSO 44 54 61 94

Others (Jacket and TLWP) 78 80 81 83

Production

Platform (FPSO)Drilling RigsSupply Vessel

Platform (FPSO)pp y

Water Depth 2006 2008 2010 2011 2012 2013

DRILLING RIGS UNDER CONTRACT

Water Depth 2006 2008 2010

Up to 1,000 meters 6 11 11

1,000 to 2,000 meters 19 19 21

Over 2 000 meters 2 3 15

2011 2012 2013

+2 +1 +1

+10 +13 +1

57

(1) Two rigs reallocated from international operations, expire in 2015, so it is not considered in the 2020 accumulated value

(2) The demand for long‐term will be adjusted as new demand assessments are made.

Over 2,000 meters 2 3 15 +10 +13 +1

Minimum and maximum limits by block:

LOCAL CONTENTFlexibility in concession agreements

Rounds 7, 9 and 10

Rounds 1 Maximum limit50% i th l t h

No local content required Round 0Minimum and maximum limits by block:

In deep water, between 37% and 55% in the exploration phase, and between 55% and 65% in

the production development phase.

Minimum exploration limit: 37%

Rounds 5 and 6

Minimum limit by blockBetween 30% and 70% in the exploration and

to 450% in the exploratory phase

70% in the production development phaseTransfer of Rights

Concession

pMinimum production development limit:

• Up to 2016: 55%• 2017‐2018: 58%• After 2019: 65%

and 6 production development phases

2011 2012 2013 2014 2015

2011‐2015 Projects

Marlim SulSS P-56

Baleia AzulFPSO

Roncador Papa-Terra

Guará NorteFPSO Cid. de Ilhabela

Parque das BaleiasFPSO P-58

ESP/MARIMBÁ

Guará PilotoFPSO Cid. São Paulo

Lula NEFPSO Cid. de Paraty

Cernambi SulFPSO Cid. de Mangaratiba

Lula Central FPSO P-67

Lula Alto FPSO P-66

BALEIA AZUL

Roncador FPSO P-62

Roncador SS P-55

Papa-Terra P-61 & FPSO P-63

Tiro/SidonFPSO Cid. de Itajaí

ESP/MARIMBÁFPSO

Aruana

MarombaFPSO

SIRI2 jacket and FPSO

Franco 1

BALEIA AZULFPSO

FPSO P-62 FPSO P-74

Lower local content requirements in the ANP’s initial concession rounds give local industry time to adapt.

Concession and Transfer of Rights agreements permit waivers from local content requirements when terms are

58

Concession and Transfer of Rights agreements permit waivers from local content requirements when terms are uncompetive relative to international metrics (e.g. price, deadline, technologies).

DEVELOPMENT OF NATIONAL INDUSTRYDetailing of needs into critical categories permits long‐term strategy

CATEGORYNATIONAL MARKET

AVAILABILITYFPSO cost

AVAILABILITY 1 Process equipment ▲▲2 Turbomachinery ▲▲▲3 Mechanical equipment ▲4 Electrical equipment ▲▲5 Instrumentation/automation ▲5 Instrumentation/automation ▲6 Ship structure and systems ▲▲▲7 Pipeline and valves ▲8 Security 9 Telecommunications10 Ventilation and AC (VAC)

▲Proportional

▲10 Ventilation and AC (VAC)11 Engineering services 12 Architecture 13 Commissioning services

share of FPSO cost

59

Extensive experience of contracting FPSOs combined with operational scale and equipment standardizationwill help create an internationally competitive offshore industry.

PLATFORM CONSTRUCTIONJoint ventures with foreign shipbuilders creating additional shipyard capacity

l b l l f

Under Construction: P‐55: Estaleiro Atlântico Sul – PE (hull) /QUIP‐ RS (modules)

Recently built platform:P‐57: BrasFels – RJ

Capacity: 180 thous. boe/day Value: US$ 1.2 billion Delivered two months ahead of scheduleDelivered two months ahead of schedule

P‐61: Brasfels (RJ)P‐62: Jurong (ES)

Under Construction:

P‐56: Brasfels (RJ)

gP‐74: Inhaúma (RJ)FPSO Cidade de Paraty: Brasfels (RJ) ‐modules and integrationFPSO Cidade de São Paulo: Brasfels (RJ) ‐modules and integration

Under Construction:

8 FPSOs (Pre‐salt ‐ P‐66; P‐67; P‐68; P‐69; P‐70; P‐71; P‐72; P‐73 ): Ecovix – Rio Grande (RS)P‐63: QUIP (RS)Under Construction:

P‐58: Estaleiro Rio Grande –RS , UTC Engenharia S/A – RJ e EBE – RJ.

o 2 Jack-ups under construction (P-59 and P-60) in São Roque (BA)o Inclusion of 900 new suppliers per year in Petrobras' Corporate Vendor List; o 13 new shipyards currently under construction raising the total number to 50*;

60

o 13 new shipyards currently under construction, raising the total number to 50*;

*Source: Sinaval – Executive Summary -2011, Jan.

LOCAL CONTENT ACHIEVEMENTSHigh level of local content already in place

Roncador development P 54 M li S l d l t P 56Roncador development P‐5468% local content

Marlim Sul development P‐56 73% local content

Jubarte development P‐57 65% Local Content

61

HUMAN RESOURCESIntensive training programs created to meet Business Plan demands

2010 2011 2012 2013 2014 2015 2016200920082007

Business plan 2008 - 201228 Probes146 Support boats146 Support boatsNew production platformsPromef II19 charter vesselsPremium I RefinaryPremium II RefineryPremium II RefineryReplanning Comperj and RNESTNew projects

212.638HR Demand

78.402Already been qualified

(R$ 554 million)PN 2010‐14

Already been qualified(R$ 228 million)

62

HUMAN RESOURCES REQUIREMENTSWorkers with elementary and high school education most needed

PROFESSIONALS REQUIRED FOR O&G PORTFOLIO IMPLEMENTATION

189189 PROFESSIONALS CATEGORIES189189 PROFESSIONALS CATEGORIES

212.638 Qualified professionals212.638 Qualified professionals

ENGINEERINGENGINEERING41414141

4%4%8.6748.674

CONSTRUCTION & ASSEMBLYCONSTRUCTION & ASSEMBLY

90909090

79%79%168 197168 197

CIVIL CONSTRUCTIONCIVIL CONSTRUCTION

7777

9%9%20.20020.200

OPERATIONS MAINTENAINCEOPERATIONS MAINTENAINCE

51515151

7%7%15 56715 567168.197168.197

HIGH SCHOOLHIGH SCHOOL14141414

44%44%3 8063 806 27272727

BASICBASIC21212121

71%71%118.654118.654BASICBASIC

7777

100%100%20 20020 200

15.56715.567

BASICBASIC12121212

25%25%3 9093 9093.8063.806

HIGH SCHOOLHIGH SCHOOL27272727

21%21%34.82734.827

20.20020.200 3.9093.909

HIGH SCHOOLHIGH SCHOOL19191919

49%49%7.6907.690TECHNICIANTECHNICIAN

2222

1%1%

TECHNICIAN TECHNICIAN 3333

11%11%988988

GRADUATEGRADUATE24242424

45%45%3.8803.880

1%1%2.1032.103

TECHNICIANTECHNICIAN1111

22%22%3.3933.393

INSPECTORSINSPECTORS21212121

3%3%5.0605.060

63

GRADUATEGRADUATE19191919

7.5537.5534%4%

GRADUATEGRADUATE11111111

4%4%575575

fi i i &Refining, Transportation & Marketing (RTM), d h i land Petrochemicals

64

DOWNSTREAM STRATEGYExpansion, quality, logistics and marketing

Expand the downstream, ensuring domestic supply and distribution leadership, developing markets for the oil surplus produced in Brazil

2011‐15 Business Plan Highlights:

• Downstream capacity will increase by 395 thousand bpd between 2011‐15 and 1,065 thousand bpd between 2016‐2020;

• Completion of the process to modernize the downstream segment;

• Logistics integrated with E&P activities to ensure the commercialization of the oil surplus;

• Increase petrochemicals and biopolymers production.

