35

March 2017

March 2017

Forward-looking Statements

Statements and information herein that are not historical facts are "forward-looking information". Words such as “plans”, “intends”, “outlook”, “expects”, “anticipates”, “estimates”, “believes”, "likely", “should”, "could", "will", "may" and similar expressions often identify forward-looking information and statements. Forward looking statements and information may include, without limitation, statements regarding the operations, business, financial condition, liquidity, expected financial results, performance, obligations, market conditions, prospects, opportunities, priorities, targets, goals, ongoing objectives, strategies and outlook of Toromont and its business units.

Forward-looking information and statements contained herein are based on, among other things, Toromont management's current assumptions, expectations, estimates, objectives, plans and intentions regarding projected revenues and expenses, the economic, industry and regulatory environments in which Toromont operates or which could affect its activities, Toromont's ability to attract and retain customers as well as Toromont's operating costs and raw materials supply. By their nature, forward-looking information and statements, and the factors upon which they are based, are subject to risks and uncertainties which may be beyond Toromont's ability to control or predict. Actual results or events could differ materiallyfrom those expressed or implied by forward-looking information and statements. Factors that could cause actual results or events to differ from current expectations include, among others: business cycle risk, including general economic conditions in the countries in which Toromont operates; risk of commodity price changes including precious and base metals; risk of changes in foreign exchange rates, including the Cdn$/US$ exchange ate; risk of the termination of distribution or original equipment manufacturer agreements; risk of equipment product acceptance and availability of supply; risk of increased competition; credit risk related to financial instruments; risk of additional costs associated with warranties and maintenance contracts; interest rate risk on financing arrangements; risk of availability of financing; risk of environmental regulation.Additional information on these factors and other risks and uncertainties that could cause actual results or events to differfrom current expectations can be found in the “Risks and Risk Management” and “Outlook” section of Toromont’s annual MD&A for 2016 contained in the 2016 Toromont Annual Report. Other factors, risks and uncertainties not presently known to Toromont or that Toromont currently believes are not material could also cause actual results or events to differ materially from those expressed or implied by forward-looking information and statements.

Forward-looking information and statements contained herein about prospective results of operations, financial position or cash flows are presented for the purpose of assisting Toromont's shareholders in understanding managements' current view regarding those future outcomes and may not be appropriate for other purposes. Readers are cautioned not to place undue reliance on the forward-looking information and statements contained herein, which are given as of the date of this document, and not to use such information and statements for anything other than their intended purpose. Toromont disclaims any obligation or intention to update or revise any forward-looking information or statement, whether the result of new information, future events or otherwise, except as required by applicable law.

2

Investment Highlights

Market Leading Brands And Position

Product Support Provides Stability

Superior Financial Track Record

Strong Balance Sheet

Growth Opportunities In Diversified Segments

49 Year Dividend Record, 28 Of Consecutive Growth

Continuous Focus on Operational Excellence

3

Safety

4

Be Fit For Duty

Assess All Hazards

ControlHazardous

Energy

Proper PPE for Work

Area/ Task

Immediate Incident

Reporting

Multiple Growth Platforms

Construction Industries

Resource Industries

5

EQU

IPM

ENT

GR

OU

P

GROWTH FUELED BY:► Expanded Markets and New Branches

► Expanded Service Offerings

► Increased Population and Larger Equipment Fuels Product Support

Growth In Revenue

Revenue presented is based on trailing 12 months. Installed units based on management estimates for Toromont CAT. 6

0

5,000

10,000

15,000

20,000

25,000

30,000

0

250

500

750

1,000

1,250

1,500

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Esti

mat

ed

In

stal

led

Bas

e (

Un

its)

Re

ven

ue

($

mil

lio

ns)

Product Support Sales Equipment Sales Rental Estimated Installed Base

Strong Dealer Network

33 Toromont CAT BranchesHistory of Successful Consolidation

>250 Brands >28,000 Items42 Stores Serving

14,500 Customers

Newfoundland & Labrador

Ontario

Nunavut

Musselwhite

Meadowbank

Porcupine

Voisey’s Bay

VictorDetour

Lake

2

3

4

5

6

Manitoba

Toromont CAT Mine Site Branches

1. Agnico Eagle2. Goldcorp3. DeBeers4. Detour Gold5. Goldcorp6. Vale7. Baffinland

Toromont CAT Branches

DEDICATED TEAM DELIVERSSPECIALIZED EQUIPMENTAND MUCH MORE

Remote mine sites contributed $1,400MM over past decade

1

Mary River7

+2,700 Members

75 Locations

IN NEWFOUNDLAND & LABRADOR, ONTARIO, MANITOBA AND NUNAVUT

7

Equipment Group

8

11

Large

Contractor

24%

Local

Contractor

16%

Mining

24%

Industrial

6%

Equipment

Services

6%

Other

19%

Quarry &

Aggregate

5%

Large & Local Contractors 40%

Source: Internal data Toromont Cat total sales for the three years ended Dec. 31.16

