19

FINANCIAL RESULTS PRESENTATION FY2019 March 2020

FINANCIAL RESULTS PRESENTATION FY2019

March 2020

2

❑ FY2019 Results Highlights

❑ Summary Financial Results

❑ Business Units Performance

PRESENTATION

3

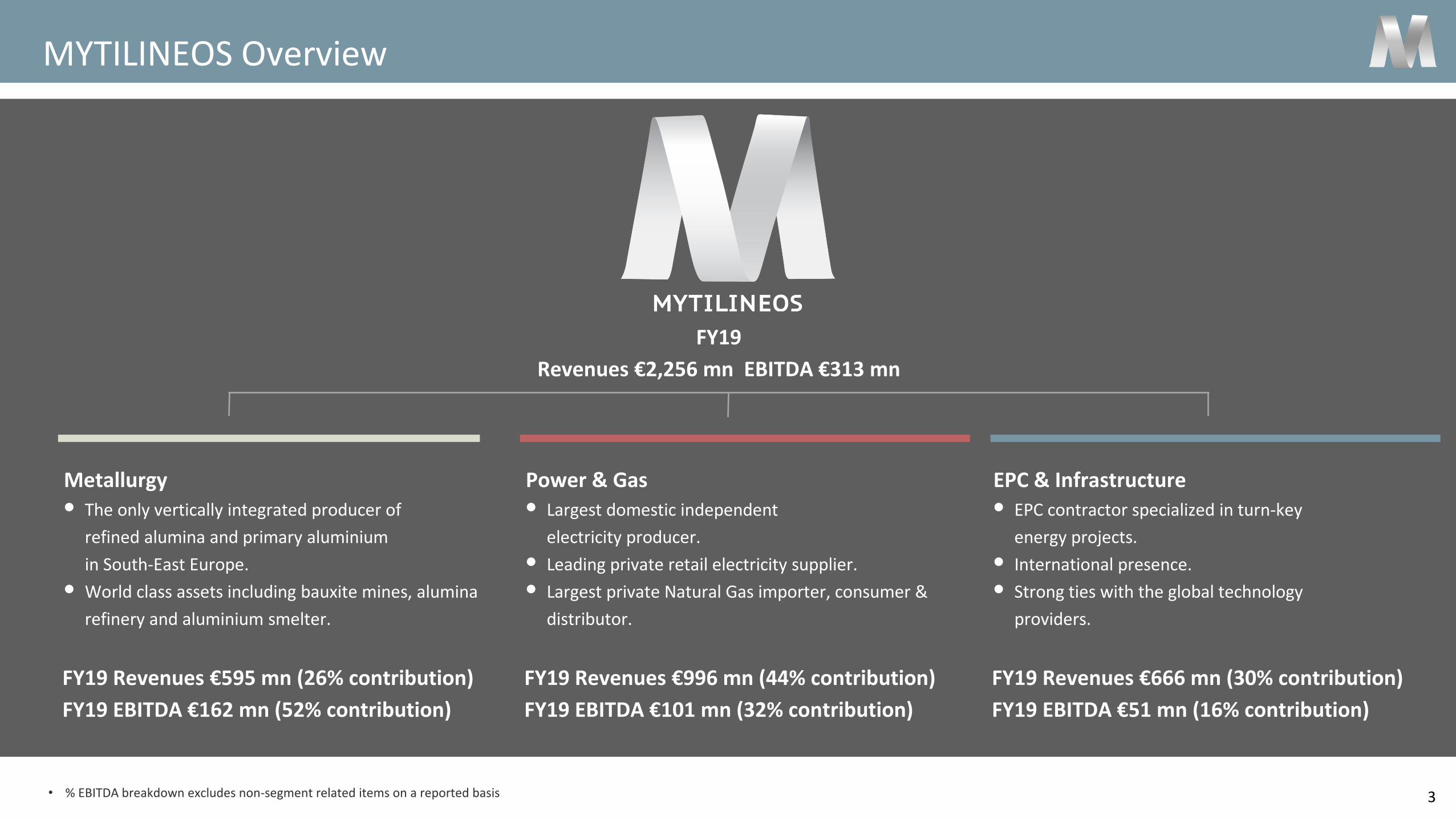

MYTILINEOS Overview

Metallurgy

• The only vertically integrated producer of

refined alumina and primary aluminium

in South-East Europe.

• World class assets including bauxite mines, alumina

refinery and aluminium smelter.

FY19 Revenues €595 mn (26% contribution)

FY19 EBITDA €162 mn (52% contribution)

Power & Gas

• Largest domestic independent

electricity producer.

• Leading private retail electricity supplier.

• Largest private Natural Gas importer, consumer &

distributor.

FY19 Revenues €996 mn (44% contribution)

FY19 EBITDA €101 mn (32% contribution)

EPC & Infrastructure

• EPC contractor specialized in turn-key

energy projects.

• International presence.

• Strong ties with the global technology

providers.

FY19 Revenues €666 mn (30% contribution)

FY19 EBITDA €51 mn (16% contribution)