65

INVESTMENTSNew refineries, fuel quality and modernization responsible for 75% of spending

• Refining Capacity Expansion: Abreu e Lima

US$70.6 billion

Logistics for Oil InternationalRefinery, Premium I and II, and Comperj;

• Quality and Conversion: Modernization, conversion and hydrodesulfurization;6,2%

4,9%1,0%

Fleet Expansion

Logistics for Oil International

conversion, and hydrodesulfurization;

• Operating improvement: maintenance and optimization, HSEE, and R&D;

50 1%

13,9%Refining Capacity

Expansion

Operating Improvement

• Fleet Expansion

• Logistics for Oil: oil supply for refineries and

50,1%

23,9%

Quality and Conversion

Logistics for Oil: oil supply for refineries and infrastructure for oil exports.

Petrochemical Investments amount to US$3.8 billion

66

TRANSPORT MATRIX

MIDDLE DISTILLATE DEMAND EVOLUTIONExpectations of strong middle distillate growth

GDP and AGRICULTURE GDP IN BRAZIL

81%

46% 11%

11%8%

43%Canada

Russia

TRANSPORT MATRIXThe Brazilian transportation matrix strongly depends on trucks

150

160

170

180

+52%

GDP and AGRICULTURE GDP IN BRAZIL

46%

43%

43% 25%

11%

32%USA

53% 4%

43%

Australia

Canada

120

130140

150

37%

25%

13%

17%

50%

Brazil

China

58%90

100

110

Q10

Q09

Q08

Q07

Q06

Q05

Q04

Q03

Q02

Q01

Q00

Agriculture GDPGDP

Trucks Maritime and OthersTrains

10 000

Number of passengers carried ‐ Air Transportation in Brazil (thousand)

JET FUEL MARKETDIESEL AND JET SALES

11111111111

8.000

9.000

10.000

+12%a.a.

+4,5% p.y.

+9%

+17%

5 000

6.000

7.000

2006 2007 2008 2009 2010 9M11

67

4.000

5.000

jan 10jan 09jan 08jan 07 jan 12jan 11

2006 2007 2008 2009 2010 9M11Diesel Jet Fuel

The 9M11 sales exceeded expected growth, keeping a faster‐than‐GDP growth

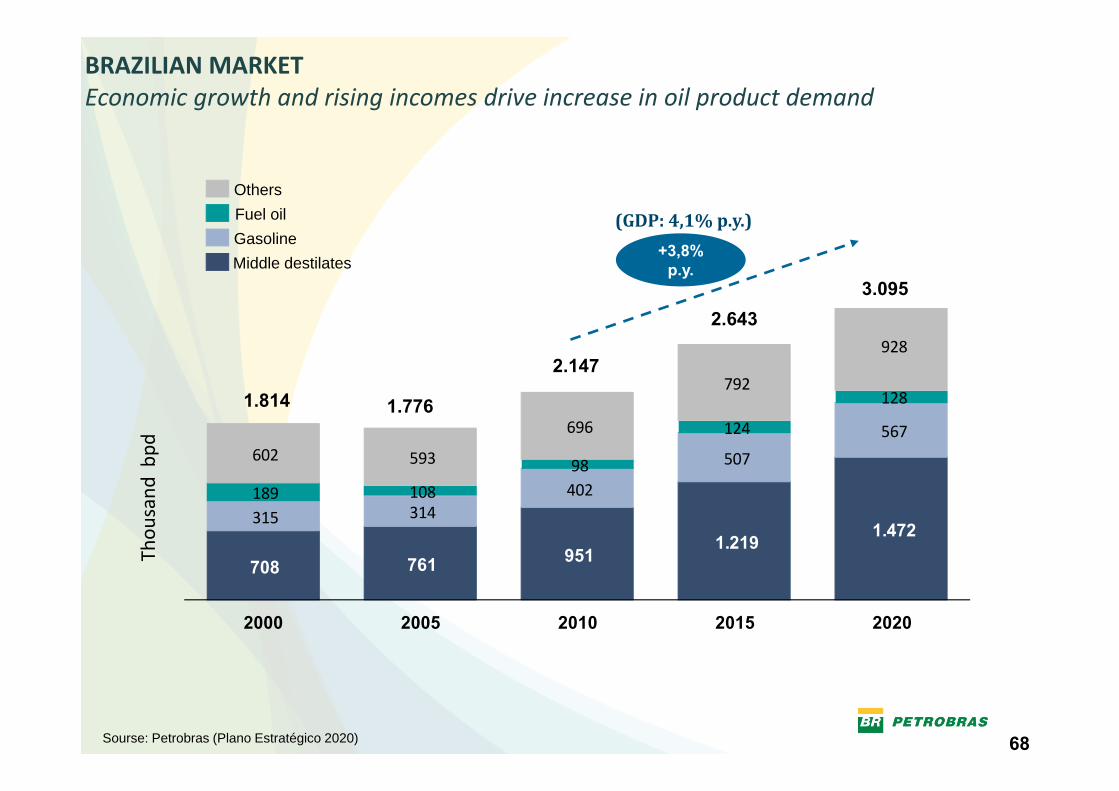

BRAZILIAN MARKETEconomic growth and rising incomes drive increase in oil product demand

(GDP 4 1% )

OthersFuel oil

3.095

+3,8% p.y.

