1 “Portfolio Risk Management Using Six Sigma Quality Principles” Abstract As the financial crisis of 2008 has revealed, there are some flaws in the models used by financial firms to assess risk. Credit, volatility, and liquidity risk were all inadequately modeled by supposedly sophisticated financial institutions employing dozens of financial engineers with advanced degrees. What went wrong? It is now becoming clear that some of the underlying assumptions of the statistical models utilized were seriously flawed, and interactive and systemic effects were ignored or improperly modeled. Correcting these modeling flaws is one approach to preventing a reoccurrence. However, another approach is suggested by Six Sigma quality programs used in manufacturing and service industries. Some basic tenets of the Six Sigma programs are directly applicable to improving risk management in financial firms and in portfolio design. These include the features of over-engineering, robust design, and reliability engineering. This paper will discuss the main features of Six Sigma quality programs, show how they can be applied to financial modeling and risk management, and demonstrate empirically that the Six Sigma approach would have provided an adequate safety margin at the actual daily one percent Value-at-Risk measure observed for the period from 1926 to 2011. Keywords: risk management, VaR, Black Swan event, Six Sigma, portfolio design Introduction In March of 2008 Bear Stearns was acquired by JP Morgan Chase after becoming insolvent. Bear Stearns had been considered one the best Wall Street firms in managing risk. Within a few months Lehmann Brothers had gone bankrupt, Merrill Lynch had been acquired by Bank of America, Wachovia merged with Wells Fargo, and Washington Mutual with JP Morgan Chase. American International Group (AIG) was bailed out by the federal government and many hedge funds have failed. What had caused so many prominent financial institutions to succumb in such a short time? The common explanation is sub-prime mortgages defaulting, but the real problem is much more fundamental—a failure of risk management. The no down-payment, no income verification mortgages issued by many reputable financial institutions may have started the problems, but they would not have spread worldwide without the explosive advance in securitization of these assets (Collateralized Debt Obligations or CDO’s) by financial firms and the high credit ratings assigned to them by the rating agencies Standard & Poor’s and Moody’s. The problems would probably not have grown to be a global financial crisis if so many other financial institutions had not purchased these risky assets including many banks in Europe and hedge funds around the world. Once the dominos began falling, liquidity dried up, and equity markets plummeted. The outcome became a financial crisis leading to a global recession which still continues.

Transcript

1

“Portfolio Risk Management Using Six Sigma Quality Principles”

Abstract

As the financial crisis of 2008 has revealed, there are some flaws in the models used by

financial firms to assess risk. Credit, volatility, and liquidity risk were all inadequately

modeled by supposedly sophisticated financial institutions employing dozens of financial

engineers with advanced degrees. What went wrong? It is now becoming clear that

some of the underlying assumptions of the statistical models utilized were seriously

flawed, and interactive and systemic effects were ignored or improperly modeled.

Correcting these modeling flaws is one approach to preventing a reoccurrence. However,

another approach is suggested by Six Sigma quality programs used in manufacturing and

service industries. Some basic tenets of the Six Sigma programs are directly applicable

to improving risk management in financial firms and in portfolio design. These include

the features of over-engineering, robust design, and reliability engineering. This paper

will discuss the main features of Six Sigma quality programs, show how they can be

applied to financial modeling and risk management, and demonstrate empirically that the

Six Sigma approach would have provided an adequate safety margin at the actual daily

one percent Value-at-Risk measure observed for the period from 1926 to 2011.

Keywords: risk management, VaR, Black Swan event, Six Sigma, portfolio design

Introduction

In March of 2008 Bear Stearns was acquired by JP Morgan Chase after becoming

insolvent. Bear Stearns had been considered one the best Wall Street firms in managing

risk. Within a few months Lehmann Brothers had gone bankrupt, Merrill Lynch had

been acquired by Bank of America, Wachovia merged with Wells Fargo, and Washington

Mutual with JP Morgan Chase. American International Group (AIG) was bailed out by

the federal government and many hedge funds have failed. What had caused so many

prominent financial institutions to succumb in such a short time? The common

explanation is sub-prime mortgages defaulting, but the real problem is much more

fundamental—a failure of risk management.

The no down-payment, no income verification mortgages issued by many reputable

financial institutions may have started the problems, but they would not have spread

worldwide without the explosive advance in securitization of these assets (Collateralized

Debt Obligations or CDO’s) by financial firms and the high credit ratings assigned to

them by the rating agencies Standard & Poor’s and Moody’s. The problems would

probably not have grown to be a global financial crisis if so many other financial

institutions had not purchased these risky assets including many banks in Europe and

hedge funds around the world. Once the dominos began falling, liquidity dried up, and

equity markets plummeted. The outcome became a financial crisis leading to a global

recession which still continues.

2

How could these sophisticated financial institutions have been so wrong in their

assessment of credit and market risk? After all, many had invested millions of dollars in

risk modeling and believed that they had a good handle on risk management. With

increasing power of computer hardware and software, firms were able to build

complicated models using advanced statistical techniques and Monte Carlo simulations.

To develop these models they hired dozens of mathematicians, statisticians, physicists,

and computer scientists, and a new profession was created—the financial engineer. Very

few top executives responsible for risk management likely understood these models, but

they confidently used them to take ever-riskier positions to increase profitability, often

driven by competitive pressures. Short-term oriented compensation schemes fostered

excess risk-taking in many of these financial firms. Few believed that there were any

flaws in the models.

Clearly there were some critical elements in the risk models that caused them to fail when

they were most needed. In the next section we will examine some of the deficiencies of

these models. In subsequent sections Six Sigma quality programs will be explained and

it will be shown how the process and methods of Six Sigma can be applied to financial

instrument and portfolio design. An empirical example using returns data from T-Bills,

NYSE/AMEX and NASDAQ over a period of 49 years from 1963 to 2011 will be

presented. The case will be made for robust portfolio design and reliability engineering

used as the way to achieve robustness. The last section draws some conclusions.

Flaws in Risk Modeling

The most commonly used model to measure risk is the VaR or Value-at-Risk. It is based

on the Gaussian or normal probability distribution widely used for many applications in

business, science, education and other fields. By specifying an acceptable confidence

level for unlikely occurrences (such as the probability of a 5% chance of a 30% fall in the

price of a stock), risk managers could feel comfortable that these rare events had such a

low probability they could be neglected. A three sigma confidence level indicates a 0.3

percent chance (3 in 1000) of the event occurring. The probabilities were based on

historic price and volatility data for various types of assets. This stochastic approach to

risk management seemed safe and reasonable as long as the underlying assumptions of

the statistical model are valid. However, as recent events have dramatically illustrated

some of the underlying assumptions are clearly not valid.

The most serious flaw in the VaR models is the assumption that the underlying

distribution is Gaussian. There is much evidence that many asset prices follow a

distributive pattern that is not a Gaussian, or normal, distribution (Mandelbrot 1963,

Fama 1965, Kon 1984, Chen 2015). This means that rare events such as a sharp fall in a

market occur much more frequently than a normal distribution would predict. With the

Gaussian model an event like the September 29, 2008, drop in the DJIA of 777 points or

7% had a probability of 1 in a billion, a probability so small that it can be neglected and

is essentially unpredictable with conventional forecasting models (Mandelbrot and

Hudson, 2004). These Black Swan events happen much more often than any Gaussian

3

model can predict. Taleb (2007) defines a Black Swan event as one that is rare, has an

extreme impact, and is retrospectively (though not prospectively) predictable. The 2008

crash can be seen as a Black Swan event that the models did not predict. Since a Black

Swan event cannot be predicted, what can a risk modeler do? Suggestions will be offered

below on how to mitigate the consequences of such events.

