27

Petrochemical Scenario Across Continents: What is Happening in the World of Polypropylene? IOCL Petrochemical Conclave New Delhi, February 2014 Sanjay Moolji Tricon Energy Ltd.

Petrochemical Scenario Across Continents:

What is Happening in the World of Polypropylene?

IOCL Petrochemical Conclave

New Delhi, February 2014

Sanjay Moolji

Tricon Energy Ltd.

• World Polymer Business

• PP – Trends, Trade balance & Global

Markets

• Challenges & Uncertainties

• Conclusions

• About Tricon EnergySTRICTLY CONFIDENTIAL

CONTENTS

Polymer Business – Global Overview

STRICTLY CONFIDENTIAL

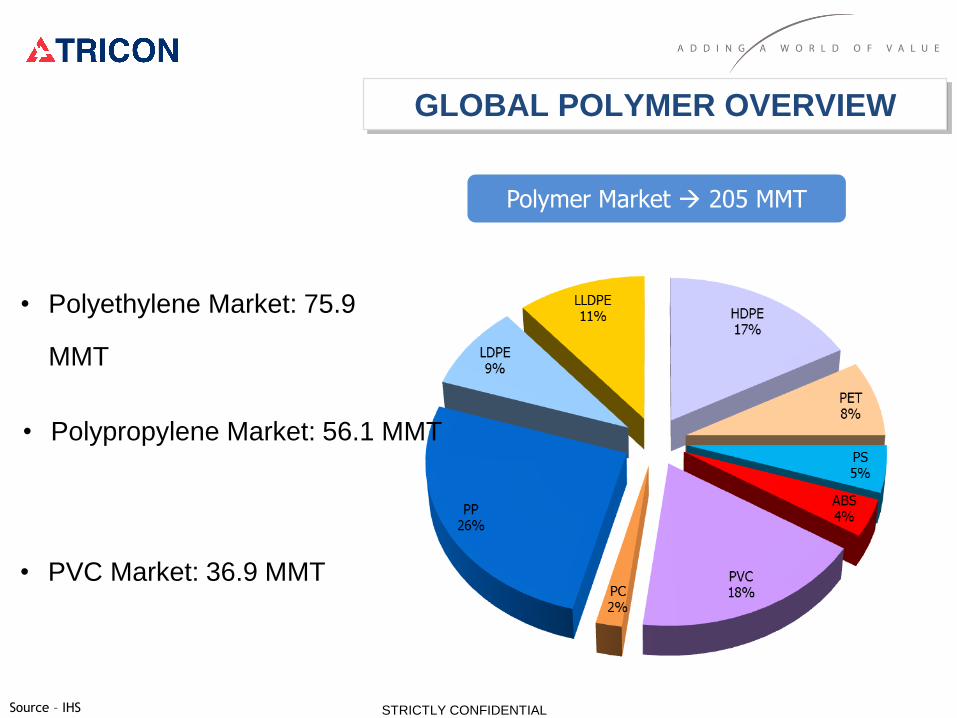

Polymer Market 205 MMT

• Polyethylene Market: 75.9

MMT

• Polypropylene Market: 56.1 MMT

