41

Petroleum Retail Market in Pakistan Kalim A. Siddiqui President Petroleum Marketing Byco Petroleum Pakistan Limited (Formerly Bosicor Pakistan Limited) 1

Petroleum Retail Market

in Pakistan

Kalim A. SiddiquiPresident Petroleum Marketing

Byco Petroleum Pakistan Limited

(Formerly Bosicor Pakistan Limited)

1

2

Presentation Outline

• Overview of:

World Economic Outlook

World Oil Scenario

• Overview of:

Pakistan Economic Outlook

Pakistan Oil Scenario

• Overview of Petroleum Retail Market in Pakistan

• Overview of Byco Petroleum Marketing in Pakistan

• Conclusion

World Economic Outlook

3

World Economic Highlights

• Global GDP is expected to grow at 3.4% in 2010.

• The main contribution for growth is coming from developing Asia, with:

- China expected to grow by 9.1% in 2010.

- India forecasted to grow by 7.0% in 2010.

• The OECD is forecast to grow on a much lower level of 1.7%. The US is expected to

contribute the most within the OECD at 2.5% in 2010.

• Growth in 2010 continues to be challenged by following concerns:

- Level of public debt in almost all OECD regions.

- Record high unemployment levels across the globe.

- Government efforts in China to prevent the economy from overheating.

4Source : OPEC Oil Market Report – Jan’2010OECD is Organization for Economic Cooperation and Development

5

3.00

4.80

2.20

2.70

3.80

4.90 4.70

5.30 5.20

3.10

3.40

-

1.00

2.00

3.00

4.00

5.00

6.00

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010p

GD

P G

row

th r

ate

Source : CIA World Factbook

World Real GDP Growth Rate

World Oil Scenario

6

7

World Oil Statistics - 2009

• Oil Production: 85.43 million bbl/d

• Oil Consumption : 85.98 million bbl/d

• Oil Exports: 66.13 million bbl/day

• Oil Imports: 66.68 million bbl/day

• Oil - proved reserves: 1.343 trillion bbl/day

Source : CIA World Fact Book

8

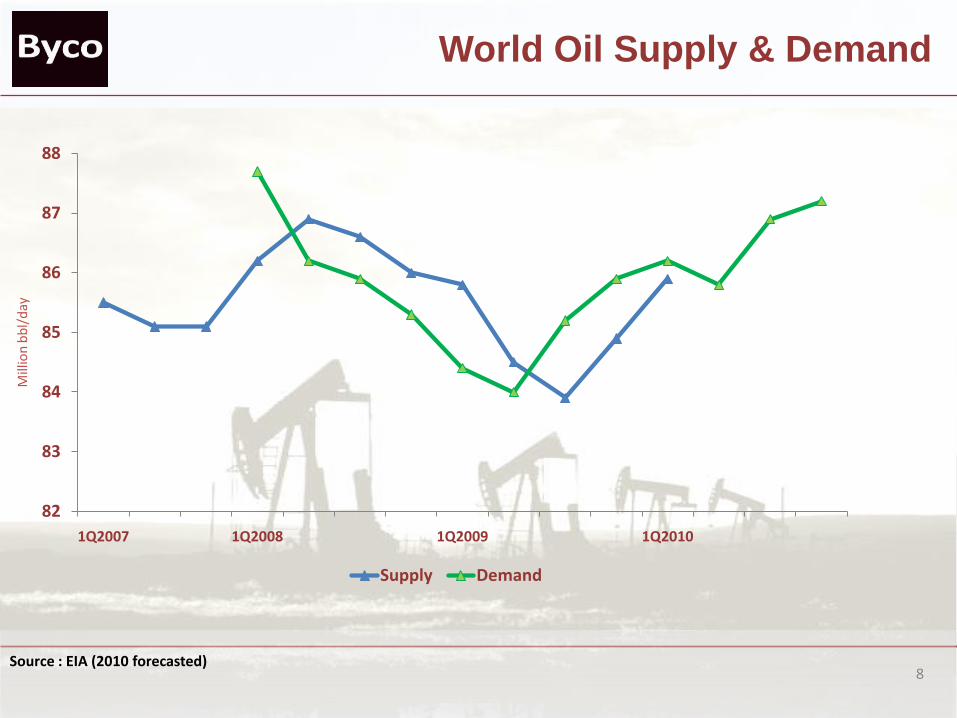

World Oil Supply & Demand

Source : EIA (2010 forecasted)