VaR models assume that the distribution is symmetric. There is substantial research

evidence that this assumption is invalid for many asset prices and markets. Risk

preferences are often asymmetric towards upside and downside risk. Arditti (1967) show

that investors prefer positive to negative skewness in returns. Mitton and Vorkink (2007)

find that a sample of investors in a discount brokerage firm hold less than optimal

portfolios according to mean-variance theory with lower Sharpe ratios and positive

skewness. The multivariate normal assumption of symmetry is therefore suspect.

Gaussian-based risk modeling assumes a stationary distribution with no shift of the mean.

In reality, for a variety of reasons both economic and psychological, the mean of a

distribution of asset prices may suddenly shift (economists call this a regime change),

leading to a greater area in one tail of the distribution than previously forecast. Such a

mean shift can increase dramatically the probability of an unlikely event that might have

seemed remote before, such as a sudden, large fall in a market. The stationarity

assumption is also empirically suspect (Considine 2008).

Another flaw in conventional VaR models is the volatility variable utilized. This is the

standard deviation (sigma) from the normal distribution based on historic volatility.

There are three problems with this approach. First, if the underlying distribution (the

normal) is not the correct one, then standard deviation as a measure of variability will

also be wrong (Haug and Taleb 2008). Second, historic volatility may not be a good

representation of future volatility. If in fact the distribution is leptokurtic, then a

variability measure based on the normal distribution will seriously underestimate the

probability of an extreme movement. Third, volatility is not stationary (Chen 2015). In

times of market stress, volatility can spike dramatically. Many risk management models

were calibrated to 2003-2006 volatility which was very low by historical standards

(Varma 2009). There is also evidence for volatility clustering and intra-day volatility

being much greater than day-to-day volatility which is typically used in risk modeling

(Basu 2009).

A further problem with conventional risk modeling is the assumption of independence of

various markets and assets. This is clearly not a valid assumption in times of market

stress as they become much more correlated as recent events demonstrate. Heightened

volatility in one market quickly spreads to another increasing the covariance of the

markets. Under such conditions of contagion, diversification by country or asset class

does not provide the expected protection. Correlations among assets categories and

markets have been shown to be non-linear (increasing in times of market stress) and

asymmetric (differing between rising and falling markets). (Varma 2009) As the recent

financial crisis has demonstrated, a sudden loss of liquidity in markets and rapid changes

4

in credit-worthiness of counterparties are examples of systemic risk. These risks were not

well modeled in VaR-based risk management systems.

VaR models are typically validated by backtesting against historical data. This presents a

set of problems that make their use suspect. The asset prices and markets used, the

historical period selected, and measurement errors as well as model misspecification all

can lead to improper validation of the VaR models used by financial institutions.

Escanciano and Pei (2012) and Gabrielsen, et al (2012) discuss these issues and propose

better methods for backtesting of VaR models.

These same deficiencies underlie much of modern finance theory. Mean-variance

portfolio optimization (Markowitz, 1952), the Capital Asset Pricing Model (Sharpe,

1964), and the Black-Scholes Option Pricing Model (Black and Scholes, 1973) all are

based on the Gaussian probability distribution. If this is not the correct distribution for

modeling asset prices, or variance is incorrectly measured, or mean shifts occur and

markets are interdependent, then these models must be suspect as well. Yet many asset

pricing and investment decisions are made based on these models. This also contributed

to the recent financial crisis (Haug and Taleb 2011, Varma 2009).

All of these deficiencies in conventional risk modeling (non-normal distributions, mean

shifts, volatility measures, and lack of independence) are not easily overcome with

standard statistical techniques. One can use a leptokurtic distribution like the Student’s t,

model regime changes, attempt to find better measures of prospective volatility, and

model interdependencies between markets, but there are disagreements about appropriate

ways to accomplish these improvements, and there are no standard methods. As Chen

(2015) notes “The problem is so severe that we may need to concede that the entire class

of problems best modeled by fat-tailed distributions transcends the category of risk,

where probability is quantifiable, and enters the distinct category of uncertainty, where

probability is unquantifiable.” Another approach may be needed in such a situation, and

one that holds promise to improve risk modeling is Six Sigma, which is widely used in

quality and process improvement programs in industry and services. This will be

discussed in the following section.

Six Sigma Quality Programs

Beginning in the 1980’s at Motorola Corporation, Six Sigma quality programs have

slowly spread through American manufacturing and recently have been applied in service

businesses like banking, hospitals, and even government. The basic idea behind Six

Sigma is to reduce variability in processes to improve quality and increase efficiency.

The rigorous application of statistical tools to targeted business processes has led to some

dramatic improvements. The most visible example of success with Six Sigma has been

General Electric Company which has used it widely in manufacturing and transactional

areas calculating the savings corporate-wide at $3 billion (Evans and Lindsay, 2008). A

key insight that underlies the Six Sigma philosophy is that as business processes and

products become more and more complex, a much higher level of internal quality is

5

needed. This leads to some methods of the Six Sigma toolkit being directly applicable to

financial modeling, which like manufacturing has become increasingly complex with

significant interactions among variables.

The name Six Sigma refers to six standard deviations from the mean. This signifies a

level of quality equal to three defects per billion opportunities based on the normal

distribution. To many observers this seems like an unnecessarily high level of quality

that is not only unattainable but too expensive. However, when one considers several

characteristics of products and processes as well as how Six Sigma programs are carried

out, these objections are not valid. The cost criticism can be rejected in some cases based

on the experience of companies like GE that have found that the savings from reduction

in defects (i.e. scrap, rework, warranties, etc.) and improved process efficiency far

outweigh the costs of implementing the program (Evans and Lindsay, 2008).

The criticism of being an unrealizable goal has also been disproved by companies such as

Motorola, GE and others that have attained six sigma quality levels in both

manufacturing and transactional areas like bill processing. But whether such a high

standard is really needed is a further issue. One consideration is an issue neglected in

VaR models discussed in the previous section. This issue is the probability of mean

shifts in the process being considered (due to such factors in production processes such as

variations in machine and human performance over time). Six Sigma programs typically

assume a 1.5% shift in the mean is possible and adjust for this by seeking a higher sigma

level than would otherwise be needed with no such mean shift. With a 1.5% mean shift,

Six Sigma quality becomes three defects per million opportunities (rather than per

billion), and this is commonly the statistical quality level assumed in a Six Sigma

program where the mean is assumed likely to shift. In investment portfolios mean shifts

of the return distribution can be expected to occur due to contagion causing increasing

covariance in financial crises.

For a product with multiple parts, the reliability of the product is a multiplicative function

of the reliability of its component parts. For example, in a product with a thousand parts,

each one having a reliability of six sigma, the overall reliability of the product is about

three sigma (3 defects per thousand). Many products have more than one thousand

parts—a car has about 2000-3000 parts and a jetliner 200,000-300,000 parts and

components. Therefore, designing in very high levels of individual component

performance is essential to reliability of the finished product. This suggests one

fundamental aspect of Six Sigma that has direct applicability to financial modeling—

what we might call over-engineering. The more assets an investment portfolio contains

and the more complex these assets may be (i.e. derivatives), the greater the possibility of

severe drawdown in a financial crisis.

Rather than assume that we are correctly modeling the underlying distribution with the

Gaussian, Six Sigma builds in a margin of error for fat tails. Although Six Sigma

statistical processes are also based on the normal distribution, the high levels of sigma

applied provide a much greater safety margin than the normal three sigma assumption of

VaR. Correctly specifying the underlying distribution becomes much less critical in a Six

6

Sigma process--it does not matter very much when the probability of a tail event is so

small.

Mean shifts, another weakness of financial models, is allowed for explicitly in Six Sigma

by targeting a high level of standard deviations. Even if the mean does shift, as it is

assumed likely to do, in Six Sigma the confidence level is still very high. This again

illustrates the concept of over-engineering the process to account for rare but expected or

unexpected occurrences.