• PVC Market: 36.9 MMT

GLOBAL POLYMER OVERVIEW

STRICTLY CONFIDENTIALSource – IHS

Source – IHS STRICTLY CONFIDENTIAL

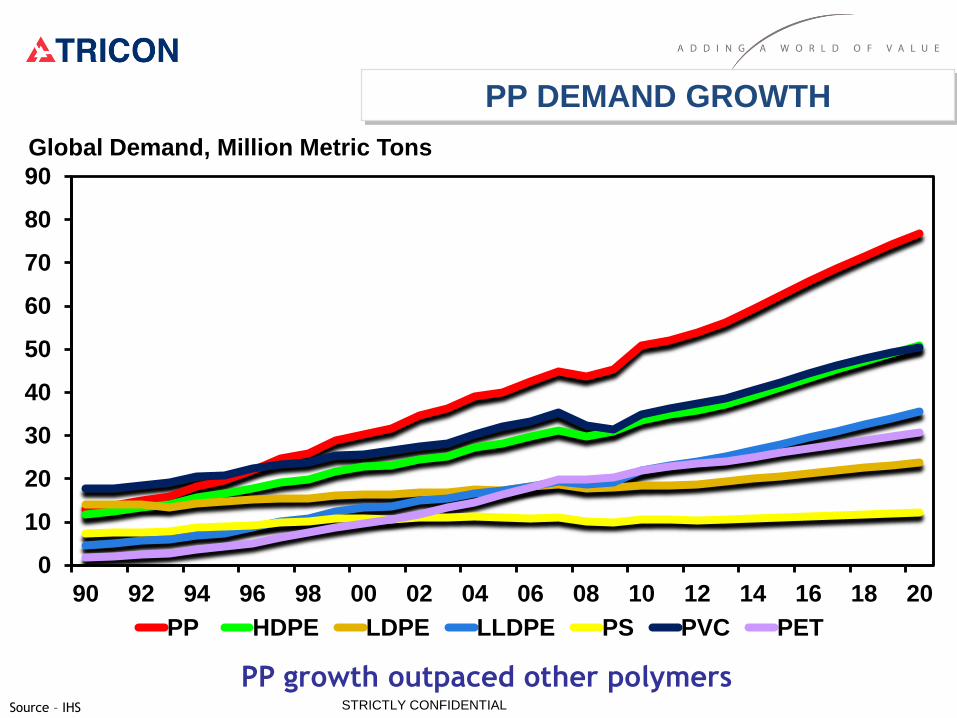

PP DEMAND GROWTH

0

10

20

30

40

50

60

70

80

90

90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 20

PP HDPE LDPE LLDPE PS PVC PET

Global Demand, Million Metric Tons

PP growth outpaced other polymers

Polypropylene Business – Global Overview

STRICTLY CONFIDENTIAL

18.6 mmta

STRICTLY CONFIDENTIAL

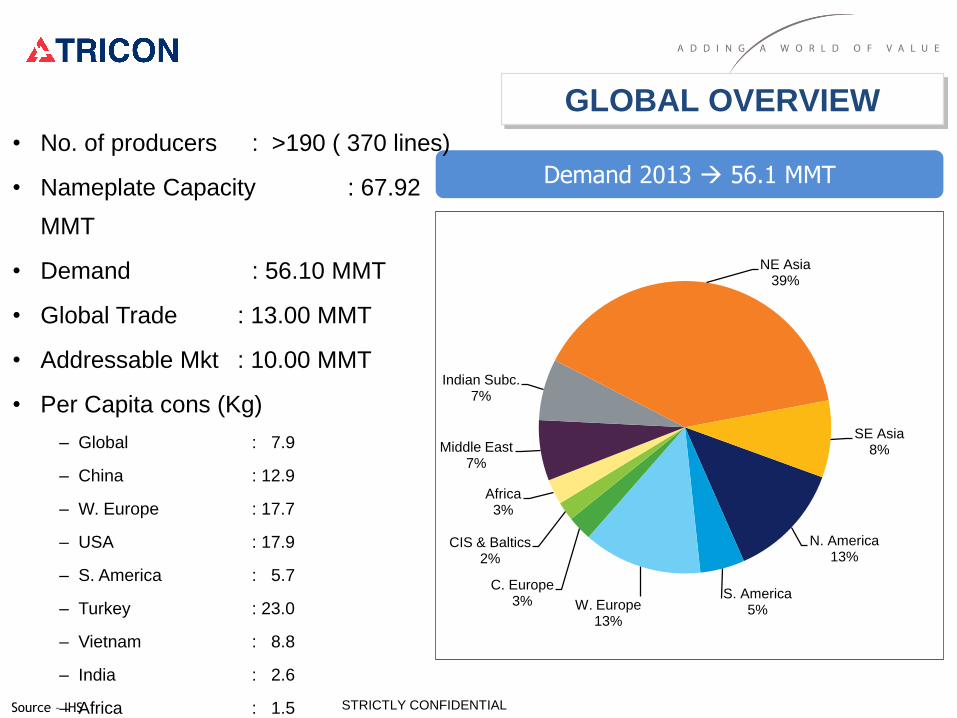

N. America13%

S. America5%W. Europe

13%

C. Europe3%

CIS & Baltics2%

Africa3%

Middle East7%

Indian Subc.7%

NE Asia39%

SE Asia8%

Demand 2013 56.1 MMT

GLOBAL OVERVIEW

• No. of producers : >190 ( 370 lines)

