Page 1

e-Proceedings of the Global Conference on Islamic Economics and Finance 2018

24th & 25th October 2018 / Sasana Kijang, Bank Negara Malaysia, Kuala Lumpur

e-ISBN: 978-967-2122-63-0

59

Poverty Alleviation in Mogadishu, Somalia: The Role of Islamic

Microfinance

MOHAMED ABDI ELMI XALANE

DR. MARHANUM BINTI CHE MOHD SALLEH

Department of Finance

Islamic International University of Malaysia (IIUM)

Mogadishu

SOMALIA

[email protected]

[email protected]

ABSTRACT

The objective of this paper is to empirically examine the role of Islamic microfinance in poverty

alleviation in Mogadishu, Somalia. The study basically concerns on two objectives which are; to

observe the current practice of Islamic microfinance in Mogadishu, Somalia, and to investigate the

effectiveness of Islamic microfinance institutions in this country towards poverty reduction. To

achieve the research objectives, quantitative methodology is adopted and primary data is relied on

for analysis. Based on survey questionnaire, the sample of this research were microfinance

recipients in Mogadishu, Somalia. Via descriptive analysis, it is revealed that the current practice of

Islamic microfinance activities in Mogadishu, Somalia is serving the poor people, but these

microfinance activities are not effective in terms of the procedure of obtaining loans, enhancement

of standard living, usefulness of the system, and the awareness level of the people. In addition, the

findings of this study will be beneficial for the Islamic microfinance institutions, Islamic banks who

involve microfinance services, enterprises, academicians and researchers who interest in this area.

Keywords: Microfinance, Islamic Microfinance Institutions, Poverty Alleviation, Current Practice,

Effectiveness

Paper type- Research paper

1.0 INTRODUCTION

Poverty has a huge challenge to the less developed and developing nations. Poverty alleviation

requires diverse projects to encourage supplying productive resources and income among the poor

people in an effective way. Actually, the multidimensionality of poverty shows continuous barriers

facing all governments (Pramanik et al., 2008). Therefore, to manage poverty as a social issue,

microfinance has been supported as the best tool of poverty alleviation. Microfinance has acquired

global acknowledgment and great outcomes diminishing the power of poverty stages in less

developed and developing nations (Chemin, Hossain and Knight, 2008).

In Africa where the microcredit development started in the 1980s, and it wound up more grounded

in the 1990s is the poorest continent on the earth, as indicated by the new multidimensional poverty

Page 2

e-Proceedings of the Global Conference on Islamic Economics and Finance 2018

24th & 25th October 2018 / Sasana Kijang, Bank Negara Malaysia, Kuala Lumpur

e-ISBN: 978-967-2122-63-0

60

file reported by Oxford University (Hiedhues, 1995). The issue is especially strong in Sub-Saharan

Africa, where just 5% to 25% of families have a formal association with microfinance

institutions(Kipesha, 2012). The state is the home of 2% of the world's microfinance organizations,

and this shows the absence of access to microfinance institutions (MFIs) as one of the biggest

barriers to the African people(Businesses, n.d.).

Somalia, even though there were a numerous problems and challenges, keeps on trying imperative

endeavours towards re-establishing its key economic and financial institutions(Hurlburt, 2012).

Although a huge obstacles stay ahead to enhance financial conditions and lift a large number of

Somali people from the outrageous poverty and lack of income. Around, 60% for Somalia's

population lives under the poverty line(Ali & Abu-hadi, 2013). The type of poverty that Somalia is

facing is same as those other African countries have, except that Somalia is in fight against terrorist

group. Poverty is the consequence of a set of complex and interconnected social and economic

crisis, which resulted from lack of income-generating institutions(Taiwo, 2012). However, the

economic development of the country is not too bad and year after year a lot of financial institutions

are emerging around the country. These institutions offer different financial services to the

customers such as saving, financing, investment funds, and microfinance packages(Mohamed &

Ahmed, 2015). Salaam Somali Bank and a small number of NGOs such as Saïd Foundation and

KAAH microfinance institution began microfinance services targeting the poor people and their

performance has stayed minimal and mostly limited to cities (Aden, 2011).

Therefore, the objective of this study is to investigate (1) the Current practice of Islamic

microfinance activities in Mogadishu, Somalia. The study also examines (2) the effectiveness of

Islamic microfinance institutions in poverty reduction in Mogadishu, Somalia. In order to achieve

the above stated objectives, the following research questions are developed: (1) what is the Current

practice of Islamic microfinance activities in Mogadishu, Somalia? (2) Are they effective the

Islamic microfinance institutions in Mogadishu, Somalia?

The structure of this paper is as follows: section 2 is the literature review which consists of sub-

topics, section 3 is the research methodology, section 4 consists of the analysis and findings of the

research objectives, and section 5 is the conclusion and recommendation of the study.

