53

Planned Giving on a Shoestring Budget L. Paul Hood, Jr., J.D., LL.M. The University of Toledo Foundation

| Date post: | 24-Dec-2015 |

| Category: |

Documents |

| Upload: | amberly-neal |

| View: | 214 times |

| Download: | 0 times |

Planned Givingon a Shoestring Budget

L. Paul Hood, Jr., J.D., LL.M.The University of Toledo Foundation

Quote of the Day

People who cannot recognize a palpable absurdity are very much in the way of civilization. Agnes Rupellier

Conversation Starters•Q: “Paul, what do you

do for a living?”•A: “I help people make

a difference.”

Conversation Starters

• Q: “What do you mean by ‘make a difference?’”

• A: “I help people create their personal legacy.”

Conversation Starters• Q: “How do you do that?”• A: “By helping people leave legacies to UT

in their estate plans and by working with their lawyers and financial advisors on the most taxwise way to structure their legacies.”

Tips and Tidbits• Note what isn’t there in my description of what I do. My

title. Or an in-depth description of what I do until after they ask. People’s eyes glaze over when you do that too early.

• I purposely give short (fewer than ten words) answers that invite further questions and peek interest. And I never say that I am in planned giving. I purposely use the word legacy. It is donor-centric and in the form of an “elevator speech.”

Elevator Speeches• What’s an “elevator speech?”

• An elevator speech is in the form of a persuasive pre-rehearsed brief sound byte that you use to spark interest in what your organization does or to create interest in a project, idea, or product – or in yourself. It often starts in the form of a question.

Elevator Speeches• A good elevator speech should last no longer

than a short elevator ride of 20 to 30 seconds, hence the name.

• If your elevator speech can’t be said in the form of a sound byte for the press (no longer than one minute-and usually half of that), then it is too long.

Elevator Speeches

You should have eight to ten good elevator speeches for planned giving ready at all times for whenever they are needed.

Elevator SpeechesSome examples of “elevator speeches” for planned giving:

• “Did you know that it can be more advantageous to gift stock rather than cash?” (Gifts of appreciated stock to a public charity)

• “Did you know that there’s a way to make a meaningful gift that can be changed in the future and won’t ever cost you a cent?” (Bequests)

• Did you know that there’s a way to get income for life in an amount that may exceed your current return and make a gift? (Charitable remainder trusts and charitable gift annuities).

More Tips and Tidbits

I usually identify myself as a “recovering tax lawyer” for purposes of both levity and credibility.

More Tips and Tidbits• I help people understand that you don’t

need a lot of wealth to make a difference and leave a personal legacy.

• Every gift makes a difference in the life of someone at the organization.

• All you need is affinity and desire to do good.

Tips and Tidbits

You make much more headway with a donor when you focus in on what attracts them to the organization, what excites them and what they are passionate about-their legacy.

Tips and Tidbits

People often are motivated to do their estate planning by a desire to leave a legacy, thereby achieving a form of immortality, which is what all people want, according to the research.

What is Planned or Legacy Giving?

•Before we can talk about planned or legacy giving, let’s step back and define it.•What is planned or legacy giving?

What is Planned or Legacy Giving?

• Planned gifts are those gifts that are deferred until some point in the future like bequests or charitable remainder trusts, where the charitable organization’s interest is to be enjoyed in the future.• They also can involve a split-interest gift where the entire amount

of the gift is not made to the charitable organization but part of the gift is either retained or given to other individuals, such as charitable gift annuities or charitable remainder trusts), but they also include gifts of life insurance policies, gifts of interests in retirement plans/IRAs and donations of real estate with a retained life estate.

Tips and Tidbits• Don’t talk to people about planned

giving vehicles without talking about what interests them-you might lose them, and you might get confused.

• Find out their needs, and then you can discuss ways to satisfy their needs and desires.

Tips and Tidbits• If the donor can’t make a major gift now,

gently probe to ascertain what might be holding them back.

• Usually, it is because they believe that they can’t afford it now, especially if they have the interest. These people are legacy gift candidates.

Hidden Treasure

The research and my over 25 years of experience as an estate planning lawyer and estate planning consultant tells us that for every bequest about which we are told in advance, somewhere between two and three times that number will come in totally unexpected as bequests mature at the donor’s death.

Hidden Treasure

Nevertheless, if properly cultivated, more donors will make their plans known prior to death, and fewer donors will change their dispositive plans as current research indicates that more people are changing their estate plans within the last five years of their life, particularly charitable legacies.

