28

PFC Energy North American Onshore Service September 2012

PFC Energy North American Onshore ServiceSeptember 2012

Thinking About Unconventional Resources

Chickens48 MMtons

Sheep and Goats10 MM

Cows520 MMtons 48 MMtons105 MMtons

Presentation Name | © PFC Energy | Page 3Ⓒ PFC Energy 2012

Question 1: What About Ants? (Yes, Ants)

What is the total estimated biomass of all the ants in the world, in kilotons?

a) 25

b) 75b) 75

c) 600

d) 5,000

Presentation Name | © PFC Energy | Page 4

Thinking About Unconventional Resources

Chickens48 MMtons

Sheep and Goats10 MM

Cows520 MMtons 48 MMtons105 MMtons

AntsAnts5,000 MMtons

Hydrocarbons are naturally distributed such that difficult and expensive

Presentation Name | © PFC Energy | Page 5

Hydrocarbons are naturally distributed such that difficult and expensive resources are much larger than easy and cheap oil and gas.

Ⓒ PFC Energy 2012

Graphic courtesy of Steve Sonnenberg, Colorado School of Mines

Technology Has Evolved to Overcome Energy Inefficiency

The Problem with Ants (and Unconventional Resources):If you pick them up and peat them one at a time, energy output is

The Solution

output is greater than input.

Horizontal Drilling

Presentation Name | © PFC Energy | Page 6Ⓒ PFC Energy 2012

We Are Getting After It…

Unconventionals (shale, tight, and CBM) have come to dominate new source production

80%

90%

100%Contribution to Total Peak Output from New Wells

50%

60%

70%

80%

20%

30%

40%

50%

0%

10%

20%

an-0

1

ul-0

1

an-0

2

ul-0

2

an-0

3

ul-0

3

an-0

4

ul-0

4

an-0

5

ul-0

5

an-0

6

ul-0

6

an-0

7

ul-0

7

an-0

8

ul-0

8

an-0

9

ul-0

9

an-1

0

ul-1

0

an-1

1

ul-1

1

Presentation Name | © PFC Energy | Page 7

Ja J Ja J Ja J Ja J J a J J a J J a J J a J J a J J a J J a J

Unconventional Conventional

Source: PFC Energy, DrillingInfo, RigData, state databases

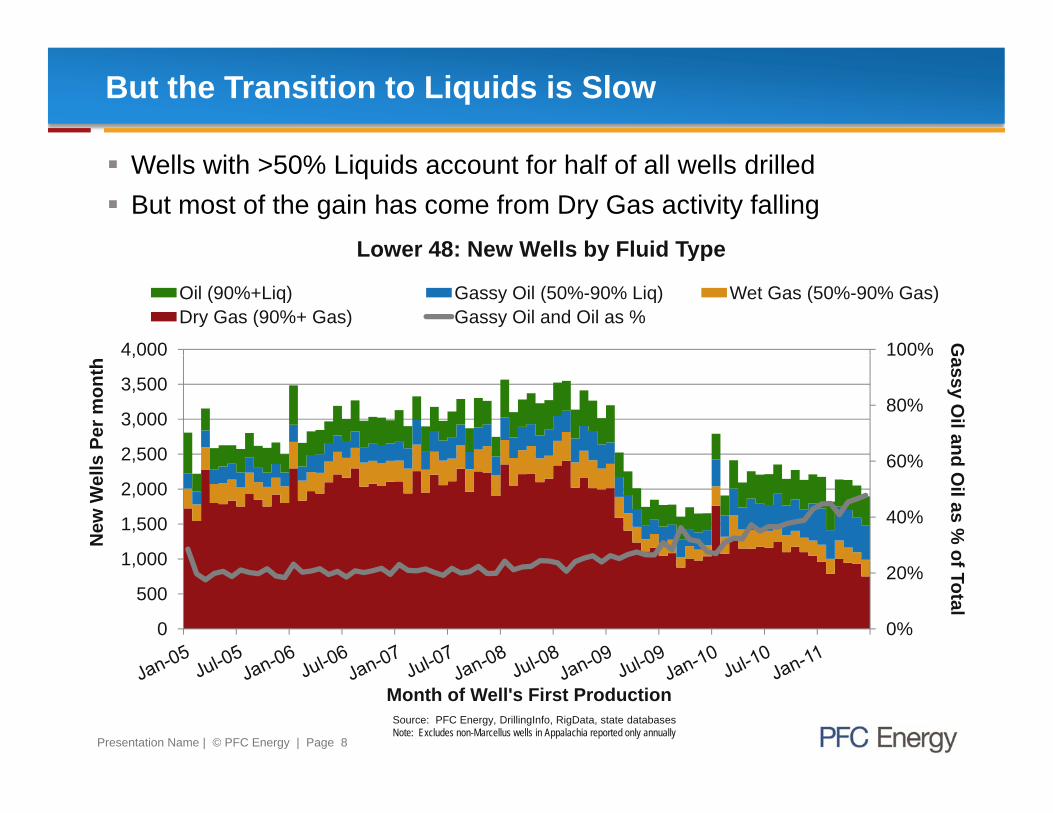

But the Transition to Liquids is Slow

Wells with >50% Liquids account for half of all wells drilled But most of the gain has come from Dry Gas activity falling

