40

Policy Update Michelle G. Bulls Chief Grants Management Officer Grants Policy

| Date post: | 29-Dec-2015 |

| Category: |

Documents |

| Upload: | peregrine-griffith |

| View: | 216 times |

| Download: | 2 times |

Policy Update

Michelle G. BullsChief Grants Management Officer

Grants Policy

Policy Update

What’s New?IHS Grants Policy Source DocumentsPolicy TopicsPrior ApprovalReporting RequirementsCloseout

What’s New?

Grants Policy Statement

U.S. Department of Health and Human ServicesOffice of the Assistant Secretary for Resources and Technology

Office of Grants

October 1, 2006

What’s New?HHS Grants Policy Statement

Effective: October 1, 2006

Applicability: HHS Operating Divisions and Staff Divisions that issue Discretionary Grant Awards w/the exception of NIH.

Makes available to HHS grantees, in a single document, up-to-date policy guidance.

IHS Grants Policy Source Documents

Grants Policy DirectivesAwarding Agency Grants

Administration Manual (AAGAM)Policy Announcements – “coming

soon”45 CFR 74 and 92HHS Grants Policy StatementIndian Health Service Circular

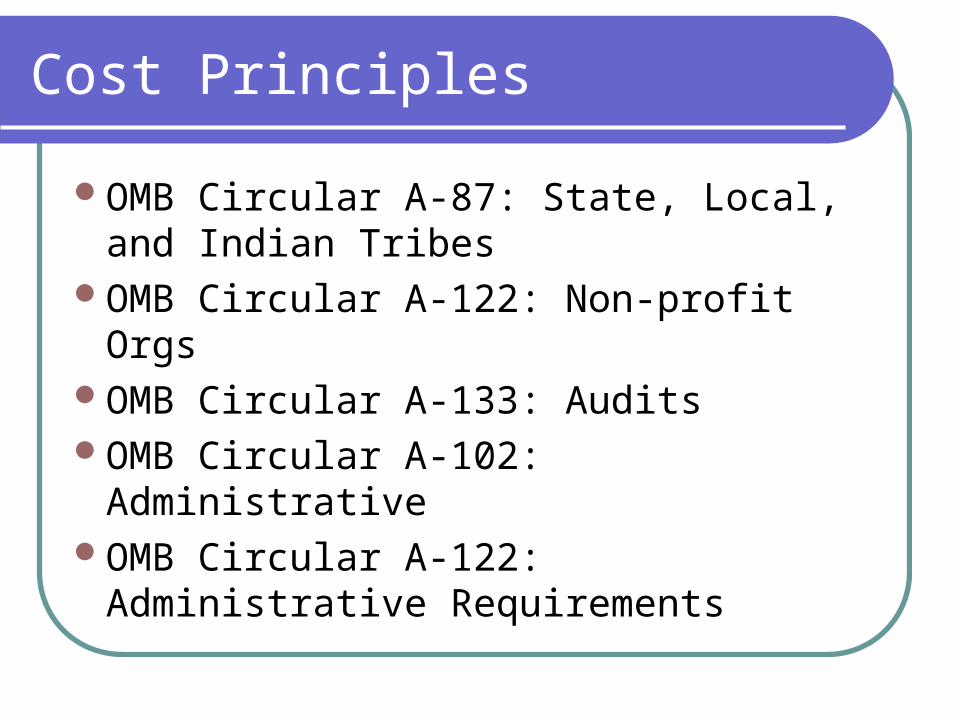

Cost Principles

OMB Circular A-87: State, Local, and Indian Tribes

OMB Circular A-122: Non-profit OrgsOMB Circular A-133: AuditsOMB Circular A-102: AdministrativeOMB Circular A-122: Administrative

Requirements

Cost Principles What are the Cost Principles?