• Nameplate Capacity : 67.92

MMT

• Demand : 56.10 MMT

• Global Trade : 13.00 MMT

• Addressable Mkt : 10.00 MMT

• Per Capita cons (Kg)

– Global : 7.9

– China : 12.9

– W. Europe : 17.7

– USA : 17.9

– S. America : 5.7

– Turkey : 23.0

– Vietnam : 8.8

– India : 2.6

– Africa : 1.5Source – IHS

Top 10 producers account for 55% of global capacity

Capacity Capacity

(Kt) (Kt)

Lyondell Basell 6.47 1 Lyondell Basell 6.52

Sinopec Group 4.93 2 Sinopec Group 6.46

Braskem Group 4.03 3 PetroChina Group 4.61

SABIC 3.46 4 Braskem Group 4.03

PetroChina Group 3.04 5 Borealis / Borouge 3.72

Reliance Industries 2.75 6 SABIC 3.46

Borealis / Borouge 2.75 7 Exxon Mobil 2.79

Total PC 2.72 8 Reliance Industries 2.75

Exxon Mobil 2.28 9 Total PC 2.72

Formosa Plastics Corp. 2.27 10 Formosa Plastics Corp. 2.27

Total (Top 10) 34.69 Total (Top 10) 39.32

Global Capacity 64.18 Global Capacity 76.81

2011 2016Rank

Source – IHS/INTERNAL STRICTLY CONFIDENTIAL

PP PRODUCERS – THE BIG DADDY’S

20013-2018 =+18.5 MMT

2013 – 2018 AAGR

Total Capacity = 4.9%

Total Demand = 5.0%

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018North America South America West Europe

CEP/CIS Africa/Middle East Indian Sub.

Northeast Asia Southeast Asia Global Demand Growth

Million Metric Tons

Capacity Builds in Middle East and China Over-Capacity ??

