50

Strategic Advisors in Global Energy PFC Energy’s Global Crude Oil and Natural Gas Liquids Supply Forecast September 2004

Strategic Advisors in Global Energy

PFC Energy’s Global Crude Oil and Natural Gas Liquids

Supply Forecast

September 2004

Key Messages

1. The world is not in imminent danger of running out of oil, but certain countries/regions are depleting much faster than others. This will cause a shift in the geographic dominance of production sources.

2. In spite of high oil prices, Non-OPEC production has been stagnant with the notable exception of the FSU. This trend is likely to continue through this decade.

3. Exploration results in the last 10 years (with a few exceptions like Angola, Sudan, Mauritania) have been much less significant than in previous decades. Without a significant reversal of this trend, Non-OPEC production is likely to peak just after 2010 and begin a long term decline.

Key Messages

5. Every year, in every region (including OPEC), the world producesmore oil than it finds. It is only logical to conclude that inevitably this will lead to dwindling supplies.

6. As demand continues to grow beyond 2010 and Non-OPEC production capacity plateaus or falls, OPEC will have an increasing burden to make up the difference resulting in an inevitable increase in dependency on OPEC sources.

7. OPEC production capacity and reserves will suffer from the additional strain and some models suggest that even OPEC will struggle to fill the differential between Non-OPEC supply and global demand beyond 2015-2020.

Non-OPEC Supply ForecastAssumes Exploration Reserve Additions Typical of the Last 15 Years

0

10,000

20,000

30,000

40,000

50,000

60,000

1985

1988

1991

1994

1997

2000

2003

2006

2009

2012

2015

2018

Dai

ly P

rodu

ctio

n (m

bopd

)

Non-OPEC Oil SandsNon-OPEC NGLFSUNon OPEC/Non FSU

This production profile is based on a model which takes into account known discovered oil, historical production, all known (large and small) discoveries that are undeveloped, likely future exploratory drilling, trends in discovery sizes, and decline rates.

The Problem - The Expected Growing Gap Between Global Demand and Global Non-OPEC Supply in the Next Decade

0

20,000

40,000

60,000

80,000

100,000

120,000

198519871989199119931995199719992001200320052007200920112013201520172019

Dai

ly P

rodu

ctio

n (m

bopd

)

0

20,000

40,000

60,000

80,000

100,000

120,000

Non OPECCrude Oil Non-OPEC NGL

Non-OPEC Oil Sands 1.1% Grow th

1.8% Grow th 2.4% Grow th

The Growing Differential Between Non-OPEC Supply Capacity and

Global Demand

Egypt – A Typical Life Cycle for an Oil Producing Country

Total Onshore Wells

0

10

20

30

40

50

60

7019

64

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

Wells

0%

5%

10%

15%

20%

25%

30%

35%

Dry HolesDiscoveriesSmoothed Success Rate

Exploration usually begins with a play concept which if successful (results in oil discoveries) leads to increasing numbers of wells over time –generally speaking the percentage of exploration wells which arediscoveries does not change much over time

Egypt Total Country

0

2,000

4,000

6,000

8,000

10,000

12,000

1953 1963 1973 1983 1993 2003Year Discovered

Cum

ulat

ive

Dis

cove

red

Res

erve

s (m

mbo

)

CUMULATIVE RESERVES DISCOVERED

Typically large reserve growth occurs in the early years with large steps followed by smaller steps and much lower rates of reserve additions in the later years

Total of 6 billion barrels found by the mid 1960s

Total of 9 billion barrels found by the early 1980s

Much lower rates of reserve growth once exploration matures

Egypt – A Typical Life Cycle for an Oil Producing Country

0

100

200

300

400

500

600

700

1950-1970 1970-1980 1980-1990 1990-Present

Mea

n Fi

eld

Size

(mill

ions

of b

arre

ls)

0

10

20

30

40

50

60

70

Num

ber

of N

ew D

isco

veri

es

Mean Field Size Number of Discoveries

In most cases as exploration matures field sizes drop but the numbers of actual discoveries increase – even though there are often more new fields in recent years, the much smaller field sizes has the net effect of much lower rates of reserve additions

Egypt – A Typical Life Cycle for an Oil Producing Country

As reserve additions fall and production rates increase countries evolve from having net a positive annual reserve balance to a negative annual petroleum balance – in the case of Egypt there have been 20 consecutive years where 250 mmbo more oil is produced than discovered every year

0

100

200

300

400

500

600

700

800

900

1000

1950

1953

1956

1959

1962

1965

1968

1971

1974

1977

1980

1983

1986

1989

1992

1995

1998

2001

2004

Dai

ly P

rodu

ctio

n (m

bopd

)

-500

-250

0

250

500

750

1000

1250

1500

1750

2000

Ann

ual B

bls

Dis

c - A

nnua

l Bbl

s Pr

od (m

mbo

)

