Submitted in Partial Fulfillment of the Requirements

for the Degree of

Doctor of Philosophy

August 2006

The thesis of Anuja Jayaraman was received and approved* by the following Jill. L. Findeis Professor of Agricultural, Environmental and Regional Economics and Demography Thesis Advisor Chair of Committee Carolyn E. Sachs Professor of Rural Sociology and Women’s Studies Gretchen T. Cornwell Research Associate and Assistant Professor of Rural Sociology and Demography Bee-Yan Roberts Professor of Economics Stephen M. Smith Professor of Agricultural and Regional Economics Committee Member and Head of Department of Agricultural Economics and Rural Sociology * Signatures are on file in the Graduate School.

Abstract

South Asia has the largest concentration of the world’s poor, with over half a

billion people surviving on less than a dollar a day. One of the Millennium Development

Goals (MDG) aims to halve the proportion of the world’s people whose income is less

than one dollar a day and the proportion of people who suffer from hunger by the year

2015. The success of poverty alleviation programs in South Asia is critical if this MDG

is to be met. Within South Asia, Bangladesh has the highest incidence of poverty and

only India and China have larger numbers of poor people. It is estimated that nearly half

of Bangladesh’s population of 135 million people live below the poverty line. The

Human Poverty Index reported by the Human Development Report places Bangladesh at

the 86th position among 103 developing countries. Apart from high poverty levels and

low gender empowerment rates, the country also faces yearly natural disasters in the form

of floods. In this dissertation, we first analyze issues relating to chronic and transient

poverty following a major catastrophic event using a short panel of household data from

Bangladesh. Bangladesh experienced the largest floods of the century in 1998. Increase

in private borrowing was one of the medium-term impacts of the floods. The

International Food Policy Research Institute’s Food Management and Research Support

Project (IFPRI-FMRSP) household survey of rural Bangladesh for the years 1998-99 is

used for the analysis. The dissertation attempts to identify the characteristics that

distinguish between those who are able to eventually escape poverty following the flood

(the transient poor) versus those unable to leave poverty (chronic poor). The study uses

cost-of-basic-needs (CBN) poverty lines calculated by the World Bank for Bangladesh

for the year 2000. We use multinomial logit models to asses the determinants of chronic

iii

and transient poverty, comparing them to Bangladeshi households that were never poor.

We also use Censored Quantile Regression models to identify the correlates of each kind

of poverty.

We find that household size, dependency ratio, number of working members, land

ownership, location, social assistance and education characterize the chronically poor.

Ownership of physical and human capital make households less likely to be chronically

poor. Larger household size and dependents in the household push families towards

chronic poverty. Increase in number of working members in the family bring in more

income and reduce the chances of households being chronically poor. Given that

Bangladesh is an agrarian society and faces yearly floods, it is not surprising that

households with heads employed in the trade and self-employment sectors are less likely

to be chronically poor compared to those in the agricultural sector. Long term

investments in human and physical assets clearly help households out of chronic poverty.

Apart from household size, dependency ratio, number of working members, and land

ownership, the transient poor are characterized by their access to credit. Credit access

and remittances explain transient poverty better. Our models are not able to characterize

the transient poor as well as the chronically poor.

After having studied the poor and their characteristics, we seek to study how

individuals interact and operate within a family or household. We asses intra-household

dynamics (e.g., variations in household bargaining behaviors) with a focus on the

household’s expenditure patterns. Receipt of credit is taken as the measure of bargaining

between the head and the spouse. Food and non-food share equations were individually

estimated using random effect OLS and Tobit models to test if participation in credit

iv

markets influences food and non-food expenditure shares. Endogeneity corrections were

incorporated whenever tests indicated an endogenous relationship between total

household consumption and a particular expenditure share. 2SLS models and

simultaneous Tobit models were used to correct for endogeneity between the expenditure

shares and total expenditure. Our results indicate that more men compared to women

participate in the credit market. As is typical of any rural-developing economy,

household expenditure share is highest for food. Amount borrowed by the household

head has effects on food expenditure, adult goods and education expenditure. Amount of

credit taken by the household head negatively affects food expenditure and positively

affects share spent on adult goods. The negative effect on food expenditure has policy

implications related to nutritional intake of children in the household. Women and girls

in the household may also suffer from resultant nutritional deficiencies. Women’s use of

credit has a positive impact on expenditure on children’s goods, durable goods, education

and housing. Results show that resources in the hands of women have implications for

improvement in child outcomes, especially educational outcomes. The positive and

significant impact of spouse’s credit on housing share indicates that resources in the

hands of women also go towards improvement in household and related outcomes. We

also find that households are more likely to spend in round 2 and round 3 than in round 1

on food, education and personal care and more likely to spend on adult goods, children’s

goods, durable goods, fuel, health and housing in round 1 than in round 2 or 3.

v

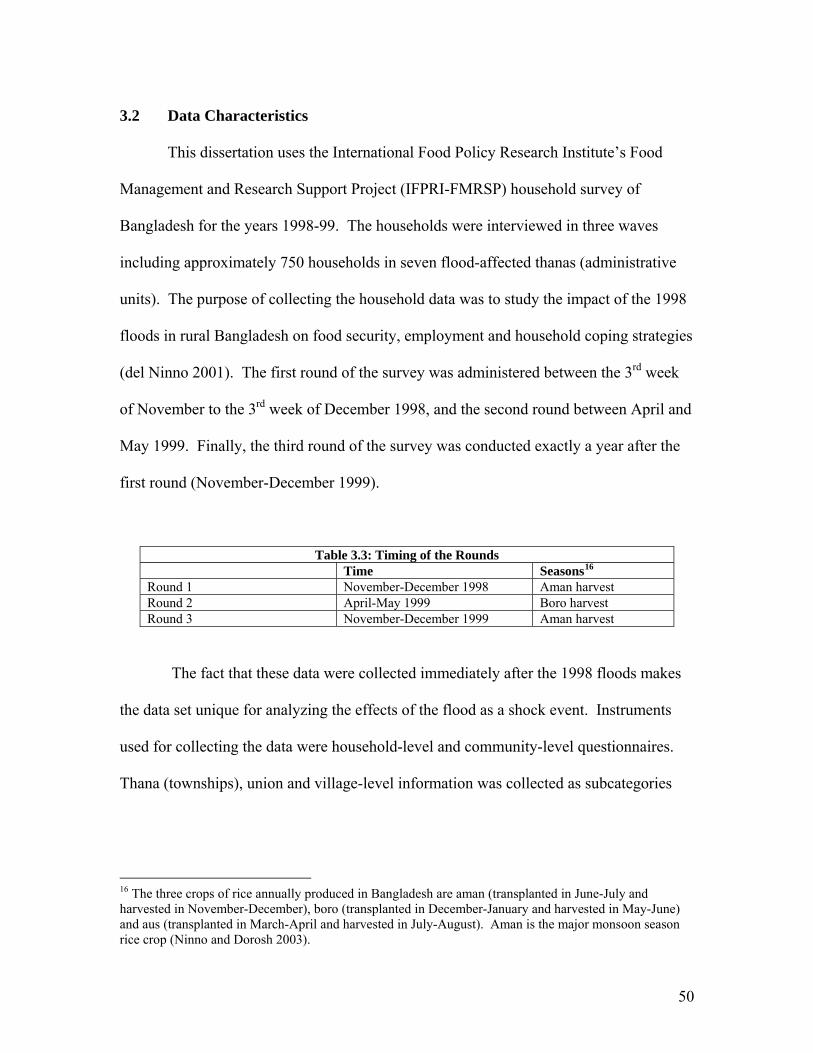

Table of Contents List of Tables viii List of Figures ix Acknowledgements x 1 Chapter 1: Research Problem 11.1 Introduction 11.2 Poverty and Vulnerability to Shocks 31.3 Shocks in Bangladesh 71.4 Poverty in Bangladesh 81.5 Consumption Smoothing 111.6 Gender and Poverty 131.7 Study Objectives 141.8 Organization of the Dissertation 16 2 Chapter 2: Literature Review and Theoretical Framework 172.1 Introduction 172.2 Poverty Dynamics 182.2.1 Definition of Chronic and Transient Poverty 192.2.2 Measuring Chronic and Transient Poverty 202.2.3 Empirical Studies 222.2.4 Characteristics of the Chronically Poor 252.2.5 Characteristics of the Transient Poor 262.3 Intrahousehold Resource Allocation Models 272.3.1 Unitary Household Model 272.3.2 Agricultural Household Models 302.3.3 Collective Models 332.3.4 Cooperative Model 332.3.5 Cooperative Bargaining Models 362.3.6 Non-Cooperative Model 42 3 Chapter 3: Data and Descriptions 443.1 Country of Study: Bangladesh 443.2 Data Characteristics 503.2.1 Sampling Procedure 533.3 Research Trip to Bangladesh, February 2005 543.4 Data Description 573.4.1 Regional Variations 61 4 Chapter 4: Methods 664.1 Poverty Dynamics 664.2 Measurement of Transient and Chronic Poverty 674.2.1 Approach I 674.2.1.1 Estimation Technique 684.2.2 Approach II 69

vi

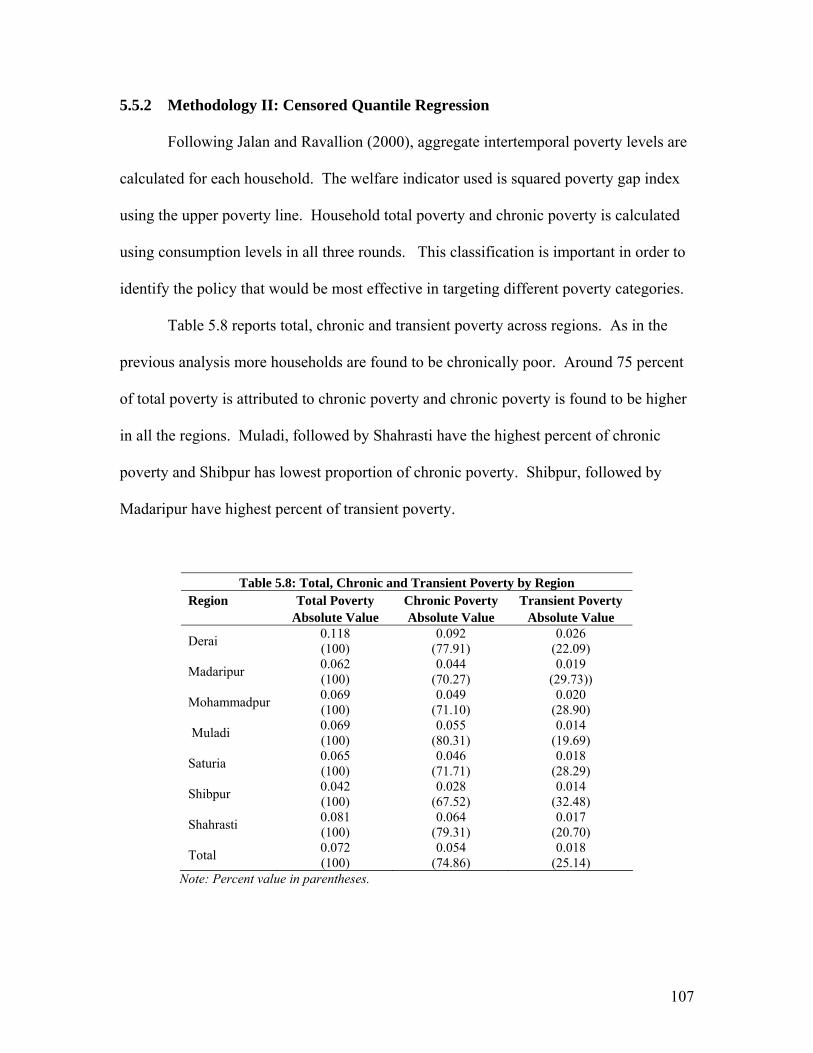

4.2.2.1 Estimation Technique 704.2.3 Distinguishing Between Approaches 734.3 Poverty Lines 744.4 Household Expenditure and Credit 754.4.1 Fixed Versus Random Effects 764.4.2 Empirical Framework 774.4.3 Econometric Issues 79 5 Chapter 5: Poverty Dynamics Results 835.1 Introduction 835.2 Descriptive Analysis 845.2.1 Incidence of Poverty 845.2.2. Time-Specific Profile of Poverty 865.3 Stochastic Dominance (First-order) Test 905.4 Receiver Operating Characteristic (ROC) Analysis 915.5 Econometric Analysis: Poverty Dynamics 955.5.1 Methodology I 955.5.1.2 Results from Multivariate Analysis 1025.5.2 Methodology II: Censored Quantile Regression 1075.6 Conclusion 110 6 Chapter 6: Household Expenditure and Credit as