2008-2013 =+16.5 MMT

PP CAPACITY OVERVIEW

STRICTLY CONFIDENTIALSource – IHS

Polypropylene Trade Balance

STRICTLY CONFIDENTIAL

523188

1105

0

500

1000

1500

2000

2500

3000

3500

2010 2014 2018NORTH AMERICA

SOUTH AMERICA

WEST EUROPE

CENTRAL EUROPECIS/ BALTIC

AFRICA

N E ASIA

S E ASIA

MIDDLE EAST

INDIAN S C

Changing Global Dynamics…. Significant Shift in Global TradeSource: IHS

PP TRADE BALANCE

-214-376

-960

-3500

-3000

-2500

-2000

-1500

-1000

-500

0

2010 2014 2018

1654

3132 3167

0

500

1000

1500

2000

2500

3000

3500

2010 2014 2018

-516-710

-1039

-3500

-3000

-2500

-2000

-1500

-1000

-500

0

2010 2014 2018

-174 -106

-1382

-3500

-3000

-2500

-2000

-1500

-1000

-500

0

2010 2014 2018 -214-376

-960

-3500

-3000

-2500

-2000

-1500

-1000

-500

0

2010 2014 2018

-474 -458-272

-3500

-3000

-2500

-2000

-1500

-1000

-500

0

2010 2014 2018

973

395

-358-1000

-500

0

500

1000

1500

2000

2500

3000

3500

2010 2014 2018-1467 -1503

498

-2000

-1500

-1000

-500

0

500

1000

1500

2010 2014 2018

STRICTLY CONFIDENTIAL

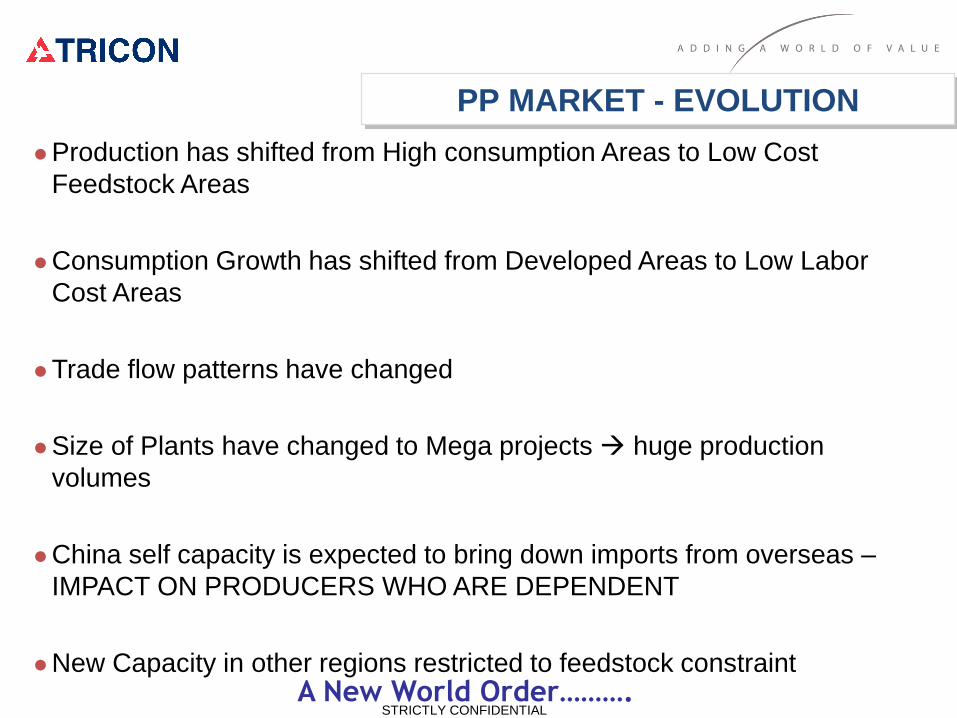

Production has shifted from High consumption Areas to Low Cost

Feedstock Areas

Consumption Growth has shifted from Developed Areas to Low Labor

Cost Areas

Trade flow patterns have changed

Size of Plants have changed to Mega projects huge production

volumes

China self capacity is expected to bring down imports from overseas –

IMPACT ON PRODUCERS WHO ARE DEPENDENT

New Capacity in other regions restricted to feedstock constraintA New World Order……….

PP MARKET - EVOLUTION

STRICTLY CONFIDENTIAL

Challenges & Uncertainties

STRICTLY CONFIDENTIAL

Propylene Produced from Multiple Sources…………

Propane

MetathesisEthylene/Butylene

Naphtha/NGL

Refinery

FCC Unit

Alkylation

Unit

Isobutane

High Octane

Alkylate

GasolineGas Oil

Non-ChemicalRefinery Grade60% purity

Cracker

Cumene, Oligomers,

Isopropanol

Polymer Grade (99.5%)

Chemical Grade (94%)Purificatio

n Splitter

Propane

Chemical

Propane

Dehydrogenation

(PDH)

On Purpose

On Purpose

MTO / MTPOn PurposeMethanol (ex-

Synthesis Gas, ex-

coal) STRICTLY CONFIDENTIALSource – IHS

Propylene Demand Profile 2013……….

Stm. Crackers

55%

FCC Splitters

31%

Dehydro5%

Metathesis4%

Coal to Propylene

1%

HS FCC3%

Others On-Purpose

1%

2013 Production Estimate = 83.6 Million Metric Tons

Production by Feedstock Demand by End-Use

Acrylic Acid4%

Acrylo-nitrile7%

Cumene4% Iso-propanol

1%

2-Ethyl Hexanol

3%

Butanols3%

Poly-propylene

68%

Propylene Oxide

8%

Others2%

STRICTLY CONFIDENTIALSource – IHS

• Demand for propylene growing faster than ethylene demand

• Propylene a co-product – Naphtha cracking makes much more propylene versus ethane

cracking

– Refining FCC units produce propylene

• Increased investment in ethane crackers in the Middle East & Americas forces producers to look for other sources– Refining

o FCC units crack heavy gas oils to higher valued distillates

o Petrochemicals buys propylene away from refinery

– On-Purpose

o “On Purpose” propylene production includes metathesis, PDH, olefin cracking and gas-to-olefins

o Propane dehydrogenation (PDH) must have feed advantages to be competitive.

