42

Planned Borrowing

| Date post: | 26-Dec-2015 |

| Category: |

Documents |

| Upload: | agnes-butler |

| View: | 213 times |

| Download: | 0 times |

Planned Borrowing

Planned Borrowing

Most people use installment credit 12+ times during their life.

Yet, only 1:3 shop for credit terms!

DID YOU KNOW!

Planned Borrowing

A knowing decision to borrow to finance a

purchase or simply to borrow cash.

Planning Your Credit Usage

• When

• How often

• How much

THE TASK OF DETERMINING:

The debt limit most people establish for

themselves is lower than what lenders would

be willing to lend.

Establishing a Debt Limit

• Debt-payments-to-disposable-income method

• Ratio of debt-to-equity method

• Continuous-debt method

Establishing a Debt Limit

Credit Capacity Indicators

*Not including housing

Debt Payments-to-Income Ratio

monthly payments*

monthly after tax income

6-9

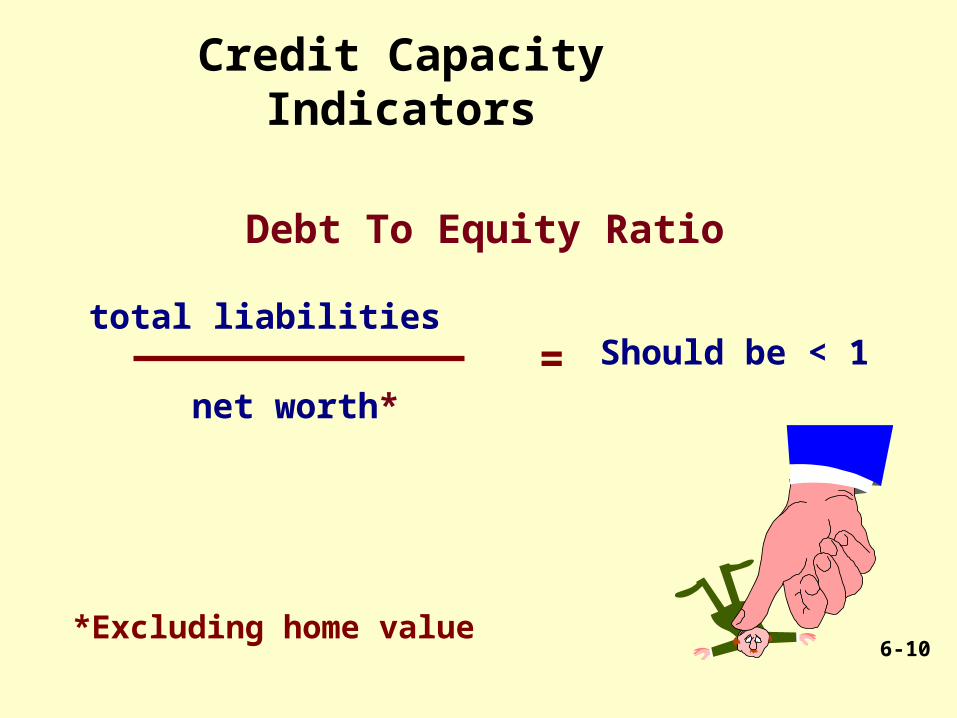

Credit Capacity Indicators

Debt To Equity Ratio

total liabilities

net worth*= Should be < 1

*Excluding home value6-10

Debt-Payment Limits as a Percentage of Disposable Income

Percent

For Current Debt*

Take on Additional Debt?

10 or less Safe limit; borrower feels little debt pressure.

Could be undertaken cautiously.

11 to 15 Possibly safe limit; borrower feels some pressure.

Should not be undertaken.

16 to 20 Fully extended; borrower hopes that no emergency arises.

Only the fearless or foolhardy ask for more.

21 to 25 Overextended; borrower worries about debt

No, borrower should see a credit counselor.

* Excluding home mortgage loans and convenience credit to be repaid in full when the bill arrives.

If one of the earners reduces/eliminates

earnings, debts that had been manageable with

two incomes may become overwhelming.

Setting Debt Limits for Dual-Earner Households

BEWARE!

