30

© 2018 LMC Automotive Limited, All Rights Reserved. Outlook A Policy Driven ASEAN Automotive Outlook Titikorn L., ASEAN Manager

| Date post: | 08-Nov-2018 |

| Category: |

Documents |

| Upload: | hoangthien |

| View: | 213 times |

| Download: | 0 times |

© 2018 LMC Automotive Limited, All Rights Reserved.

Outlook

A Policy Driven ASEAN Automotive Outlook

Titikorn L., ASEAN Manager

© 2018 LMC Automotive Limited, All Rights Reserved.

Global presence with regional expertise

São Paulo

Offices

Affiliates

Detroit Oxford

Bangkok

Shanghai

Tokyo

© 2018 LMC Automotive Limited, All Rights Reserved.

Our Partnerships

Oxford Economics is one of the world’s

leaders in the field of macro-economic

forecasting and provides many of the

underlying global macroeconomic forecasts

which underpin the LMC Automotive’s

vehicle forecasts.

J.D. Power is a global market

information firm, whose independent and

unbiased benchmark studies provide

LMC with insights of the carmakers,

products and consumers

JATO Dynamics provides LMC with the

world’s most timely, accurate and up-to-

date information on vehicle specifications

and pricing, sales and registrations,

news and incentives

OXFORD

ECONOMICS

Marklines, the world’s leading on-line

strategic automotive portal and B2B

Gateway, provides strategic market strategy

data, proprietary and custom B2B e-

marketing solutions, customized market

research, and actionable business

intelligence with LMC.

CENO Consulting develops automotive

market retail intelligence for the Chinese

market. Our alliance provides a

comprehensive database of China’s

regional automobile market.

ACT Research, the recognized leader in the

provision of data and forecasts for the

commercial vehicle industry in North America,

co-publish with LMC the Global Commercial

Vehicle Forecast.

© 2018 LMC Automotive Limited, All Rights Reserved.

ASEAN5: High Compound Annual Growth Rate

Low Vehicle Density and Large Population

Global Light Vehicle (LV) Sales 2017 & 2025

North America

Asia-Pacific

Europe

South America

World

China

ASEAN5

2017 2025 CAGR

95 mn 114 mn 2.3%

2017 2025 CAGR

29 mn 36 mn 2.7%

2017 2025 CAGR

45 mn 55 mn 2.7%

2017 2025 CAGR

3 mn 4 mn 4.2%

2017 2025 CAGR

21 mn 24 mn 2.1%

2017 2025 CAGR

4 mn 6 mn 4.3%

2017 2025 CAGR

21 mn 21 mn 0.2%

Others

2017 2025

4 mn 8 mn

India

2017 2025 CAGR

4 mn 7 mn 7.8%

© 2018 LMC Automotive Limited, All Rights Reserved.

2.92 2.99 3.13 3.27 3.44

3.61 3.76 3.93 4.08 4.22 4.35

0.0

1.0

2.0

3.0

4.0

5.0

6.0

'15 '16 '17 '18 '19 '20 '21 '22 '23 '24 '25

Mill

ions

ASEAN Sales: Increasing Trend in LV Demand

© 2018 LMC Automotive Limited, All Rights Reserved.

3.79 3.88 3.93 4.16 4.29

4.51 4.70 4.81

4.98 5.10 5.15

0.0

1.0

2.0

3.0

4.0

5.0

6.0

'15 '16 '17 '18 '19 '20 '21 '22 '23 '24 '25

Mill

ions

ASEAN Production Surplus Sales

© 2018 LMC Automotive Limited, All Rights Reserved.

Countries with Output of More Than 1 million units

0

5

10

15

20

25

30M

illio

ns 2016 2017

© 2018 LMC Automotive Limited, All Rights Reserved.

Thai Annual Sales Exceed 1 million units in 2012 -2013

0.60 0.54

0.78 0.77

1.40

1.29

0.85 0.77 0.74

0.85 0.94 0.95

0.99 1.03 1.06 1.09 1.11 1.14

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

'08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22 '23 '24 '25

Mill

ion

s

2.70 mn 2.70 mn -> 1st car scheme

© 2018 LMC Automotive Limited, All Rights Reserved.

