Singapore Singapore Shanghai Shanghai Houston Houston New York New York London London Düsseldorf Düsseldorf Dubai Dubai Prepared for: LSU Energy Summit October 2007 Prepared for: Prepared for: LSU Energy Summit LSU Energy Summit October 2007 October 2007 Petrochemical Market Outlook Petrochemical Market Outlook Chuck Carr Director Propylene Studies [email protected]Chuck Carr Chuck Carr Director Director Propylene Studies Propylene Studies [email protected][email protected]

Transcript

SingaporeSingapore ShanghaiShanghai HoustonHouston New YorkNew York LondonLondon DüsseldorfDüsseldorf DubaiDubai

Prepared for:LSU Energy Summit

October 2007

Prepared for:Prepared for:LSU Energy Summit LSU Energy Summit

October 2007October 2007

Petrochemical Market OutlookPetrochemical Market Outlook

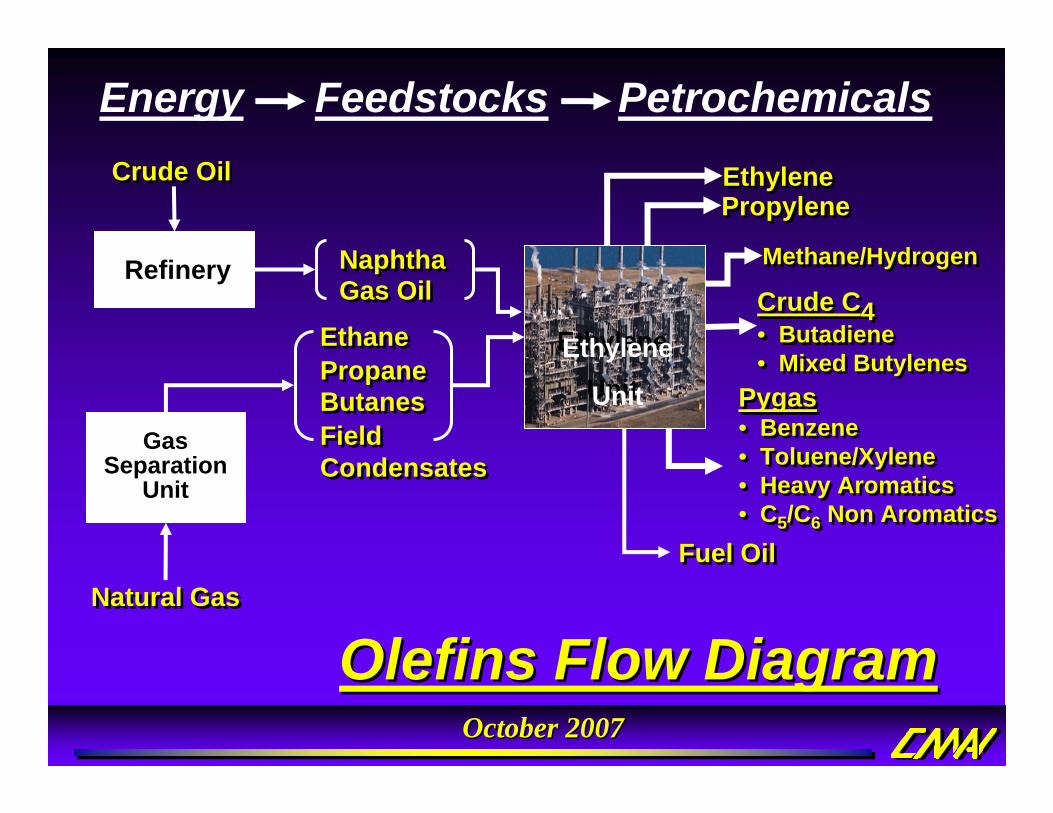

EnergyEnergy Olefins ProductionOlefins Production DerivativesDerivatives

Durable / Non-DurableDurable / Non-Durable

ConsumersConsumers Retail SectorRetail Sector

October 2007October 2007

Olefins Flow DiagramOlefins Flow Diagram

FeedstocksEnergy Petrochemicals

NaphthaNaphthaGas OilGas Oil

Field CondensatesField Condensates

EthaneEthanePropanePropaneButanesButanes

PropylenePropyleneEthyleneEthylene

Pygas• Benzene• Toluene/Xylene• Heavy Aromatics• C5/C6 Non Aromatics

Pygas• Benzene• Toluene/Xylene• Heavy Aromatics• C5/C6 Non Aromatics

Crude C4• Butadiene• Mixed Butylenes

Crude C4• Butadiene• Mixed Butylenes

Fuel OilFuel Oil

Methane/HydrogenMethane/Hydrogen

Natural GasNatural Gas

Crude OilCrude Oil

Refinery

GasSeparation

Unit

Ethylene

UnitEthylene

Unit

October 2007October 2007

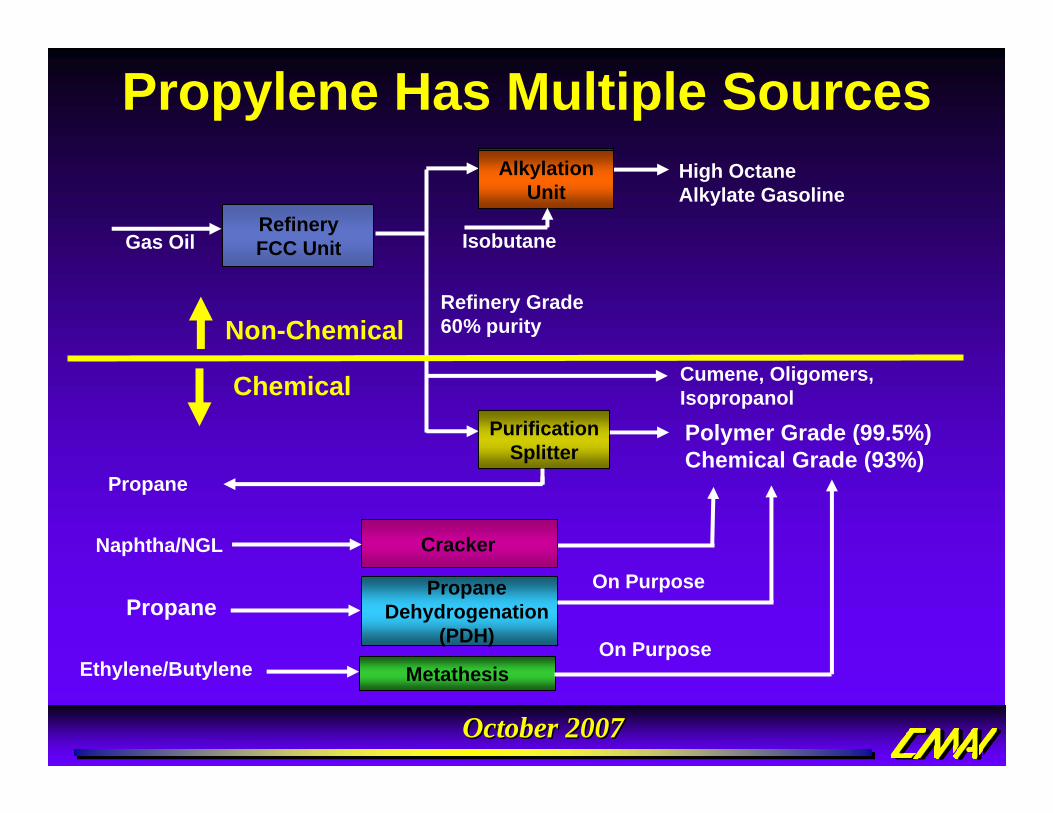

Propylene Has Multiple Sources

Propane

MetathesisEthylene/Butylene

Naphtha/NGL

RefineryFCC Unit

Alkylation Unit

Isobutane

High Octane Alkylate Gasoline

Gas Oil

Non-ChemicalRefinery Grade60% purity

Cracker

Cumene, Oligomers, Isopropanol

Polymer Grade (99.5%)Chemical Grade (93%)