• Installment loans

• Secured/unsecured loans

• Purchase loan installment contracts

The Language of Consumer Loans

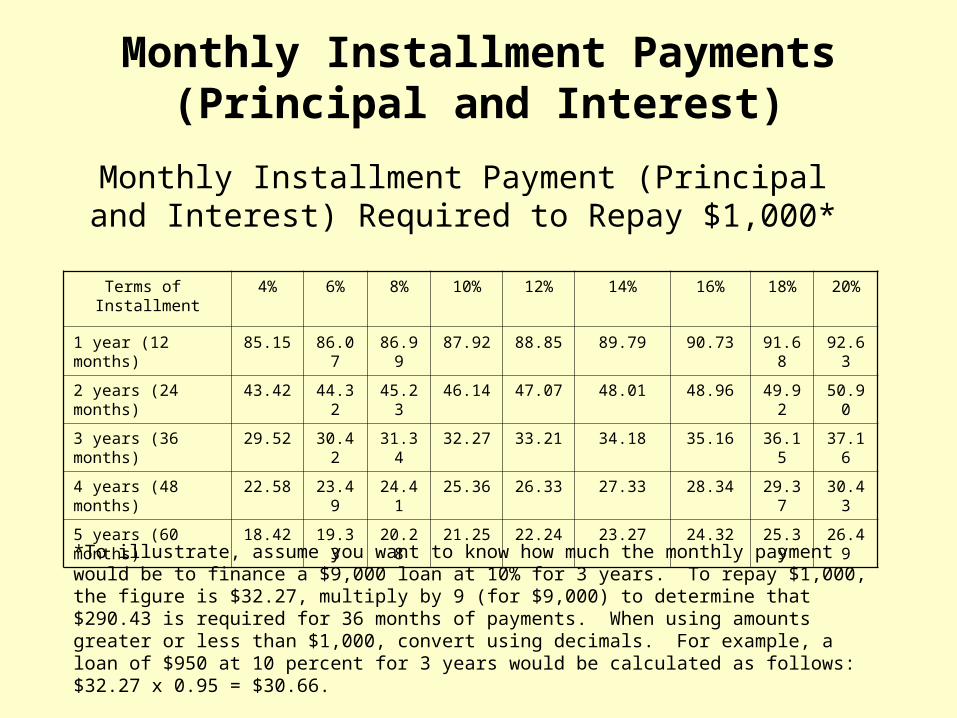

Monthly Installment Payments (Principal and Interest)

Terms of Installment

4% 6% 8% 10% 12% 14% 16% 18% 20%

1 year (12 months) 85.15 86.07 86.99 87.92 88.85 89.79 90.73 91.68 92.63

2 years (24 months) 43.42 44.32 45.23 46.14 47.07 48.01 48.96 49.92 50.90

3 years (36 months) 29.52 30.42 31.34 32.27 33.21 34.18 35.16 36.15 37.16

4 years (48 months) 22.58 23.49 24.41 25.36 26.33 27.33 28.34 29.37 30.43

5 years (60 months) 18.42 19.33 20.28 21.25 22.24 23.27 24.32 25.39 26.49

Monthly Installment Payment (Principal and Interest) Required to Repay $1,000*

*To illustrate, assume you want to know how much the monthly payment would be to finance a $9,000 loan at 10% for 3 years. To repay $1,000, the figure is $32.27, multiply by 9 (for $9,000) to determine that $290.43 is required for 36 months of payments. When using amounts greater or less than $1,000, convert using decimals. For example, a loan of $950 at 10 percent for 3 years would be calculated as follows: $32.27 x 0.95 = $30.66.