(GDP: 4,1% p.y.)Fuel oilGasolineMiddle destilates

128792

9282.147

2.643

1 814

402

507

567

98

124

128

602 593

696

dbp

d

1.814 1.776

708 761 9511.219 1.472

315 314402189 108

Thou

sand

2000 2005 2010 2015 2020

68Sourse: Petrobras (Plano Estratégico 2020)

INTEGRATION AND BALANCEConstruction of new refineries intended to meet Brazilian demand

5000

PREMIUM I(2nd phase)300,000 bpd

(2019)

Thous bpd4,910

3000

4000 COMPERJ(2nd phase)165,000 bpd

(2018)

2,643 3,095

3,3273,2173,070

2000

Abreu e Lima

COMPERJ(1st phase)165,000 bpd

(2013)

PREMIUM I

PREMIUM II300,000 bpd

(2017)

2,536

1,641

2,2052,004

1,3931,798

1,036

2,1471,814

1,323

0

1000

1980 2000 2010 2015 2020

Abreu e LimaRefinery (RNE)230,000 bpd

(2012)

PREMIUM I(1st phase)300,000 bpd

(2016)181

... ... ... ...1980 2000 2010 2015 2020

Oil and NGL Production ‐ Brazil Total crude oil processed – Brazil Oil Products Market (2 scenarios)

• No new refineries built since 1980• Demand now exceeds refining capacity, with demand growing 20% last two years and growing

69

DOWNSTREAM EXPANSIONNew refineries needed to avoid excessive dependence on product imports

Net Imports as a percentage of total demand (%)*Net Product Imports (’000 bpd)

2006 2007 2008 2011E2009 2010

Brazil (2010)USA

ChinaGermany

FranceBrazil (2010)

IndonesiaMexico

SpainJapan

Brazil (2020)**Indonesia

* S IEA 2010 W ld E St ti ti

• Increasing imports will lead to higher logistical costs and increasing exposure to availability of international supplies

70

* Source: IEA – 2010 World Energy Statistica** Without considering Capacity Expansion

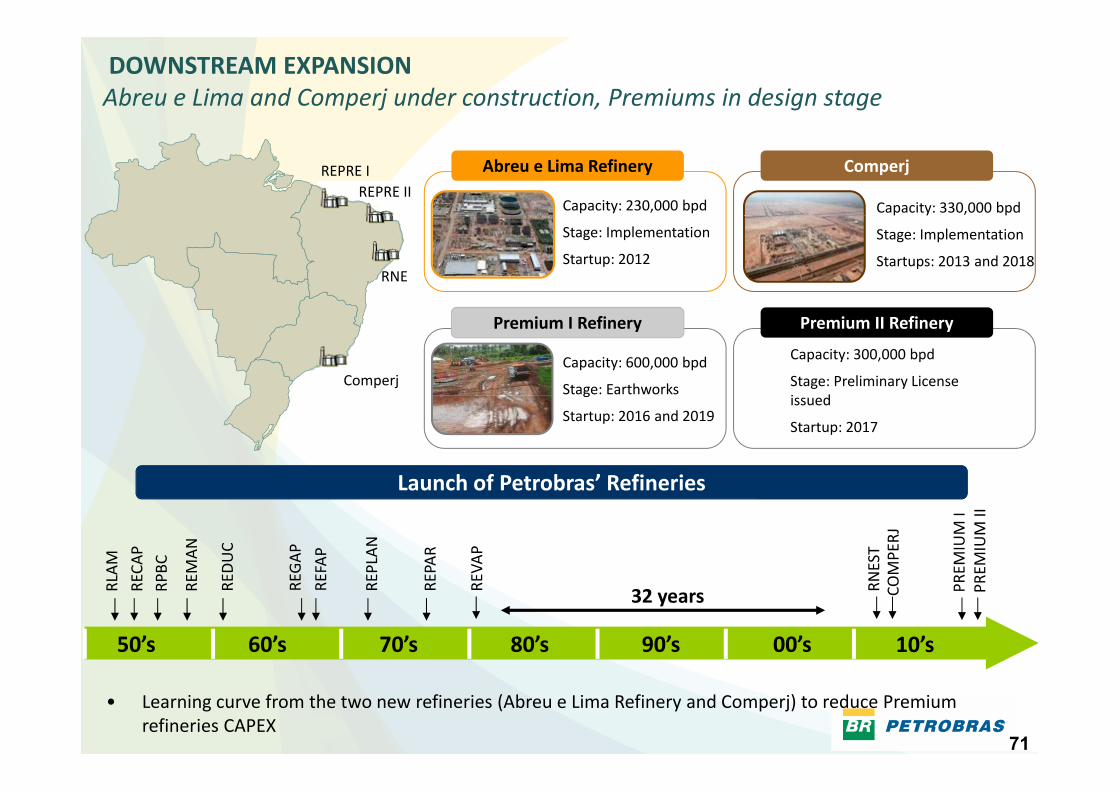

DOWNSTREAM EXPANSIONAbreu e Lima and Comperj under construction, Premiums in design stage

Capacity: 230,000 bpd

REPRE I Abreu e Lima Refinery

Capacity: 330,000 bpdREPRE II

Comperj

Stage: Implementation

Startup: 2012

Stage: Implementation

Startups: 2013 and 2018RNE

Comperj

Capacity: 300,000 bpd

Stage: Preliminary License i d

Capacity: 600,000 bpd

Stage: Earthworks

Premium I Refinery Premium II Refinery

issued

Startup: 2017

g

Startup: 2016 and 2019

Launch of Petrobras’ Refineries

LAM

ECAP

PBC

EMAN

EDUC

EGAP

EFAP

EPLAN

EPAR

EVAP

NEST

MPERJ

Launch of Petrobras Refineries

REMIUM I

EMIUM II

60’s50’s 70’s 80’s 90’s 00’s

RL RE RP RE RE RE RE RE RE RE RN CO

10’s

32 years PR PR

71

• Learning curve from the two new refineries (Abreu e Lima Refinery and Comperj) to reduce Premium refineries CAPEX

LOGISTICSDistances have relevant freight costs to reach the different markets

Freight cost ($/bbl)

2 8

2 8

2,8

4,9 5,4

2,87,7

4,1,

Processing in Brazil implies:• Lower Lead-Times• Reduced Tankage needs

L I t i

72

CrudeProducts

• Lower Inventories• Reduced need for ships

CONVERSIONNew refineries will have significant higher conversion than existing refineries , allowing l t f t i lless costs of raw material

7064%

68%65% (US$/bbl)

Average Cost of Oil (2020)Convertion Capacity/ Destilation Capacity

FCCCoker

31% 26%

40

50

60

37%

‐5,8

‐2,3

HCCFCC

10% 65%

27%10

20

30

38%36%

PREMIUMExistentBrent0

PREMIUMExistent Refineries

Brent

PREMIUMCOMPERJRNEExisting Refineries(2010)

