30

Improving Africa’s Information and Communications Infrastructure African Development Forum - ADF ‘99 UNCC Addis Ababa 24-28 Oct 1999 Mike Jensen [email protected]

| Date post: | 26-Dec-2015 |

| Category: |

Documents |

| Upload: | dennis-erik-webster |

| View: | 218 times |

| Download: | 4 times |

Policies and Strategies forImproving Africa’s Information and

Communications Infrastructure

African Development Forum - ADF ‘99

UNCC Addis Ababa24-28 Oct 1999

Mike [email protected]

What is Information and Communication Infrastructure?

• Telecommunications• Internet• Computers and Software• Broadcasting - TV & Radio• Human resources to install, operate, develop

and set policy

Infrastructure is the key barrier to Info Society development, requires longer planning time horizons and very substantial capital resources- just doubling the phone lines would cost about US$20billion

Radio is the most widespread medium on the continent, but

diversity of broadcasting is limited• A growing number of countries have liberalised

the sector and allowed private sector radio & TV stations

• A few countries such as Mali, South Africa and Uganda, have issued notable numbers of community radio and non-profit licenses

• But outside of the capital cities, coverage is still usually limited to one or two state operated channels.

Telecommunication Infrastructure is even more limited

• In ‘98 there were about 17 million lines for about 750 million people - 1 in 50

• But in the Sub Sahara outside South Africa there were only 3.5 M lines - 1 in 200 - less than the number installed in China in ‘97 alone

• Access to public phones is similarly restricted - about 1 for every 15 000 people compared to a world average of 1 in 600

Fixed Lines / 100 people

6

More than 2/100Less than 0.5/100

NoYes

DuopolyFullMonopoly

State owned monopolies are seen as the major cause of high prices,

poor service and slow growth

Competition in the local loop

Independent Regulator

Fixed Line Telecom Growthis over 10% in 97-98

15%

Mobile Lines / 100 people

.25

17 countries have more than .25

65% growth in 97-98

Mobile is now 20% of fixed network

The Internet is now widespread in Africa

• Three years ago, only 12 countries had full Internet access.

• At the end of 1999 the Internet will be locally available in the capitals of every country in Africa

• Low cost communications and access to global information sources has fuelled rapid adoption

But the Internet is expensive and not widely available outside the

capital cities• At an average of US$50/month, ISP

subscription fees are more than an average monthly salary.

• Only 17 countries have Internet servers in some of the secondary towns

• With this limited coverage, for the majority of people, even if they could afford a computer, it is a long distance call use the Internet.

Less costly Internet Access is available in some countries

• Prices are lower ($10-20/month) in the more mature markets where many ISPs compete and are unencumbered by high license fees or excessive tariffs for bandwidth

• In some countries (14), there is a special policy to provide local call access across the whole country. The Telecom operator sets up an 'area-code' for Internet access that is charged at local call tariffs, so ISPs can immediately roll out a network with national coverage

Number of users still very low• There are now over 500 000 dialup

subscribers in Africa (about 175 000 outside of South Africa).

• Each computer with an Internet or email connection has an average of three users.

• This puts current estimates of African Internet users at somewhere around 1.5 million.

• Most of these are in South Africa (about 1 000 000), leaving only about 500 000 for 700 million people

• This is about one Internet user for every 1400 people, compared to a world average of about one user for every 35 people, and a North American and a European average of about one in every 3-4 people.

• About half the African countries have 1000 or more dialup subscribers, but only about 9 countries with 5000 or more

Internet Subscribers / 100 people

0.15

Average: 1 in 1400

Local call charges are still a big barrier

• Even in the African countries with the lowest local call charges, these are the still the largest part of the cost of Internet.

• Not a problem specific to Africa - even some European countries are considering adopting flat rate local calls in an effort to match North American Internet access.