Sources of Consumer Credit

Parents and family members

Commercial bank

Credit union

Life insurance company

Savings and loan association

Finance company

Retailers

Cash advances

Truth In Lending Rights

The Truth In Lending Act requires creditors to provide you with accurate and complete credit costs and terms. APR

Creditors must disclosecredit terms and information... In a clear and conspicuous manner In a form you can keep

Calculating Finance Charges and APR

•Simple-interest method

•Discount method

APR CALCULATIONS FOR SINGLE-PAYMENT LOANS:

Calculating Finance Charges and APR

•Simple-interest method

•Add-on method

•Discount method

APR CALCULATIONS FOR INSTALLMENT LOANS:

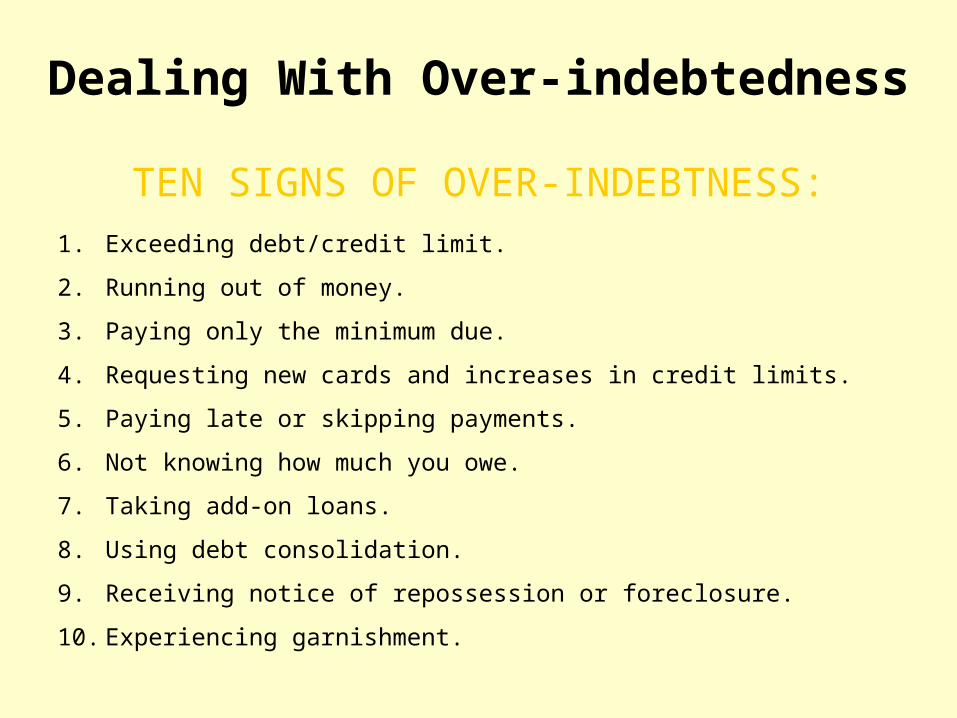

Dealing With Over-indebtedness

TEN SIGNS OF OVER-INDEBTNESS:

1. Exceeding debt/credit limit.

2. Running out of money.

3. Paying only the minimum due.

4. Requesting new cards and increases in credit limits.

5. Paying late or skipping payments.

6. Not knowing how much you owe.

7. Taking add-on loans.

8. Using debt consolidation.

9. Receiving notice of repossession or foreclosure.

10. Experiencing garnishment.

Dealing With Over-indebtedness

• Federal law regulates debt collection

• Bankruptcy as last resort

• Chapter 13

• Chapter 7

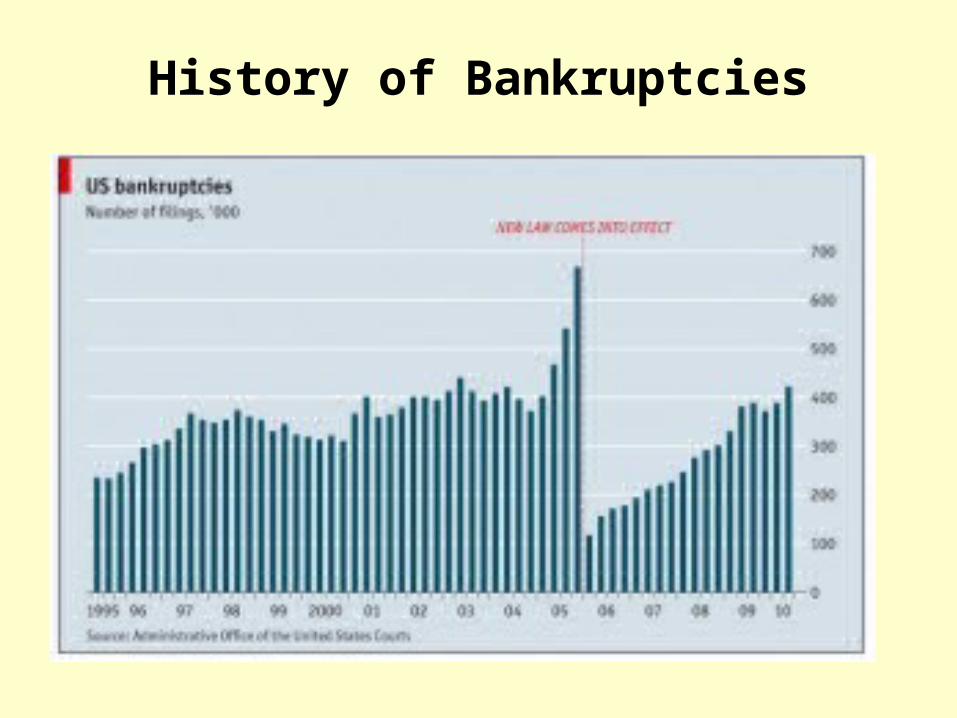

History of Bankruptcies

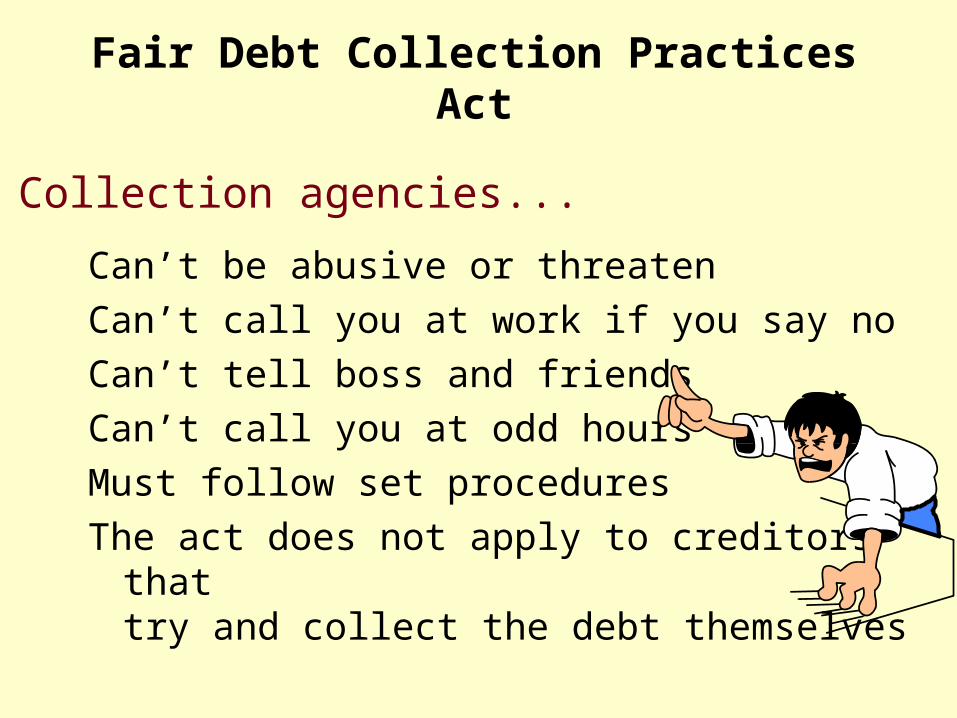

Fair Debt Collection Practices Act

Can’t be abusive or threaten

Can’t call you at work if you say no

Can’t tell boss and friends

Can’t call you at odd hours

Must follow set procedures

The act does not apply to creditors thattry and collect the debt themselves

Collection agencies...