Bargaining Measure 1116.1 Introduction 1116.2 Credit Availability 1126.3 Results 1146.3.1 Descriptive Statistics 1156.3.2 Credit and Household Expenditure 1226.3.3 Amount of Credit and Household Expenditure 1236.3.4 Credit Participation and Household Expenditure 130 7 Chapter 7: Conclusions 1357.1 Introduction 1357.2 Policy Implications 1417.3 Future Research 142 Reference 144

vii

List of Tables

Table 1.1 Types of risks faced by the households 4Table 1.2 Policy instruments for risk reduction 5Table 1.3 Trends in poverty and inequality in the 1990s in Bangladesh 10Table 2.1 Five-tier classification of the poor 21Table 2.2 Studies decomposing the poor into relevant categories 24Table 3.1 Country profile 44Table 3.2 Division profile 48Table 3.3 Timing of the rounds 50Table 3.4 Summary of the content of the household and community-level

questionnaire 52

Table 3.5 Selected Thanas 53Table 3.6 Demographic characteristics of sample of households in rural

Bangladesh, 1998-99 59

Table 3.7 Financial Asset ownership of sample households in rural Bangladesh, 1998-99

60

Table 3.8 Amount of credit taken by gender and region 65Table 4.1 CBN region poverty lines 75Table 5.1 Consumption expenditure and poverty 85Table 5.2 Number of periods poor 86Table 5.3a Occupation of the household head and poverty measures 87Table 5.3b Educational attainment of the household head and poverty measures 88Table 5.3c Age and gender of the household head and poverty measures 89Table 5.4 Area under the ROC curve for individual poverty indicators and over

all model using upper poverty line 94

Table 5.5 Number of poor in Bangladesh by poverty categories 96Table 5.6 Characteristics of sample households in rural Bangladesh 100Table 5.7 Estimates and marginal effects from multinomial logistic regression:

persistent and sometimes poor 105

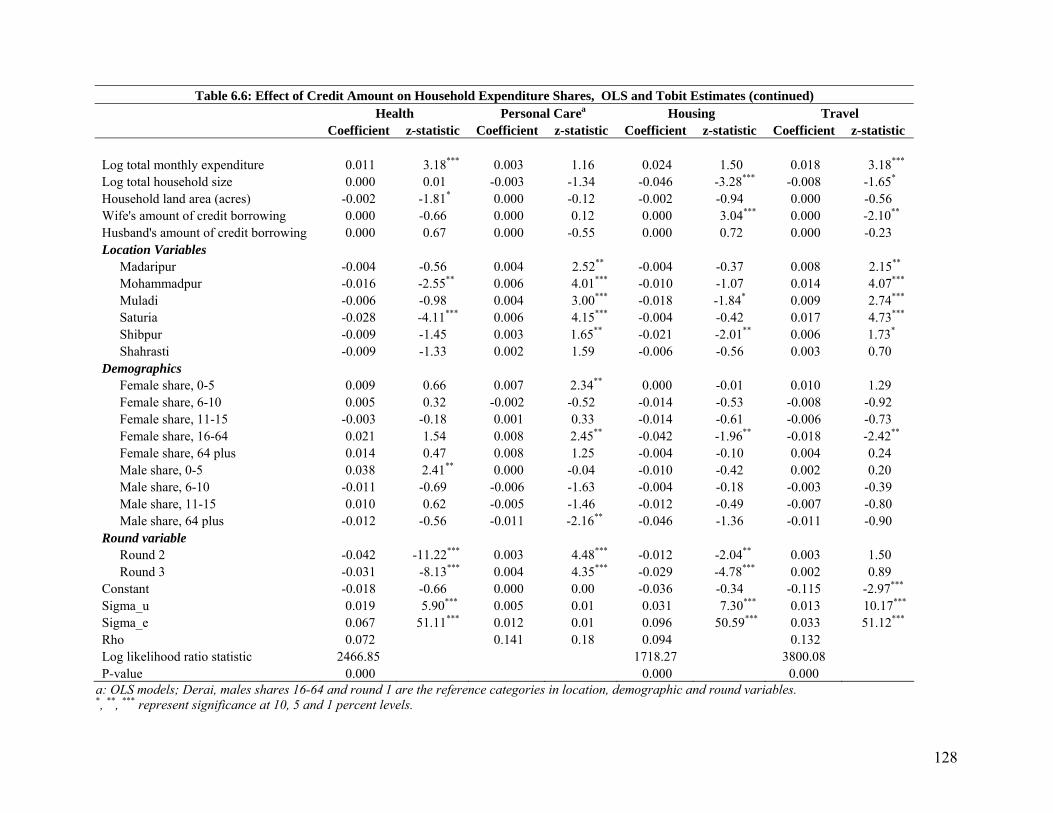

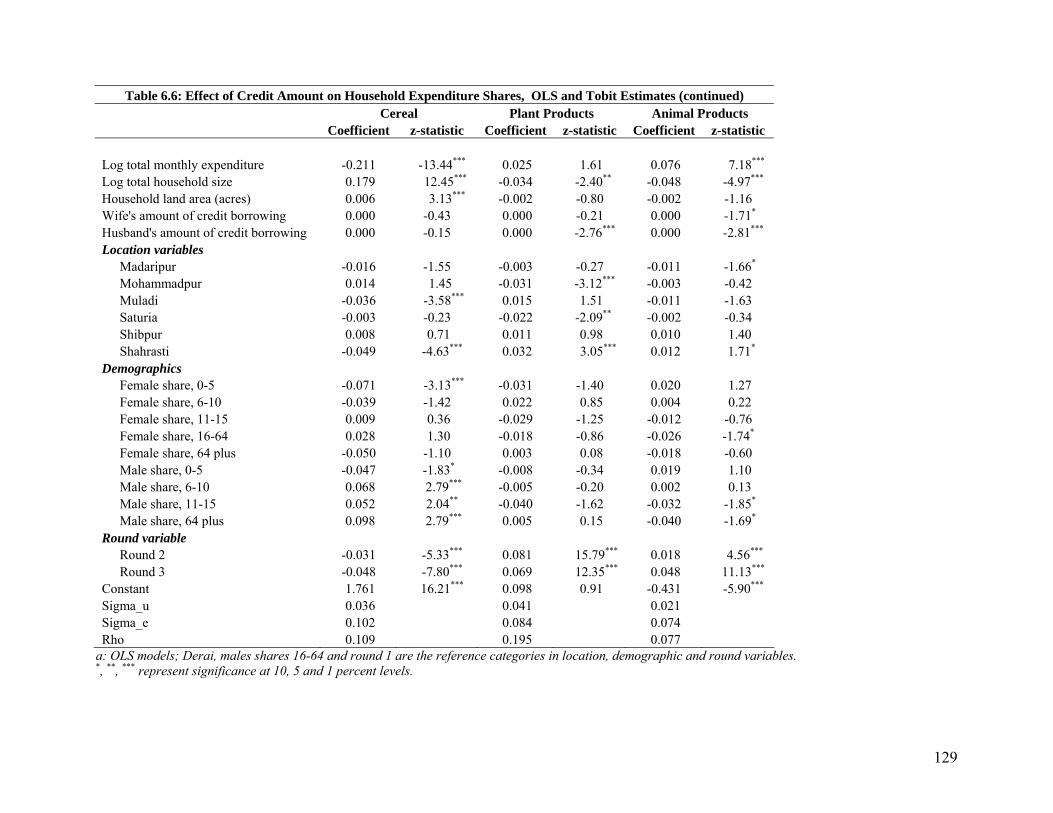

Table 5.8 Total, chronic and transient poverty by region 107Table 5.9 Censored quantile regression results (85th quantile) 109Table 6.1 Number of households in which men, women or both take loans 116Table 6.2 Formal and informal loans amount by head and spouse 117Table 6.3 Use of informal credit (%) 120Table 6.4 Use of formal credit (%) 121Table 6.5 Mean and standard deviations 122Table 6.6 Effect of credit amount on household expenditure shares, OLS and