Lower 48: New Wells by Fluid Type

100%4,000

G

Lower 48: New Wells by Fluid Type

Oil (90%+Liq) Gassy Oil (50%-90% Liq) Wet Gas (50%-90% Gas)Dry Gas (90%+ Gas) Gassy Oil and Oil as %

60%

80%

100%

2 500

3,000

3,500

4,000

Gassy O

il ands Pe

r mon

th

40%

60%

1 000

1,500

2,000

2,500 d Oil as %

oNew

Wel

ls

0%

20%

0

500

1,000 f Total

Presentation Name | © PFC Energy | Page 8

Month of Well's First ProductionSource: PFC Energy, DrillingInfo, RigData, state databasesNote: Excludes non-Marcellus wells in Appalachia reported only annually

Question 2: So Is It Working?

Which countries has the combination of Bakken + Eagleford surpassed in terms of total wellhead liquids production?

a) Ecuador (OPEC member)a) Ecuador (OPEC member)

b) UK

c) Indonesia

d) All of the above

e) None of the abovee) None of the above

Presentation Name | © PFC Energy | Page 9

Oil Growth Is World Scale

Hyperactivity growing play-level production rapidly Expansion of wellhead production out of synch with mid-stream and downstream,

leading to basis blowouts and local surpluses

UK

1,200

1,400

uctio

n in

Bakken + Eagleford Wellhead Liquids Production

UK

Ecuador

Indonesia

600

800

1,000

dens

ate

Prod

um

bd

Ecuador

-

200

400

rude

and

Can

d

Shale oil production is still small from a global view but forms a major part of

Jan-

07A

pr-0

7Ju

l-07

Oct

-07

Jan-

08A

pr-0

8Ju

l-08

Oct

-08

Jan-

09A

pr-0

9Ju

l-09

Oct

-09

Jan-

10A

pr-1

0Ju

l-10

Oct

-10

Jan-

11A

pr-1

1Ju

l-11

Oct

-11

Jan-

12A

pr-1

2Cr

Presentation Name | © PFC Energy | Page 10

Shale oil production is still small from a global view but forms a major part of global new source supply.

Data: PFC Energy, HPDI, State Data

The Gas Conundrum

Since 2008, gas supply has climbed considerably, even in the face of enormous a declining rig count and price level. This has led to a view of permanent bearishness.

70,000

16.00

18.00

Gas Prod in mmcfd

$/MMBtu or100 Rigs US Nat Gas Production 3-Yr Strip BHI Gas Rigs

Correlation Breakdown: B ll M k t

Correlation Breakdown:

60,000

65,000

10 00

12.00

14.00

Bull Market Bear Market

50,000

55,000

6.00

8.00

10.00

40,000

45,000

0.00

2.00

4.00

00 00 00 01 01 02 02 02 03 03 04 04 05 05 05 06 06 07 07 07 08 08 09 09 10 10 10 11 11 12

Presentation Name | © PFC Energy | Page 11

1/1/

200

6/1/

200

11/1

/200

4/1/

200

9/1/

200

2/1/

200

7/1/

200

12/1

/200

5/1/

200

10/1

/200

3/1/

200

8/1/

200

1/1/

200

6/1/

200

11/1

/200

4/1/

200

9/1/

200

2/1/

200

7/1/

200

12/1

/200

5/1/

200

10/1

/200

3/1/

200

8/1/

200

1/1/

206/

1/20

11/1

/20

4/1/

209/

1/20

2/1/

20

Source: PFC Energy, DrillingInfo, RigData, state databases

Question 3: The Source of the Gas “Problem”

Gas production in the US has been incredibly resilient even though prices and rig activity have continued to fall dramatically. This is due to many reasons but the single most important one in 2011 was:many reasons, but the single most important one in 2011 was:

a) Impressive high-grading of drilling locations by industry

b) The wave of associated gas being produced in the stampede to liquids.

) W ll d ti it i d t b tt ll t h l d l tic) Well productivity gains due to better well technology and completion techniques

Presentation Name | © PFC Energy | Page 12

We’re Skewed!

