Copyright 2013 Sustainalytics - All rights reserved • Emerging markets are increasingly pivotal in the growth of the pharmaceutical industry. Pharmaceutical companies operating in these markets, whether global or domestic players, are exposed to market- specific social risks that affect public health and may also pose material financial risks. • This Insight examines the key market-specific social issues in both China and India, two of the main growth markets for the pharma industry. For China this Insight will address the topics of product quality and safety and marketing/corruption. For India, the research focus is on patenting and pricing issues and ethical conduct during clinical trials. • Assessing the performance of both global and domestic players on the above-mentioned issues, we see that global pharma companies need to tailor their corporate responsibility initiatives more specifically to the emerging markets context, and domestic players should provide more disclosure on how they mitigate key risks. Recent events in India and other emerging markets have intensified the debate over intellectual property (IP) and public health concerns. On 1 April 2013, the Indian Supreme Court ruled against Novartis, denying its patent application for cancer drug Gleevec on the grounds that the drug is not sufficiently innovative (Indian patent law requires proof of significantly improved efficacy). In addition, the Indian government issued its first compulsory license 1 in March 2012 and has plans for several more. Indonesia, meanwhile, issued seven compulsory licenses for various HIV and hepatitis drugs in September 2012. Chinese authorities, while less likely to issue compulsory licenses, have exerted significant pricing pressures on global pharma companies over the past few years, and this trend is expected to continue. Such developments are notable because of the importance of emerging markets, particularly Asia, to the future of the pharma industry. The industry faces a multitude of challenges, including patent expirations, a lack of innovation, tighter regulation, and spending cuts in public healthcare budgets. Thus, new business models are required and new markets need to be conquered. Collectively, emerging markets are expected to amount to a third of the global pharma market by 2016, up from 20 per cent in 2011. 2 China is currently the third largest pharmaceutical market in the world and is expected to grow by 15 to 18 per cent annually over the coming years. 3 India, Brazil and Russia follow closely behind China. Global pharma companies, while keen to seize the opportunities presented, have not been able to sufficiently tap into this huge potential market, in part because they have failed to tailor their approaches to local Pharma in China and India Market-Specific Social Risks and Opportunities Hazel Goedhart Additional research by Alex Read-Brown July 2013

Transcript

ESG Ins ight ASIA — July 2013 1

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

ESG Insight

ASIA

•Emergingmarketsareincreasinglypivotalinthegrowthofthepharmaceuticalindustry.Pharmaceuticalcompanies operating in these markets, whether global or domestic players, are exposed to market-specificsocialrisksthataffectpublichealthandmayalsoposematerialfinancialrisks.

•This Insight examines the key market-specific social issues in both China and India, two of the maingrowthmarketsforthepharmaindustry.ForChinathisInsightwilladdressthetopicsofproductqualityandsafetyandmarketing/corruption.ForIndia,theresearchfocusisonpatentingandpricingissuesandethicalconductduringclinicaltrials.

•Assessingtheperformanceofbothglobalanddomesticplayerson theabove-mentioned issues,weseethatglobalpharmacompaniesneed to tailor their corporate responsibility initiativesmorespecificallyto the emerging markets context, and domestic players should provide more disclosure on how theymitigatekeyrisks.

Recent events in India and other emerging markets have intensified the debate over intellectual property (IP) and public health concerns. On 1 April 2013, the Indian Supreme Court ruled against Novartis, denying its patent application for cancer drug Gleevec on the grounds that the drug is not sufficiently innovative (Indian patent law requires proof of significantly improved efficacy). In addition, the Indian government issued its first compulsory license1 in March 2012 and has plans for several more. Indonesia, meanwhile, issued seven compulsory licenses for various HIV and hepatitis drugs in September 2012. Chinese authorities, while less likely to issue compulsory licenses, have exerted significant pricing pressures on global pharma companies over the past few years, and this trend is expected to continue.

Such developments are notable because of the importance of emerging markets, particularly Asia, to the future of the pharma industry. The industry faces a multitude of challenges, including patent expirations, a lack of innovation, tighter regulation, and spending cuts in public healthcare budgets. Thus, new business models are required and new markets need to be conquered. Collectively, emerging markets are expected to amount to a third of the global pharma market by 2016, up from 20 per cent in 2011.2 China is currently the third largest pharmaceutical market in the world and is expected to grow by 15 to 18 per cent annually over the coming years.3 India, Brazil and Russia follow closely behind China. Global pharma companies, while keen to seize the opportunities presented, have not been able to sufficiently tap into this huge potential market, in part because they have failed to tailor their approaches to local

Pharma in China and IndiaMarket-Specific Social Risks and Opportunities

Hazel GoedhartAdditional research by Alex Read-Brown

July 2013

ESG Ins ight ASIA — July 2013 2

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

needs. A lack of public healthcare, drug affordability/pricing and a perceived lack of IP protection are viewed by global pharma as key obstacles to entering these growth markets.4

This Insight argues that indeed, pharmaceutical multinational companies (MNCs) need to get their patenting and pricing strategies right in order to access key growth markets whilst at the same time improving access to drugs for low income groups. They should address these issues proactively if they are to pre-empt growing patenting and pricing pressures in emerging markets such as India and China. But access to considerable untapped Asian markets requires more; companies should have the ability to deal with a range of inherent social risks specific to these markets. In the same vein, access to high quality healthcare for low income groups is also determined by a broader range of issues than merely patenting and pricing policies. For instance, corruption in drug distribution channels can stimulate the prescription of unsuitable, ineffective or overpriced drugs.

In addition to examining MNC performance on market specific ESG issues in China and India, this Insight will take a closer look at the performance of domestic drug companies. For local pharma companies, most of whom are generics producers or distributors, IP and pricing strategies are inevitably less salient, but strong policies and programs on other environmental, social and governance (ESG) issues like product quality and safety are all the more important in order for them to evolve into socially responsible companies.

For companies operating in emerging markets, whether global or domestic, tackling the key ESG issues described in this Insight is often not treated as standard business practice because of weak regulatory capacity in these areas. However, as civil society activity increases, wealth accumulates, and priorities change, it is likely that regulatory mechanisms in emerging markets will be strengthened and more diligently enforced. Companies will thus need to be vigilant to remain ahead of the regulatory curve.

ESG Ins ight ASIA — July 2013 3

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

Analysis of Key ESG Challenges per MarketSince China and India are two of the key growth markets for the pharmaceutical industry, understanding how their particular market structures give rise to various social challenges is paramount to entering these markets in a successful and responsible manner. (For full details on market characteristics, see Appendix 1.)

In China, complex and bureaucratic processes surrounding drug purchasing, a high level of decentralization, and complex distribution channels all conspire to make the system sensitive to corruption and marketing of poor quality drugs. Regulation addressing corruption in drug marketing and quality and safety tends to be lacking or poorly enforced, but this is expected to improve in the near future.

In India, patenting and pricing issues remain of primary concern considering the government’s commitment to ensuring a proper balance between IP rights and the right to health. Due to the country’s strong domestic generics industry and its status as “pharmacy of the developing world,” developments in India will affect patients around the world who depend on a steady supply of cheap Indian drugs. In addition, recent controversies surrounding the treatment of participants in clinical trials have brought this issue under the regulatory spotlight.