Propylene Challenges

Propylene availability …challenge for Polypropylene !!STRICTLY CONFIDENTIAL

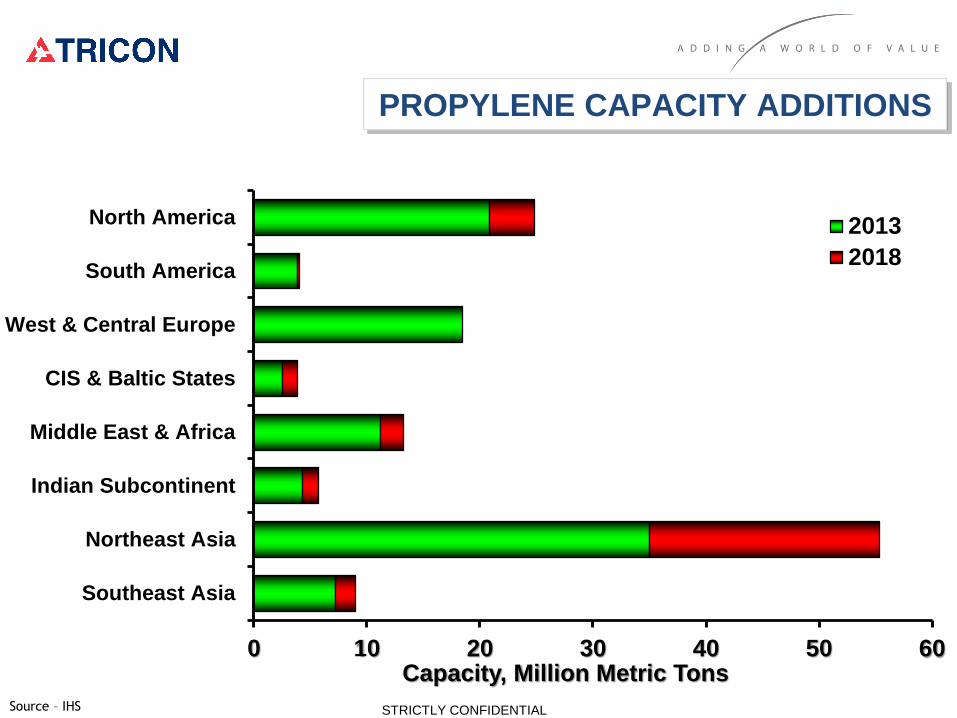

0 10 20 30 40 50 60

North America

South America

West & Central Europe

CIS & Baltic States

Middle East & Africa

Indian Subcontinent

Northeast Asia

Southeast Asia

2013

2018

PROPYLENE CAPACITY ADDITIONS

STRICTLY CONFIDENTIALSource – IHS

Capacity, Million Metric Tons

NAM Propylene Capacity Additions

Abundant Propane Driving Investments…will it make PP ??