Purification Splitter

Propane

Chemical

Propane Dehydrogenation

(PDH) On Purpose

On Purpose

October 2007October 2007

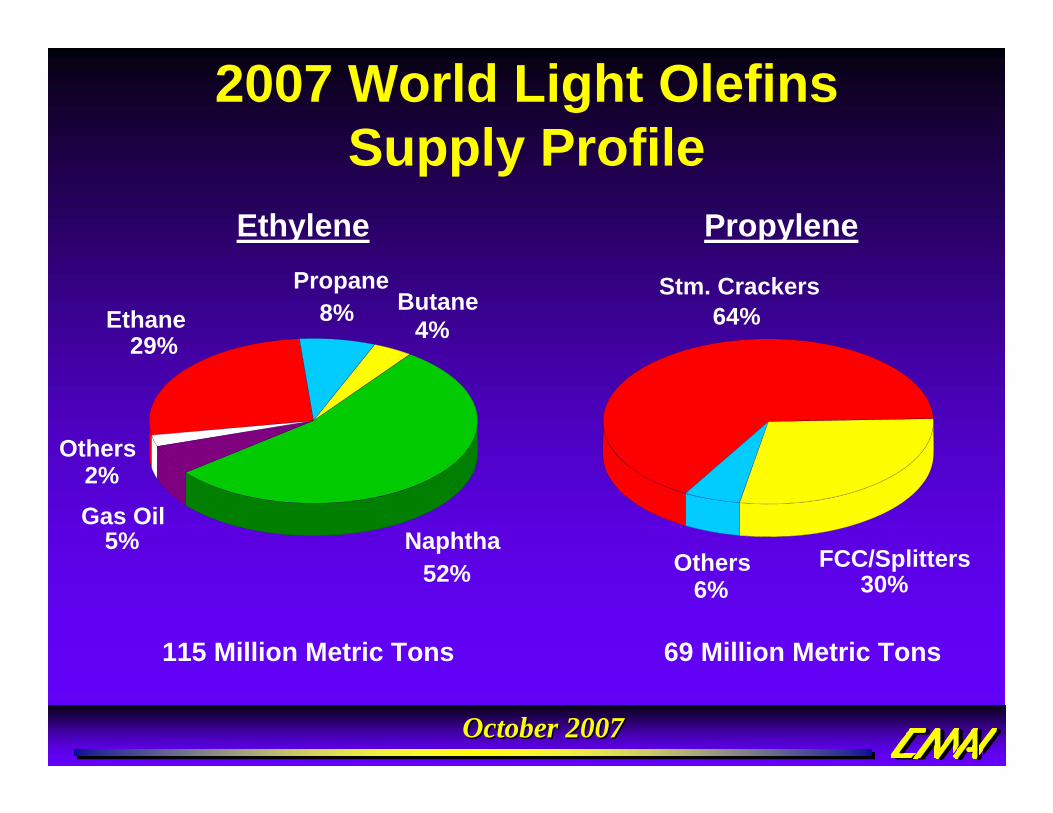

2007 World Light Olefins Supply Profile

Ethylene Propylene

69 Million Metric Tons

Others6%

Stm. Crackers64%

FCC/Splitters30%

Others2%

Butane4%

Gas Oil5%

Propane8%Ethane

29%

Naphtha52%

115 Million Metric Tons

October 2007October 2007

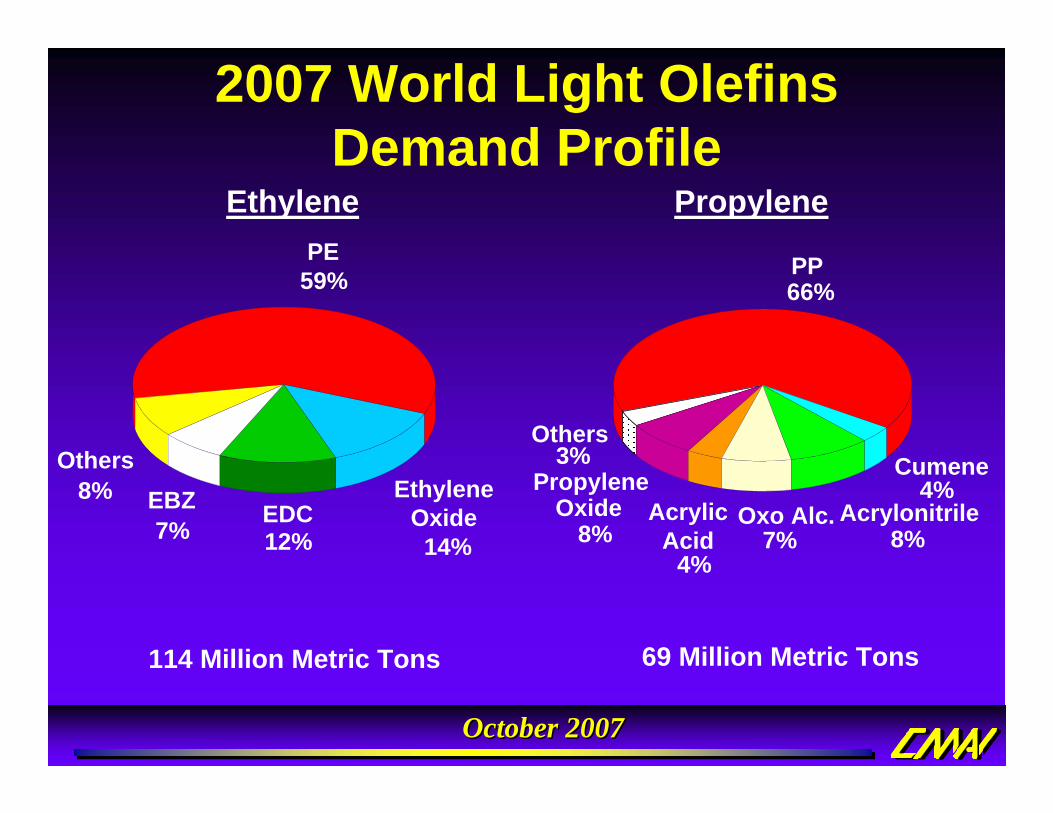

EDC12%

Ethylene Oxide

14%

PE59%

Others8% EBZ

7%

Others3%

Acrylonitrile8%

Cumene4%

Acrylic Acid

4%

Oxo Alc.7%

Propylene Oxide

8%

PP66%

Ethylene Propylene

69 Million Metric Tons114 Million Metric Tons

2007 World Light Olefins Demand Profile

October 2007October 2007

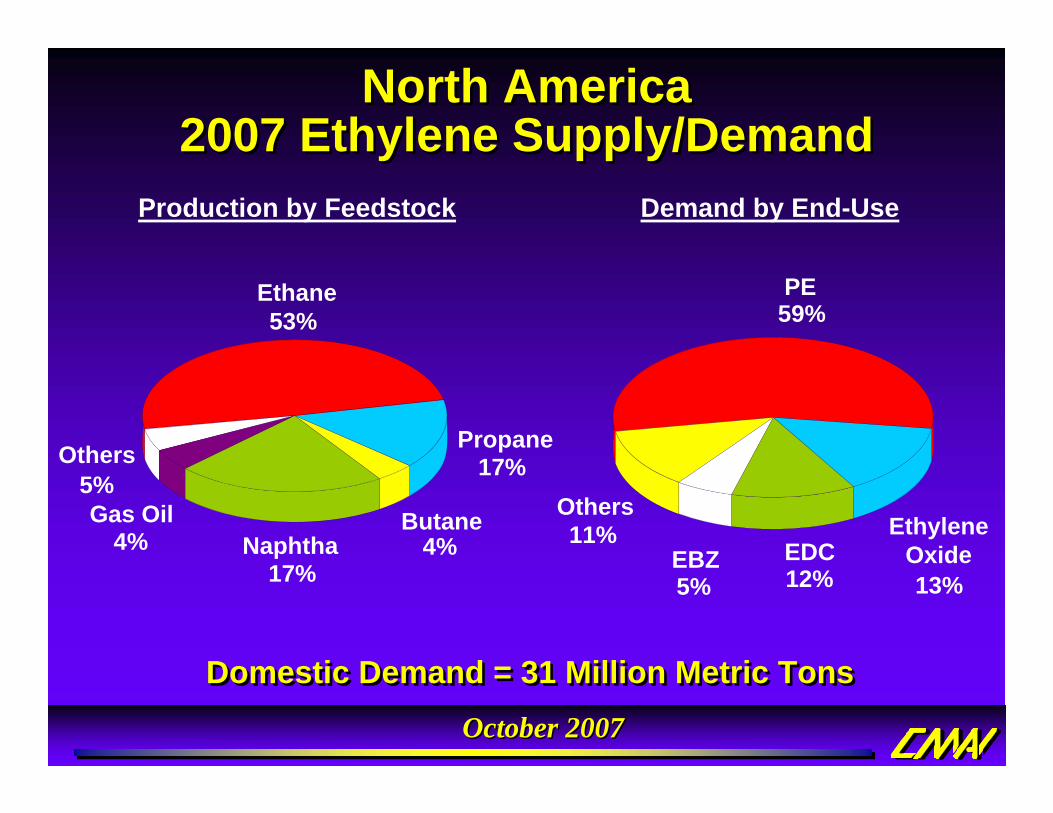

North AmericaNorth America2007 Ethylene Supply/Demand2007 Ethylene Supply/Demand

Domestic Demand = 31 Million Metric TonsDomestic Demand = 31 Million Metric Tons

Production by Feedstock Demand by End-Use

EDC12%

Ethylene Oxide13%

PE59%

Others11%

EBZ5%

Propane17%

Ethane53%

Others5%Gas Oil

4% Naphtha17%

Butane4%

October 2007October 2007

North AmericaNorth America2007 PG/CG Propylene Supply/Demand2007 PG/CG Propylene Supply/Demand

Domestic Demand = 15 Million Metric TonsDomestic Demand = 15 Million Metric Tons

Production by Source Demand by End-Use

Stm. Crackers48%

Others3%

FCC/Splitters49%

Others6%

Acrylo-nitrile10%

Cumene1%

Acrylic Acid6%

Oxo Alc.7%

Propylene Oxide12%

PP58%

October 2007October 2007

Future Propylene Supply In North America

Future supply to meet continued growth in North America propylene demand will come from:

Capacity creep on existing unitsIncreased operating rates at on-purpose metathesis units. Debottlenecks, and increased feed flexibility at refinery’s and steam crackersCanadian tar sands production