The particularities of the Chinese and Indian markets each make for their own unique set of ESG (mainly social) challenges and opportunities. These issues will be outlined below, highlighting the local context and associated potential risks and opportunities for the industry. Also outlined is the degree to which different types of companies are exposed to these risks and what measures they could/should take to proactively address these issues. Finally, the analysis will clarify the business case for companies to address the issues.

ESG Ins ight ASIA — July 2013 4

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

Key ESG Issues in ChinaDrug Quality and SafetyThe lack of quality and safety assurance for drugs produced and marketed in China is a grave threat to patient health in China and abroad (where adulterated Chinese drugs may be sold). Substandard drugs can have detrimental health consequences and can even result in death. China in particular has seen its fair share of drug safety concerns, such as the April 2012 scandal concerning industrial waste being used to make drug capsules.5 Furthermore, counterfeiting of drugs is rampant in China due to a lack of regulation and enforcement in this area. Counterfeit products are at best ineffective and at worst dangerous. It is estimated that worldwide over 700,000 people die annually (mostly in developing countries) from the deleterious effects of substandard and counterfeit drugs, produced largely in China.6 Within the Chinese market, such concerns have triggered a lack of consumer trust in domestic pharmaceutical producers.

Domestic drug companies are able to operate with relatively little oversight. Of particular concern are producers of active pharmaceutical ingredients (APIs). China is the world’s largest producer of APIs, yet the country has very little regulation for API producers. Since API producers are categorized as chemical rather than pharmaceutical companies, they are not controlled by China’s State Food and Drug Administration (SFDA), and can function without Good Manufacturing Practice (GMP) certification.

On the positive side, the stricter GMP rules, to which all pharmaceutical manufacturing facilities must fully comply by 2016, indicate that the government is serious about tackling drug quality and safety. In March 2013, the SFDA was elevated to ministerial level, giving the agency greater authority, manpower, and financial resources. Enforcement may, however, remain a problem.

Comparative Company AssessmentSince quality and safety problems apply mainly to local companies rather than MNCs, this study compares four domestic pharma producers: Fosun Pharma, Shanghai Pharma, Sinopharm, and Sihuan Pharma. The companies are compared on two dimensions: exposure to quality and safety concerns, as well as mitigation and management of product quality and safety violations (preparedness). The indicators used to measure exposure and preparedness are outlined in Appendix 2. A third performance dimension could be assessed using companies’ track records (i.e., whether they have been involved in significant product quality and safety violations); however, not enough company-specific information was available to make an assessment on this dimension.

ESG Ins ight ASIA — July 2013 5

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

Overall, we can conclude that company exposure levels are relatively high. Shanghai Pharma and Sinopharm in particular are greatly exposed to quality and safety risks due to their high production volumes, quick growth, and complex supply/distribution channels, which increase the number of potential failure points. In addition, the companies also act as distributors of other companies’ pharmaceuticals, which means there are large portions of the quality and safety process outside of their direct sphere of control. Preparedness levels, gauged by various measures taken to provide quality assurance, vary significantly between companies. While Sinopharm and Sihuan Pharma provide very little disclosure on their quality assurance processes, Shanghai and Fosun Pharma demonstrate clear management oversight and go beyond regulatory compliance (see Best Practice box below for further details).

Business Drivers for Proactively Dealing with Product Quality and Safety in ChinaDomestic producers are generally less trusted by the Chinese public than foreign brands. Thus, building brand recognition and consumer trust is critical to obtaining and maintaining a strong market share. Reputational damage for Chinese companies could be considerable if a sizeable proportion of their portfolio consists of branded products or if this is a key factor for its growth. The flip side is that domestic producers may be able to charge a premium price if they can gain consumer trust in their brands. Beyond reputational issues, quality and safety regulation and enforcement are expected to improve, and thus companies are advised to adopt best practices ahead of regulatory changes in order to avoid costly compliance measures and fines.

Risk Analysis: Product Quality & Safety - Chinese Companies

Figure 1: Comparative assessment of quality and safety risk for four Chinese companies

High Risk Medium/High Risk Medium Risk Low/Medium Risk Low Risk

ESG Ins ight ASIA — July 2013 6

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

Even though quality and safety procedures for their own production units are generally well established, global pharma companies may be indirectly implicated in product quality issues through their collaborations with Chinese producers. Sourcing of APIs as well as outsourcing of manufacturing constitutes risk when there is insufficient control over the quality and safety standards of partners. Involvement in a drug scandal, even if indirectly, can considerably damage a company’s reputation and may involve sizeable costs related to drug recalls and stalled operations.

Best Practice in Product Quality and Safety (Domestic)Shanghai Pharmaceuticals and Fosun Pharmaceuticals – Both companies have voluntarily embraced international

best practice through the adoption of production standards in line with the International Conference on Harmonization of

Technical Requirements for Registration of Pharmaceuticals for Human Use, augmenting those required by Chinese GMP.

Shanghai Pharmaceuticals – The company has senior management involved in setting quality and safety control policy

and overseeing its implementation. Shanghai Pharma also reports screening its suppliers on both their capacity to meet

the company’s heightened production standards and on their compliance with said standards once selected.

Fosun Pharmaceuticals – The company conducts trial production runs with samples provided by suppliers, checking for

product stability, quality and safety, as part of its supplier selection process.

Marketing/CorruptionAlthough detailed information on corruption in the Chinese pharmaceutical industry is relatively sparse, the Chinese market is considered susceptible to bribery and other improper marketing practices. The industry globally has seen its share of marketing violations over the past few years, culminating in some huge fines. Violations typically concern: providing false or misleading statements on drug safety and effectiveness, off-label marketing,7 and bribing of doctors to prescribe certain products. Improper marketing practices ultimately harm consumers, who may end up being prescribed drugs that are unsuitable, ineffective, overly expensive, or even hazardous to their health.

The Chinese market is susceptible to such practices because of its notoriously complex and opaque distribution channels. The lack of transparency on how distribution takes place facilitates corrupt practices, which in turn may hamper drug availability and exacerbate price inequalities. Until recently, Chinese hospitals were allowed to take a commission on drug prescriptions, thus increasing the incentive to issue more, sometimes unnecessary, prescriptions, particularly for more expensive drugs. This practice is now being curtailed; according to the government’s 12th Five-Year Plan (2011-2015)8 for medical reform, hospital drug sale margins will be phased out before 2015. The government is also pushing for a more transparent purchasing system through open tendering and bidding for medical products at the provincial level, increasing transparency and economies of scale and achieving price reductions. Furthermore, a new drug circulation law may soon be proposed, which will bring tighter anti-corruption regulation and more frequent campaigns.

