39

Petroleum Geo-Services ASA Unaudited Preliminary 4th Quarter 2003 Results Prepared on Norwegian GAAP basis Oslo, March 16, 2004

| Date post: | 14-Dec-2015 |

| Category: |

Documents |

| Upload: | ulises-stockman |

| View: | 213 times |

| Download: | 0 times |

Petroleum Geo-Services ASA

Unaudited Preliminary 4th Quarter 2003 Results

Prepared on Norwegian GAAP basis

Oslo, March 16, 2004

P E T R O L E U M G E O - S E R V I C E S

Cautionary Statement & Qualifications

• This presentation contains forward looking information

• Forward looking information is based on management assumptions and analyses

• Actual experience may differ, and those differences may be material

• Forward looking information is subject to uncertainties and risks which are disclosed in PGS SEC filings

• This presentation must be read in conjunction with the press release for the 4th quarter and full year 2003 results and the disclosures therein

The accompanying unaudited, preliminary financial statements have been prepared under Norwegian GAAP. This information could be subject to adjustment, and any such adjustment could be material. This information should be read in conjunction with and is subject to qualifications discussed in the Press Release “PGS Announces Unaudited, Preliminary Results Under Norwegian GAAP for the 4th Quarter and Full Year 2003.” PGS is continuing its efforts to have an audit of its 2002 financial statements and a re-audit of its 2001 financial statements completed under U.S. GAAP. PGS is also continuing efforts to prepare audited financial statements for 2003 under both Norwegian GAAP and U.S. GAAP and to address material weaknesses in its system of internal control over financial reporting that were disclosed in November 2003. There can be no assurance, however, as to whether or when these audits and re-audit can be completed. In addition, if and when completed, the audits and re-audit could result in restatements of PGS’ previously filed U.S. GAAP audited financial statements and restatements or other adjustments to its 2002 and 2003 U.S. GAAP interim financial statements. Those restatements and adjustments could be material, although they are expected to be of a non-cash nature. Furthermore, although the audits and re-audit are being conducted under U.S. GAAP, the findings from these audits and re-audit may have an impact on Norwegian GAAP 2002 and 2003 historical financial statements. Classification of debt in the accompanying unaudited, preliminary consolidated balance sheet has been made assuming that either the audited U.S. GAAP financial statements will be timely completed or that necessary waivers under PGS’ debt agreements will be obtained.

P E T R O L E U M G E O - S E R V I C E S

We have come a long way…

Unsustainable debt levels

Failed Veritas merger catalyst for fundamental change

Redirection of business priorities

New Board and new management

Refinancing goals developed

Focus on operations and customers

Convincing cash flow and cost performance

Successful debt restructuring

High level of stakeholder support, with high stakeholder recovery

2002: Facing Realities

2002: Facing Realities

2003: FinancialRestructuring

2003: FinancialRestructuring

P E T R O L E U M G E O - S E R V I C E S

Successful financialRestructuring

We gained a competitiveedge for the future

Successful financialRestructuring

We gained a competitiveedge for the future

2003 Main Achievements

Our bestSafety

Performanceever

Our bestSafety

Performanceever

StrongRegularity

Performance

StrongRegularity

Performance

ImprovedSeismic

Contract Position

ImprovedSeismic

Contract Position

SuccessfulRevenue Build inPertra

SuccessfulRevenue Build inPertra

Improved Cost

Position

Improved Cost

Position

3 FPSOContractsProlonged

3 FPSOContractsProlonged

P E T R O L E U M G E O - S E R V I C E S

Well ahead of our main targets communicated February 2003

• Deliver cost cutting of minimum $75 millionAhead

• Improve Working capital by a minimum of 25 million Done• Reduce Multi-Client investments by minimum 20% Done• Increase level of pre-funding of Multi-Client projects Done• Continue to improve market share in the contract market Done• Improve late sales from the Multi-Client library No• Increase production over the Ramform Banff FPSO

Partly• Keep Petrojarl I, Petrojarl Varg and Petrojarl Foinaven Done

employed on attractive contracts Done• Fully capture the upside of Pertra’s cash generation potential Done• Implement a flatter and simpler organisational structure Done

2003 full year Cash flow post CAPEX $327 million –up 56,4% -Well ahead of business plan

P E T R O L E U M G E O - S E R V I C E S

• Q4 Group cash flow post CAPEX 1) of $63,7 million brings year in line with Business Plan

• Impairment charges totaling $496,6 million recognized in Q4 ($716,8 for the full year)

• Varg Field extension confirmed after EOR drilling success

• Chapter 11 process completed in 100 days – Nov 5th

– Massive support from creditors and shareholders

– Interest bearing debt reduced by $1.283 million

– New Board of Directors

• broad international and industry background

Q4 Group Highlights

1) Defined as Adjusted EBITDA (as defined) less CAPEX and Investments in Multi Client Library

P E T R O L E U M G E O - S E R V I C E S

Comments:• Marine seismic: Decline in late sales, strong contract market performance low vessel utilization in Q4 2003; Accounting rules changes impact $9 million • Pertra: High volume and high oil prices• FPSO: Foinaven production problems solved end October 2003

1) Defined as EBITDA (as defined) less CAPEX and Investments in Multi Client Library

2002 v.s 2003 Cashflow(1) Post Capex – Changes Q4 2002/2003

MarineGeo 2002 2003ProductionPertra

209

-2889

29

327

USD million

Onshore

27

The accompanying unaudited, preliminary financial statements have been prepared under Norwegian GAAP. This information could be subject to adjustment, and any such adjustment could be material. This information should be read in conjunction with and is subject to qualifications discussed in the

Press Release “PGS Announces Unaudited, Preliminary Results Under Norwegian GAAP for the 4th Quarter and Full Year 2003.”