Future supply to meet continued growth in North America propylene demand will come from:

Capacity creep on existing unitsIncreased operating rates at on-purpose metathesis units. Debottlenecks, and increased feed flexibility at refinery’s and steam crackersCanadian tar sands production

October 2007October 2007

Economy and Energy Impact on

Regional Ethylene Economics

Economy and Energy Impact on

Regional Ethylene Economics

October 2007October 2007

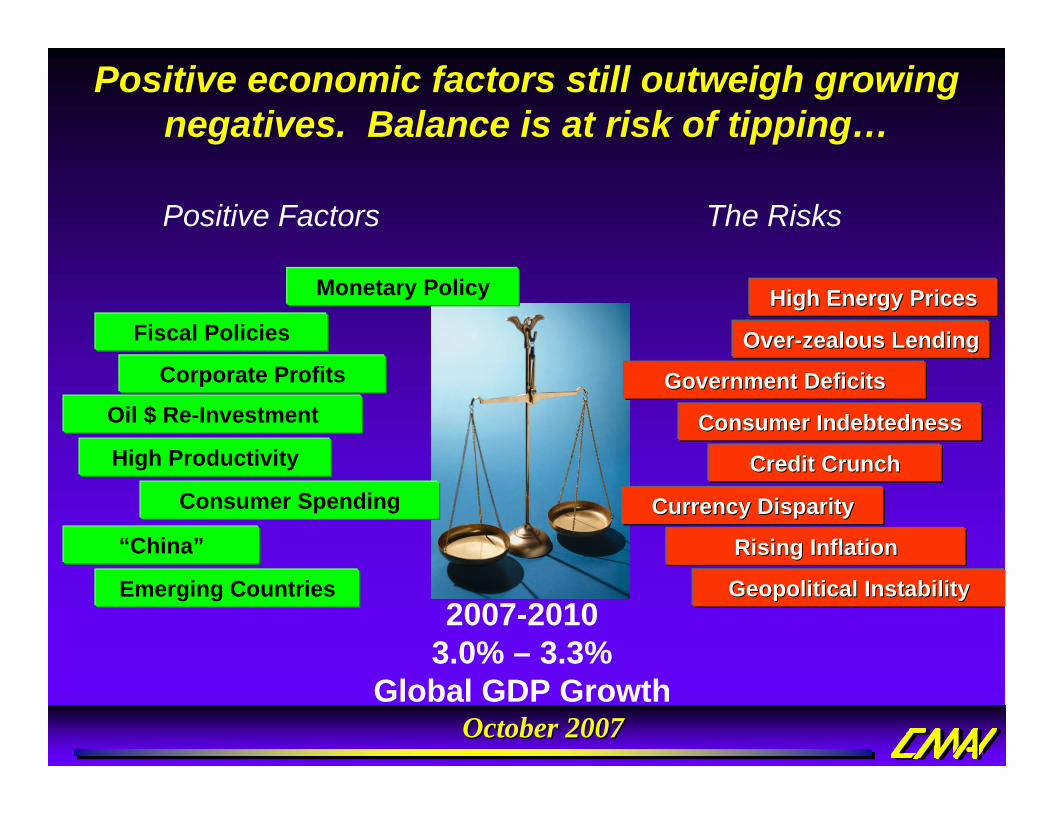

2007-2010 3.0% – 3.3%

Global GDP Growth

Positive economic factors still outweigh growing Positive economic factors still outweigh growing negatives. Balance is at risk of tippingnegatives. Balance is at risk of tipping……

Positive Factors

Monetary Policy

Corporate Profits

Fiscal Policies

Consumer Spending

“China”

