Post Signing Market Check or Window Dressing? The Role of Go-Shop Provisions in M&A Transactions 1. Introduction By the time of a takeover deal agreement, an acquirer has devoted a significant amount of time, efforts and money to identifying a target firm and assessing the target’s value. In the event that the deal is not completed, the acquirer is suffering a decrease of its stock price, being viewed as weak in the M&A market, and losing their reputation. Because of these potential costs, an acquirer frequently asks a target to provide a device for deal protection to protect the deal. Such deal protections includes the lockup, termination fee, confidentiality agreement, force to vote, and no shop provisions. 1 A no-shop provision which has been commonly included in the takeover agreements for decades restricts target managers from actively soliciting third party bids after signing the deal agreement, which reduces the possibility of termination of the initial agreement (Balz, 2003; Burgess, 2001). Hotchkiss, Qian, and Song (2005) report that more than 98% percent of deals, either implicitly or explicitly, include no-shop provisions, making it difficult to examine the role of no-shops due to the lack of variation across deals. Since 2005, however, the use of go-shop clauses has gained prominence in takeover deals. In particular, the use of go-shops becomes more common during the 2005-2007 private equity LBO (Leveraged Buyout) boom (Subramanian, 2008; Morrel, 2008). Contrary to no-shops, go- shops allow a target to actively solicit and negotiate with other potential third parties for a limited period of time after signing a takeover agreement. If a target receives a superior proposal from a third party, go-shops allow a target to terminate the initial takeover agreement after paying a relatively low termination fee. One example of a takeover deal including a go-shop provision is 1 Several papers document examine the role of deal protection devices. Coates and Subramanian (2000) and Burch(2001) examine the lockup and Officer(2003), Bates and Lemmon(2003), and Boone and Mulherin (2007) study the termination fee provisions.

Transcript

Post Signing Market Check or Window Dressing? The Role of Go-Shop Provisions in M&A Transactions

1. Introduction

By the time of a takeover deal agreement, an acquirer has devoted a significant amount of

time, efforts and money to identifying a target firm and assessing the target’s value. In the event

that the deal is not completed, the acquirer is suffering a decrease of its stock price, being viewed

as weak in the M&A market, and losing their reputation. Because of these potential costs, an

acquirer frequently asks a target to provide a device for deal protection to protect the deal. Such

deal protections includes the lockup, termination fee, confidentiality agreement, force to vote, and

no shop provisions.1

A no-shop provision which has been commonly included in the takeover agreements for

decades restricts target managers from actively soliciting third party bids after signing the deal

agreement, which reduces the possibility of termination of the initial agreement (Balz, 2003;

Burgess, 2001). Hotchkiss, Qian, and Song (2005) report that more than 98% percent of deals,

either implicitly or explicitly, include no-shop provisions, making it difficult to examine the role

of no-shops due to the lack of variation across deals.

Since 2005, however, the use of go-shop clauses has gained prominence in takeover deals.

In particular, the use of go-shops becomes more common during the 2005-2007 private equity

shops allow a target to actively solicit and negotiate with other potential third parties for a limited

period of time after signing a takeover agreement. If a target receives a superior proposal from a

third party, go-shops allow a target to terminate the initial takeover agreement after paying a

relatively low termination fee. One example of a takeover deal including a go-shop provision is 1 Several papers document examine the role of deal protection devices. Coates and Subramanian (2000) and Burch(2001) examine the lockup and Officer(2003), Bates and Lemmon(2003), and Boone and Mulherin (2007) study the termination fee provisions.

1

found in the deal where Maytag agreed to be sold at $14 per share ($1.125 billion in total) to

Ripplewood Holdings on May 2005. After the deal agreement, Maytag canvassed more than 100

potential bids during the go-shop period and, on August 2005, accepted a competing bid from

Whirlpool Corp. which offered $1.7 billion. Maytag paid $40 million of the termination fee (or

about 3.5% of deal value) to Ripplewood.

While the case of Maytag is considered as an exemplary practice for the use of go-shops,

it has been debated whether go-shop deals are beneficial or detrimental to target shareholders..

The important question is whether the inclusion of go-shops in deal agreements reflects target

mangers’ efforts to fulfill their Revlon duties by achieving the best price for their shareholders or

just reflects target board’s “window dressing” to survive judicial scrutiny. 2 As stated in the New

York Times article, “..But in practice, it may be more a disingenuous article that boards are

including in deals to protect themselves from angry shareholders who may think that a transaction

was a sweetheart deal to a favored bidder….“We made this deal, but we’re still open to higher

bids.” The buyer effectively acts as a stalking horse…”.3

While several studies (e.g, Bloch, 2010; Morrel, 2008 ; Sautter, 2008) deal with the legal

issues concerning the efficacy of the go-shop provision, Subramanian (2008) is the first study that

empirically examines the go-shop provisions in takeover agreements. He finds that the go-shop

provision has emerged as an important device as a deal-making technique after 2005, a period

characterized as the private equity boom. According to his study, go-shops can be either add-on,

following a traditional solicitation of bids, or pure in which there is no pre-signing canvass of the

markets and that follows an exclusive negotiation with a single bidder. He also provides empirical

evidence that the deals including pure go-shops yield approximately 5% higher announcement

returns than traditional the deals with no-shops. The results support a notion that go-shop

2 When it is clear that a target will be acquired, Revlon duty requires the target managers to run a fair auction to maximize target shareholders’ wealth (Revlon v. MacAndrew, 506 A2d 173, Del. 1986). 3 See “Looking for More Money, After Reaching a Deal”, the New York Times, March 26,2006.