Establish principles to determine cost applicability to grants, contract & other agreements

Designed to ensure that the Federal Government provide its fair share of total costs

In accordance with generally accepted accounting principles

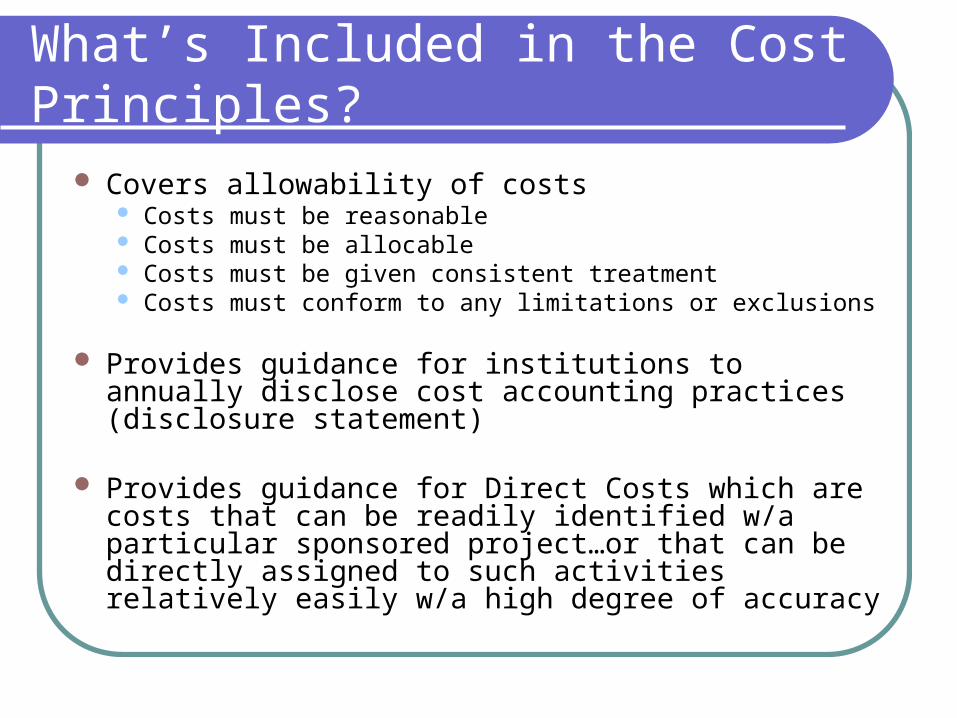

What’s Included in the Cost Principles?

Covers allowability of costs Costs must be reasonable Costs must be allocable Costs must be given consistent treatment Costs must conform to any limitations or exclusions

Provides guidance for institutions to annually disclose cost accounting practices (disclosure statement)

Provides guidance for Direct Costs which are costs that can be readily identified w/a particular sponsored project…or that can be directly assigned to such activities relatively easily w/a high degree of accuracy

What’s Included in the Cost Principles?

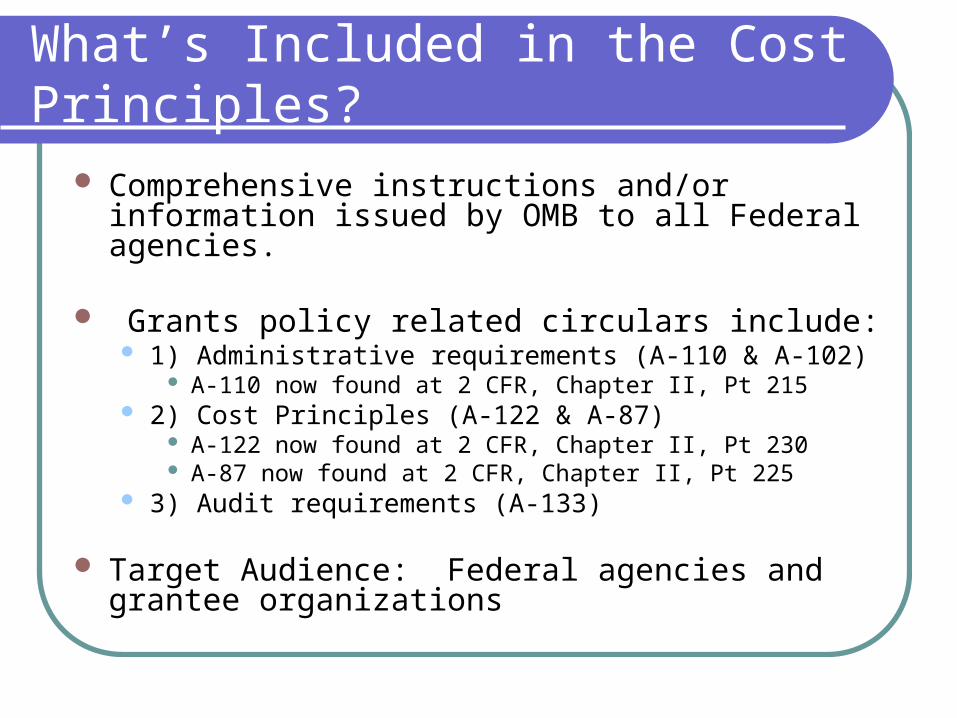

Comprehensive instructions and/or information issued by OMB to all Federal agencies.