More Tips and Tidbits• A planned or legacy gift usually is a capstone gift for a

donor.• It usually is the largest gift that the donor will or can

make, but it often is not the last gift that a donor will make.• It requires much more cultivation and a longer

consideration period than other gifts. You cannot push a planned giving prospect, or you will lose them. We operate at the donor’s speed.

More Tips and Tidbits•Who makes planned or legacy gifts?• This may surprise you, but it usually is a donor

who flies under the radar screen of fundraisers because they don’t give much during lifetime, but they have exhibited continuous loyalty to the mission of the organization by contributing almost every year. The amount given annually is irrelevant.

More Tips and Tidbits

Moral: pay attention to your most loyal donors, as these are your best planned giving prospects. We purposely target loyal donors with our marketing efforts.

More Tips and Tidbits

•Why waste time on planned giving? Isn’t it better to get a current gift now than waiting for something that may never happen?• Planned giving accounts for a sizable percentage of

donations. The research is clear that donors who make a planned gift actually increase their current giving. Why? Because they are invested long-term in your organization!

Impact of ATRA on Charitable Giving

What does the 2013 tax law mean for planned giving?

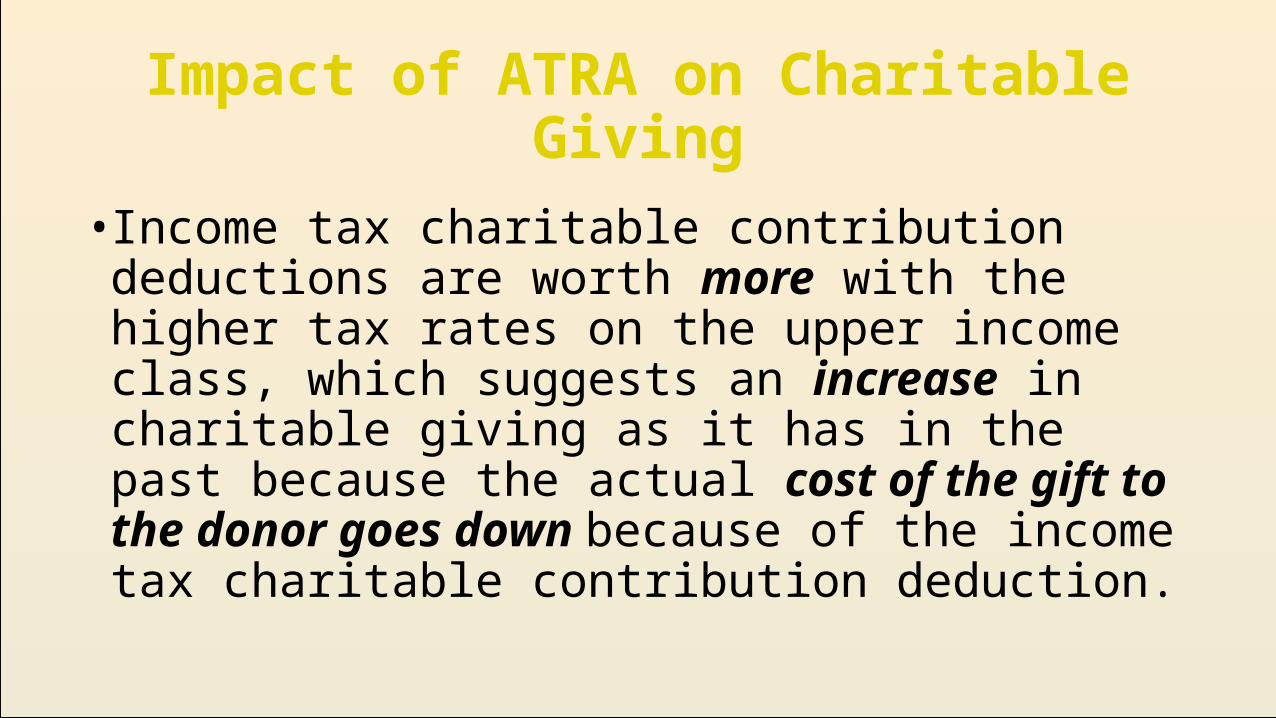

Impact of ATRA on Charitable Giving

• Income tax charitable contribution deductions are worth more with the higher tax rates on the upper income class, which suggests an increase in charitable giving as it has in the past because the actual cost of the gift to the donor goes down because of the income tax charitable contribution deduction.