2

provisions allow target managers to fulfill Revlon’s requirement. Although Subramanian (2008)

makes important contribution to furthering our understanding of the role of go-shop provisions,

little has been studied on how a go-shop provision and the length of go-shops affect takeover deal

performance and target shareholders’ welfare.

This paper supplements Subramanian (2008) by providing additional analysis for the go-

shop provision, deal performance, and target shareholders’ wealth. Specifically, we ask the

following questions: Do go-shops really allow targets to receive more competing bids during the

interval periods? Are the takeover deals including go-shops less likely to be consummated with

the initial bidder? Does the length of go-shop periods matter for deal performance? Finally, are

go-shops beneficial to target shareholders? The study investigates these questions using a sample

of 1,254 takeover deals from 2004 through 2008. We find that 95 deals include the go-shop

provisions during the sample period and the average go-shop period is 52 days.

To address the questions above, we examine the effect of the use of go-shops on target

shareholders’ wealth, measured by deal premiums, the probability of receiving competing bids,

and the probability of deal completion. We also look at whether the length of go-shop periods

affects our measures for target shareholders’ wealth. The empirical models include the multiple

regressions as well as instrumental variable regressions which control for possible endogeneity of

the inclusion of go-shops. Our findings generally support the proposition that go-shops reflect

target managers’ effort to fulfill the Revlon duties, consistent with Subramanian (2008). We find,

however, that the length of go-shop periods does not have significant effects on shareholder

welfare.

First, we look at the relationship between deal premiums and a go-shop provision. The

results show that deals including go-shops tend to have a greater, never less, premium than

typical no-shop transactions, suggesting that once initial bidder agree to include a go-shop clause,

she tends to offer the higher premium in order to avoid the possibility that the deal is jumped by

competing bidders. The length of go-shops, however, does not affect a deal premium. Second, we

3

examine the probability of receiving competing bids during the interval period and go-shops. We

find that by allowing managers to actively solicit the competing offers deals including go-shops

are more likely to receive competing bids. The result does not support the, so called, “window

dressing” hypothesis that target managers who intend to sell the company to the initial bidder put

go-shops to survive judicial scrutiny. Again, there is no evidence that the longer go-shops tend to

invite more competing offers. Finally, we examine the probability of deal consummation and go-

shops. The data show that both the inclusion of go-shops and the length of go-shops significantly

reduce the probability of deal completion. However, go-shops and the length of go-shops are not

significantly correlated with the completion of high-premium deals. That is, once an initial deal

has a high premium, the likelihood of deal termination is not affected by, or does not decrease in,

the inclusion of a go-shop provision.

In sum, this study provides decisive evidence in favor of a go-shop provision by showing

that the inclusion of go-shops improve deal performance and target shareholders’ welfare. The

remainder of this paper is organized as follows. Section 2 details the sample selection process,

describes test variables and presents the descriptive statistics. In Section 3, we perform regression

analysis for target shareholders’ wealth, and Section 4 concludes.

2. Data, Variable Description, and Sample Statistics

A. Data

The sample contains all mergers and acquisitions, obtained from the Securities Data

Corporation (SDC) Platinum Mergers and Acquisitions database, announced between 2004 and

2008, a period characterized by emergence of go-shop provisions. We construct the sample using

the following criteria:

1) Deal value is publicly disclosed and is greater than $1 million,

4

2) Toehold, the percentage of shares held by a bidder at the announcement date is less

than 50%,

3) Stock prices are available in the Center for Research in Securities Prices (CRSP),

4) Financial data are available in Compustat.

We initially obtain information on go-shop information from the SDC and check the data

by reviewing SEC filings 4. The sample restrictions result in a final sample of 1,254 takeover

deals. Of these, a go-shop provision appears in 95 deals (7.58%) of which 75 deals are completed

and 20 deals are withdrawn.

B. Variable Description

B.1. Key Variables : Go-shops and Deal performance

We use a dummy variable, Go-Shop, which equals one if a go-shop provision is included

in the deal contract and 0, otherwise. Go-shop information is obtained from both the SDC

database and SEC filings. For the length of go-shop periods, Go-Shop Days, we count the number

of days when go-shops are allowed. We use three measures for deal performance and target

shareholders’ wealth. Deal premium is defined as a bidder's offer value over the pre-offer market

value of a target minus one. Following Officer (2003), we measure the offer value two methods:

the aggregate value of cash, common stocks, convertible bonds, and preferred stocks paid to

target shareholders or the share price paid to target shareholders as reported by SDC. The second

measure for deal performance is deal competition, a dummy variable which takes the value of one

if a target receives any competing bids during the interval period. The last measure for deal

performance is deal completion, the probability that a takeover deal, especially a deal with a high

premium, is successfully consummated. A deal has a higher premium if its premium is greater

than the industry (1-digit SIC code) median for deal in the same calendar year.