ProductionOil Disc - Oil Produced3 per. Mov. Avg. (Oil Disc - Oil Produced)

Egypt – A Typical Life Cycle for an Oil Producing Country

0

100

200

300

400

500

600

700

800

900

1000

1950

1954

1958

1962

1966

1970

1974

1978

1982

1986

1990

1994

1998

2002

Dai

ly P

rodu

ctio

n (m

bopd

)

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

Cum

Pro

duct

ion/

Cum

Res

erve

s

Daily Production

Cum Production/Cum Reserves

Once large discoveries are no longer made and production rates increase, depletion levels (percentage of oil discovered that has been produced) accelerate – this depletion history has been mapped for every major oil and most minor producing countries

Growth Plateau Decline

Egypt – A Typical Life Cycle for an Oil Producing Country

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

USA Tunisia

PeruDem Rep

CameroonOther_Eur

EgyptPNG

SyriaNew_Zeal

GabonArgentina

UKColombiaAustralia

NorwayOmanCongo

PakistanYemen

CanadaDenmark

IndiaChina

MalaysiaBrunei

Mexico

Non-OPEC Countries that are Either in Decline or Currently in a Plateau

The above bars show the onset and duration of documented production peaks or plateaus – tracking country life cycle shows an acceleration of the number of countries passing from peak to decline

Countries in the decline phase

Countries in the plateau phase

Onset of Plateau

Duration of Plateau

Onset of Decline

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Papua N

ew Guinea

Camero

onCon

goSyriaPeruOmanEgyp

tColumbia

Norway

GabonTunis

iaYem

en

New Zea

land

Dem R

ep C

ongoArg

entin

aPakis

tan UKAus

tralia

Non-OPEC Countries that are in Decline

The above bars shows the depletion level at the transition from peak/plateau to decline – tracking depletion level is a good way to anticipate the cessation of growth and the onset of decline

Depletion Ranges for Decline

Depletion Ranges for Growth or Plateaus

Average depletion level which corresponds to the

onset of decline – 54%

Transition from Growth

to Decline

Non-OPEC Countries that are in Plateau

The above bars shows the depletion level of several producers which have reached a production plateau – several significant producers are rapidly approaching critical (60 – 65%) depletion levels which typically signal the onset of production declines

0%10%20%30%40%50%60%70%80%90%

100%

Mexico

Brunei

China

Malaysia

Denmark

IndiaDepletion Ranges for Decline

China - Non OPEC Country in Plateau but are Declines Likely in the Near Term?

0

500

1,000

1,500

2,000

2,500

3,000

3,50019

65

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

Dai

ly P

rodu

ctio

n (m

bopd

)

-1500

-1000

-500

0

500

1000

1500

2000

Oil

Dis

cove

red

- Oil

Prod

uced

(mm

bl)

ProductionAnnual Balance3 per. Mov. Avg. (Annual Balance)

0

500

1000

1500

2000

2500

3000

3500

4000

1965

1968

1971

1974

1977

1980

1983

1986

1989

1992

1995

1998

2001

2004

Dai

ly P

rodu

ctio

n (m

bopd

)

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

Cum

Pro

duct

ion/

Cum

Res

erve

s

Daily Production

Cum Production/Cum Reserves

China’s production volumes have exceeded new discovered volumes for all but 4 years since 1975.

China’s depletion level has reached 60% and production levels have gone flat over the last 3 years.

Mexico – Non-OPEC Country in Plateau but are Declines Likely in the Near Term?

0

500

1,000

1,500

2,000

2,500

3,000

3,50019

60

1963

1966

1969

1972

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

Dai

ly P

rodu

ctio

n (m

bopd

)

-2000

-1000

0

1000

2000

3000

4000

5000

Oil

Dis

cove

red

- Oil

Prod

uced

(mm

bl)

0

500

1000

1500

2000

2500

3000

3500

4000

1965

1970

1975

1980

1985

1990

1995

2000

Dai

ly P

rodu

ctio

n (m

bopd

)

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

Cum

Pro

duct

ion/

Cum

Res

erve

s

Daily Production

Cum Production/Cum Reserves

Mexico’s depletion level has reached 50% although production levels have continued to increase over the last few years – based on current rates 60% depletion would likely occur in 2008, however the Mexican Government has stated that absent significant new discoveries in the deepwater GOM, 14% declines are expected to start in 2006.

Mexico’s production volumes have exceeded new discovered volumes for all but 1 year since 1984.

India - Non OPEC Country in Plateau but are Declines Likely in the Near Term?

0

100

200

300

400

500

600

700

800

900

1,00019

65

1968

1971

1974

1977

1980

1983

1986

1989

1992

1995

1998

2001

2004

Dai

ly P

rodu

ctio

n (m

bopd

)

-500

-250

0

250

500

750

1000

1250

1500

1750

2000

Oil

Dis

cove

red

- Oil

Prod

uced

(mm

bl)

0

100

200

300

400

500

600

700

800

1965

1968

1971

1974

1977

1980

1983

1986

1989

1992

1995

1998

2001

2004

Dai

ly P

rodu

ctio

n (m

bopd

)

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

Cum

Pro

duct

ion/

Cum

Res

erve

s

Daily Production

Cum Production/Cum Reserves

India’s production volumes have exceeded new discovered volumes for all but 3 years since 1980.