Tobit estimates 126

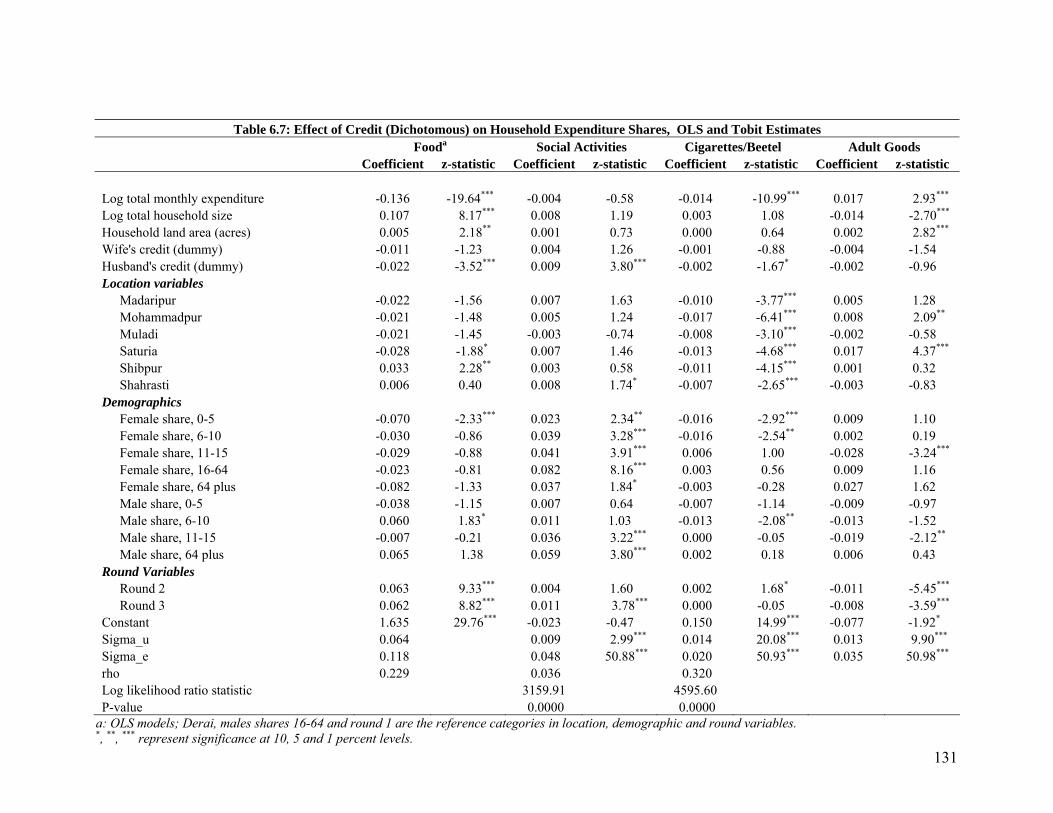

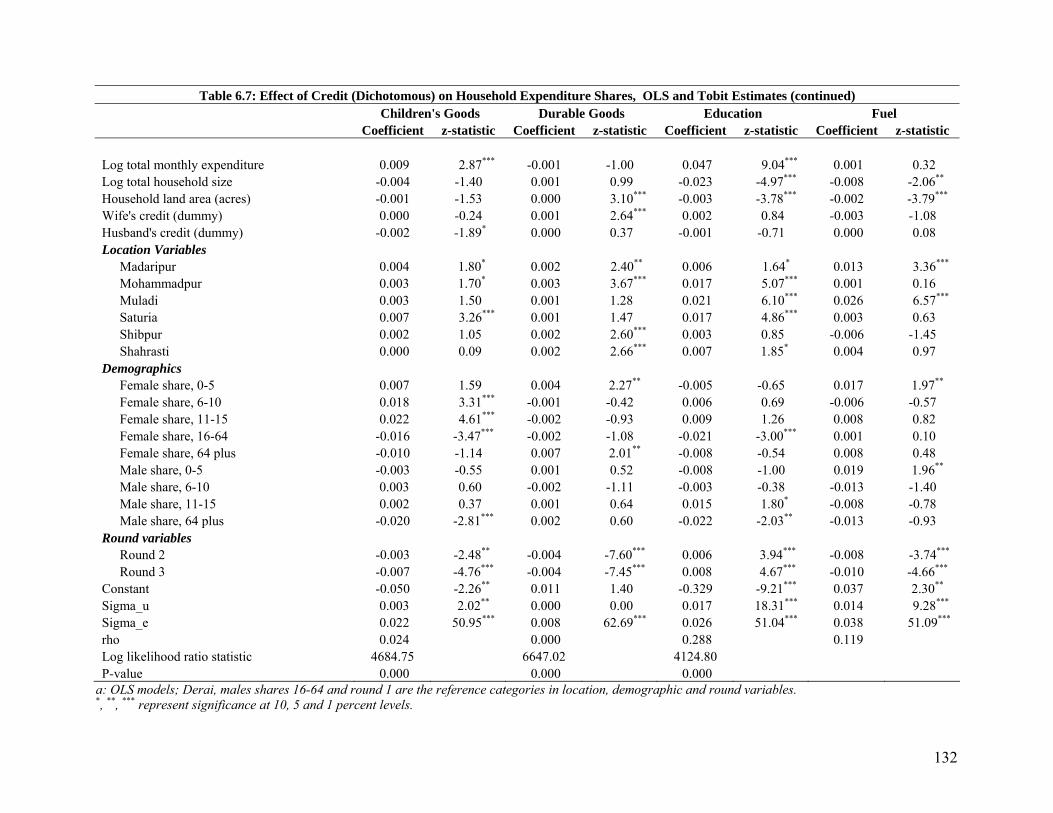

Table 6.7 Effect of credit (dichotomous) on household expenditure shares, OLS and Tobit estimates

131

viii

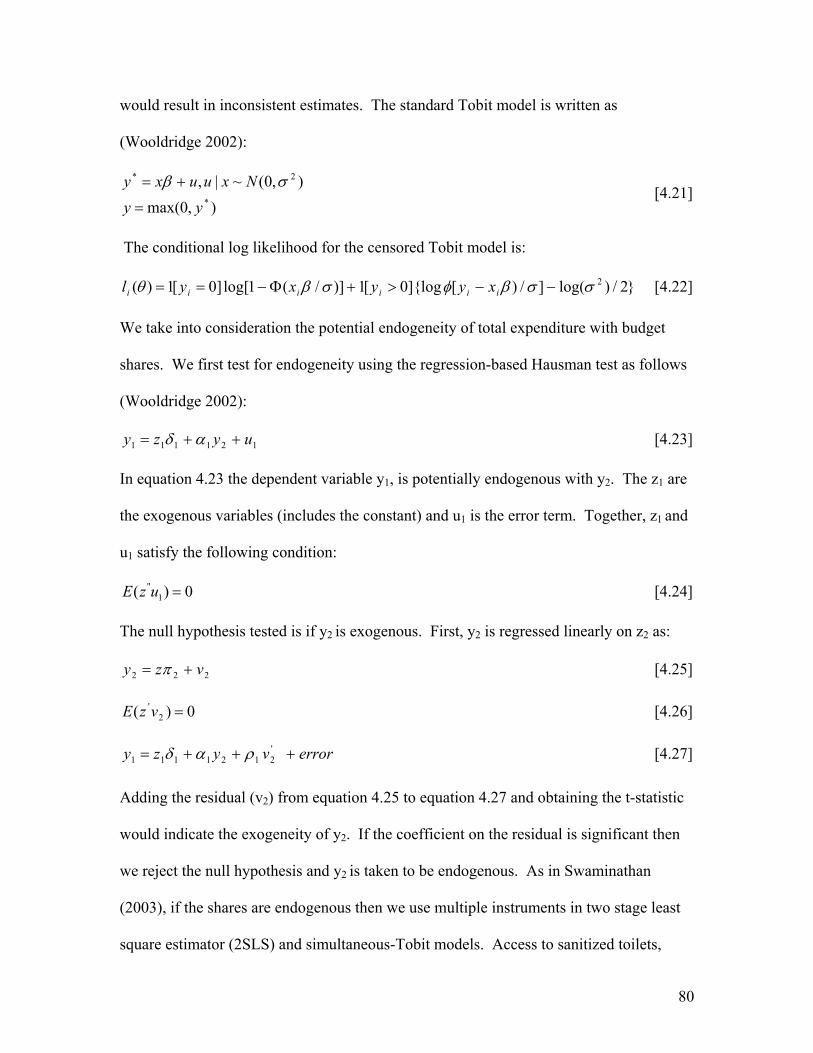

List of Figures

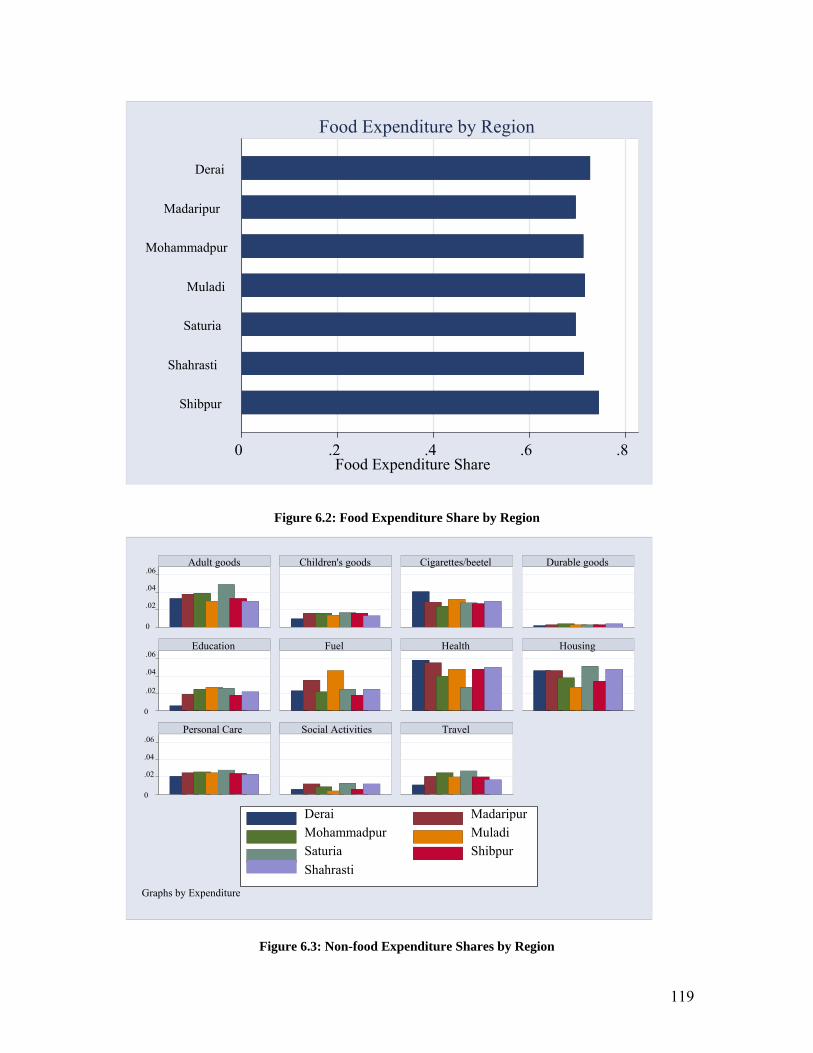

Figure 3.1 Political map of Bangladesh 45Figure 3.2 Flood affected area in Bangladesh 47Figure 3.3 Administrative divisions of Bangladesh 49Figure 3.4 Mean Consumption levels by lower poverty line 61Figure 3.5 Head count rate calculated using the lower poverty line 63Figure 3.6 Poverty gap ratio calculated using the lower poverty line 64Figure 3.7 Squared poverty gap ratio calculated using the lower poverty line 65Figure 5.1 Stochastic dominance curve 91Figure 5.2 ROC curve for poverty models 93Figure 6.1 Credit receipt of household head and spouse 117Figure 6.2 Food expenditure share by region 119Figure 6.3 Non-food expenditure shares by region 119

ix

Acknowledgements

I express my sincere gratitude to my advisor Prof. Jill L. Findeis for making this

dissertation possible. She has trained me to be a good researcher and also helped me

become a better person. Her deep commitment and optimism to research has been a

constant source of inspiration. I am grateful to each of my committee members; Profs.

Gretchen Cornwell, Bee-Yan Roberts, Carolyn Sachs, and Steve Smith for their support

and help. I would especially like to thank Prof. Cornwell for encouraging me to

undertake a qualitative study in Bangladesh. This study was funded by grants from the

Office of International Programs, College of Agricultural Sciences; Population Research

Institute; Women in Science and Engineering Institute; and the Department of

Agricultural Economics and Rural Sociology. The focus group discussions would not

have been possible without the help of Bangladesh Institute of Development Studies and

in particular Mr. Mohammad H.R. Bhuyan. I have also benefited from numerous

discussions with Hema and Tesfayi. I am extremely grateful to Prof. Francis Dodoo for

providing me with funding during the final stages of my dissertation.