Announced

Company Location Type

Capacity

KT Start-up Date

Debottlenecks /

New build

Dow Freeport, TX PDH 750 Q3 2015 NB

Enterprise Mont Belvieu, TX PDH 750 Q4 2015 NB

Formosa Point Comfort, TX PDH 600 Q3 2016 NB

Ascend Alvin, TX PDH 1000 Q1 2017 NB

Williams Redwater, Alberta PDH 500 Q2 2017 NB

Dow Freeport, TX PDH 750 Q3 2018 NB

Total 4350

On Hold

Company Location Type

Capacity

KT Start-up Date

Debottlenecks /

New Build

Petrologistics Houston, TX PDH 658 On hold DB/NB

STRICTLY CONFIDENTIAL

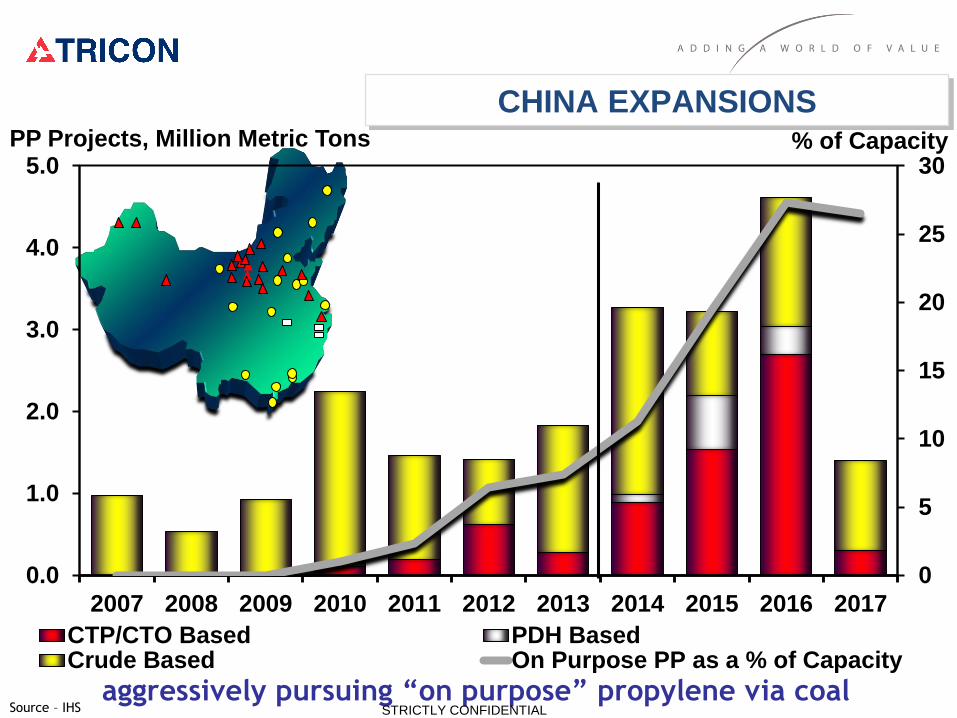

aggressively pursuing “on purpose” propylene via coal

PP Projects, Million Metric Tons

0

5

10

15

20

25

30

0.0

1.0

2.0

3.0

4.0

5.0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

CTP/CTO Based PDH BasedCrude Based On Purpose PP as a % of Capacity

% of Capacity

CHINA EXPANSIONS

STRICTLY CONFIDENTIALSource – IHS

Fushun PC (300kt)

Datang Int'l Power (500kt)

Sichuan PC (450kt)

Ningxia Refinery (100kt)

SINOPEC Wuhan (400kt)

Shanghai PC (200kt)

Daqing Refinery (300kt)

Hohhot Refining (150kt)

Sinopec BeiHai PC (200kt)

Yulin Energy & Chemical Co. (600kt)

Luoyang PC (140kt)

PuCheng Clean Energy (400kt)

Hebei Haiwei (300kt)

Ningbo Heyuan Chemical (300kt)

Shaanxi Yanchang (250kt)

Yankuang Guohong Chem. (300kt)

Shanxi Coking Corp. (300kt)

Sinopec-KPC PC JV (745kt)

CNOOC & Shell PC (700kt)

Yili Meidianhua (300kt)

Guangzhou PC (200kt)

Maoming PC (200kt)

Qinghai Salt (160kt)

Shenhua Ningmei (500kt)

SINOPEC Zhijin (300kt)

Shenhua Xinjiang (450kt)

2012

2013

2014

2015

2016

2017

Shandong Shenda (200kt)

Huating Coal Group (200kt)

Ningxia Yongda PC (120kt)

Baofeng Energy (300kt)

Jiutai Energy (IM) (300kt)

Sinopec /Wanbei JV (300kt)

Fujian ZhongJiang PC (350kt)

Fujian Zhongjing PC (350kt)

China Coal Crop. Yuheng (300kt)

Qingdao Ref&Chem (350kt)

Zhongtian Hechuang (700kt)

Shenhua Xiwan (380kt)

CPI/Total JV (400kt)

Sinopec Hainan R&C (400kt)

Yangzijang 400 KT

CHINA…..

STRICTLY CONFIDENTIALSource – IHS

0

10

20

30

40

50

60

70

80

90

100

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

2008 2010 2012 2014 2016 2018

Domestic Demand Exports

Total Capacity Imports

Operating Rate Imports as a % of Dom. Dem.