Thai Sales Back On Track

0.60 0.54

0.78 0.77 0.85

0.77 0.74

0.85 0.94 0.95

0.99 1.03 1.06 1.09 1.11 1.14

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

'08 '09 '10 '11 '14 '15 '16 '17 '18 '19 '20 '21 '22 '23 '24 '25

Mill

ion

s

Sales 2016: - 4% YoY

- Sales in Q1-Q3 2016: +0.6% YoY

- Sales in Q4 2016: -14% YoY

(PV -27% / LCV +5% YoY)

On a YoY basic, April 18 sales is the 16th consecutive month of growth.

© 2018 LMC Automotive Limited, All Rights Reserved.

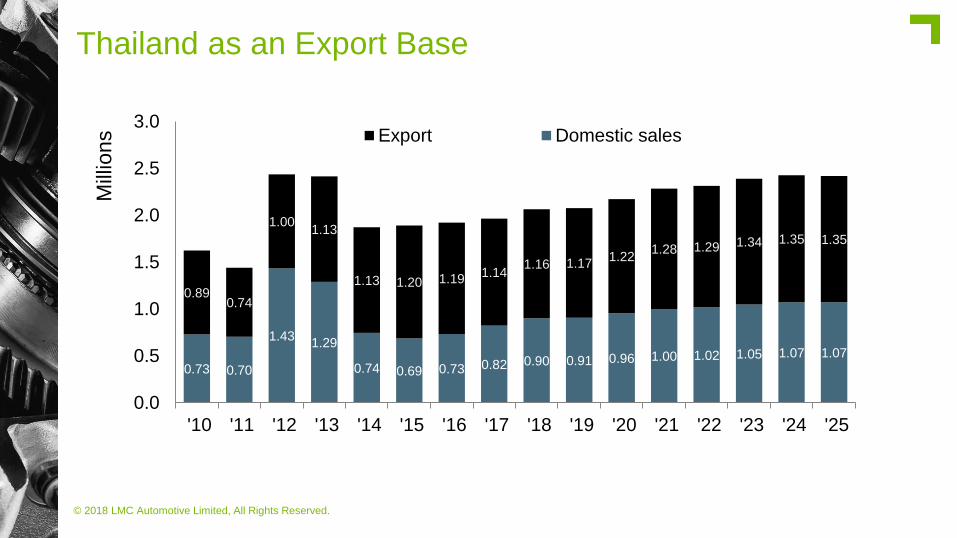

Thailand as an Export Base

0.73 0.70

1.43 1.29

0.74 0.69 0.73 0.82 0.90 0.91 0.96 1.00 1.02 1.05 1.07 1.07

0.89 0.74

1.00 1.13

1.13 1.20 1.19 1.14

1.16 1.17 1.22

1.28 1.29 1.34 1.35 1.35

0.0

0.5

1.0

1.5

2.0

2.5

3.0

'10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22 '23 '24 '25

Mill

ions

Export Domestic sales

© 2018 LMC Automotive Limited, All Rights Reserved.

Eco Cars – Thailand’s second pillar

Toyota - Yaris / Yaris Ativ Honda - Brio and Brio Amaze

Mazda - Mazda2

Mitsubishi Mirage and Attrage Suzuki - Swift, Celerio and Ciaz

Nissan - March, Almera and Note

Minimum production requirement; 100k units per year

© 2018 LMC Automotive Limited, All Rights Reserved.

Thailand Export Structure Change

0.58 0.41

0.60 0.58 0.60

0.19

0.19

0.12

0.29

0.61 0.54

0.18

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

2008 2009 2010 2016 2017 Jan - Apr2018

Millio

ns

Passenger Vehicle Pickup

© 2018 LMC Automotive Limited, All Rights Reserved.

Thailand – maintaining the S Curve

1970s

2010s

xEV;

HEV, PHEV & BEV

© 2018 LMC Automotive Limited, All Rights Reserved.

