Philippine Economy: In sweet spot, but facing difficult global challenges and has a lot of catching up to do. Felipe M. Medalla Monetary Board Member Bangko Sentral ng Pilipinas September 25, 2012

Transcript

Philippine Economy: In sweet spot, but facing

difficult global challenges and has a lot of catching up to do.

Felipe M. MedallaMonetary Board Member

Bangko Sentral ng PilipinasSeptember 25, 2012

• 1. Philippine Economy is in a sweet spot, but monetary policy in the advanced economies pose difficult challenges for Philippine economic policy makers.

• 2. Weak advanced economies reduce our growth prospects in second half of 2012 and in 2013

• 3. Weak economy in US means another round of QE• 4. Rising sovereign bond yields for troubled economies in Euro

zone (e.g., Spain and Italy) mean ECB will have its own version of QE (what Draghi called Outright Monetary Transactions).

• 5. #3 and #4 mean more portfolio inflows (which means lower GS yield and upward pressure on the peso)

• 6. If non-residents are buying Phil GS, where will Filipinos and Philippine Banks put their money?

• 7. Will #6 result in bubbles and too much credit growth than is good for our macroeconomic and financial stability?

Philippines is in a “mini” demographic transition. The fastest growing segment of our population is from age groups which earn and save more.

The demographic transition raised our savings rate....

and, together with OFW remittances, generated 10 consecutive years of current account surplus in our balance of payments (which raised our GIR, making our external balance virtually invulnerable to global shocks like the collapse of Lehman). In short, we don’t need foreign funds.

Passage of EVAT and our external surpluses moved us out of the vicious cycle of public debt (high deficit and depreciating currency high credit spreads high interest expense of the government high deficit…)

6

Philippine Fiscal Deficit is very managable (especially if congress passes the sin tax and fiscal incentives rationalization laws)

Market perceptions of improving Philippine sovereign credit risk are way ahead of credit rating agencies.

8

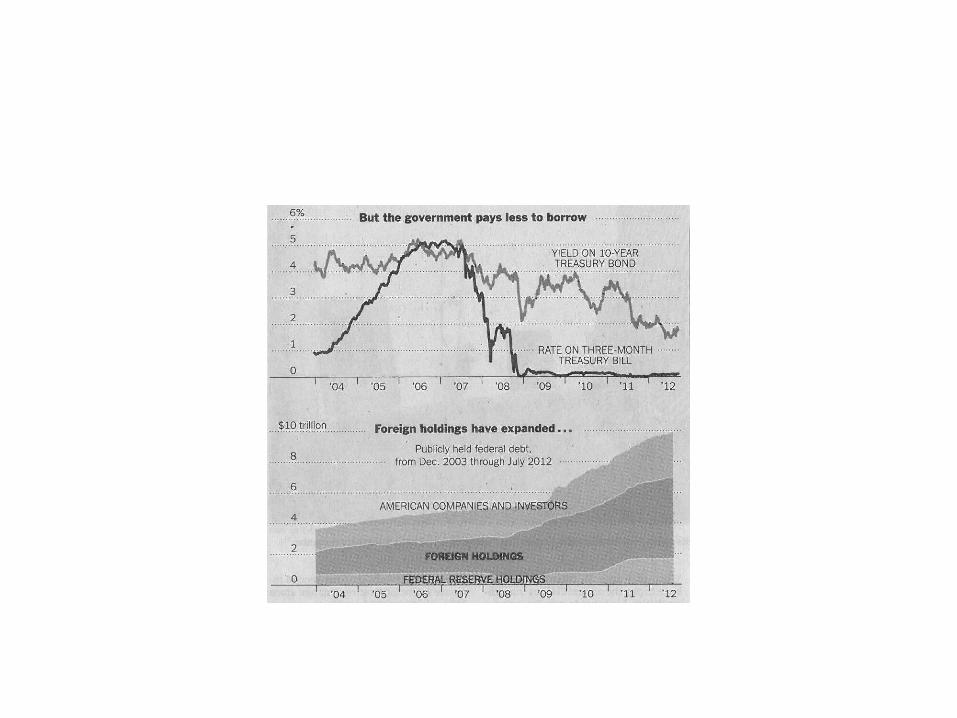

Both the slope and intercept (level) of the GS Yield curve fell significantly.

