19

PHILIPPINE MANUFACTURING INDUSTRY ROADMAP and GLOBAL VALUE CHAINS Rafaelita M. Aldaba Ateneo de Manila University Professional Schools, Rockwell, Makati City November 12, 2014 1

| Date post: | 21-Dec-2015 |

| Category: |

Documents |

| Upload: | merilyn-gallagher |

| View: | 219 times |

| Download: | 1 times |

PHILIPPINE MANUFACTURING INDUSTRY ROADMAP and

GLOBAL VALUE CHAINS Rafaelita M. Aldaba

Ateneo de Manila UniversityProfessional Schools, Rockwell, Makati City

November 12, 2014

1

Outline

Objective: implications of GVCs on the growth & development of PH manufacturing • Global Value Chains• Manufacturing Performance• Philippine Manufacturing Industry Roadmap• Services Vision and Strategy• Future Implications

2

Part 1: GVCsSTAN SHIH’S SMILE CURVE

• Opportunities for upgrading & diversification in both upstream & downstream in goods & services

• Strategic positioning in the GVC

HIGHER

VALUE ADDED

LOWER

MANUFACTURE

MARKETINGBRANDING

DESIGN DISTRIBUTION

TIME

SALES, AFTER SERVICECONCEPT, R&D

3

Distribution of value for Iphone

• GVCs require high quality services embodied in production & increasingly outsourced

• US (Apple) captures 58.5% of Iphone sales price• Korea: 5%• Japan: 0.5%; China: 1.8%• Most value: product design, software development, product management,

marketing & other high wage functions kept by Apple• Trend: dispersion of functions

Source: Kraemer et al 2011Apple profits

58%

Non-Apple

US profits

2%

EU profits

1%

Tai-wan

profits0%

Japan profits

0%

S. Ko-rea

profits5%

Unidentified profits

5%

Cost of in-puts ma-teri-als

22%

Cost of inputs China labor2%

Cost of inputs non-China labor

3%

4

Distribution of Value for Ipad

• For Ipad, US: 30% & 15% distribution & retail• Korea: 7%, Taiwan: 2%, China: 2%

Source: Kraemer et al 2011

Apple profits30%

Distribution & retail

15%

Non-Apple US profits2%

Taiwan profits2%

Japan profits1%

S. Korea profits7%

Unidentified profits

5%

Cost of in-puts mate-

rials31%

Cost of inputs China labor

2%

Cost of inputs non-China labor

5%

5

Auto Global Value ChainFUNCTION R&D &

DESIGNMATERIAL SUPPLY

PARTS SOURCING

PARTS INTEGRATION

ASSEMBLY MARKETING & SERVICES

COST FOR AUTOMAKERS

Low to medium: 10%

Low: <10% High: 40-70% Low: <10% Medium to high: 20%

(R&D, model design-Toyota, Honda, etc.)Standardizers

Material suppliers

Component specialists

Integrators 1st tier

Assemblers

Distributor

ExporterGlass, rubber, plastic, steel, textile, electronics

Body panels, mechanical & electrical Wheels, tires, seats,engines, transmission

6

Global auto production network

• Toyota’s IMV Project: transmission (Phils. & India), diesel engine (Thai), gas engine (Indonesia)

Source: Toyota Motor Corporation

7

Electronics GVC

8

Part 2: Impressive Growth PerformancePH as ASIA’S NEW ECONOMIC TIGER

• PH growth rate: 6.8 (‘12), 7.2% (’13, 2nd to China 7.7%)• H1 (’14): PRC 7.45%, MAL: 6.3%, PH 6%, INO 3.8%, TH -

0.1%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

GDP Growth

PHTHINOVNPRCMAL

9

Manufacturing Resurgence

• Industry growth: 7.3% (‘12); 9.3% (’13, highest)• Manufacturing resurgence: 5.4% (‘12); 10.3% (‘13); 8.8%

(H1’14)