4 Boone and Mulherin (2007) reports that the SDC incompletely reports the incidence of termination fee provisions during the 1989-1999 period. However, after reviewing SEC filings, I do not find any evidence that the SDC under-reports go-shop provisions for the 2004 to 2008 period.

5

B.2. Deal Characteristics Variables

We use several variables to control for the effects of deal characteristics on deal

performance. Tfee Size is termination fees as a percentage of deal value. Coates and Subramanian

(2000) argue that an acquirer tends to pays for termination fees with greater deal premiums.

Officer (2003) reports a negative correlation between termination fees and the likelihood of

competing bids, while Boone and Mulherin (2007) find the opposite results using their new

measure for competition where they consider competition before the publicly announced bid.

Voting Agreement is a dummy variable equal to one if a target provides a voting

agreement clause in the deal agreement. Long-term Affiliation is a dummy equal to one if a target

and bidder have a parent-subsidiary relationship. According to Boone and Mulherin (2007),

voting agreement clauses and long-term ownership affiliation can be substitutes for termination

fees. Toehold is a dummy variable which takes a value of one if the fraction of target shares held

by the bidder is greater than 5%. Toehold represents short-term ownership affiliation between

targets and bidders. Hotchkiss, et al. (2005) suggest that the toehold substitutes for other deal

protection devices by reducing the hold-up problem by targets.

Cash Deal is a dummy variable equal to one if a deal involves a payment of cash to target

shareholders. Since the establishment of “Revlon duties” by Delaware courts in 1980s, target

management considering a cash offer has been cast into something like the role of auctioneers,

with the responsibility to obtain the largest deal premium (Coates and Subramanian, 2000).

Managers considering stock or stock and cash mixed deals are held to a looser standard. That is,

they are not required to maximize immediate shareholder value provided they have a plan for

maximizing value over a longer period.

LBO is a dummy variable equal to one if the takeover transaction is classified as a

leveraged buyout (LBO) by SDC. Since the use of go-shop clauses has gained prominence during

the 2005-2007 LBO boom, we control for the effect of LBOs on deal performance. Related is a

6

dummy equal to 1 if a bidder and target share the same primary 2-digit SIC code and 0 otherwise.

Hostile is a dummy equal to 1 if deal attitude is "hostile" and zero if "friendly" or "unsolicited" as

classified by SDC.

B.3. Target Characteristics Variables

We also attempt to control for the effects of the characteristics of target companies on

deal performance. Ln(Market Cap) is the natural logarithm of common shares outstanding

multiplied by share price of target companies. Market to Book is calculated as (total assets –

book value of equity + market value of equity) / total assets, where, book value of equity is

measured as total assets – total liabilities – preferred stock + deferred taxes + convertible debt.

Leverage is defined as total liabilities divided by total assets.

B.4. Instrumental Variables

In order to account for endogeneity of the inclusion of go-shops and the length of go-

shop period, we introduce two instrumental variables for each endogenous variables. Average

target Industry % Go-shops(or length of Go-shops) is the target industry-average (based on the 1-

digit acquirer SIC code) proportion of go-shop deals (or the number of days of the go-shop

period). Average quarter % Go-shops (or length of Go-shops) is the average proportion of go-

shop deals (or the number of go-shop days) during the quarter prior to the deal agreement. Over

These two instruments are highly correlated with the probability of go-shop inclusion and with

the length of go-shops, respectively, while they are not significantly with performance of

individual deals (not reported.). This confirms that we are free of weal instrumental problems.5

C. Sample Statistics

[Table 1 about here]

5 A full description of this analysis and the results are available on request.

7

Panel A of Table 1 describes the sample distribution of a go-shop provision in merger

and acquisition agreements. 7.58% (95 deals) of total observations include go-shop clauses during

the sample period. Among these, 75 deals are successfully consumed, while 20 deals were

withdrawn. The table also reports that the average number of days for target go-shops is about 52

days and its median is 41days. Panel B presents the characteristics of go-shop deals. Of 95 deals

including go-shops, 33 deals are leverage buyouts (LBO). 59 deals include a termination fee

provision as well and the average fee rate as a percentage of deal value is 2.6%. This figure is

relatively lower than one reported in previous studies. For example, Officer (2003) shows the

mean and median of termination fees are 3.80 % and 3.27 %, respectively, while Jeon and Ligon

(2010) report 3.407% and 3.25%. Termination fees in go-shops deals are relatively lower because

termination fees are often bifurcated with a lower fee during the go-shop period and a higher fee

after its expiration (Subramanian, 2008).