India’s production levels have been relatively flat since the mid 1990s as depletion levels have continued to increase – current depletion is estimated at 65% which would imply that near term declines should begin unless reserves have been somewhat underestimated.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Maurit

ania

ChadIvo

ry Coas

tThaila

ndSudan

Eq GuineaBraz

ilAngolaViet

namEcu

ador

Non-OPEC, Non-FSU Countries with Production Growth Profiles

The above bars shows the depletion level of several producers which have new discoveries and are considered very likely to increase production – Azerbaijan, Kazakhstan and Russia are also expected to have growth profiles

Depletion Ranges for Decline

Historical Crude Production (Excluding OPEC, FSU, Natural Gas Liquids and Canadian Oil Sands)

0

5000

10000

15000

20000

25000

30000

35000

1965

1968

1971

1974

1977

1980

1983

1986

1989

1992

1995

1998

2001

2004

Dai

ly P

rodu

ctio

n (m

bopd

)

Latin AmericaWest AFricaMiddle EastAsiaMexicoEuropeCanadaUSA

Several key producing regions have reached or exceeded the critical depletion point of 50-60% which typically marks the onset of production decline. It is worth noting that production gains from large new projects have not increased the aggregate production capacity of these regions for about 8 years.

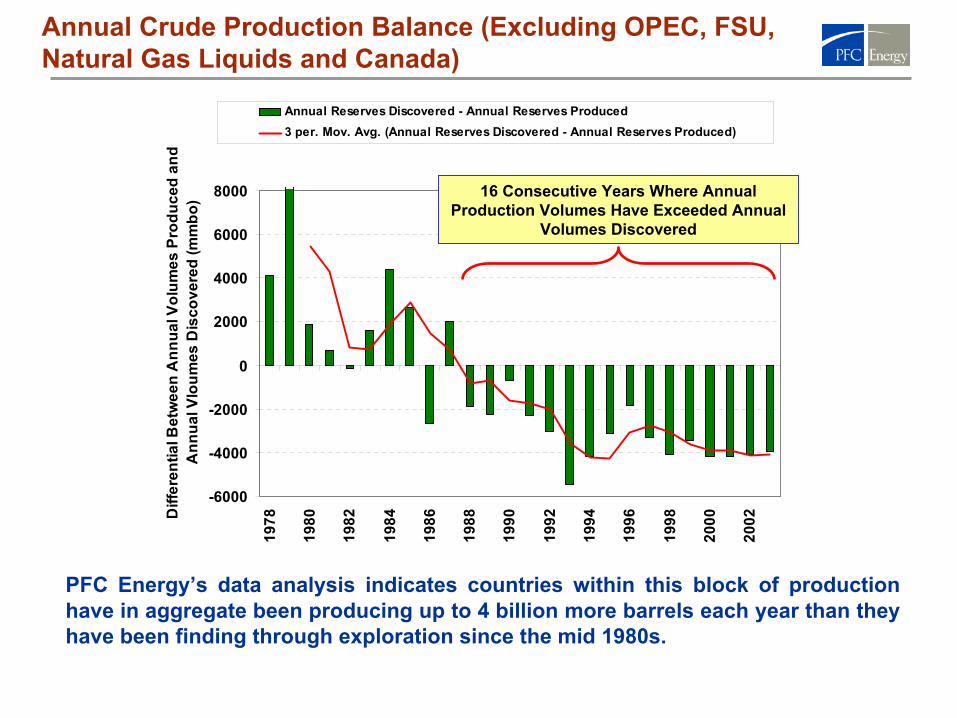

Annual Crude Production Balance (Excluding OPEC, FSU, Natural Gas Liquids and Canada)

-6000

-4000

-2000

0

2000

4000

6000

8000

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002D

iffer

entia

l Bet

wee

n A

nnua

l Vol

umes

Pro

duce

d an

d A

nnua

l Vlo

umes

Dis

cove

red

(mm

bo)

Annual Reserves Discovered - Annual Reserves Produced3 per. Mov. Avg. (Annual Reserves Discovered - Annual Reserves Produced)

PFC Energy’s data analysis indicates countries within this block of production have in aggregate been producing up to 4 billion more barrels each year than they have been finding through exploration since the mid 1980s.