20002001

20022003

20042005

20062007

20082009

20102011

20122013

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0Industry Growth

PHTHINOVNPRC

Year

in %

10

WHAT MAKES PH DIFFERENTMarket Opportunities• Growing market & middle class: demographic sweet spot Labor• Young, English speaking, highly trainable workforce• Moderate wage increasesOperating Environment• Strong macroeconomic fundamentals• Political stability, business/consumer confidencePolicy Focus• New Industrial Policy & a more pro-active Government• Industry programs to support manufacturing resurgence• Philippine Economic Zone Authority, Board of Investments, Subic,

Clark: investment facilitation, investor careImproved competitiveness ranking (World Economic Forum)• Rank #52 in 2014-15 from rank #59 11

Part 3: Roadmap for Structural Transformation

Vision: globally competitive manufacturing

-Rebuild capacity existing industries, strengthen emerging industries, maintain competitiveness of comparative advantage industries

-Participate as hubs in regional & global production networks for auto, electronics, machinery, garments, food

-Shift to high value added activities,investments in upstream industries -Link & integrate industries-SMEs & large enterprises

Phase I 2014-2017

Phase II 2018-2021

Phase III 2022-2025

12

Strategic Actions, Complementary Measures

30% value added; 15% employment

Horizontal measures

Coordination mechanism

Vertical measures

• Close supply chain gaps• Expand domestic market &

exports• HRD & skills• SME development• Technology upgrading,

innovation, green growth

• Investment promotion

• Power, smuggling, logistics & infrastructure

• Competitive exchange rate

open trade regime, sustainable macro policies, sound tax policies & administration, efficient bureaucracy, secure property rights, institutions that promote adaptive research & patent regime, access to finance & technology for SMEs

Required Components• Materials• Skills• Energy• Capital• Digital

technology

13

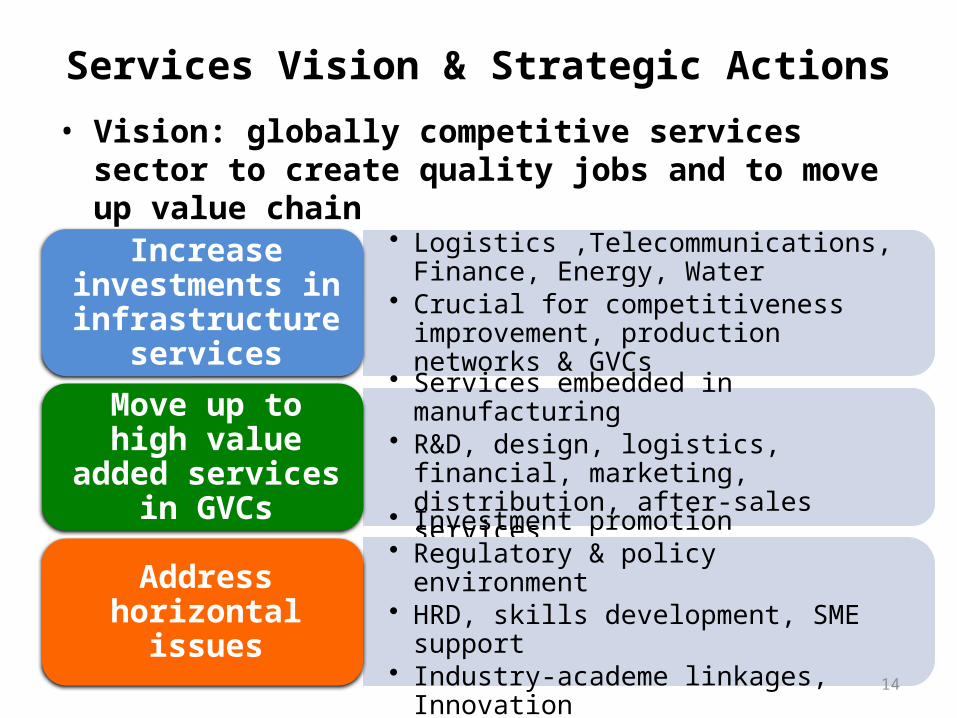

Services Vision & Strategic Actions• Vision: globally competitive services sector to create quality