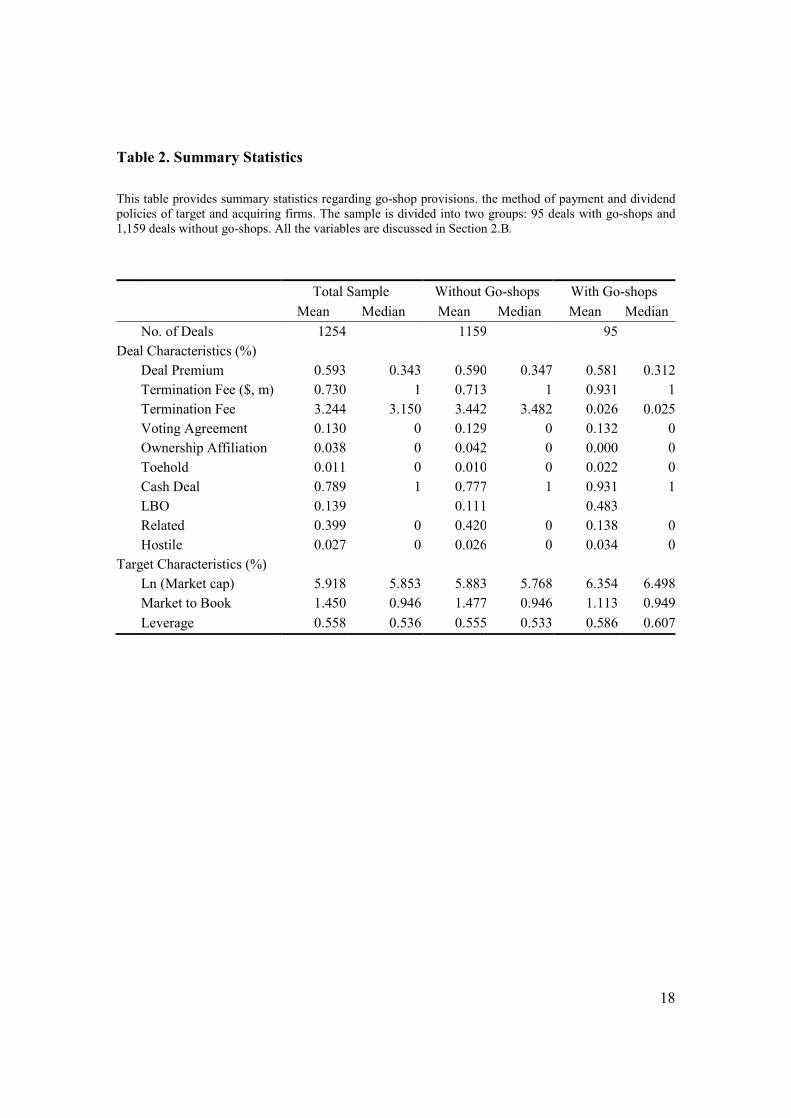

[Table 2 about here]

Table 2 presents descriptive. The deal premium of the sample takeover transactions is, on

average, 59.3%, while it is 58.1% for the deals including go-shops. About 71% of the deals

without go-shops include termination fees of which the size is, on average, 3.44% as a percentage

of deal value. However, about 93% of deals which includes go-shops also include termination

fees and the average of fee size is 2.57%. The percentage of including voting agreements is about

12.9% for non go-shop deals and 13.1% for go-shop deals. In 4.1% of non go-shops deals,

bidders and targets are affiliated through a parent-subsidiary relationship, while there is no case

of affiliation in go-shop deals. However, the frequency of Toehold, which refers to a short-term

relationship between targets and acquirers, is higher for go-shop deals, 2.2% than non go-shop

deals, 0.99%. Target firm size, defined as the natural logarithm of market capitalization of target

companies, and leverage is relatively higher for targets in go-shop deals, while the market book

ratio is higher for targets in deals without go-shops.

8

3. Effects of Go-Shops on Target Shareholders’ Wealth

In this section, we investigate whether the inclusion of go-shops is beneficial or

detrimental to target shareholders’ welfare. We also examine the effect of the length of go-shop

periods. Specifically, we study how the deals including go-shops, or the length of go-shops affect

deal premiums, the probability of receiving competing bids, and the probability that high-

premium deals are successfully consummated.

A. Univariate Tests

[Table 3 around here]

Panel A in Table 3 presents the results of univariate tests on go-shops and our measures

for target shareholders’ wealth. Deal premiums are higher for non go-shop deals, 59%, than go-

shop deals, 58.1%, but the difference is not statistically significant. The probability of receiving

competing bids during the interval period is greater for go-shop deals, 15.3%, than non go-shop

deals, 9.2% and the different is significant at the 5% level. Given that deal premiums provided by

competing bidders are usually higher than initial bidders or, at least, targets have an opportunity

to compare the premiums, target shareholders would be better off with more competing bids. The

probability of deal completion is greater for non go-shop deals, 85%, than go-shop deals, 79%.

However, there is no statistical difference in the probability of completion of high-premium deals

between deals with and without go-shops.

