27

Polish case: Electronic Trading Platform for Treasury securities 4th Annual WB Government Bond Market Conference and Technical Workshop March 12-14, 2014 Bucharest, Romania

Polish case: Electronic Trading Platform

for Treasury securities

4th Annual WB Government Bond Market Conference

and Technical Workshop

March 12-14, 2014

Bucharest, Romania

2

Content

1. Polish Primary Dealership System in short

1) Treasury Securities Dealers in 2014

2) Duties of Treasury Securities Dealers

3) Rights of TSDs

4) Selection of TSDs

2. Electronic trading platform

1) History

2) Market structure and segments

3) Participants

4) Settlement

5) Statistics

3

Treasury Securities Dealers in 2014

The title of Treasury Securities Dealer for the year 2014 was awarded to the following

banks (the alphabetical order, in the competition held from October 31st, 2012 to

September 30th, 2013):

1. Bank Handlowy w Warszawie S.A. (Citibank)

2. Bank Millennium S.A. (BCP)

3. Bank PEKAO S.A. (UniCredit)

4. Bank Zachodni WBK S.A. (Santander)

5. Barclays Bank plc

6. BNP Paribas S.A.

7. Deutsche Bank Polska S.A. (Deutsche Bank AG)

8. Erste Group Bank AG

9. Goldman Sachs International

10. HSBC Bank plc

11. ING Bank Śląski S.A.

12. mBank S.A. (Commerzbank)

13. PKO BP S.A.

14. Société Générale S.A. Oddział w Polsce.

4

Duties of TSDs

• Participation in auctions of Treasury bonds and bills

• Purchase each quarter no less than minimum required share (50% divided by the

number of TSDs selected for a given year) of the total weighted face value of

Treasury Securities sold at auctions (weights: for TS with maturity less than 4 years

– 0.5, for TS with maturity equal or above 4 years – 1.5)

• Submitting bid and offer prices for benchmark TS on the electronic market for at

least 5 hours per day

• Participation in everyday fixing sessions of TS

• Quoting bid/offer TS prices at any request of the Minister of Finance

• Cooperation with the Minister towards further development of the transparent, liquid

and efficient TS market

• Undertaking actions aimed at widening of the investor base.

• Promotion of the TS market

• Duly fulfilment of duties resulting from the participation in the depository/clearing

systems.

5

Rights of TSDs

• Exclusive right to submit bids at all auctions (including switching and buy-back

auctions) of Treasury Securities

• Purchase of TS at non-competitive auctions

• Exclusive rights or preferences in concluding individual transactions with the

Minister of Finance, including:

• repo and buy-sell back transactions

• hedging transactions

• private placement transactions

• securities issuances on foreign markets

• other financial transactions defined by the Minister

• Exclusive right to use the title of a Treasury Securities Dealer in a given year (during

the term of the Agreement on fulfilling the function of TSD)

• Regular meetings with representatives of the Minister of Finance in order to discuss

issuance policy, plans for financing state budget borrowing needs and financial

market conditions and to solve material, organizational and technical problems

connected with functioning of the TS market (Market Participants Council)

6

Selection of TSDs

• Competitive process – rules of candidates’ performance evaluation defined in The

Rules and Regulations Governing the Activities of the Treasury Securities Dealers

(updated annually)

• Competition organized every year, lasting 12 months (4 quarterly assessments)

• Competition for TSDs in the year T starts in October of the year T-2 and ends in

September of the year T-1

203 2014 2015 2016

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

Example

Competition for TSDs in 2015

Beginning date: 1 October 2013

End date: 30 September 2014

Results announced: October/November 2014 TSD

1 October 2013

Final results / Signing of agreements

C O M P E T I T I O N

30 September 2014

7

Selection of TSDs – details

Criteria used for evaluation of TSDs’ and candidates’ performance:

1. Activity on the primary TS market (40%)

• Percentage share of total (weighted) face value of TS sold at auctions within

a given Competition period

• Positive or negative scoring possible

2. Activity on the secondary TS market (40%)

• Quality quotation index - evaluation of the activity on the interbank market,

calculated as weighted mean of spread (75%) and volume (25%) and of

quoting time

3. Co-operation with the Minister (20%)

• Consultations on issuance policy (market preferences, expected demand on

auctions)

• Consultations on current financial markets situation

• Quality of quotations of TS and other financial instrument provided at the

Minister’s request

• Other activities (duly participation in the depository systems, cooperation

towards further development of the transparent, liquid and efficient TS

market, widening the TS investor base and promoting the government TS

market).