Indonesia Sales: Largest Market in ASEAN

0.55

0.44

0.68

0.79

1.00

1.11 1.11

0.95 1.01 1.00

1.04 1.10

1.17 1.22

1.28 1.34

1.40 1.45

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

'08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22 '23 '24 '25

Mill

ion

s

The commodities

super cycle

2010 - 2013

16% 17% 23% 23% 22%

2014 2015 2016 2017 Jan - Apr2018

LCGC share of domestic sales

Low Cost

Green Car

New Segment

© 2018 LMC Automotive Limited, All Rights Reserved.

Tight Auto Loans Pressure PV but LCV Saw Growth

0

5,000

10,000

15,000

20,000

25,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2014 2015 2016 2017 2018

November 2015: LCV sales begin to decline

April 2017: LCV sales begin to rise year-over-year

© 2018 LMC Automotive Limited, All Rights Reserved.

Indonesia: Limited Export Due to Unfavorable Tax Structure

0.57 0.64 0.79

0.94 1.02

0.83 0.93 0.92 0.97 1.02 1.09 1.13 1.18 1.24 1.30 1.35

0.08 0.11

0.18

0.17 0.20

0.21 0.19 0.23

0.26 0.30

0.30 0.30

0.30 0.30

0.30 0.31

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

'10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22 '23 '24 '25

Mill

ions

Export Domestic sales

© 2018 LMC Automotive Limited, All Rights Reserved.

Indonesia Automotive Industry Roadmap

2010

2015

2020

2025

MPV, LCV and

Environment Friendly Vehicle

MPV, LCV, Environment Friendly Vehicle

MHCV, SUV and Small Car

80% Local Content for MPV and LCV

MPV, LCV, Environment Friendly Vehicle

MHCV, SUV and Small Car,

Hybrid Vehicle and Sedan

80% Local Content for MPV, LCV, Small Car and SUV

MPV, LCV, MHCV, SUV,

Environment Friendly Vehicle,

Small Car, Sedan, Hybrid Vehicle

and Luxury car

80% Local Content for MPV, LCV,

Small Sedan, SUV and Medium Sedan

2013: LCGC

Low Cost

Green Car

2018-2019: LCEV

Low Carbon

Emission Vehicle

© 2018 LMC Automotive Limited, All Rights Reserved.

Malaysia: Mature Market

0.54 0.53

0.60 0.60 0.61 0.65 0.66 0.66

0.58 0.57 0.57 0.60 0.61 0.63 0.64 0.65 0.66 0.68

0.00

0.20

0.40

0.60

0.80

1.00

'08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22 '23 '24 '25

Mill

ion

s

© 2018 LMC Automotive Limited, All Rights Reserved. 9

Malaysia: National Brands and Non-National Brands

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

'13 '14 '15 '16 '17 '18 '19 '20 '21 '22 '23 '24 '25

Perodua Proton Honda Toyota Nissan Other

© 2018 LMC Automotive Limited, All Rights Reserved.

Malaysian Production Lower Than Domestic Sales

0.54 0.53

0.60 0.60 0.61 0.65 0.66 0.66

0.58 0.57 0.57 0.60 0.61 0.63 0.64 0.65 0.66 0.68

0.52 0.48

0.56 0.53

0.57 0.59 0.59 0.61

0.54 0.50

0.54 0.56 0.57 0.59 0.60 0.62 0.63 0.63

0.00

0.20

0.40

0.60

0.80

1.00

'08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22 '23 '24 '25

Mill

ion

s

Domestic Sales Production

© 2018 LMC Automotive Limited, All Rights Reserved.