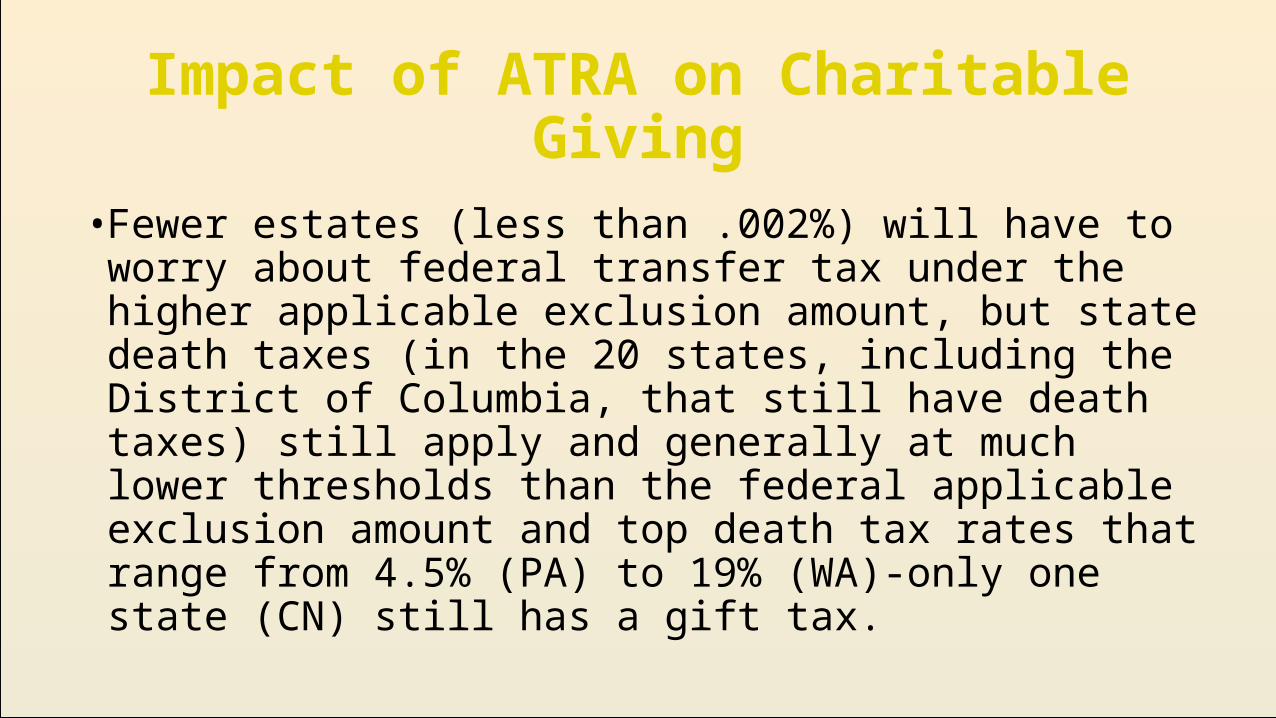

Impact of ATRA on Charitable Giving

• Fewer estates (less than .002%) will have to worry about federal transfer tax under the higher applicable exclusion amount, but state death taxes (in the 20 states, including the District of Columbia, that still have death taxes) still apply and generally at much lower thresholds than the federal applicable exclusion amount and top death tax rates that range from 4.5% (PA) to 19% (WA)-only one state (CN) still has a gift tax.