82

83

84

85

86

87

88

1Q2007 1Q2008 1Q2009 1Q2010

Supply Demand

Mill

ion

bb

l/d

ay

Crude Oil Price Trend

Source : EIA USAOPEC

9

0

20

40

60

80

100

120

140

160F

eb

-95

Ju

n-9

5

Oct-

95

Feb

-96

Ju

n-9

6

Oct-

96

Feb

-97

Ju

n-9

7

Oct-

97

Feb

-98

Ju

n-9

8

Oct-

98

Feb

-99

Ju

n-9

9

Oct-

99

Feb

-00

Ju

n-0

0

Oct-

00

Feb

-01

Ju

n-0

1

Oct-

01

Feb

-02

Ju

n-0

2

Oct-

02

Feb

-03

Ju

n-0

3

Oct-

03

Feb

-04

Ju

n-0

4

Oct-

04

Feb

-05

Ju

n-0

5

Oct-

05

Fe

b-0

6

Ju

n-0

6

Oct-

06

Feb

-07

Ju

n-0

7

Oct-

07

Feb

-08

Ju

n-0

8

Oct-

08

Feb

-09

Ju

n-0

9

Oct-

09

Feb

-10

US

$/B

BL

WTI North Brent OPEC

Global Refining Capacity

Source : ENI World Oil Gas Review

80.1

81.5 81.3 81.482.0

82.3

82.8

85.3 85.4 85.5

87.2

76.0

78.0

80.0

82.0

84.0

86.0

88.0

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Mill

ion

bar

rels

pe

r d

ay

10

Global Energy Mix For 2009

Source : EIA

35.8%

26.9%

23.4%

8.0%5.8%

Liquids Coal Gas Renewables Nuclear Total

Share 35.8% 27.0% 23.4% 8.1% 5.7% 100.0%

Volume (MnToe)

4,421 3,341 2,889 1,005 703 12,359

11

12

3%10%

46%6%

35%

Global Oil Consumption in 2009

Agriculture Industry Transportation Residential All Other*Total

Consumption 3% 10% 46% 6% 35% 100%

Source : OPEC Market Review Dec 2009* All Other may include Electricity generation, Non-energy uses, Commercial uses, etc