2.0 LITERATURE REVIEW

2.1 Overview of poverty and Islamic microfinance system

Poverty reduction has been an on-going challenge throughout the history of human being. As it is

narrated from the Qur’an and Sunnah, the religion of Islam orders people who are wealthier to help

the poor people in terms of giving them Zakat, Sadaqah, Waqf and Gifts. The Prophet Muhammad

peace be upon him (p.b.u.h.), inquired for Allah’s safety from the worship of idols and poverty by

saying: “O Allah, I seek your protection from poverty, deficiency and humbleness”(Stagg-Macey,

2007). Muslims should pay for their best to contest against poverty at all stages, because poverty is

a risk to a man’s trust, community safety and stability. Unfortunately, most countries who are

members of the Organization of Islamic Conference (‘OIC’) are undeveloped or less developed

nations and that is why poverty is devastatingly exist in Muslim states(Rokhman, 2013). Likewise,

Muslim people do not give especial consideration to the challenge of poverty because of lack of

integration and mutual interdependence(Badr, Din, & College, n.d.).

Page 3

e-Proceedings of the Global Conference on Islamic Economics and Finance 2018

24th & 25th October 2018 / Sasana Kijang, Bank Negara Malaysia, Kuala Lumpur

e-ISBN: 978-967-2122-63-0

61

Therefore, in order to fight poverty, Islamic microfinance has been introduced as the effective

technique to combat and eliminate poverty(Stagg-Macey, 2007). For the last years, conventional

microfinance institutions (‘MFIs’) have completed a remarkable effect in low-income countries and

their existence is touched and acknowledged around the world. Islamic finance is a new field in the

economy and still is in the development stage. So, it is not unanticipated that Islamic Microfinance

Institutions (IMFIs) have not completely industrialized so far(Usman & Tasmin, 2016). Even

though the evolution of Islamic banking and finance exists, it was a decade ago when Islamic banks

started to give special consideration the importance of Islamic microfinance, because of two

reasons. First reason, the World Bank recognized the year 2005 as the year of Microfinance. The

second reason was, in 2006, the founder of Grameen Bank Bangladesh Prof. Muhamad Yunus,

succeeded the Nobel Peace Prize for microfinance. Although there was a few number of researches

relating to microfinance which have been published prior to these years 2005 and 2006, but the

most of the researches have been done after these two years(Stagg-Macey, 2007).

One of the first papers of Islamic microfinance was done by Dhumale and Sapcanin, who presented

the connection between Islamic banking and microfinance. They got that the available methods of

financing within the Islamic banking can be simply modified to and applied to the MFIs(Finance,

2008). Basically, Islamic banking and microfinance packages may be complementary on each other,

in terms of conceptually and practically. In their study, they did comparison in mudarabah,

murabahah, and qard al-hasan as possible technique for Islamic microfinance. They revealed that

murabahah is the most applied and appropriate tool for Islamic microfinance(Abdelkader & Salem,

2013). Their outcome is not astonishing because murabahah is the most well-known method in

Islamic banks. Because of Murabahah is somehow similar to conventional interest-based lending. It

is thought that the structure of Islamic microfinance institutions (IMFIs) will be same as to its

counterpart. Taking this in mind, Ahmed (2002), critically analysed the nature of IMFs and matched

them with their counterpart. As a consequence, the following dissimilarities are appeared; first,

sources of funds, second, types of financing, third, way of dealing with defaults and other

differences(Ahmed & Ammar, 2015).

2.2 Islamic Microfinance around the Globe

The World Bank states that dangerous poverty is living on less than 1.25 dollar per day, whereas

living on less than 2 dollar a day is moderate poverty (World Bank, 2008). In 2015 report, the

Millennium Development Goals (MDGs) discovered that the number of individuals living in

extreme poverty has dropped from 1.9 billion to 836 million in 1990 to 2015 respectively, while the

middle class families who are living more than 4 dollar a day has almost increased sharply between

1991 and 2015(Usman & Tasmin, 2016). This indicates the massive financing for the combat

against poverty. In terms of the low-income people, the view of getting out of poverty was hard

because financial organizations seeming them as un-bankable for their incapability to possess

guarantee security, and having a poorer human ability (GIFR, 2012). Micro-finance emerged as an

economic improvement for the purpose of helping poor people which are economically

omitted(Jegatheesan, Ganesh, S, & Banks, 2011). Islamic microfinance is a branch of Islamic

finance. The purpose of Islamic finance is to develop businesses which are established on profit and

loss sharing and avoiding everything that is prohibited by the shari’ah such as interest, gharar,

maysir in business contacts (Bhuiyan et al., 2011). Islamic microfinance is based on the thought of

Islamic social fairness that inspires charity to the poor families. It practices profit and loss sharing

(PLS) procedures in trade between the entrepreneurs and the capital providers (Rahman and Rahim

2007). It organizes capitals, savings and hiring chances to achieve the fundamental needs of the

Page 4

e-Proceedings of the Global Conference on Islamic Economics and Finance 2018

24th & 25th October 2018 / Sasana Kijang, Bank Negara Malaysia, Kuala Lumpur

e-ISBN: 978-967-2122-63-0

62

poor to overcome poverty (Kahf, 2007). The Islamic microfinance has generated actual values in

improving the standard of living of the low-income people(“Journal of Islamic Banking and

Finance Jan. - Mar. 2016 1,” 2016).