Impact ofDivorce on Credit

• Pay attention to accounts held jointly

• Ask creditors to close joint accounts

• Remember, creditors can legally collect from either party

• Get updated copy of credit report

Alternative Lenders

• Pawnshop

• Rent-to-own program

• Check cashers

• Rapid refund services

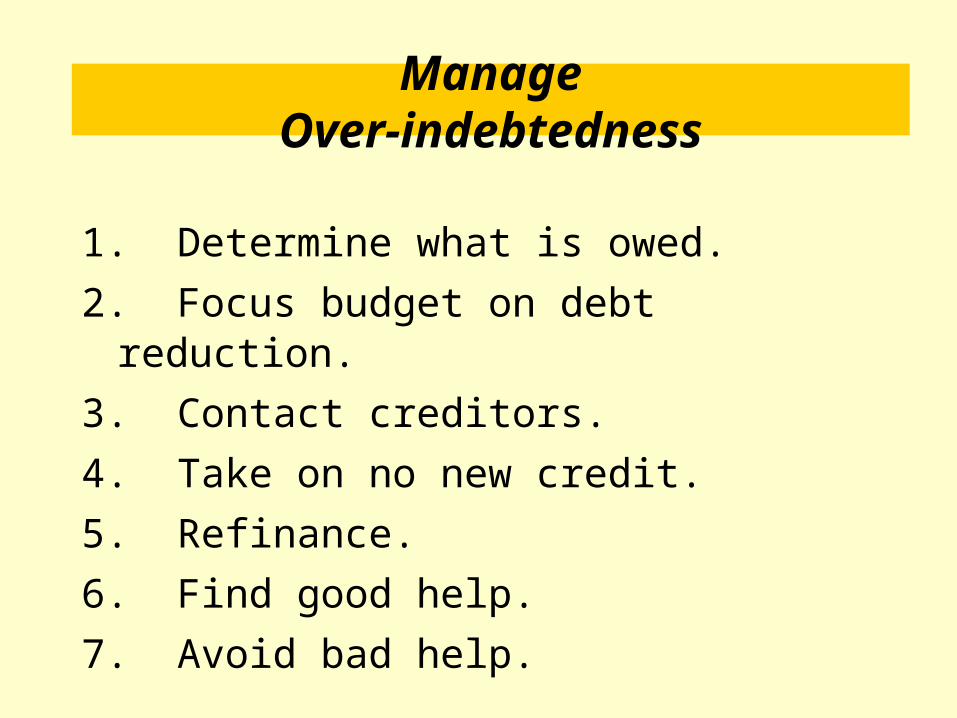

ManageOver-indebtedness

1. Determine what is owed.

2. Focus budget on debt reduction.

3. Contact creditors.

4. Take on no new credit.

5. Refinance.

6. Find good help.

7. Avoid bad help.

Manage StudentLoan Debt

1. Choose most advantageous repayment

pattern allowed.

2. Consolidate student loans.

3. Pay electronically.

4. Be punctual with repayments.

5. Refinance with second mortgage loan.

Automobiles and Other Major Purchases

Guidelines for Wise Buying

• Control buying on impulse

• Pay cash

• Buy at the right time

• Don’t pay extra for a “name”

• Recognize the high price of convenience shopping

• Use life-cycle planning for major purchases

• Calculate unit pricing or price per hours worked.

Steps Before Interacting with Seller

• Prioritize wants

• Do pre-shopping research

• Price

• Trade-in

• Cost of financing

• Fit expenditure into budget

Purchasing a Car: A Research-Based Approach - Phase 1: Preshopping

Activities

Problem identification. Information gathering.

• Personal contacts.• Media information-television, websites • Independent testing organizations- Consumer

Reports• Government agencies. • Online Sources – www.edmunds.com,

www.caranddriver.com, www.autoweb.com

Phase 2: Evaluation of Alternatives

Comparison shopping.Selecting vehicle options-convenience, appeal, etc.Comparing used vehicles- www.carmax.com,

www.carfax.com Leasing an automobile 1) lower payments, small initial cash outlay 2) no ownership in vehicle 3) maximum # of miles/year; charged for extra miles. 4) know the capitalized cost of the lease, the money factor, the monthly payment, number of payments, and the residual value.