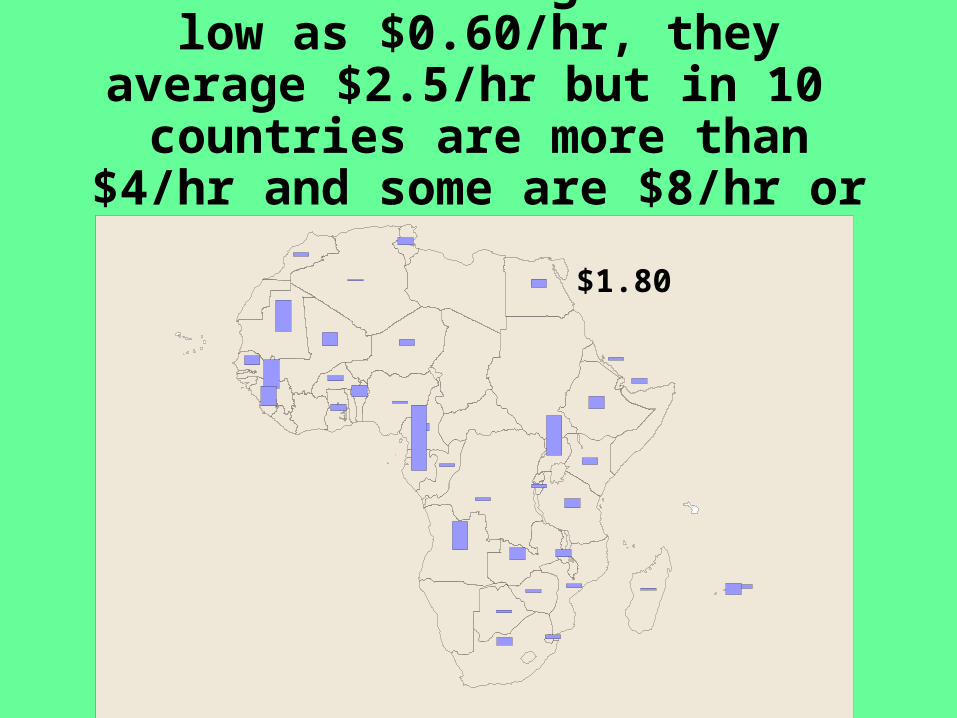

Local call charges are as low as $0.60/hr, they average $2.5/hr but

in 10 countries are more than $4/hr and some are $8/hr or more

$1.80

Few regional links in Africa• Almost all upstream Internet circuits

connect to the USA, with a few to the UK, Italy and France.

• But ISPs in countries with borders shared with South Africa benefit from low tariff policies of the SA telecom operator for international links to neighbouring countries.

• As a result South Africa is a hub for some of its neighbours- Lesotho, Namibia, and Swaziland.

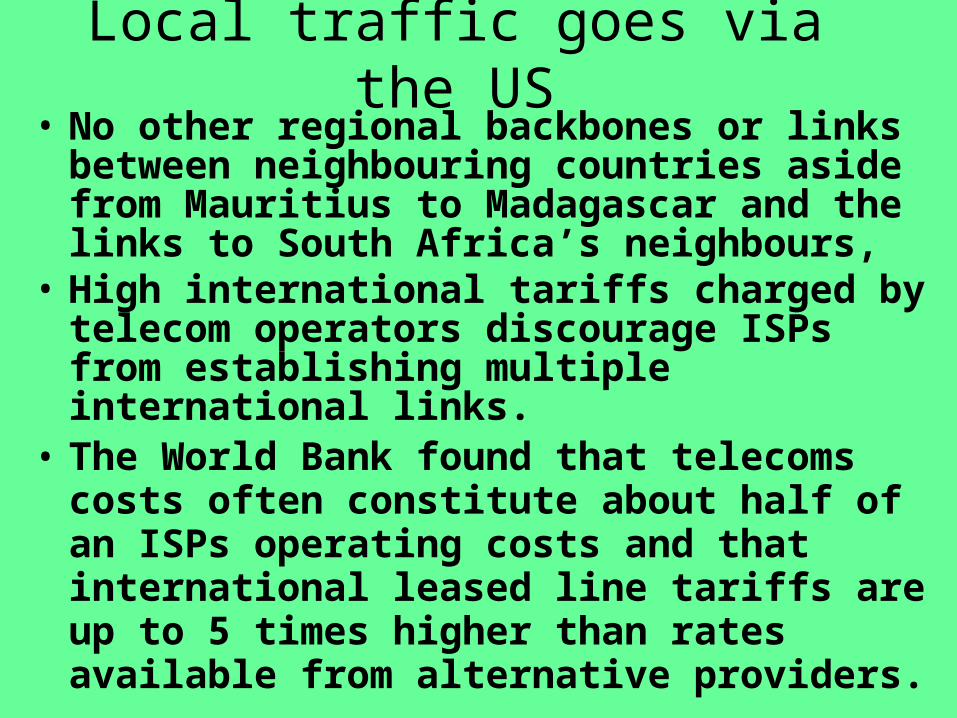

Local traffic goes via the US• No other regional backbones or links

between neighbouring countries aside from Mauritius to Madagascar and the links to South Africa’s neighbours,

• High international tariffs charged by telecom operators discourage ISPs from establishing multiple international links.