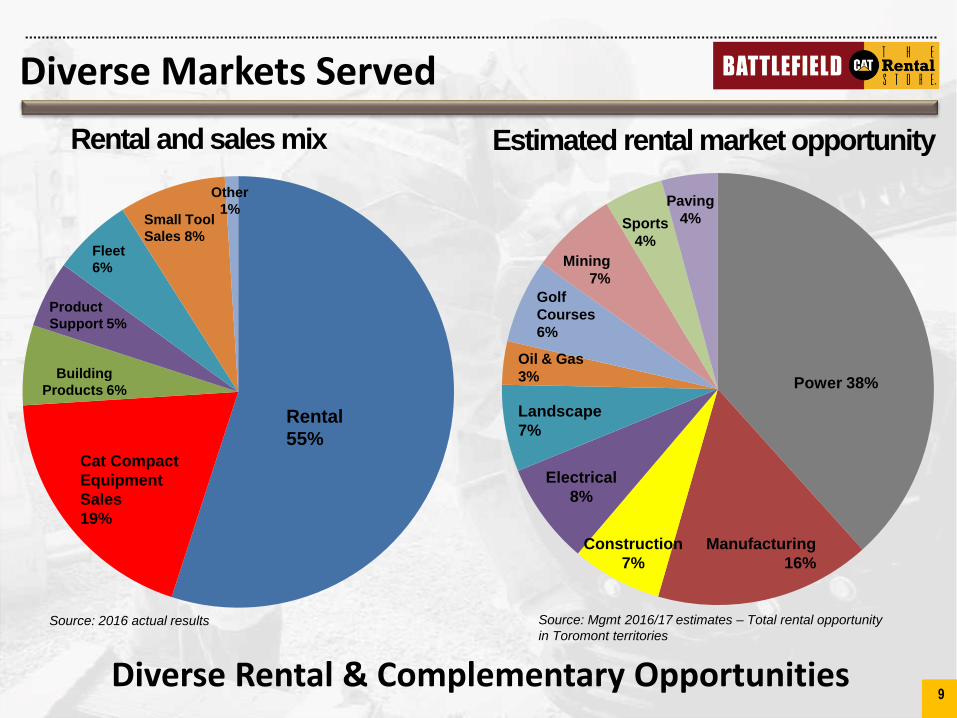

Diverse Markets Served

DIVERSE MARKETS WITH EMPHASIS ON INFRASTRUCTURE

Infrastructure

Road

Construction

15%

Residential

3%

Other

12%

Utilities

4%

Excavation &

Earthmoving

4%

9

11

Cat Compact

Equipment

Sales

19%

Rental

55%

Building

Products 6%

Product

Support 5%

Fleet

6%

Other

1%Small Tool

Sales 8%

Power 38%

Manufacturing

16%

Golf

Courses

6%

Landscape

7%

Construction

7%

Electrical

8%

Diverse Markets Served

Oil & Gas

3%

Mining

7%

Sports

4%

Paving

4%

Rental and sales mix Estimated rental market opportunity

Source: 2016 actual results Source: Mgmt 2016/17 estimates – Total rental opportunity

in Toromont territories

Diverse Rental & Complementary Opportunities9

Substantial Infrastructure Deficit

$388 billion*

79 % infrastructure

ffailing

The Greater Toronto and Hamilton Area is one of the fastest-growing regions in North America.

Approximately 100,000 new residents per year.