The Chinese market’s susceptibility to improper marketing is further illustrated by a growing and increasingly active sales staff, as MNCs attempt to increase market penetration and domestic companies develop more sophisticated and aggressive sales tactics. As of March 2012, pharmaceutical sales force levels in China had overtaken those in the U.S., with 80,000 sales representatives active in the country.9

ESG Ins ight ASIA — July 2013 7

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

The fact that direct-to-consumer marketing is allowed in China (although regulated by the SFDA) further increases opportunities for improper marketing. The WHO Ethical Criteria for Medicinal Drug Promotion recommends that advertisements to the general public not be permitted for prescription drugs because of the risk of advertisements containing misleading statements about drug efficacy or safety.

In 2007, China investigated over 1,000 cases of suspected bribery related to drug marketing.10 Authorities have recently stepped up their investigation and enforcement efforts. In October 2012, seven managers and directors of key public hospitals in Shenzhen were jailed for taking bribes to purchase particular drugs and medical equipment.11 Foreign drug companies are also being targeted, as demonstrated by the July 2013 arrest of four senior Chinese executives of GlaxoSmithKline (GSK). According to Chinese police officials, GSK used a network of travel agencies and consultancies to bribe officials and doctors to boost its drug sales in China.12

Comparative Company AssessmentDue to a dearth of information and lack of transparency across the industry regarding marketing practices in China, a comparative company assessment is beyond the scope of this study. For MNCs, which typically have strong anti-corruption programs and ethical marketing codes in place, some elaboration on how such policies and programs are applied in the Chinese context would be warranted, particularly considering MNCs’ increased focus on this market. Domestic producers typically lack any kind of policy or program on anti-corruption and ethical marketing, in spite of expanding sales and promotion efforts. Indicators that may be used to measure company exposure and preparedness are outlined in Appendix 2.

Business Drivers for Proactively Dealing with Marketing/Corruption in ChinaGiven their increased activity in the country, it is in their best interest for companies to take measures to avoid involvement in marketing/corruption scandals in China. The Chinese government seems committed to tackling drug marketing issues, and regulatory authorities are expected to significantly increase regulations, enforcement efforts, and fines in coming years. It is difficult to predict when these changes will happen, but once the decision to act is made they will likely be implemented swiftly and rigorously, as the track record of the Chinese government proves. Therefore, companies should be prepared to deal with stricter regulation and enforcement when it comes.

ESG Ins ight ASIA — July 2013 8

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

Key ESG Issues in India Drug Patenting and PricingDrug patenting and pricing have long been contentious issues in India. In 2005, the country strengthened its patent law in line with the World Trade Organization’s 1994 Agreement on Trade Related Aspects of Intellectual Property Rights (TRIPS). However, India’s current patent law does stipulate that a product must be truly innovative in order for a patent to be granted, and limits patenting in the interest of public health. In addition, India has made use of the TRIPS amendments made in 2001, which created certain flexibilities to overrule patents in order to promote access to medicines for all. In March 2012, the Indian Patent Office issued its first ever compulsory license for Bayer’s liver and kidney cancer drug Nexavar, providing an opportunity for Indian generic competitor Natco to market its copy of the drug for a mere three per cent of Bayer’s price. In January 2013, India followed up with three more compulsory licenses for Roche’s breast cancer drug Herceptin, and BMS’s leukemia treatment Sprycel and breast cancer treatment Ixempra. In the case of Herceptin, a well-organized civil society coalition, including breast cancer survivors and health activists, targeted Roche for its “irrational and unethical” pricing policies and successfully urged the government to approve a compulsory license.

Similar pressures are exerted on the industry in the area of pricing, affecting both innovator companies and generics producers. While pricing is an issue in all markets, in India, where 32.7 per cent of people live below the international poverty line of USD 1.25 dollar a day, it is particularly crucial.13 Even for middle income groups, many drugs are priced out of range, considering the lack of health insurance coverage and reimbursement schemes in the country. The percentage of the population with access to a certain treatment depends on a range of factors such as: availability of healthcare services (which is severely lacking in some rural regions), affordability of the treatment, and propensity to spend. For example, treatment for a life-threatening cancer costing USD 10,000 per year would be affordable to only 4.2 per cent of the Indian population, assuming perfect healthcare availability.14

Drug prices in India are generally lower than in other emerging markets, as the government has always taken a strict line on keeping prices down. The new Drug Price Control Order (DPCO), approved by the cabinet in November 2012, extends the list of price-controlled drugs from 74 to 348, covering close to 30 per cent of India’s drug market. However, there is uncertainty over how ceiling prices will be determined, and civil society groups have expressed concern that maximum prices may actually increase significantly. Overall, it is clear that the Indian context is currently in flux, creating a host of uncertainties for drug companies.

Comparative Company AssessmentSince patenting and pricing pressures primarily affect MNCs, this study compares seven MNCs: Abbott, Bayer, Gilead, GlaxoSmithKline (GSK), Pfizer, Roche and Sanofi. The companies were assessed on two dimensions: exposure to patenting and pricing pressures, as well as preparedness to deal with these pressures through proactive access to medicines programs. The indicators used to measure exposure and preparedness are outlined in Appendix 2. A third performance dimension is provided by companies’ track records (i.e., whether they have been involved in significant patenting and pricing controversies).

ESG Ins ight ASIA — July 2013 9

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

Exposure to patenting and pricing risks depends mainly on drug portfolio composition and diversification. A company like Gilead, for example, has high risk exposure due to its almost exclusive focus on HIV treatments, which are likely targets for compulsory licenses. Regarding preparedness, while clear leaders such as GlaxoSmithKline and Gilead can be identified (see Best Practice boxes below), access to medicine programs in general tend to be rather ad hoc, philanthropic and limited in scope (i.e., only for certain markets or certain products). In short, these programs are not truly integrated into core business activities, and lack clear long-term commitments and targets. Some companies have also been involved in patenting and pricing controversies. For instance in November 2011, Abbott faced public health campaigns in over a dozen countries because it allegedly restricted access to its HIV/AIDS drug Kaletra.

Business Drivers for Proactively Dealing with Patenting and Pricing Issues in IndiaAlthough improving drug access by lowering prices and sharing IP rights is perceived as primarily a normative imperative, a business case can definitely be made in favour of these practices. First, the industry globally will need to play a more proactive role in curbing healthcare expenses whilst improving quality. It is clear, particularly considering the decline of the blockbuster model and the impact of the “patent cliff,”15 that new business models are needed in order for the industry to remain profitable. Business models that target more consumers at the middle and bottom end of the income pyramid (e.g., a volumes-over-margins approach) fit with this need for change.

Risk Analysis: Parenting and Pricing - MNCs

Figure 2: Comparative assessment of patenting and pricing risk for seven MNCs

High Risk Medium/High Risk Medium Risk Low/Medium Risk Low Risk

company* = some additional risk due to mediocre track recordcompany** = additional high risk due to poor track record

ESG Ins ight ASIA — July 2013 10

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

Access programs can have positive reputational effects for companies, while still generating considerable profits. Differential pricing16 schemes constitute a clear business case in terms of increasing penetration into the untapped markets of poor and middle income populations. Intra-country differential pricing17

schemes increase access for those in need, while still allowing the company to charge a premium price for those customers who can afford it. Furthermore, voluntarily lowering prices for key drugs that are likely to be targeted by patenting restrictions and pricing pressures may successfully pre-empt regulatory measures; this is a strategy that some MNCs in India have already adopted. Voluntary licensing18 schemes can also have a pre-emptive effect, and still allow the patent holder to make profits (albeit lower than otherwise) through royalty payments.