In 2012, GIFR has classified the Islamic microfinance products into three groups: micro-credit,

micro-equity and charity(Usman & Tasmin, 2016). The micro-credit involves the procedure of

business assets which is based on loan and lease. One of the concerns for this notion is a lack of

assets in the aspect of commercial chances. Micro-equity facilitates the process of business

contracts where one party is the capital provider and the other party is the entrepreneur. The last one

is the charity feature of Islamic microfinance(Usman & Tasmin, 2016). In conventional

microfinance, one of the main reasons that they are failed to reduce poverty is default problem,

because lenders always divert loan in order to generate high income because of the high interest

they are charging to the loan recipients(Kipesha, 2012). In this situation, lenders deviate the goal of

eliminating poverty and they go to income generators from the poor people’s low income that is

why God is prohibited interest rate (riba), which is always makes richer to those who are already

rich (Laila, 2007). On the other hand, Islamic microfinance has a comprehensive method which is

based on Shari ah principles. The micro-credit (qardhul hasan) delivers to the innocent people an

interest-free financing procedure. Such as Murabaha contract which assists to the low-income

individuals to buy things they want without paying any extra amount of money except the

repayment in equal amount of the principles they already borrowed(Smolo & Ismail, 2011). In

addition to that, ijarah which may come into two forms an operating lease or financial lease helps to

the poor people to take only the advantage of the asset since they do not afford to purchase the

product in exchange providing rental payments to the owner of the assets(Smolo & Ismail, 2011).

The notion of profit and loss sharing (PLS) is to confirm risk elimination, and that is achieved

among the suppliers of factors of production (Rahman & Rahim, 2007). The PLS goods in the

procedure of mudaraba and musharaka possibly present more business prospects for the people.

These partnership business contracts share PLS fairly, and simplify wealth reallocation as well as

generating productive volumes that clue to the business expertise(Rahim, Rahman, Rahim, &

Rahman, 2013). In order to develop the Islamic microfinance, it should meet up with the ambitions

of the Islamic economic system, which is to enhance PLS products (Saad et al., 2013). The charity

aspect consists of Zakat, Waqf, and Sadaqah is to give money and any other useful resources to

those who need it. It also alleviates unfairness in capital distribution and also confirms economic

stability(Usman & Tasmin, 2016).

2.3 Nature and practice of Islamic microfinance in Muslim Countries

In the last decades, the combined Islamic banks and the conventional banks which also have Islamic

divisions have widely blow-out. In 2007, Islamic institutions reached approximately 300

organisations including banks, insurance companies, and investment banks, with total assets of 500

billion US dollar. The conventional banks which are also have Islamic banking branches spread out

to the whole world especially non-Muslim countries such as China, Switzerland, Germany, India,

UK, Luxemburg, Canada, Japan, and USA(Badr et al., n.d.). This large number of Islamic banks has

motivated some of them to penetrate the microfinance field. Some of these institutions began

helping the low-income people in some of the Muslim countries by providing services which are

Shari ah compliance. These growths led to the arrival of Islamic Microfinance institutions(Badr et

al., n.d.). Every year, Microfinance increases by 15 to 30% which is approximately in terms of

money $ 6 billion dollar annually(Taiwo, 2012). Thus, in this market there is a great opportunity for

the private Islamic institutions to go in, perceiving that contribution of the private wealth is

Page 5

e-Proceedings of the Global Conference on Islamic Economics and Finance 2018

24th & 25th October 2018 / Sasana Kijang, Bank Negara Malaysia, Kuala Lumpur

e-ISBN: 978-967-2122-63-0

63

constantly growing and estimated to reach nearly 20 billion in US dollar in 2020 (Standards &

Poors’s Ratings Direct, 11 March 2008, p. 2). The study directed by the Consultative Group states

that the number of Islamic financial organizations proposing microfinance is 120 signifying merely

0.5% of the total worldwide microfinance establishments which is about 389 thousands. Almost

80% of the Islamic microfinance associations are situated in Afghanistan, Bangladesh, and

Indonesia. Whereas, according to the Study, the demand for these Islamic microfinance institutions

reached 20% to 40% in countries such as Jordan, Algeria, and Syria(Abdelkader & Salem, 2013).