In a similar fashion, the proper measurement of variability in a process is also less

critical. A machine’s variability may be more accurately captured by historic data than

an asset price, but again the margin of error for an incorrect assessment is much greater

with a six sigma confidence level. Once more we find the concept of over-engineering

being applied.

The fourth weakness of traditional financial models is the interactive effects between

financial instruments and markets. Six Sigma quality programs face a similar problem in

complex processes with many interacting variables. An example is a metal plating

process where temperature, humidity, fluidity, and other factors all affect process results.

Six Sigma has developed ways to analyze these interactive effects and determine the best

combination of variables to minimize process variation. These are part of the process of

robust design and include methods like Design of Experiments (DOE) and Design Failure

Mode and Effects Analysis (DFMEA). These and other methods for robust design will

be discussed in the next section.

Another element of Six Sigma that has applicability to financial risk modeling is

reliability engineering. This concept is used in product design where failure of one

component can lead to failure of others and even complete product failure. Especially

when components operate in series, it is essential to build in high levels of reliability and

use redundant systems as backup. An example is an auxiliary power or hydraulic system

on a airplane that kicks in if the main system fails. Design of financial products can also

take account of the interactive effects of the instruments and markets and attempt to build

in reliability. It would involve extensive stress testing and simulation of performance

under a variety of conditions. It could also involve using hedging instruments to add

resiliency. This concept will be considered in a subsequent section along with other

suggestions and a process for applying Six Sigma to the design of financial products.

First, though, let us examine if a Six Sigma approach to portfolio construction would

prevent massive drawdowns during financial crises.

7

Empirical Investigation: Can Six Sigma Give Us A More Realistic Measure of

Value-at-Risk? Example on Portfolio Construction and Results

Since the normal distribution is known to severely underestimate the tail probability

density of actual rates of returns, we cannot get a realistic measure of the Value-at-Risk

(VaR) that is computed based on the mean and standard deviation from a normal

distribution. A relatively easy and direct approach to resolve this issue is to amplify the

standard deviation used in the VaR calculation while still keeping the normal distribution

assumption. This is akin to fitting the tail of the actual distribution with a normal

distribution by inflating the standard deviation of the normal distribution. For example,

the one percent VaR is computed as: 𝐸(𝑅) − 2.33 × 𝜎. The essence of the Six Sigma

approach we propose here is to replace the actual standard deviation, 𝜎, by an amplified

version of this standard deviation, 𝜋 × 𝜎, where π is the multiplicative factor. Following

the standard Six Sigma approach, one would amplify the standard deviation six times (π

=6). Would this be adequate to give us a realistic measure of the one percent VaR and

thereby provide an adequate safety margin for actual outcomes? To address this

question, we analyze the distribution of actual daily portfolio returns for portfolios

constructed using stocks that were traded on NYSE/AMEX and NASDAQ over a period

of 49 years from 1963 to 2011. These portfolios are the value-weighted, equally-

weighted, S&P500, and Decile 1 through Decile 10 portfolios.

Description of Data

The data used in this study are the daily returns for stocks traded on NYSE/AMEX

/NASDAQ over the period from 1963 to 2011. These stocks are organized into portfolios

for our analysis. The value-weighted and equally-weighted portfolios contain all the

stocks that existed in each year. The weight of each stock in the value-weighted portfolio

is determined by the market capitalization of the stock relative to the total market

capitalization. The decile portfolios for each year are formed by grouping stocks into ten

portfolios based on market capitalization with each portfolio containing roughly the same

number of stocks. Each decile portfolio is also constructed using the value-weighted

method. Decile 1 contains stocks with the smallest market capitalization and Decile 10

the largest market capitalization.

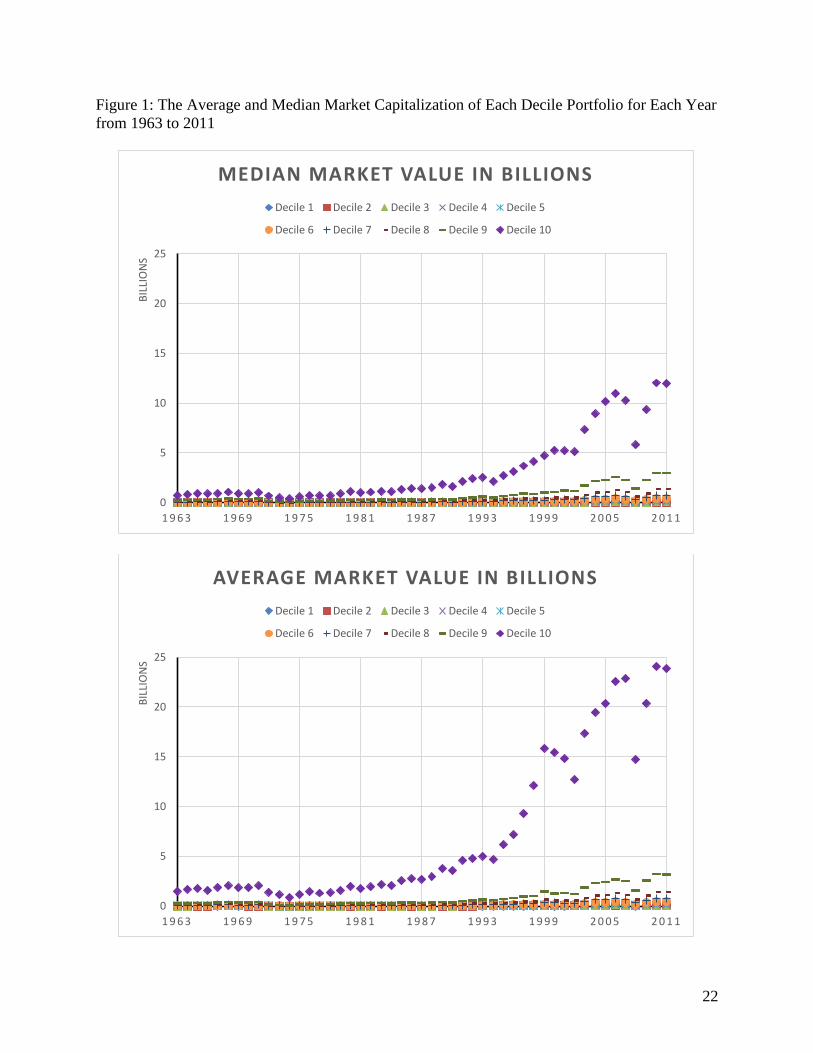

Table 1 shows the number of stocks that are in each decile portfolio for each year from

1963 to 2011. The total number of stocks traded in NYSE/AMEX /NASDAQ reached a

peak of 9,520 stocks in 1997 and since then the number of stocks has reduced over time

to 5,602 stocks in 2011. Figure 1 shows a plot of the average and median market

capitalization of each decile portfolio over time. For the largest decile portfolio, Decile

10, the average market capitalization is roughly twice its median market capitalization

value suggesting that within Decile 10, the market capitalization for the top half in this

decile is a lot larger than the bottom half.