I would like to thank my parents, Gita and Jayaraman for encouraging me to come

to Penn State and pursue my dream. They have prayed for my success and happiness. I

am grateful to my husband Chandrasekhar for all the help and support. Life in State

College would not have been fun without my good friends: Abhiroop, Priya, Smita, Ram,

Viji and Julia. I would also like to mention Meenakshi, Rajesh, Vijay and Anuja for

helping me at every stage. Finally, a word of thanks to Durga Athai for constant supply

of goodies!

x

1

Chapter 1

Research Problem

1.1 Introduction

South Asia has the largest concentration of the worlds’ poor1, with over half a

billion people surviving on less than a dollar a day. One of the Millennium Development

Goals (MDG) is halving the proportion of the world’s people whose income is less than

one dollar a day and the proportion of people who suffer from hunger by the year 2015

(OECD 2001). The success of poverty alleviation programs in South Asia is critical if

this MDG is to be met. Within South Asia, Bangladesh has the highest incidence of

poverty and only India and China have larger numbers of poor people. It is estimated

that nearly half of Bangladesh’s population of 135 million people live below the poverty

line (World Bank 2003a).

The United Nation’s General Assembly declared 1996 as the International Year

for the Eradication of Poverty. This was done "recognizing that poverty is a complex and

multi-dimensional problem with origins in both the national and international domains,

and that its eradication in all countries, in particular in developing countries, has become

one of the priority development objectives for the 1990s in order to promote sustainable

development.” (United Nations’ General Assembly Resolution 48/183 1993: p. 1). The

World Bank Group defines poverty as a multidimensional phenomenon where to be poor

not only means to be hungry and to lack access to shelter and resources but also means to

be illiterate, have poor health, not receive adequate nutrition and be vulnerable to shocks,

violence and crime. Not being in poverty entails individuals leading a life free from 1 Poverty is still a global problem in the 21st century, with 2.8 billion people living on less than $2 a day and 1.2 billion living on less than $1 a day (World Bank 2001b).

2

anxiety (World Bank 2001a, OECD 2001). Poverty has also been defined as the

combination of two interacting deprivations, namely physiological and social (Hazell and

Haddad 2001). Physiological deprivation includes deprivation resulting from lack of

income, food, education, shelter, sanitation and health. It can be quantified, and

household-level data capturing physiological deprivation are frequently collected and

readily available. Social deprivation is difficult to quantify because it includes elements

such as autonomy, time information, dignity and self-esteem (Hazell and Haddad 2001).

The traditional method of measuring poverty is to use the consumption or income

concept (defined as income poverty). An individual is deemed poor if his/her

consumption or income falls below the set minimum. The poverty line sets this

minimum standard specific to each society (Lipton and Ravallion 1995). Poverty has

different implications for individuals, families and societies. The International Labor

Organization defines different levels of poverty: individual, family and society-level

poverty (ILO 2003). Poverty results in poor health, lower working capacity, lower

productivity and a shorter life expectancy among individuals, and for families it leads to

inadequate schooling and income, early parenthood, poor health, and often early death.

At the societal level, poverty is an impediment to growth, stability and sustainable

development.

According to Hulme and Shepherd (2003), policy makers often define the poor as

those individuals who have not been integrated into the market economy and policy goals

often tend to view the poor as belonging to a single homogeneous category. Further,

policy makers tend to focus on only those poor whom the market can help (Hulme and

Shepherd 2003). Given that poverty alleviation is one of the most important challenges

3

faced by the international community today (ILO 2003), an understanding of the

dynamics of poverty alleviation is critical to the formulation of appropriate policy.

Poverty measures such as the head count ratio2 are static measures that are useful for

gauging the prevalence of poverty but do not indicate the severity of poverty or

fluctuations in economic welfare indicators over time including (but not limited to)

income and consumption.

1.2 Poverty and Vulnerability to Shocks

It is clear that one of the most important aspects of poverty is vulnerability. The

poor are the most vulnerable to health hazards, economic downturns, natural

catastrophes, and even man-made violence (World Bank 2001b). The World Bank

defines vulnerability as the likelihood of being affected by shocks, which have negative

impacts on the income and consumption of poor households. Further, households in most

developing countries face a high level of income variability due to factors beyond their

control, and their poverty makes them particularly vulnerable to shocks.

Shocks can be common or idiosyncratic. Common (or aggregate) shocks are

experienced by everyone in a particular group, community or geographical region while

an idiosyncratic shock affects only a particular individual or household (Dercon 2001a).

2 The most basic measure of poverty is the head count, which is the count of the poor below the poverty line. The head count index is the head count of those in poverty as the fraction of the total population. Other measures are the poverty gap index and the squared poverty gap index (Ray 1998). The depth of poverty is measured by the poverty gap index that calculates the average income shortfall from the poverty line. The squared poverty gap index measures the severity of poverty taking into account both distance separating the poor from the poverty line and income inequality (Ray 1998). These measures can be represented using the following equation where z is the poverty line, y is per capita expenditure and N is population size (World Bank 2002b): Pα= Σ [(z-y)/z]α/N with α = 0, 1 or 2, where α = 0 gives the head count index, α = 1 gives the poverty gap index and α = 2 gives the squared poverty gap index.

4

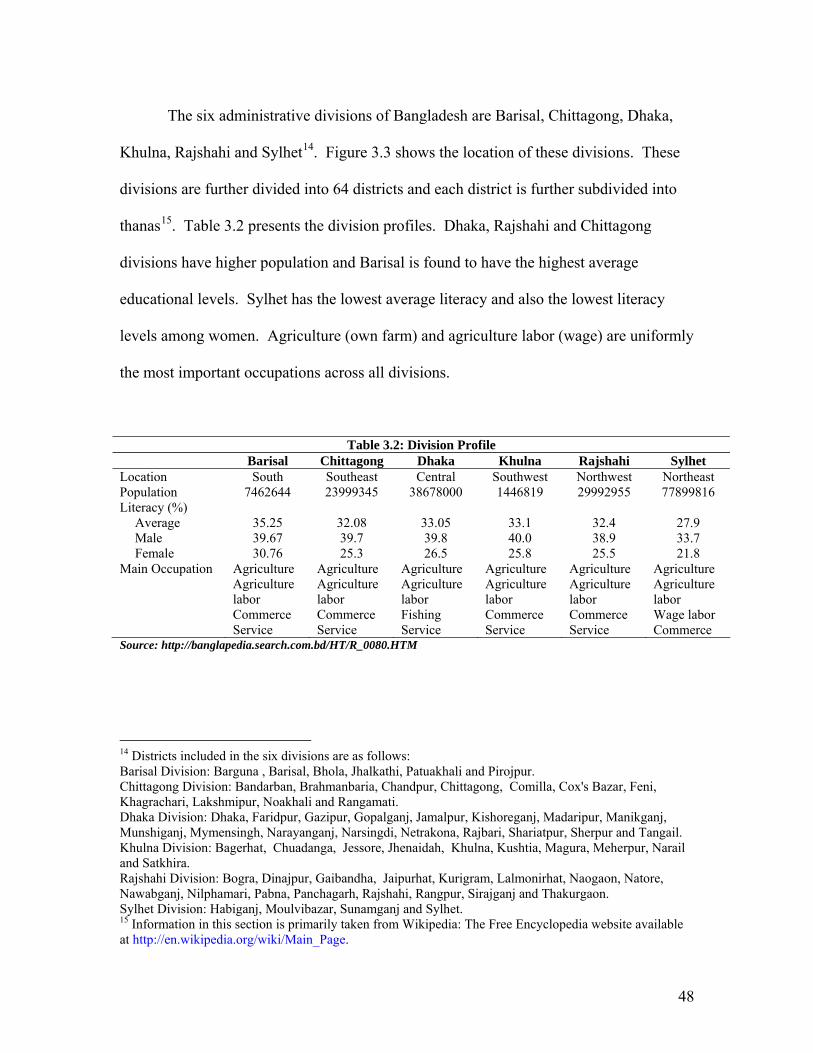

Table 1.1 categorizes the types of risks faced by individuals, households, communities

and geographical regions. Risks can be classified based on the level at which they occur

(micro, meso and macro) and can also be classified on the basis of type: natural, health,

social, economic, political and environmental (World Bank 2000). At the micro level,

individuals or specific households face a particular set of micro-level shocks focused at

the individual or household level, e.g., old age or domestic violence. Meso-level shocks

include shocks to groups of households or villages (for example, excessive rainfall,

landslides and epidemics), and national and international shocks are best classified as

macro shocks (World Bank 2000).

Table 1.1: Types of Risks Faced by Households Type of risk Risk affecting

individual or households (micro)

Risk affecting groups of households or

communities (meso)

Risk affecting regions or nations (macro)

Natural Rainfall, landslide, volcanic eruption

Earthquake, flood, drought, high winds

Health Illness, injury, death, disability, old age,

Epidemic

Social Crime, domestic violence

Terrorism, gang activity Civil strife, war, social upheaval

Change in food prices, growth collapse, hyperinflation, balance of payments, financial or currency crisis, technology shock, terms of trade shock, transition costs of economic costs

Political Riots Political default on social programs, Coup d’etat

Natural disasters Epidemics Illness, disability Old age Economic crises √ √ Labor market risk √ √ Harvest failure, food price

√ √ √

Crime & violence Environmental resettlement

√

Source: World Bank 2002a: p. 15.

6

Table 1.2 suggests potential policy instruments to reduce risks. These instruments

promote growth, increase the quality of human capital and reduce poverty. Public

awareness could play an important role in helping individuals and households to cope

with natural disasters, epidemics, crime and violence, and environmental resettlement.

The table also indicates that having a sound health, education and macro-economic

infrastructure provides a cushion against various shocks and risks such as economic

crisis, crop failure, labor market risks and epidemics (World Bank 2002a).

Kochar (1995), while analyzing idiosyncratic crop shocks faced by agrarian

households in India, found that well-functioning labor markets and not credit markets

helped farmers to smooth consumption. These households were able to increase the

number of hours of work and thereby avoid depleting their savings and the selling off of

assets. Dercon and Krishnan (2000) observed high seasonal variability in consumption

and poverty in short-panel data from Ethiopia. They attribute the variability to the

presence of shocks. Households were found to be prone to both common shocks

(rainfall) and idiosyncratic shocks (household-specific crop and livestock shocks).

Dercon and Krishnan (2000) found that poverty transitions during the period under study

could be explained by people’s vulnerability to shocks and seasonal incentives in terms

of prices and employment opportunities that affected household consumption.

Households employ various coping strategies once affected by a shock, as they

attempt to return to their original level of consumption. Disinvestment is a popular

means of coping. Liquid assets such as jewelry are initially disposed, followed by more

productive assets, making it increasingly difficult for households to return to their pre-

crisis state. Intensity, frequency and length of the shock have different impacts and

7

require different consumption-smoothing strategies. Consumption smoothing becomes

increasingly difficult for households with successive shocks (Alderman 1996). Poor

agrarian households are most susceptible to climatic shocks that directly affect crop

production and indirectly affect labor income. Household savings, asset accumulation,

income diversification, reallocation of labor, temporary migration and group-based risk

sharing are among the coping strategies used by households (Fafchamps 1999).