8-8

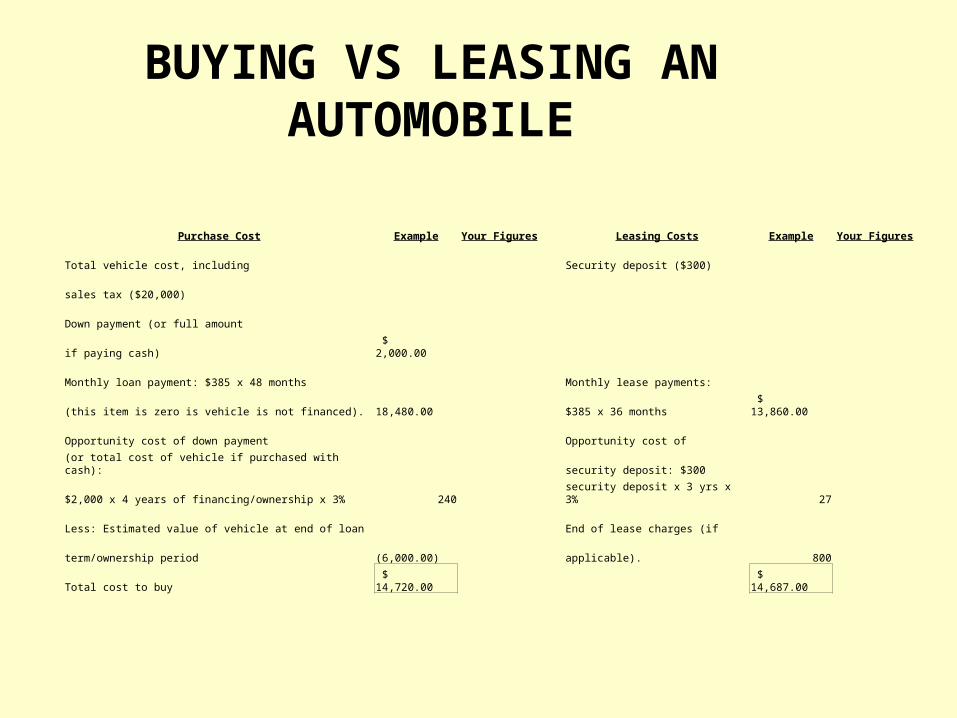

BUYING VS LEASING AN AUTOMOBILE

Purchase Cost Example Your Figures Leasing Costs Example Your Figures

Total vehicle cost, including Security deposit ($300)

sales tax ($20,000)

Down payment (or full amount

if paying cash) $ 2,000.00

Monthly loan payment: $385 x 48 months Monthly lease payments:

(this item is zero is vehicle is not financed). 18,480.00 $385 x 36 months $ 13,860.00

Opportunity cost of down payment Opportunity cost of

(or total cost of vehicle if purchased with cash): security deposit: $300

$2,000 x 4 years of financing/ownership x 3% 240 security deposit x 3 yrs x 3% 27