P E T R O L E U M G E O - S E R V I C E S

Comments:• Marine seismic: Still high share in the contract market, low vessel utilization in Q4 2003; Accounting rules changes impact $... million • Pertra: High volume and high oil prices• FPSO: Foinaven production problems solved end October 2003

1) Defined as EBITDA (as defined) less CAPEX and Investments in Multi Client Library

Q4 Cashflow(1) Post Capex – Changes Q4 2002/2003

Q4 2002 Q4 2003ProductionMarineGeo

Pertra

85,4

-2,9

-33,2

8,063,7

USD million

Onshore

5,4

The accompanying unaudited, preliminary financial statements have been prepared under Norwegian GAAP. This information could be subject to adjustment, and any such adjustment could be material. This information should be read in conjunction with and is subject to qualifications discussed in the

Press Release “PGS Announces Unaudited, Preliminary Results Under Norwegian GAAP for the 4th Quarter and Full Year 2003.”

P E T R O L E U M G E O - S E R V I C E S

Q4 Highlights Marine Geophysical and Onshore

• Competitors follow PGS’ lead into contract market

• Q4 Cash flow post CAPEX down 25,4% YOY

– More steaming and yard stay– 2 C crew shut down in November– Lower MC sales (Brazil), partly offset by

higher contract sales and revenues per vessel month

• Q4 Contract / MC use of vessel capacity 78/22% (71/29%)

• Continued improvement in vessel efficiency/revenue

• Onshore Cashflow increasing due to improved project management

P E T R O L E U M G E O - S E R V I C E S

Q4 Marine Geophysical Capacity use and Vessel Revenue

0 %

20 %

40 %

60 %

80 %

100 %

Q4 02 Q1 03 Q2 03 Q3 03 Q4 03

Contract

MC

Average Monthly Contract Revenue per Vessel

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2002 2003

US

D 1

,00

0

All vessels

12 moths moving average

P E T R O L E U M G E O - S E R V I C E S

Multi Client NBV v.s Late Sale

2 %

17 %

19 %

41 %

13 %

8 %

Middle East

Europe

GoM

Brazil

Asia

Africa

3 %

15 %

29 %

16 %

7 %

30 %

Net Book value per region MC Revenue 2003 per region

Historical NBV development

2001 –$960 million

2002 -$640 million

2003 –$428 million

P E T R O L E U M G E O - S E R V I C E S

Marine and Onshore Multi-client Investments cash in/out 1991-03

P E T R O L E U M G E O - S E R V I C E S

Q4 highlights Production and Pertra

• Foinaven compressor problems solved and vessel back in full production late October 2003. EBITDA effect $9.5 million for 2003

• 1st well in the Varg Enhanced Oil Recovery (EOR) program confirms new reservoir model, increasing recoverable reserves substantially.– Reserve estimate increased to 70 million barrels– Production increased substantially into 2004

• Heads of Agreement in place for improved Banff contract with Canadian Natural Resources (CNR)– Minimum day rate $125,000,-– Fixed day rate $68,000,-– Tariff $5 per barrel of produced oil

– Subject to license partners approval

P E T R O L E U M G E O - S E R V I C E S

Revised FPSO Deployment Schedule PGS estimate

Petrojarl I - Operating for Statoil on Glitne field. Additional well extends production to 2007.

Petrojarl Varg - Operating for Pertra on Varg field. Successful drilling program extends field life,

possibly into 2008

Petrojarl Foinaven - Operating for BP on Foinaven field. Duration estimated to be past 2008

Ramform Banff - Operating for CNR on Banff field. Duration expected to 2011

2002 2003 2004 2005 2006 2007 2008 2009

Ramform Banff

Petrojarl Varg

Petrojarl Foinaven

Petrojarl I

2002 Business Plan New estimate

P E T R O L E U M G E O - S E R V I C E S

Pertra headlines - 2003

•Pertra’s oil replacement rate from start 2003 to start 2004 is 458%

•Pertra has completed 4 wells to date, all in accordance with the predicted outcome.

•PGS seismic and reservoir services have been fundamental to the success.

•Pertra has introduced new incentive arrangements with drilling contractors.

•Pertra is seeking new licenses in the Norwegian 18th round to apply its competence in small field E&P.

P E T R O L E U M G E O - S E R V I C E S

Q4 Key Figures, Norwegian GAAP

New accounting principles reduces comparability between 2003 and 2002.

Vessel steaming and yard stay is no longer deferred or capitalised to multi-client.