8

Further assessment of TSDs

1. Three additional measures of TSDs’ performance, linked to the TSDs’

requirements listed before

2. Measures are binary, i.e. „requirement fulfilled” or „requirement not fulfilled”

3. If any of the requirements is not fulfilled in two consecutive quarters, TSD looses

its status

• Meeting the minimum required share a TSD is obliged to purchase in each

quarter

• Performance for TS benchmark quotation not lower than 90%

• Performance for TS fixings not lower than 90%

9

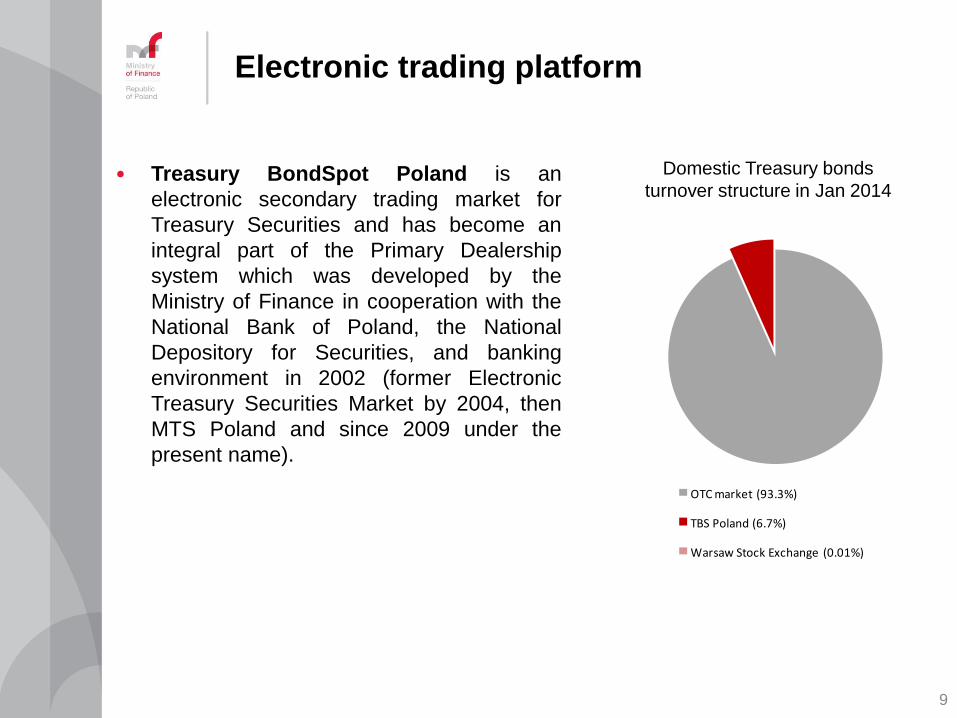

Electronic trading platform

• Treasury BondSpot Poland is an

electronic secondary trading market for

Treasury Securities and has become an

integral part of the Primary Dealership

system which was developed by the

Ministry of Finance in cooperation with the

National Bank of Poland, the National

Depository for Securities, and banking

environment in 2002 (former Electronic

Treasury Securities Market by 2004, then

MTS Poland and since 2009 under the

present name).