• % EBITDA breakdown excludes non-segment related items on a reported basis

FY19

Revenues €2,256 mn EBITDA €313 mn

4

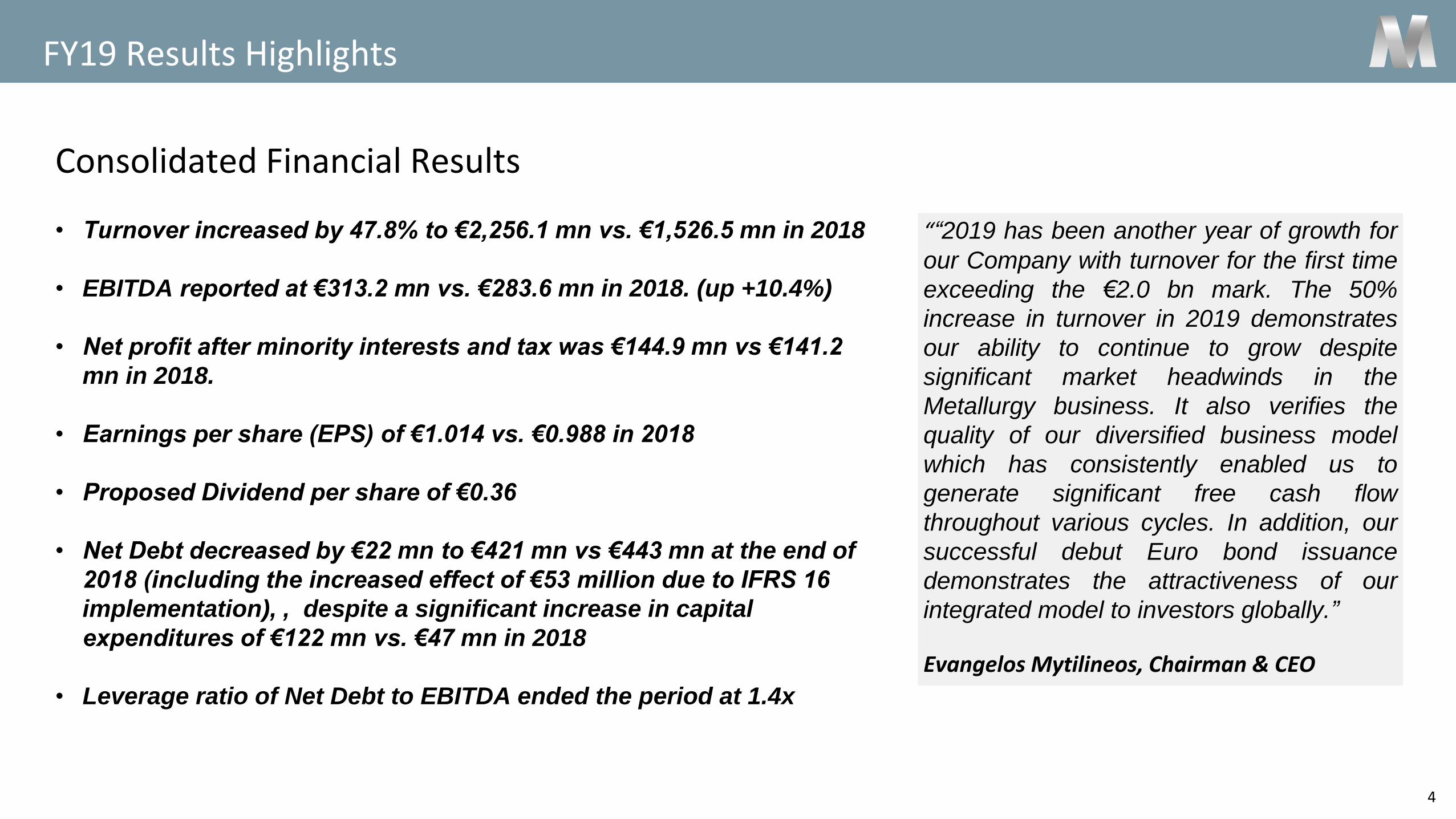

FY19 Results Highlights

Consolidated Financial Results

• Turnover increased by 47.8% to €2,256.1 mn vs. €1,526.5 mn in 2018

• EBITDA reported at €313.2 mn vs. €283.6 mn in 2018. (up +10.4%)

• Net profit after minority interests and tax was €144.9 mn vs €141.2

mn in 2018.

• Earnings per share (EPS) of €1.014 vs. €0.988 in 2018

• Proposed Dividend per share of €0.36

• Net Debt decreased by €22 mn to €421 mn vs €443 mn at the end of

2018 (including the increased effect of €53 million due to IFRS 16

implementation), , despite a significant increase in capital

expenditures of €122 mn vs. €47 mn in 2018

• Leverage ratio of Net Debt to EBITDA ended the period at 1.4x

““2019 has been another year of growth for

our Company with turnover for the first time

exceeding the €2.0 bn mark. The 50%

increase in turnover in 2019 demonstrates

our ability to continue to grow despite

significant market headwinds in the

Metallurgy business. It also verifies the

quality of our diversified business model

which has consistently enabled us to

generate significant free cash flow

throughout various cycles. In addition, our

successful debut Euro bond issuance

demonstrates the attractiveness of our

integrated model to investors globally.”