Panel B presents the univariate tests on the length of go-shop periods on target

shareholders’ wealth. In this test, we divided our go-shop sample into two groups, Short and Long.

The deals with go-shop belong to the Short group if their go-shop periods are shorter than the

sample median, while the others belong to the Long group. The results show that deal premiums

9

are, in fact, greater for Short go-shops, 60.1%, than Long go-shops, 56.1%, while the difference is

not statistically significant. The results show that the probability of competing bids is greater for

deals included in the Short group, 13.8%, than the Longs group, 0.069, which suggests that, in

fact, the length of go-shop periods adversely affects the probability of receiving competing bids.

The probabilities of deal completion are significantly higher for deals including short go-shops.

However, the probabilities that high premium deals are consummated are not statistically

different between go-shop and non go-shop deals. Even though Table 3 provides important

evidence on the role of a go-shop provision, it is nevertheless simple unvariate tests. To pin down

the effect of go-shops on deal performance and target shareholders’ welfare, one needs regression

analysis to control for factors that also affect the deal performance, which we do in the next

section.

B. Effects on Deal Premiums

This section examines whether agreements with go-shops, or the length of go-shop

periods, increases deal premiums. We hypothesize that inclusion of go-shops, or the length of go-

shop periods, will be positively correlated with deal premiums, if this post-market check permits

target managers to fulfill the Revlon duties by achieving the best price for their shareholders.

We conduct OLS regressions as a base line-model to examine the effect of the presence

of go-shop provisions, or the length of go-shop periods, on deal premiums. We then estimate

instrumental variable regressions allowing the inclusion of go-shop provisions or the choice of

go-shop length to be endogenously determined. That is, there would be common factors that

would affect deal premiums and go-shop provisions simultaneously. Specifically, the following

treatment effects model is estimated, using the maximum likelihood estimator (MLE):

1st step: yi = 1[γ xi+σ zi + vi >0] (1)

10

2nd step: Deal Premiumsi = β xi+δ yi +c il + ui

where yi=1 if a go-shop provision is included in the takeover deal, z is a set of instrumental

variables for y , and il is the inverse of Mill’s ratio estimated in the first step. 6

The length of go-shop periods would be determined in the endogenous way, too.

Assuming the number of days of go-shops is a continuous variable, we estimate the following 2

stage least squared (2SLS) model.

1st step: yi= γ xi+σ zi + vi (2)

2nd step: Deal Premiumsi = β xi+δ iy + ui

Where iy is the predicted go-shop days obtained from the first regression and z is a set of

instrumental variables.

[Table 4 around here]

Table 3 reports the regression results. Panel A in Table 3 shows that the presence of go-

shop provisions is positively and significantly correlated with deal premiums. Deal premiums are,

on average, 2.4% (OLS) or 4.8% (treatment effects model) higher for a deal including a go-shop

provisions. Go-shop deals are beneficial to target shareholders who enjoy a greater premium and,

therefore, the result is consistent with a notion that go-shops permits target boards to fulfill their

Revlon duties by achieving the best price for target shareholders. Panel B, however, shows that

the number of go-shop days does not significantly affect deal premiums. In the OLS regression,

the coefficient for Goshopdays is negative but not significant. In the treatment effects model, the

coefficient is positive but, again, not significant. Therefore, even though inclusion of go-shop

provisions leads a greater deal premium, the length of go-shop periods does not matter to increase

target shareholders’ wealth.

6 Instrumental variables are described in Section 2.B.

11

For each estimation reported in Table 3, several control variables are significantly

correlated with deal premiums. The negative effects of Toehold and Related suggest that deal

premiums are, on average, lower when targets are affiliated with bidders prior to the deal

agreements. Lower premiums for LBOs support that LBO bidders usually underpay via earnings

management. Perry and Williams (1994) document that target managers, often as a part of

bidding groups, understates reported earning or earnings forecasts prior to the LBO deal in order

to depress the stock price. Deal premiums are higher for the hostile deals and for the targets with

growth potentials, while target size (Lnmcap) has a negative effect on deal premiums.

C. Effects on Post-Bid Competition

In this section, we examine whether agreement with go-shops or the length of go-shop

periods is associated with increase in the probability that a target receives competing bids during

the interval period. If the use of go-shop provisions reflects target managers efforts on fulfilling

the Revlon by performing post-signing market checks, we expect the positive correlation between

go-shops and post-bid competition. On the other hand, go-ships might permit target management

to justify uninformed decisions and to accept inadequate initial bids that go unchallenged by any

meaningful auction. If this is the case, go-shops would not be directly associated with deal

completion.

[Table 5 around here]

Panel A in Table 5 shows the results of the logit regressions on the determinants of post-

bid competition. The dependent variable is a dummy which equals 1 if a target receives any

competing bid after the initial deal agreement. The coefficient of Go-Shops is positive and

statistically significant, representing that a target including go-shop provisions is more likely to

receive the competing bid during the interval period. Since the coefficient in the logit regression

is not equivalent to the marginal effect, we calculate the marginal effects at the mean value of

12

each variable in the third column. We find that, by including go-shop provisions, there is about 12%

more probability for targets to receive a bid from third parties during the interval period. We find

that by allowing managers to actively solicit the competing offers deals including go-shops are

more likely to receive competing bids. The result is consistent with a notion that target managers

actively solicit the third parties and fulfill their Revlon duties by accepting the go-shop provisions.