(In $ millions) 2003 2002 % change 2003 2002 % change

Revenues 260,5 261,7 -0,5 % 1 111,5 992,3 12,0 %

EBITDA as defined (A) 99,4 127,1 -21,8 % 477,7 460,5 3,7 %

CAPEX (B) (24,6) (7,2) 241,7 % (57,4) (60,8) -5,6 %

Investments in MCS (C) (11,0) (34,5) -68,1 % (93,0) (190,4) -51,2 %

Cashflow post investments 63,7 85,4 -25,4 % 327,3 209,3 56,4 %(A+B+C)

Shareholders Equity 373,0 (42,0)

Quarter ended December 31, Twelve months ended Dec. 31,

The accompanying unaudited, preliminary financial statements have been prepared under Norwegian GAAP. This information could be subject to adjustment, and any such adjustment could be material. This information should be read in conjunction with and is subject to qualifications discussed in the

Press Release “PGS Announces Unaudited, Preliminary Results Under Norwegian GAAP for the 4th Quarter and Full Year 2003.”

P E T R O L E U M G E O - S E R V I C E S

150

170

190

210

230

250

270

290

310

Q102

Q202

Q302

Q402

Q103

Q203

Q303

Q403

Revenues by Quarter 2002/2003

$ Million

Q4 2003 comments:

Revenues at par with 4Q 2002

Marine Geophysical down $18.5 million due to reduced MC sales and increased steaming

Onshore increased revenue by $6.7 million

Production revenue unchanged

Pertra increased revenue by 60% ($9.9 million)

The accompanying unaudited, preliminary financial statements have been prepared under Norwegian GAAP. This information could be subject to adjustment, and any such adjustment could be material. This information should be read in conjunction with and is subject to qualifications discussed in the

Press Release “PGS Announces Unaudited, Preliminary Results Under Norwegian GAAP for the 4th Quarter and Full Year 2003.”

P E T R O L E U M G E O - S E R V I C E S

Adjusted EBITDA (1) by Quarter 2002/03

(1) EBITDA, as defined, consists of operating income (loss) before depreciation and amortization, as well as unusual items

Q4 2003 comments:

•Down $27.8 m to $99.3 million

•Marine Geophysical decreased by $51.4 million

Reduced MC salesReduced

capitalization to MC library

Lower vessel utilization

•Onshore increased by $8.9 million

•Production unchanged

•Pertra up $13.7 million

$ million

A MC sale of USD 18,3 million in Brunei was booked in Q1 03,

and reversed in Q2 03

The accompanying unaudited, preliminary financial statements have been prepared under Norwegian GAAP. This information could be subject to adjustment, and any such adjustment could be material. This information should be read in conjunction with and is subject to qualifications discussed in the

Press Release “PGS Announces Unaudited, Preliminary Results Under Norwegian GAAP for the 4th Quarter and Full Year 2003.”

P E T R O L E U M G E O - S E R V I C E S

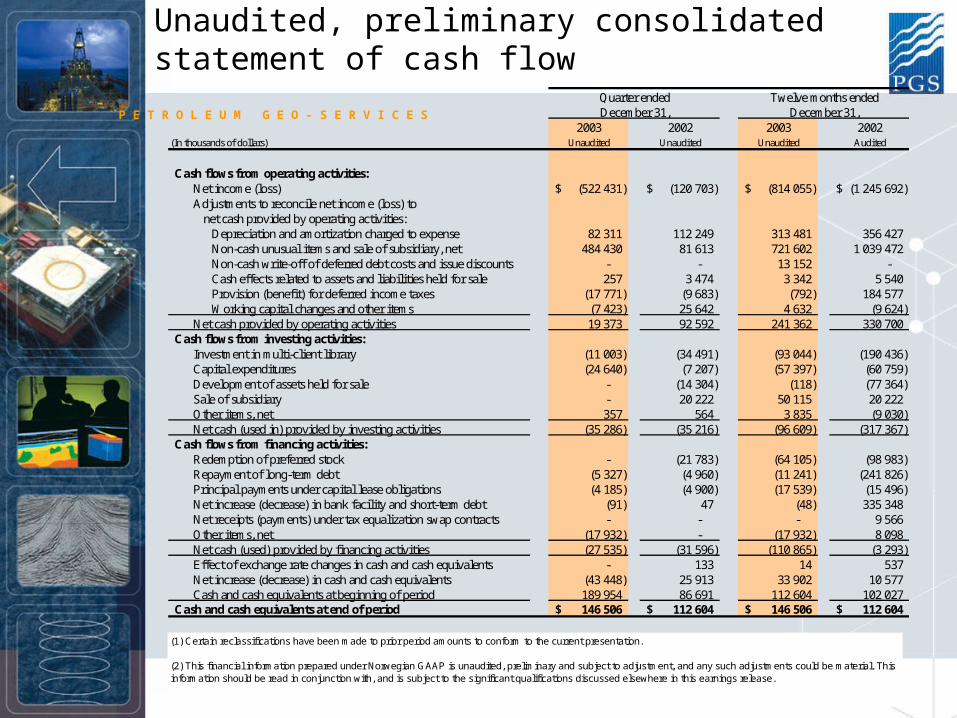

Unaudited, preliminary consolidated statement of cash flow

2003 2002 2003 2002(In thousands of dollars) Unaudited Unaudited Unaudited Audited