1.3 Shocks in Bangladesh

In 1998, Bangladesh experienced one of the largest floods of the century, which

covered more than two-thirds of the country and caused a loss of 2.04 million metric tons

of rice crop (del Ninno et al. 2001). While the overall economic impact of this flood was

less severe than previous flood occurrences and caused less damage than anticipated

(Benson and Clay 2002), the floods significantly damaged the crops and other productive

assets and further contributed to underemployment. Fortunately, trade liberalization in

the early 1990s made large-scale private food imports possible, and government food

transfers and non-governmental organization activities averted a major food crisis in

Bangladesh. However, there were short-term and medium-term negative impacts

attributable to the major flooding that occurred. In the short-term, consumption declined

and there were observed increases in the incidence of illness, especially among children.

The medium-term impact was an increase in private borrowing and negative impacts on

nutritional intake (del Ninno et al. 2003).

In Bangladesh, the agricultural sector and the labor market were the most

negatively affected after the 1998 flood. Households coped by growing alternative crops

8

and feeding alternative feed to livestock, and by finding alternative employment

opportunities. Private borrowing, used mainly for buying food, was the most widely used

coping mechanism relied on by Bangladeshi households (del Ninno et al. 2001).

Subsequent food insecurity resulted in households buying food on credit, reducing food

consumption, and borrowing money to buy food. The resulting changes in food

consumption had health implications, especially among children: an increase in stunting

and wasting among Bangladeshi preschoolers was observed (del Ninno et al. 2003).

Admittedly, shocks are an integral part of a developing economy and policies

should be geared towards equipping the poor to cope. The standard policy prescriptions

aimed at poverty reduction typically focus on ways to improve the mean utility of a poor

household. In contrast, policies that reduce the variance of households’ well-being over

time are becoming increasingly popular. Here a distinction is being made between

policies aimed at reducing chronic poverty and those to reduce transient poverty. The

World Bank (2002a) recommends a social protection strategy that extends “beyond the

traditional poverty reduction measures, to focus on creating opportunities for households

to manage risk better, primarily through a variety of instruments that perform the role of

safety nets” (World Bank 2002a: p. vi).

1.4 Poverty in Bangladesh

Bangladesh has received considerable international focus because of its high

density of population and low income. It is recognized as one of the most disaster-prone

countries in the world (Benson and Clay 2002). These factors make Bangladesh one of

the most vulnerable societies in the world. From the time of its independence in 1971,

9

Bangladesh has made considerable progress on all fronts (World Bank 2003b). The

country has achieved commendable reductions in population growth rates, child mortality

and child malnutrition (World Bank 2002b). There has also been successful disaster

management, increasing emancipation of women and growth of grass-root activism

through Non-government Organizations (NGOs) and Community-based Organizations

(CBOs) (World Bank 2003b).

There has been a reduction in both ‘income poverty’ and ‘human poverty’ in

Bangladesh since independence3. Human poverty in Bangladesh has declined at a faster

rate than income poverty in the past two decades but income poverty reduction has been

faster in the 1990s compared to the 1980s. Overall income poverty has declined at the

rate of 1 percent per annum (World Bank 2003b). Despite this progress, there has also

been an increase in inequality, both income and gender, during this period.

The difference in poverty between the poor and the poorest group is stark, where

45 percent of the poor live in extreme poverty4. Further, extreme poverty is higher

among female-headed or female-managed households. Table 1.3 shows that while all

poverty measures declined from 1991-92 to 2000, the Gini index of inequality indicates

an increase in income inequality in Bangladesh over this time period (World Bank

2003b).

3 Taking into account the multidimensionality of poverty, it is possible to categorize it into income poverty and human poverty. Income poverty measures poverty in quantitative terms. Over the 1990s, there has been increase in consumption expenditure, that is, a decline in income poverty (World Bank 2003b). The concept of human poverty was first defined in UNDP’s Human Development Report in the year 1997. It focuses on what people can or cannot do. The human poverty index captures health, literacy and economic provision deprivation (UNDP 2000). 4 Extreme poverty is defined as taking less than 1800 Kcal as per the direct calorie measure (World Bank 2003b).

10

Table 1.3: Trends in Poverty and Inequality in the 1990s in Bangladesh 1991/92 2000 Change per year (%)

Headcount Rate National Rural Urban

58.8 44.9 61.2

49.8 36.6 53.0

-1.8 -2.2 -1.6

Poverty Gap National Rural Urban

17.2 12.0 18.1

12.9 9.5

13.8

-2.9 -2.5 -2.8

Squared Poverty Gap National Rural Urban

6.8 4.4 7.2

4.6 3.4 4.9

-3.8 -2.7 -3.8

Gini Index of Inequality National Rural Urban

0.259 0.307 0.243

0.306 0.368 0.271

2.1 2.3 1.4

Source: BBS, Preliminary Report of Household Income and Expenditure Survey 2000, Dhaka, 2001 and World Bank, op.cit.(World Bank 2003b).

Roughly half of Bangladesh’s population still lives in extreme poverty (World

Bank 2002b). Poverty declined by 9 percent over 1990-2000 but the absolute number of

poor remained stable because of population growth. It is the eighth most populous

country in the world, with a total population of 135.7 million and a population growth

rate of 1.7 percent per annum in 2002 (World Bank 2004).

There have also been changes in the structural composition of the Bangladeshi

economy. During the 1990s, the share of agriculture in the Gross Domestic Product

(GDP) declined and that of the service and manufacturing industry sectors increased.

Structural adjustments in terms of trade liberalization since the 1980s brought about

macroeconomic stability, improved fiscal and monetary management and encouraged

private sector investment in the economy (Benson and Clay 2002). The question

becomes, given these important changes in Bangladesh, how can the vulnerability of

these households be reduced so as to better adjust to exogenous shocks. Among

Bangladesh’s poor, this is a critical question.

11

1.5 Consumption Smoothing

Provision of a safety net should include availability of credit to the rural

households. Ray (1998) divides credit requirements into fixed capital, working capital

and consumption credit. He defines fixed capital as the credit required for investment in

new production units which could be used to cover the fixed cost of the units. Working

capital includes costs of day-to-day running of the unit and finally, consumption credit

includes credit needed by the poor to smooth consumption due to shocks. This type of

credit need arises in agrarian societies where seasonality dictates earnings of the

households. Among the consumption smoothing mechanisms, consumption credit is

most prominent in the developing world and most of it is informal (Fafchamps 1999).

Credit could come from formal or informal sources. Formal sources include government

banks, commercial banks and NGOs and informal sources include borrowing from a local

money lender, landlord, friends and neighbors. Informal credit markets are found to

charge high, exploitative interest rates but play an important role in rural credit markets.

Other income-smoothing mechanisms used by households are remittances and transfers

from family, friends and other institutions such as NGOs. These could be viewed as

returns to social capital (Dercon 2001a).

Policy makers in the developing world have found it difficult to provide access to

credit to small rural borrowers and microfinance is an attempt to reach the poor deprived

of financial services (UNCDF 2005). In Bangladesh, microcredit programs play an

important role and these programs focus on the poor. An estimated 13 million poor

people benefit from microfinance and credit availability in Bangladesh (UNCDF 2005).

NGOs have become actively involved in the microfinance sector. The four large

12

institutions that play a crucial role in this sector are BRAC (Bangladesh Rural

Advancement Committee), Grameen, Association for Social Advancement (ASA) and

Proshika (Zaman 2004).

Zaman (2004), in his exposition of the evolution of the microfinance sector in

Bangladesh, observes that the earliest microcredit models came about in Bangladesh in

the 1970s in an attempt to rehabilitate people post-independence. The 1980s witnessed

growth in NGO in the provision of credit and which subsequently in the 1990s developed

into the ‘Grameen-model’ of credit delivery. The majority of borrowers are women who

are targeted by these programs. Individuals receive loans as members of a group. Group

liability ensures repayment and extending credit to women also has an element of

empowerment. Kabeer (2001), in her evaluation of empowerment potential of credit

programs in rural Bangladesh, finds improvement in household outcomes when women

are given loans but cautions that patriarchal society in Bangladesh is still a constraint for

women.

Focused leadership and supportive legal systems have contributed to the success

of the microcredit movement (Morduch 1999). It is argued that these formal financial

services do not reach the poorest of the poor. In Bangladesh, microfinance prominence is

lowest among the poorest group and highest among the second lowest quintile group

(Hashemi and Rosenburg 2006; Morduch 1999). These programs have improved the

lives of poor households but it is important to note that they are costly to implement and

need to be heavily subsidized (Morduch 1999).

13

1.6 Gender and Poverty

Individuals interact and operate within a family or household. To improve the

well-being of individuals, development policies not only have to take into account how

resources are allocated within the family or household but also the impact of this resource

allocation on individuals. This process of resource allocation and the resulting outcomes

are referred to as “intrahousehold resource allocation” (Haddad et al. 1997; Quisumbing

2003). Differential intrahousehold resource allocation has implications for inequality and

poverty among household members (Strauss and Beegle 1996).

Numerous studies have shown that equality of men and women in a society has

positive effect on growth of the economy, poverty alleviation and individual well-being

of household members. Productive assets in the hands of the women have led to

reduction in poverty levels and empowerment of women (World Bank 2002c).

Empowerment indicators include both participation in the political process and control

over household resources. Access to credit and financial resources are limited for women

especially in rural areas (Bamberger et al. 2002). Moreover, the intrahousehold resource

allocation literature supports the fact that transfer of resources improves the bargaining

position of women in the household and thereby improves resource allocation and child

outcomes.

As part of this research focus group discussions were held in Bangladesh. The

rationale for the focus groups was to explore not only the coping strategies employed by

the households during and after floods but also to see if there was evidence of any form

of bargaining within the household. These discussions raised a number of questions:

What decision making power did the wife have in the household? Did that affect

14

intrahousehold resource allocation? Did receipt of credit or any other form of resource

give her more power to make decisions in the household? Could the decisions taken in

the household be gender differentiated? The qualitative study was not only important in

understanding the social and cultural context in Bangladesh and therefore helped in better

interpretation of the empirical results but also indicated that receipt of financial help

could possibly increase women’s say in family matters. They also pointed that that

borrowing money especially from informal sources was one of the major coping

mechanisms employed by Bangladeshi households.

1.7 Study Objectives

Given this perspective, this research analyzes issues related to chronic and

transient poverty following a major catastrophic (flood) event using a short panel of

household data from Bangladesh. This analysis is at the household level where the

research examines how the poverty level changes and how poor and non-poor families

are different from each other. Households have been found to adjust to shocks such as

floods by borrowing, selling assets and altering expenditures (del Ninno et al. 2001).

Among these coping mechanisms, we focus on credit receipt by the household head and

the spouse and the resultant differential household-level outcomes. Here the focus is on

individuals in the household and an attempt is made to study how their interaction affects

household resource allocation. The data used in this study were primarily collected to

identify policy prescriptions for sustainable improvement in household food security in

the period following the 1998 Bangladesh flood. The specific research objectives are:

15

1 To identify the determinants of poverty in Bangladesh, with a specific focus on

differentiating those who experienced poverty following the 1998 flood in

Bangladesh and those who did not.