Pakistan Economic Outlook

13

Pakistan Real GDP Growth RateG

DP

Gro

wth

rat

e

Source : CIA World Factbook ,International Monetary Fund

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

2003 2004 2005 2006 2007 2008 2009 2010 p

14

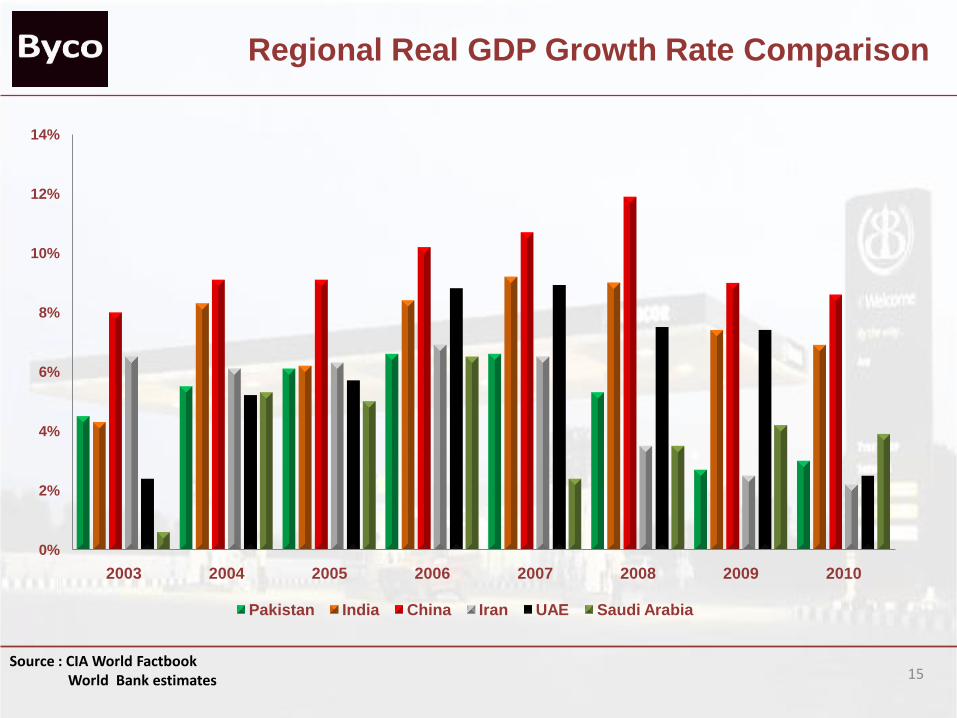

Regional Real GDP Growth Rate Comparison

Source : CIA World FactbookWorld Bank estimates 15

0%

2%

4%

6%

8%

10%

12%

14%

2003 2004 2005 2006 2007 2008 2009 2010

Pakistan India China Iran UAE Saudi Arabia

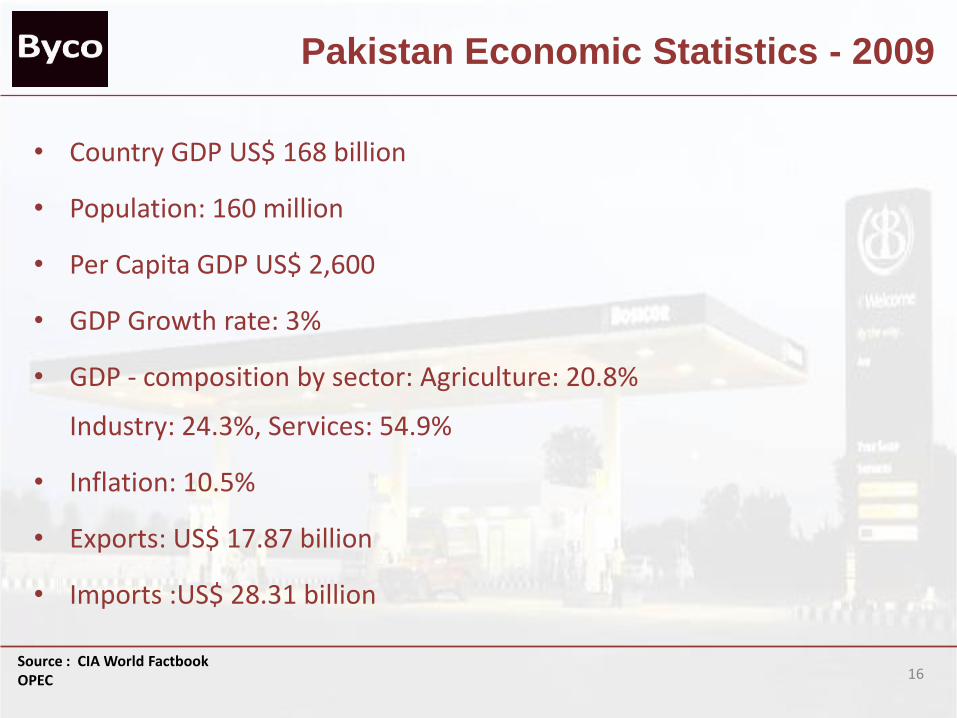

Pakistan Economic Statistics - 2009

• Country GDP US$ 168 billion

• Population: 160 million

• Per Capita GDP US$ 2,600

• GDP Growth rate: 3%

• GDP - composition by sector: Agriculture: 20.8%

Industry: 24.3%, Services: 54.9%

• Inflation: 10.5%

• Exports: US$ 17.87 billion

• Imports :US$ 28.31 billion

Source : CIA World FactbookOPEC 16

Major Industries, Trading Partners & Export Items

• Major Industries–Textile, Sugar, Vegetable Oils,

–Agricultural products, Cement,

–Fertilizers, Steel, Chemicals,

–Sporting goods & carpets

• Major Trading Partners–US, Japan, Germany, China, EU

–UK, Saudi Arabia & UAE

• Major Exports– Oils Seeds, Vegetables, Cotton, Coal, Fertilizer, Telecom equipment, Textile,

Cotton, Rice, Medical instruments, Sporting goods.