Cash flows from operating activities:Net income (loss) (522 431)$ (120 703)$ (814 055)$ (1 245 692)$ Adjustments to reconcile net income (loss) to

net cash provided by operating activities:Depreciation and amortization charged to expense 82 311 112 249 313 481 356 427 Non-cash unusual items and sale of subsidiary, net 484 430 81 613 721 602 1 039 472 Non-cash write-off of deferred debt costs and issue discounts - - 13 152 - Cash effects related to assets and liabilities held for sale 257 3 474 3 342 5 540 Provision (benefit) for deferred income taxes (17 771) (9 683) (792) 184 577 Working capital changes and other items (7 423) 25 642 4 632 (9 624)

Net cash provided by operating activities 19 373 92 592 241 362 330 700 Cash flows from investing activities:

Investment in multi-client library (11 003) (34 491) (93 044) (190 436) Capital expenditures (24 640) (7 207) (57 397) (60 759) Development of assets held for sale - (14 304) (118) (77 364) Sale of subsidiary - 20 222 50 115 20 222 Other items, net 357 564 3 835 (9 030) Net cash (used in) provided by investing activities (35 286) (35 216) (96 609) (317 367)

Cash flows from financing activities:Redemption of preferred stock - (21 783) (64 105) (98 983) Repayment of long-term debt (5 327) (4 960) (11 241) (241 826) Principal payments under capital lease obligations (4 185) (4 900) (17 539) (15 496) Net increase (decrease) in bank facility and short-term debt (91) 47 (48) 335 348 Net receipts (payments) under tax equalization swap contracts - - - 9 566 Other items, net (17 932) - (17 932) 8 098 Net cash (used) provided by financing activities (27 535) (31 596) (110 865) (3 293) Effect of exchange rate changes in cash and cash equivalents - 133 14 537 Net increase (decrease) in cash and cash equivalents (43 448) 25 913 33 902 10 577 Cash and cash equivalents at beginning of period 189 954 86 691 112 604 102 027

Cash and cash equivalents at end of period 146 506$ 112 604$ 146 506$ 112 604$

Quarter ended Twelve months endedDecember 31, December 31,

(1) Certain reclassifications have been made to prior period amounts to conform to the current presentation.

(2) This financial information prepared under Norwegian GAAP is unaudited, preliminary and subject to adjustment, and any such adjustments could be material. This information should be read in conjunction with, and is subject to the significant qualifications discussed elsewhere in this earnings release.

P E T R O L E U M G E O - S E R V I C E S

The New Debt Structure as per 5th November 2003

• 10% 7 year notes

• 8% 3 year notes

• 8 year term loan

• Oslo Seismic & capital leases

$ million

194

5

250

746

Gross interest bearing debt $1,195 million

The accompanying unaudited, preliminary financial statements have been prepared under Norwegian GAAP. This information could be subject to adjustment, and any such adjustment could be material. This information should be read in conjunction with and is subject to qualifications discussed in the

Press Release “PGS Announces Unaudited, Preliminary Results Under Norwegian GAAP for the 4th Quarter and Full Year 2003.”

P E T R O L E U M G E O - S E R V I C E S

Fresh Start Accounting

Updated information on “Fresh Start” Accounting

Under US GAAP

The accompanying unaudited, preliminary financial statements have been prepared under Norwegian GAAP. This information could be subject to adjustment, and any such adjustment could be material. This information should be read in conjunction with and is subject to qualifications discussed in the

Press Release “PGS Announces Unaudited, Preliminary Results Under Norwegian GAAP for the 4th Quarter and Full Year 2003.”

P E T R O L E U M G E O - S E R V I C E S

Unaudited, preliminary Fresh Start Balance Sheet on US GAAP basis

November 1,

(In thousands of dollars) 2003

Assets

Cash and cash equivalents 142 803$

Accounts receivable, net 196 662

Other current assets 56 153

Total current assets 395 618

Multi-client library, net 429 196

Property and equipment, net 1 049 153

Oil and gas assets 23 946

Other long-term assets, net 100 207

Total assets 1 998 120$

Liabilities and Shareholders' Equity

Current portion of long-term debt and capital lease obligations 29 955$

Accounts payable and accrued expenses 221 167

Income taxes payable 46 220

Total current liabilities 297 342

Long-term debt and capital lease obligations 1 197 487

Other long-term liabilities 164 543

Deferred income taxes 10 802

Total liabilities 1 670 174

Shareholders' equity 327 946

Total liabilities and shareholders' equity 1 998 120$

The accompanying unaudited, preliminary financial statements have been prepared under Norwegian GAAP. This information could be subject to adjustment, and any such adjustment could be material. This information should be read in conjunction with and is subject to qualifications discussed in the

Press Release “PGS Announces Unaudited, Preliminary Results Under Norwegian GAAP for the 4th Quarter and Full Year 2003.”