Less: Estimated value of vehicle at end of loan End of lease charges (if

term/ownership period (6,000.00) applicable). 800

Total cost to buy $ 14,720.00 $ 14,687.00

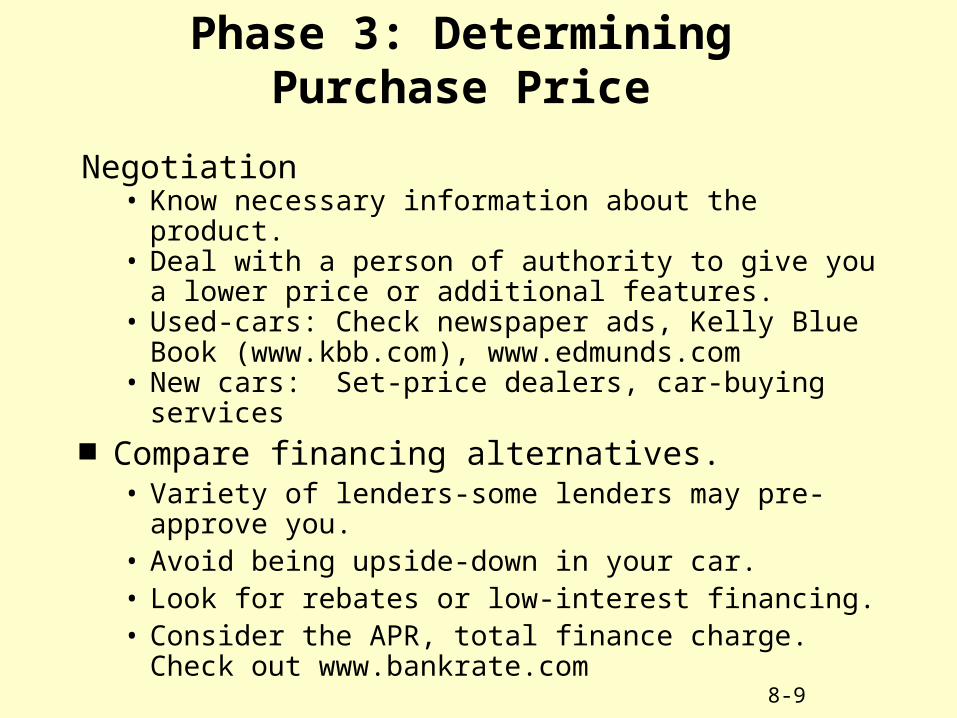

Phase 3: Determining Purchase Price

Negotiation • Know necessary information about the product.• Deal with a person of authority to give you a lower

price or additional features.• Used-cars: Check newspaper ads, Kelly Blue Book

(www.kbb.com), www.edmunds.com • New cars: Set-price dealers, car-buying services

Compare financing alternatives.• Variety of lenders-some lenders may pre-approve

you.• Avoid being upside-down in your car.• Look for rebates or low-interest financing.• Consider the APR, total finance charge. Check out

www.bankrate.com 8-9

Phase 4: Postpurchase Activities

Lemon Laws. Maintenance and ownership costs Use the item correctly to have improved

performance and fewer repairs. Investigate, evaluate and negotiate a

variety of servicing options. Operation costs; fixed and variable

expenses. Automobile servicing sources; dealers,

service stations, garages, Wal-Mart, etc.8-10

Comparison Shopping

•Warranties

• Implied

• Express

•Service contracts

•Leasing vs. buying

•Balloon financing

• Successful negotiations require information

• Make the decision

• Evaluate the decision

Negotiate and Decide On Best Deal

Financial Aspects of Leasing

Capitalized cost - the price of the vehicle. Average buyer pays 92% of list, average person who leases pays 96% of list.

Money factor - interest rate.

Monthly payment amount and number of payments.

Residual value - expected value of the vehicle at the end of the lease. You may decide to return, keep, or sell the vehicle. If the residual value is less than market value, return it.

8-20

Decision Making Grid

Price 30% 9 2.7 7 2.1 5 1.5

Durability 25% 6 1.5 8 2.0 10 2.5

Features 20% 6 1.2 8 1.6 10 2.0

Warranty 15% 6 0.9 10 1.5 8 1.2

Styling 10% 10 1.0 6 0.6 8 0.8

TOTAL 100% 7.3 7.8 8.0

Criteria

Decision

Weight (W)

Appliance A

Score (S)* W x S

Appliance B

Score (S) W x S

Appliance C

Score (S) W x S

*Using a 10-point scale.

Buying services • www.comsumerreports.org

Internet sites

• www.buyingadvice.com• www.carmax.com• www.carsbelowinvoice.com• www.edmunds.com• www.autosite.com• http://auto.consumerguide.com

Help When Buyinga New Vehicle

8 - 14

Get Things Fixed

• Get estimate in advance

• Ask how long repairs will take

• Get claim check

• Ask to be given all replaced parts

• Be available when at-home repairs are made

• Get written receipt

Choose Between LowInterest and Rebate

• Compare actual costs

• Consider opportunity cost of rebate

• Add opportunity cost of foregone rebate to finance charge of dealer financing

Buy a Used Vehicle

• Decide on features and options

• Decide how much to spend

• Select makes/models in price range

• Start search

• Check selection carefully

• Negotiate and decide

Get the Most for YourCar-Buying Dollar

• Buy used vehicles

• Buy used vehicles from private owners

• Visit dealerships at least three times

• Negotiate price first

• Consider leasing

• Use up your vehicles

Rental Car Basics

• Type

• Price and gas payment

• Additional fees

• Reservations

• Mileage restrictions

• Insurance and inspection