2 To determine the differences between those among the poor (identified in

objective 1) who are able to eventually escape poverty following the flood (the

transient poor) versus those unable to leave poverty (chronic poor). It is

hypothesized that the poor are heterogeneous and within the poverty group those

who endure poverty for a sustained period of time are characteristically different

from those who move into and out of poverty.

3 To understand how intrahousehold dynamics (e.g., variations in household

bargaining behaviors) lead to differences in outcomes of specific interest (e.g.,

food expenditure). The household bargaining model will be used to analyze the

effects of receipt of credit on consumption choices within these poor households

following the flood event. The focus is on the household’s expenditure patterns.

The study hypothesizes that receiving credit from formal and informal sources

will affect decision-making capacity of women in Bangladeshi households. This

in turn is expected to have implications for child health and nutritional outcomes.

It is important to point out that the study is not looking at how the credit amount

is spent by the receiver but instead assesses how household expenditure patterns

are associated with credit receipt by the husband and wife. Availability of data on

credit receipt by individual members of the household enables us to look at

gender differentials resulting from transfer of resources in the hands of women.

16

We also restrict our analysis to male-headed households since there are too few

female-headed households in our data.

1.8 Organization of the Dissertation

Following this introduction, Chapter 2 of the dissertation provides a review of

literature relating to poverty and the ability of households to cope with exogenous shocks.

It also addresses the bargaining literature and the theoretical model relevant for the

agricultural household. Chapter 3 presents country and data descriptions. Chapter 4

outlines the methods and the estimation strategy used in the dissertation. Chapter 5 and

Chapter 6 present the results of the analysis. Finally, Chapter 7 describes the research

conclusions and policy implications.

17

Chapter 2

Literature Review and Theoretical Framework

2.1 Introduction

The World Bank Group defines poverty as a multidimensional phenomenon

where to be poor not only means to be hungry and to lack access to shelter and resources

but also means to be illiterate, have poor health, fail to receive adequate nutrition and be

vulnerable to shocks, violence and crime. The poor can be divided into those who remain

poor continuously over time and those who enter and exit poverty from time to time. A

large proportion of the poor include people moving into and out of poverty (Baulch and

Hoddinott 2000). As noted in Section 1, the poor are the most vulnerable to health

hazards, economic downturns, natural catastrophes, and even man-made violence (World

Bank 2001a). The World Bank defines vulnerability as the likelihood of being affected

by shocks, which have negative impacts on the income and consumption levels of poor

households. Further, households in most developing countries face high income

variability due to factors beyond their control, and their poverty makes them particularly

vulnerable to shocks. Depending on how well households are able to cope, they could

remain in poverty or may be able to move out of poverty following the shock (Baulch and

Hoddinott 2000).

The coping strategies that result in consumption smoothing in response to a shock

reflect poverty dynamics5. Recent advances in computation coupled with the more

frequent collection of panel data at the household level have contributed to the study of

both the dynamics of poverty and the coping strategies that households use over time as

5 Poverty dynamics is defined as the movement into and out of poverty (Baulch and Hoddinott 2000).

18

they attempt to escape poverty. Recent studies of poverty, a topic widely covered in the

literature, have focused on the dynamics of poverty, including what it means to be in

poverty for the long term versus in the transient poverty state. At the same time, new

theories of household interactions have emerged in the economics literature, allowing

examination of intrahousehold effects. This section examines both of these topics – i.e.,

the recent literature that examines poverty dynamics, and in specific, chronic versus

transient poverty, and the literature on the new household models that focus on

intrahousehold behaviors.

2.2 Poverty Dynamics

The percentage of people living below the poverty line is an aggregate measure

that is useful in some respects but limited in others. A limitation of the aggregate

measures is their failure to provide any indication of how poor households are faring or

whether their economic status is changing over time. It is important to disaggregate the

poor to understand their circumstances and dynamics. It is critical to understand the

differences among the different types of households and individuals within households

who are classified as ‘poor’. One salient difference is the difference between those

households and individuals who move into and out of poverty versus those who fail to

move out of poverty over time. This calls for incorporating a dynamic perspective into

poverty analysis, with differentiation between the chronic and transient poor.

Households who experience poverty and deprivation for prolonged periods are

defined as chronically poor and those who move into and out of poverty (temporary) are

the transient poor (Hulme and Shepherd 2003). These two types of poverty require

19

different policy measures. Chronic poverty eradication measures include long-term

investments such as increasing human and physical capital and the returns to assets. On

the other hand, policies to help the poor cope with idiosyncratic shocks are appropriate to

tackle the problem of transient poverty. Understanding why households move into and

out of poverty can help to target the poor more effectively than assessing only static

welfare indicators; static measures may (wrongly) include those experiencing short-term

misfortunes but otherwise are not poor based on their permanent incomes or levels of

consumption. Similarly, excluding those experiencing only temporary spells out of

poverty but in fact who are in poverty the majority of the time is also a weakness (Baulch

and Hoddinott 2000). Baulch and Hoddinott (2000) emphasize that understanding factors

affecting poverty dynamics help in designing safety net policies and, most importantly,

help to target the vulnerable.

Finally, while income and consumption measures of poverty are often used to

study chronic and transient poverty, there is an increasing emphasis on adopting a

multidimensional approach in poverty studies by considering other measures such as

educational attainment, nutritional intake and ownership of assets in the analysis (McKay

and Lawson 2002).

2.2.1 Definition of Chronic and Transient Poverty

It is widely accepted that the poor are a heterogeneous group. Studies of poverty

dynamics generally treat a household as a single economic unit6. Jalan and Ravallion

(2000) define transient poverty as the poverty that is caused by variability in

6 Assumes a unitary model framework.

20

consumption. A household with mean consumption below the poverty line across all

periods is defined to be experiencing chronic poverty. Hulme and Shepherd (2003)

define the chronically poor as those who experience poverty for a period of five years or

more and transient poor as those who move into and out of poverty. They argue that the

five-year period is a significant length of time and studies show that individuals who are

poor for five years or more have a high probability of remaining poor for the rest of their

lives. The chronic poor suffer from persistent deprivation. The chronically poor are also

those who need external help to get out of the poverty trap and they remain poor despite

implementation of policies to tackle poverty (Aliber 2003). Chronic poverty also is

transmitted from one generation to another, and children within chronically poor

households are more likely to be caught in the poverty trap and likely to remain poor the

rest of their lives (Aliber 2003).

2.2.2 Measuring Chronic and Transient Poverty

Income and consumption7 measures at the household level are common measures

of chronic and transient deprivation and longitudinal or panel data sets are ideally suited

to study poverty movements or transitions8. However, the multidimensional definition of

poverty requires that other welfare indicators – for example, asset ownership, nutritional

intake, educational enrollment, the human deprivation index -- could be included to

provide a more inclusive measure of poverty.

Even households that are sometimes poor are heterogeneous. The question

becomes how to rigorously define the transient poor (Baulch and Hoddinott 2000). For 7 Also called metric welfare measure (Baulch and Hoddinott 2000). 8 Atleast a three-year panel data set is needed (Baulch and Hoddinott 2000).

21

example, using the definition that the chronically poor are poor continuously over time

and the transient poor experience at least one spell out of poverty, in five-year panel data,

a household classified as poor for four years would be categorized as transient poor but

then so would be a household that is poor just one year. Treating both households alike is

probably not reasonable. Hulme and Shepherd (2003) categorize poor as ‘always poor’,

‘usually poor’, ‘churning poor’, ‘occasional poor’ and ‘never poor’ (see Table 2.1). Both

income and non-income indicators are used in their categorization.

Table 2.1: Five-tier Classification of the Poor Aggregate category Specific category Definition Chronic poor

Always poor Usually poor

Those whose poverty score is below the poverty line for each period. Those whose mean poverty score over all periods is below the poverty line but not poor in every period.

Transient poor Churning poor Occasionally poor

Those with a mean poverty score around the poverty line and who are poor in some periods. Those with mean a poverty score above the poverty line and that have experienced at least one period of poverty.

Non-poor Never poor Those whose mean score is always above the poverty line.

Source: Hulme and Shepherd (2003).

The poverty literature delineates two approaches to study transitory and chronic

poverty using income or consumption data. First, the spells approach is used, where the

number or length of poverty spells experienced classifies the poor as chronic or transient

(McKay and Lawson 2002). A transition matrix can be used to provide information on

the proportion or number of people moving into and out of poverty using deciles,

quintiles or poverty lines, and also gives information about the poverty experiences of

22

households in the intervening period (Oduro 2002). Using this approach, Oduro (2002)

found that consumption measures are generally less variable compared to income

measure of poverty. This is because households have the ability to smooth consumption

over time. Therefore, the number of poor in the transient category increase when the

income measure of poverty is used and different welfare measure could yield different

estimates of transient and chronic poverty. The spells approach is plagued by

measurement error occurring in the process of collecting income and consumption data

(Hulme and Shepherd 2003). Difficulty in measuring the values of own production (as

well as problems recalling and imputing values) and in determining the revenue and cost

of farm and non-farm enterprises result in errors (Baulch and Hoddinott 2000).

A second approach, the components approach, decomposes the permanent component of

household income from its transitory variations. Households that have permanent

components below the poverty line are then defined as the chronically poor (McKay and

Lawson 2002).

It is recommended that to have a complete picture, the spells and component

approach based on income or consumption have to be complemented by the used of

qualitative studies. That is, there is a need to move beyond defining poverty in monetary

terms.

2.2.3 Empirical Studies

An important question is why some households are not able to move out of

poverty while others appear to move into and out of poverty over time – they escape

being poor but often fall back into poverty at least temporarily. Some studies have been

23

able to predict chronic poverty better than transitory poverty (Haddad and Ahmed 2003;

Baulch and Hoddinott 2000; Jalan and Ravallion 2000). Analysis of chronic poverty

across 25 countries shows that chronic poverty is spatially concentrated, affected by

demographic composition of the household and determined by human and physical

capital and labor markets (Yaqub 2002).

Jalan and Ravallion (2000) define total poverty as the sum of chronic and

transient poverty and decompose households into total, chronic and transient poor using

the squared poverty gap index. The censored quantile regression technique is used to

identify the determinants of both chronic and transient poverty. Their model is able to

predict chronic poverty better than transient poverty, with the determinants of chronic

and total poverty being similar. Haddad and Ahmed (2003), using a two-round panel

data set for Egypt, measure changes in per capita consumption among households. They

calculate squared poverty gap measures for each household and divide the sample

population into total, transient and chronically poor groups. The censored quantile

regression method is again applied to identify the determinants of chronic and transient

poverty. As was also true for Jalan and Ravallion (2000), their model predicts chronic

poverty better than transient poverty, with the determinants of total and chronic poverty

again being quite similar.

Kedir and McKay (2003) analyze three waves of household survey to study

chronic poverty in Ethiopia using total household expenditure per month as the welfare

indicator and the population is classified into ‘always poor’, ‘two-period poor’, ‘one-

period poor’ and ‘never poor’. Multinomial regression analysis indicates that household

24

composition, unemployment, lack of asset ownership, lack of education, ethnicity, and

the age and gender of the household head are important determinants of chronic poverty.