The evidence does not support the, so called, “window dressing” hypothesis that target managers

who intend to sell the company to the initial bidder put go-shops to survive judicial scrutiny.

Table B reports the regression results where the length of go-shop provisions is used as an

independent variable. The coefficient of Go-Shop Days is negative but not statistically significant.

In sum, by agreeing with the go-shop provision targets tend to have a greater chance to receive a

competing bid, which is beneficial to target shareholders. The decision on the length of go-shop

periods, however, does not significantly affect post-bid competition.

When a target provides a greater termination fee, the probability to receive competing

bids would decrease because the cost of acquisitions for third parties who must pay the fee if

successful increases.7 We find that targets are less likely to receive competing bids if they have a

parent-subsidiary relationship with acquirers or if they belong to the same industry as acquirers.

D. Effects on Deal Completion

It is plausible that a takeover deal which includes go-shop provisions is less likely to be

successful, if target managers actually attempt to fulfill the Revlon duties by actively searching

for a better bid during the go-shop provisions. Previous literature argues that a higher deal success

rate is mainly due to an acquirer’s substantial efforts and investments during the deal process and,

therefore, is positively correlated with target shareholders welfare (Officer, 2003; Bates and

7 Note, Officer (2003) reports weak evidence that the inclusion of termination fee provisions reduce post-bid competition. Boone and Mulherin (2007), however, find a position correlation between agreement of termination fees and pre-bid competition by measuring competition differently. In this study, we use the rate of termination fees rather than employing a discrete variable for the presence of termination fees.

13

Lemmon, 2003). However, we point out that a high success rate might not be directly related to

shareholders’ wealth, if deals with low premiums are consummated. In this section, we revisit the

relationship between go-shops and deal completion, especially when deals have higher premiums,

because the greater successful rate for the deals with high premiums is definitely beneficial to

target shareholders.

[Table 6 around here]

Table 6 reports the results of the determinants of deal completion, focusing on the deals

with greater premiums. Panel A examines whether go-shops increase the probability of deal

success. The coefficient of Go-Shop is negative and statically significant at the 10% level with

the marginal effect of -5.1%, suggesting that a deal including go-shop provisions is less likely to

be successful. This supports that go-shops effectively work as post-bid market checks. Also, the

go-shop period has a significant and negative effect on deal completion. That is, with longer go-

shop periods a target has a better chance to receive a better bid. As discussed above, however, the

higher rate of deal completion might not be directly related to shareholders welfare. Therefore,

we additionally examine whether go-shops increases the deal completion when a deal has a

higher premium.

Panel B presents the results of the determinants of completion of high-premium deals.

The dependent variable of this logit regression is a dummy equal to 1 if a deal with a high

premium is successfully consummated and 0, otherwise. A deal has high premium if its premium

is greater than the industry (1-digit SIC code) median premium for deals in the same calendar

year. The coefficient of Go-shop is positive but not statistically significant. The result suggest that,

even if agreement of go-shops tends to decrease the probability of deal success as shown in Panel

A, it does not has a negative effect on the probability that a high-premium deal is successful.

Therefore, the inclusion of go-shop provisions is not, at least, detrimental to shareholder welfare.

The coefficient of Go-shop Days is negative but, again, statistically not significant, suggesting

14

that the length of go-shop periods has not a significant effect on the completion of high-premium

deals.

In sum, our results show that the inclusion of go-shop provisions is positively correlated

with deal premiums and the probability of receiving competing bids, but is not negatively

correlated with the completion of high-premium deals. The results are consistent with a notion

that agreements with go-shop provisions reflect target managers’ efforts on fulfilling the Revlon

duties

4. Conclusion

This study examines whether the inclusion of go-shops in deal agreements reflects target

mangers’ efforts to fulfill their Revlon duties by achieving the best price for their shareholders or

just reflects target board’s “window dressing” to survive judicial scrutiny.

We supplement Subramanian (2008) by providing additional analysis for the go-shop

provision, deal performance, and target shareholders’ wealth. Specifically, we ask the following

questions: Do go-shops really allow targets to receive more competing bids during the interval

periods? Are the takeover deals including go-shops less likely to be consummated with the initial

bidder? Does the length of go-shop periods matter for deal performance? Finally, are go-shops

beneficial to target shareholders?

We find that 95 deals out of 1,254 deals from 2004 to 2008 include the go-shop

provisions and the average go-shop period is 52 days. To address the questions above, we

examine the effect of the use of go-shops on target shareholders’ wealth, measured by deal

premiums, the probability of receiving competing bids, and the probability of deal completion.