• The World Bank found that telecoms costs often constitute about half of an ISPs operating costs and that international leased line tariffs are up to 5 times higher than rates available from alternative providers.

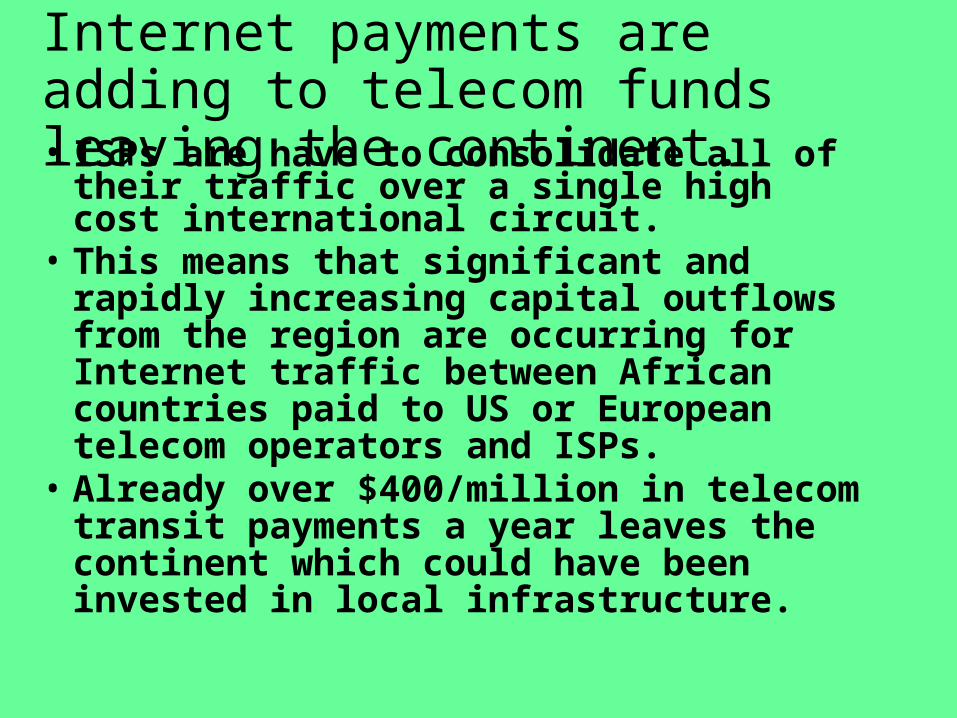

• ISPs are have to consolidate all of their traffic over a single high cost international circuit.

• This means that significant and rapidly increasing capital outflows from the region are occurring for Internet traffic between African countries paid to US or European telecom operators and ISPs.

• Already over $400/million in telecom transit payments a year leaves the continent which could have been invested in local infrastructure.

Internet payments are adding to telecom funds leaving the continent.

Connectivity Comparisons/capita

Infrastructure Developments• Low cost network computers, smart

cards and Internet appliances• GMPCS - Iridium, ICO, Globalstar• Cellular Phones• Wireless - Local loop / data services• Geo Satellites and VSAT - RASCOM,

PanamSat, ESAT, NewSkies, Lockheed• LEO Satellites - HealthNet, VITASat• Data Broadcasting - WorldSpace & DSTV• Hybrid Systems • Using power supply infrastructure - VRA• Internet Models for Telephony

Encourage, accelerate and replicate:• Careful liberalisation and expanded universal

service objectives • Better Support for Regulators and Public

Participation in Policy Development• Integrated National Information &

Communications Infrastructure (NICI) planning• Telecentres & Multipurpose Community

Access, and Community Radio Stations• Universal Smart Cards & E-Commerce policies• Government Content and Applications

Development• Regional Infrastructure Projects

Strategies for Infrastructure Improvement [1]