73

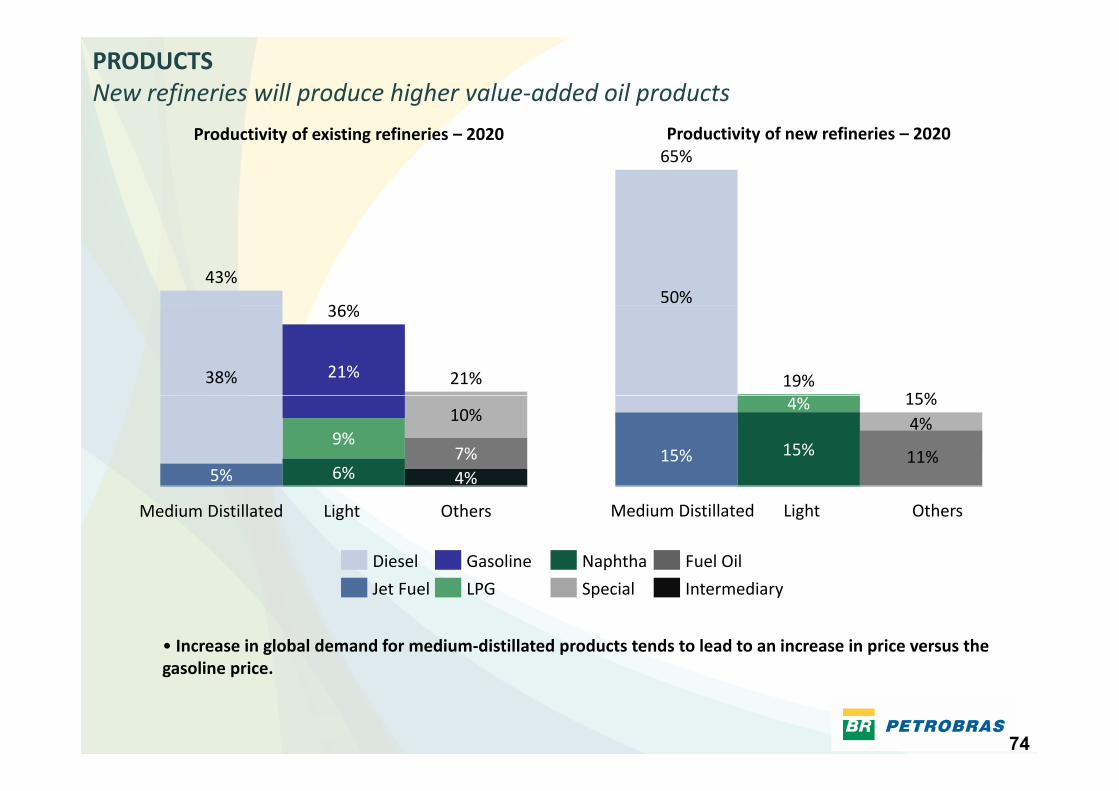

PRODUCTSNew refineries will produce higher value‐added oil products

65%Productivity of existing refineries – 2020 Productivity of new refineries – 2020

36%

43%50%

21%

36%

21%38% 19%15%

4%7%

10%

6%

9%

5%

4%

15%4%

11%

15%

15%

LightMedium Distillated Others

Fuel OilNaphthaGasolineDiesel

LightMedium Distillated Others

SpecialLPGJet Fuel Intermediary

• Increase in global demand for medium‐distillated products tends to lead to an increase in price versus the li i

74

gasoline price.

PREMIUM REFINERIESFuture refineries designed to optimize scale and resources

Lower refining costs due to design quality and scale

Economies of scale and new implementation strategies to reduce Capex, including:

• Design competition based on the lowest final cost

• Selection of UOP ‐ international company with extensive refining experience Age (years)

Current downstream cost(US$ / bbl in 2010)

refining experience

• Single design integrating all the refinery on‐site and off‐site

• Designer involved from conceptual design to technical assistance in the start up

• Scale economies (RPRE: 300kbpd modules)

Ma im m standardi ation of eq ipments specification• Maximum standardization of equipments specification

• Scheduling the construction stage allowing long‐term planning for equipment suppliers

• Reuse of the executive project allowing the incorporation of lessons learned Scale (’000 bpd)

75

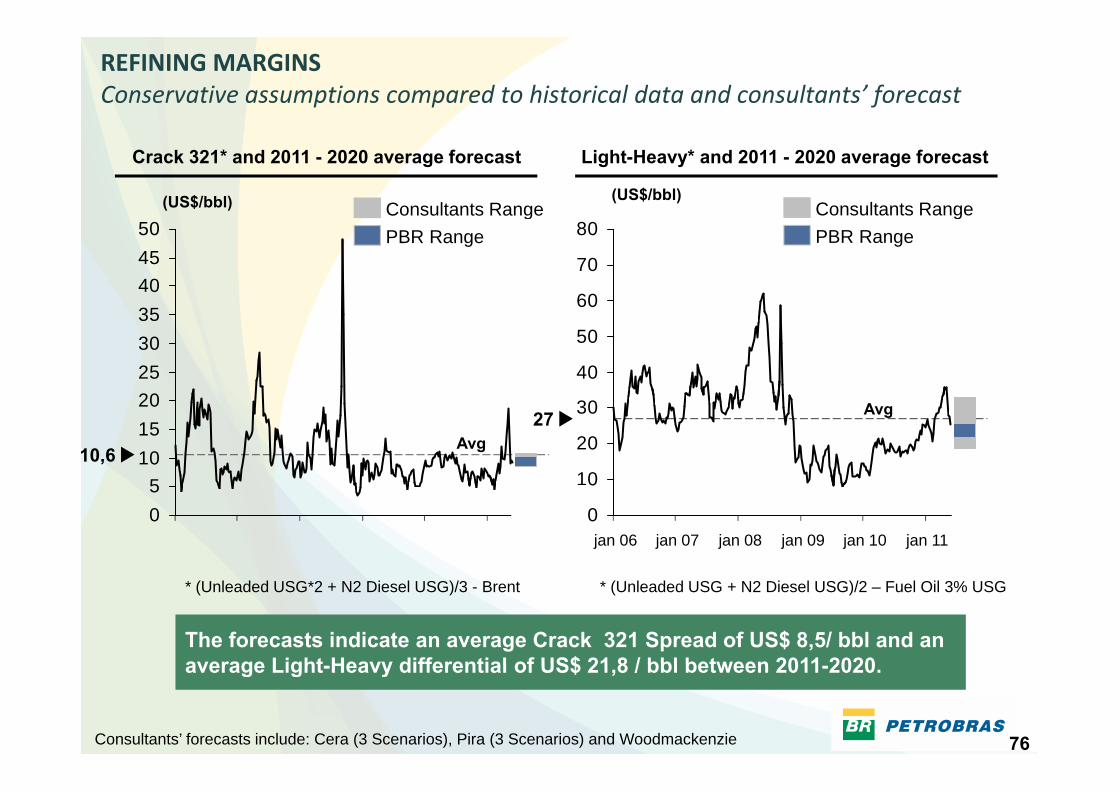

REFINING MARGINSConservative assumptions compared to historical data and consultants’ forecast

Crack 321* and 2011 - 2020 average forecast

Consultants Range(US$/bbl)

Light-Heavy* and 2011 - 2020 average forecast

(US$/bbl)Consultants Range

404550 50

45PBR Range

g

60

70

80 PBR Rangeg

20253035

40

50

60

5101520

10,6 Avg

Avg

10

20

3027

05

0

0

jan 12jan 11jan 10jan 09jan 08jan 07jan 06

The forecasts indicate an average Crack 321 Spread of US$ 8,5/ bbl and an average Light Heavy differential of US$ 21 8 / bbl between 2011 2020

* (Unleaded USG + N2 Diesel USG)/2 – Fuel Oil 3% USG* (Unleaded USG*2 + N2 Diesel USG)/3 - Brent

76

average Light-Heavy differential of US$ 21,8 / bbl between 2011-2020.