16 Consecutive Years Where Annual Production Volumes Have Exceeded Annual

Volumes Discovered

Egypt – Modeling Different Reserve Categories

0

100

200

300

400

500

600

700

800

900

100019

50

1954

1958

1962

1966

1970

1974

1978

1982

1986

1990

1994

1998

2002

2006

2010

2014

2018

2022

2026

2030

Dai

ly P

rodu

ctio

n (m

bopd

)

Exploration

PUDs

New Source Projects

Base Production

Actual Production

0

100

200

300

400

500

600

700

800

900

1000

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

2020

2025

2030

Dai

ly P

rodu

ctio

n (m

bopd

)

P90 Forecast

P10 Forecast

P25 Forecast

P50 Forecast

P75 Forecast

Actual Production

With Exploration

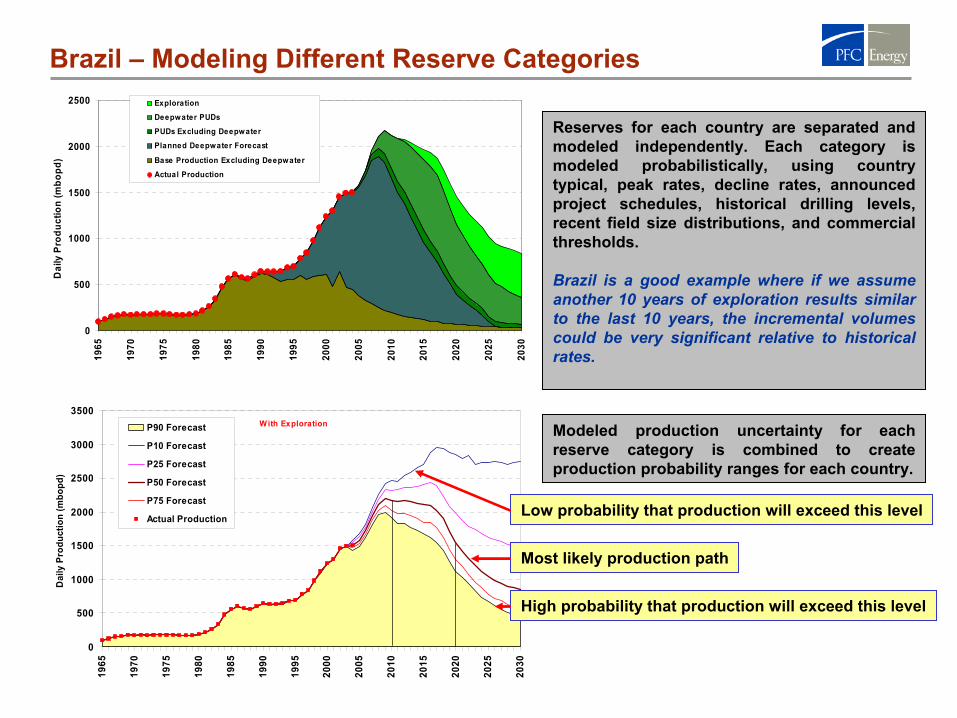

Reserves for each country are separated and modeled independently. Each category is modeled probabilistically, using country typical, peak rates, decline rates, announced project schedules, historical drilling levels, recent field size distributions, and commercial thresholds.

Egypt is a good example where if we assume another 10 years of exploration results similar to the last 10 years, the incremental volumes are small relative to historical rates.

Modeled production uncertainty for each reserve category is combined to create production probability ranges for each country.

High probability that production will exceed this level

Low probability that production will exceed this level

Most likely production path

0

500

1000

1500

2000

2500

3000

3500

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

2020

2025

2030

Dai

ly P

rodu

ctio

n (m

bopd

)

P90 Forecast

P10 Forecast

P25 Forecast

P50 Forecast

P75 Forecast

Actual Production

With Exploration

Brazil – Modeling Different Reserve Categories

Reserves for each country are separated and modeled independently. Each category is modeled probabilistically, using country typical, peak rates, decline rates, announced project schedules, historical drilling levels, recent field size distributions, and commercial thresholds.

Brazil is a good example where if we assume another 10 years of exploration results similar to the last 10 years, the incremental volumes could be very significant relative to historical rates.

Modeled production uncertainty for each reserve category is combined to create production probability ranges for each country.

High probability that production will exceed this level

Low probability that production will exceed this level

Most likely production path

0

500

1000

1500

2000

250019

65

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

2020

2025

2030

Dai

ly P

rodu

ctio

n (m

bopd

)

Exploration

Deepwater PUDs

PUDs Excluding Deepwater

Planned Deepwater Forecast

Base Production Excluding Deepwater

Actual Production

Global: Non-OPEC Non FSU Crude Supply Forecast (With Exploration)

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

2020

Dai

ly C

rude

Pro

duct

ion

(mb/

d)

P10e Forecast

P25e Forecast

P50e Forecast

P75e Forecast

P90e Forecast

Crude Oil Production Forecast with an Exploration Component (Excluding OPEC, Natural Gas Liquids, FSU, and Canadian Oil Sands)

PFC Energy’s models suggest that the flat trend noted since the late 1990s is very likely to continue through the end of this decade with production declines beginning in the early part of the next decade – going forward it is possible that for a few years production could increase before declines start in the next decade or it is possible that production could start a gentle decline sooner

Possible production path if exploration results and decline rates fall at the more pessimistic end of the scale

Most likely production path

Possible production path if exploration results and decline rates fall at the more optimistic end of the scale

Historical Crude Production (Excluding OPEC, Natural Gas Liquids and Canadian Oil Sands)

Post 1998 Non-OPEC conventional crude oil production growth was largely drivenby growth in the FSU and specifically Russia.