Plays are not created equally. Thus, the NA supply system is composed of a relatively small number of highly productive wells and long tail of very small contributors– Stop looking at the gas rig count simplistically

What matters is the trend within the categories– What matters is the trend within the categories

4,500

5,000

WellCount NewWellsbyAbsoluteCategory

180%

200%

NewWellsbyCategoryIndexedtoPeak

2 500

3,000

3,500

4,000

100%

120%

140%

160%Peak of Drilling

1,000

1,500

2,000

2,500

40%

60%

80%

100%

‐

500

2001Q1

2001Q3

2002Q1

2002Q3

2003Q1

2003Q3

2004Q1

2004Q3

2005Q1

2005Q3

2006Q1

2006Q3

2007Q1

2007Q3

2008Q1

2008Q3

2009Q1

2009Q3

2010Q1

2010Q3

2011Q1

0%

20%

2001Q1

2001Q3

2002Q1

2002Q3

2003Q1

2003Q3

2004Q1

2004Q3

2005Q1

2005Q3

2006Q1

2006Q3

2007Q1

2007Q3

2008Q1

2008Q3

2009Q1

2009Q3

2010Q1

2010Q3

2011Q1

Presentation Name | © PFC Energy | Page 13

Data Source: PFC Energy; State oil and gas databases; Drillinginfo Excludes GOM Deepwater, CBM & non-Marcellus Appalachian wells from states with annual/quarterly reporting

Focus on What MattersAnnual “Base” and “Wedge”

While focus is on emerging plays, well-established plays are the backbone of new source gas production

Relatively few plays are operators can

Growth

Maintenance Annual Wedgeol

ume

gCombine to Form Production

Relatively few plays are operators can move the needle for the US Base

Wedge

Time

Vo

Jan Dec

Haynesville Shale28%

Uinta Tight Gas2%

GOM Deepwater1%

All Oth Pl

2011 Gas Wedge By Play

CHESAPEAKE13%

EXXONMOBIL6%

2011 Gas Wedge by Operator

Pi Ti ht G

GOM Shelf3%

Cotton Valley2%

Misc TX & LA Gulf Coast

2%

All Other Plays16%

ENCANA6%

EXCOSAMSON

OTHER30%

Marcellus Shale13%

Eagleford ShaleFayetteville Shale

6%

Pinedale/Jonah4%

Anadarko Wash Plays4%

Piceance Tight Gas3%

5%

ANADARKO5%

BHP4%RANGE

RESOURCESWILLIAMS

EL PASO1%

APACHE1%

CHEVRON1%

SAMSON1%

Presentation Name | © PFC Energy | Page 15

Barnett Shale10%

g6%

SOUTHWESTERN5%

DEVON4%

SHELL3%

EOG3%CABOT

2%

QEP2%

ULTRA Petroleum

2%TALISMAN

2%

RESOURCES2%

WILLIAMS2%

Source: PFC Energy-Guggenheim, DrillingInfo, RigData, state databases

What Will Happen As the Plays Evolve?

It is a mistake to treat plays as static; they pass through distinct life stages Each stage requires a different set of skills and resources to succeed

O

ily TuscaloosaBakkenNiobrara

WolfcampMississippian

Monterey

id T

ype>

Granite Wash

Eagleford OilUticaBone Spring

Smackover

<

Flui Granite Wash

BarnettEagleford Pinedale/

Prove It(Infancy)

Optimize It(Adolescence)

Standardize It(Adulthood)

Re-invent It(2nd Career)

Gas

sy Barnett

FayettevilleHaynesville

EaglefordGas Pinedale/

JonahMarcellus

Presentation Name | © PFC Energy | Page 16

Life Stages of Unconventional Plays (Infancy) (Adolescence) (Adulthood) (2nd Career)

What Matters for the Future of a Particular Play?

Each play is unique and unfolds in three dimensions:1. Spatially – How does the play develop geographically and where are the

sweet spots?sweet spots?

2. Distributionally – How good is good?

3. Temporally – How does the play change over time?

L t’ t k “li ” l k t th l t h h f th t Let’s take a “live” look at three plays to show each of these aspects of the play.

Presentation Name | © PFC Energy | Page 17

Quality Map of the Bakken

Presentation Name | © PFC Energy | Page 18

Well productivity is not randomly distributed, but rather clusters in sweet spots.

Question 4: How Far Ahead?

Looking at relative peak per lateral foot productivity of all wells in the Bakken, the most productive quintile is how much better than the bottom quintile?bottom quintile?

a) 10% better

b) 100% better (twice as productive)

) 1 000% (10 d ti )c) 1,000% (10x as productive)

d) 10,000% (100x as productive)

Presentation Name | © PFC Energy | Page 19

Plays Exhibit Widely Variable Results

The inherent variability of rock productivity is far larger than differences in cost

Presentation Name | © PFC Energy | Page 20

The inherent variability of rock productivity is far larger than differences in cost structures or operational practices.