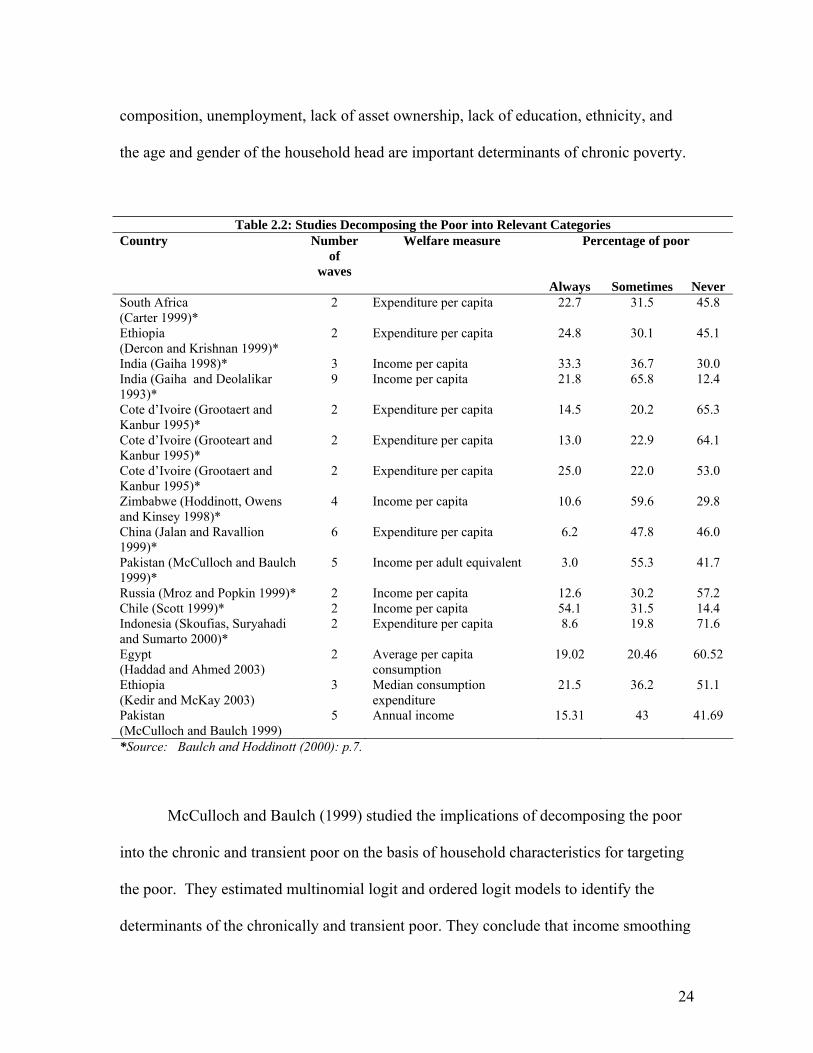

Table 2.2: Studies Decomposing the Poor into Relevant Categories Country Number

of waves

Welfare measure Percentage of poor

Always Sometimes Never South Africa (Carter 1999)*

2 Expenditure per capita 22.7 31.5 45.8

Ethiopia (Dercon and Krishnan 1999)*

2 Expenditure per capita 24.8 30.1 45.1

India (Gaiha 1998)* 3 Income per capita 33.3 36.7 30.0 India (Gaiha and Deolalikar 1993)*

9 Income per capita 21.8 65.8 12.4

Cote d’Ivoire (Grootaert and Kanbur 1995)*

2 Expenditure per capita 14.5 20.2 65.3

Cote d’Ivoire (Grooteart and Kanbur 1995)*

2 Expenditure per capita 13.0 22.9 64.1

Cote d’Ivoire (Grootaert and Kanbur 1995)*

2 Expenditure per capita 25.0 22.0 53.0

Zimbabwe (Hoddinott, Owens and Kinsey 1998)*

4 Income per capita 10.6 59.6 29.8

China (Jalan and Ravallion 1999)*

6 Expenditure per capita 6.2 47.8 46.0

Pakistan (McCulloch and Baulch 1999)*

5 Income per adult equivalent 3.0 55.3 41.7

Russia (Mroz and Popkin 1999)* 2 Income per capita 12.6 30.2 57.2 Chile (Scott 1999)* 2 Income per capita 54.1 31.5 14.4 Indonesia (Skoufias, Suryahadi and Sumarto 2000)*

2 Expenditure per capita 8.6 19.8 71.6

Egypt (Haddad and Ahmed 2003)

2 Average per capita consumption

19.02 20.46 60.52

Ethiopia (Kedir and McKay 2003)

3 Median consumption expenditure

21.5 36.2 51.1

Pakistan (McCulloch and Baulch 1999)

5 Annual income 15.31 43 41.69

*Source: Baulch and Hoddinott (2000): p.7.

McCulloch and Baulch (1999) studied the implications of decomposing the poor

into the chronic and transient poor on the basis of household characteristics for targeting

the poor. They estimated multinomial logit and ordered logit models to identify the

determinants of the chronically and transient poor. They conclude that income smoothing

25

policies are more appropriate for tackling the problem of transitory poverty while growth

policies designed to increase the mean income level help the poor to escape being

chronically poor. Table 2.2 provides a summary of selected studies of chronic and

transient poverty.

2.2.4 Characteristics of the Chronically Poor

Education is a powerful and important predictor of chronic poverty. Studies have

found that an increase in number of years of education decreases the probability of being

chronically poor (McCulloch and Baulch 1999; Jalan and Ravallion 2000; Aliber 2003;

McCulloch and Calandrino 2003). Human capital accumulation in Bangladesh is an

important form of asset holding for the poor, which equips them to participate in the

growth process (World Bank 2002b).

Larger households are more likely to experience chronic poverty. This is true

among households that have limited access to resources and assets. McCulloch and

Baulch (2000), Jalan and Ravallion (2000), Haddad and Ahmed (2003) and Aliber (2003)

in their study of Pakistan, China Egypt and South Africa, respectively, found this to be

true. Older household heads and female-headed households are also more likely to be

chronically poor (Aliber 2003). All things equal, the same is true for households with a

greater number of children, more members above the age of 60 and for households with

more disabled members.

Place of residence determines the opportunities and facilities available to the

households (McKay and Lawson 2002). Remote geographical locations are

disadvantaged in terms of access to resources. The likelihood of being persistently or

26

chronically poor in such locations is higher. McKay and Lawson (2002) also find that

chronic poverty is a major problem in rural areas because of lack of employment

opportunities and resources.

Lack of physical assets is associated with chronic poverty (McCulloch and Baulch

2000; Aliber 2003). Assets such as livestock and land help poor households not only

generate income but are also a form of investment. Poorer households commonly hold a

greater share of their assets in the form of liquid assets such as livestock and financial

assets (World Bank 2002a).

The sector of occupation of the household head is shown to be very important in

most studies. Haddad and Ahmed (2003), in their study of chronic and transient poverty,

report that being employed in the manufacturing, recreation or non-farm sectors

decreases the likelihood of being chronically poor as compared to being engaged in the

agricultural sector. Seasonal, casual and retrenched farm workers are also vulnerable

(Aliber 2003).

2.2.5 Characteristics of the Transient Poor

Some factors affect both chronic and transitory poverty but there are others that

are associated with transient poor alone. Poverty levels in general decline rapidly with

increases in education of the household head (World Bank 2002a). There is also a strong

negative association between transient poverty and educational attainment (Haddad and

Ahmed 2003; Jalan and Ravallion 2000). Jalan and Ravallion (2000) find higher

transitory poverty among smaller Chinese households. Adoption of new technology and

adverse price fluctuations can result in temporary poverty (McKay and Lawson 2002).

27

The adoption of new agricultural techniques involves risk taking on the part of farmers,

which, in turn, causes variability in their income. The study of Argentinean households

by Cruces and Wodon (2003) found that the risk of running a business made employers

vulnerable to transient poverty, and the provision of social security by the public sector

made households engaged in this sector more resistant to transient poverty.

2.3 Intrahousehold Resource Allocation Models

Individuals interact and operate within a family or household. To improve the

well-being of individuals, development policies not only have to take into account how

resources are allocated within the family or household but also the impact of this resource

allocation on individuals. This process of resource allocation and the resulting outcomes

are referred to as “intrahousehold resource allocation” (Haddad et al. 1997; Quisumbing

2003). Differential intrahousehold resource allocation has implications for inequality and

poverty among household members (Strauss and Beegle 1996).

2.3.1 Unitary Household Model

The traditional approach to intrahousehold resource allocation is the unitary

approach where the household is viewed as a single economic unit. Becker (1965)

proposed that the household, sharing a single set of preferences, maximized utility by

combining time, goods purchased in the market and goods produced at home. Becker’s

theory of time allocation assumes that households are both consumers and producers. As

producers, household combine nonlabor inputs and time using the cost minimization

approach and, as consumers, maximize their utility subject to prices and resource

28

constraints. Unitary models assume that all members of a household share the same

preference function and pool their resources. In Becker’s time allocation model,

households maximize the following utility function

U = U (Z1,…., Zm) ≡ U (f1,…., fm) = U (x1,….,xm; T1,…., Tm) [2.1]

where Zi are goods produced within the household, x1 is the vector of market goods, and

Ti is a vector of time inputs used in producing the ith commodity. The utility of the

household is maximized subject to:

1. Household production function which combines time and market goods to

produce goods:

Zi= fi (xi, Ti) [2.2]

The production function is characterized by fixed coefficients as:

T1 ≡ ti Zi [2.3]

xi ≡ bi Zi [2.4]

where ti is input of time required to produce one unit of household good (Z) and bi

is the input of market good required to produce a unit of household good (Z).

2. Goods constraint

∑m

tt xp1

= I = V + Tw ẅ [2.5]

where I is total income, V is other income, Tw denotes market work and ẅ is the

vector of wage rates.

3. Time constraint

Tc = T – Tw [2.6]

29

where T is the total time available during the day and Tc is the time spent on

consumption (leisure).

Equations 2.3, 2.4, 2.5 and 2.6 can be combined to yield the full-income constraint:

Σ (pibi+ t ẅ) Zi = V + T ẅ [2.7]

Households thereby make consumption and production decisions based on exogenous

factors, namely market prices, wages and non-earned income (Schultz 2001).

Apart from being applied to standard demand analysis, unitary models were

extended to include determinants of education, health, fertility, migration and labor

supply (Haddad et al. 1997). This approach is popular because it is straightforward and

household-level data are readily available. Attempts have been made to assess questions

of intrahousehold resource allocation within the unitary framework, despite its treatment

of households as ‘black box’ (Pitt 1997; Alderman and Gertler 1997). For example, Pitt

(1997) looks at household resource allocation using intrahousehold conditional demand

equations. These equations determine how allocations such as time and food to one

member affect allocations to others. This model requires prices of person-specific goods

for estimating demand equations. Absence of prices lead to issues of identification and

Pitt suggests solutions to overcome this problem. Further, Alderman and Gertler (1997)

use the unitary framework to show how gender plays a role in human capital investment

within households with different levels of resources. They find that the demand for

daughters’ human capital is more income and price elastic in cases where there is a son

preference. This was empirically tested in their study of Pakistan and expected

relationships were observed.