OTC market (93.3%)

TBS Poland (6.7%)

Warsaw Stock Exchange (0.01%)

Domestic Treasury bonds

turnover structure in Jan 2014

10

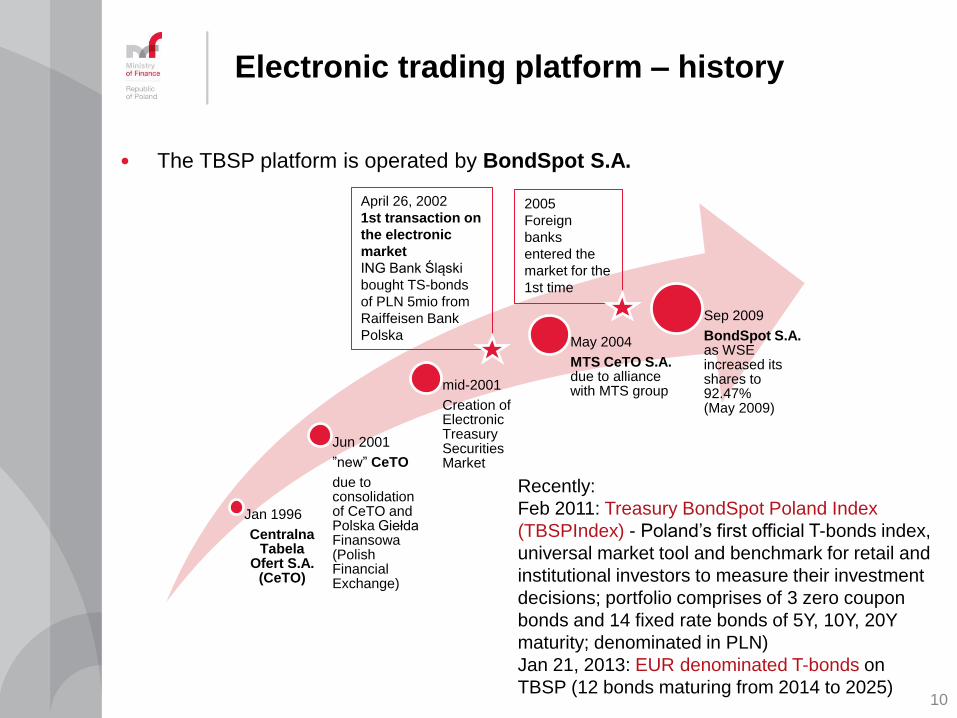

Electronic trading platform – history

• The TBSP platform is operated by BondSpot S.A.

Jan 1996

Centralna Tabela

Ofert S.A. (CeTO)

Jun 2001

”new” CeTO

due to consolidation of CeTO and Polska Giełda Finansowa (Polish Financial Exchange)

mid-2001

Creation of Electronic Treasury Securities Market

May 2004

MTS CeTO S.A. due to alliance with MTS group

Sep 2009

BondSpot S.A. as WSE increased its shares to 92.47% (May 2009)

April 26, 2002

1st transaction on

the electronic

market

ING Bank Śląski

bought TS-bonds

of PLN 5mio from

Raiffeisen Bank

Polska

Recently:

Feb 2011: Treasury BondSpot Poland Index

(TBSPIndex) - Poland’s first official T-bonds index,

universal market tool and benchmark for retail and

institutional investors to measure their investment

decisions; portfolio comprises of 3 zero coupon

bonds and 14 fixed rate bonds of 5Y, 10Y, 20Y

maturity; denominated in PLN)

Jan 21, 2013: EUR denominated T-bonds on

TBSP (12 bonds maturing from 2014 to 2025)

2005

Foreign

banks

entered the

market for the

1st time

11

Electronic market structure

BONDSPOT S.A.

TREASURY BONDSPOT POLAND

Organized, non-regulated

market

CATALYST

wholesale markets

Regulated market

Alternative Trading System

WSE

CATALYST

retail markets

Regulated market

Alternative Trading System

12

Catalyst

• Launched together with the Warsaw Stock Exchange on Sept 30, 2009

• Electronic trading platform for debt securities:

• Corporate bonds

• Municipal bonds

• Mortgage bonds

• Treasury bonds (less popular)

• Operates on 4 transaction platforms:

• Regulated market operated by BondSpot (wholesale market)

• Regulated market operated by WSE (retail market)

• Alternative Trading System operated by BondSpot (wholesale market)

• Alternative Trading System operated by WSE (retail market)

• Operated by 22 domestic brokerage houses and banks (BondSpot platforms)

• Dedicated to institutional and individual investors - adapted to all issuers’

needs seeking for financing their capital needs via private placement or public

offering for securities of different size and parameters

• As of Jan 2014 over 240 series of 90 local and foreign issuers have been

listed on two markets operated by BondSpot with turnover value of almost

PLN 90mio and outstanding value reaching over PLN 500bn (0.02%)..