Grants policy related circulars include: 1) Administrative requirements (A-110 & A-102)

A-110 now found at 2 CFR, Chapter II, Pt 215 2) Cost Principles (A-122 & A-87)

A-122 now found at 2 CFR, Chapter II, Pt 230 A-87 now found at 2 CFR, Chapter II, Pt 225

3) Audit requirements (A-133)

Target Audience: Federal agencies and grantee organizations

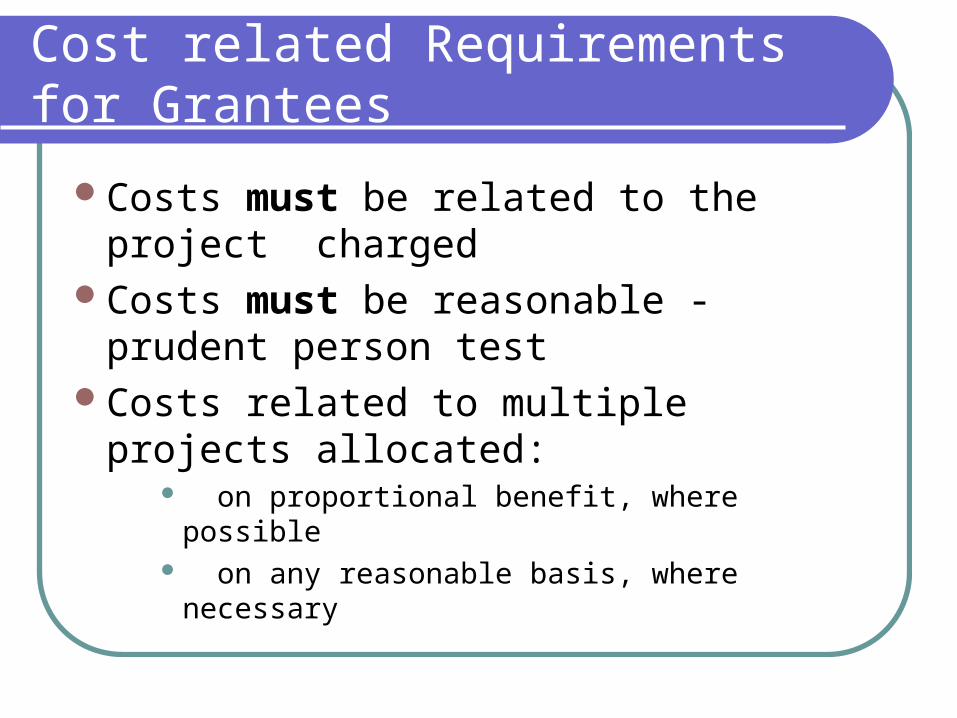

Cost related Requirements for Grantees

Costs must be related to the project charged

Costs must be reasonable - prudent person test

Costs related to multiple projects allocated:

on proportional benefit, where possible on any reasonable basis, where

necessary

Grants Management 101Definitions of Frequently Used Terms Used

Unobligated Balance

Unliquidated Obligations

Prior Approval

Change in Scope

Significant Rebudgeting

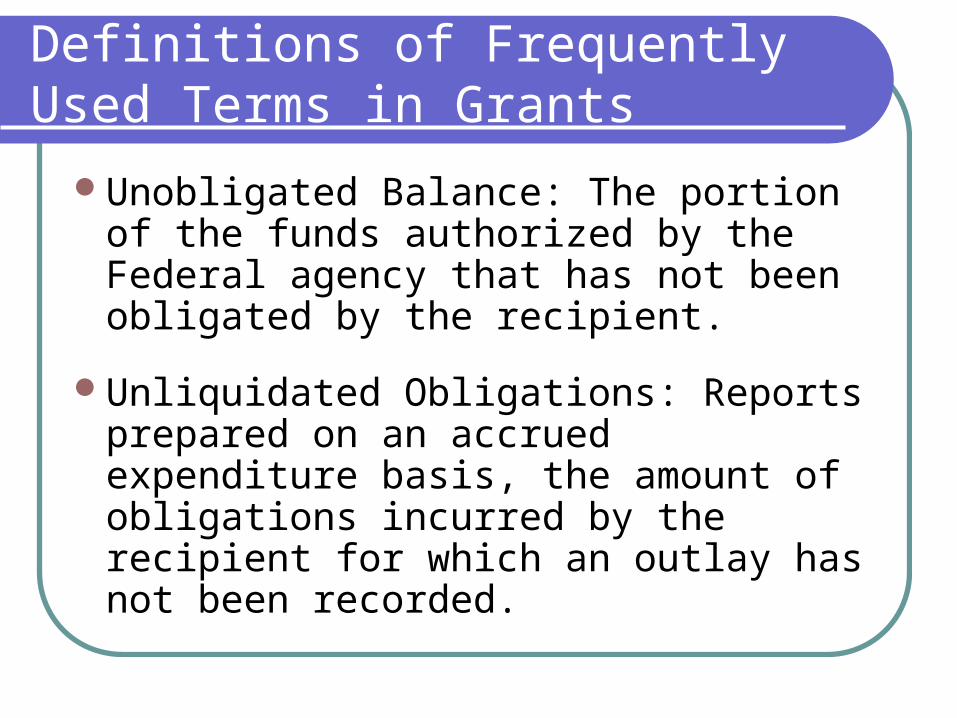

Definitions of Frequently Used Terms in Grants

Unobligated Balance: The portion of the funds authorized by the Federal agency that has not been obligated by the recipient.

Unliquidated Obligations: Reports prepared on an accrued expenditure basis, the amount of obligations incurred by the recipient for which an outlay has not been recorded.

Definitions of Frequently Used Terms in Grants (Continued)

Prior Approval: Written permission provided by the authorized granting official from the IHS grants and program office before the recipient may undertake certain activities (such as performance or modification of an activity), significant rebudgeting, or exceed a certain dollar level.

Change in Scope: A process, usually initiated by the grantee, whereby the objectives or specific aims identified in the approved grant application are significantly changed.

Goals of Project Monitoring

Assess progress toward meeting the goals and objectives of the project

Determine level and use of Federal resources

Why is it Important to Monitor Progress?

Assess progress in the fieldIdentify potential problemsCreate annual reportsAbility to give an account for the

Federal dollarsJustify budget requestsDetermine future needs in the

program areas

Progress Reporting Requirements

Generally, progress reports are due annually unless otherwise indicated in the NoA.

Format of the progress report is generally included in the NoA.

Financial Reporting Requirements

Reports of expenditures are required as documentation of the grants financial status according to the records of the recipient.

Generally, due annually unless otherwise indicated in the NoA.

Expanded Authorities

Waives certain cost related and other prior approval requirements for the grantee.

Available to all grantees unless otherwise indicated in the NoA.

Expanded Authorities

Pre Award Costs up to (and including) 90 days

One-time no cost extension up to 12 months

All cost-related prior approvals unless the action is considered a change in scope.

Prior Approval Requirements

Alterations and renovationsCapital expendituresAddition of a foreign componentPreaward Costs >90 days prior to

effective date of new or competing awardDeviation from award terms and

conditionsChanges in grantee organizational status

Prior Approval Requirements Transferring of funds between

construction and nonconstruction work Second no-cost extension or extension >

12 months Need for additional NIH funds—aka

supplement Carryover of unobligated balances Change in scope Change in key personnel Change in grantee Institution

Carryover Policy

Special Term of Award for NARCH:

All carryover actions require prior approval from the GMO and Program Official. The request must include be made in writing signed by the authorized organizational official and must include a budget and budget justification for carryover amounts.

Carryover of Large Unobligated Balances

Both Grants Management and ProgramStaff must approve the request.

Both officials will ask the following questionsas they review the request:

Will it benefit the proposed research (goals of the project)?