P E T R O L E U M G E O - S E R V I C E S

Fresh Start Accounting (cont’d)

• Property and equipment– FPSO’s $678.2 million (contract value excluded)– Seismic vessels and equipment $355.8

• Other long term assets– Fair value of intangible assets $68.8 million – most important;

• FPSO related contracts $31.8 million• Existing technology $31.6 million

– Order backlog $5.4 million

• Other long term liabilities– $46.7 million PV of defeased financial lease payments sensitive to

sterling LIBOR changes

• Long term debt:– Nominal value of $1,189.8 adjusted to $1,227.4 million market value

• Accounts payable– $40.6 million to be distributed to former banks and bondholders

• Oil and gas assets valued at $23.9 million could be subject to a gross-up

The accompanying unaudited, preliminary financial statements have been prepared under Norwegian GAAP. This information could be subject to adjustment, and any such adjustment could be material. This information should be read in conjunction with and is subject to qualifications discussed in the

Press Release “PGS Announces Unaudited, Preliminary Results Under Norwegian GAAP for the 4th Quarter and Full Year 2003.”

P E T R O L E U M G E O - S E R V I C E S

Fresh Start Accounting (cont’d)

• Accounting for steaming and yard stay:– Previously deferred such expenses, now be expensed as

incurred.• Capitalization of cost into multi-client library:

– Expenses related to steaming and yard stay and certain indirect cost, now expensed as incurred rather than capitalized.

• Amortization of multi-client library:– Continue to use Sales Forecast Method– Maximum amortization period reduced from 8 to 5 year

• Oil & gas assets:– Full Cost Method replaced with Successful Efforts Method

• Depreciation of long lived assets:– Seismic Ramform vessels + FPSO’s from 30 to 25 years– Petrojarl 1 remain at 30 years due to recent refurbishment

The accompanying unaudited, preliminary financial statements have been prepared under Norwegian GAAP. This information could be subject to adjustment, and any such adjustment could be material. This information should be read in conjunction with and is subject to qualifications discussed in the

Press Release “PGS Announces Unaudited, Preliminary Results Under Norwegian GAAP for the 4th Quarter and Full Year 2003.”

P E T R O L E U M G E O - S E R V I C E S

Outlook - Financial

• Overall: 2004 Cash Flow anticipated to be in line with Business Plan

• Production– EBITDA Positively impacted by prolonged Varg Contract

• Marine Geophysical– Market expected to strengthen after Q1– Uncertainty around licensing rounds in Brazil – Increased competition in Contract Markets a main uncertainty

• Onshore– High bidding activity, -limited growth

• Pertra– Significant increase in production

The accompanying unaudited, preliminary financial statements have been prepared under Norwegian GAAP. This information could be subject to adjustment, and any such adjustment could be material. This information should be read in conjunction with and is subject to qualifications discussed in the

Press Release “PGS Announces Unaudited, Preliminary Results Under Norwegian GAAP for the 4th Quarter and Full Year 2003.”

P E T R O L E U M G E O - S E R V I C E S

Perspectives on The Seismic Industry

• Contract markets are growing• Continued overcapacity likely• Need and room for higher pricing of technology• ”Leakages” will continue, -new marginal players and capacity

expected to enter the scene• Substantial differences in cost/productivity among the different

companies

PGS strategy is to further enhance our leadership in productivity, through continued focus on cost and technology.

We aim to retain our high market share in the contract market without sacrificing profitability.

P E T R O L E U M G E O - S E R V I C E S

PGS’ Main Business Goals 2004

Achieve re-listingin the US andbest possible

Ratings

Achieve re-listingin the US andbest possible

Ratings

Free Cash Flowabove previousBusiness Plan

Free Cash Flowabove previousBusiness Plan

Furtherimprovements in

Safety, Regularityand Cost

Furtherimprovements in

Safety, Regularityand Cost

Identifyattractive

Restructuring Opportunities

Identifyattractive

Restructuring Opportunities

Realise concrete BusinessSynergies between

BU’s

Realise concrete BusinessSynergies between

BU’s

Build strengthin Governance

and HR capabilities

Build strengthin Governance

and HR capabilities

Rebuilding

Confidence

P E T R O L E U M G E O - S E R V I C E S

Supplementary Attachments

P E T R O L E U M G E O - S E R V I C E S

Q4 Unaudited, preliminary Consolidated P&L

(In $ millions) 2003 2002 Variance 2003 2002 VarianceRevenues 260.5 261.7 (1.2) 1 111.5 992.3 119.2 COGS (143.4) (122.0) (21.4) (577.1) (473.9) (103.2) SG&A (17.0) (11.9) (5.1) (54.2) (55.2) 1.0 R&D (0.8) (0.7) (0.1) (2.5) (2.8) 0.3 Operating costs (161.2) (134.6) (26.6) (633.8) (531.9) (101.9) Adjusted EBITDA as defined 99.3 127.1 (27.8) 477.7 460.4 17.3 CAPEX (24.6) (7.2) (17.4) (57.4) (60.7) 3.3 Cash Investment in MCS library (11.0) (34.5) 23.5 (93.0) (190.4) 97.4 Cashflow before debt service 63.7 85.4 (21.7) 327.3 209.3 118.0