13

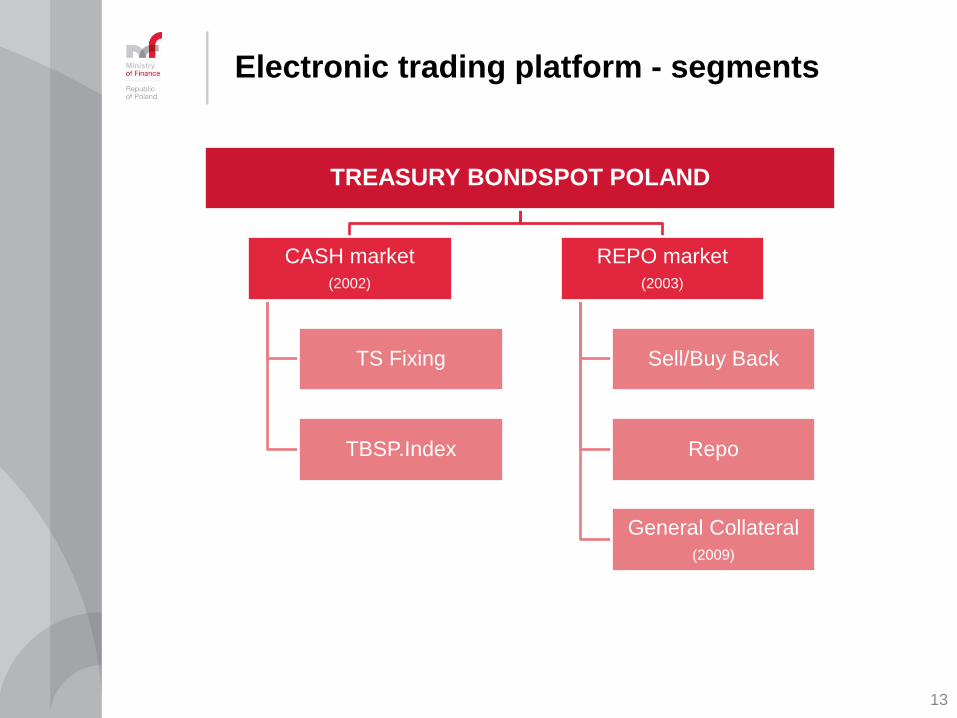

Electronic trading platform - segments

TREASURY BONDSPOT POLAND

CASH market

(2002)

TS Fixing

TBSP.Index

REPO market

(2003)

Sell/Buy Back

Repo

General Collateral

(2009)

14

Electronic market participants

1. Bank Handlowy w

Warszawie S.A.

2. Bank Millennium S.A.

3. Bank PEKAO S.A.

4. Bank Zachodni WBK S.A.

5. Barclays Bank plc

6. BNP Paribas S.A.

7. Deutsche Bank Polska SA

8. Erste Group Bank AG

9. Goldman Sachs

International

10. HSBC Bank plc

11. ING Bank Śląski S.A.

12. mBank S.A.

13. PKO BP S.A.

14. Société Générale S.A.

Oddział w Polsce.

15. Banco Espirito Santo

de Investimento S.A.

16. Bank BPH S.A.

17. Bank Gospodarki

Żywnościowej S.A.