Does it signify a program expansion? Will the approval generate the need for recurring

costs in future years? Is the project on target considering the amount of

carryover that is available?

Carryover of Unobligated Balances Continued

DGO and Program Staff will check FSR to make sure that the total cost of the request is available.

Grantee should be notified, in writing, from the GMO of the decision within 30 days after receiving the request.

Second No Cost Extension

No additional funds required

Scope of project will not change

Time required to ensure adequate completion of originally approved project

Grantee agrees to update all required assurances

Change of Status of PI and Other Key Personnel

Withdrawal of PI or Key Personnel named in NGA

Absence for period of 3 continuous months

Reduction of effort by 25 or more percent of level approved at award

Approval of Substitute PI/Key Personnel Requires…

Justification for the change

Biographical sketch of proposed individual

Other support for that individual

Budget changes resulting from the proposed change

Change in Scope

Change in specific aims

Change from approved use of human subjects

Shift in emphasis to a different disease area

More Indicators of Change in Scope?

Significant Rebudgeting—i.e., when expenditures in a single direct cost budget category deviate by more than 25% of the current budget year total costs awarded

Transfer of the performance of substantive programmatic work to a third party

Incurrence of patient care costs if not previously approved

Purchase of a unit of equipment >$25,000

Indian Health Service Incentives Policy

Incentive items are allowable costs and may be purchased with IHS grant funds. Incentives may be used to support participants in such activities that include, but are not limited to, health fairs, and fitness programs.

The items purchased by grantees must have a reasonable value, not to exceed $30 each, per activity

Indian Health Service Incentives Policy (Continued)

The incentive funds should be reflected under the “other expenses” category of the budget.

Generally, items that are not considered incentives include, but are not limited to, gifts, cash and/or cash prizes, door prizes, or any type of entertainment (e.g., movie passes).

Policy Link: http://www.ihs.gov/PublicInfo/Publications/IHSManual/Circulars/Circ05/Circ05_06/circ05_06.htm

Reimbursement of Indirect Costs

Necessary part of our grants

Cannot be readily identified with the project

Current rate must be established with the cognizant Federal agency in order to receive indirect costs in the award.

Enforcement Actions

In the event of a grantee’s failure to comply with the terms and conditions of award, IHS may take one or more enforcement actions, depending on the severity and duration of the non-compliance.

Enforcement Actions(continued)

Modification of the Terms of Award:

Include special conditions in the award to identify financial or administrative deficiencies.

Withdraw approval of PI or key personnel if there is basis to conclude that the PI and other key personnel are no longer qualified.