Depreciations/amortization (82.3) (112.2) 29.9 (313.5) (356.4) 42.9 Unusual items (18.9) (8.8) (10.1) (77.0) (15.4) (61.6) Impairment of long-term assets (496.6) - (496.6) (716.8) (807.4) 90.6 Other Gain (loss), net (9.8) (0.3) (9.5) (32.0) 37.7 (69.7) Net financial items (19.8) (41.6) 21.8 (110.3) (147.3) 37.0 Income taxes 6.2 (7.2) 13.4 (35.9) (201.9) 166.0 Discontinued operations, net of tax (0.5) (77.7) 77.2 (6.3) (215.3) 209.0 Net income, before accounting change (522.4) (120.7) (401.7) (814.1) (1 245.6) 431.5

Working capital:Accounts receivable 168.2 220.1 (51.9) Other current assets 64.7 74.1 (9.4) Accounts payable/ other liabilities (229.6) (278.5) 48.9 Net working capital 3.3 15.7 (12.4)

Quarter ended December 31, Twelve months ended December 31,

The accompanying unaudited, preliminary financial statements have been prepared under Norwegian GAAP. This information could be subject to adjustment, and any such adjustment could be material. This information should be read in conjunction with and is subject to qualifications discussed in the

Press Release “PGS Announces Unaudited, Preliminary Results Under Norwegian GAAP for the 4th Quarter and Full Year 2003.”

P E T R O L E U M G E O - S E R V I C E S

Q4 Unaudited, preliminary Revenues

(In thousands of dollars) 2003 2002 Variance 2003 2002 VarianceMarine Geophysical: - Multi-client pre-funding 8 113$ 17 391$ (9 278) 49 964$ 94 025$ (44 061) - Multi-client late sales 45 804 61 797 (15 993) 148 128 160 373 (12 245) - Contract seismic 70 436 65 778 4 658 348 579 261 904 86 675 - Other 10 063 7 885 2 178 36 708 31 884 4 824 Total Marine Geophysical 134 416 152 851 (18 435) 583 379 548 186 35 193 Onshore: - Multi-client pre-funding 3 608 2 372 1 236 15 953 12 361 3 592 - Multi-client late sales 1 203 865 338 9 215 1 726 7 489 - Contract seismic 27 489 22 412 5 077 119 332 95 459 23 873 - Other 195 119 76 -266 -452 186 Total Onshore 32 495 25 768 6 727 144 234 109 094 35 140 Production: - Petrojarl I 20 152 16 285 3 867 67 741 62 631 5 110 - Petrojarl Foinaven 26 872 32 781 (5 909) 112 099 133 364 (21 265) - Ramform Banff 11 645 10 133 1 512 45 694 37 886 7 808 - Petrojarl Varg 13 487 12 535 952 67 288 69 455 (2 167) - Other 382 383 (1) 592 1 061 (469) Total Production 72 538 72 117 421 293 414 304 397 (10 983) Pertra: - Pertra 26 239 16 360 9 879 121 640 32 697 88 943 Total Pertra 26 239 16 360 9 879 121 640 32 697 88 943 Total Corporate/Global Services 4 014 3 283 731 13 986 12 845 1 141 - Elimination of internal charter of Petrojarl Varg(1) -9 166 (8 651) (515) -45 105 -14 883 (30 222)

Total 260 536 261 728 (1 192) 1 111 548 992 336 119 212

(1) Intercompany charter of Petrojarl Varg to Pertra AS.

Quarter ended December 31, Twelve months ended December 31,

The accompanying unaudited, preliminary financial statements have been prepared under Norwegian GAAP. This information could be subject to adjustment, and any such adjustment could be material. This information should be read in conjunction with and is subject to qualifications discussed in the

Press Release “PGS Announces Unaudited, Preliminary Results Under Norwegian GAAP for the 4th Quarter and Full Year 2003.”