Emerging Countries

High Productivity

Oil $ Re-Investment

High Energy PricesHigh Energy Prices

Credit CrunchCredit Crunch

Government DeficitsGovernment Deficits

OverOver--zealous Lendingzealous Lending

Consumer IndebtednessConsumer Indebtedness

Currency DisparityCurrency Disparity

Geopolitical InstabilityGeopolitical Instability

Rising InflationRising Inflation

The Risks

October 2007October 2007

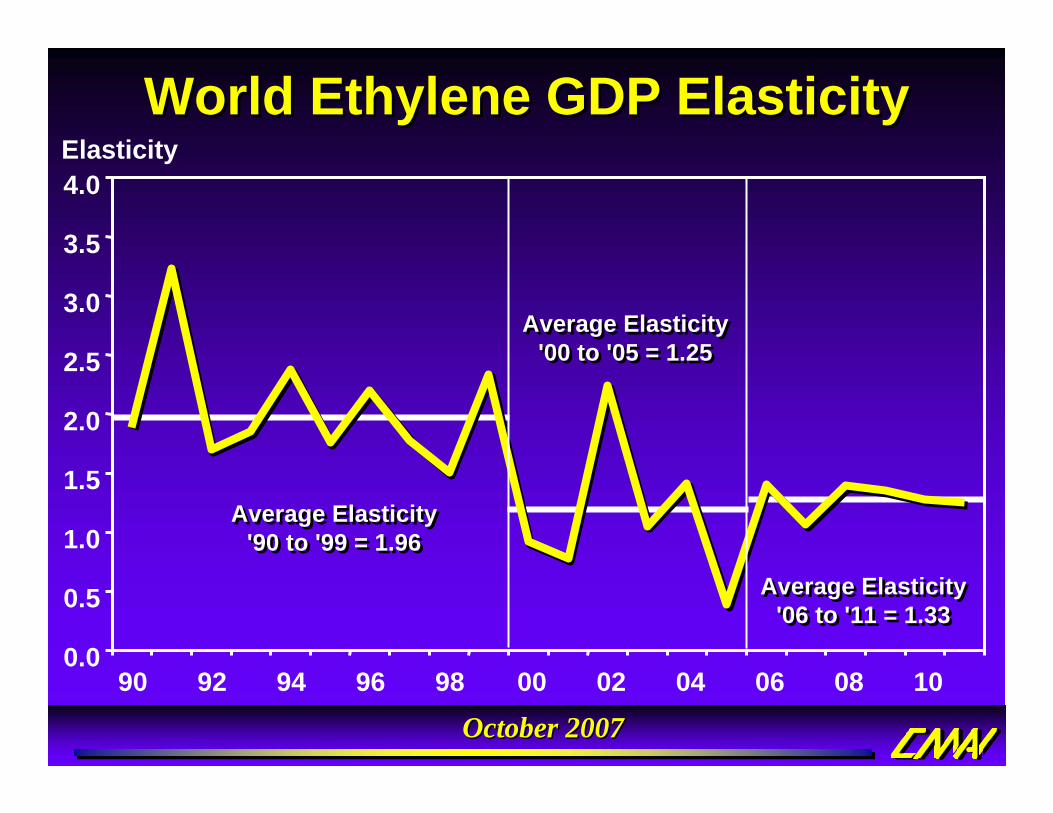

World Ethylene GDP ElasticityWorld Ethylene GDP ElasticityElasticity

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

90 92 94 96 98 00 02 04 06 08 10

Average Elasticity '90 to '99 = 1.96

Average Elasticity '90 to '99 = 1.96

Average Elasticity '00 to '05 = 1.25

Average Elasticity '00 to '05 = 1.25

Average Elasticity '06 to '11 = 1.33

Average Elasticity '06 to '11 = 1.33

October 2007October 2007

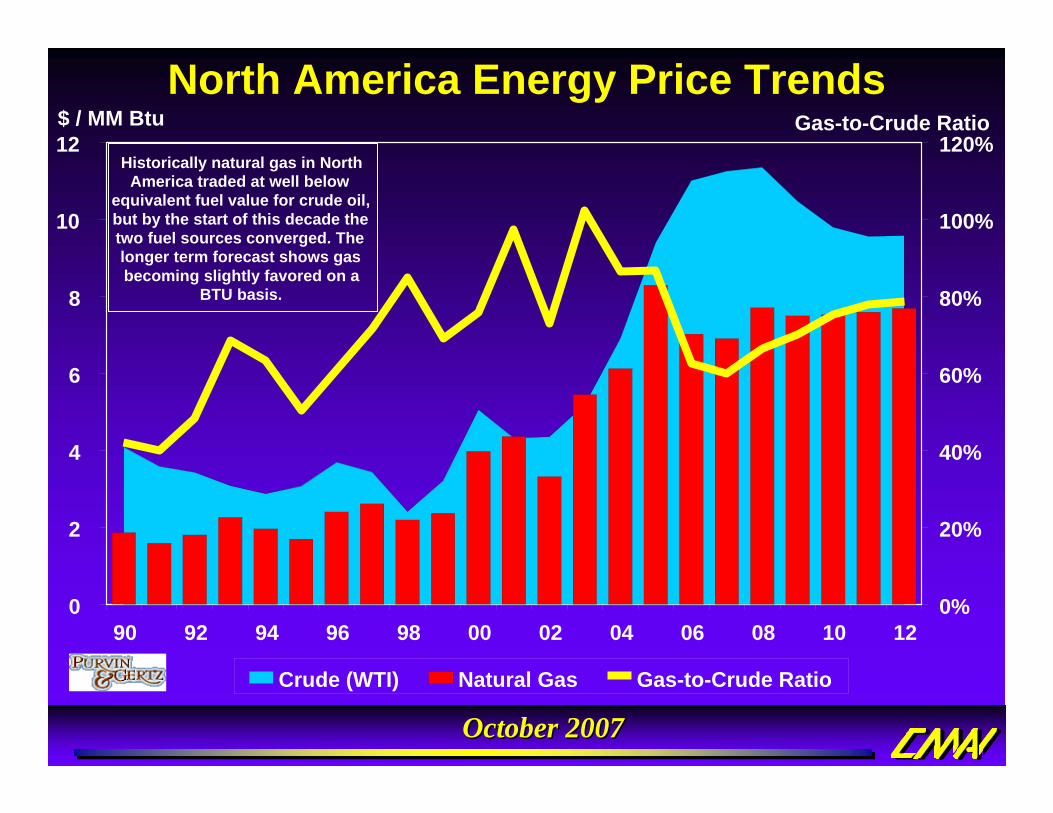

North America Energy Price Trends

0

2

4

6

8

10

12

90 92 94 96 98 00 02 04 06 08 10 12

$ / MM Btu

0%

20%

40%

60%

80%

100%

120%Gas-to-Crude Ratio

Crude (WTI) Natural Gas Gas-to-Crude Ratio

Historically natural gas in North America traded at well below

equivalent fuel value for crude oil, but by the start of this decade the two fuel sources converged. The longer term forecast shows gas becoming slightly favored on a

BTU basis.

October 2007October 2007

Higher “worry premiums” regarding perceived threats or real constraints to international crude oil

supplies favor gas based petchem units.

Exports from Canada and U.S. to Europe and Asia are possible as long as this advantage prevails. In the longer term, cost parity and severe surpluses could limit export opportunities – but for now…

Export Markets Are Very Attractive

Higher “worry premiums” regarding perceived threats or real constraints to international crude oil

supplies favor gas based petchem units.

Exports from Canada and U.S. to Europe and Asia are possible as long as this advantage prevails. In the longer term, cost parity and severe surpluses could limit export opportunities – but for now…