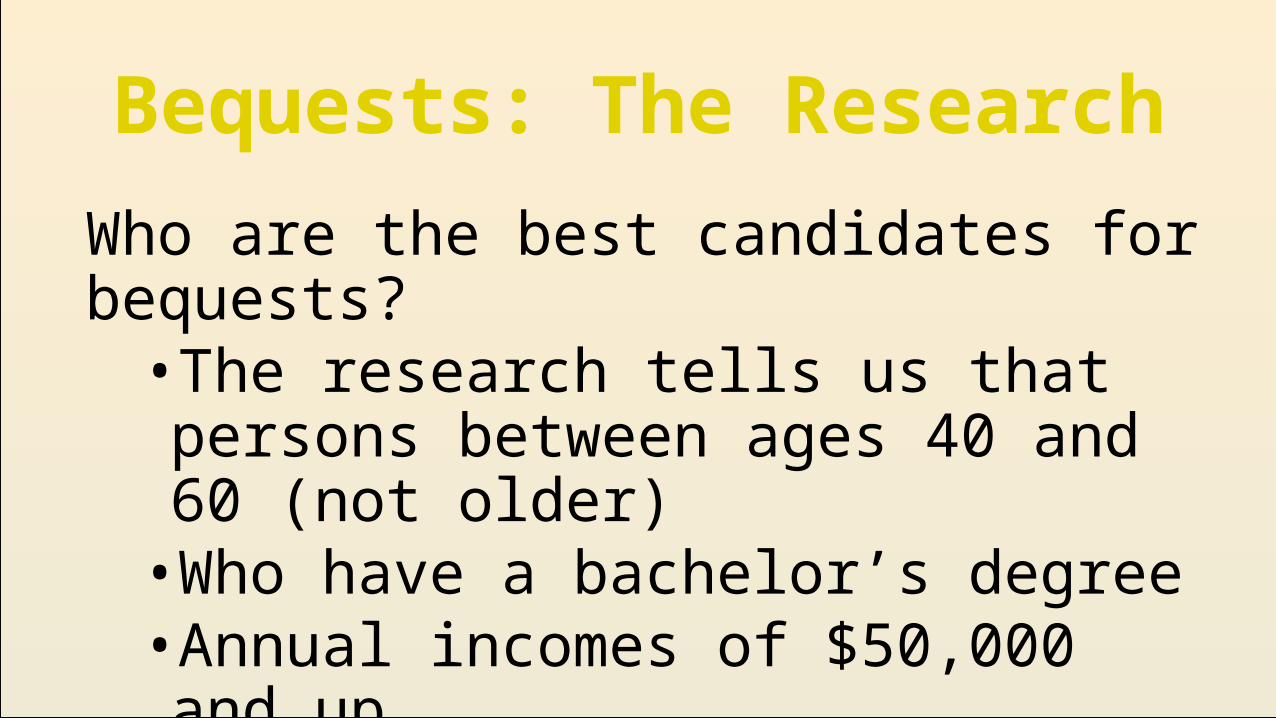

Bequests: The Research

Who are the best candidates for bequests?•The research tells us that persons

between ages 40 and 60 (not older)•Who have a bachelor’s degree•Annual incomes of $50,000 and up•Who are motivated by a desire to “do

good.”

Bequests: The ResearchWhat are some of the best indicators for bequests?• Single and childless.• Between ages 40 and 60 (in my experience,

persons over ages 75 and over rarely made significant changes in their estate plans, but this may be changing according to recent research).• Regularly attends religious services.

Bequests-Challenges

Far and away, the most common planned gift is a testamentary bequest from a will or trust-challenges: • It requires waiting for the donor to die.• Usage of wills and trusts is declining in favor of non-

probate transfers.• Heirs can feel jilted and either contest or drag their heels

on administration, or even try to divert the assets some other way, even illegally.

Bequests-Challenges

Far and away, the most common planned gift is a testamentary bequest from a will or trust-challenges (cont.): • These must be tracked and properly and regularly

stewarded once the donor’s intentions are made known because the donor can change his or her mind and particularly after the donor’s death to make sure that the organization receives the bequest because some heirs resent having to share the estate with a charitable organization and sometimes resist turning the bequest over.

Bequests-Challenges

• For every bequest that the organization knows about, there are two to three that come in an unexpected gifts as many donors are unwilling to share the information, so unless you have copies of the will or trust, you really can’t count the bequest as part of a campaign without documentation because all you may get out of a donor is an oral statement such as “you’re in my will” without specifying amount, etc.

Bequests

• This is where smaller organizations should start planned giving efforts because it is such an easy ask (doesn’t impact their current lifestyle, can be changed in the future, etc.) and can apply to all age groups; a suggestion of a bequest or a planned gift to the organization must be on every buckslip (receipt) for a gift and probably on the organization’s promotional materials and correspondence (letterhead and e-mail signature blocks)-it must be inculcated into the organizational culture.

Life Insurance

Probably the second most common planned gift is the gift of a life insurance policy (some policies that the organization receives death benefits from are never owned by the organization-it is only the beneficiary)-challenges: • The overwhelming number of life insurance policy gifts require an ongoing

premium payment obligation, which donors usually continue to bear, at least for awhile, but you can’t count on that-sometimes hard decisions concerning the policies must be made.

• For donors who actually donate the entire policy during lifetime to a charitable organization, they are entitled to an income tax charitable contribution deduction essentially equal to the fair market value of the donated policy.

Life Insurance

• Life insurance policies require consistent and active investment management-you can’t just receive a policy and forget about it-there are tough decisions such as whether the policy should be retained or whether it should be cashed in or sold in a life settlement, with concomitant donor relations and stewardship issues, so it requires someone’s attention at the organization.

• Like the bequest, you usually have to wait until the insured dies-note: the overwhelming number of life insurance policies aren’t designed to last until the insured actually dies, and most lapse prior to the insured’s demise, which underscores the need for active policy management, which should be, at a minimum, ordering a free in-force illustration on the policy from the insurance company annually to see how it is performing.