17

Pakistan Oil Scenario

18

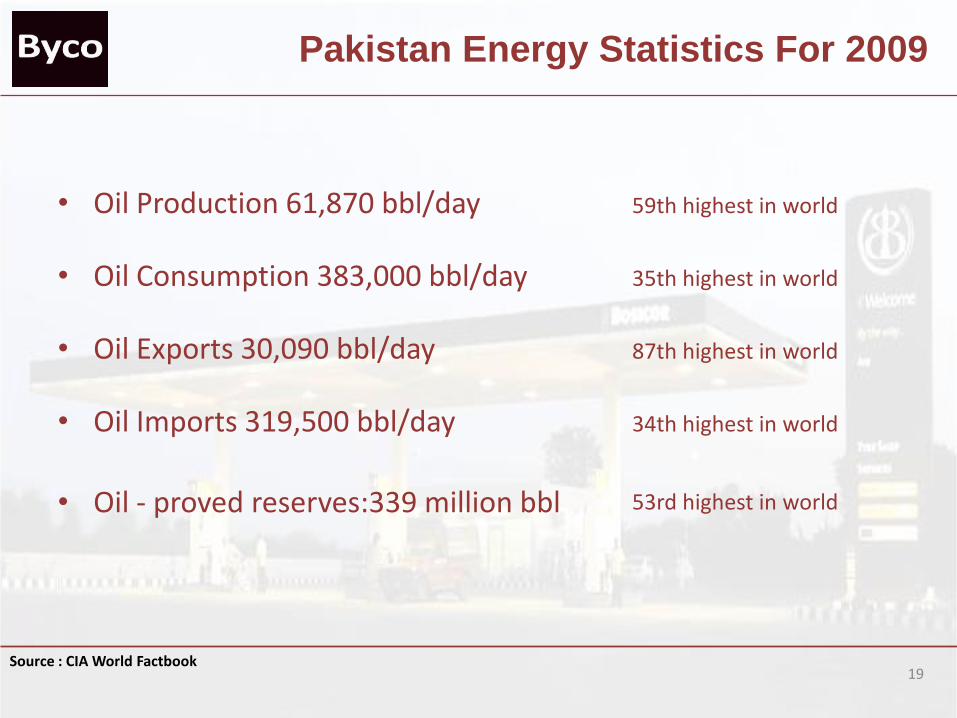

Pakistan Energy Statistics For 2009

• Oil Production 61,870 bbl/day 59th highest in world

• Oil Consumption 383,000 bbl/day 35th highest in world

• Oil Exports 30,090 bbl/day 87th highest in world

• Oil Imports 319,500 bbl/day 34th highest in world

• Oil - proved reserves:339 million bbl 53rd highest in world

Source : CIA World Factbook19

Pakistan Energy Statistics For 2009

• Natural gas production:37.5 billion cu m 23rd highest in world

• Natural gas consumption:37.5 billion cu m 21st highest in world

• Natural gas proved reserves: 885.3 billion cu m 26th highest in world

• Coal reserves more then 185bn tons 04th highest in world

Source : CIA World Factbook20

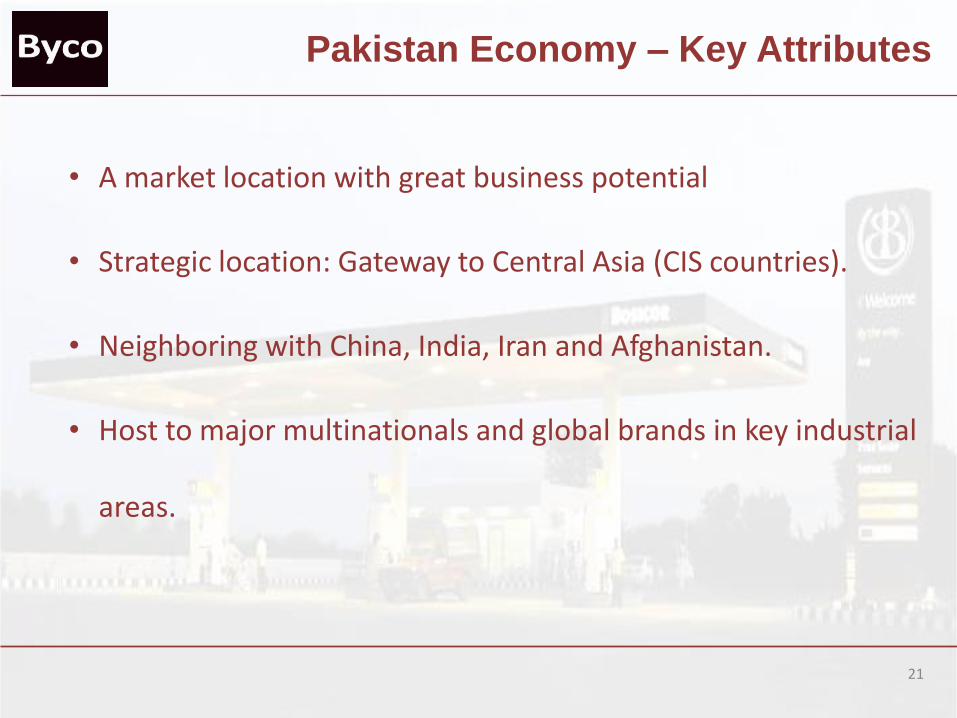

Pakistan Economy – Key Attributes

• A market location with great business potential

• Strategic location: Gateway to Central Asia (CIS countries).

• Neighboring with China, India, Iran and Afghanistan.

• Host to major multinationals and global brands in key industrial

areas.

21

Pakistan Economy – Key Attributes

• High growth areas are education & training, agribusiness

health & medical, oil & gas, building & construction,

multilateral Projects (ADB-WB), information, communication &

telecom, defense & aviation.

• Economy still recovering from oil price inflation and global

downturn.

• Infrastructure development still under process in many areas.

22

Pakistan Economy – Key Attributes

• Nascent democratic /political setup and security concerns

• Proven investment potential during the past few years.

• Promising prospects as region is showing good economic

recovery.

• Untapped potential of natural resources and alternative

energy avenues.

23

24

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

1998-99 1999-00 2000-01 2001-02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-2009 2009-10

Vo

lum

e in

Mn

MT

Year 1998-99 1999-00 2000-01 2001-02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-2009 2009-2010

Consumption (MnMT)