Best Practice in Patenting: Gilead SciencesIn July 2011, Gilead was the first company to enter into a licensing agreement with the Medicines Patent Pool (MPP), a non-

profit entity that negotiates voluntary license agreements for patents on HIV medicines. The MPP pools multiple patents

related to HIV medicines in one place, which are then licensed out to generic manufacturers, while the patent holder

receives royalty payments (typically of three to five per cent). Gilead currently has five HIV patents in the pool: Tenofovir,

Cobicistat, Elvitegravir, Emtricitabine, and a fixed-dose combination called the Quad. MPP licenses are non-exclusive

within India, which means that any company that meets the eligibility criteria may receive a license from the MPP. So far

six companies have received licenses: Shauna Pharma Solutions, Aurobindo Pharma, Emcure Pharmaceuticals, Hetero

Labs, Laurus Labs, and MedChem. Generic competition has lowered the price of tenofovir by over 80 per cent in the past

few years. The licenses allow for the marketing of the drug in over 100 low- and middle-income countries, covering more

than 82 per cent of people living with HIV in those countries. A unique feature of this licensing agreement is that the terms

and conditions have been made entirely public.

For Indian generic drug producers, the threat that compulsory licensing poses to MNCs translates into a potential wealth of opportunities to copy patented drugs, as long as they are well-prepared to grab these opportunities. However, generics producers do need to consider pricing, since even relatively cheap generic drugs may be priced out of range for a significant proportion of the population. Taking fierce generic competition as well as the threat of government drug price controls into account, lowering generic drug prices could be a smart business decision in some cases.

Best Practice in Affordable Pricing: GlaxoSmithKline (GSK)In July 2011, GSK expanded its tiered-pricing strategy in India to include two new cancer drugs at a rate 70 per cent lower

than in the U.S. Although the drugs’ prices, at over USD 600 per month, are still out of reach for the majority of the Indian

population, GSK’s pricing strategy does seem more adaptive to local needs and market conditions than many of its MNC

competitors. Since 2009, GSK has pursued an explicit strategy of high volume, low margins in order to succeed in emerging

markets. GSK’s CEO, Andrew Witty, has repeatedly indicated that he sees the company’s tiered pricing strategy as key

to its success in the Indian market: “At GSK we will continuously […] defend tiered pricing to make sure that we have

appropriate pricing for the affordability of the country, and that’s why, in my personal view, our business in India has been

so successful for so long.” (CNBC-TV18 interview, 19 October 2012)

ESG Ins ight ASIA — July 2013 11

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

Ethical Conduct in Clinical TrialsIndia has become one of the prime locations for clinical trials,19 but this development has raised serious concerns regarding the treatment of trial participants. The appeal of India as a trial location lies in its relatively low costs, its huge potential “treatment-naïve” patient base, and its high-quality research professionals. In addition, if companies want to market drugs in India, they are required to submit data generated using Indian patients. Ethical violations in clinical trials, such as failure to acquire free, prior and informed consent from patients, or failing to pay adequate compensation, are industry-wide problems, which have been exacerbated in recent years as more and more trials have moved to developing countries.

India in particular has seen its fair share of controversies around clinical trials. A report by the Indian Ministry of Health released in February 2013 stated that 436 people died in 2012 due to serious adverse events during clinical trials; the cases are still under investigation to determine whether these deaths were caused by the trials themselves or other factors. In 2011, 438 such deaths were reported, of which 16 were found to be due to clinical trials.20

Regulations around trials are relatively weak in India. No clear minimum ethical clinical standards for trials currently exist, though this situation is quickly changing. In January 2013, the Supreme Court severely criticized the Central Drug Standard Control Organization (CDSCO) for failure to properly regulate and monitor ethical trial standards. In the same month, the ministry of health announced plans to make compensation payments mandatory in the event of a study-related injury or death. The ministry also instated a new rule requiring companies to have registered ethics committees in place to review and approve clinical trial protocols. The regulatory framework is thus clearly evolving, and companies need to stay ahead of the regulatory curve.

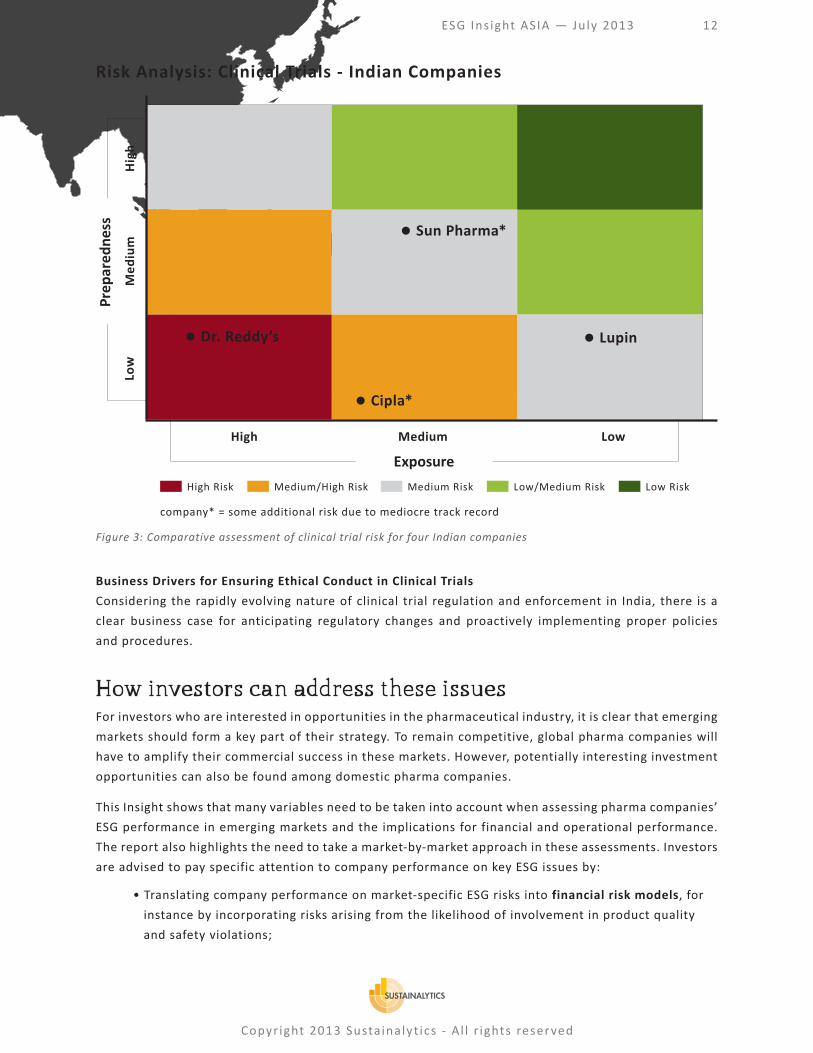

Comparative Company AssessmentThis study compares four domestic pharma producers: Cipla, Dr Reddy’s, Lupin and Sun Pharma. The companies are compared on two dimensions: exposure to concerns regarding the treatment of trial participants, and preparedness to prevent ethical violations. The indicators used to measure exposure and preparedness are outlined in Appendix 2. A third performance dimension is provided by companies’ track records (i.e., whether they have been involved in significant clinical trial controversies).