(Insert Figure 1 here)

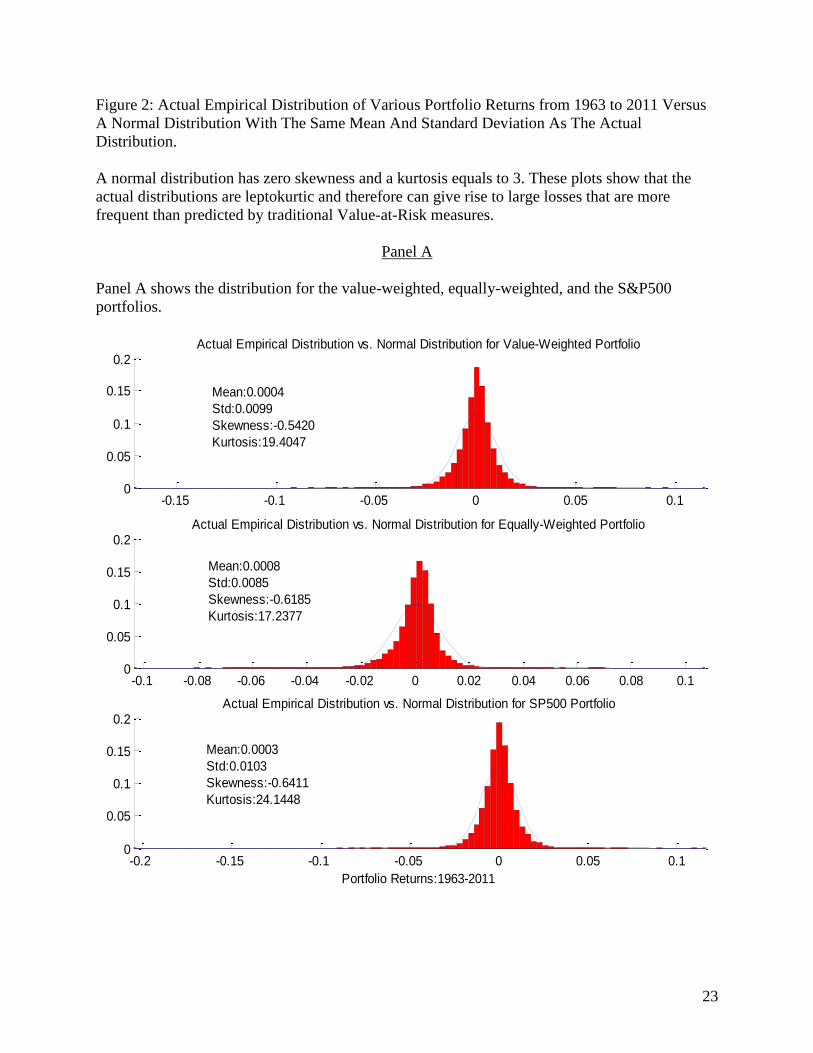

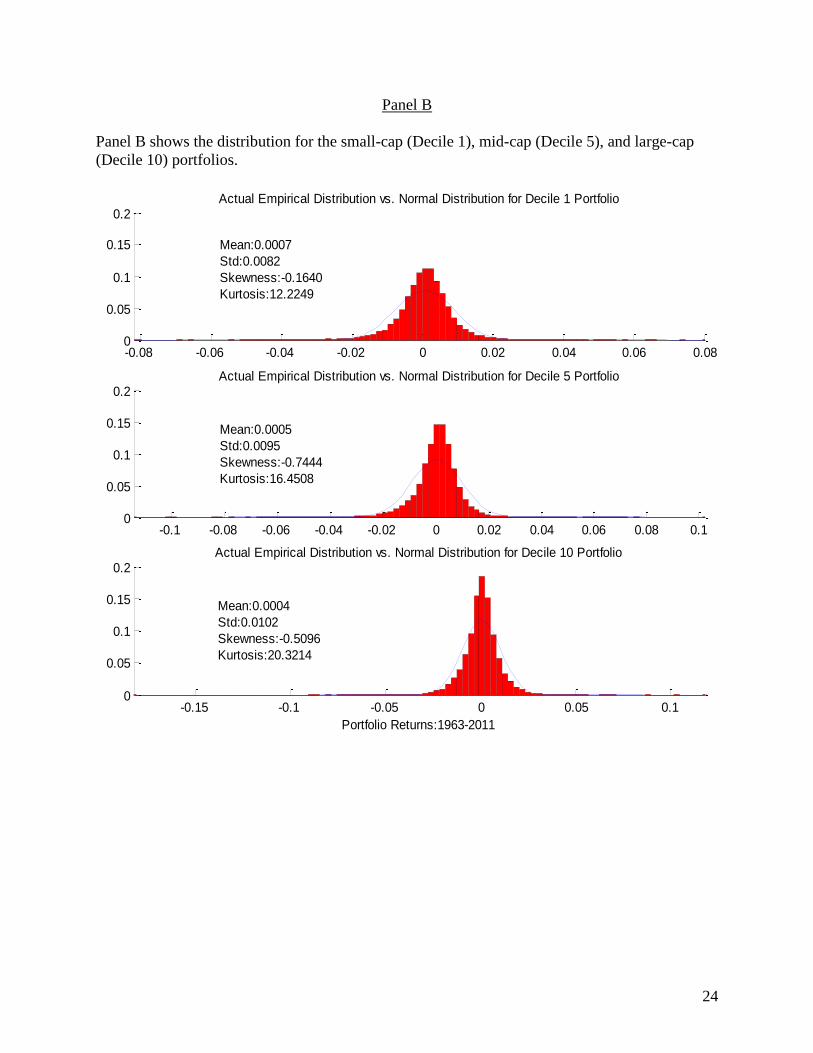

We pointed out at the start of this section that the normal distribution severely

underestimates the tail probability density of actual rates of returns. To provide a visual

8

illustration of this problem, we present Figure 2. Figure 2 compares the actual empirical

distribution of portfolio returns to a normal distribution with identical average return and

standard deviation as the actual distribution. The actual empirical distribution is

represented as a histogram and the normal distribution by a line in Figure 2. To save

space, we present the results for only the value-weighted, equally-weighted, S&P500,

Decile 1, Decile 5 and Decile 10 portfolios. In all cases we see that the actual

distributions are leptokurtic in comparison to the normal distribution. The kurtosis for a

normal distribution is 3 and the kurtosis for the actual distributions ranges from 12.22 to

24.14. It is therefore not surprising that the extreme losses that were encountered in

practice are much larger and more frequent than predicted by traditional VaR measures

that assume that returns are normally distributed.

(Insert Figure 2 here)

Next, we explain how we calculate the multiplicative factor in the six-sigma approach we

propose to address the problems in traditional VaR measures and discuss the results.

Calculation of the Sigma Multiplicative Factor

An easy and direct approach to resolve the problems in traditional VaR measures is to

amplify the standard deviation used in the VaR calculation while still keeping the normal

distribution assumption. In other words, we calculate the one percent VaR as 𝐸(𝑅) −2.33 × 𝜋 × 𝜎 where 𝜋 is the multiplicative factor. Following the standard Six Sigma

approach, one would amplify the standard deviation six times, that is set π =6. Would this

be adequate to give us a realistic measure of the one percent VaR and thereby provide an

adequate safety margin for actual outcomes? We present our results in Figure 3 and 4.

The actual values for the multiplicative factors are presented in Tables 2, 3, and 4. The

essence of our findings is that a multiplicative factor of “6” is adequate to compensate for

the higher likelihood of encountering extreme events in actual distribution.

To simplify our exposition, we will use t to identify a period that starts at t and ends right

before t+1. For instance, if the period is a year, then t could be Jan 1st, 1963 and t+1

would be Jan 1st, 1964. We begin by first calculating the empirical one percent VaR for a

given period, t, by sorting the returns in ascending order and then determining the cut-off

value, 𝑅∗𝑡, at the 1% level. We then calculate the multiplicative factors associated with

the ex-post and ex-ante theoretical VaR. In both cases, we need to determine the value of

the multiplicative factor, 𝜋, that is necessary for the theoretical VaR to match the

empirical VaR. The calculations are summarized by the following two equations:

Ex-Post Theoretical VaR: 𝜇𝑡 − 𝜋|𝑍𝛼|𝜎𝑡 = 𝑅∗𝑡 or

𝜋𝑡 =𝜇𝑡 − 𝑅∗

|𝑍𝛼|𝜎𝑡

Ex-Ante Theoretical VaR: 𝜇𝑡−1 − 𝜋|𝑍𝛼|𝜎𝑡−1 = 𝑅∗𝑡 or

𝜋𝑡 =𝜇𝑡−1 − 𝑅∗

|𝑍𝛼|𝜎𝑡−1

9

Note that R* is a negative value and |𝑍𝛼| is the z-score of the standard normal

distribution at the (1-α%) (e.g. α%=1%) cut-off of the left tail. For a 1% VaR, 𝑍𝛼 = 2.33.