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

1965

1968

1971

1974

1977

1980

1983

1986

1989

1992

1995

1998

2001

2004

Dai

ly P

rodu

ctio

n (m

bopd

)

FSULatin AmericaWest AFricaMiddle EastAsiaMexicoEuropeCanadaUSA

FSU Data incomplete prior to 1985

FSU Crude Oil Production Forecast with Exploration

PFC Energy’s models suggest that FSU production could grow though the end of this decade (peaking at about 14 million barrels per day), however the increasing level of reserve base depletion will inevitably result in production declines in the next decade.

Russia and CIS: Non-OPEC Crude Supply Forecast (With Exploration)

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,00019

85

1990

1995

2000

2005

2010

2015

2020

Dai

ly C

rude

Pro

duct

ion

(mb/

d)

P10e Forecast

P25e Forecast

P50e Forecast

P75e Forecast

P90e Forecast

Possible production path if exploration results and decline rates fall at the more optimistic end of the scale

Possible production path if exploration results and decline rates fall at the more pessimistic end of the scale

Most likely production path

Production Forecast from Canadian Oil Sands

0

500

1000

1500

2000

2500

3000

3500

4000

4500

1980

1985

1990

1995

2000

2005

2010

2015

2020

Dai

ly P

rodu

ctio

n (m

bopd

)P90 Forecast

Current Forecast

P75 Forecast

P50 Forecast

P25 Forecast

P10 Forecast

A review of various project proposals suggests that in an optimistic case Canadian Oil Sand production could quadruple by 2020 although the Canadian Government has stated the most likely case is a doubling of production by 2012 and continued growth beyond

NGL Production Forecast

0

2000

4000

6000

8000

10000

12000

14000

1600019

93

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

Dai

ly N

GL

Prod

uctio

n (m

bopd

)

OPEC

FSU

North America

Middle East

Latin America

Europe

Asia

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

Dai

ly P

rodu

ctio

n (m

bopd

)

P90 Forecast

P75 Forecast

P50 Forecast

P25 Forecast

P10 Forecast

NGL Production will grow as large scale global gas projects are built to supply growing demands for natural gas. Much of the NGL growth is located within OPEC group countries like Qatar, UAE, Nigeria and others.

Global Non-OPEC Total Liquids with Exploration

A combined forecast of Non-OPEC crude as well as Non-OPEC natural gas liquids and Canadian Oil Sand production suggests that production will grow to between 52 and 55 million barrels per day with declines beginning in the early to middle part of the next decade.

Global: Non-OPEC All Liquids Supply Forecast (With Exploration)

-

10,000

20,000

30,000

40,000

50,000

60,000

1985

1990

1995

2000

2005

2010

2015

2020

Dai

ly C

rude

Pro

duct

ion

(mb/

d)

P10e Forecast

P25e Forecast

P50e Forecast

P75e Forecast

P90e Forecast

Global Non-OPEC Total Liquids without Exploration

There are forecasts out there or coming out which argue that the peak is already here or very close – most forecasts do not build in an exploration component which has been attempted in PFC Energy’s methodology

Global: Non-OPEC All Liquids Supply Forecast (Without Exploration)

-

10,000

20,000

30,000

40,000

50,000

60,000

1985

1990

1995

2000

2005

2010

2015

2020

Dai

ly C

rude

Pro

duct

ion

(mb/

d)P10 Forecast

P25 Forecast

P50 Forecast

P75 Forecast

P90 Forecast

Global Non-OPEC Total Liquids with Exploration

A combined forecast of Non-OPEC crude as well as Non-OPEC natural gas liquids and Canadian Oil Sand production suggests that production will grow to between 52 and 55 million barrels per day with declines beginning in the early to middle part of the next decade.