P E T R O L E U M G E O - S E R V I C E S

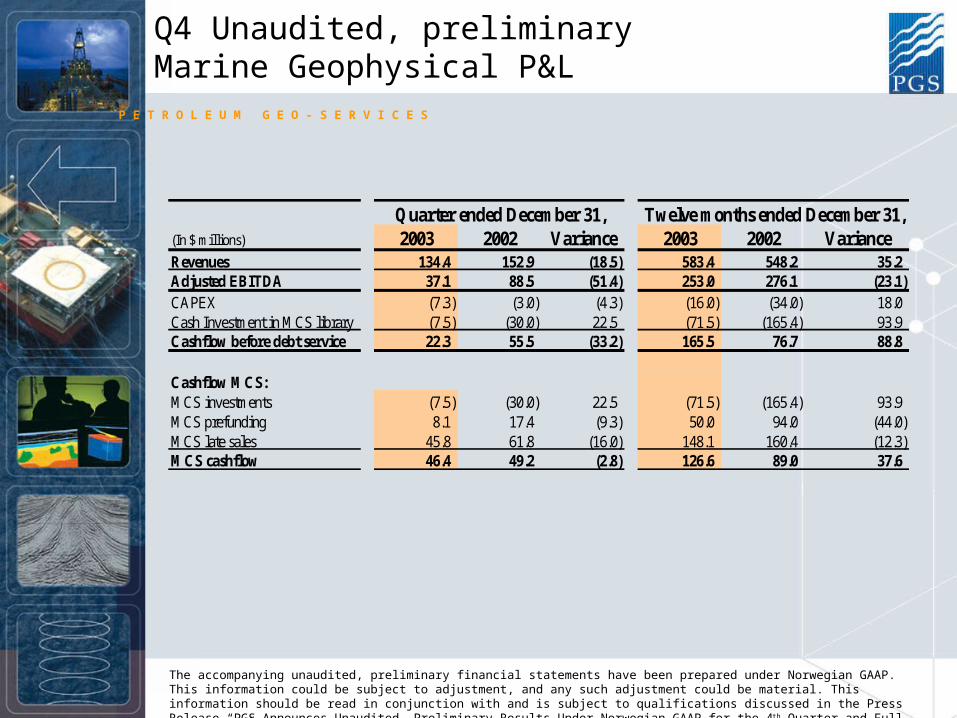

Q4 Unaudited, preliminaryMarine Geophysical P&L

(In $ millions) 2003 2002 Variance 2003 2002 VarianceRevenues 134.4 152.9 (18.5) 583.4 548.2 35.2 Adjusted EBITDA 37.1 88.5 (51.4) 253.0 276.1 (23.1) CAPEX (7.3) (3.0) (4.3) (16.0) (34.0) 18.0 Cash Investment in MCS library (7.5) (30.0) 22.5 (71.5) (165.4) 93.9 Cashflow before debt service 22.3 55.5 (33.2) 165.5 76.7 88.8

Cashflow MCS:MCS investments (7.5) (30.0) 22.5 (71.5) (165.4) 93.9 MCS prefunding 8.1 17.4 (9.3) 50.0 94.0 (44.0) MCS late sales 45.8 61.8 (16.0) 148.1 160.4 (12.3) MCS cashflow 46.4 49.2 (2.8) 126.6 89.0 37.6

Quarter ended December 31, Twelve months ended December 31,

The accompanying unaudited, preliminary financial statements have been prepared under Norwegian GAAP. This information could be subject to adjustment, and any such adjustment could be material. This information should be read in conjunction with and is subject to qualifications discussed in the

Press Release “PGS Announces Unaudited, Preliminary Results Under Norwegian GAAP for the 4th Quarter and Full Year 2003.”

P E T R O L E U M G E O - S E R V I C E S

Q4 Unaudited, preliminary Onshore P&L

(In $ millions) 2003 2002 Variance 2003 2002 VarianceRevenues 32.5 25.8 6.7 144.2 109.1 35.1 Adjusted EBITDA 16.5 7.6 8.9 53.6 30.9 22.7 CAPEX (4.4) (4.4) (6.7) (7.0) 0.3 Cash Investment in MCS library (3.5) (4.4) 0.9 (21.5) (25.0) 3.5 Cashflow before debt service 8.6 3.2 5.4 25.4 (1.1) 26.5

Cashflow MCS:MCS investments (3.5) (4.4) 0.9 (21.5) (25.0) 3.5 MCS prefunding 3.6 2.4 1.2 16.0 12.4 3.6 MCS late sales 1.2 0.9 0.3 9.2 1.7 7.5 MCS cashflow 1.3 (1.1) 2.4 3.7 (10.9) 14.6

Quarter ended December 31, Twelve months ended December 31,

The accompanying unaudited, preliminary financial statements have been prepared under Norwegian GAAP. This information could be subject to adjustment, and any such adjustment could be material. This information should be read in conjunction with and is subject to qualifications discussed in the

Press Release “PGS Announces Unaudited, Preliminary Results Under Norwegian GAAP for the 4th Quarter and Full Year 2003.”

P E T R O L E U M G E O - S E R V I C E S

Q4 Unaudited, preliminary Production P&L

(In $ millions) 2003 2002 Variance 2003 2002 VarianceRevenues 72.5 72.1 0.4 293.4 304.4 (11.0) Adjusted EBITDA 31.8 31.9 (0.1) 126.0 164.2 (38.2) CAPEX (1.7) 1.1 (2.8) (0.5) (10.9) 10.4 Cashflow before debt service 30.1 33.0 (2.9) 125.5 153.3 (27.8)

Quarter ended December 31, Twelve months ended December 31,

The accompanying unaudited, preliminary financial statements have been prepared under Norwegian GAAP. This information could be subject to adjustment, and any such adjustment could be material. This information should be read in conjunction with and is subject to qualifications discussed in the

Press Release “PGS Announces Unaudited, Preliminary Results Under Norwegian GAAP for the 4th Quarter and Full Year 2003.”