9 million35% of assets in need of attention*

• $141 billion in very poor and poor conditions

• $247 billion in fair physical condition

*Source: 2016 Canadian Infrastructure Report Card, Federation of Canadian Municipalities

Roads, municipal buildings, sport and recreational facilities and public transit are the asset classes most in need of attention

Continued need demands continued investment – recognized by all levels of government (Municipal, Provincial, Federal) 10

people

by 2031

Infrastructure Commitment Ontario

11

Source: 2016 Ontario Budget

Infrastructure Ontario plans $137 billion ten-year spend (up $3B from plans announced in the prior year)

12

Infrastructure Commitment Federal

• Including pre-existing programs and commitments in the 2016 Budget and Fall Economic Statement, total committed spend add up to an unprecedented $186 billion over 12 years

• To-date, specific projects have been slower to release leading to reluctance for customers to pull the trigger on equipment investment and rental commitments

Source: Fall Economic Statement 2016, The Government of Canada

Rental Market

HEAVY RENTS

LIGHT EQUIPMENT

POWER GENERATION

13

Equipment Group

0

50

100

150

200

250

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

R12 R

even

ue (

$m

illio

ns)

Light Equipment Heavy Equipment Power Generation Rent with a Purchase Option Rental - Used

$1,000

$200

$40

$1,240

$150 $25 $11186

0

200

400

600

800

1,000

1,200

1,400

Battlefield Heavy Rent Power Total

Total market* Toromont revenue

Rental Market OpportunityR

enta

l Rev

enu

es $

Mill

ion

s

15% 12% 28% 15%

R’12 Revenues to Dec. 31/16* Market Size based on internal management estimates

SUBSTANTIAL ROOM FOR CONTINUED GROWTH

Significantgrowthopportunity

14

Equipment Group

($ Millions) Battlefield Heavy Rent Power Total

Fleet at Original 314.2$ 112.1$ 46.4$ 472.7$

Mining Opportunities

CAT 6060FS Diesel Shovel Loads 795F AC Truck CAT R2900G

► Good diversity of commodities in Toromont territories

► Gold has been a significant contributor

► Opportunities continue – albeit tight market

► Significant increase in installed base increases product support opportunity.

► Large geography in safe jurisdiction

Resource Industries

15

Growth In Mining Installed Base

SUBSTANTIAL INCREASE IN MINING EQUIPMENT INSTALLEDBASE CREATES INCREASED PRODUCT SUPPORT OPPORTUNITY

Replacement value based on current pricing. Installed units based on management estimates.

Resource Industries

16

0

200

400

600

800

1000

1200

1400

0.0

200.0

400.0

600.0

800.0

1,000.0

1,200.0

1,400.0

1,600.0

1,800.0

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Inst

alle

d B

ase

(Un

its)

Cu

rre

nt

Re

pla

cem

en

t V

alu

e o

f Fle

et

($M

M)

Other Underground Mining Trucks Shovels Number of Units

0

200

400

600

800

1000

1200

$-

$100

$200

$300

$400

$500

$600

Dec'03

Jun'04

Dec'04

Jun'05

Dec'05

Jun'06

Dec'06

Jun'07

Dec'07

Jun'08

Dec'08

Jun'09

Dec'09

Jun'10

Dec'10

Jun'11

Dec'11

Jun'12

Dec'12

Jun'13

Dec'13

Jun'14

Dec'14

Jun'15

Dec'15

Jun'16

Dec'16

Nu

mb

er

of

Tech

nic

ian

s

Trai

ling

12

mo

nth

Pro

du

ct

Sup

po

rt R

eve

nu

es

($M

M)

Product Support Revenues Number of Technicians

Product Support

► Technician recruitment continues

17

Expanded Product Support Offering

Largest opportunity

2nd largest and expanding opportunity

Larger customers adverse to holding facilities or techs

18

Equipment Management Solutions Advancing

► Increasing focus on EM and CM (condition monitoring) solutions

► Provides further opportunity for differentiation and customer service

► Toromont CAT currently has over 3,500 contracted service agreements in place (PMs and MARCs)

19

Complementary Products Supplement Growth

Machine Control & Guidance Systems Mobile Crushing & Screening Products

20

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2008 2009 2010 2011 2012 2013 2014 2015 2016

Sale

s ($

000'

s)

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2008 2009 2010 2011 2012 2013 2014 2015 2016

Re

ve

nu

e (

$0

00

's)

Power Systems Growth Opportunities

► Increasing share of higher investment in CHP & alternative energies (MWM)

► Large power plants for remote mine sites (MaK)

► Natural gas-fueled distributed power (District Energy)

► Expanded products – Toshiba UPS & Switch Gear offering, Gorman pumps

► Rental – industrial, commercial & special events

29%

26%

20%

20%

5%

Electric Power

Industrial

Prime Power

Rental

Marine21Based on 2016 Sales

Growth Platform In Manitoba

22

Six locations :► Elie► Portage la Prairie► Neepawa► Brandon► Steinbach► Morden

96 employees including34 technicians

Manitoba

Product Range

Market Share

Parts & Service

Construction

Power Systems

Mining

ORGANIC GROWTH

How WillThe Equipment Group Continue To Grow?