However, we can say that the Islamic microfinance is still in its first stages. A small number of

Islamic microfinance banks and institutions are currently operating in the field of microfinance.

According to estimations, the Islamic microfinance covers presently about 380 thousands customers

only (CGAP, Microfinance Gateway, 2010), while the deprived Muslims institute 35% of the total

number of Muslims projected at 1.2 billion (Asia-Pasific Economic Cooperation, 2008). The UNDP

predicted that there is a huge chance for the Islamic microfinance providers which is about 7 million

recipients from Islamic finance and about 19 million investors (Balake Goud,

http://www.investhalal.org/articles/articles/IslamicMF.pdf.), which clearly indicating that there is a

large market for Islamic microfinance institutions(Jegatheesan et al., 2011).

2.4 Islamic Microfinance in Somalia

In 1993, the first micro-credit program emerged in Mogadishu, Somalia which was developed by

SA‟ID Foundation. This organization was getting a financial support from Oxfam America in 1996

(SA‟ID report, 2005). Then, the SA‟ID was given loans to the poor people with a lower

rate(Mohamed & Ahmed, 2015). Additionally, in 2010, Salam Somali Bank (SSB) which is

commercial bank also started microfinance packages such as loans with no interest rates ( qard

loans), mudarabah, Waqf, financial aids to support the low-income individuals who live in

Mogadishu, Somalia (Salam Somali Bank Website, 2011). Three years later after SSB began

Microfinance programs, a new Microfinance institution was established which is called KAAH

Islamic Microfinance (KIM)(Mohamed & Ahmed, 2015). The purpose which was established this

institution was to enhance and participate poverty alleviation campaigns around Somalia. KIM

gives especial priorities for small-medium enterprises, youth, and women by providing them Shari

ah compliant services(Ali & Abu-hadi, 2013). The institution offer to the clients same services like

SSB, but KIM also provides additional services to the customers such as savings, insurance services

to cover the needs of the people to have different programs in Islamic Microfinance in Mogadishu,

Somalia.

3.0 RESEARCH METHODOLOGY

This study is applied descriptive research design. The purpose of employing descriptive research

design is to answer the how, Why, and what questions(Mohamed & Ahmed, 2015). The study uses

primary data and adopts quantitative research method in order to reach the research objectives.

Thus, survey questionnaire was used to collect the required data. This study also adopts cross-

sectional research method because the data was collected at one specific time in different places (17

districts) in Mogadishu, Somalia. The population of this study are Islamic Microfinance recipients

who live in Mogadishu, Somalia. The sample of this study is taken from randomly in the target

population that are properly living in the 17 districts in Mogadishu, Somalia. The number of

respondents that was taken as a sample size is 65. In general, the study applies a pilot study because

of this mini research is designed to test the availability of the data and groundwork prior to a larger

Page 6

e-Proceedings of the Global Conference on Islamic Economics and Finance 2018

24th & 25th October 2018 / Sasana Kijang, Bank Negara Malaysia, Kuala Lumpur

e-ISBN: 978-967-2122-63-0

64

study, in order to enhance the quality and efficiency of the upcoming research project. The research

tool used to collect data for this study is self-administrated questionnaire. The use of this

questionnaire is justified as it is online platform. It is fast and effective method of collecting data

within a short period of time and with less cost compared to other research mechanisms. The

limitation of the research to meet all requirements is the distance because the study is conducted in

Kuala Lumpur, Malaysia and it is applied in Mogadishu, Somalia. The questions in the

questionnaire were adopted from the previous studies relating on IMFIs(Taiwo, 2012). The

collected date from the respondents were analysed using Statistical Package for Social Science

(SPSS) software to run descriptive analysis.

4.0 ANALYSIS AND FINDINGS

This section consists of data analysis, interpretation and findings. The data analysis and findings

were based on the research objectives as well as research questions. The first part was presented the

respondents profile or demographic data, the second part deals with analysis and third part relates to

findings of the research objectives.