Types of Enforcement Actions

Temporarily withhold grant funds pending correction of the deficiency

Disallow costs

Suspension

Termination

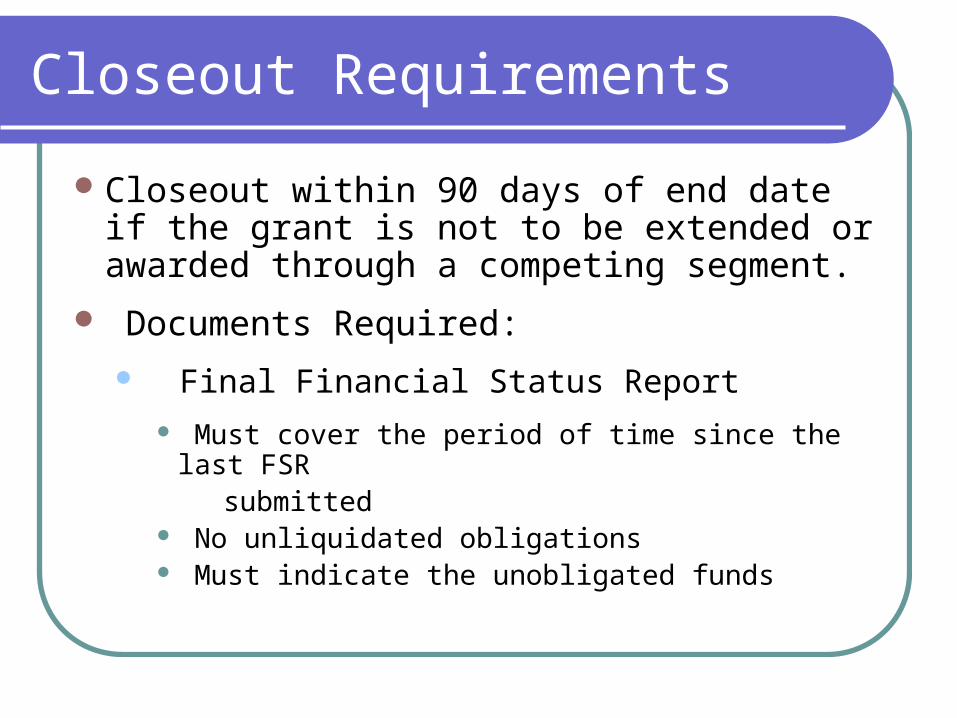

Closeout Requirements

Closeout within 90 days of end date if the grant is not to be extended or awarded through a competing segment.

Documents Required: Final Financial Status Report

Must cover the period of time since the last FSR

submitted No unliquidated obligations Must indicate the unobligated funds

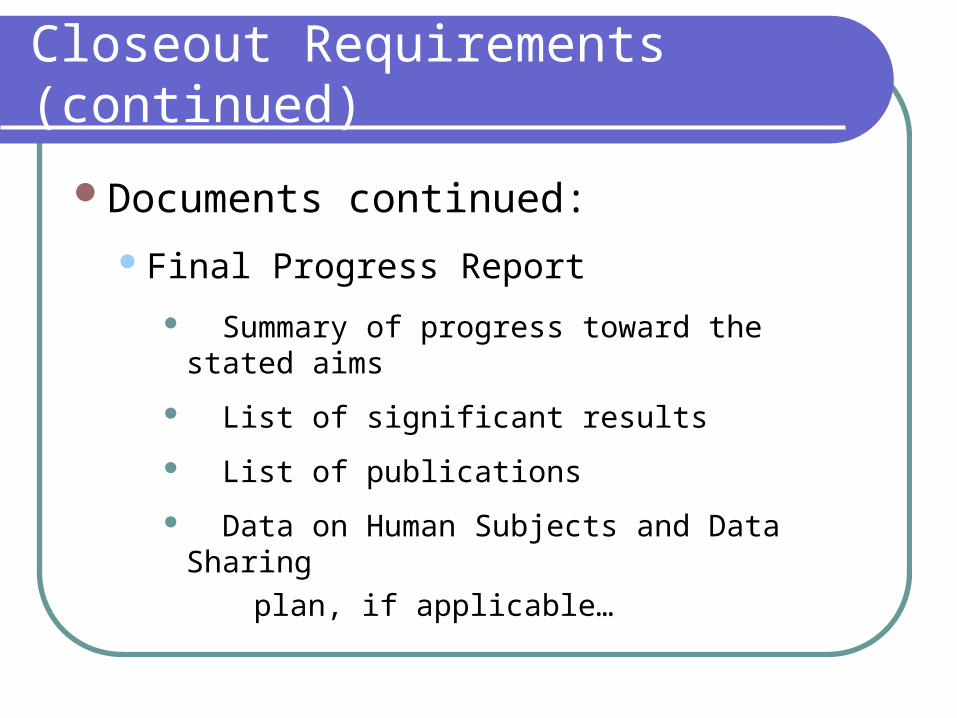

Closeout Requirements(continued)