The four Indian companies’ exposure to ethical conduct issues varies mainly according to their (propensity for) direct involvement in clinical trials. For instance, clinical trials are essential to Dr Reddy’s business, both for its own innovative products, developments of biosimilars, and for the testing services it provides to others. Preparedness of Indian companies to mitigate clinical trial risks, through comprehensive trial protocols and monitoring mechanisms, is generally low. This is further compounded by the fact that two companies, Cipla and Sun Pharma, have been involved in clinical trial-related controversies.

ESG Ins ight ASIA — July 2013 12

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

Business Drivers for Ensuring Ethical Conduct in Clinical TrialsConsidering the rapidly evolving nature of clinical trial regulation and enforcement in India, there is a clear business case for anticipating regulatory changes and proactively implementing proper policies and procedures.

How investors can address these issuesFor investors who are interested in opportunities in the pharmaceutical industry, it is clear that emerging markets should form a key part of their strategy. To remain competitive, global pharma companies will have to amplify their commercial success in these markets. However, potentially interesting investment opportunities can also be found among domestic pharma companies.

This Insight shows that many variables need to be taken into account when assessing pharma companies’ ESG performance in emerging markets and the implications for financial and operational performance. The report also highlights the need to take a market-by-market approach in these assessments. Investors are advised to pay specific attention to company performance on key ESG issues by:

• Translating company performance on market-specific ESG risks into financial risk models, for instance by incorporating risks arising from the likelihood of involvement in product quality and safety violations;

Risk Analysis: Clinical Trials - Indian Companies

Figure 3: Comparative assessment of clinical trial risk for four Indian companies

High Risk Medium/High Risk Medium Risk Low/Medium Risk Low Risk

company* = some additional risk due to mediocre track record

ESG Ins ight ASIA — July 2013 13

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

• Identifying and investing in industry leaders that demonstrate best practice by proactively addressing market-specific ESG issues and anticipating related opportunities, such as opportunities to access new markets through progressive pricing policies;

• Maintaining active dialogues with pharma companies on market-specific ESG risks;

• Urging Chinese and Indian companies to provide more disclosure on their policies, programs and performance regarding market-specific ESG risks, and on how they proactively anticipate pending legislation in these areas. For instance:

For Chinese companies:• How do they manage product quality and safety (e.g. in terms of compliance with China’s

new GMP guidelines and moving beyond Chinese regulatory compliance)?• What marketing codes and anti-corruption measures do they have in place, and how do

they aim to stay ahead of the regulatory curve in this regard?

For Indian companies:• What role do access considerations play in their pricing strategies? Have they developed

clear pricing policies to ensure that maximum prices set by the government are respected?• What steps have they taken to implement and guarantee international best practice for

ethical conduct of clinical trials, such as the Helsinki Declaration?21

• Urging MNCs to provide more insight into how their corporate responsibility strategies on certain market-specific ESG issues are tailored to the context of emerging markets. Examples of market-specific ESG considerations for MNCs are:

• How are their access to medicine initiatives incorporated into their growth strategies for India, China and other emerging markets? How will they shift from ad hoc, philanthropic initiatives to structural approaches that are applied across the board (i.e. across markets and portfolios)?

• What product quality and safety assurance process do they have in place for their Chinese API suppliers?

• How do they implement their ethical marketing codes and anti-corruption programs in emerging markets?

• How do they monitor clinical trials conducted in emerging markets, specifically when outsourced?

ESG Ins ight ASIA — July 2013 14

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

Appendix I – Market CharacteristicsChina – Characteristics of the Pharmaceutical Market

• Third largest market in the world for over-the-counter and prescription drugs22 and projected to be the second largest by 2015;23

• Massive population of 1.3 billion people, which is aging, urbanizing, becoming increasingly affluent, and changing lifestyles; this will increase demand for healthcare;

• Non-communicable diseases, such as cancer, heart disease and cerebrovascular disease, are the top causes of death; China has the world’s largest diabetes population of approximately 92 million people, followed by India with 63 million;24

• More than 95 per cent of the population has some form of healthcare insurance, but coverage remains basic and out-of-pocket expenses high; the government aims to have everyone covered by medical insurance by 2020 and reduce out-of-pocket expenses to 30 per cent by 2015;25

• Local companies dominate the market, but are mostly active pharmaceutical ingredient (API) or generics producers; there are very few integrated players that are involved in R&D, manufacturing and distribution;

• Distribution channels are complex; products are distributed through national and provincial wholesalers, which sell the drugs to hospitals, clinics and pharmacies, who in turn sell to patients;

• Decentralized reimbursement processes with drug lists and pricings at provincial level further complicate matters; conditions may vary considerably at province, city and hospital level;

• Thousands of distributors are active, but consolidation is moving fast under government encouragement, which is expected to create more transparency and facilitate enforcement of regulations;

• Drug prices are fixed by the government for the 300 or so drugs on the Essential Drug List (EDL), last updated in 2012; most other drug prices are set in negotiation with manufacturers.

India – Characteristics of the Pharmaceutical Market• Government has implemented numerous measures since the 1970s to encourage the growth of its domestic

generics industry, including not recognizing product patents;• New patent law was adopted in 2005 in line with World Trade Organization standards;• Strong local pharmaceutical industry and status as “pharmacy of the developing world”; • Top three local players have a higher collective market share than top three multinationals;26

• Globally, India is the third largest producer of medicines by volume and tenth in terms of value;27

• Lowest dependence on drug imports of the BRIC countries;28

• Relatively low per capita consumption of medicines amongst emerging markets29 in combination with its large population (more than 17 per cent of the world’s population lives in India) indicates great growth potential;

• Very high out-of-pocket healthcare spending and very limited healthcare insurance coverage place access to key lifesaving drugs out of reach even for middle income groups;

• Affordability is expected to be the main growth driver for pharmaceutical sales.30

ESG Ins ight ASIA — July 2013 15

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

Market characteristics China India GlobalPharmaceutical sales (2011) - USD billion31 66.9 15.6 1084