Evangelos Mytilineos, Chairman & CEO

5

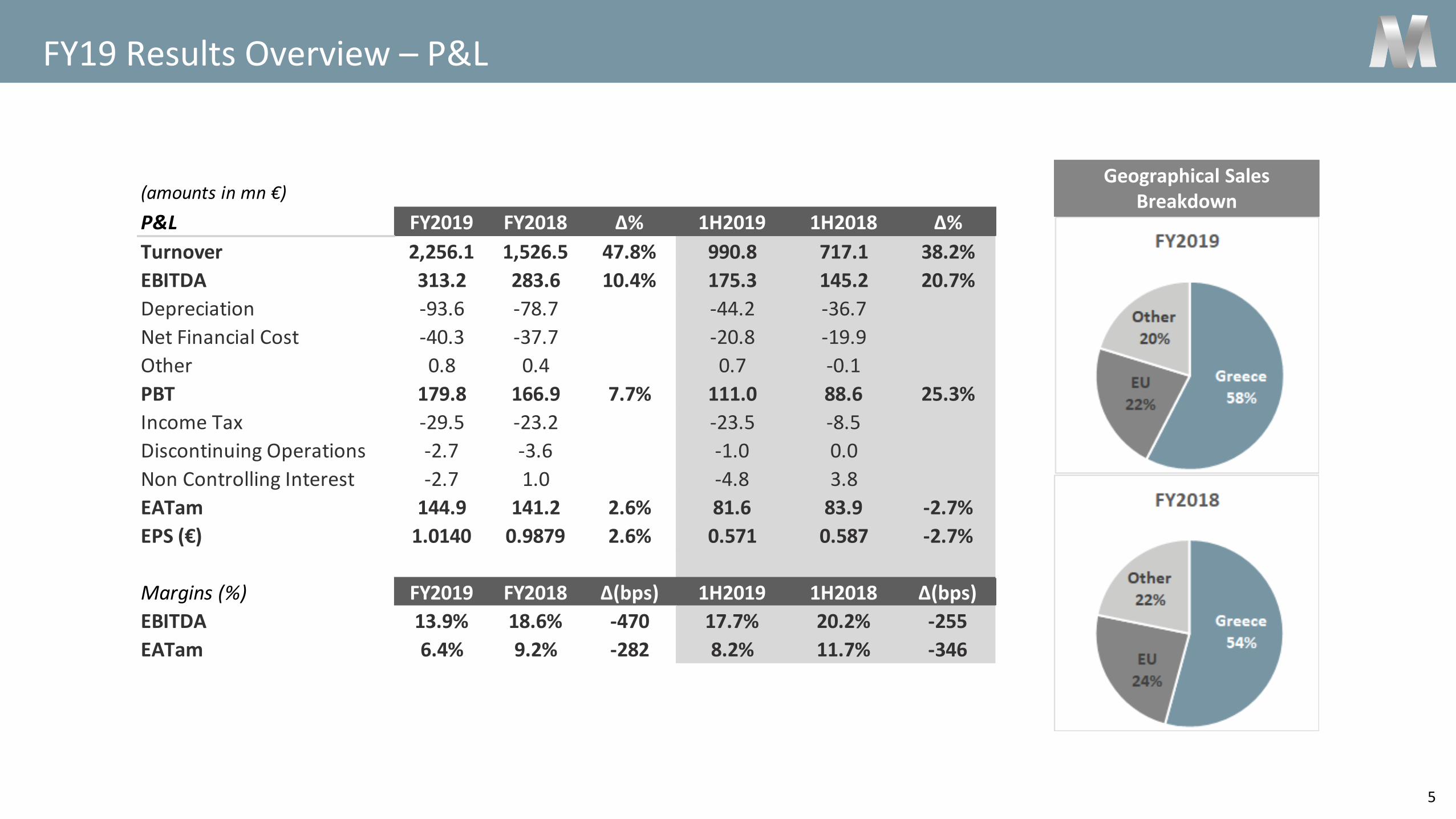

FY19 Results Overview – P&L

Geographical Sales Breakdown(amounts in mn €)

P&L FY2019 FY2018 Δ% 1H2019 1H2018 Δ%

Turnover 2,256.1 1,526.5 47.8% 990.8 717.1 38.2%

EBITDA 313.2 283.6 10.4% 175.3 145.2 20.7%

Depreciation -93.6 -78.7 -44.2 -36.7

Net Financial Cost -40.3 -37.7 -20.8 -19.9

Other 0.8 0.4 0.7 -0.1

PBT 179.8 166.9 7.7% 111.0 88.6 25.3%

Income Tax -29.5 -23.2 -23.5 -8.5

Discontinuing Operations -2.7 -3.6 -1.0 0.0

Non Controlling Interest -2.7 1.0 -4.8 3.8

EATam 144.9 141.2 2.6% 81.6 83.9 -2.7%

EPS (€) 1.0140 0.9879 2.6% 0.571 0.587 -2.7%

Margins (%) FY2019 FY2018 Δ(bps) 1H2019 1H2018 Δ(bps)

EBITDA 13.9% 18.6% -470 17.7% 20.2% -255

EATam 6.4% 9.2% -282 8.2% 11.7% -346

6

FY19 Results Overview – Balance Sheet

ROCE & ROE calculations are available in FY2019 Financial Results Notes

*

Net Debt decreased by 22 mn

* Due to the application of IFRS 16 since Jan. 1, 2019, FY19 Debt includes €53 mn of leases