4.1 Demographic Data

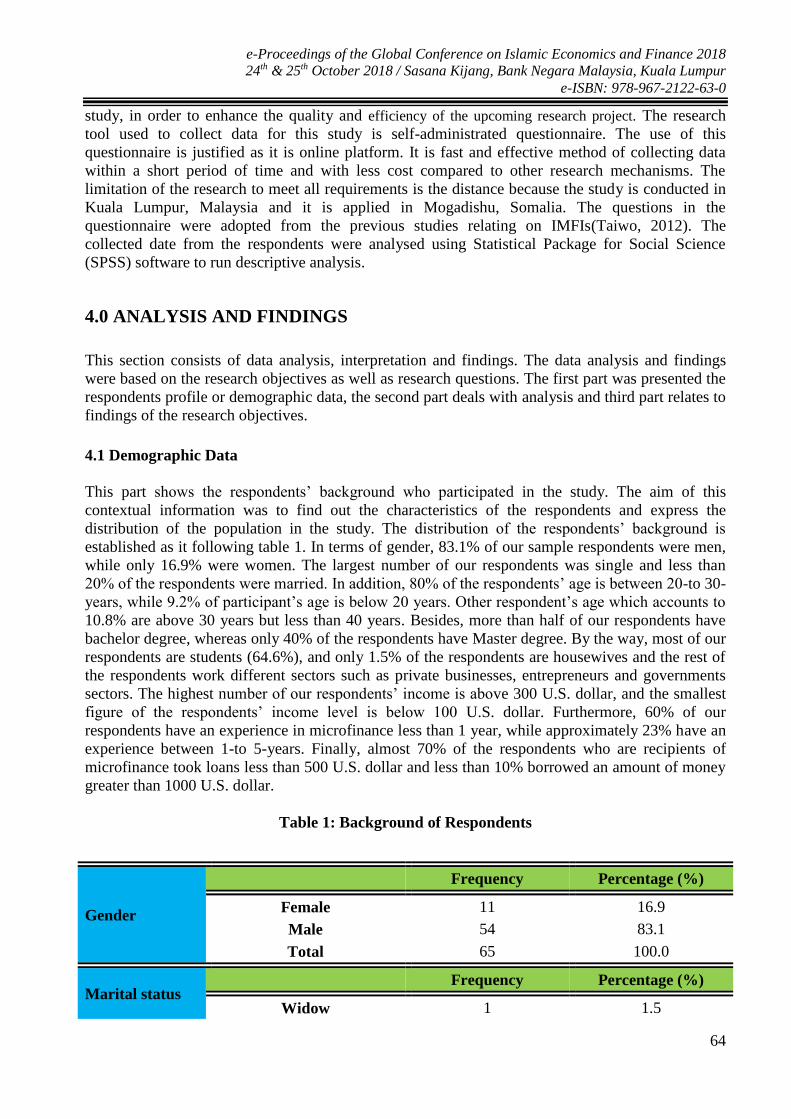

This part shows the respondents’ background who participated in the study. The aim of this

contextual information was to find out the characteristics of the respondents and express the

distribution of the population in the study. The distribution of the respondents’ background is

established as it following table 1. In terms of gender, 83.1% of our sample respondents were men,

while only 16.9% were women. The largest number of our respondents was single and less than

20% of the respondents were married. In addition, 80% of the respondents’ age is between 20-to 30-

years, while 9.2% of participant’s age is below 20 years. Other respondent’s age which accounts to

10.8% are above 30 years but less than 40 years. Besides, more than half of our respondents have

bachelor degree, whereas only 40% of the respondents have Master degree. By the way, most of our

respondents are students (64.6%), and only 1.5% of the respondents are housewives and the rest of

the respondents work different sectors such as private businesses, entrepreneurs and governments

sectors. The highest number of our respondents’ income is above 300 U.S. dollar, and the smallest

figure of the respondents’ income level is below 100 U.S. dollar. Furthermore, 60% of our

respondents have an experience in microfinance less than 1 year, while approximately 23% have an

experience between 1-to 5-years. Finally, almost 70% of the respondents who are recipients of

microfinance took loans less than 500 U.S. dollar and less than 10% borrowed an amount of money

greater than 1000 U.S. dollar.

Table 1: Background of Respondents

Gender

Frequency Percentage (%)

Female 11 16.9

Male 54 83.1

Total 65 100.0

Marital status Frequency Percentage (%)

Widow 1 1.5

Page 7

e-Proceedings of the Global Conference on Islamic Economics and Finance 2018

24th & 25th October 2018 / Sasana Kijang, Bank Negara Malaysia, Kuala Lumpur

e-ISBN: 978-967-2122-63-0

65

Married 11 16.9

Single 53 81.5

Total 65 100.0

Age

Class Frequency Percentage (%)

20 – 30 years 52 80.0

31 – 40 years 7 10.8

Below 20 years 6 9.2

Total 65 100.0

Level of

Education

Frequency Percentage (%)

Degree 39 60.0

Master 26 40.0

Total 65 100.0

Occupation

Frequency Percentage (%)

Business owner 6 9.2

Government sector 4 6.2

Housewife 1 1.5

Others 3 4.6

Private sector 9 13.8

Students 42 64.6

Total 65 100.0

Income Level

U.S. Dollar Frequency Percentage (%)

101 - 200 17 26.2

201 - 300 17 26.2

301 and above 22 33.8

50 - 100 9 13.8

Total 65 100.0

Years of

Experienced

Frequency Percentage (%)