18. Bank Gospodarstwa

Krajowego

19. FM Bank PBP S.A.

20. JPMorgan Securities plc

21. Raiffeisen Bank Polska S.A.

22. UBS Ltd

1. Alior Bank S.A.*

2. Bank Pocztowy S.A.*

3. Bank Polskiej

Spółdzielczości S.A.*

4. OFE PZU "Złota Jesień"

1. Deutsche Bank AG

2. Getin Noble Bank S.A.

3. Merrill Lynch International

4. Morgan Stanley & Co.

International plc

5. Nomura International plc

6. Standard Bank plc

7. Unicredit Bank AG

TREASURY BONDSPOT POLAND

Market Maker (TSDs)

Market Makers (non-TSDs)

Market Takers Institutional

Investors

* Repo market only

15

Electronic market participants – cash market

Market Makers

• Eligible financial institutions designated as TSDs by the MoF and other

institutions willing to participate as MM

• Must have net worth of at least EUR 50mio

• Must commit to market making obligations for assigned securities with a

defined maximum spread and a minimum size according to the market rules

Market Takers

• Eligible financial institutions

• Must have net worth of at least EUR 30mio

• Cannot enter quotes into the system but can place orders against quotes

provided by Market Makers

Institutional Investors:

• Must fulfil two from the following:

• Balance sheet total of at least EUR 20mio

• Annual net turnover of at least EUR 40mio

• Must have net worth of at least EUR 2mio

• Allowed to trade on the repo market as well as on the cash market in

a separate institutional segment (B2C) or act via RFQ.

16

Electronic market participants – MM

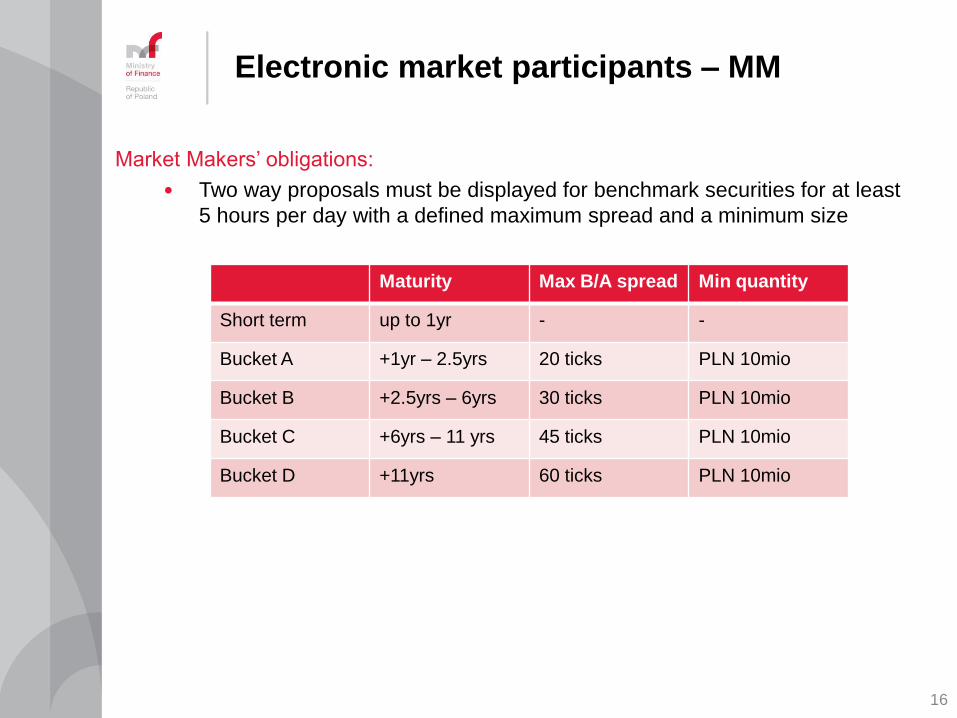

Market Makers’ obligations:

• Two way proposals must be displayed for benchmark securities for at least

5 hours per day with a defined maximum spread and a minimum size

Maturity Max B/A spread Min quantity

Short term up to 1yr - -

Bucket A +1yr – 2.5yrs 20 ticks PLN 10mio

Bucket B +2.5yrs – 6yrs 30 ticks PLN 10mio

Bucket C +6yrs – 11 yrs 45 ticks PLN 10mio

Bucket D +11yrs 60 ticks PLN 10mio

17

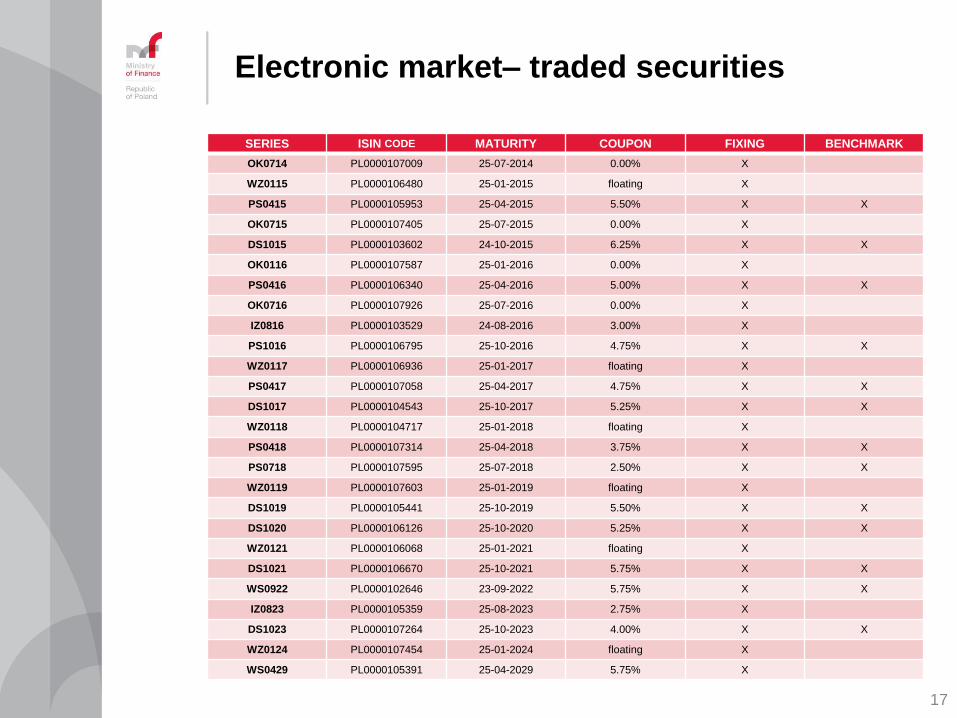

Electronic market– traded securities

SERIES ISIN CODE MATURITY COUPON FIXING BENCHMARK

OK0714 PL0000107009 25-07-2014 0.00% X

WZ0115 PL0000106480 25-01-2015 floating X

PS0415 PL0000105953 25-04-2015 5.50% X X

OK0715 PL0000107405 25-07-2015 0.00% X

DS1015 PL0000103602 24-10-2015 6.25% X X

OK0116 PL0000107587 25-01-2016 0.00% X

PS0416 PL0000106340 25-04-2016 5.00% X X

OK0716 PL0000107926 25-07-2016 0.00% X

IZ0816 PL0000103529 24-08-2016 3.00% X

PS1016 PL0000106795 25-10-2016 4.75% X X

WZ0117 PL0000106936 25-01-2017 floating X

PS0417 PL0000107058 25-04-2017 4.75% X X

DS1017 PL0000104543 25-10-2017 5.25% X X

WZ0118 PL0000104717 25-01-2018 floating X

PS0418 PL0000107314 25-04-2018 3.75% X X

PS0718 PL0000107595 25-07-2018 2.50% X X

WZ0119 PL0000107603 25-01-2019 floating X

DS1019 PL0000105441 25-10-2019 5.50% X X

DS1020 PL0000106126 25-10-2020 5.25% X X

WZ0121 PL0000106068 25-01-2021 floating X

DS1021 PL0000106670 25-10-2021 5.75% X X

WS0922 PL0000102646 23-09-2022 5.75% X X

IZ0823 PL0000105359 25-08-2023 2.75% X

DS1023 PL0000107264 25-10-2023 4.00% X X

WZ0124 PL0000107454 25-01-2024 floating X

WS0429 PL0000105391 25-04-2029 5.75% X

18

Electronic market – repo market

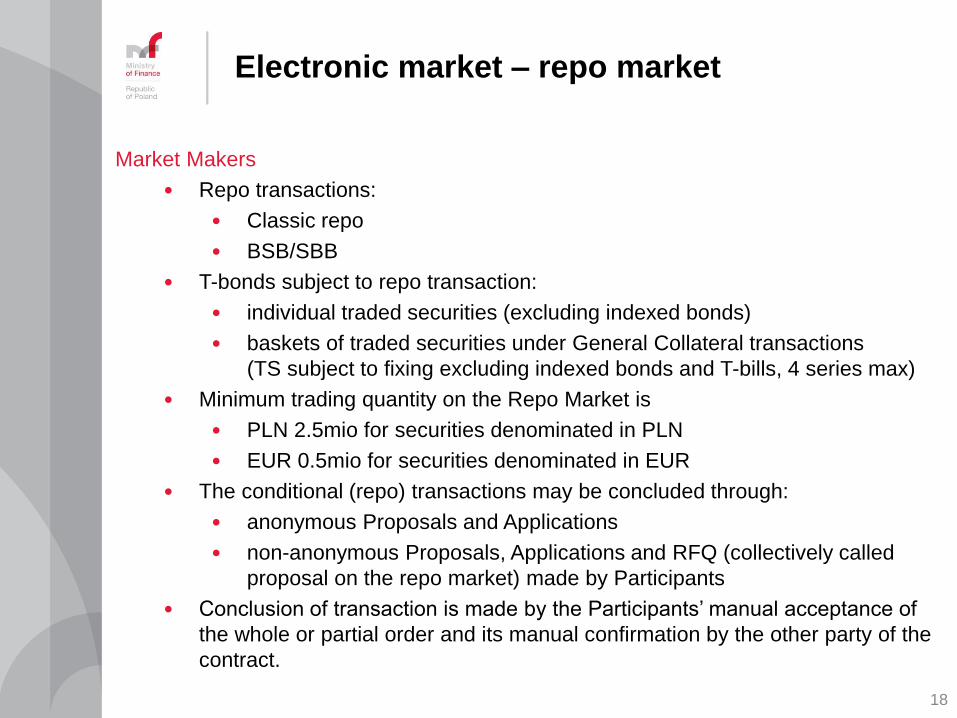

Market Makers

• Repo transactions:

• Classic repo

• BSB/SBB

• T-bonds subject to repo transaction:

• individual traded securities (excluding indexed bonds)

• baskets of traded securities under General Collateral transactions

(TS subject to fixing excluding indexed bonds and T-bills, 4 series max)