Retirement Plans/IRAs

The next most common planned gift is a gift of a beneficiary interest in a qualified plan or IRA: (the beauty of these planned gifts is that there is little management that is involved)-challenges:• Another beauty of these gifts is that a charitable organization is a favored beneficiary

under the tax law because a charitable organization is tax-exempt, while the participant or the participant’s family must pay income tax on distributions from the plan/IRA, which significantly reduces the net benefit to the family.

• These gifts are most commonly received at the donor’s death, which means the organization has to wait, because, with one limited exception that hasn’t yet been renewed for 2014, the lifetime rollover by persons who are age 70.5 and older directly to the organization from an IRA (not a qualified plan), which was permitted for transfers up to $100,000 annually, a participant usually has to take the money out of the plan/IRA, first pay income tax on the distribution and then make a donation.

Retirement Plans/IRAs

• Most of these gifts come from persons who are forced to start receiving benefits from the plan or IRA-essentially those who are age 70.5 and older-the problem there is the risk that the donor will survive for so long that the plan/IRA is significantly depleted due to forced distributions during the donor’s lifetime because of the method that the IRS forces plan/IRA benefits out and into the taxable income of the participant/beneficiary.• Most of these gifts come in unexpectedly, so they can’t be

budgeted or planned for or stewarded very well unless you know about them in advance.

Charitable Gift Annuities• This is strongly not recommended for small

organizations because a charitable gift annuity is a contractual promise that is backed by all of the assets of the organization that is given in exchange for a donation, to make lifetime payments to up to two people, who are called “annuitants”; this is really for larger organizations that have the assets to cover the liability for the payments.

• Annuity payments can started immediately or be deferred into the future.

© L. Paul Hood, Jr. 2014

Charitable Gift Annuities• Annuities are “bets to live.” In other words, the

annuitant does better the longer that the annuitant survives and continues to receive annual annuity payments, which means the organization fares worse. You can have “under water” charitable gift annuities.

• Contrast this with life insurance, which is a “bet to die”-the sooner the insured dies, the lower the total amount of premiums that will be paid and the better off the life insurance policy beneficiaries are.

© L. Paul Hood, Jr. 2014

Charitable Gift Annuities

• Annuitants usually enjoy a mix of tax-exempt return of basis (essentially the donation, amortized over the estimated remaining life expectancy of the annuitant(s)) and ordinary income, which is taxed at ordinary income tax rates.

• Unlike charitable remainder trusts, one can establish a charitable gift annuity with less money; for example, our minimum is $10,000, with $25,000 being the minimum amount most donated, and many are much larger than that.

© L. Paul Hood, Jr. 2014

Charitable Gift Annuities

• We generally require that the annuitant be age 65 before the annuity payments commence, but, for example, a 49 year old can establish a deferred charitable gift annuity where the annuity payments commence at age 65, i.e., retirement age.

• Donors receive an income tax charitable contribution deduction equal to the present value of the organization’s future interest, which is purely a function of the age(s) of the annuitant(s) when the annuity is purchased.

© L. Paul Hood, Jr. 2014

Charitable Remainder Trusts

After gifts of charitable gift annuities, charitable remainder trusts (more to follow on charitable remainder trusts in upcoming slides) are the next most common planned gift-challenges:• There is a risk that the payout to the private beneficiary is set so high

(has to be a minimum of 5% and must result in at least a 10% remainder of the trust donation surviving the entire trust term in order to be qualified, computed at the beginning of the trust) in relation to trust investment experience that there is little or nothing left at the end of the charitable remainder trust term.

• Many of these are unknown and, therefore, can’t be stewarded.• In periods of low IRS applicable federal rates, it is very difficult for a

person who is younger than age 70 to establish a lifetime charitable remainder annuity trust.

Charitable Remainder TrustsCharitable remainder trusts-challenges (cont.):

• Most donors retain the power to change charitable beneficiaries, so when you know about the existence of a charitable remainder trust, it is essential to properly continue to steward the donor.

• Usually requires a minimum of $100,000 to make the effort and expense worthwhile, with $250,000 being usually the beginning amount of a charitable remainder trust.

• Can be funded with cash or property.• Someone must serve as trustee; I don’t recommend the organization serve in

that capacity because it’s not its core business; donors often serve as the initial trustee.

© L. Paul Hood, Jr. 2014

Charitable Remainder Trusts

• Special type of tax-exempt irrevocable trust for tax purposes – unlike a charitable gift annuity, which is a simple two page agreement, this type of gift requires significant expertise from a lawyer to draft one because of IRS governing instrument requirements.

• Donors can either retain or give their loved ones a payout of a minimum of 5% of the value of the trust property each year, either for life or for up to 20 years, with at least one charitable organization as the irrevocable remainder beneficiary.