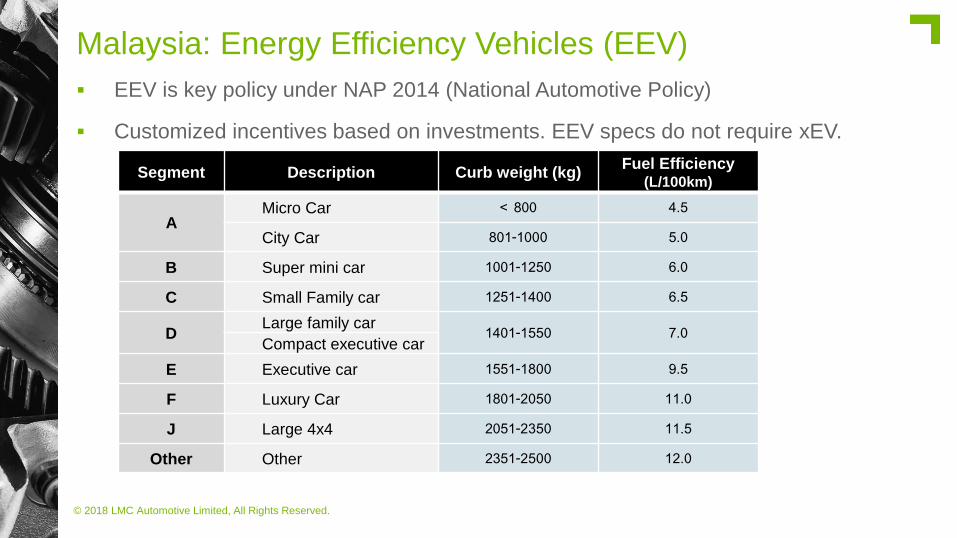

Malaysia: Energy Efficiency Vehicles (EEV)

EEV is key policy under NAP 2014 (National Automotive Policy)

Customized incentives based on investments. EEV specs do not require xEV.

Segment Description Curb weight (kg) Fuel Efficiency

(L/100km)

A Micro Car < 800 4.5

City Car 801-1000 5.0

B Super mini car 1001-1250 6.0

C Small Family car 1251-1400 6.5

D Large family car 1401-1550 7.0 Compact executive car

E Executive car 1551-1800 9.5

F Luxury Car 1801-2050 11.0

J Large 4x4 2051-2350 11.5

Other Other 2351-2500 12.0

© 2018 LMC Automotive Limited, All Rights Reserved.

Malaysia: NAP 2018 Could Be Delayed

NAP 2018 - Connectivity, Mobility, Next-Generation Vehicles, Big Data and Lifestyle.

*Source: https://paultan.org

© 2018 LMC Automotive Limited, All Rights Reserved.

Philippines: Pull-forward Purchases in 2017

0.12 0.13 0.17 0.16 0.18

0.21

0.27

0.32

0.40

0.46 0.41

0.44 0.46

0.49 0.53

0.55 0.58

0.60

0.00

0.20

0.40

0.60

0.80

'08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22 '23 '24 '25

Mill

ion

s

LV Demand boosted by

- Strong remittance inflow

- Booming Service Export; BPO

Sales in Jan – Apr 2017: -9% YoY

BUT Pickup sales rose by +23% YoY

© 2018 LMC Automotive Limited, All Rights Reserved.