Export Markets Are Very Attractive

Ratio of Natural Gas to Crude Oil Price

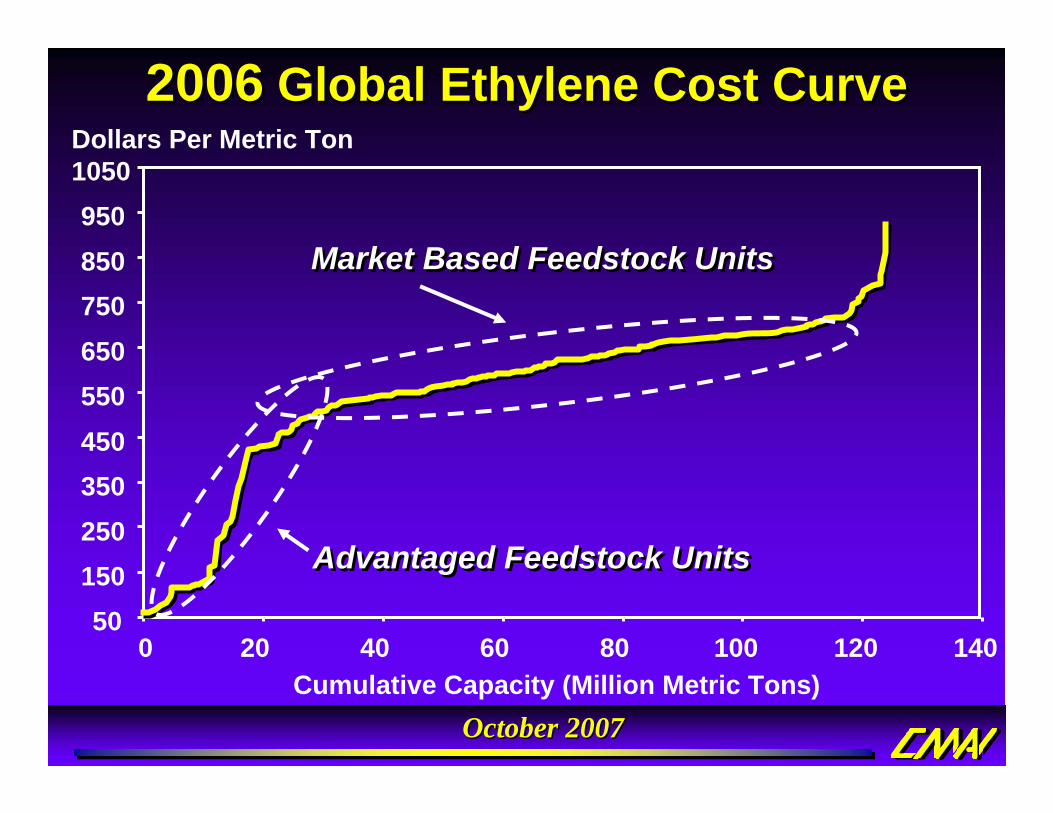

October 2007October 2007Cumulative Capacity (Million Metric Tons)