The difference between the ex-post and ex-ante theoretical VaR calculation lies in what

we used as estimates for the average return, 𝜇, and standard deviation, 𝜎, in the

calculation. In the ex-post VaR calculation, we use the sample estimates for the average

return and standard deviation from period t; the same period used to determine the actual

empirical VaR. But in the ex-ante VaR calculation, we use the sample estimates for the

average return and standard deviation from the preceding period, which is (t-1). In other

words, we use the average return and standard deviation in the preceding period as a

forecast of the same variables in the current period. In managing the risk of actual

portfolios with VaR, we do not know in advance the actual average return and standard

deviation that are needed for calculating the VaR for the forward looking period and

therefore will have to forecast these values. Clearly our analysis for the ex-ante VaR case

employs a rather naïve forecasting method for forecasting the average return and standard

deviation. The point we want to demonstrate is whether the six-sigma approach could

indeed work in practice even with a naïve forecast of the average return and standard

deviation. If it works, then it would certainly work better with more sophisticated

forecasting method. Consequently, the results for the ex-ante case will be critical in

shedding light on the validity of the six-sigma approach.

The calculations above assume daily returns and the computation of VaR for a 1-day

horizon. For a h-day horizon VaR, the calculation of the multiplicative factor, assuming

returns are iid, becomes

𝜋(ℎ)𝑡 =(𝜇𝑡−1 − 𝑅∗

𝑡) × ℎ

|𝑍𝛼|𝜎𝑡−1 × √ℎ= √ℎ × 𝜋𝑡

The results for the ex-post VaR case are presented in Figure 3 and Table 2. Figure 3

shows that that the multiplicative factor for each portfolio consistently remains less than

3 over the 49 years from 1963 to 2011.

(Insert Figure 3 here)

This implies that if we have perfect forecast of the average return and standard deviation

for the period in which we want to compute the VaR, then using a multiplicative factor of

6 is more than adequate to compensate for the higher likelihood of encountering extreme

events in the actual distribution. Obviously, we cannot expect to have perfect forecast of

the average return and standard deviation in the future period. To better understand if the

six-sigma approach will be useful in practice, we repeat the analysis by using a naïve

forecast described earlier. The results for the multiplicative factor associated with naïve

forecast or what we called the ex-ante VaR case are presented in Figure 4 and Table 3.

(Insert Figure 4 here)

10

We see from Figure 4 that the values for the multiplicative factors rarely exceed 6 times

over the 49 years even with a naïve forecast of the average return and standard deviation.

To be more specific, Table 3 shows that the values for the multiplicative factor exceed 6

only once for some portfolios. This happened in 1987 for Decile 3, Decile 4, Decile 5,

Decile 6, and Decile 7 portfolios and their respective values for the multiplicative factor

are 6.70, 6.80, 6.78, 6.32, and 6.10. Even when the value for the multiplicative factor

exceeds 6, we see that it is not that much larger and it is still less than 7. Our results

suggest that the six-sigma approach provides a reasonable approximation of actual ex-

ante VaR measure.. In the next section, we apply the six-sigma approach to manage the

risk of various portfolios and compare the performance of the risk-managed portfolios to

that of a risk-free security.

Managing Portfolio Risk with the Six-Sigma Approach

We focus now on illustrating how to use the six-sigma approach to manage the risk of

these risky portfolios: value-weighted, equally-weighted, S&P500, and Decile 1 to Decile

10. We construct our hypothetical portfolio (C) to be a two asset one: 1) a risk-free asset

(T-Bill) and 2) a risky portfolio (one of the risky portfolios mentioned above). Our target

investor in this combined portfolio (C) is one who wishes, with specified certainty that

his holding will not fall by more than the desired % during his defined target period.

Using the six-sigma approach described in the previous section, a one percent VaR is

defined as 𝜇𝑐 − 2.33 × 6 × 𝜎𝑐.

In our two asset portfolio construction, let 𝜇𝑓, 𝜇𝑐 and 𝜎𝑐 (𝜇𝑝 𝑎𝑛𝑑 𝜎𝑝) represent the risk-

free rate of return, the expected daily return and standard deviation of the combined

portfolio (risky portfolio) and w be the investment weight in the risky portfolio.

Assuming zero correlation between the riskless and risky portfolios, the expected daily

return and standard deviation of the combined portfolio can be written as:

𝜇𝑐 = 𝑤𝜇𝑝 + (1 − 𝑤)𝜇𝑓

𝜎𝑐 = 𝑤𝜎𝑝

For the combined portfolio to meet a certain VaR requirement; for example to have a (1-

α) probability of suffering a loss no larger than ∅∗(where ∅∗ is a negative value) within a

day, we will need

𝜇𝑐 − 𝜋|𝑍𝛼|𝜎𝑐 ≥ ∅∗

Substituting into this equation the expressions for 𝜇𝑐 and 𝜎𝑐 and focusing on the

boundary case lead to

𝑤𝜇𝑝 + (1 − 𝑤)𝜇𝑓 − 𝜋|𝑍𝛼|𝑤𝜎𝑝 = ∅∗

𝑤(𝜇𝑝 − 𝜇𝑓 − 𝜋|𝑍𝛼|𝜎𝑝) = ∅∗ − 𝜇𝑓

𝑤 =∅∗ − 𝜇𝑓

(𝜇𝑝 − 𝜇𝑓 − 𝜋|𝑍𝛼|𝜎𝑝)

11

To compute 𝑤𝑡 at t, given that we haven’t observed the expected return and standard

deviation at t, we will assume that these values can be forecasted by the estimates for 𝜇𝑝,

𝜇𝑓, and 𝜎𝑝 at (t-1). 𝜋𝑡 is set to 6 in the six-sigma approach and 𝑍𝛼 is equal to 2.33 for a

1% VaR. Since ∅∗ by definition is a negative number:

𝑤𝑡 =∅∗ − 𝜇𝑓𝑡−1

(𝜇𝑝𝑡−1− 𝜇𝑓𝑡−1

− 𝜋𝑡|𝑍𝛼|𝜎𝑝𝑡−1)

The calculations above assume daily returns and the computation of VaR for a 1-day

horizon. For an h-day horizon VaR, the calculation of the weight, 𝑤𝑡, assuming returns

are iid, becomes

𝑤𝑡 =(∅∗ − 𝜇𝑓𝑡−1

) × ℎ

[(𝜇𝑝𝑡−1− 𝜇𝑓𝑡−1

) × ℎ − (√ℎ × 𝜋𝑡)|𝑍𝛼| (𝜎𝑝𝑡−1× √ℎ)]

𝑤𝑡 =∅∗ − 𝜇𝑓𝑡−1

(𝜇𝑝𝑡−1− 𝜇𝑓𝑡−1

− 𝜋𝑡|𝑍𝛼|𝜎𝑝𝑡−1)

which is the same as the 1-day result.