23

CIMCO

► 100+ year history

► Strong industrial customer base

► Leader in recreational systems

► U.S. growth opportunity

24

AR

AL

FL

Revenue Split(2016)

WI

IL

MS GA

SC

NC

PA

ME

VTNH

RI

VAVW

MI

DENJ

MA

Over 100 Years Of Serving Refrigeration Markets

25

Recreational

20%Product Support

42%

Industrial

38%

Note: Total of 22 CIMCO locations not reflected in map above due to overlapping markets resulting from close proximity of locations.

► Strong industrial customer base

► Leader in recreational systemsUS Sales Coverage400 Mile Sales Ring

Excellent Growth Opportunities

EXPAND MARKETS – TECHNOLOGY & VALUE-ADDED SERVICES► Increase application of Eco Chill into Industrial Applications

► Expand scope of work – related HVAC, automation & bldg controls

► Application of heat pump systems

► Develop of Ammonia/CO2 solutions

EXPAND TERRITORIES AND CUSTOMERS► Expand U.S. footprint by building product support network – secured

largest food services refrigeration CSA in U.S. – and adding points of presence (service and sales offices)

► Add to Canadian service locations

► Penetrate new customer accounts (new technologies)

26

DELIVERINGRESULTS

27

High Performance Capital Management

18.9*

Return on Opening Shareholders’ Equity (%)

Net Debt-to-Capitalization Ratio

* Excludes goodwill, intangibles and transaction costs* * Continuing operations from 2011

(%)

21.6 21.5

15.5

9.1

29.928.9

25.7

23.09.1

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

21.6

20.0

18.9*0.16

0.05

-0.06

0.17

0.13

0.25

0.10

0.06

0.10

-0.04

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

28

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Div

ide

nd

s P

er

Shar

e $

Sustained Growth In Dividends Since 1989

Annual Dividends Per Share(Cents)

49 Year Dividend Record, 28 Of

Consecutive Growth

Note: Historic pro forma based on Butterfly proportion 56.4%* 2017 estimated based on current quarterly rate of $0.19

Ten Year CAGR 10.9%

29

Growth And Profitability Throughout The Cycle

Pro Forma Net Earnings from Continuing Operations (Millions)

155.7

119.5

83.1

59.4

76.7

102.7

123.0

145.7

133.2

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

73.0

30

472.0REVENUES

$ millions except EPS

61.7OPERATING INCOME

44.4NET EARNINGS

0.57EPS (BASIC)

480.7

62.9

45.5

0.58

2016 2015

2

3

2

% Change

Q4 Results

2

31

1,802.2REVENUES

$ millions except EPS

204.5OPERATING INCOME

145.7NET EARNINGS

1.88EPS (BASIC)

1,867.3

216.6

155.7

1.99

2016 2015

6

7

6

% Change

DECEMBER YTD Results

4

32

Experienced Management

E X E C U T I V E T E A M

► Collective 148 years with Toromont (21 yr avg), 214 years career (31 yr avg)

► Significant experience in operating units with similar stats

► Detailed succession plans in place with good depth of talent

SCOTT J. MEDHURSTPresident and Chief Executive Officer

29 years with Toromont29 year career

Randy B. CassonPresident Construction Industries

40 years with Toromont / 40 year career

Paul R. JewerExecutive Vice President & Chief Financial Officer

12 years with Toromont / 31 year career

David A. MalinauskasPresident CIMCO

18 years with Toromont / 22 year career

Jennifer J. CochraneVice President Finance

14 years with Toromont / 27 year career

Mike P. CuddyVice PresidentChief Information Officer

22 years with Toromont / 37 year career

David C. WetheraldVice PresidentHuman Resources & Legal

13 years with Toromont / 28 year career

33

Equity Ownership

O W N E R S H I P :

EQUITY OWNERSHIP KEY REQUIREMENT ► Defined minimums for senior executives (3x CEO, 2x CFO, 1.5x VPs)

► For option participation – annual option grants limited to ownership

► Employee participation in ESPP – 50%

Units $MM %

Board 2,688,128 $ 113.8 3.4

Senior Management 927,011 39.3 1.2

Employees (ESPP) 1,393,242 59.0 1.8

TOTAL 5,008,381 $ 212.1 6.4

Balances as at December 31, 2016 with closing price $42.35Units include shares and DSUs, both of which are purchased

34

March 2017