0

10,000

20,000

30,000

40,000

50,000

60,000

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

Dai

ly P

rodu

ctio

n (m

bopd

)

Canadian Oil SandsNGL

FSUAustral Asia

North AmericaNon OPEC MENA

Latin AmericaEurope

West Africa

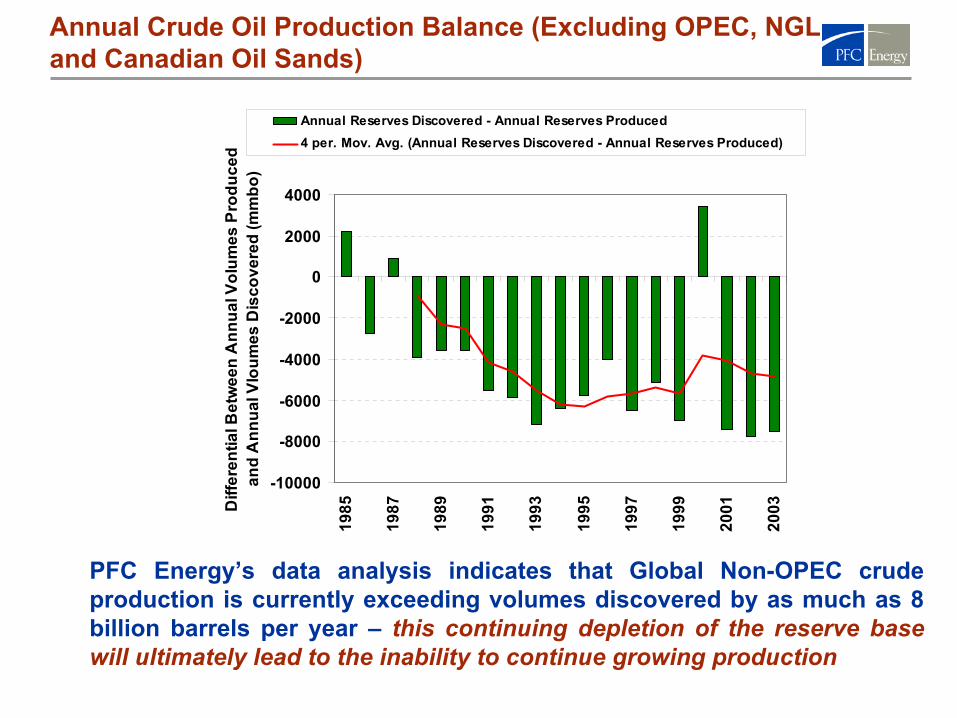

Annual Crude Oil Production Balance (Excluding OPEC, NGL and Canadian Oil Sands)

-10000

-8000

-6000

-4000

-2000

0

2000

4000

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003D

iffer

entia

l Bet

wee

n A

nnua

l Vol

umes

Pro

duce

d an

d A

nnua

l Vlo

umes

Dis

cove

red

(mm

bo)

Annual Reserves Discovered - Annual Reserves Produced4 per. Mov. Avg. (Annual Reserves Discovered - Annual Reserves Produced)

PFC Energy’s data analysis indicates that Global Non-OPEC crude production is currently exceeding volumes discovered by as much as 8 billion barrels per year – this continuing depletion of the reserve base will ultimately lead to the inability to continue growing production

The Problem - The Expected Growing Gap Between Global Demand and Global Non-OPEC Supply

0

20,000

40,000

60,000

80,000

100,000

120,000

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

Dai

ly P

rodu

ctio

n (m

bopd

)

0

20,000

40,000

60,000

80,000

100,000

120,000

Non OPECCrude Oil Non-OPEC NGL

Non-OPEC Oil Sands 1.1% Growth

1.8% Growth 2.4% Growth

The Growing Differential Between Non-OPEC Supply Capacity and

Global Demand

Global Demand Trends

PFC demand scenarios in historical context: demand (excluding the FSU) grew by 1.7% between 1980 and 2004

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

1980 1985 1990 1995 2000

2.4% growth rate1.8% growth rate1.1% growth rate

OPEC Creaming Curve

Cumulative Reserves (mmbo)

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1950

1954

1958

1962

1966

1970

1974

1978

1982

1986

1990

1994

1998

2002

Cum

ulat

ive

Res

erve

s (m

mbo

)

OPEC’s creaming curve is no different from creaming curves for other basins, countries, or regions – hundreds of new fields were discovered during the period 1975 to Present but like other areas they are considerably smaller than fields discovered in years prior