16.9 18.1 18.1 17.4 17.8 15.4 15.5 14.9 17.1 18.5 18.8 20

Petroleum Products Consumption

Source : OCAC

Infrastructure

Source : OCAC

MHKGAT

MCH

RWP

QTA

TJB

KHI

SKP

GWD

VHR

CTL

JGT

CPI

RefineriesSouth NRL, PRL, BPPLCentral PARCONorth ARL

MFM

KMK

WOP

DEPOT

REFINERY

25

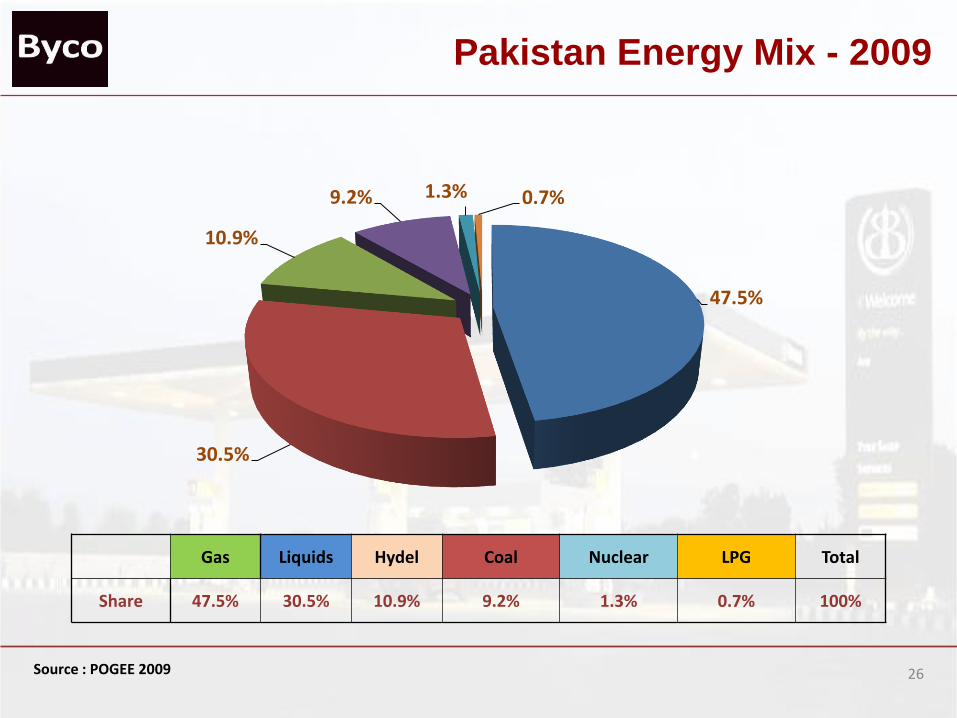

Pakistan Energy Mix - 2009

Source : POGEE 2009

47.5%

30.5%

10.9%

9.2% 1.3% 0.7%

Gas Liquids Hydel Coal Nuclear LPG Total

Share 47.5% 30.5% 10.9% 9.2% 1.3% 0.7% 100%

26

27

Petroleum Retail Market in Pakistan

Downstream Oil Industry

• Annual sales of US$ 11.8 billion.

• Direct employment of over 100,000 people.

• Indirect employment (transport sector) of another 24,000

persons.

• Capital investment of over US$ 0.36 billion over last 5 years.

• Annual generation of taxes around US$ 2.37 billion.

• Progressive IT infrastructure.

28Source : OCAC, HDIP, Pakistan Energy Outlook

Downstream Oil Industry

• Skill sets ranging from Technical, IT, Finance, Sales, Marketing

& HR.

• Pakistan has the largest no. of CNG vehicles in the world (2.2

million)

• CNG Dispensing Facility 2,941 stations. Largest in the world.

29Source : OCAC, HDIP, Pakistan Energy Outlook

Industry Players

30

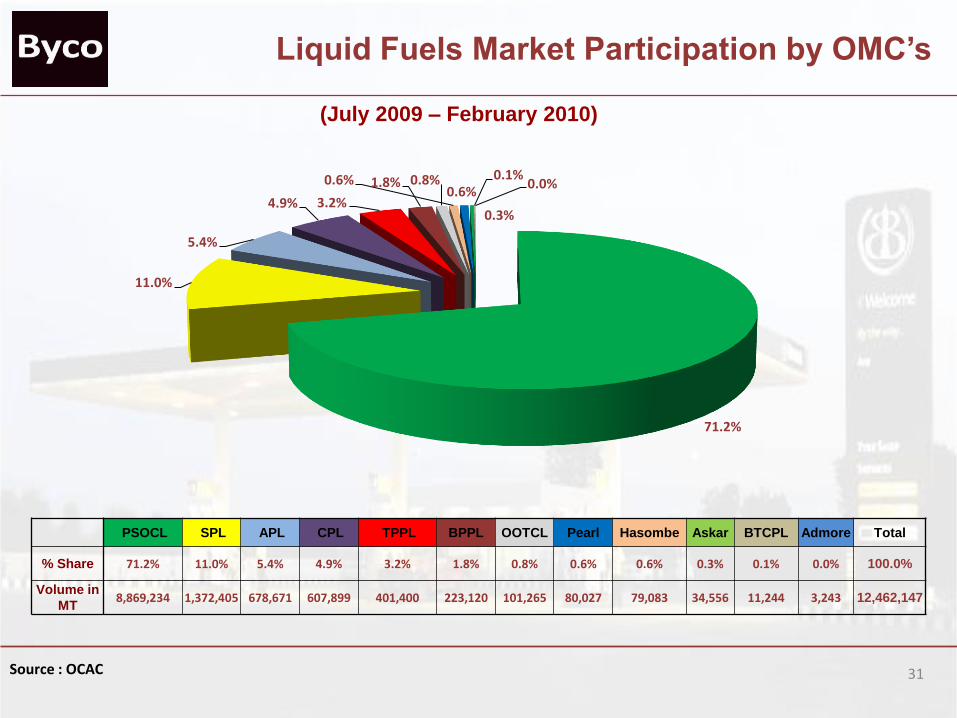

(July 2009 – February 2010)