Less than 1 year 39 60.0

1 - 5 years 15 23.1

11 - 20 years 3 4.6

Page 8

e-Proceedings of the Global Conference on Islamic Economics and Finance 2018

24th & 25th October 2018 / Sasana Kijang, Bank Negara Malaysia, Kuala Lumpur

e-ISBN: 978-967-2122-63-0

66

1-5 Years 3 4.6

6 - 10 years 4 6.2

Above 20 years 1 1.5

Total 65 100.0

Amount of

Loans

U.S. Dollar Frequency Percentage (%)

Less than 500 45 69.2

501-1000 14 21.6

more than 1000 6 9.2

Total 65 100.0

4.2 Analysis of the research objectives

4.2.1 Research Objective One

The first objective of this study was to examine the current practice of Islamic microfinance

activities in Mogadishu, Somalia. To reach this goal, we asked our target sample’s respondents a

number of questions to give responses to the research question one stated above. The questions are

organized to the respondents for the purpose to investigate the respondents’ views about the

research objective one.

Table 2: The practice of Islamic Microfinance in Somalia

No Descriptive Statistics 1 2 3 4 5 Mean Std.

Dev. Interpretation

1 The rate of return charged

by the IMFIs is acceptable. 15.4 13.8 12.3 41.5 16.9 3.31 1.33 Agree

2

The term and conditions for

collateral are reasonable and

flexible (e.g. client can use

guarantor)

16.9 6.2 26.2 30.8 20.0 3.31 1.33 Agree

3

IMFIs in Mogadishu

provides financial services

to the poor

16.9 16.9 15.4 29.2 21.5 3.22 1.41 Agree

4

Products and services

offered by IMFIs cover the

needs of the poor.

9.2 13.8 21.5 40.0 15.4 3.38 1.18 Agree

5

Islamic MFIs indirectly

increases the employment in

the country

4.6 6.2 9.2 55.4 24.6 3.90 1.00 Disagree

6 Islamic microfinance

services are available for all 4.6 7.7 18.5 41.5 27.7 3.8 1.08 Disagree

Page 9

e-Proceedings of the Global Conference on Islamic Economics and Finance 2018

24th & 25th October 2018 / Sasana Kijang, Bank Negara Malaysia, Kuala Lumpur

e-ISBN: 978-967-2122-63-0

67

living below the poverty line

income

Average 3.49 1.22 Agree

1= Strongly Disagree (%), 2= Disagree (%), 3= Neutral (%), 4= Agree (%), 5= Strongly Agree (%)

The above table two relates to the respondents’ views about the current practice of Islamic

microfinance in Mogadishu, Somalia. It shows that the recipients are responded whether the rate of

return charged by the Islamic microfinance institutions is acceptable, and if the term and conditions

for collateral are reasonable and flexible with a mean and standard deviation of 3.31 of 1.33

respectively. Besides, respondents also replied that the current Islamic microfinance institutions in

Mogadishu provide financial support to the low-income people with a mean of 3.22 and standard

deviation of 1.41. Furthermore, respondents responded that the products and services offered by the

Islamic microfinance institutions in Mogadishu cater the needs of the poor people. According to

the scale unit which is 3.49, respondents agreed the above four statements we asked them.

However, respondents rejected the last two questions. They said that the Islamic microfinance

institutions do not indirectly increase the employment opportunities in Somalia, with a mean of 3.90

and standard deviation of 1.00. They also mentioned that the Islamic microfinance services are not

available for all living below the poverty line income with a mean and standard deviation of 3.8 and

1.08 respectively.

4.2.2 Research Objective Two

The second objective of this study was to observe the effectiveness of Islamic microfinance

institutions in poverty reduction in Mogadishu, Somalia. To achieve this objective, respondents are

asked a number of questions to give answers to the research question two stated above. The

questions are prepared to the recipients for the aim to explore the respondents’ opinions about the

research objective two.

Table 3: The effectiveness of Islamic Microfinance Institutions in Somalia

No Descriptive Statistics 1 2 3 4 5 Mean Std.

Dev. Interpretation

1

The procedure of obtaining

loans from IMFIs is easier

and convenient. 20.0 10.8 16.9 23.1 29.2 3.61 1.50 Disagree

2 IMFIs have improved their

clients standard of living 6.2 13.8 18.5 32.3 29.2 3.65 1.22 Disagree

3

IMFIs in Mogadishu

enhanced monthly income

of their client

3.1 13.8 21.5 47.7 13.8 3.56 1.00 Disagree

4

IMF is a useful tool to

develop basic needs of the

society

6.2 9.2 21.5 40.0 23.1 3.65 1.12 Disagree

5 IMFIs increase the

awareness level (educational 4.6 16.9 27.7 30.8 20.0 3.45 1.13 Agree

Page 10

e-Proceedings of the Global Conference on Islamic Economics and Finance 2018

24th & 25th October 2018 / Sasana Kijang, Bank Negara Malaysia, Kuala Lumpur

e-ISBN: 978-967-2122-63-0

68

level) of the society.