Note: 2019 BOT spending amounted c. €50mn

7

EBITDA Gap Analysis

283,6

22,4 11,7 1,8 10,2 3,5 3

-1,4

-45,5 -40

16,8

-8,8 -1,9

5,4

-14 -1,6 -3,2

71,2

313,2EB

ITD

A 2

01

8

Nat

ura

l Gas

New

RES

Oth

er

Pri

or

year

s C

O2

reb

ate

Pri

ce r

evie

w o

f B

OTA

S ga

s in

20

18

resu

lts

of

Po

wer

& G

as

Pri

ce r

evie

w o

f B

OTA

S ga

s in

20

18

resu

lts

of

Met

allu

rgy

Oth

er

Alu

min

ium

Alu

min

a

€/$

rat

e ef

fect

-M

etal

lurg

y

€/$

rat

e ef

fect

-Po

wer

& G

as

€/$

rat

e ef

fect

-EP

C

CO

2 M

etal

lurg

y

CO

2 P

ow

er &

Gas

Cap

acit

y p

aym

ents

Oth

er

Hed

gin

g

EBIT

DA

20

19

Intrinsic Effect€35.9mn

One-Off Items€15.3mn

Market Effect€-92.8mn

Hedging€71.2mn

8

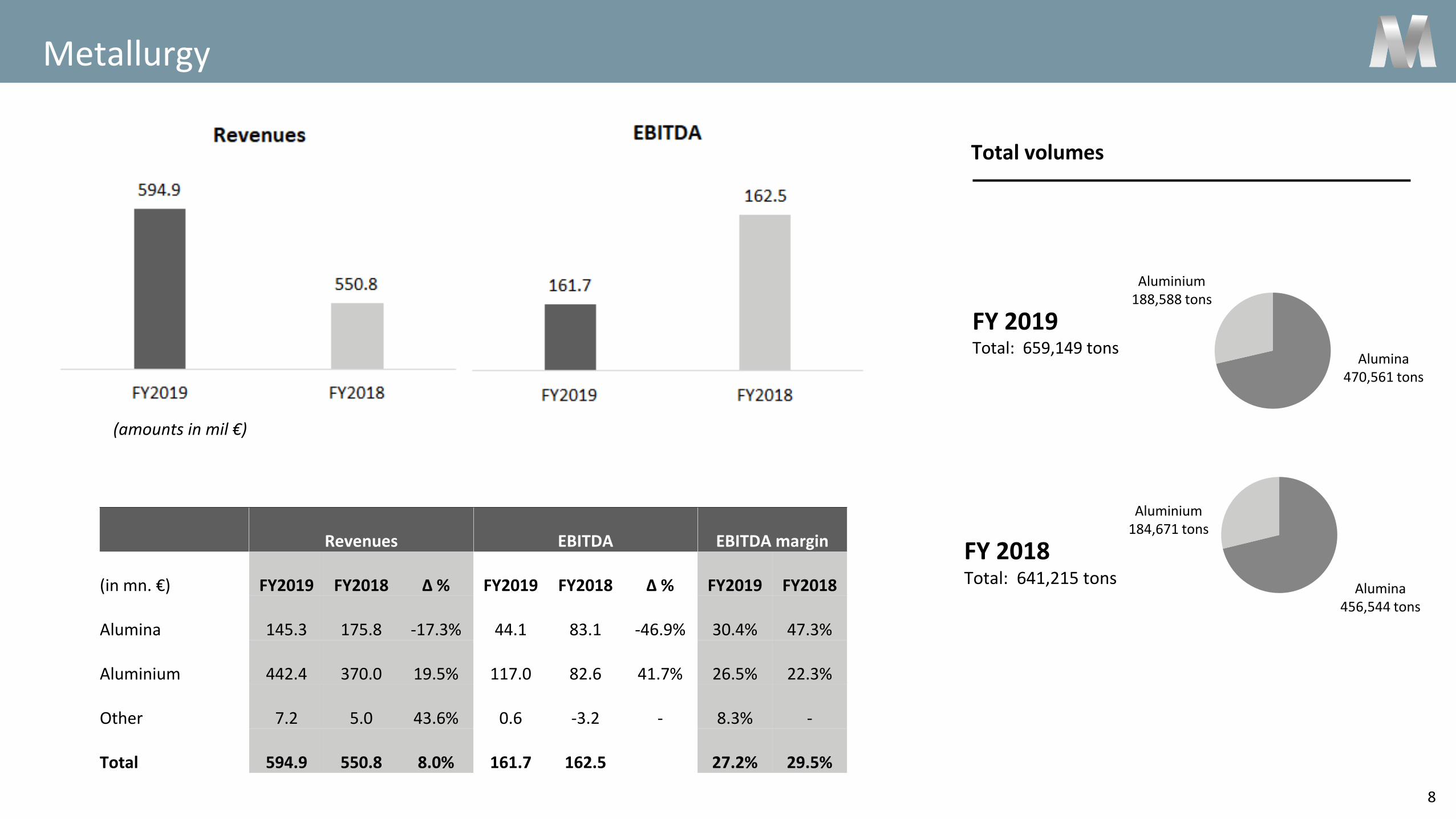

Metallurgy

FY 2019Total: 659,149 tons

FY 2018Total: 641,215 tons

Total volumes

Aluminium188,588 tons

Alumina470,561 tons

Aluminium184,671 tons

Alumina456,544 tons

(amounts in mil €)