© L. Paul Hood, Jr. 2014

Charitable Remainder Trusts

• The income tax charitable contribution deduction is a function of the estimated present value of the charitable organization’s future interest, which in turn is a function of the term of the trust, which can be for a set number of years that can’t exceed 20 years or for the lifetimes of the private beneficiaries (which is then a function of the remaining life expectancies of the private beneficiaries).

• There are two basic varieties of Charitable Remainder Trusts: the Charitable Remainder Unitrust and the Charitable Remainder Annuity Trust.

© L. Paul Hood, Jr. 2014

Charitable Remainder Trusts

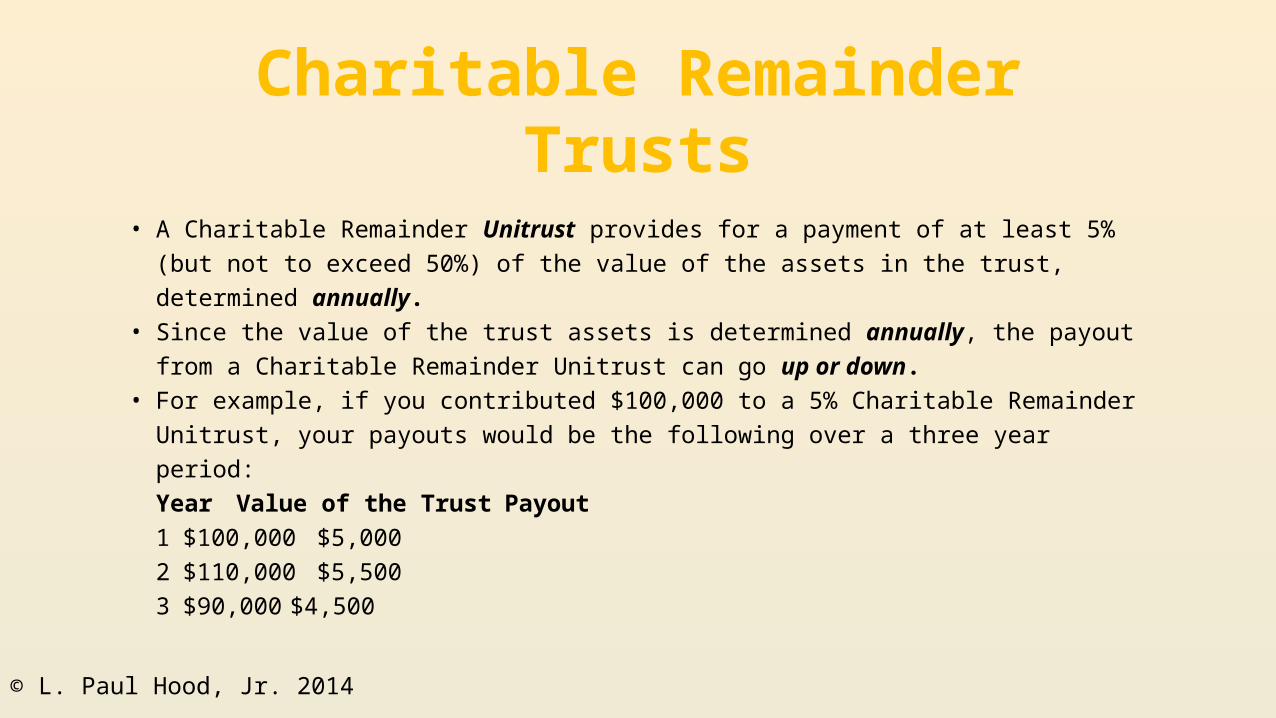

• A Charitable Remainder Unitrust provides for a payment of at least 5% (but not to exceed 50%) of the value of the assets in the trust, determined annually.

• Since the value of the trust assets is determined annually, the payout from a Charitable Remainder Unitrust can go up or down.

• For example, if you contributed $100,000 to a 5% Charitable Remainder Unitrust, your payouts would be the following over a three year period:

Year Value of the Trust Payout1 $100,000 $5,0002 $110,000 $5,5003 $90,000 $4,500

© L. Paul Hood, Jr. 2014

Charitable Remainder Trusts

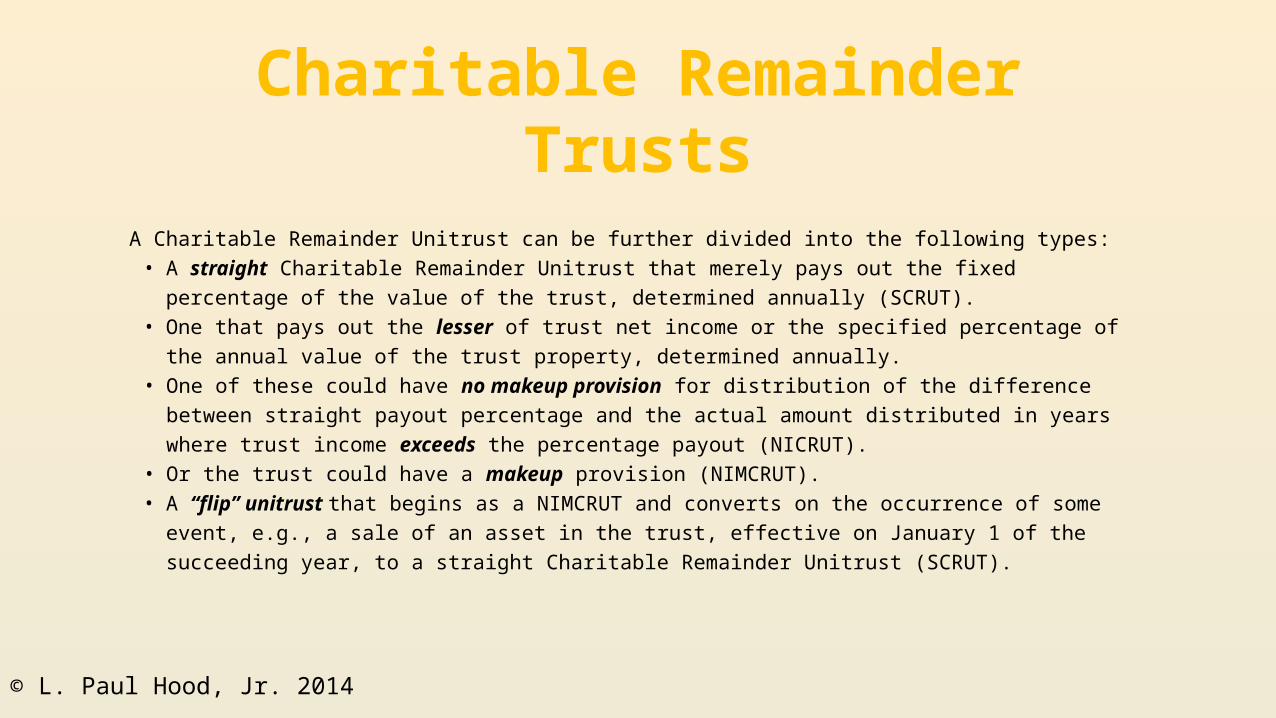

A Charitable Remainder Unitrust can be further divided into the following types:• A straight Charitable Remainder Unitrust that merely pays out the fixed percentage of the

value of the trust, determined annually (SCRUT).• One that pays out the lesser of trust net income or the specified percentage of the annual

value of the trust property, determined annually.• One of these could have no makeup provision for distribution of the difference between

straight payout percentage and the actual amount distributed in years where trust income exceeds the percentage payout (NICRUT).

• Or the trust could have a makeup provision (NIMCRUT).• A “flip” unitrust that begins as a NIMCRUT and converts on the occurrence of some event,

e.g., a sale of an asset in the trust, effective on January 1 of the succeeding year, to a straight Charitable Remainder Unitrust (SCRUT).

© L. Paul Hood, Jr. 2014

Charitable Remainder Trusts

• A Charitable Remainder Annuity Trust provides for a payout of at least 5% (but not to exceed 50%) of the initial value of the trust assets.

• Therefore, unlike the Charitable Remainder Unitrust, payouts from a Charitable Remainder Annuity Trust are fixed and don't change unless and until the trust runs out of assets.

• Unlike a charitable remainder unitrust, a charitable remainder annuity trust can run out of assets if the initial donation plus the investment experience is insufficient to withstand the annual payouts to the private beneficiaries during the trust term.

© L. Paul Hood, Jr. 2014

Charitable Remainder Trusts

Charitable remainder trusts are becoming far more popular after ATRA. Reasons include:• Income tax charitable contribution deduction is worth more.• 3.8% Medicare tax can be avoided or deferred.• Tax on an outright sale of a business has increased, versus

doing a split CRT/sale.• It is possible in a split CRT/sale to increase net family wealth.