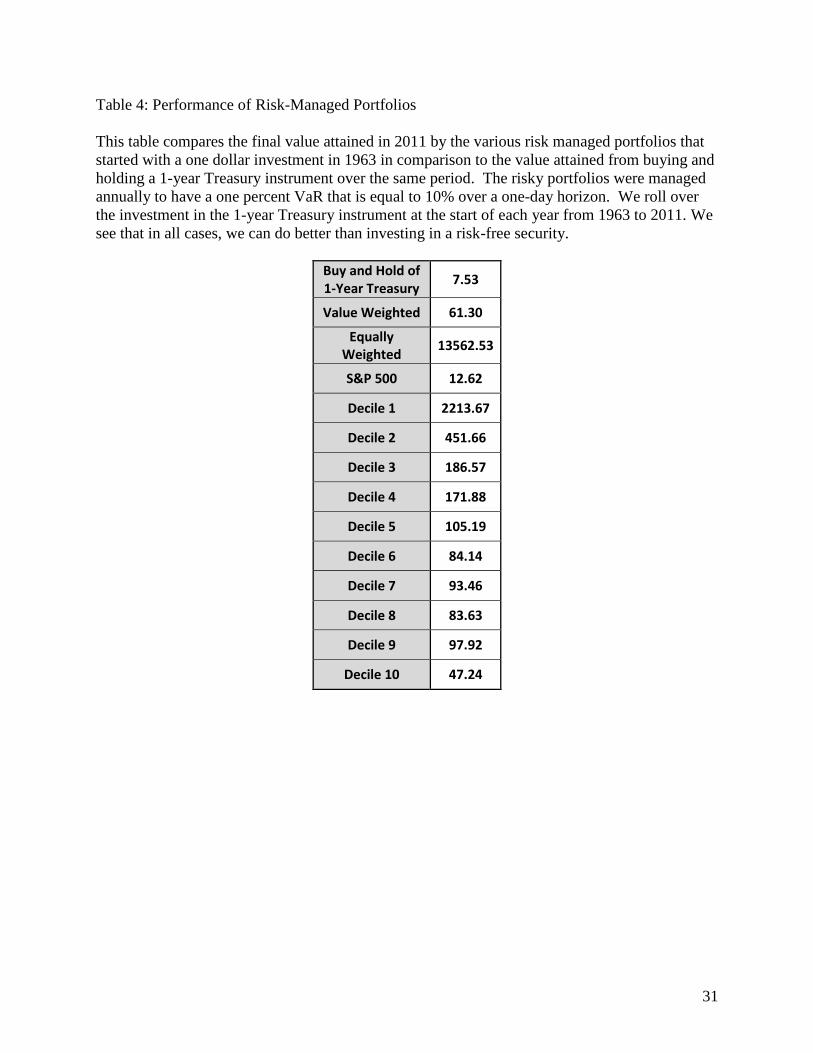

The equation above allows us to determine the weight, 𝑤𝑡, to allocate to the risky

portfolio and the riskless asset (1-𝑤𝑡) so that our combined portfolio will have a 1% VaR

that is equal to ∅∗. In our simulation, the portfolios were rebalanced annually to have a

one percent VaR that is equal to 10% over a one-day horizon. That is, we set ∅∗ to 10%

and we set the weight at the beginning of each year from 1963 to 2011 to the value

derived from the equation for 𝑤𝑡. This means that for each year we are constructing a

portfolio that 99 percent of the time will not lose more than 10% in value in the next day.

Table 4 shows the final value attained in 2011 by the various risk managed portfolios that

started with a one dollar investment in 1963. We see that in all cases, we can do better

than investing in a risk-free security.

(Insert Table 4 here)

Applying a Six Sigma Approach to Portfolio Risk Management

The major goal of a Six Sigma Quality Program is to reduce process variability to

improve product quality and reduce cost. The major goal of portfolio management is to

maximize a return to risk tradeoff. In essence they are the same objective—to get the

best results (return/quality) with the lowest cost (risk/cost). Six Sigma quality programs

emphasize a process approach to improving system reliability and performance. A

process approach stresses the sequencing and interactive effects in a system rather than

compartmentalizing the steps and activities. As was discussed above, the failure of risk

managers to account for systemic risks in investment portfolios contributed to the

12

financial crisis. The most widely used framework is the DMAIC process developed at

General Electric which includes the following steps: Define Measure, Analyze, Improve,

and Control (DMAIC). This same approach is applicable to portfolio design for financial

instruments and risk management systems for these portfolios. In this section we will

discuss how the DMAIC process can be used by financial firms to better design

investment products and control for risk, and, in the subsequent section, create a simple

example to illustrate how the process can work.

The first stage in applying the DMAIC process to portfolio design is to Define the types

of financial products to be considered in terms of the desired return to risk profile, the

types of instruments that can be considered, and the investment horizon. These of course

should be determined by top management of the firm, not by the quant’s developing the

products. Without these parameters clearly defined, financial engineers will not have

clear guidance in terms of the products they should develop. As the recent financial crisis

illustrates, this failure to have clear goals and constraints led to some products being

offered that were not well thought out and introduced a high level of unexpected and

undesired risk. Managers who did not understand the instruments because of complexity

approved these products with disastrous consequences.

The second step in the DMAIC process is to Measure. In a manufacturing process this

would normally involve collecting statistical data and finding process capabilities. Using

statistical control charts is common in industry to measure whether a process is

operationally under control and when it may be deviating from the norm. This can

provide a warning to the production staff that a process is going out of control and

corrections can be made before defects are produced The analogue in financial product

design would be to perform statistical tests and simulations using historical data to

determine the probability distributions of the instruments and markets. SPC might then

be utilized to indicate when these instruments or markets are deviating significantly from

their historical performance. An example of this can be found in the use of statistical

control charts to predict the bubble in the U.S. housing market in the first decade of this

century (Berlemann, et al, 2012).

Another goal is to ascertain how the instruments perform independently and together in a

portfolio. More advanced measurements would attempt to find the systemic effects on

the portfolio of liquidity and credit crises. This was a deficiency in the design of many of

the financial products that imploded in 2007 and 2008 such as CDO’s. A process

capability study determines the distribution of results of a machine or process in terms of

a density function (usually the normal distribution) to see if it can meet design

specifications. For a financial instrument this would involve finding the distribution of

returns over a period. For multiple instruments these can be analyzed with multivariate

regression and simulation studies to determine covariance and interactive effects. This

data will be essential for the next step in the process.

The third stage of the DMAIC process is to Analyze. For financial products this could

involve the technique called Design of Experiments (DOE). This method has been used

in manufacturing for many years to determine interactive effects in processes. As noted

13

above, interactive effects between financial instruments such as varying and asymmetric

correlations were poorly understood and modeled. DOE provides a tool to analyze these

kinds of influences on an investment portfolio. It involves a well-defined set of statistical

techniques to vary several variables simultaneously and see the combined effect on

performance of the process. For financial instruments this could be done by simulation

methods. For example, various asset categories could be combined in a systematic way

in hypothetical portfolios to see how they perform under differing market scenarios.

These interactive effects are a key element in another portion of analysis of portfolios

called stress testing. The systemic effects of disappearing market liquidity and rapidly

changing credit-worthiness on portfolios were poorly modeled in the recent crisis. Stress

testing using DOE and simulations can provide valuable insight into how investment

portfolios will respond under different economic and market scenarios.

Another tool from Six Sigma that may have some at least conceptual significance for

designing financial portfolios is Design Failure Modes Effects Analysis (DFMEA). This

technique is a systematic process of recording and analyzing failure of a product to meet

specifications. The objective is to understand the most frequent causes of failure and

why they occurred. This approach has been very successfully applied in the airline

industry where every crash is carefully analyzed to find the cause, and then modifications

to equipment and/or training are required by regulatory authorities. The result has been

continually improving air flight safety. Applied to portfolio design this would involve

determining why particular instruments did not perform as expected in terms of return

and risk. There is certainly a wealth of data from the last several years to perform this

kind of analysis. It will be critical to the design of better portfolios to understand why so

many failed in the financial crisis. Of special interest will be examining the interactive

and systemic effects in these portfolios. Andrew Lo (2015) has proposed such an

approach to investigating financial “accidents” such as market crashes to improve risk

management and reduce drawdown risk in investment portfolios.