Revenues EBITDA EBITDA margin

(in mn. €) FY2019 FY2018 Δ % FY2019 FY2018 Δ % FY2019 FY2018

Alumina 145.3 175.8 -17.3% 44.1 83.1 -46.9% 30.4% 47.3%

Aluminium 442.4 370.0 19.5% 117.0 82.6 41.7% 26.5% 22.3%

Other 7.2 5.0 43.6% 0.6 -3.2 - 8.3% -

Total 594.9 550.8 8.0% 161.7 162.5 27.2% 29.5%

9

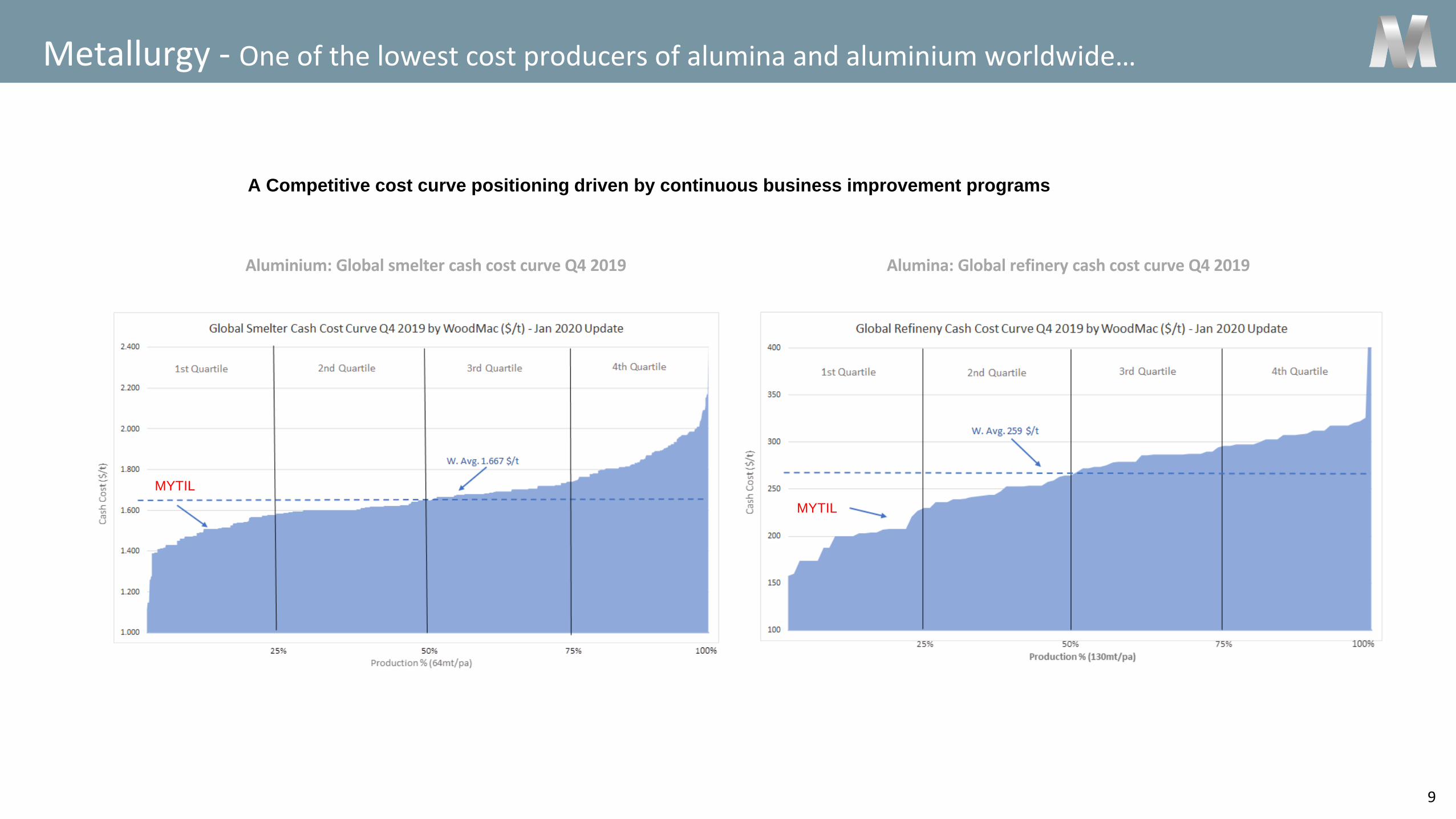

Metallurgy - One of the lowest cost producers of alumina and aluminium worldwide…

Alumina: Global refinery cash cost curve Q4 2019

A Competitive cost curve positioning driven by continuous business improvement programs

Aluminium: Global smelter cash cost curve Q4 2019

MYTIL

MYTIL

10

Metallurgy - ...with successful and continuous cost optimisation initiatives

Over €230mn of cumulative cost

savings were identified and

achieved since 2012

Total saving: €119mn Total saving: €78mn Total saving: €35mn

2012 – 2014 2015 – 2016 2017 – 2018

Improved operations from 4th quartile

to the 2nd quartile

Focused on raw material

supply and natural gas

cost

Continuous improvements

to remain 1st quartile

“Mellon” “Excellence”

34%

26%

17%

8%

8%7% Electricity

CHP

Operational

Other

Natural gas

Raw materials

2242

87 98 84124

166

1.500

1.750

2.000

2.250

2.500

020406080

100120140160180

2012 2013 2014 2015 2016 2017 2018

EBITDA €mm All-in Aluminium Sales Price $/tn

Hephaestus initiative

July 2019 – 2021

Cost base optimization and improving

refinery & smelter productivity

Total Targeting Savings: €60mn

(50% one-off - 50% recurring)

“The Best”

Initiatives aimed at expanding alumina & aluminium output, optimising procurement of