30

2.3.2 Agricultural Household Models

The agricultural household model describes household behavior using the unitary

model. The vast majority of households in rural areas in developing countries are

engaged in agricultural activities. The agricultural household production model is a

model of both production and consumption; in this model, the household is both a

consumer and producer and hired labor is assumed perfectly substitutable with family

labor. The model assumes the presence of perfect labor markets where excess labor can

be employed in the non-agricultural sector and households can also hire labor under

situations of excess demand for labor (Schultz 2001). Within the agricultural household

models, production and consumption decisions can be analyzed either sequentially

(separable) or simultaneously (nonseparable model).

The basic agricultural household model posits a farm household that is assumed to

maximize a household utility function (Singh et al.1986a):

U = U (Xa, Xm, Xl) [2.8]

where utility is a function of agricultural staples (Xa), market goods (Xm) and leisure (Xl).

The household production function is represented as Q (L, A), where L is labor and A is a

fixed quantity of land. Household utility is maximized subject to a budget constraint,

time constraint and the production technology:

pm Xm = pa (Q - Xa) – w (F - L) [2.9]

Xl + F = T [2.10]

Q = Q (L, A) [2.11]

where w is the wage rate, pm and pa are market prices, F is family (household) labor input

and T is total stock of time within the household. The Q (L, A) - Xa is marketed surplus

31

and F - L yields net sales of labor. All prices (w, pm, pa) are exogenous and the

household is a price-taker in all three markets. The three constraints are collapsed into

one full-income budget constraint:

pmXm + paXa + wXl = wT + paQ(L, A) – wL [2.12]

The paQ (L, A) – wL represents farm profits and the left-hand side of equation 2.12

represents total household expenditures including purchase of market goods, the

household’s purchase of its own output and its own purchase of time in the form of

leisure.

Optimal levels of consumption of each of the commodities (Xa, Xm, Xl) and the

total labor input utilized in agricultural production are determined. Optimal value of

labor, output and full income is derived solving the first-order conditions. In the case of

agricultural households, production activities determine income and factors affecting

production influence the household’s full income, which in turn affects household

consumption. Therefore, household production and consumption are separable or

recursive. Separability of the decision implies that production decisions are not

influenced by consumption and labor supply decisions but consumption and labor supply

decisions are dependent on production decisions. That is, production decisions do not

depend on consumption preferences but consumption decisions are influenced by

production through the full income. Households follow a two-step optimality procedure:

first, farm profits are maximized using the optimal combination of inputs and the

household utility function is maximized (Singh et al. 1986a).

Separable models are not applicable under all circumstances and nonseparable

models may be more appropriate in the case of presence of imperfect markets, when sale

32

and purchase prices for goods differ or when markets fail (Singh et al. 1986b). Market

failures are characteristic of developing agrarian economies and nonseparable models are

more applicable (Sadoulet and de Janvry 1995).

However, unitary household models are very restrictive in nature. They do not

indicate how household decisions are made and how resources are allocated among

members (Schultz 2001). Individuals constitute the household and taking individuals as

the unit of analysis theoretically makes more sense. Given that individuals within a

household could have access to different kinds of resources, the assumption of income

pooling may not hold empirically (Mendoza 1997). Also, household production

functions are difficult to estimate as the output produced in the household (for example,

children’s education) is not sold in the market. Individual members of the household

may have different tastes and preferences which could be distinct from that of the

household.

Unitary models also do not take into account intrahousehold allocation of

consumption and the implications of this allocation for welfare. Different allocations to

different members have different welfare outcomes (Mendoza 1997). For example, in

many developing countries human capital investments in men and women have different

implications for the household and child outcomes (Behrman 1997). Development

policies only sometimes target individuals. Unitary models which do not take into

account individual preferences could yield misleading policy directives (Quisumbing

2003).

33

2.3.3 Collective Models

During the 1980s alternatives to the unitary approach to household resource

allocation emerged. Under the collective approach, the household utility function is

disaggregated and the model takes into account the different preferences of each member

of the household (Chiappori 1988, 1992; Browning and Chiappori (1998); Haddad et al.

1997; Quisumbing 2003; Mendoza 1997). Here the focus is on the individuals within the

household rather than on the entire household as one unit, and resources are no longer

pooled. Individuals decide the amount of their income to be transferred to others and the

amount allocated to purchasing common household goods (Doss 1996).

Unitary models can be shown as a special case of the collective models.

Collective household models can be divided into cooperative and non-cooperative models

(Mendoza 1997). All cooperative models assume that households make Pareto efficient

allocations, i.e., no one can be made better off without making someone else worse off

(Chiappori 1988, 1992) whereas non-cooperative models may or may not yield Pareto

optimal outcomes.

2.3.4 Cooperative Model

Cooperative models postulate that individuals form households only if there is a

net gain in doing so. There are two approaches within the cooperative framework. The

first approach assumes that all households have a sharing rule to allocate income among

members (Chiappori 1988, 1992; Browning and Chiappori 1998; Apps and Rees 1997).

The income-sharing rule is a function of the incomes of the husband and the wife and

total household income (Mendoza 1997). The household uses the sharing rule to allocate

34

resources among its members. Doss (1996) outlines four assumptions that are needed to

recover the sharing rule from household expenditure data: 1) requires that some goods be

private, 2) the utility of other members is included as one of the arguments in one’s own

utility function, 3) a separable utility function exists with respect to private and public

goods, and 4) at least one private good is assignable in order to observe who consumes

that good.

Browning et al. (1994) develop a model showing how income affects household

outcomes within the framework of family expenditure data. They assume that

households make Pareto efficient decisions and find that resource allocation decisions

among Canadian couples depend on their current income, age and lifetime wealth.

Browning et al. (1994) consider a two-member household (a, b) where households

maximize the weighted sum of household members’ utility subject to a budget constraint

(Strauss and Beegle 1996):

Max μ UA (xA, xB) + (1-μ) UB (xA, xB) [2.13]

subject to p (xA + xB) = Y [2.14]

where Ui is the utility function of the household members, xi is the private consumption

good, Y is total household income and p is the price vector for the market good. The μ is

the welfare weight for household member A which lies between 0 and 1 and is a function

of prices, household income and other factors such as the distribution of income (Strauss

and Beegle 1996). This model collapses into the unitary model if individuals A and B are

identical or if μ equals 0 or 1. This would imply that everybody has identical preferences

or there is a dictator in the household. Demand for the market good x is a function of

prices, income and μ (xA = xA (p, Y, μ (p, Y))).

35

Strauss and Beegle (1996) derive tests for the collective approach using a two-

stage decision process with an income-sharing rule. The household first pools resources

and allocates income to each individual and then individuals maximize their sub-utility

subject to the income they have been allotted. Suppose θ is the income allotted to one

member out of the total income Y, then in a two-member household the other member

would have (Y – θ) left for him/her. Therefore, in the second-stage, members maximize:

max UA (xA) [2.15]

subject to pxA = θ [2.16]

The sharing rule (θ) is a function of prices, income and other distributional factors and

the model is a unitary model when θ is fixed. The conditional demand curve is xA =

xA (p, θ). It is also postulated that the ratio of the marginal propensity to consume a good

with respect to changes in income of the two individuals is to be the same across all

goods. That is,

Bj

Aj

Bk

Ak

YXYX

YXYX

∂∂∂∂

=∂∂∂∂

//

// [2.17]

In a unitary model this ratio is equal to one and in a collective model this ratio represents

the sharing weights that determine the control of the individual over the resources.

Chiappori (1992) develops a collective model of household labor supply where the

economic agents first share nonlabor income based on the sharing rule and then in the

second-stage make labor supply and consumption decisions.

36

2.3.5 Cooperative Bargaining Models

The other approach was developed by McElroy and Horney (1981) and Manser

and Brown (1980) which explicitly assumes a bargaining rule among members of the

household. Manser and Brown (1980) provide a cooperative bargaining solution to the

issue of marriage and household decision-making where benefits derived from marriage

are distributed between the husband and wife. In the Manser and Brown model, a rule is

derived to resolve household allocative and distributional issues using a Nash-bargaining

model. Individuals have a guaranteed utility level that they enjoy when they do not

cooperate, and they marry or form a family only if the utility they derive from

cooperating is greater than being single. This minimum reservation utility is defined as

the threat point9 and gains from cooperation are a function of the bargaining strength of

the individual family members (Mendoza 1997). In the bargaining approach, control

over the income plays an important role in household decision-making unlike in Becker’s

unitary model where the household collectively controls the total income.

McElroy and Horney’s (1981) Nash-bargaining household decision model

assumes a two-individual household, m and f. Market goods of interest to m are

xm = (x0, x1, x3) at prices pm = (p0, p1, p3) and those of interest to f are xf = (x0, x2, x4) at

prices pf = (p0, p2, p4) where x1 and x2 are the market goods consumed by the husband and

the wife, respectively, and x3 and x4 are the leisure time10 of the husband and wife,

respectively. The x0 is the household good that is consumed which has a public good

characteristic. If individuals are not married then they maximize their individual utility

functions subject to their individual budgets, to derive their indirect utility functions 9 Defined as maximum level of utility outside of the household (McElroy 1990). 10 Leisure time is defined as time not spent in market work (McElroy and Horney 1981).

37

),(0 mmm

om IpVV = and ),(0 ff

fo

f IpVV = where Ik (k = m, f) is non-wage income.

Further, the McElroy and Horney model assumes gains from marriage, with the married

couple maximizing the Nash utility function

)];,()()][;,()([ 00 fffff

mmmmm IpVxUIpVxUN αα −−= [2.18]

subject to a full-income constraint

fm IITppxpxpxpxpxp +++=++++ )( 434433221100 [2.19]

where T is the time endowment of both individuals and the Vi are the threat points of the

individuals m and f (threat of becoming divorced). Threat points represent the utility

individuals would receive if they remain single (reservation utility) and the αi are the

extrahousehold environmental parameters (EEPs) (McElroy 1990). Solution to the

maximization problem yields Marshallian demand equations which are functions of

prices, nonlabor income, and the EEPs:

4,3,2,1,0),,;,,( == iIIphx fmfmii αα [2.20]

The EEPs shift the threat points and have no effect on nonwage income and prices

(McElroy 1990). They include social, legal and institutional parameters that have welfare

impacts on households, and thus enabling the policy component to be explicitly included

in the model (Swaminathan 2003). Examples of EEPs are divorce laws, welfare policies

of single mothers, extended family support networks and local ratios of marriageable men

to women (Schultz 2001). These factors may affect the reservation utilities and family

outcomes within the bargaining process.

Lundberg and Pollak (1993) introduce a ‘separate spheres’ bargaining model

within marriage. Divorce as a threat point is replaced by a non-cooperative equilibrium

38

that reflects traditional gender roles. Within this framework, Lundberg and Pollak (1993)

study the distributional implications of the child allowance schemes to the mother in

United Kingdom. This would make outcomes of cooperative bargaining favor the

woman. Ermisch (2003) suggests that an increase in mother’s income has an income