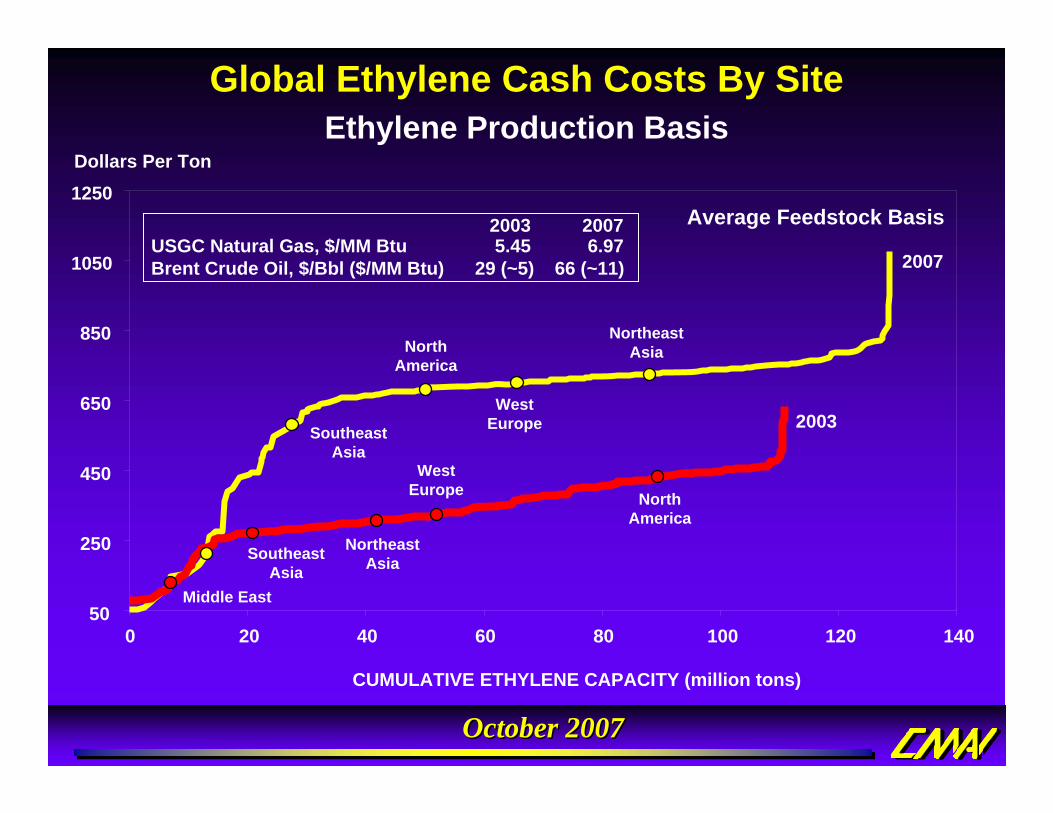

2006 Global Ethylene Cost Curve2006 Global Ethylene Cost CurveDollars Per Metric Ton1050

50150250350450550650750850950

0 20 40 60 80 100 120 140

Advantaged Feedstock UnitsAdvantaged Feedstock Units

Market Based Feedstock UnitsMarket Based Feedstock Units

October 2007October 2007

Ethylene Production BasisGlobal Ethylene Cash Costs By Site

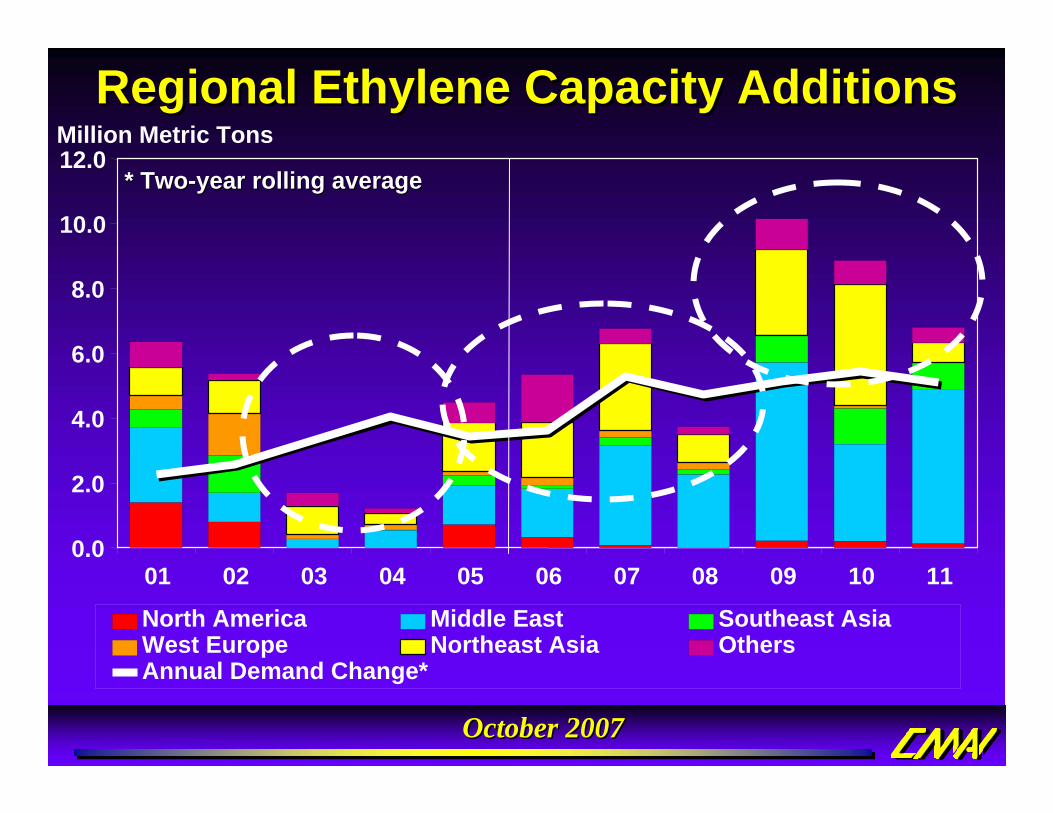

North America Middle East Southeast AsiaWest Europe Northeast Asia Others

* Two* Two--year rolling averageyear rolling average

Annual Demand Change*

October 2007October 2007

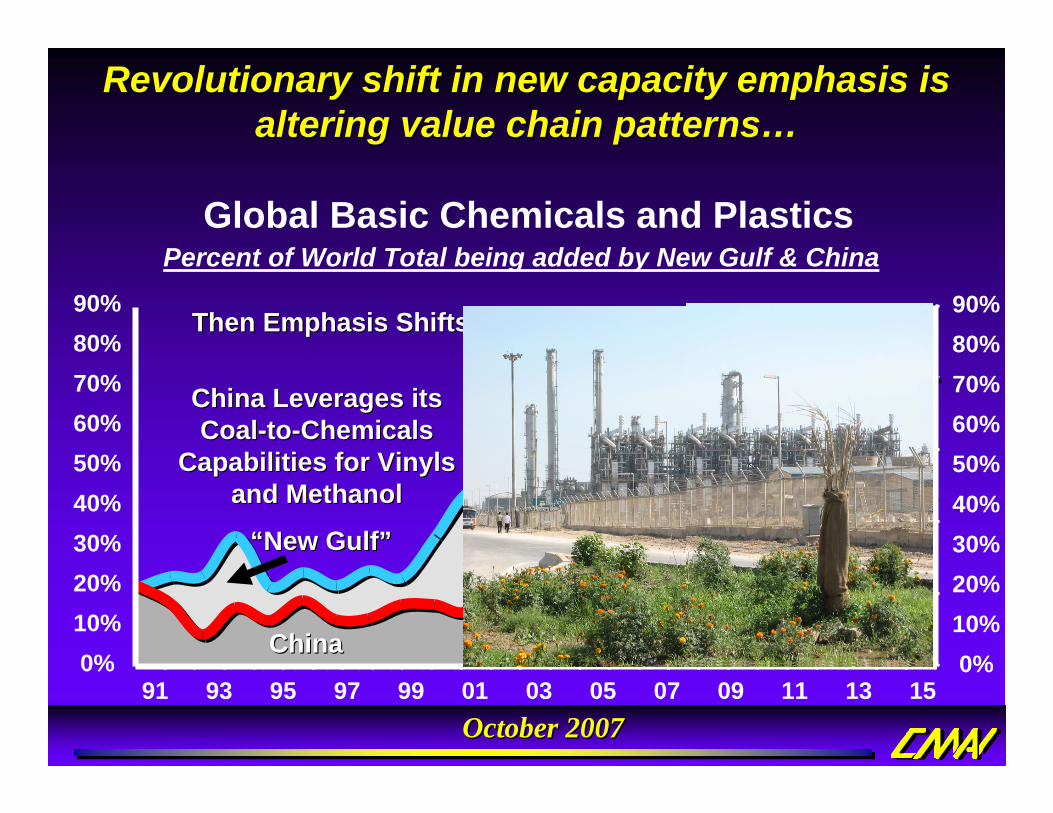

Global Basic Chemicals and PlasticsPercent of World Total being added by New Gulf & China

Then Emphasis Shifts to the Then Emphasis Shifts to the ““New GulfNew Gulf””

Revolutionary shift in new capacity emphasis is Revolutionary shift in new capacity emphasis is altering value chain patternsaltering value chain patterns……

0%10%20%30%40%50%60%70%80%90%

91 93 95 97 99 01 03 05 07 09 11 13 150%

10%20%30%40%50%60%70%80%90%

China Leverages its China Leverages its CoalCoal--toto--Chemicals Chemicals

Capabilities for Vinyls Capabilities for Vinyls and Methanoland Methanol

ChinaChina

““New GulfNew Gulf””

““New GulfNew Gulf””