raw materials and other input costs, with continuous operational improvements

12

14

16

18

20

22

24

26

28

30

100

200

300

400

500

600

700

Dec

-13

Mar

-14

Jun

-14

Sep

-14

Dec

-14

Mar

-15

Jun

-15

Sep

-15

Dec

-15

Mar

-16

Jun

-16

Sep

-16

Dec

-16

Mar

-17

Jun

-17

Sep

-17

Dec

-17

Mar

-18

Jun

-18

Sep

-18

Dec

-18

Mar

-19

Jun

-19

Sep

-19

Dec

-19

Alumina Price % of LME

11

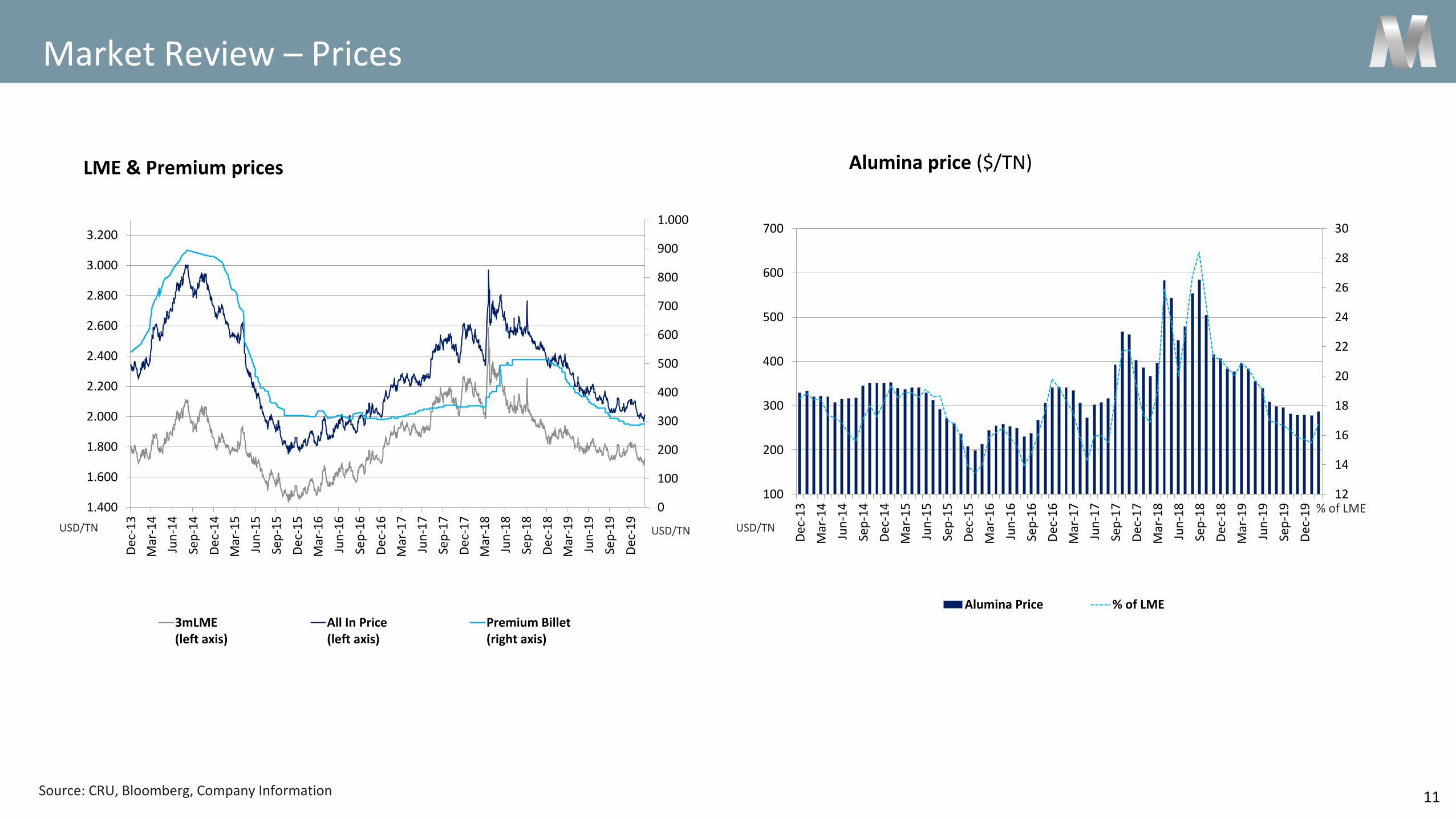

Market Review – Prices

Source: CRU, Bloomberg, Company Information

LME & Premium prices

USD/TNUSD/TN

Alumina price ($/TN)

% of LME

USD/TN

0

100

200

300

400

500

600

700

800

900

1.000

1.400

1.600

1.800

2.000

2.200

2.400

2.600

2.800

3.000

3.200

Dec

-13

Mar

-14

Jun

-14

Sep

-14

Dec

-14

Mar

-15

Jun

-15

Sep

-15

Dec

-15

Mar

-16

Jun

-16

Sep

-16

Dec

-16

Mar

-17

Jun

-17

Sep

-17

Dec

-17

Mar

-18

Jun

-18

Sep

-18

Dec

-18

Mar

-19

Jun

-19

Sep

-19

Dec

-19

3mLME(left axis)

All In Price(left axis)

Premium Billet(right axis)