Documents continued:Final Progress Report

Summary of progress toward the stated aims

List of significant results

List of publications

Data on Human Subjects and Data Sharing

plan, if applicable…

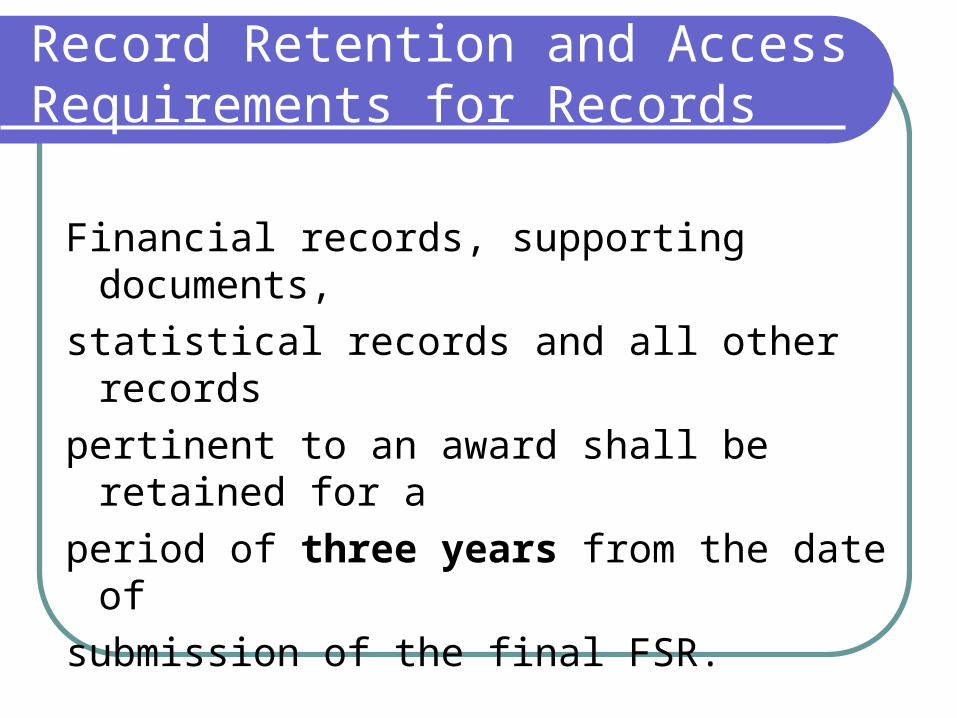

Record Retention and Access Requirements for Records

Financial records, supporting documents,

statistical records and all other records pertinent to an award shall be retained

for aperiod of three years from the date of submission of the final FSR.

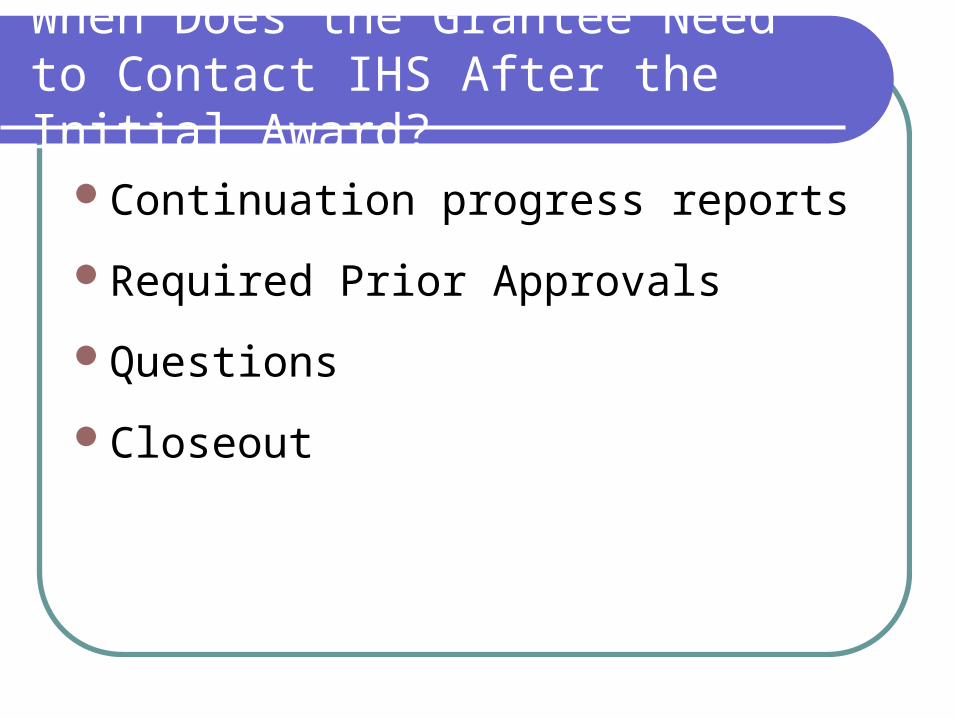

When Does the Grantee Need to Contact IHS After the Initial Award?

Continuation progress reports

Required Prior Approvals

Questions

Closeout

Policy Matters?

Contact Michelle G. Bulls for policy-related matters.

Telephone: 301-443-6290

Email: [email protected]