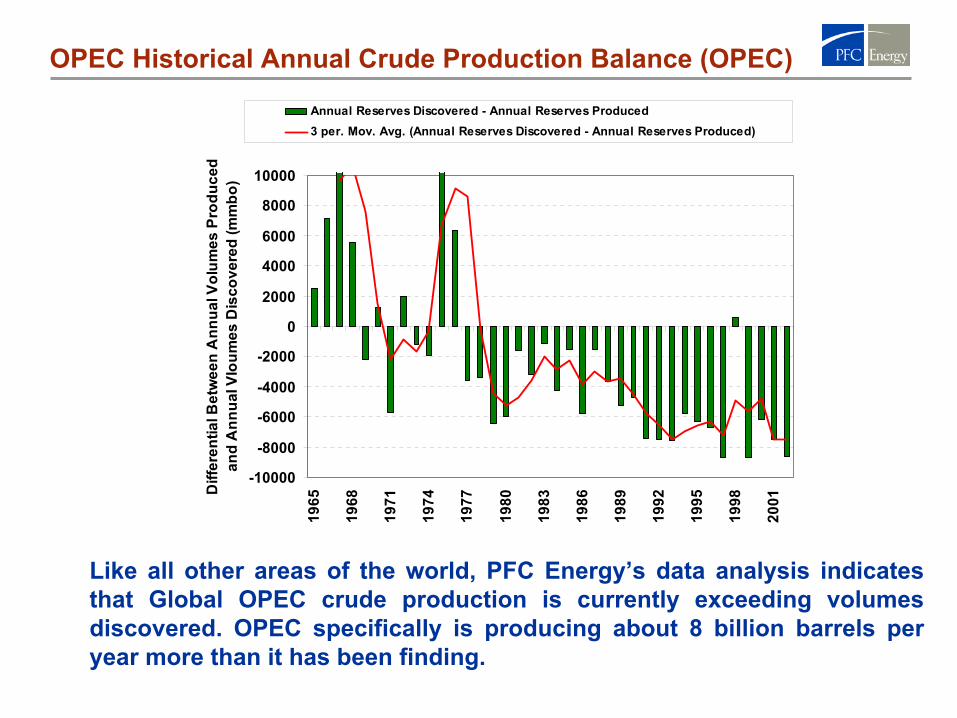

OPEC Historical Annual Crude Production Balance (OPEC)

Chart Title

-10000

-8000

-6000

-4000

-2000

0

2000

4000

6000

8000

10000

1965

1968

1971

1974

1977

1980

1983

1986

1989

1992

1995

1998

2001

Diff

eren

tial B

etw

een

Ann

ual V

olum

es P

rodu

ced

and

Ann

ual V

loum

es D

isco

vere

d (m

mbo

)

Annual Reserves Discovered - Annual Reserves Produced3 per. Mov. Avg. (Annual Reserves Discovered - Annual Reserves Produced)

Like all other areas of the world, PFC Energy’s data analysis indicates that Global OPEC crude production is currently exceeding volumesdiscovered. OPEC specifically is producing about 8 billion barrels per year more than it has been finding.

Historical Production and Depletion Levels (OPEC)

0

4000

8000

12000

16000

20000

24000

28000

32000

36000

40000

1965

1968

1971

1974

1977

1980

1983

1986

1989

1992

1995

1998

2001

2004

Dai

ly P

rodu

ctio

n (m

bopd

)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Cum

Pro

d/C

um R

eser

ves

Daily Production

Cum Production/Cum Reserves

OPEC as a group is depleting at a rate of about 1% per year, even taking into account new discoveries – during the 1990s reserves likely depleted by another 10 percentage points

0%10%20%30%40%50%60%70%80%90%

100%

Iraq

UAEKuwait

LibyaSau

diAlgeri

aNigeri

a

Iran

Venez

uelaQata

rIndones

iaR

eser

ve B

ase

Dep

letio

n (%

)

Historical Production and Depletion Levels (OPEC)

In Decline

Conventional Oil Production has been declining for several years calling into question currently

reported reserves

At or Near Plateau

OPEC as a whole is depleting but some countries are depleting faster than others

When Is The Tipping Point in a Low (1.1%) Demand Growth Scenario?In a low demand growth scenario, as in all demand growth scenarios, OPEC will see a growing market share as non OPEC liquids production falls in the latter part of the next decade. Based on estimates of remaining OPEC reserves and persistent negative annual petroleum balances, there will come a time when OPEC production will not be able to fill the growing gap between demand and non-OPEC production capacity. In a low demand growth scenario, OPEC production will likely meet global demand in the through the end of the next decade but not beyond 2025.

2030405060708090

100

2005

2007

2009

2011

2013

2015

2017

2019

Non OPEC Proc GainNGLs OPEC ProductionDemand

Global Supply and Demand; million b/d

When Is The Tipping Point in a Base Case (1.8%) Demand Growth Scenario?

In a base case demand growth scenario, as in all demand growth scenarios, OPEC will see a growing market share as non OPEC liquids production falls in the latter part of the next decade. Based on estimates of remaining OPEC reserves and persistent negative annual petroleum balances, there will come a time when OPEC production will not be able to fill the growing gap between demand and non-OPEC production capacity. In a base case demand growth scenario, OPEC production will likely not be able to meet global demand in the latter part of the next decade.

Global Supply and Demand; million b/d

2030405060708090

100110

2005

2007

2009

2011

2013

2015

2017

2019

Non OPEC Proc GainNGLs OPEC ProductionDemand

When Is The Tipping Point in a High (2.4%) Demand Growth Scenario?

In a high demand growth scenario, as in all demand growth scenarios, OPEC will see a growing market share as non OPEC liquids production falls in the latter part of the next decade. Based on estimates of remaining OPEC reserves and persistent negative annual petroleum balances, there will come a time when OPEC production will not be able to fill the growing gap between demand and non-OPEC production capacity. In a high demand growth scenario, OPEC production will likely not be able to meet global demand as early as the middle part of the next decade.