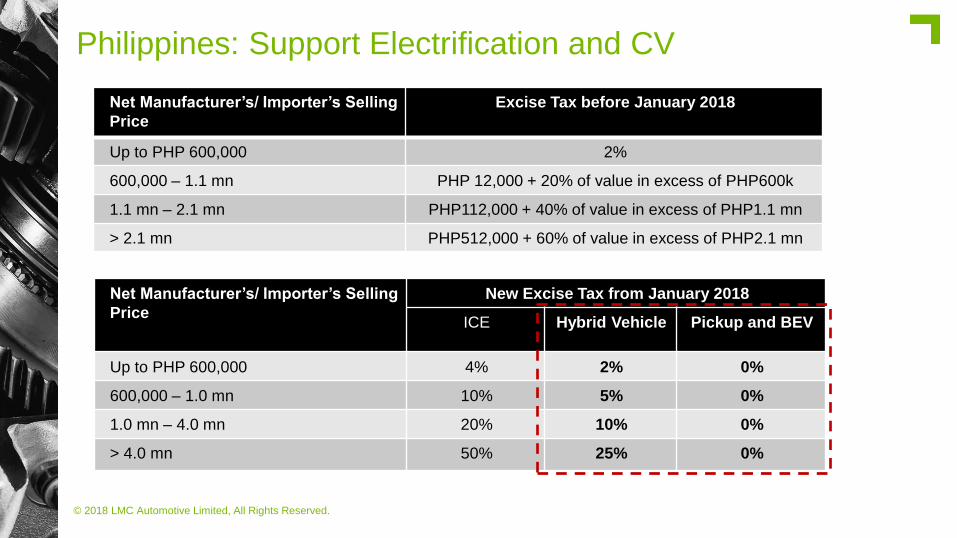

Philippines: Support Electrification and CV

Net Manufacturer’s/ Importer’s Selling

Price

Excise Tax before January 2018

Up to PHP 600,000 2%

600,000 – 1.1 mn PHP 12,000 + 20% of value in excess of PHP600k

1.1 mn – 2.1 mn PHP112,000 + 40% of value in excess of PHP1.1 mn

> 2.1 mn PHP512,000 + 60% of value in excess of PHP2.1 mn

Net Manufacturer’s/ Importer’s Selling

Price

New Excise Tax from January 2018

ICE Hybrid Vehicle Pickup and BEV

Up to PHP 600,000 4% 2% 0%

600,000 – 1.0 mn 10% 5% 0%

1.0 mn – 4.0 mn 20% 10% 0%

> 4.0 mn 50% 25% 0%

© 2018 LMC Automotive Limited, All Rights Reserved.

Philippines: No More Production of Euro 3 & Older Models

2017 production boosted by CARS program.

0.07 0.07

0.08

0.07 0.07 0.07

0.09

0.10 0.10

0.14

0.09

0.09

0.12 0.12 0.13 0.13 0.13 0.12

0.00

0.05

0.10

0.15

'08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22 '23 '24 '25

Mill

ion

s

Production in 2017: +44% YoY

- Mitsubishi started to produce Mirage and Attrage under CARS

- HARI started to produce Hyundai Eon under “MVDP”

© 2018 LMC Automotive Limited, All Rights Reserved.

Vietnam: Anticipation of Zero Tariff Led to 2017 Sales Drop

0.12

0.15 0.13 0.12

0.09 0.11

0.14

0.21

0.26 0.25

0.31

0.35

0.38 0.40

0.42 0.44

0.46 0.49

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

'08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22 '23 '24 '25

Mill

ion

s

Sales in 2017: - 5% YoY

- Consumer expected the lower prices in 2018

a) Lower SCT tax for small engines

b) Zero import tariff under ASEAN trade agreement

© 2018 LMC Automotive Limited, All Rights Reserved.

Vietnam Production: Decree 116 (Non-Tariff Barrier)

0.09 0.08 0.08 0.08

0.06 0.08

0.10

0.15

0.20 0.18

0.23 0.24

0.27 0.27

0.29 0.30

0.31 0.31

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

'08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '22 '23 '24 '25

Mill

ion

s

Production in 2017: - 10% YoY

a) Production stops replaced by imports from ASEAN

b) Lower Demand

© 2018 LMC Automotive Limited, All Rights Reserved.

Vietnam Government Supports Local Industry

Time Detail

January 2016 Government changed import tariffs calculation from “CIF” to “Wholes sales prices”

April 2016 THACO announced to capacity expansion to 100,000 units per year for Mazda

September 2017 Vingroup announced production of made-in-Vietnam Car or “VinFast”

Plant Capacity:

- 300,000 units for Motorbike (start production in 2018)

- 250,000 units for Sedan and SUV (start production in Q3 2019)

October 2017 Government planned to cut import tariffs for auto components to support local car makers.

Government announced Decree 116:

- Require VTA issued by a foreign authorized agency or government

- Every batch of CBU Imports must be tested and inspected.

January 2018 - Automakers stopped exporting cars to Vietnam

March 2018 - Automakers resumed exporting cars to Vietnam and increased CBU model prices.

© 2018 LMC Automotive Limited, All Rights Reserved.

Collaboration Among ASEAN: Toyota’s IMV Project

Source: Hideo KOBAYASHI (2015), Current State and Issues of the Automobile

and Auto Parts Industries in ASEAN, ERIA Discussion Paper Series.

+44 1865 791737

+1 248 817-2100

+66 264 2050

+86 21 5283 3526

Oxford

Detroit

Bangkok

Shanghai

For experts by experts

Thank you © 2018 LMC Automotive Limited, All Rights Reserved.

lmc-auto.com