6

The type of the IMF used by

IMFIs is the best tool for

poverty eradication.

6.1 9.2 13.8 50.8 20.0 3.68 1.13 Disagree

Average 3.55 1.18 Disagree

1= Strongly Disagree (%), 2= Disagree (%), 3= Neutral (%), 4= Agree (%), 5= Strongly Agree (%)

In table 3, the responses of our respondents related to whether the Islamic Microfinance Institutions

in Mogadishu, Somalia are effective in terms of poverty alleviation. It indicates that the

respondents are asked whether the procedure they obtain loans from the Islamic microfinance

institutions are easier and convenient with a mean of 3.61 and standard deviation of 1.50 in

accordance to the range scale mean (3.55) which denotes “agree”. Recipients of microfinance

facilities mentioned that the present microfinance facilities in Mogadishu, Somalia have not

improved their standard of living, and even these facilities have not increased their monthly income

with a mean and standard deviation of 3.56 and 1.00 respectively. Respondents also said that the

type of the Islamic Microfinance used by Islamic Microfinance Institutions in Mogadishu, Somalia

is not the best tool for poverty eradication, with a mean of 3.68 and standard deviation of 1.13.

However, according to the scale mean and the standard deviation unit, they agreed that Islamic

Microfinance Institutions in Mogadishu increase the level of awareness of the society about the

existence of Islamic microfinance services, with a mean and standard deviation of 3.45 and 1.13

respectively.

4.3 Findings of the Research Objectives

In research objective one, recipients of microfinance services who are our respondents agreed that

the rate of return charged by Islamic microfinance institutions is acceptable, which means the rate is

low and low-income people are able to pay it. They also agreed that the terms and conditions for

collateral are reasonable and flexible and it is also possible to use guarantor. In addition to that, they

also admired that the Islamic microfinance institutions in Mogadishu provides financial services to

the poor, and these services offered by Islamic microfinance institutions can cover the needs of the

poor families. However, respondents argue that these microfinance facilities are not creating

employment opportunities to the poor people, and this means their services remain minimal. They

also believe that the Islamic microfinance services in Mogadishu are not available for all people

who are living below the poverty line income, because the institutions will not give money to the

people they think will default. In general, the current practice of Islamic microfinance activities in

Mogadishu, Somalia is reasonable and it is serving to the poor people.

In research objective two, we were examining the effectiveness of Islamic microfinance institutions

in Mogadishu, Somalia. We measured the effectiveness of these Islamic microfinance services in

terms of easiness and convenience of obtaining the loans, how the microfinance services participate

the improvement of the standard-living of poor people, the usefulness of the system, the awareness

level, and the whether the type of the Islamic microfinance offered by Islamic microfinance

institutions is the exact tool that can be used to eliminate poverty. After asking several questions to

the recipients of microfinance services, Respondents agreed only that the Islamic microfinance

institutions in Mogadishu enhanced the awareness level of the society. Because the service of

microfinance is spreading to the whole country, so a lot of people are becoming to know

Page 11

e-Proceedings of the Global Conference on Islamic Economics and Finance 2018

24th & 25th October 2018 / Sasana Kijang, Bank Negara Malaysia, Kuala Lumpur

e-ISBN: 978-967-2122-63-0

69

microfinance facilities which are provided by Islamic microfinance institutions. However, they

disagreed all other measures of effectiveness. They mentioned that the process of obtaining loans is

not easy, the service is not increasing the standard of living of the people, and the Islamic

microfinance is not a useful tool to develop basic needs of the society, and the type of the Islamic

microfinance used by Islamic microfinance institutions in Mogadishu is not the best tool for poverty

eradication. Overall, we may conclude that the Islamic Microfinance Institutions in Mogadishu,

Somalia are not effective in terms of the above factors. Other studies also indicate the same

conclusion we found in this study. According to the study done by Ali and Abu-hadi, they showed

that the Islamic microfinance in Somalia is not effective because of difficulties borrowing loans,

and they also mentioned that majority of Somali people are not able to excess microfinance

facilities(Ali & Abu-hadi, 2013). In addition, in 2015, study conducted by Ahmed Dahir, stated that

the current microfinance in Somalia have positive impact in poverty reduction(Mohamed & Ahmed,

2015).