• Minimum trading quantity on the Repo Market is

• PLN 2.5mio for securities denominated in PLN

• EUR 0.5mio for securities denominated in EUR

• The conditional (repo) transactions may be concluded through:

• anonymous Proposals and Applications

• non-anonymous Proposals, Applications and RFQ (collectively called

proposal on the repo market) made by Participants

• Conclusion of transaction is made by the Participants’ manual acceptance of

the whole or partial order and its manual confirmation by the other party of the

contract.

19

Electronic market – trading and settlement

• Trading hours: 9.00 a.m. - 5 p.m. Monday to Friday, excluding holidays

• Real-time information on current offers and transactions concluded on TBS

Poland (distributed via MTS and WSE) and the fixing on bonds are presented

in the news bulletins Bloomberg and Reuters

• Daily market data and statistics are published after a trading day is finished

Settlement

• All trades executed on BondSpot markets are settled by the National

Depository for Securities (T-bonds and other debt instruments) and the

National Bank of Poland (T-bills)

• Cash market transactions in traded securities are settled:

• at T+2 time, where T is the date of the transaction.

• at T+3 time for securities denominated in EUR

• Conditional (repo) transactions are settled:

• at T+0 time or another time agreed by the parties of transaction in case of

the opening transaction

• at time agreed by the parties of transaction, after the day of settlement of

opening transaction but no later than 365 days after the opening transaction

settlement day in case of the closing transaction.

20

Electronic market statistics – monthly

average turnover

• Significant change since Nov 2011 when new regulations were introduced

• The highest increase in TBSP market share in the T-bonds market; in 2012 above

the level of 12%, by 2013 at the level of 9%.