Source : OCAC 31

Liquid Fuels Market Participation by OMC’s

71.2%

11.0%

5.4%

4.9% 3.2%

1.8% 0.8%0.6%0.6%

0.3%

0.1%0.0%

PSOCL SPL APL CPL TPPL BPPL OOTCL Pearl Hasombe Askar BTCPL Admore Total

% Share 71.2% 11.0% 5.4% 4.9% 3.2% 1.8% 0.8% 0.6% 0.6% 0.3% 0.1% 0.0% 100.0%

Volume in

MT8,869,234 1,372,405 678,671 607,899 401,400 223,120 101,265 80,027 79,083 34,556 11,244 3,243 12,462,147

Source : Corporate websites

Retail Outlets Market Participation by Company

32

55.8%

14.2%

9.2%

6.2%

4.1%3.1% 3.3%

1.9% 1.1%0.6%

0.6%

PSO SPL COPL Admore APL TPPL Askar Hascol BPPL OOTCL BTCPL TOTAL

Share 55.8% 14.2% 9.2% 6.2% 4.1% 3.1% 3.3% 1.9% 1.1% 0.6% 0.6% 100.0%

No. Of Outlets 3,620 922 598 401 265 200 213 120 73 38 38 6,488

Retail Fuel Industry Trends

• Non Fuel activities are growing fast.

• Stiff competition on retail sites development.

• Enhanced branding activities.

• Customer more demanding on product quality and

forecourt services.

• Growing use of technology and innovation to provide

products and services.

33

Byco Petroleum Pakistan Limited

34

35

• Current refinery capacity 30,000 bbl/day

• Upcoming refinery capacity 120,000 bbl/day

• Combined refining capacity 150,000 bbl/ day

• Will be the largest refining complex in Pakistan after

commissioning of upcoming refinery

• Plan to have the first and largest petrochemical facility for the

production of aromatics

Byco’s Petroleum Marketing Business

Emerging Energy leader

36

• Aggressive expansion strategy for Petroleum Marketing to become

a major player

• Developing storage / product handling infrastructure.

• Plan astronomical growth in retail network

• Plan to introduce LPG dispensing at our retail outlets

• New brand identity to be launched shortly.

Byco’s Petroleum Marketing Business

Emerging Energy leader

37

• Plan to develop state of the art NFR facilities at our retail outlets

through the provision of the following facilities:

• ATM Services

• C-stores

• Fast food franchises

• Business Centers

• Plan to introduce Byco branded lubricants for automotive and

industrial segments.

Byco’s Petroleum Marketing Business

Emerging Energy leader

Progressive Commissioning of Retail Outlets

38

4 46 7 8

11 1214

16

20

2832

32 3235 36 37 37 37 37 37 38

50 50 5052 52 53 53

56

66

73

0

6

12

18

24

30

36

42

48

54

60

66

72

Aug-0

7

Sep-0

7

Oct-

07

Nov-0

7

Dec-0

7

Jan-0

8

Feb-0

8

Mar-

08

Apr-

08

May-0

8

Jun-0

8

Jul-

08

Aug-0

8

Sep-0

8

Oct-

08

Nov-0

8

Dec-0

8

Jan-0

9

Feb-0

9

Mar-

09

Apr-

09

May-0

9

Jun-0

9

Jul-

09

Aug-0

9

Sep-0

9

Oct-

09

Nov-0

9

Dec-0

9

Jan-1

0

Feb-1

0

Mar-

10

Num

ber

Of

Sit

es

39

Current Rank is 6th

Progressive Growth in Liquid Fuels Market Share

Rank in 2007 was 11th

0.01%

0.88%

1.42%

2.64%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

Jul-

07

Au

g-0

7

Sep

-07

Oct

-07

No

v-0

7

De

c-0

7

Jan

-08

Feb

-08

Mar

-08

Ap

r-0

8

May

-08

Jun

-08

Jul-

08

Au

g-0

8

Sep

-08

Oct

-08

No

v-0

8

De

c-0

8

Jan

-09

Feb

-09

Mar

-09

Ap

r-0

9

May

-09

Jun

-09

Jul-

09

Au

g-0

9

Sep

-09

Oct

-09

No

v-0

9

De

c-0

9

Jan

-10

Feb

-10

Share

40

• Petroleum retail market in Pakistan is growing at a rapid pace.

• This segment Offers lucrative business opportunities for investors

and vendors.

• Petroleum retail segment is dynamic and is receptive to

technological and service innovation in alignment with the

international market.

• NFR activities are expected to increase in this segment in the

coming years.

Conclusion

41

THANK YOU