5.0 CONCLUSION AND RECOMMENDATION

The purpose of this paper was to investigate the role of Islamic microfinance in poverty alleviation

in Mogadishu, Somalia. The study focused on two objectives; the first objective was to examine the

current application of Islamic microfinance activities in Mogadishu, Somalia. After analysing this

factor, we found that the current practice of Islamic microfinance activities in Mogadishu is serving

the poor people and facilitated the low income people to get loans in a convenient rate, although this

service is not available to all poor people. The second objective of this study was to investigate the

effectiveness of Islamic microfinance institutions in poverty reduction in Mogadishu, Somalia. The

study concluded after analysing the respondents responses that the Islamic microfinance institutions

in Mogadishu is not effective in terms of the process of obtaining loans, usefulness of the service,

and the system is not the best tool to fight for the poverty, and the Islamic microfinance

institutions’ support is not enough to cover the needs of the low-income people. Furthermore, the

findings of this study will be beneficial for the Islamic microfinance institutions, Islamic banks who

involve microfinance services, enterprises, and researchers who interest in this area. Thus, other

researchers who want to do research in this topic and other related topics can examine the

efficiencies and challenges of Islamic microfinance institutions in Somalia. They can also

investigate the relationship between small-medium enterprises and microfinance institutions.

Finally, as a recommendation, Islamic Microfinance institutions in Mogadishu should improve their

products and services in order to cover the demand of the people. They should also rearrange the

type of microfinance techniques they employed to increase their support for the poor people. The

government should also give subsidies to the Islamic institutions and banks who offer microfinance

facilities in order to expand their support to the low-income people.

Page 12

e-Proceedings of the Global Conference on Islamic Economics and Finance 2018

24th & 25th October 2018 / Sasana Kijang, Bank Negara Malaysia, Kuala Lumpur

e-ISBN: 978-967-2122-63-0

70

REFERENCES

Abdelkader, I. Ben, & Salem, A. Ben. (2013). Islamic vs Conventional Microfinance Institutions:

Performance analysis in MENA countries. International Journal of Business and Social

Research, 3(5), 219–233. https://doi.org/10.18533/ijbsr.v3i5.21

Ahmed, E. M., & Ammar, A. (2015). Islamic Microfinance in Sudanese Perspective Business &

Financial Affairs, 4(3). https://doi.org/10.4172/2167-0234.1000149

Ali, A. H., & Abu-hadi, A. O. (2013). The Accessibility of Microfinance for Small Businesses in

Mogadishu , Somalia , The Accessibility of Microfinance for Small Businesses in Mogadishu ,

Somalia, (December 2014).

Badr, P., Din, E., & College, M. (n.d.). No Title, 1–23.

Businesses, S. (n.d.). Microfinance in Africa.

Finance, I. (2008). Islamic Microfinance: An Emerging Market Niche, (March).

Hurlburt, K. (2012). Microfinance and Remittances, (December).

Jegatheesan, S., Ganesh, S., S, P. K., & Banks, A. (2011). Research Study about the Role of

Microfinance Institutions in the Development of Entrepreneurs, 2(4), 2–5.

Journal of Islamic Banking and Finance Jan. - Mar. 2016 1. (2016).

Kipesha, E. F. (2012). Efficiency of Microfinance Institutions in East Africa : A Data Envelopment

Analysis, 4(17), 77–88.

Mohamed, A., & Ahmed, D. (2015). The Challenges Facing Microfinance Institutions in Poverty

Eradication : A Case Study in Mogadishu, 2(2), 56–62.

Rahim, A., Rahman, A., Rahim, A., & Rahman, A. (2013). Islamic microfinance : an ethical

alternative to poverty alleviation. https://doi.org/10.1108/08288661011090884

Rokhman, W. (2013). The Effect of Islamic Microfinance on Poverty Alleviation: Study in

Indonesia. Journal of Economics and Business, XI(2), 21–31.

Page 13

e-Proceedings of the Global Conference on Islamic Economics and Finance 2018

24th & 25th October 2018 / Sasana Kijang, Bank Negara Malaysia, Kuala Lumpur

e-ISBN: 978-967-2122-63-0

71

Smolo, E., & Ismail, A. G. (2011). A theory and contractual framework of Islamic micro-financial

institutions operations. Journal of Financial Services Marketing, 15(4), 287–295.

https://doi.org/10.1057/fsm.2010.24

Stagg-Macey, C. (2007). An Overview of Islamic Insurance. ICMIF Takaful, (January 2012).

Taiwo, J. N. (2012). THE IMPACT OF MICROFINANCE ON WELFARE AND POVERTY

ALLEVIATION IN SOUTHWEST NIGERIA BY CU03GP0036 Department of Banking and

Finance School Of Business College of Development Studies Covenant University , Ota Being

A PhD Thesis Submitted in Partial Fulfillm.

Usman, A. S., & Tasmin, R. (2016). The Role of Islamic Micro-finance in Enhancing Human

Development in Muslim Countries. Journal of Islamic Finance, 5(1), 053–062.

https://doi.org/10.13140/RG.2.1.3233.1762