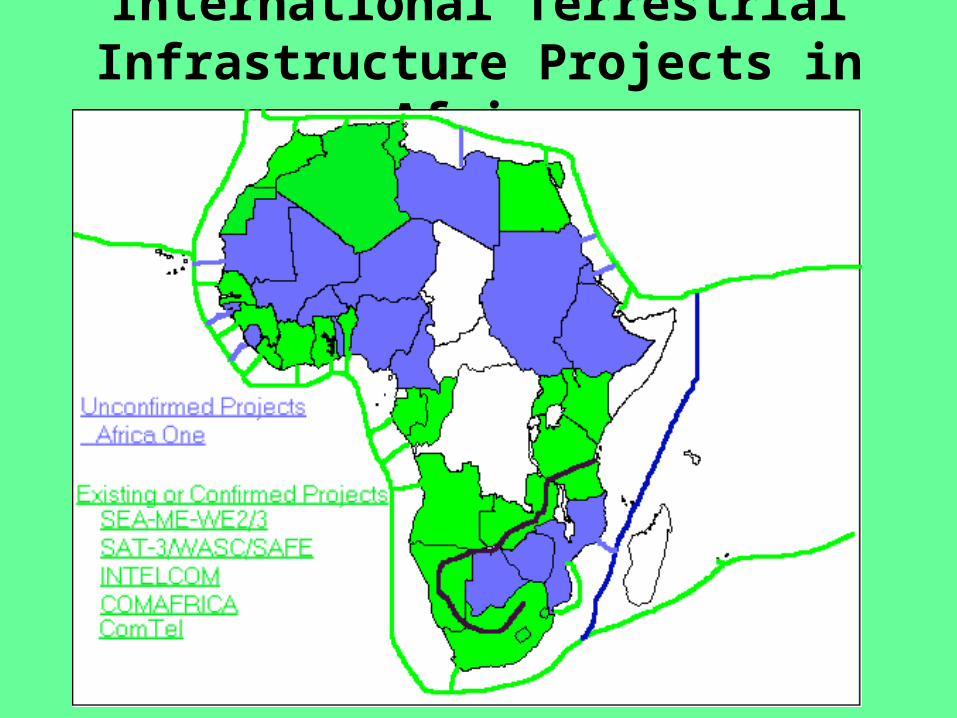

International Terrestrial Infrastructure Projects in Africa

Strategies for Infrastructure Improvement [2]

• African Connection• SADC IT Theme document and model

telecoms policy legislation• Telecom Regulators Association of

Southern Africa (TRASA)• Conference of West African Telecom

Operators (CTOA) • East African Internet Providers

Association (EAIA)• Bulk Purchasing - ?

Broader regional collaboration for information sharing and common policy development:

Strategies for Infrastructure Improvement [3]

Capacity Building & Human Resource Development:

• Training of National Regulators• Centres for Excellence in Telecommunications

Administration - ESMT and AFRALTI• National Internet Training Centres - CITI• Standards for User Training in Computer

Applications - Computer Drivers License - CSSA• Improved ICT Training programmes at schools,

universities, research networks, workplace and informal environment

National Collaboration• Association of Telecom Service

Providers of Kenya

• Information Workers Association of Namibia

• Internet Service Providers Association of South Africa

• National Internet Society chapters - Egypt, Morocco, Ghana, South Africa

• Smart partnerships between govt and private sector - esp in access provision

Raising Finance for Infrastructure• Regional collaboration to increase economies of

scale and make investment more attractive - ComTel

• Privatisation - 25 countries committed to privatising PTOs

• Public Offerings - AfricaOnline raised US$25million on London Stock Exchange

• Revenue sharing - Build Operate Transfer

• Joint Ventures - many cellular networks

• Sale of bonds to users or potential users

Key Barriers To Be Eliminated• High license fees for telecom operators

and ISPs• Slow process for licensing• Lack of radio frequency spectrum

planning• Excessive import duties on ICT equipment• Restricted access to broadcasting

licenses• High call charges• Limited skills and knowledge of options• Political instability, strife corruption and a

poor business environment

Other Important Considerations• Development of phased approach which priorises

certain activities esp, connectivity of key decision makers in business and govt

• Need for strategy on use of wireless & the Internet model for development of telecom infrastructure, esp rural telecom profitability

• Ensure linkage with needs to redirect more resources to transport and power supply networks, including cross-border links

• Ensure free movement of people across national borders

• Improve representation at global level