Consultants’ forecasts include: Cera (3 Scenarios), Pira (3 Scenarios) and Woodmackenzie

PROFITABILITYNew refining projects have return rate above the cost of capital

Return rate (%)

Key Assumptions:18

• Refinery with trains of 300 k bpd

• Refining scheme with HCC, Coque and HDT12

14

16

•Refining costs in line with the current refineries that has the same scale

• Integrated Analysis

P d ti f th d ti k t6

8

10

• Production for the domestic market

• Does not include tax benefits in the operation of the asset

0

2

4

6

Case 1 – Capex US$ 30.000/bpd

C 2 C S$ 0 000/b d

Margin

US$/bbl

013 14 15 16 17 18 19 20 21 22 23

Case 3 ‐ Capex US$ 50.000/bpd

Case 2 – Capex US$ 40.000/bpd Expected Scenario

77

HYDROREFINING INVESTMENTSCatch up phase to meet international standards for quality products

95%100

Hydrorefining Capacity relative to Distillation Capacity

70%

95%

69%70%67%

86%

80

100

74% (2020)67%

15%60

59% (2015)

36%

20

40

23% (current)

0

23%

Adding value to domestic crude oil by producing diesel and gasoline in‐line with international standards.

78

Underinvested over the past years requires catching up with hydrorefining capacity (for removal of sulfur)

INVESTMENTS IN QUALITYInvestment cycle in modernization and quality has peaked

US$16 billion in 2011‐15 Reduction in sulfur level

US$ 16 billion

5.9

7.0

4.94.5 Avg. Sulfur Level – Diesel (ppm)

3.2

2.3

1.01.01.1

0.20.1

<250

15141312111098765

• After 2013 investment can be focused principally on expansion alone

79

• After 2013 investment can be focused principally on expansion alone

SUPPORTTING UPSTREAM OPERATIONSLogistics support represent 11% of Capex

Capex for Fleet Expansion Capex for Logistics for Oil

US$ 3,5 billionUS$ 4,4 billion

Capex for Fleet Expansion Capex for Logistics for Oil

Pre‐SaltProjects

21%

Plangás

30%Others

51%

30%

28%

Supply

70%

OilOil

80

PETROCHEMICALS

OWNERSHIP STRUCTURETotal ON

Braskem

Nominal Capacity by Petrochemical TypeTotal ON

36,1% 47,0% PETROBRAS38,2% 50,1% ODEBRECHT25,7% 2,9% OthersAlagoas

(mmt/y)Ethylene 3.77Propylene 1.59Polyethylene 3.06

l l 2 88

yp

The Largest Thermoplastic Resins Producer in the Americas

BahiaPolypropylene 2.88PVC 0.51Cumene 0.32

• Production Capacity: 15 million metric tons of thermoplasticresins and other chemical products• 31 industrial units: 28 in Brazil and 3 in the US• 400 patents in Brazil, the US and EuropeW ld l d i h fi ld f bi l b f G PE

São Paulo

Rio de Janeiro

• World leader in the field of biopolymers because of Green PE,first produced on a commercial scale in September 2010

Rio Grande do Sul

Petrobras has also 3 new petrochemicals projects under construction:• Complexo Petroquímico do Rio de Janeiro: petrochemicals complex to be integrated with the Comperj refinery to produce materials for the plastics industry;• Petroquímica Suape Complex in Pernambuco: to produce purified terephthalic acid (PTA), polyethylene terephthalate

81

(PET) resin, and polymer and polyester filament textiles• Companhia de Coque Calcinado de Petróleo—Coquepar: calcined petroleum coke plants in Rio de Janeiro and Paraná

BIOFUELSBIOFUELS

82

2011‐2015 INVESTMENTS

INVESTMENTS IN BIOFUELSFocus to increase the ethanol supply in Brazil

2011 2015 INVESTMENTS US$ 4.1 billion

Ethanol

7%

14% 0 3 Ethanol

Ethanol Logistics

Biodiesel47%

14%

1.90.6

0.3

R&D

32%

1.3

5.6

Market Share Pbio+Partners:• 2011: 28%

Biodiesel supply (’000 m³)Ethanol supply (million m³)

Market‐share Pbio+Partners:• 2011: 5.3%2015 12%

273%

16%

735

855

• 2015: 26%• 2015: 12%

1.5

2011 20152011 2015

83

Pbio + Partners Pbio + Partners

Natural Gas, Electric Energy and Fertilizers

84

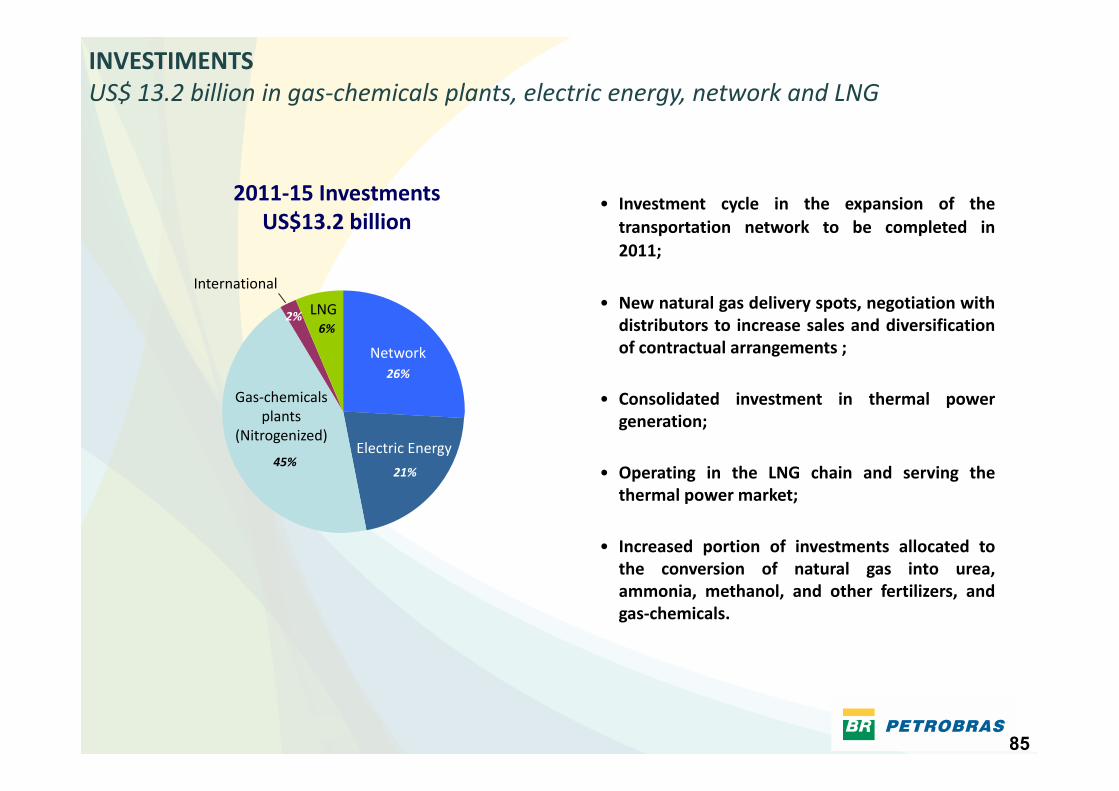

INVESTIMENTSUS$ 13.2 billion in gas‐chemicals plants, electric energy, network and LNG

• Investment cycle in the expansion of the2011‐15 InvestmentsUS$13 2 billi

International

LNG

transportation network to be completed in2011;

• New natural gas delivery spots negotiation with

US$13.2 billion

0,30,8

26%

2%6%

Network

Gas chemicals

LNG New natural gas delivery spots, negotiation withdistributors to increase sales and diversificationof contractual arrangements ;

C lid t d i t t i th l5,9

21%45%

Electric Energy

Gas‐chemicalsplants

(Nitrogenized)

• Consolidated investment in thermal powergeneration;

• Operating in the LNG chain and serving thethermal power market;

• Increased portion of investments allocated tothe conversion of natural gas into urea,g ,ammonia, methanol, and other fertilizers, andgas‐chemicals.