Pharmaceutical sales (projection 2020) - USD

billion32175.8 48.8 1571

CAGR forecast (2012-2016)33 15-18% 14-17% 13.70%

Total health expenditure as % of GDP (2010)34 5.10% 4.10%

Per capita annual health spending (2011) - USD

billion35221 54

Generics market share as % of total sales

(2011)3664.2% 72.2%

Additional spending on patented versus

generic drugs by 2020 - USD billion3730.0/60.2 3.3/24.2

Market share of MNCs (2010)38 27% 28%

Out-of-pocket expenditures on health - as % of

total private healthcare spending (2010)3978.90% 86.40%

Comparative Market Facts and Figures

ESG Ins ight ASIA — July 2013 16

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

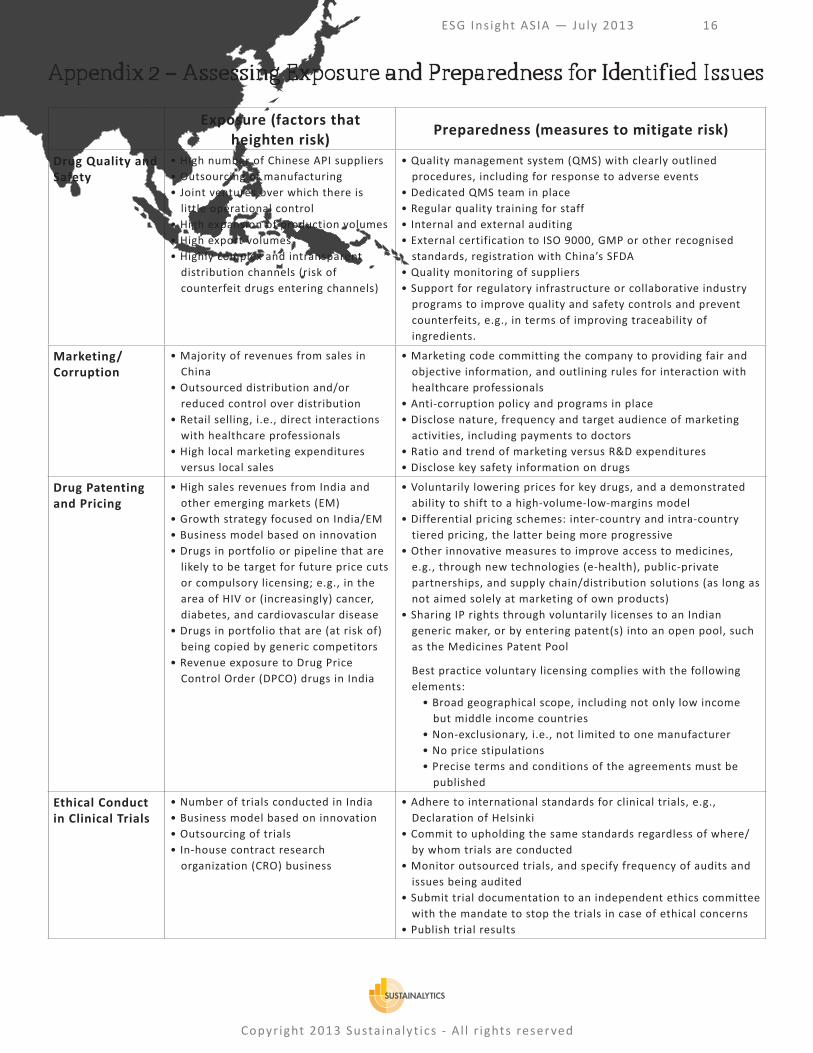

Appendix 2 – Assessing Exposure and Preparedness for Identified Issues

Exposure (factors that heighten risk) Preparedness (measures to mitigate risk)

Drug Quality and Safety

• High number of Chinese API suppliers• Outsourcing of manufacturing• Joint ventures over which there is

little operational control• High expansion of production volumes• High export volumes• Highly complex and intransparent

distribution channels (risk of counterfeit drugs entering channels)

• Quality management system (QMS) with clearly outlined procedures, including for response to adverse events

• Dedicated QMS team in place• Regular quality training for staff• Internal and external auditing• External certification to ISO 9000, GMP or other recognised

standards, registration with China’s SFDA• Quality monitoring of suppliers• Support for regulatory infrastructure or collaborative industry

programs to improve quality and safety controls and prevent counterfeits, e.g., in terms of improving traceability of ingredients.

Marketing/ Corruption

• Majority of revenues from sales in China

• Outsourced distribution and/or reduced control over distribution

• Retail selling, i.e., direct interactions with healthcare professionals

• High local marketing expenditures versus local sales

• Marketing code committing the company to providing fair and objective information, and outlining rules for interaction with healthcare professionals

• Anti-corruption policy and programs in place• Disclose nature, frequency and target audience of marketing

activities, including payments to doctors• Ratio and trend of marketing versus R&D expenditures• Disclose key safety information on drugs

Drug Patenting and Pricing

• High sales revenues from India and other emerging markets (EM)

• Growth strategy focused on India/EM• Business model based on innovation• Drugs in portfolio or pipeline that are

likely to be target for future price cuts or compulsory licensing; e.g., in the area of HIV or (increasingly) cancer, diabetes, and cardiovascular disease

• Drugs in portfolio that are (at risk of) being copied by generic competitors

• Revenue exposure to Drug Price Control Order (DPCO) drugs in India

• Voluntarily lowering prices for key drugs, and a demonstrated ability to shift to a high-volume-low-margins model

• Differential pricing schemes: inter-country and intra-country tiered pricing, the latter being more progressive

• Other innovative measures to improve access to medicines, e.g., through new technologies (e-health), public-private partnerships, and supply chain/distribution solutions (as long as not aimed solely at marketing of own products)

• Sharing IP rights through voluntarily licenses to an Indian generic maker, or by entering patent(s) into an open pool, such as the Medicines Patent Pool

Best practice voluntary licensing complies with the following elements:

• Broad geographical scope, including not only low income but middle income countries

• Non-exclusionary, i.e., not limited to one manufacturer• No price stipulations• Precise terms and conditions of the agreements must be

published

Ethical Conduct in Clinical Trials

• Number of trials conducted in India• Business model based on innovation• Outsourcing of trials• In-house contract research

organization (CRO) business

• Adhere to international standards for clinical trials, e.g., Declaration of Helsinki

• Commit to upholding the same standards regardless of where/by whom trials are conducted

• Monitor outsourced trials, and specify frequency of audits and issues being audited

• Submit trial documentation to an independent ethics committee with the mandate to stop the trials in case of ethical concerns

• Publish trial results

ESG Ins ight ASIA — July 2013 17

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

Appendix 3 – Sample Company AssessmentsPlease note that customized assessments are available for the following companies upon request: Please email

Assessment: As a global pharmaceutical innovator company, Roche’s approach to patenting and pricing issues is considered crucial to creating shared value in the realm of public health. Roche’s growth strategy is explicitly focused on seven key emerging markets, including India and China. Its oncology focused drug portfolio makes the company particularly susceptible to patenting and pricing pressures. The company has not been proactive in addressing these issues through patenting and pricing strategies tailored to emerging markets, thus potentially missing out on access to untapped markets. In line with many of its peers, Roche tends to aggressively defend its IP rights in court; the high profile nature of Roche’s current Indian court battles could, however, damage the company’s reputation in the country. Overall, this puts Roche in a very high risk category compared to many of its peers.

Exposure: High – Roche’s business model relies heavily on innovation; in 2011 Roche spent more than any of its peers on R&D as a percentage of sales.40 Compared to its competitors, Roche faces particularly high exposure to patenting and pricing pressures in emerging markets. This is in great part due to its portfolio focus on oncology, a disease area where we have already seen and can expect to see more compulsory licensing, as non-communicable diseases are on the rise in emerging markets.