We also look at whether the length of go-shop periods affects target shareholders’ wealth. The

empirical models include the multiple regressions as well as instrumental variable regressions

which control for possible endogeneity of the inclusion of go-shops. Our findings generally

15

support the proposition that go-shops reflect target managers’ effort to fulfill the Revlon duties,

consistent with Subramaniam(2008). We find, however, that the length of go-shop periods does

not have significant effects on shareholder welfare. First, we look at the relationship between deal

premiums and a go-shop provision. The results show that deals including go-shops tend to have a

greater, never less, premium than typical no-shop transactions, which is consistent with a notion

that once initial bidder agree to include a go-shop clause, she tends to offer the higher premium in

order to avoid the possibility that the deal is jumped by competing bidders. The length of go-

shops, however, does not affect a deal premium.

Second, we examine the probability of receiving competing bids during the interval

period and go-shops. We find that by allowing managers to actively solicit the competing offers

deals including go-shops are more likely to receive competing bids. The result does not support

the, so called, “window dressing” hypothesis that target managers who intend to sell the company

to the initial bidder put go-shops to survive judicial scrutiny. Again, there is no evidence that the

longer go-shops tend to invite more competing offers.

Finally, we examine the probability of deal consummation and go-shops. The data show

that both the inclusion of go-shops and the length of go-shops significantly reduce the probability

of deal completion. However, go-shops and the length of go-shops are not significantly correlated

with the completion of high-premium deals. That is, once an initial deal has a high premium, the

likelihood of deal termination is not affected by, or does not decrease in, the inclusion of a go-

shop provision. In sum, this study provides decisive evidence in favor of a go-shop provision by

showing that the inclusion of go-shops improve deal performance and target shareholders’

welfare.

16

References

Balz, K. F. 2003, “No-Shop Clauses”, Delaware Journal of Corporate Law 28, 513-561.

Bates, T. and M. Lemmon, 2003, Breaking up is Hard to Do? An Analysis of Termination Fee Provisions

and Merger Outcomes, Journal of Financial Economics 69, No. 3, 469–504.

Boone A. L. and J. H. Mulherin, 2007, Do Termination Provisions Truncate the Takeover Bidding

Process?, The Review of Financial Studies 20, 461-489.

Amanda K. Bloch. 2010. Go-Shop Provisions: Beneficial Inducement Mechanisms or Window Dressings

for Powerful Private Equity Buyers?, University of Chicago, Manuscript.

Burch, T.R. ,2001, Locking Out Rival Bidders: The Use of Lockup Options in Corporate Mergers,

Journal of Financial Economics 60, 103–41.

Burgess, K. J., 2001, Gaining Perspective: Directors Duties in the Context of “No-Shop” and “No-Talk”

Provisions in Merger Agreements, Columbia Business Law Review 2001, 431-472.

Coates, J. and G. Subramanian, 2000, A Buy-Side Model of Lockups: Theory and Evidence, Stanford

Law Review 53, No. 2, 307–96.

Hotchkiss, E., Qian, J., and W. Song, 2005, Holdups, Renegotiation, and Deal Protection in Mergers,

SSRN Discussion Paper.

Morrel, J.L., Go Shops : A Ticket to Ride Past a Target Board’s Revlon Duties?, Texas Law Review 86,

1123-1157.

Officer, M. ,2003, Termination Fees in Mergers and Acquisitions, Journal of Financial Economics 69,

No. 3, 431–67.

Perry, S. E., and T.H. Williams, 1994, Earning management preceding management buyout offers,

Journal of Accounting and Economics 18, 157-179.

Sautter, C.M., 2008, Shopping During Extended Store Hours: From No Shops to Go-Shops, Brooklyn

Law Review 73, 525-577.

Subramanian, G., 2008, Go-Shops vs. No-Shops in Private Equity Deals: Evidence and Implications, The

Business Lawyer 63, 729-760.

17

Table 1. Sample Distribution

This table provides summary statistics regarding go-shop provisions. The sample includes 1,254 merger agreements during the period 2004 to 2008. Panel A. Go-Shop Provisions by Year

Year No. Go-Shops Go-Shop days of Deals No. (%) Completed Withdrawals Mean Median

This table provides summary statistics regarding go-shop provisions. the method of payment and dividend policies of target and acquiring firms. The sample is divided into two groups: 95 deals with go-shops and 1,159 deals without go-shops. All the variables are discussed in Section 2.B.

Total Sample Without Go-shops With Go-shops Mean Median Mean Median Mean Median No. of Deals 1254 1159 95 Deal Characteristics (%) Deal Premium 0.593 0.343 0.590 0.347 0.581 0.312

Market to Book 1.450 0.946 1.477 0.946 1.113 0.949 Leverage 0.558 0.536 0.555 0.533 0.586 0.607

19

Table 3. Univariate Tests

In Panel A, deals that include go-shops are categorized as the Yes group, while deals without go-shops as the No group. In Panel B, deals are categorized as the Short or Long groups if the number of go-shop days are below or above the median number of days, respectively. Tests for statistically significant differences are from the t-tests and Wilcoxon rank-sum tests for differences in deal performance between two groups. The symbols a, b, and c represent statistical significance at the 1%, 5%, and 10% level, respectively. All the variables are discussed in Section 2.B.