© L. Paul Hood, Jr. 2014

Charitable Remainder Trusts

Benefits of charitable remainder trusts:• Can diversify an investment

concentration.• Gift to charity.• Income tax charitable contribution

deduction is worth more.© L. Paul Hood, Jr. 2014

Charitable Remainder Trusts

Benefits of charitable remainder trusts (cont.):• Defer capital gains tax and recognize

that gain ratably over the trust term.• Tax-advantaged growth.• Possible payout during years of lower

taxable income.© L. Paul Hood, Jr. 2014

Shoestring Budget Ideas

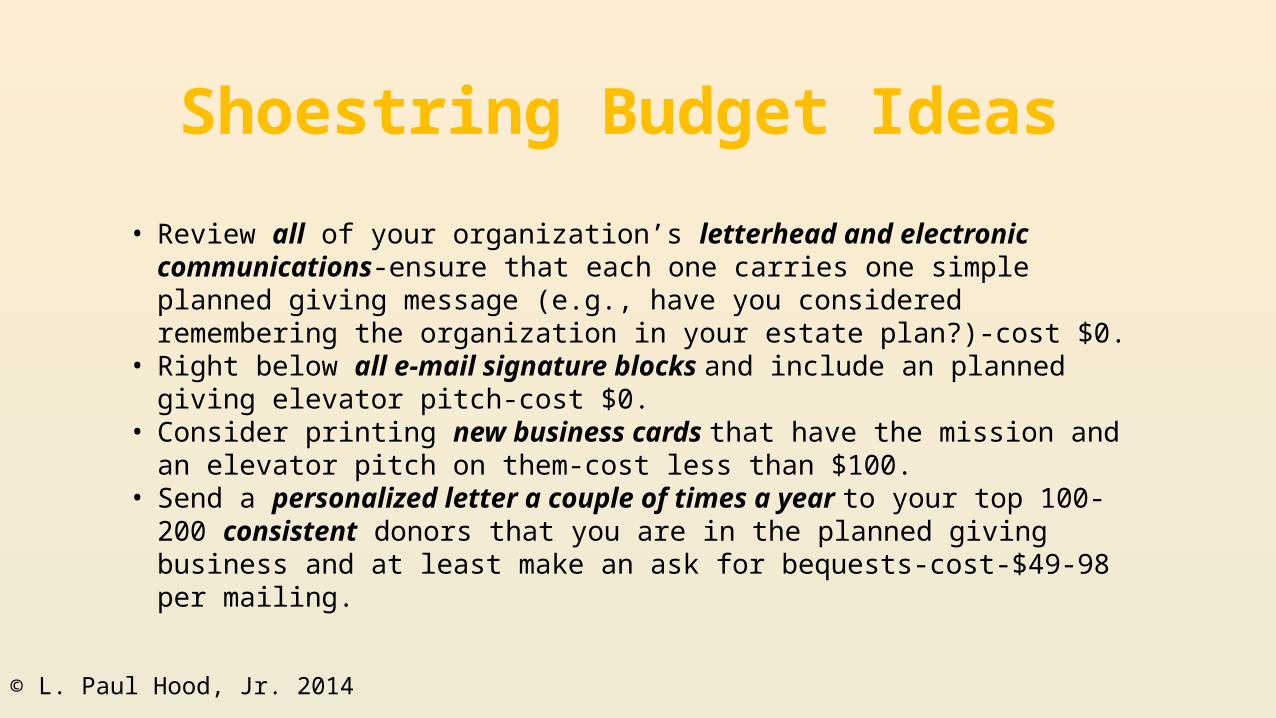

• Review all of your organization’s letterhead and electronic communications-ensure that each one carries one simple planned giving message (e.g., have you considered remembering the organization in your estate plan?)-cost $0.

• Right below all e-mail signature blocks and include an planned giving elevator pitch-cost $0.

• Consider printing new business cards that have the mission and an elevator pitch on them-cost less than $100.

• Send a personalized letter a couple of times a year to your top 100-200 consistent donors that you are in the planned giving business and at least make an ask for bequests-cost-$49-98 per mailing.

© L. Paul Hood, Jr. 2014

Comments? Questions?

Questions? Comments or thoughts? Please share them with me now, via the telephone (419.530.5303) or e-mail (

[email protected] or paul@[email protected]).

If you would like to receive my weekly Foundation tax and estate planning update, simply send an e-mail to me at

Thanks for your invitation and attendance!

© L. Paul Hood, Jr. 2014

![ENERGY STORAGE: CAN WE GET IT RIGHT?FINAL].pdf · * David Schmitt, J.D., LL.M, is a Federal/Regional Attorney at the Iowa Utilities Board. Dr. Glenn M. Sanford, J.D., Ph.D., is a](https://static.documents.pub/doc/80x56/5f8f089e92474d00a6651593/energy-storage-can-we-get-it-right-finalpdf-david-schmitt-jd-llm-is.jpg)