85

1ST INVESTMENT CYCLENatural gas transportation and processing infrastructure now largely concluded

9.538 9.728

9 000

10.000

Transportation Infraestructure (km)km

5.623 5.6676.098

7.086

7.991

6.000

7.000

8.000

9.000

2 000

3.000

4.000

5.000

0

1.000

2.000

2003 2005 2007 2008 2009 2010 2011

Investments: R$ 29,2 billion

Compressor Stations and Delivery PointsDelivery Points

Compressor Stations

By 2013 2003 to 2011

86

Delivery Points

1st Investment Cycle 2nd Investment Cycle2nd Investment Cycle

2ND INVESTMENT CYCLE:Monetization of the pre‐salt reserves drives future investments

90%

100%UFN III (Sep/14)

LNG Pecém

LNG BGUA

TPP Bicomb Conversion

Cubatão

Sulfato de Amônio (May/13)

Acquisition TPPs

UFN V (Sep/15)

COMPLETED 20112011‐‐2015 BP2015 BP

70%

80%TPP Bicomb. Conversion

TermoaçuSulfato de Amônio (May/13)

ARLA 32 (out/11)

UFN IV (Jun/17)

tal

50%

60%

Regás BahiaGasbel II

Gasduc III

estim

ento

To

30%

40%

Regás Bahia

(Jan/14)

New NG TPPs

Gasene

Pilar-Ipojuca

% d

o In

ve

10%

20% Gastau

Gaspal II

Gasan IIAtalaia-Itaporanga

Cacimbas-Vitória

Catu-Pilar

Japeri-Reduc

Gascav

Gascar UPGN Cabiúnas –Route 2 Pre-Salt

0%

10%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Urucu-Manaus Gasan II

Ecomps + Delivery Spots + Network Maintainance

Route 2 Pre-Salt(Aug/14)

87

Adaptation of the Gas Pipelines Network (US$ 3.34 bi)New TPPs run on Natural Gas (US$ 1.82 bi)LNG regasification (US$ 0.74 bi)Chemical Transformation of NG (US$ 5.85 bi)

TPP Commitments (US$ 0.94 bi)Renewable Energy: Wind Power and Biomass (US$ 0.02 bi)Natural Gas Liquefaction (US$ 0.10 bi)

87

NATURAL GAS SUPPLY & DEMAND (MILLION M3/D) Increasing domestic gas supply and demand flexibility

DEMANDPCS 9.400 kcal/m³ SUPPLY

Thermal Power Plants Demand : Petrobras + Third partiesDomestic NG Supply (Includes third parties)

76(15.1 GW)

599

9 Northern Region

55

78

102

Inflexible

Flexible40

13

3725

To be contracted (5.5 GW(10.7 GW)38(6.7 GW)

4969

936Other Regions

NG Distributors Demand

202020152011

Supply via LNG Regasification Terminals

2011 2015 2020

Non‐thermal power

2011 2015 20202011 2015 2020

Guanabara BayPecém

Bahia41

20

1441

20

1421

14

F tili61

Petrobras’ Demand: Downstream + Fertilizers

2011 2015 20202011 2015 2020

Bolivian Supply

Firm

Flexible30

24

30

24

30

24

202020152011

Downstream

UPGN

Fertilizers

32

1639

2517

2011 2015 2020

88

Total

Demand

Total

Supply173149106 20015196

NATURAL GAS PRICESA policy that allows Bolivian imports and domestic gas to substitute fuel oil

u 182022

S$/M

MBtu

68

1012141618

US

0246

n/08

ar/0

8

ai/0

8

ul/0

8

et/0

8

ov/0

8

n/09

ar/0

9

ai/0

9

ul/0

9

et/0

9

ov/0

9

n/10

ar/1

0

ai/1

0

ul/1

0

et/1

0

ov/1

0

n/11

ar/1

1

ai/1

1

ul/1

1

et/1

1

ov/1

1

ja ma

ma ju se no ja ma

ma ju se no ja ma

ma ju se no ja ma

ma ju se no

Faixa dos Contratos Internacionais GN Brasil: Boliviano GN Brasil: Nova Política

OC Brasil (SE) GN Europa: Contrato GNL Ásia: Contrato (PIRA)Fuel Oil in Brazil (Southeast Region)

Range for International Contracts Brazilian NG: Bolivian

European NG: Contract

Brazilian NG: New Policy

Asia NGL: Contract (PIRA)

• Petrobras has 2 umbrella contracts: the Bolivian and the Brazilian New Policy (domestic gas)

• New Policy indexed to IGPM, while the Bolivian contract linked to Dollar

• Appreciation of the Real from 2009 until August 2011 created a differential between the twosources of natural gas, that is largely now closed.

89

InternationalInternational

90

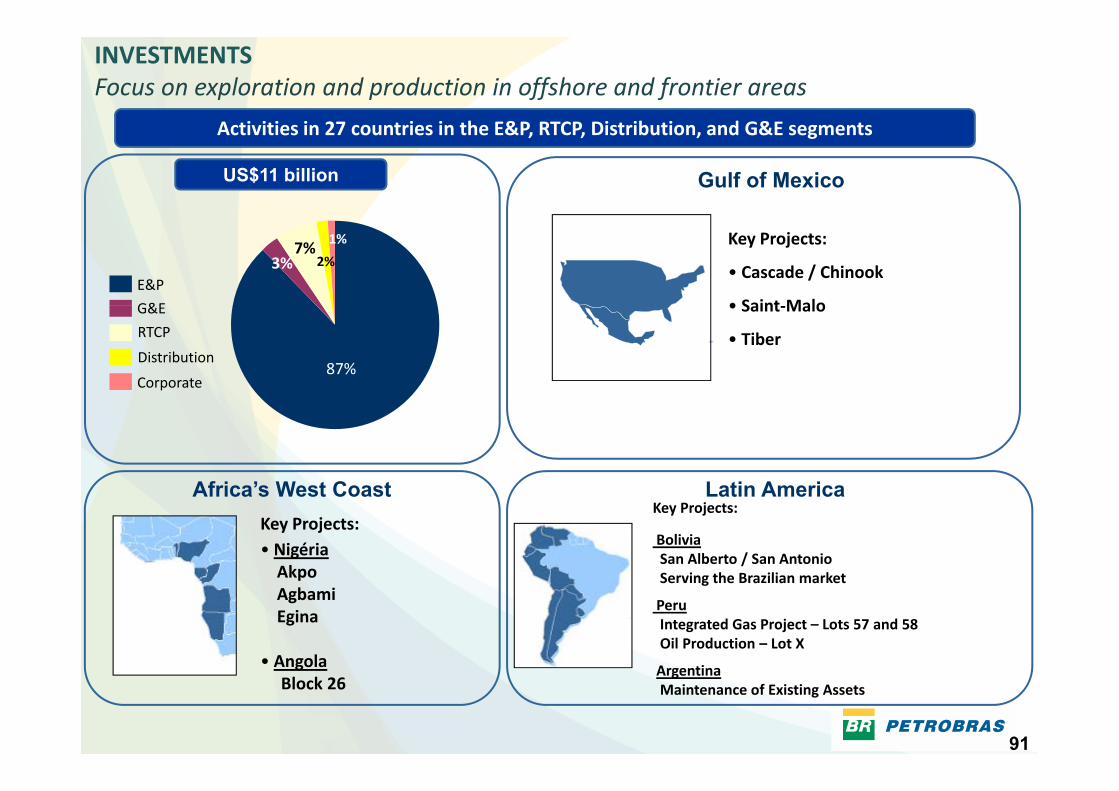

INVESTMENTSFocus on exploration and production in offshore and frontier areas

Activities in 27 countries in the E&P RTCP Distribution and G&E segments

US$11 billion

Activities in 27 countries in the E&P, RTCP, Distribution, and G&E segments

Gulf of Mexico

Key Projects:

• Cascade / Chinook

• Saint MaloG&E

E&P

1%

3% 2%7%

• Saint‐Malo

• Tiber

Corporate

Distribution

G&E

RTCP

87%

Africa’s West Coast Latin AmericaKey Projects:

BoliviaSan Alberto / San Antonio S i th B ili k t

Key Projects: • NigériaAkpo

Africa’s West Coast Latin America

Serving the Brazilian market

PeruIntegrated Gas Project – Lots 57 and 58 Oil Production – Lot X

Akpo AgbamiEgina

• Angola

91

ArgentinaMaintenance of Existing Assets

AngolaBlock 26

CASCADE ‐ CHINOOK DEVELOPMENTFirst oil expected from the ultra deep of GOM in the beginning of 2012

FPSOShuttleTanker

Petrobras America operated fields - Water Depth ~ 2,500 meters

Chinook

FSHR

Control

Gas Export Pipeline

p ,(8,200 feet).

US regulators approved Petrobras plans to bring first FPSO (*) to the US Gulf of Mexico

CascadeT

Control Umbilical Power

Umbilical

Flow line

M if ld

US Gulf of Mexico.

Technologies new to US Gulf of Mexico, including disconnectable turret buoy, allowing the vessel to

TreeManifoldy, g

move offsite during hurricanes, and transportation via shuttle tanker.

(*) FPSO Floating Prod ction Storage and Offloading facilit(*) FPSO – Floating, Production, Storage and Offloading facility.Petrobras has an extensive experience in the use of FPSO with18 units currently under operation offshore Brazil.

92Source: Petrobras America inc

FINANCIAL CONSIDERATIONSCONSIDERATIONS

93

2011‐2015 INVESTMENTSInvestment level similar to the previous Plan, with more focus in E&P

2010‐14 Business Plan

1%1% 2%

2011‐15 Business PlanUS$224.7 billionUS$224 billion

2%2% 1%1% 2%

8%2,9

14,7 3,24,2

2,314,7 3,2

4,22,46%

2% 1%1% 2%

17.8 2.43.52.9

13.2 3.14.1

2.4

53% 65,5

4,1

65,5

4,1

(*)118.873 6

5.1

127.570 6

3.8

33%

,

57%31%73.6 127.570.6

• 5% of investments will be made overseas, 87%

(*) US$22.8 billion in ExplorationE&P RTCE&P

P t h i l

RTM5% of investments will be made overseas, 87%

of which in E&P.

• Note: HSEE (US$ 4.2 bi), IT (US$ 2.7 bi), Technology

Gás,Energia & Gás Química Petroquímica

Distribuição Biocombustíveis

Corporativo

Biofuels

Gas, Energy & Gas Chemicals

Distribution

Corporate

Petrochemicals

94

Note: HSEE (US$ 4.2 bi), IT (US$ 2.7 bi), Technology(US$ 4.6 bi), Logistics (US$ 17.4 bi) and Maintenance &Infrastructure (US$ 20.6 bi)

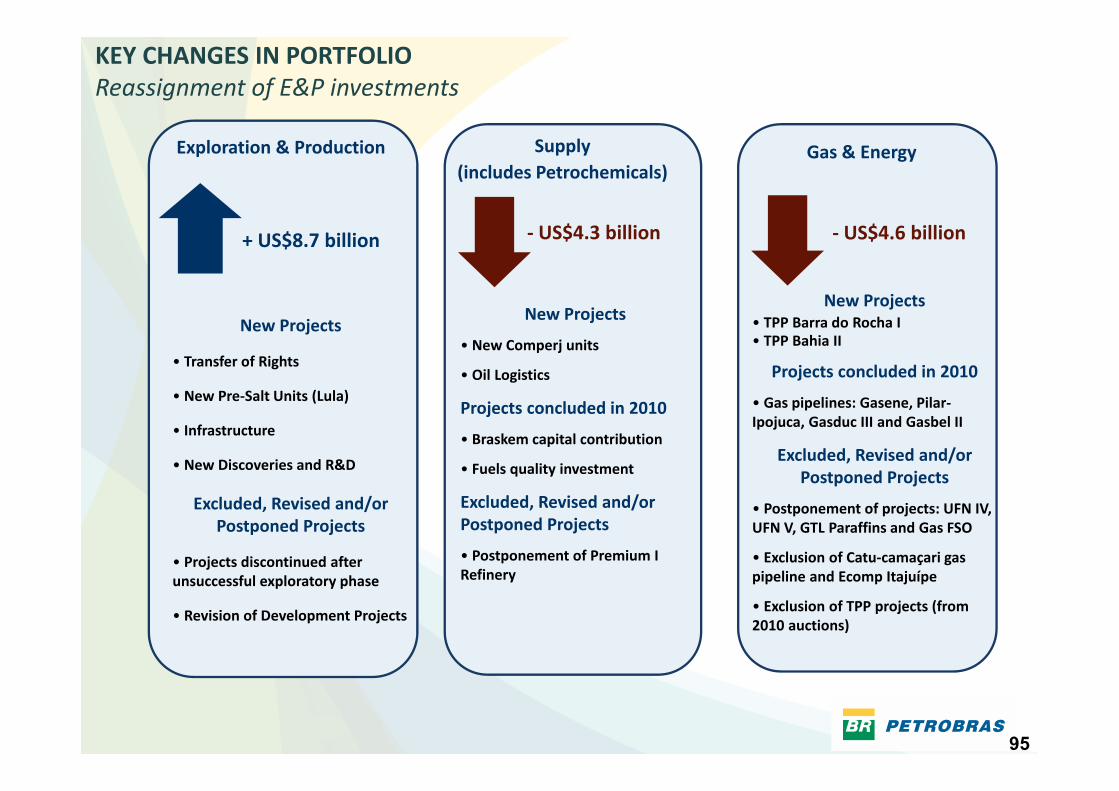

KEY CHANGES IN PORTFOLIOReassignment of E&P investments

Exploration & Production Gas & EnergySupply (includes Petrochemicals)

+ US$8.7 billion ‐ US$4.6 billion‐ US$4.3 billion

New ProjectsNew Projects

• Transfer of Rights

• New Pre Salt Units (Lula)