Million Metric Tons Operating Rate,%

• New Capacity

− 2008-13: +7.8 MMT

− 2013-18: +13.1

MMT

• More than 25%

capacity via on-purpose

by 2017, mainly CTP

• Import requirements

drop to less than 7% of

domestic demand in 5

years

STRICTLY CONFIDENTIALSource – IHS

CHINA : DEMAND SUPPLY FORECAST

STRICTLY CONFIDENTIAL

• Polypropylene no longer cheapo Incremental supply of C3 will come from non-

traditional/on purpose technologies

o China pursuing aggressively on Coal technology

o PDH based PP in North America can be advantaged : US may build new capacity by 2017/2018

• Demand to continue to grow, but at lower pace than expected in previous years

o Relative price position versus other polymers taking a toll on demand growth

o Developing economies will lead demand expansion

• Next 5 Years brings significant shifts in trade flows

o China becomes more self sufficient

o Middle East Redirects exports

o Europe transitions to new import position

o New Capacity in North America may increase export Position

CONCLUSIONS : PP

A volatile future....

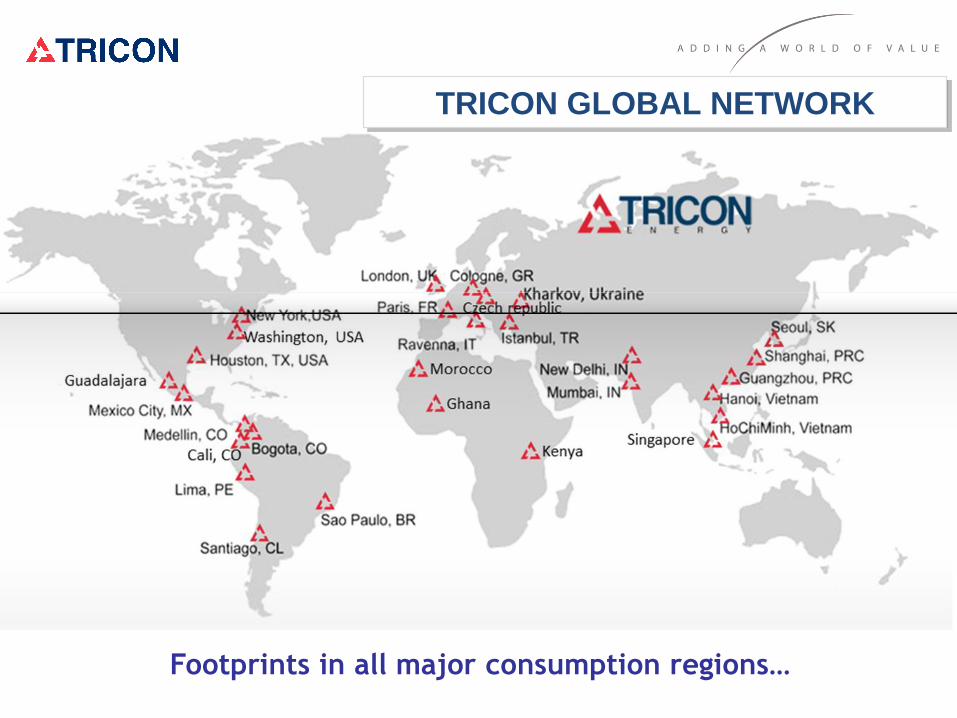

Founded in 1996

29 Local Offices

22 Languages

28 Nationalities

300+ Employees

Operating in over 100 countries

Leader in Caustic, Styrene, Xylenes & Pygas

TRICON GLOBAL NETWORK

Footprints in all major consumption regions…

FUTURE

Curiosity for new products

Passion for new places

Creativity for new services

“Tricon’s evolution is the result of the commitment of its partners to expand into additional

markets and support new product lines and industries, but always keeping our people as the

core of our strategy. As a result, the employee base, the number of offices, and the quantity

and quality of our business keeps growing year after year.”

Ignacio Torras, CEO

www.triconenergy.com

Thank you

Plastics is Fantastic !!!