To Improve is the next step in designing financial products by the DMAIC process. Here

a couple of techniques from the Six Sigma tool box can be useful. The first of these is

reliability engineering. Reliability engineering involves designing products to be robust

under difficult operating conditions. This is accomplished through several techniques

including standardization and redundant systems as well as the previously discussed

DOE. Standardization tends to make physical products more robust because of fewer

number of parts reducing complexity and interactive effects and the streamlining of

assembly and testing improving quality and reliability. Applied to financial products the

analogue would be to use established financial instruments that have a track record of

performance under different market conditions rather than new and customized

instruments. It will be difficult to construct a low-risk portfolio with many new and

bespoke instruments where the correlations and interactive effects are unknown.

Redundancy is an essential element in complex products to assure reliability. This can

take the form of parallel systems that backup the primary system in case of failure. In the

case of financial products this could be achieved by the use of financial hedges that will

offset any opposite movement in the underlying instrument. The concept of portfolio

14

insurance is relevant here. There are various ways to achieve this in an investment

portfolio by taking offsetting long and short positions and the use of options. A common

hedge is to take out-of-the-money puts to hedge against a large market drop. For hedging

against counterparty risk, Credit Default Swaps (CDS) can be used. CDS’s contributed

to the recent financial crisis because of the huge volume outstanding and their lack of

transparency. They were undoubtedly being used as a speculative instrument rather than

a hedge by many of the participants, but can be an effective hedge against credit risk if

used properly.

The last stage of the DMAIC process is to Control. Although risk management issues

should be considered throughout all five steps in the process, they are the main focus of

the last stage for financial products. The most important part of the control process is

assigning clear-cut responsibility for this activity. It should be at a high enough level in

the firm to have real control which was a problem with some of the financial firms most

impacted by the recent crisis where control responsibility was diffuse and ineffective.

Control also involves frequent reporting of essential information and separation of the

trading, sales, and reporting roles. Compensation systems should not encourage excessive

risk taking. Beyond these organizational issues portfolios should be continually subject

to stress testing as market and economic conditions change. This calls for individuals

with the requisite analytical skills.

The overall process for designing and controlling financial products following the

DMAIC model will allow for a more systematic and thorough process that has the

potential to prevent some of the problems which surfaced in the recent financial crisis.

The ad hoc and diffuse nature of risk management in many financial firms was revealed

during this crisis, and a more integrated and rational process is clearly called for.

Relevance of Model to DMAIC

The model developed previously is a rather simple one; only two assets, one risk-free, are

utilized, and simplifying assumptions are made regarding volatility. From this starting

point of defining a model, a DMAIC-type process would allow for a better and more

efficient portfolio construction as well as better estimates of volatility. A brief suggestion

of how this process might unfold follows.

We measured the standard deviation of the risky asset as the observed volatility of the

S&P 500 over the prior period of estimation. This choice of using a simple measure of

prior volatility to estimate future volatility is one of convenience and ease of calculation.

Alternate forms of measurement, such as volatility implied by option pricing, could and

should be utilized.

Use of prior volatility is the first stage in the measurement process. The results can then

be analyzed to determine how well it performed and compared to alternative models.

The next step is improving the model. For example, to improve the measure of volatility,

we could test how reliable the estimate is. How well does past volatility predict future

volatility? Here we can design experiments (DOE) to test more reliable predictions of

15

future volatility may be achieved. Processes described elsewhere in the paper suggest

how more accurate measures of volatility might be constructed. The goal is to develop a

model that will estimate prospective volatility with a high degree of accuracy. .Another

improvement might be in designing in redundancy. This may be achieved through a

variety of techniques that we may characterize as portfolio insurance, to be discussed

later in the paper. Other aspects of the model could also be analyzed and improved as

tests are run, alternatives tried, and results compared.

The final stage in the DMAIC process is control which could require a dedicated

portfolio manager to oversee the portfolio and assure compliance with portfolio

requirements. Clearly, different portfolios, depending upon the objectives of its

investors, will require different approaches to risk management. These approached

should be carefully defined, as noted above.

We have indicated a few examples of how the process might yield a more robust method

of portfolio management with an objective of protecting the investor from unacceptable

downturns in the value of their portfolio. We now turn to applying methods of Six Sigma

to portfolio design.

Six Sigma Methods of Robust Portfolio Design

Robustness, or performing well under all market conditions, is certainly a desirable

quality in an investment portfolio and one in which many investment products were

clearly lacking in the recent financial crisis. This is also a major goal of Six Sigma

quality programs which attempt to design robust products and processes. Typically

financial managers may not have thought of robustness as a critical quality in their

products, but many may now begin to do so. Six Sigma provides a conceptual and

methodological approach to do this as the last section indicated. .

The financial crisis that began in 2007 affected many financial firms in commercial and

investment banking, hedge funds, private equity funds, and insurance companies. But

one major category of financial institution escaped the havoc. These are the

derivatives/futures exchanges throughout the world. Not one futures exchange

experienced distress in the crisis (Varma 2009). The reason for this is that derivative

exchanges apply, and have applied for years, over-margining of positions. The margins

that counterparties must maintain with the exchange are very conservative. The primary

approach to establishing margin requirements at most derivative exchanges is the SPAN

(Standard Portfolio Analysis of Risk) developed by the Chicago Mercantile Exchange

(CME) in 1988. SPAN calculates the potential worst-case asset loss based on several

price and volatility scenarios to set the margin. This conservative approach worked well

with the chaos in the global asset and credit markets in the face of a sudden increase in

volatility and correlation breakdowns. It is a financial equivalent of over-engineering.

As was mentioned previously, asymmetrical and non-normal distributions cannot be

modeled adequately using VaR techniques. Attempts have been made to improve upon

16

VaR which have some potential. Coleman (2014) and Chen (2015) suggest using the

Student’s-t to account for fat tails. Goh, et al (2009) recently developed PVaR for

Partitioned Value-at-Risk. Their method divides the asset return distribution into positive

(gains) and negative (losses) half-spaces. This generates better risk-return tradeoffs for

portfolio optimization than the Markowitz model and is useable when asset return

distributions are skewed or abnormal. Other adaptations of VaR methods include BVAR

which incorporates stochastic volatility and fat-tailed disturbances (Chiu, et al, 2015),

EVAR for Extended Value at Risk by Chaudhury (2011), WVaR for Worst-Case VaR (El

Ghaoui, et al, 2003), and AR-VaR for Asymmetry-Robust VaR (Natarajan, et al, 2008).

All of these methods deal with some of the weaknesses of the basic VaR approach but

present computational difficulties and do not deal with non-stationarity due to

interdependencies and systemic effects completely.

There are various approaches to stress testing of a portfolio involving VaR or

simulations. Basu (2009) compares different stress tests on the foreign exchange (FX)

market. He postulates that a good stress test has several characteristics. First,

hypothetical scenarios must be combined with historical data to capture the impact of

severe shocks that have not yet occurred. Second, the tests should be probabilistic to be

interpreted as a refinement of VaR techniques. The third requirement is that they be

simple enough to communicate to top management. Using these criteria he concludes

that VWHS or Volatility Weighted Historical Simulation (Hull and White 1998)

performs the best in terms of smooth changes in the risk estimates as the size of the shock

varies. VWHS dynamically adjusts volatility rather than using historic volatility in the

simulations resulting in a more current scenario analysis. It also better models the impact

of stress on short positions and captures volatility clustering and fat tails in a simple

framework.