New Projects• TPP Barra do Rocha I• TPP Bahia II

Projects concluded in 2010

New Projects

• New Comperj units

• Oil Logistics• New Pre‐Salt Units (Lula)

• Infrastructure

• New Discoveries and R&D

• Gas pipelines: Gasene, Pilar‐Ipojuca, Gasduc III and Gasbel II

Excluded, Revised and/or Postponed Projects

Projects concluded in 2010

• Braskem capital contribution

• Fuels quality investment

Excluded, Revised and/or Postponed Projects

• Projects discontinued after f

p j

• Postponement of projects: UFN IV, UFN V, GTL Paraffins and Gas FSO

• Exclusion of Catu‐camaçari gas pipeline and Ecomp Itajuípe

Excluded, Revised and/or Postponed Projects

• Postponement of Premium I Refineryunsuccessful exploratory phase

• Revision of Development Projects

pipeline and Ecomp Itajuípe

• Exclusion of TPP projects (from 2010 auctions)

Refinery

95

KEY VARIABLESOil price assumptions within market expectations

Petrobras’ 95U

S$/b

bl

Scenarios80

Based on 2011‐2012 forecasts: Banks (Source: Bloomberg)

Based on 2013‐2015 forecasts: PIRA, DOE, CERA, WoodMackenzie, IEA

Assumptions

Key variables for Cash Generation and Investment Level• Oil price • Foreign Exchange Rate• Brazilian Market GrowthAssumptions

No Capital Increase in the period

Investment grade maintenance

• Brazilian Market Growth • Average Realization Price (ARP) – Brazil

– International Parity– International margins per product

• Oil and products exports and imports

96

Investment grade maintenance • Oil and products exports and imports• Investment Program • Divestitures and business restructuring• Third‐party funding

CASH GENERATION AND INVESTMENTSDivestment and traditional funding sources adequate for Plan needs

Scenario A Scenario B

31,4 30,926,1 26,1

13,6 13,6

US$ 256.1 US$ 255.6US$ 256.1 US$ 255.6 Key assumptions

Scenario A Scenario B

E h t

91,4 67,0

Exchange rate (R$/US$)

1.73 1,73

2011 – 110 2011 – 110

2012 – 80 2012 – 95

125,0148,9

224,7 224,7 Brent (US$/bbl) 2013 – 80 2013 – 95

2014 – 80 2014 – 95

2015 – 80 2015 – 95,

Leverage (Min. and Max.)

23% ‐ 32% 22 % ‐ 29%

Net Debt/EBITDA (Average)

1.9 1.5Sources Use Sources Use ( g )

ARP (R$/bbl) 158 177Debt AmortizationInvestments

Divestment and RestructuringCashThird‐Party Resources (Debt)O ti C h Fl (Aft Di id d )

Sources Use Sources Use

• 40% of capex in dollar in comparison to 37% in the

97

Operating Cash Flow (After Dividends) Business Plan 2010‐14

CAPEX AND CASH FLOWCash flow supports maintenance plus growth

Assumptions to Maintain Existing Capacities:• $12 per barrel to replace 830MMBBL´s of production

• $1.5 bn. ‐ Exploration • $2.0 bn. ‐ Refinery maintenance•$1.0 bn. ‐ Gas & Power maintenance• $1.5 bn. ‐ Other Maintenance

35 00040.000 45.000 50.000

US$ MM

35,13445,078

33,44745,897

5.000 10.000 15.000 20.000 25.000 30.000 35.000

16,000

,

-

OCF 2011* Capex 2009 Capex 2010 Capex 2011* Maintenance Capex (Est.)

E&P Downstream Gas & Energy Others

98

* LTM as of 6/30/11

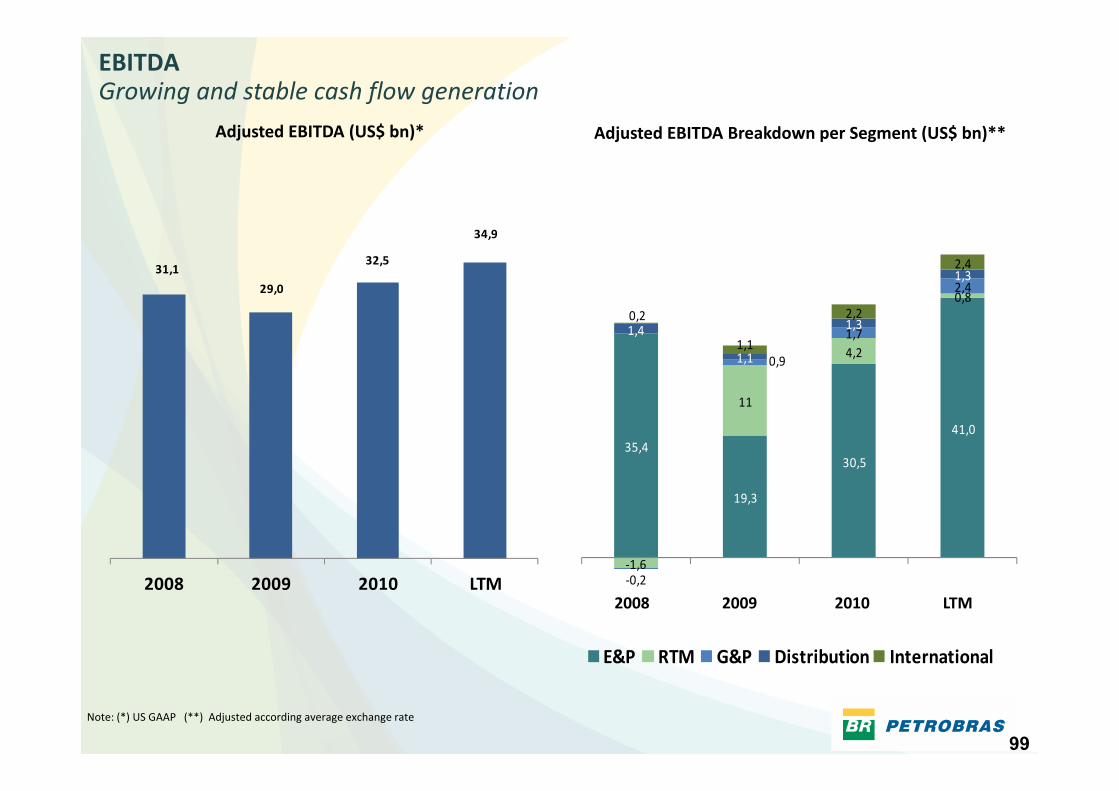

EBITDAGrowing and stable cash flow generation

Adj d EBITDA (US$ b )* d d kd ( $ b )**Adjusted EBITDA (US$ bn)* Adjusted EBITDA Breakdown per Segment (US$ bn)**

0,82,41,32,431,1

29,0

32,5

34,9

4,20,9

1,71,4

1,1

1,30,2

1,1

2,2

35,430,5

41,0

11

19,3

‐1,6‐0,2

E&P RTM G&P Distribution International

2008 2009 2010 LTM2008 2009 2010 LTM

99Note: (*) US GAAP (**) Adjusted according average exchange rate

LEVERAGE AND LIQUIDITYExchange rate was the main reason for leverage increase