Question 5: How Fast Are We Learning?

In 2008, EOG's wells in the Bakken exhibited peak month production of about 185 boed/per 1000 lat ft. What was that number in 2011?

a) That was the Stone Age! We've made leaps and bounds since then. 375

b) St d i t h h d it 240b) Steady improvements have pushed it up. 240

c) The more things change, the more they stay the same. 185

d) Going down the drain... 50

Presentation Name | © PFC Energy | Page 21

Engines of Growth in Major Gas Plays Have Hit Limits

The top 5 gas plays all appear to have hit limits to have optimized lateral length and peak the gas extracted per lateral ft of reservoir.

Without these “engines,” growing supply becomes more difficult.Without these engines, growing supply becomes more difficult.

1600

1800

Average Peak Month Production

7000

Average Lateral Length in Ft

2500

Average Peak Month Production per Lat eral Ft

1000

1200

1400

4000

5000

6000

1500

2000

600

800

1000

2000

3000

4000

1000

0

200

400

Q06

Q07

Q08

Q09

Q10

Q11

0

1000

06 07 08 09 10 110

500

Q06

Q07

Q08

Q09

Q10

Q11

Presentation Name | © PFC Energy | Page 22

1Q 1Q 1Q 1Q 1Q 1Q 1Q 1Q 1Q 1Q 1Q 1Q 1 Q 1Q 1Q 1Q 1Q 1Q

Source: PFC Energy, DrillingInfo, State databasesSource: PFC Energy, DrillingInfo, state databases

Eating the Power Bars and Leaving the Popcorn?

EOG Peak Per Lat Ft in the Bakken

Companies rightly seek to exploit the sweet spots first but this leads over time

Presentation Name | © PFC Energy | Page 23

Companies rightly seek to exploit the sweet spots first, but this leads over time to quality degradation in the play unless technology leaps forward.

Question 6: Life in the Basement

No one should be drilling in the Haynesville today. The play is uneconomic.

a) True. Those guys are setting money on fire.

b) F l Thi i th t d ti l i th tb) False. This is the most productive play in the country.

c) Kinda…sorta…it depends.

Presentation Name | © PFC Energy | Page 24

Play Works…for Some

Haynesville Signal-to-Drill is a better indicator than spot prices of the returns seen by an E&P company.

1st Quintile wells modestly profitable, but most locations play are far from being economic. Prices would need to rise to induce significant new drilling.

Presentation Name | © PFC Energy | Page 25Source: NYMEX, PFC Energy, DrillingInfo, State databases

Key Takeaways

1. Unconventional oil and gas are down the resource pyramid -- much larger than conventional resources, but difficult and expensive

2 Oil and gas are booming and the results are world scale2. Oil and gas are booming, and the results are world-scale3. The North American supply system exhibits enormous skew both

between and within plays4. Plays pass through a number of life stages, and the main

contributors to new source volumes are mature5. Within in an unconventional play, there is enormous, inherent

variability, separating winners from losers: the chess board is set6. Future production gains will have to struggle against

– The petering out of growth accelerants which characterized early stagesg g y g– Sweet spot exhaustion/quality degradation, which may well outpace

technology gains7. We will be drilling these plays for decades, but activity levels and

Presentation Name | © PFC Energy | Page 26

g p y ybreakeven prices will need to rise from here

PFC Energy Locations and Contact Information

ASIA

PFC Energy, Kuala LumpurLevel 27, UBN Tower #21

EUROPE

PFC Energy, France19 rue du Général Foy

NORTH AMERICA

PFC Energy, Washington1300 Connecticut Avenue, NW ,

10 Jalan P. Ramlee50250 Kuala Lumpur, MalaysiaTel +60 3 2172 3400Fax +60 3 2072 3599

PFC E Chi

y75008 Paris, France Tel +33 1 4770 2900Fax +33 1 4770 5905

,Suite 800Washington, DC 20036, USATel +1 202 872 1199 Fax +1 202 872 1219

PFC E H t PFC Energy, China89 Jianguo RoadChina Central Place # 4-1602 Chaoyang District, Beijing 100025, ChinaTel +86 10 6530 7010Fax +86 10 6530 5093

PFC Energy, Houston2727 Allen Parkway, Suite 1300Houston, Texas 77019, USA Tel +1 713 622 4447 Fax +1 713 622 4448

PFC Energy, Singapore9 Temasek Boulevard#09-01 Suntec Tower TwoSingapore 038989Tel +65 6407 1440Fax +65 6407 1501

www pfcenergy com | info@pfcenergy com

Presentation Name | © PFC Energy | Page 27

www.pfcenergy.com | [email protected]