Some of its drugs are being eyed by Indian generic competitors; Cipla, for instance, is in the process of copying Roche’s lung cancer treatment Tarceva, and in September 2012 Roche lost an appeal in the Delhi High Court to stop them from doing so. Furthermore, in November 2012, India’s Intellectual Property Appellate Board invalidated Roche’s patent for its Hepatitis-C drug Pegasys, after it was challenged by a public health group. And in January 2013, the Indian government initiated the process to issue a compulsory license on the breast cancer drug Herceptin. However, The question remains whether local generics producers will have the technical capacity to seize the Herceptin opportunity, since the drug belongs to a class of biologics called monoclonal antibodies, and biologics products are notoriously hard to copy.

Roche’s growth strategy is explicitly focused on what it has defined as its seven key emerging markets: Brazil, China, India, Mexico, Russia, South Korea and Turkey.41 Although Roche outperformed the Chinese market in 2012, the company experienced negative sales growth of -23 per cent in India.

Preparedness: Low – Roche’s preparedness is on the low side, since the company has been late in moving to a volume-over-margins approach, its access to medicine (AtM) programs are of limited scope, and AtM is not sufficiently integrated into the company’s core business. For example, Roche announced in February 2013 that it would reduce its Herceptin price in India by 31 per cent and its MabThera price by 53 per cent by working with local manufacturer Emcure. The company views co-marketing with a local partner as a way to increase access while reducing the risk of compulsory licensing.42 However, co-marketing seems a reactive rather than proactive measure, since it followed intensive civil society campaigns. Roche states that as of 2012 it is piloting differential pricing programs, an approach it had previously resisted. The approach so far seems to concern only a small proportion of Roche’s portfolio, and there is no indication of whether differential pricing strategies are applied to new drugs launched in India and other emerging markets.

Track record: In 2012, Roche was involved in two court battles in India concerning Tarceva and Pegasys (see above). Like many of its peers, the company has been aggressive in defending its IP rights, but Roche’s involvement in high profile court battles in India exceeds the industry average. As such, the company’s reputation in the country is on the line,

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

endangering opportunities for future collaboration with local partners and inviting further opposition from increasingly well-organized civil society groups.

Questions for engagement:

• What proactive steps is Roche taking with new drugs launched in India and other emerging markets to increase access and pre-empt the risk of compulsory licensing or other IP challenges?

• To what extent does Roche plan to expand its differential pricing program, both in terms of market coverage and portfolio coverage?

Sihuan Pharmaceuticals (China) Product Quality and Safety

Assessment: As the leading domestic Chinese pharmaceutical firm, Sihuan Pharmaceuticals has the largest market share of China’s cardio-cerebral vascular drug market, ahead of even MNCs like Pfizer and Sanofi. The company plans to expand into the North American, European, and Japanese markets, but its ability to do so successfully will hinge on its capacity to embrace best practice, and meet more thorough regulatory standards in the area of product quality and safety. As yet, there is no evidence that Sihuan is making efforts to go beyond compliance with Chinese regulations.

Exposure: Moderate – The company’s in-house manufacturing of pharmaceuticals and related products gives Sihuan a large degree of control over the quality and safety of its products. Nevertheless, Sihuan’s risk of product quality and safety violations is increased by its high production volumes and strong focus on rapid sales growth, particularly as the company seeks access to developed markets.

Preparedness: Low to Moderate – The company has a dedicated quality management team, to ensure that its own process and products are in order and that regulatory compliance is maintained. However, Sihuan shows little evidence that it goes beyond Chinese regulatory compliance; there is no evidence that the company adheres to international best practice standards, such as the Good Manufacturing Practice standards of the U.S. or EU. Sihuan’s sino-centric market exposure has rendered this approach adequate for now, but its inexperience with international best practice and more stringent quality and safety requirements may potentially hinder its growth into developed markets.

Track record: No information – There is no evidence that Sihuan has been involved and/or implicated in product quality and safety violations.

Marketing/Corruption

Assessment: Sihuan’s sharp increase in spending on marketing and sales results in increasingly direct contact with healthcare professionals, which leaves the company highly exposed to potential corruption and other improper marketing practices. Lacking any disclosure on policies or programs to mitigate these risks, Sihuan is at high risk of being involved in improper marketing, even though there is no direct evidence of this being the case.

Exposure: High – In recent years Sihuan has exponentially increased its spending on marketing and has aggressively increased the promotion of its products through direct contact with healthcare professionals, academic conferences, and direct seminars for doctors. Concurrently, its sales revenue has almost doubled. In 2011, Sihuan reported that it organized 10 national medical conferences, 59 provincial medical conferences, and 1,357 departmental seminars in various hospitals across China. It explicitly states that these activities are conducted with the primary aim of promoting its brand. Such activities make the company highly vulnerable to involvement in corrupt or otherwise improper marketing practices, including off-label marketing.

ESG Ins ight ASIA — July 2013 19

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

Preparedness: Low – Sihuan does not disclose any policies on bribery and corruption. Similarly, it does not disclose any policy or accountability program covering its interactions with healthcare professionals and hospital purchasing agents. Its aggressive marketing stance and interactions with healthcare professionals with explicit promotional intent indicates that the company may not have appropriate controls in place.

Track record: No information – There is no evidence that Sihuan has been involved and/or implicated in corruption or illicit marketing practices. However, numerous reports allege corrupt pharmaceutical marketing practices in China, such as payments to doctors and hospital purchasing officials. It should be noted that when allegations involve domestic firms, the companies involved often remain conspicuously unnamed.

Questions for engagement:

• What steps has the company taken to embrace international best practice on product quality and safety?• What controls does the company have in place to ensure appropriate interaction with healthcare professionals?• What controls does the company have in place to ensure the appropriate marketing of its products?

Cipla (India)Clinical Trials

Assessment: Cipla has moderate exposure to the possibility of ethical violations in clinical trials. The company’s preparedness is very low in comparison with its Indian peers, and the company has been alleged to be in collusion with the Indian drug authorities. Overall this indicates that the company is at high risk for negative involvement in this regard.

Exposure: Moderate – Cipla has initiated some 30 clinical trials since 2008,43 which is close to the average involvement of its peers. Since Cipla’s business model is not based on innovation, its risk exposure is not expected to rise much in future. Cipla’s trials are all conducted in India, where trial regulations are rather lax and poorly enforced. There is no evidence that the company outsources its trials.

Preparedness: Low – In contrast to its peers, Cipla does not reference any ethical standards for clinical trial conduct, such as Good Clinical Practice (GCP) guidelines or the Helsinki Declaration. There is no evidence that the company has GCP auditors or an ethical committee in place.

Track record: Mixed – In May 2012, a report by an Indian parliamentary committee accused Cipla, along with a number of other companies (mainly MNCs) of colluding with the Drug Controller General of India to allegedly violate drug approval norms. Cipla specifically was accused of failing to conduct mandatory clinical studies for two drugs. The company has denied the charges of collusion and claimed that clinical trials were not mandatory for the two drugs in question. There is no evidence that Cipla has been involved in any ethical breaches in conducting clinical trials, but company specific information on such breaches is generally sparse.