…significantly expanding the national government’s fiscal space.

10

With the fall in interest rates and appreciation of the peso, our economy has outgrown our public debt.

Source:

Economic growth in the first two quarters surprised most economists.

Even if the BOP crisis years (1984, 1985, 1991, and 1998), average GDP growth between 1950 and 2010 was only 5%. Share of Industry in GDP fell from a peak of 42% in the early 1980s to 32%. Moreover, seasonally adjusted quarter on quarter GDP growth is quite low.

The sectors that declined (in terms of employment shares) are the sectors that have to compete with imports in the domestic market or with exports from other countries in foreign markets.

Much of the increase in service sector employment is associated with low wages or non-wage income.

Service Sector employment is in the non-tradeable sectors(does not compete with foreign producers) and has strong links with the informal sector and coping with poverty (e.g., daughters of farmers working as maids in the cities) and government payrolls (teachers, government employees, police and military personnel).

Break down of Service Sector Share in Total Employment :Jan 2012 LFSServices 52.7Wholesale and retail trade; repair of motor vehicles and motorcycles 19.3Transportation and storage 6.9Accommodation and food service activities 3.2Information and communication 0.9Financial and insurance activities 1.3Real estate activities 0.4Professional, scientific and technical activities 0.5Administrative and support service activities 2.3Public administration and defense; compulsory social security 5Education 3.4Human health and social work activities 1.2Arts, entertainment and recreation 0.9Other service activities 2.3Activities of households as employers; undifferentiated goods and services 4.9

The fall in the share of manufacturing and the rise in the share of services in our country look more similar to what happened to the sectoral employment shares in rich advanced economies than in developing economies.

The “maturation” of labor export has resulted in a signficant drop in the growth rate of OFW remittances. (Aside from BPO, what will take the place

of the high growth rates of remittances?)

26

Figure 2. Gross Fixed Capital Formation as % of GDP: Selected Asian Economies

Birth rates fell much less in the Philippines than in Indonesia and Thailand

Fertility rates among well-off and better educated mothers is now close to replacement rate. Those of poor and less educated mothers are significantly higher than their desired fertility and are nearly twice replacement rates.

Why according to Benanke, the academic, QE might work (even in the absence of fiscal stimulus).

“He refers, of course, to the fact that the BOJ has for some time now pursued a policy of setting the call rate, its instrument rate, virtually at zero, its practical floor. Having pushed monetary ease to its seeming limit, what more could the BOJ do?.... Isn’t Japan stuck in what Keynes called a .“liquidity trap.”? ….Far from being powerless,the Bank of Japan could achieve a great deal if it were willing to abandon its excessive caution … The argument that current monetary policy in Japan is in fact quite accommodative rests largely on the observation that interest rates are at a very low level. I do hope that readers who have gotten this far will be sufficiently familiar with monetary history not to take seriously any such claim based on the level of the nominal interest rate. However, as I will argue in the remainder of the paper, liquidity trap or no, monetary policy retains considerable power to expand nominal aggregate demand. I will illustrate by discussing a mechanism that is highly relevant in Japan today, the so-called “balance-sheet channel of monetary policy.”.. Therefore money issuance must ultimately raise the price level, even if nominal interest rates are bounded at zero. …..I believe that a policy of aggressive depreciation of the yen would by itself probably suffice to get the Japanese economy moving again… Suppose the Bank of Japan prints yen and uses them to acquire foreign assets..

ECB is doing its own version of QE, to improve the balance sheet of troubled banks and countries.

BSP purchases of forex have been largely sterilized using our SDAs.