ChinaChina

October 2007October 2007

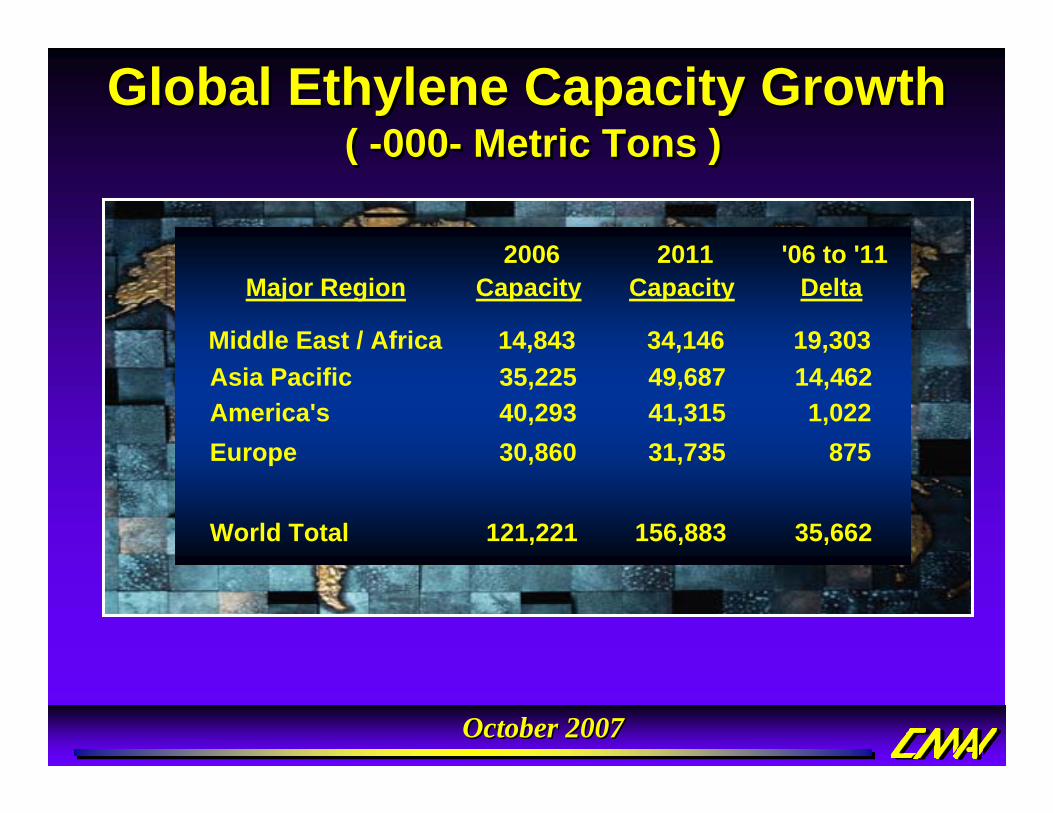

Ethylene Investments In The Americas Ethylene Investments In The Americas Western Canada limited by ethane availability. Olefins supply based on oil sands development under study

Western Canada limited by ethane availability. Olefins supply based on oil sands development under studyU.S. Gulf Coast priority shifts to feed flexibility, energy efficiency and domestic market focus

U.S. Gulf Coast priority shifts to feed flexibility, energy efficiency and domestic market focusMexico looking to leverage upstream and downstream integrationMexico looking to leverage upstream and downstream integrationTrinidad and Venezuela offer “advantaged feedstock” based investments

Trinidad and Venezuela offer “advantaged feedstock” based investments Brazil driven by upstream and downstream integration, focused on MERCOSUR

Brazil driven by upstream and downstream integration, focused on MERCOSUR

October 2007October 2007

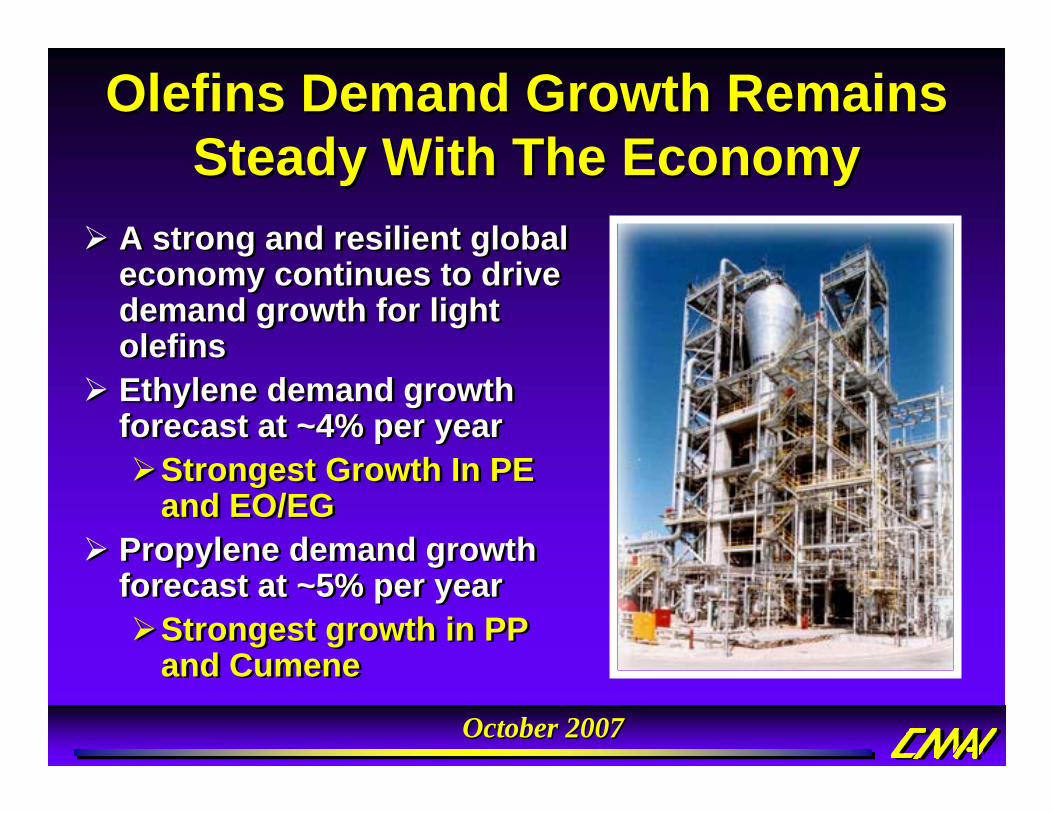

Olefins Demand Growth Remains Steady With The Economy

Olefins Demand Growth Remains Steady With The Economy

A strong and resilient global economy continues to drive demand growth for light olefinsEthylene demand growth forecast at ~4% per year

Strongest Growth In PE and EO/EG

Propylene demand growth forecast at ~5% per year

Strongest growth in PP and Cumene

A strong and resilient global economy continues to drive demand growth for light olefinsEthylene demand growth forecast at ~4% per year