jobs and to move up value chain

• Logistics ,Telecommunications, Finance, Energy, Water

• Crucial for competitiveness improvement, production networks & GVCs

Increase investments in infrastructure

services

• Services embedded in manufacturing• R&D, design, logistics, financial, marketing,

distribution, after-sales services

Move up to high value added services

in GVCs

• Investment promotion• Regulatory & policy environment• HRD, skills development, SME support • Industry-academe linkages, Innovation

Address horizontal issues

14

Manufacturing: Comparative Advantage• Motor vehicle• Engineered Products

– Motor vehicle: body panel stamping, engines, transmissions, transaxle, large injection molded parts

– E-vehicles: controller assembly, motor, battery, charging stations– Shipbuilding & Aerospace: parts & components

• Chemicals: oleochemicals, petrochemicals & derivatives, chlor-alkali • Auto electronics, LED, solar, office equipment, communication radar,

Electronic Data Processing, office equipment, consumer electronics• Virgin pulp paper• Copper wires & copper wire rods• Basic iron & steel products, long steel products, flat hot/cold rolled

products• Tool & die: simple, compound, & progressive dies for metal stamping

& forging; molds for die casting, plastic injection or blow molding; jigs & fixtures for metal cutting & forging

• Food Processing/Manufacturing15

Services: Comparative Advantage • Pool of skilled workers: main source of strength• Current comparative advantage : IT-BPM• Potential comparative advantage

Creative/knowledge-based services Services embedded in manufacturing Medical tourism, Tourism & travel related Educational, recreational, cultural & sporting Aircraft maintenance, repair, &overhaul Ship repair Distribution (retail, franchising) Construction & engineering Transport support

Energy, Public infrastructure & logistics, Public Private Partnership projects

16

IT-BPM Services from PHIT Application services Business Process services Engineering services

App dev’t & maintenance Application development AD integration & testing Application maintenanceSystem integration Analysis, Design Development Integration & testing Package implementationIT Infrastructure Services Help desk, Desktop support Data centre services Mainframe Network operations IT consultingSoftware product development New product development System testing Localization/Support Gaming

Horizontal processes Contact centers Human resources Finance & accounting Supply chain: procurement

logistics managementIndustry/vertical processes Banking & insurance Telecom Public sector, Utilities Health care, High-tech Oil & Gas, Consumer prodsKnowledge Process Outsourcing Business research, financial

research Animation Data analytics Legal process & patent

research Other high-end processes

Manufacturing engineering Upstream product

engineering- Concept design- Simulation- Design engineering Downstream product

engineering- CAD/CAM/CAE- Embedded software- Localization Plan & process

engineeringArchitecture design Design process Building

Management models

17

How to move up the GVC• Competitiveness: technology & human capital upgrading• Types of Upgrading: process, product, functional, chain• GVCs deepened globalization by affecting both

manufacturing & serviceso Services embedded in manufacturing

• Required components for manufacturing: Materials, Skills, Energy, Capital, Technologyo Human resource development & skills trainingso Power issueo Investment promotion o Manufacturing innovation ecosystem, link R&D to business, new

product development (3D printing could boost innovation)• GVC-oriented industrial policy

18

With or without AEC, we need to pursue a new industrial policy to make our industries

competitive and create an environment conducive to private sector development.

This could lead to more investments, increased competition, more innovation,

increased productivity, sustainable & inclusive growth, & more & better jobs!

THANK YOU!

19

![[Makati Urban Redevlopment Presentation : Makati City, Philipines]](https://static.documents.pub/doc/80x56/558624b4d8b42ac54a8b45f1/makati-urban-redevlopment-presentation-makati-city-philipines.jpg)