12

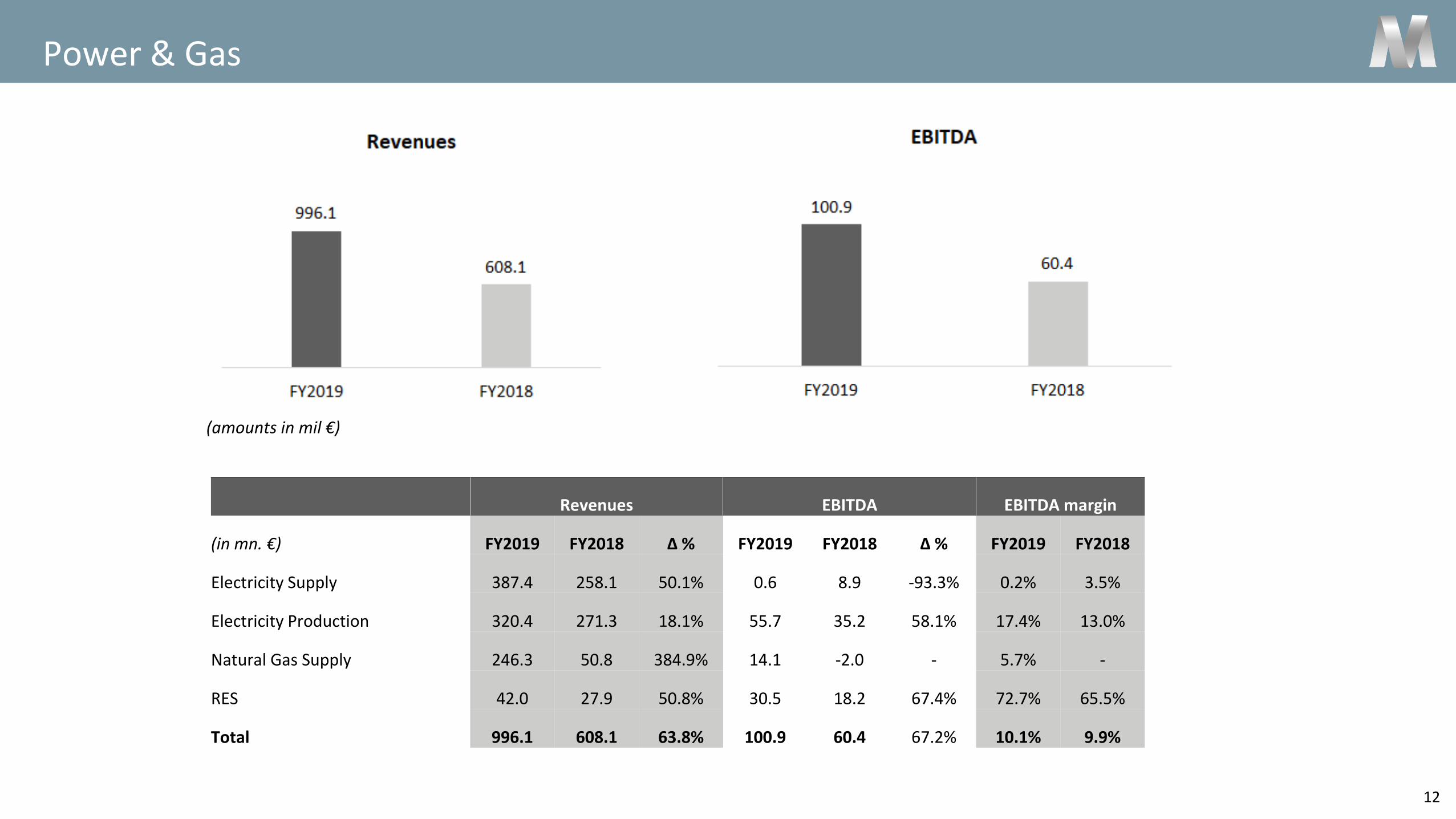

Power & Gas

(amounts in mil €)

Revenues EBITDA EBITDA margin

(in mn. €) FY2019 FY2018 Δ % FY2019 FY2018 Δ % FY2019 FY2018

Electricity Supply 387.4 258.1 50.1% 0.6 8.9 -93.3% 0.2% 3.5%

Electricity Production 320.4 271.3 18.1% 55.7 35.2 58.1% 17.4% 13.0%

Natural Gas Supply 246.3 50.8 384.9% 14.1 -2.0 - 5.7% -

RES 42.0 27.9 50.8% 30.5 18.2 67.4% 72.7% 65.5%

Total 996.1 608.1 63.8% 100.9 60.4 67.2% 10.1% 9.9%

13

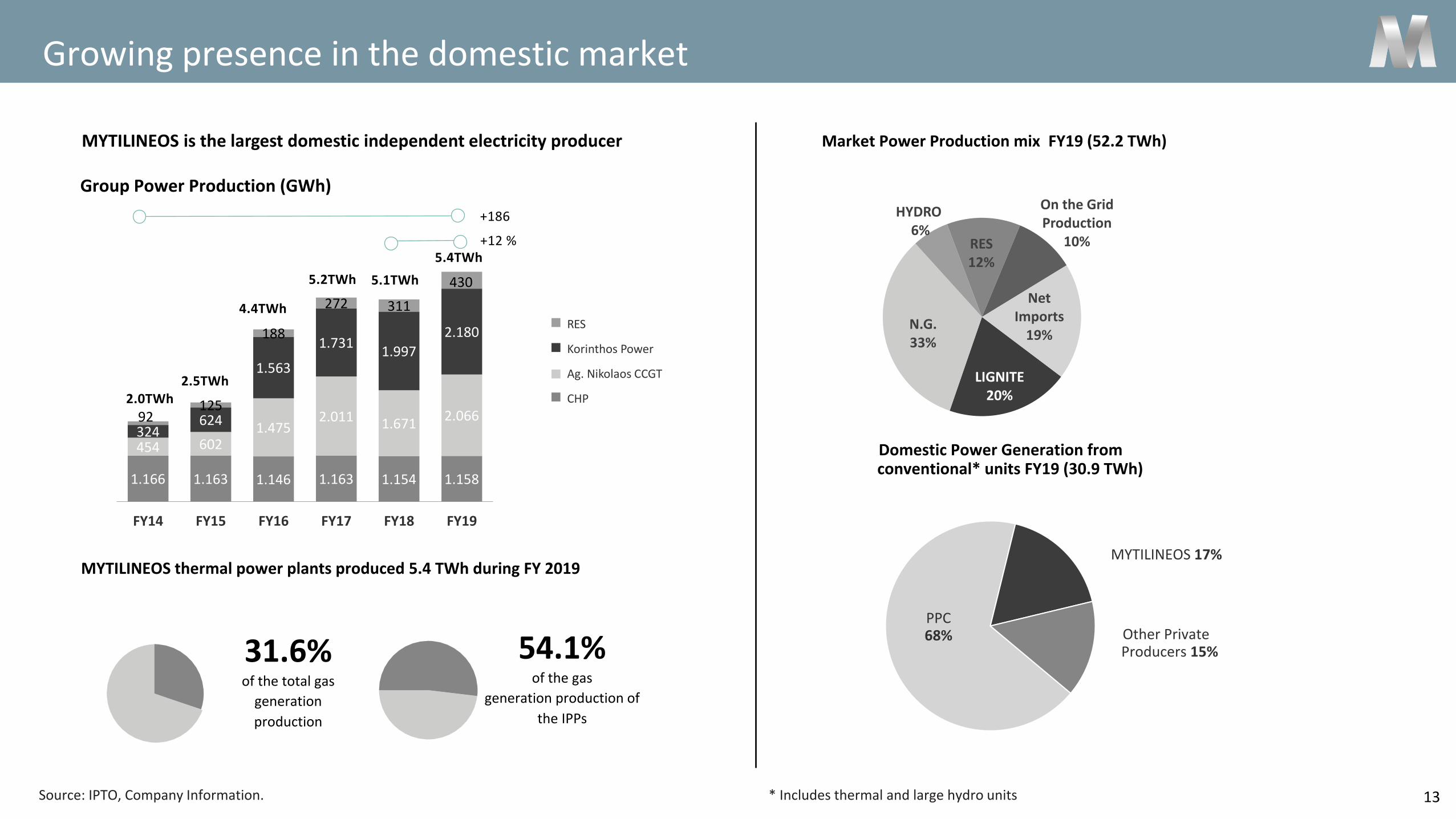

Growing presence in the domestic market

MYTILINEOS is the largest domestic independent electricity producer

1.166 1.163 1.146 1.163 1.154 1.158

454 6021.475

2.011 1.6712.066

324624

1.563

1.7311.997

2.180

92125

188

272 311

430

FY14 FY15 FY16 FY17 FY18 FY19

Group Power Production (GWh)