* Turnover single counted.

21

Electronic market statistics – annual

turnover

* Turnover single counted.

22

Electronic market statistics – effects of new

TSD rules on volumes

23

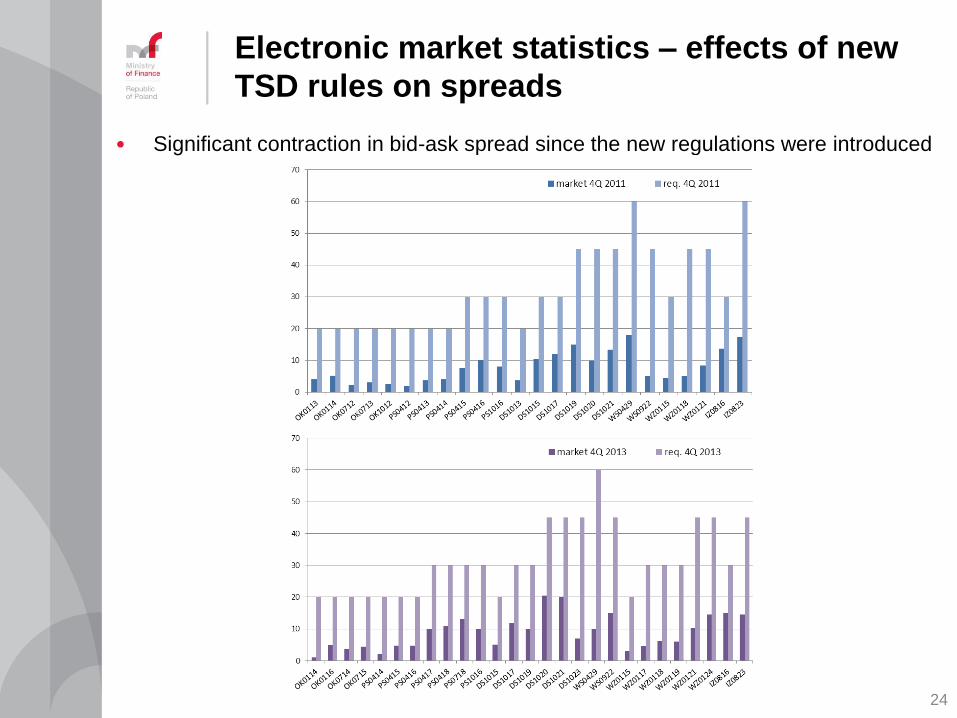

Electronic market statistics – effects of new

TSD rules on volumes

24

• Significant contraction in bid-ask spread since the new regulations were introduced

Electronic market statistics – effects of new

TSD rules on spreads

Thank you for your attention

Ministry of Finance

www.mf.gov.pl

Bloomberg: PLMF <GO>

Reuters: PLMINFIN

26

Selection of TSDs – previous rules

Criteria used for evaluation of TSDs’ and candidates’ performance until the

competition in 2012:

• Market share in OTC outright inter-bank transactions on TS

• Market share in OTC outright transactions on TS with non-banking clients

• Market share in outright transactions on the Electronic Market (calculated

for own price and another entity’s price separately)

• Market share in repo, sell-buy back and buy-sell back transactions on TS

• Share in the turnover on FRA and IRS market (in Polish Zloty)

• Market share in transactions on Polish government securities

denominated in euros

• Other (location of dealing activities, quality of TS quotations submitted at

the request of the Minister of Finance, cooperation with the Minister of

Finance with regard to issuance policy and financial market functioning).

27

Selection of TSDs – rationale for changes

• Preservation of the stimulating mechanism of TS market development and

selection of banks with the greatest potential and activity on the market

• Preservation & strengthening of the mechanism that ensures safety of financing of

State borrowing requirements

• Preservation of the mechanism promoting Electronic market transactions as the

one significantly increasing transparency of the TS market

• Simplification of rules that used to be in force and elimination of redundant criteria

• Eliminating as much as possible those elements that might distort proper

evaluation of banks

• Taking into account propositions submitted by current TSDs

• Taking advantage of practices of other European countries with TSD system.