Panel A) Differences in Deal Performance Between Deals With and Without Go-Shops

Go-Shops Yes No N 1159 95

Deal Premium Mean 0.590 0.581

Median 0.347 0.312

Post-Bid Competition Mean 0.092 0.153 b

Median 0 0

Deal Completion Mean 0.851 0.793 c

Median 1 1

Completion of Mean 0.439 0.414

High-Premium Deals Median 0 0

Panel B) Differences in Deal Performance Between Deals With Short and Long Go-Shops

Length of Go-Shops Short Long N 47 48

Deal Premium Mean 0.601 0.561

Median 0.329 0.312

Post-Bid Competition Mean 0.138 0.069 b

Median 0 0

Deal Completion Mean 0.828 0.759 b

Median 1 1

Completion of Mean 0.414 0.414

High-Premium Deals Median 0 0

20

Table 4. Effect of Go-Shops on Deal Premium

As a base-line model, OSL regressions are estimated for deal premiums in the first column of Panel A. In the second column, a treatment effects model is estimated by implementing the MLE. In the fourth column, 2SLS is estimated. The dependent variable is a deal premium, defined in 2.B. Year and industry (1-digit SIC) dummies are included but their coefficients are not reported. The z statistics are reported in brackets. The symbols a, b, and c represent statistical significance at the 1%, 5%, and 10% level, respectively. All the variables are discussed in Section 2.B.

Dependent Variable Deal Premiums

OLS Treatment OLS 2SLS Effects Model Deal Characteristics Go-Shop 0.025 c 0.048 a [1.70] [10.60] Go-Shop Days -0.001 0.001 [-1.07] [0.23] Tfee Size -0.446 -0.257 -6.072 a -6.832 a

[-0.77] [-0.44] [-2.91] [-2.72] Voting Agreement 0.047 0.051 [1.08] [1.55] Long-term Affiliation 0.041 0.016 [0.53] [0.27] Toehold -0.248 -0.448 c -1.671 a -1.701 a

[-0.91] [-1.67] [-4.62] [-3.58] Cash Deal 0.114 a 0.087 a -0.186 -0.182 [3.06] [2.05] [-0.48] [-0.90] LBO -0.067 b -0.034 0.003 0.016 [-2.13] [-1.06] [0.04] [0.18] Related -0.033 -0.019 0.006 0.038 [-1.12] [-0.73] [0.08] [0.29] Hostile 0.134 0.097 0.272 a 0.290 [1.39] [1.46] [3.85] [1.49] Target Characteristics Ln(Market Cap) -0.028 a -0.020 a -0.057 b -0.060 b

[-3.15] [-2.62] [-2.16] [-2.54] Market to Book 0.041 b 0.029 a 0.168 a 0.179 a

[2.85] [4.04] [2.70] [2.93] Leverage 0.053 0.029 0.140 0.164 [0.90] [0.81] [0.80] [0.82] Intercept 0.420 a 0.370 a 0.840 c 0.792 a

Table 5. Effect of Go-Shops on Post-Bid Competition

21

Logit regressions are estimated for post-bid competition, where the dependent variable is a dummy equal to one if a target receives any competing bid during the interval period and zero, otherwise. Marginal effects are calculated at the mean values of the covariates. Year and industry (1-digit SIC) dummies are included but their coefficients are not reported. The z statistics are reported in brackets. The symbols a, b, and c represent statistical significance at the 1%, 5%, and 10% level, respectively. All the variables are discussed in Section 2.B.

Dependent Variable : Dummy for receiving competing bids

Coeff. z value Marginal Coeff. z value Effects

Deal Characteristics Go-Shop 2.025 [3.05] 0.12 0a Go-Shop Days -0.005 [-0.27] Tfee Size -67.692 [-5.56] -4.316 a -41.439 [-4.90]a

Deal Premiums -0.490 [-1.99] -0.031 b Voting Agreement 1.039 [2.02] 0.093 b 3.002 [1.68]c

Logit regressions are estimated for deal completion. In Panel A, the dependent variable is a dummy equal to one if the deal agreement results in a successful acquisition. The dependent variable in Panel B is completion of deals with high premium, which equals one if a deal with a higher premium deal is consummated. A deal has a higher premium if its premium is greater than the industry (1-digit SIC code) median for deals in the same calendar year. Marginal effects are calculated at the mean values of the covariates. Year and industry (1-digit SIC) dummies are included but their coefficients are not reported. The z statistics are reported in brackets. The symbols a, b, and c represent statistical significance at the 1%, 5%, and 10% level, respectively. All the variables are discussed in Section 2.B.

Panel A. Determinants of Deal Completion

Dependent Variable : Dummy for deal completion

Coeff. z value Marginal Coeff. z value Effects

Deal Characteristics Go-Shop -0.743 [-1.92] -0.051 c