Diversification across asset categories and countries can provide some degree of risk

mitigation in a portfolio, but this can break down as markets become more correlated in

times of market stress. Building portfolios to maximize returns and minimize volatility

using historical data and sophisticated models is essential in portfolio design. But to be

truly robust, the portfolio must be designed to have offsetting long and short positions.

This can be accomplished through several hedging methods that provide portfolio

insurance.

There are several persuasive reasons to insure an investment portfolio against large and

unexpected losses. The most obvious is the revealed weaknesses of VaR models to

protect against large losses. The flaws in the VaR models were discussed above and

include non-normal distributions with fat-tails and skewness and non-stationarity. This

leads to poor performance of these models, particularly in the short-run (Considine 2008).

The short-run orientation of financial markets has been attributed to “reputational

concerns” of investment managers who are more concerned with retaining funds in the

near term than in long run out-performance of the market (Malliaris and Yan 2009).

“Herding effects” contribute to this phenomenon as well they say.

17

Portfolio insurance methods include the use of offsetting long and short positions for

price and market risk. These positions can be costly in terms of return that is sacrificed to

reduce risk. Another hedging method is to use options. Far out-of-the-money options

can be used to insure against extreme price moves at a modest cost of the premium which

is low for such options. To reduce the premium cost further one can write an offsetting

option but, of course, must assume some risk to do so. Simulations by Goldberg, et al,

(2009) find that out-of-the-money put options reduce ES and coincident extreme losses.

To insure against counterparty risk, one instrument that can be used is the Credit Default

Swap (CDS). For a series of premium payments counterparty risk can be transferred to

someone else. This of course assumes that the CDS counterparty does not themselves

default which has turned out to be a problem in the recent credit crisis. Other methods of

portfolio insurance will probably be developed in reaction to recent events allowing for

further refinement of reliability engineering for investment portfolios.

Conclusions

Financial markets have dramatically changed in the last three decades due to a confluence

of factors making them more volatile and less predictable. These forces include

increasing integration and globalization of the equity, bond, foreign exchange, and

commodity markets resulting in greater correlation between markets and assets and much

faster and extreme contagion between them. Secularization and financial engineering

have produced more complicated financial instruments which are difficult to model,

especially under conditions of market volatility and contagion. Automated trading has

greatly increased the speed at which volatility spreads through the markets. These forces

make financial markets much more difficult to model and forecast. The need for a

“safety margin” in portfolio design to prevent extreme drawdowns has become clear after

the recent financial crises. Earlier in the paper our descriptive model demonstrates that a

Six Sigma type framework, using a multiplier, provides a reasonably accurate description

of how an “adjusted” VaR may be created that reflects actual ex-ante risk. Six Sigma

principles, which have proven themselves adept at preventing unwanted variance in many

processes in manufacturing and services, suggest an approach to portfolio design and risk

management than can deal with the uncertainty and unpredictability of modern financial

markets and provide a margin of safety for investors. How these principles can be

applied to robust portfolio design have been discussed in this paper.

Fractal models can mimic what happens in market crises (Mandelbrot and Hudson 2004)

They are able to represent graphically “wild randomness” after the fact but are not useful

for prediction (Considine 2008). By definition Black Swan events are unpredictable and

thus cannot be mathematically modeled (Taleb 2007). We are in the realm of Knightian

uncertainty, rather than risk, here and traditional risk management approaches cannot

prevent large losses during periods of market turmoil. Since these events can have

devastating effects on an investment portfolio, how can an investor or a firm prepare for

them? There is no way to completely prepare for an unpredictable event but one can

certainly mitigate its effects. In an investment portfolio this can be accomplished through

the Six Sigma methods outlined in this paper.

18

The Six Sigma process can be applied to the design of risk management systems. It

provides a structured approach to collect data, analyze it, and develop financial products

with an integrative plan-achieve-control structure as part of the process. The DMAIC

process outlined in this paper is one way to accomplish this. Three key concepts of Six

Sigma quality programs have direct applicability to design of investment portfolios.

These are the principles of over-engineering, robust design, and reliability engineering.

Over-engineering of a financial product involves combining different instruments that

provide a return-risk tradeoff that mitigates extreme tail events. If well done, the result is

a robust design for the portfolio that will be able to respond in predictable ways to both

expected and unexpected market shocks and survive Black Swan events. Reliability

engineering provides an extra layer of protection using portfolio insurance methods to

hedge for extreme events using options, Credit Default Swaps, and other instruments and

requires stress testing and simulation to build in reliability and robustness.

Complicating design of financial instruments are behavioral factors such as the “Persaud

Paradox” where a false sense of confidence arises because peers are all using the same

approach, such as VaR models (Persaud 2003). Overcoming this is a responsibility of

risk management, and a structured approach as suggested in this paper can help in that

regard. Other behavioral issues such as herding and overconfidence also contribute to the

inadequacy of risk models and risk management (Rizzi 2009). Greenbaum (2014) and Lo

(2015) offer some suggestions for risk management practices to overcome these cognitive

biases. Much more research needs to be done to incorporate behavioral factors into risk

modeling. The difficulty of doing this is another argument to over-engineer financial

portfolios to make them robust to unpredictable behavioral phenomenon in financial

markets.

References

Arditti, Fred D. 1967, “Risk and the required return on equity”, Journal of Finance,

22, 19-36.

Basu, Sanjay, 2009, “Stress testing for Market Risk: A comparison of VaR Methods”,

Available at http://ssrn.com/abstract=1370965

Berlemann, M., J. Freese, and S. Knoth, 2012, “Eyes Wide Shut? The U.S. House

Market Bubble through the Lense of Statistical Process Control”, CESIFO

Working Paper 3962. Available at http://ssrn.com/abstract=2165772

Black, F. and M. Scholes, 1973, “The Pricing of Options and Corporate Liabilities”,

Journal of Political Economy, 81(3), 637-654

Boucher, C., P. Kouontchou, and B. Maillet, 2011, “An Economic Evaluation of the

Model Risk for Risk Models”, Available at http://ssrn.com/abstract=1943605

Chaudhury, Mo, 2011, “Extended Value at Risk Measure (EVAR) for Market Risk”

McGill University Desautels Faculty of Management Working Paper, Available at

http://ssrn.com/abstract=1809801

19

Chen, James M., 2015, “The Promise and the Peril of Parametric Value-at-Risk (VaR)

Analysis”, Social Science Research Network (SSRN), available at

http://ssrn.com/abstract=2615664

Chiu, Ching-Wai, Mumtaz, Haroon, and Gabor, Pinter, 2015, “Forecasting with VAR

Models: fat tails and stochastic volatility”, Bank of England Working Paper No.

528, Available at http://ssrn.com/abstract=2612030

Coleman, Thomas, 2014, “Financial Risk Measurement and Joint Extreme Events: The

Normal, Student-t, and Mixture of Normals”, University of Chicago Working

Paper, Available at http://ssrn.com/abstract=2437672

Considine, Geoff, 2008, “Black Swans, Portfolio Theory and Market Timing:

12 comments”, Seeking Alpha, Article 64111, Available at http://seeking

alpha.com/article/64111

El Ghaoui, L., M. Oks, F. Oustry, 2003, “Worst-case Value-at-Risk and Robust

Portfolio Optimization: A Conic Programming Approach”, Operations Research,

51(4), 543-556

Escanciano, J.C. and P. Pei, 2012, “Pitfalls in Backtesting Historical Simulation VaR

Models”, Center of Applied Economics and Policy Research Working Paper,

Indiana University, Available at http://ssrn.com/abstract=2026537

Fama, Eugene, 1965, “The Behavior of Stock Prices”, Journal of Business, 47, 244-280