Patenting and Pricing

Assessment: Cipla has positioned itself as a champion of access to medicines, leveraging its generics production capacity to make life saving drugs available at affordable prices for millions around the world, seeking to profit from a diversified product portfolio and volume of sales, while undercutting competitors. However, though much of its arguably self-serving strategies have contributed to increased access to medicine, Cipla also risks lawsuits from patent holders and has drawn the notice of authorities in India over violations of Drug Price Control Orders (DPCOs). A close examination of the company thus paints a complex picture.

ESG Ins ight ASIA — July 2013 20

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

Exposure: High – As one of the largest generic drug manufacturers in India, Cipla has a high level of exposure to pricing and patenting issues. Its domestic revenue comprises almost half of its total revenue while an unspecified, but large portion of its product portfolio in India is subject to DPCOs. Cipla also has two antibiotics and one drug for cardiovascular disorders in the development pipeline, all of which fall within areas of treatment that make them potential targets for price controls. Additionally, Cipla has adopted an aggressive strategy not just on patents as it relates to the production of generics, but on drug pricing which has increased its exposure to risks on both fronts.

Preparedness: Moderate to High – Since the introduction of drug product patents in India in 2005, Cipla has repeatedly gone to court to challenge patents in order to protect its ability to manufacture generic copies of key drugs. These actions demonstrate that the company is prepared and able to strategically litigate to promote its volume and largely generics driven business model. Cipla has also, through its expansive generics manufacturing capacity, positioned itself to benefit as drugs come off patent or have had their patents successfully challenged. This capacity, combined with a diversified product portfolio, has played a large part in giving Cipla the room needed to sharply undercut market prices, particularly on antiretroviral (ARV) and cancer drugs. However, the company has not developed an access to medicines policy or consistent strategy.

Track record: Mixed – Cipla is well known for its fierce, if self-serving, support for compulsory licensing and its efforts to challenge the validity of patents held by pharmaceutical MNCs, in spite of significant pushback from MNC patent holders. For instance, the company is embroiled in on-going litigation with Pfizer over its cancer drug Sutent. In 2001, Cipla sparked a price war when it released its generic ARV cocktail for a fraction of the market price, forcing its domestic peers and MNCs to do the same, which hugely increased access to these lifesaving drugs. In 2012, Cipla announced that it was cutting the price of three of its major cancer drugs by 65 to 70 per cent, which again forced the rest of the market to similarly cut prices and yet again sharply increased patient access to critical drugs. However, at the same time, Cipla is considered by the National Pharmaceutical Pricing Authority of India to be both the largest offender when it comes to violating maximum selling prices and the largest defaulter on fines issued for overpricing. As of April 2013, the company had not paid any pricing-related fines, instead choosing to contest them in court in a case that is still pending, and has refused to make so-called “good faith” partial payment deposits.

Questions for engagement:• What ethical standards for clinical trials does the company have in place and how are these enforced?• Is Cipla planning to develop a more structural access strategy, in line with its positive access efforts thus far?• How does Cipla plan to engage with the drug pricing authority in such a way as to not jeopardize its access efforts?

ESG Ins ight ASIA — July 2013 21

Copyr ight 2013 Susta inalyt ics - A l l r ights reserved

Endnotes1 A global patenting regime was implemented through the Agreement on Trade Related Aspects of Intellectual Property Rights (TRIPS, 1994), administered by the

World Trade Organization (WTO). Subsequent amendments to TRIPS, which were implemented in 2001, enable states to prioritize public health crises over IP rights. By issuing compulsory licenses, states can effectively overrule the patent holder’s right to exclusive marketing for a particular drug.

2 Booz & Company, “Pharma Emerging Markets 2.0 - How Emerging Markets Are Driving the Transformation of the Pharmaceutical Industry,” 2013.

3 IMS Health website, accessed May 2013.

4 Booz & Company, “Pharma Emerging Markets 2.0 - How Emerging Markets Are Driving the Transformation of the Pharmaceutical Industry,” 2013.

5 The Wall Street Journal, “China Halts Sale of Some Drugs,” 17 April 2012.

6 International Policy Network, “Combating the spread of fake drugs in poor countries,” May 2009.

7 Off-label marketing refers to the common, but illegal, practice of promoting a product for a purpose or target group for which it has not been approved by marketing authorities.

8 China’s five-year plans contain detailed social and economic development guidelines and objectives.

9 PMLive, “China has more pharma sales reps than US for first time,” 23 May 2012.

10 People’s Daily Online, “China uncovers 1,001 commercial bribery cases in health sector,” March 2008.

11 China Daily, “Hospital staff members jailed for taking bribes,” 25 October 2012.

12 The Guardian, “China accuses GlaxoSmithKline of paying ₤300m in bribes,” 15 July 2013.

13 World Bank, World Development Indicators, 2010.

14 Booz & Company, “Pharma Emerging Markets 2.0 - How Emerging Markets Are Driving the Transformation of the Pharmaceutical Industry,” 2013.

15 The “patent cliff” refers to the sharp decline in profits experienced by the industry between 2008 and 2014 due to patent expiration of numerous blockbuster drugs.

16 Also commonly called “tiered pricing,” “variable pricing” or “flexible pricing,” this term refers to the practice of adjusting price levels based on income.

17 While many MNCs employ some form of inter-country differential pricing (i.e. charging lower prices in less developed countries), intra-country differential pricing is even more progressive in the sense that individual income levels are taken into account.

18 Voluntary licensing is the practice of giving competitor(s) the right to produce and market copies of a patented drug (typically in exchange for a royalty fee). This usually results in lower market prices.

19 The term ”clinical trials” refers to the various stages of drug testing on humans that are required in order for a new drug to attain marketing approval.

20 The Times of India, “436 killed in clinical trials last year,” 23 February 2013.

21 The Helsinki Declaration, developed by the World Medical Association, is a statement of ethical principles for medical research involving human subjects.

22 This excludes traditional Chinese medicine.

23 GBI Research, “China Pharmaceutical Market Outlook - Government Incentives, Healthcare Reform and a Rapidly Ageing Population Provide Strong Stimulus for Growth,” February 2013.

24 International Diabetes Federation website, accessed May 2013.

25 McKinsey & Company, “Health care in China: Entering ‘uncharted waters’,” November 2012.

This report was drafted in accordance with the agreed work to be performed and reflects the situation as on the date of the report. The information on which this report is based has – fully or partially – been derived from third parties and is therefore subject to continuous modification. Sustainalytics observes the greatest possible care in using information and drafting reports but cannot guarantee that the report is accurate and/or complete. Sustainalytics will not accept any liability for damage arising from the use of this report, other than liability for direct damage in cases of an intentional act or omission or gross negligence on the part of Sustainalytics.

Sustainalytics will not accept any form of liability for the substance of the reports, notifications or communications drafted by Sustainalytics vis-à-vis any legal entities and/or natural persons other than its direct principal who have taken cognisance of such reports, notifications or communications in any way.