P E T R O L E U M G E O - S E R V I C E S

Q4 Unaudited, preliminary Pertra P&L

(In $ millions) 2003 2002 Variance 2003 2002 VarianceRevenues 26.2 16.4 9.8 121.6 32.7 88.9 Adjusted EBITDA 17.8 4.1 13.7 59.1 4.1 55.0 CAPEX (10.9) (5.2) (5.7) (33.8) (8.2) (25.6) Cashflow before debt service 6.9 (1.1) 8.0 25.3 (4.1) 29.4

Quarter ended December 31, Twelve months ended December 31,

The accompanying unaudited, preliminary financial statements have been prepared under Norwegian GAAP. This information could be subject to adjustment, and any such adjustment could be material. This information should be read in conjunction with and is subject to qualifications discussed in the

Press Release “PGS Announces Unaudited, Preliminary Results Under Norwegian GAAP for the 4th Quarter and Full Year 2003.”

P E T R O L E U M G E O - S E R V I C E S

Unaudited, preliminary investments & CAPEX

(In thousands of dollars) 2003 2002 Variance 2003 2002 Variance

Investments in multi-client library 11 003$ 34 491$ (23 488)$ 93 044$ 190 436$ (97 392)$

Capital expenditures: Marine Geophysical 7 336$ 3 036$ 4 300 16 030$ 34 039$ (18 009) Onshore 4 446 (84) 4 530 6 736 7 037 (301) Pertra 10 967 5 249 5 718 33 852 8 238 25 614 Production (a) 1 662 (1 052) 2 714 515 10 913 (10 398) Corporate/Global Services 229 58 171 264 532 (268) Total CAPEX 24 640 7 207 17 433 57 397 60 759 (3 362) (a) Credit in Q4 2002, relates to previous recorded disputed shipyard claim relating to a yard-stay in 2001, which now has been withdrawn.

Quarter ended December 31, Twelve months ended December 31,

The accompanying unaudited, preliminary financial statements have been prepared under Norwegian GAAP. This information could be subject to adjustment, and any such adjustment could be material. This information should be read in conjunction with and is subject to qualifications discussed in the

Press Release “PGS Announces Unaudited, Preliminary Results Under Norwegian GAAP for the 4th Quarter and Full Year 2003.”

P E T R O L E U M G E O - S E R V I C E S

Unaudited, preliminary Balance Sheet 2003 - Assets

(In thousands of dollars) 2003 2002

AssetsCash and cash equivalents 146 506$ 112 604$ Accounts receivable, net 168 187 220 085 Other current assets 64 678 74 066 Assets held for sale - 68 768

Total current assets 379 371 475 523 Multi-client library, net 388 813 660 383 Property and equipment, net 1 087 365 1 689 684 Oil and gas assets 21 182 17 324 Other long-term assets, net 34 595 119 916

Total assets 1 911 326$ 2 962 830$

December 31,

The accompanying unaudited, preliminary financial statements have been prepared under Norwegian GAAP. This information could be subject to adjustment, and any such adjustment could be material. This information should be read in conjunction with and is subject to qualifications discussed in the

Press Release “PGS Announces Unaudited, Preliminary Results Under Norwegian GAAP for the 4th Quarter and Full Year 2003.”

P E T R O L E U M G E O - S E R V I C E S

Unaudited, preliminary Balance Sheet 2003 -Liabilities & Equity

(In thousands of dollars) 2003 2002Liabilities and Shareholders' EquityShort-term debt and current portion of long-term debt and capital lease obligations 34 487$ 959 550$ Debt and other liabilities held for sale - 21 523 Accounts payable and accrued expenses 202 639 259 512

Income tax payable 26 902 19 034 Total current liabilities 264 028 1 259 619

Long-term debt and capital lease obligations 1 160 240 1 386 400 Other long-term liabilities 104 624 55 305 Deferred income taxes 9 370 97 307

Total liabilities 1 538 262 2 798 631 Minority interest 111 Commitments and contingencies Guaranteed preferred beneficial interest in PGS junior subordinated debt securities - 142 322 Mandatorily redeemable cumulative preferred stock related to multi-client securitization - 63 954 Shareholders' equity 372 953 (42 077)

Total liabilities and shareholders' equity 1 911 326$ 2 962 830$

Working capital (pre cash at hand) 3 324$ 15 605$

December 31,

The accompanying unaudited, preliminary financial statements have been prepared under Norwegian GAAP. This information could be subject to adjustment, and any such adjustment could be material. This information should be read in conjunction with and is subject to qualifications discussed in the

Press Release “PGS Announces Unaudited, Preliminary Results Under Norwegian GAAP for the 4th Quarter and Full Year 2003.”

P E T R O L E U M G E O - S E R V I C E S

Net Book Value of Library by Year of Completion

0

20

40

60

80

100

120

140

160

1995

1996

1997

1998

1999

2000

2001

2002

2003

In P

roce

ss

Africa Midle-East Europe GoM Brazil Asia

$ million

P E T R O L E U M G E O - S E R V I C E S

Seismic Fleet Activity in Streamer Months (Marine Geophysical)

0 %

10 %

20 %

30 %

40 %

50 %

60 %

70 %

80 %

90 %

100 %

Q4 02 Q1 03 Q2 03 Q3 03 Q4 03 Total 03

Standby

Yard

Steaming

Contract

MC

Yard stay and steaming no longer capitalized under MC as a result of new accounting policies.