Global Supply and Demand; million b/d

20

40

60

80

100

120

2005

2007

2009

2011

2013

2015

2017

2019

Non OPEC Proc GainNGLs OPEC ProductionDemand

Production Declining In The OECD Countries

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1997 2002 2007 2012 2017

mmb/d

Europe North America

8,000

9,000

10,000

11,000

12,000

1997 2002 2007 2012 2017

mmb/d

Latin America And Asia Not Keeping Up

AsiaLatin America

2,000

2,500

3,000

3,500

4,000

4,500

1997 2002 2007 2012 2017

mmb/d

4,500

5,500

6,500

7,500

1997 2002 2007 2012 2017

mmb/d

Increasing Dependency From Less Stable Areas

West AfricaFSU

4,000

6,000

8,000

10,000

12,000

14,000

1997 2002 2007 2012 2017

mmb/d

1,000

2,000

3,000

4,000

1997 2002 2007 2012 2017

mmb/d

The Persian Gulf Can Grow Production

17,000

21,000

25,000

29,000

33,000

1997 2002 2007 2012 201724%

28%

32%

36%OPEC Persian Gulf Production

OPEC PG Production as % of Global Supply

mmb/d

+0.55- 0.09

+ 0.50

- 0.15+0.88

Do Not Include The Totality of Suppliers. Only the Most significant flows are shown.The Map Includes Exports from Canada, Latin America, Middle East, North Sea, West Africa, West Africa, FSU to Selected Regions

Middle EastWest AfricaNorth SeaCanadaSE AsiaFSULatin America

+0.20

+4.2-0.7

-2.60 +3.7

+2.9 Imports From

- 0.30

2010-1997 Delta Growth in Crude FlowsFor Selected Consuming Regions

Increasing Dependency From Less Stable Areas

mmb/d

+53%-19%

+30%

-15%+25%

Do Not Include The Totality of Suppliers. Only the Most significant flows are shown.The Map Includes Exports from Canada, Latin America, Middle East, North Sea, West Africa, West Africa, FSU to Selected Regions

+20%-70%

+670%

-26%

2010-1997 World Flows % Change To Selected Consuming Regions

Supply Fears Due To Concentrated Exports

+269%- 21%

+60%

0

2,000

4,000

6,000

8,000

10,000

97

Canada

Latin America

NWE

Middle East

West Africa

Others0

2,000

4,000

6,000

8,000

10,000

12,000

09

Crude Flows To The US

kb/d

Exports To The US From Selected Suppliers

TOTAL = 8,900 kb/d

kb/d

3,5354,430

1,2201,770

1,7471,590

1,692 2,200

493 398

1997 2010

Exports To The US From Selected Suppliers

TOTAL = 10,800 kb/d

0

2,000

4,000

6,000

8,000

10,000

97

SE Asia

Middle East

West Africa

Others

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

09kb/d

Exports To Asia1 From Selected Suppliers

kb/d

1997 2010

Exports To Asia1 From Selected Suppliers

6,300

10,050

4423,340

1,160

790

TOTAL = 8,000 kb/d

TOTAL = 14,200 kb/d

Crude Flows To Asia1

1. Asia = China, Japan, Korea, India

Price Implications

The excess capacity that existed after 1985 has now disappeared

Who is willing to recreate a capacity cushion in the world oil market?– Iran, Russia, Venezuela, Iraq– Kuwait, UAE, Saudi Arabia

Between 2005 and 2008, both West Africa and the FSU will bring large projects on line, creating a window of vulnerability for oil prices (depending on the demand scenario)

In the medium term, if the key producers do not build excess capacity (beyond the 1.5 million b/d that Saudi Arabia appears to be willing to maintain),

– prices will move structurally higher,

– and face greater volatility

The oil market does not work well without a supply safety net

Strategic Implications

Higher volumes and higher prices will bring back large financialsurpluses to the Middle East and the Persian Gulf.

The new-found wealth will alter the present strategic relationship with the US: despite louder calls for reforms from the US, the region will spend its way out of reforms, and the regimes will have the opportunity to use their financial might to co-opt and divide the different interest groups.

The US will face more competition from emerging strategic players to secure access to oil.

There is no alternative to dependence on Middle Eastern oil, but there will be alternatives to oil.

Managing demand becomes a key strategic issue for the US

Strategic Advisors in Global Energy

Offices

1300 Connecticut Avenue, N.W. Suite 800Washington, DC 20036 USATel: (1 202) 872 1199 Fax: (1 202) 872 1219

3, cité Paradis75010 Paris, FranceTel: (33 1) 47 70 29 00 Fax: (33 1) 47 70 27 37

Houston, TexasTel: (1 281) 599 7099 Fax: (1 281) 599 9891

London, United KingdomTel: 44 (0)1256 760678Fax: 44 (0)1256 760678

[email protected] www.pfcenergy.com