RES

+186

2.0TWh2.5TWh

4.4TWh

Ag. Nikolaos CCGT

CHP

Korinthos Power

5.2TWh 5.1TWh

PPC68%

MYTILINEOS 17%

Other Private Producers 15%

Domestic Power Generation from conventional* units FY19 (30.9 TWh)

Market Power Production mix FY19 (52.2 TWh)

MYTILINEOS thermal power plants produced 5.4 TWh during FY 2019

Source: IPTO, Company Information. * Includes thermal and large hydro units

+12 %

54.1%of the gas

generation production of

the IPPs

31.6%of the total gas

generation

production

5.4TWh

LIGNITE20%

N.G.33%

HYDRO6%

RES12%

On the Grid Production

10%

Net Imports

19%

56,0 56,859,2 59,2 59,7

62,8 64,0 65,3 65,3 66,369,7 70,2 70,5

73,776,8 77,6 77,7 78,0

81,4 82,6 82,8 83,4 83,7 83,8

0

10

20

30

40

50

60

70

80

90

Fuel + Variable O&M Cost (€/MWh) CO2 Cost (€/MWh) Bid (€/MWh) Avg SMP (€/MWh)

14

Merit Order: MYTILINEOS continues to rank first among thermal energy producers

Merit Order based on Bids – FY 2019

AVG SMP: 63.82 €/MWhPrice Makers Total Hours

% of Hoursper Fuel Type 2019

Lignite 1,652 18.9%

Gas 5,038 57.5%

Hydro 401 4.6%

Imports 1,080 12.3%

Exports 521 5.9%

Pumping 68 0.8%

Total 8,760 100.0%

Avg effective CO2: 24,71 €/tn

15

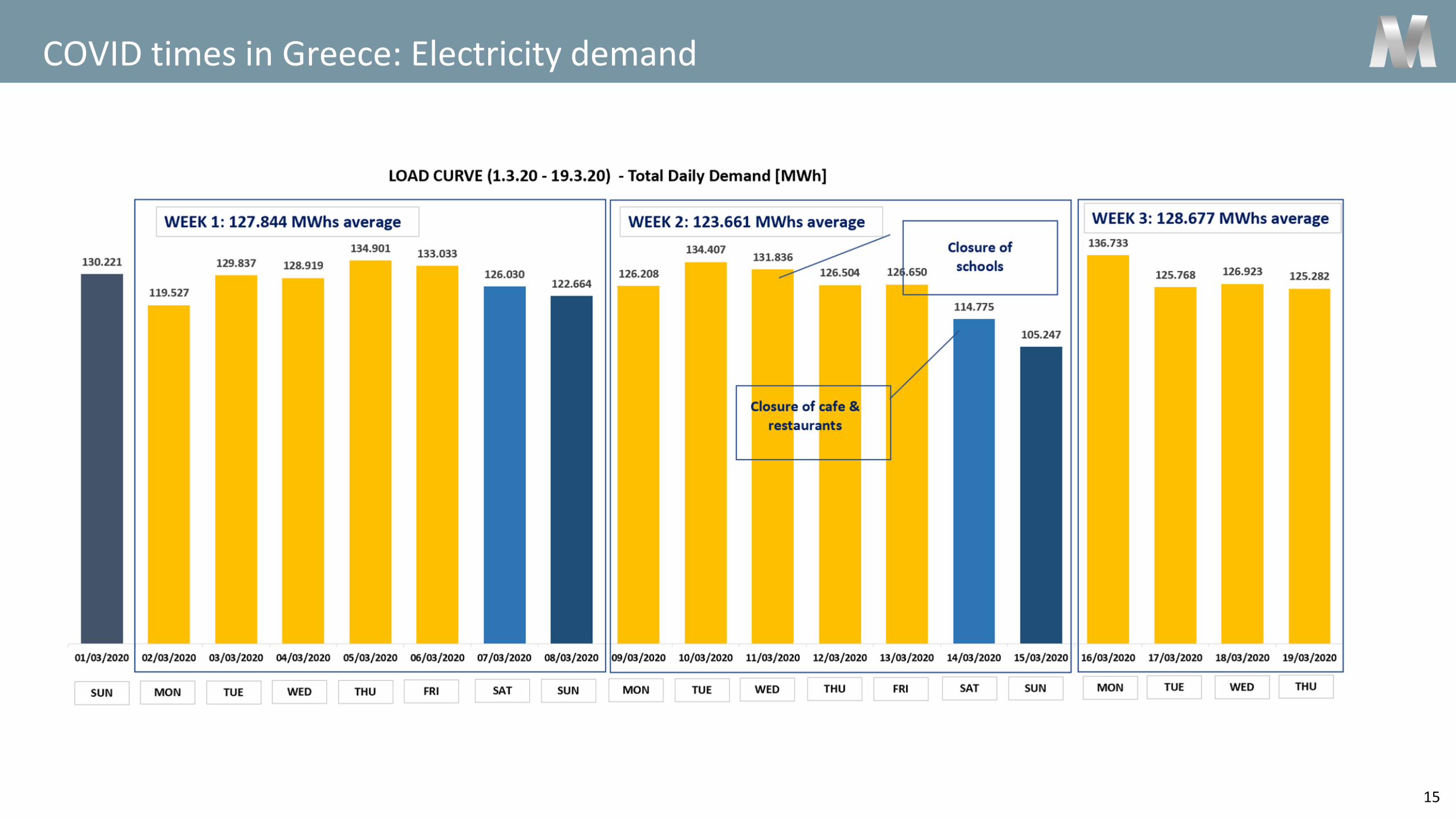

COVID times in Greece: Electricity demand

15,00

16,00

17,00

18,00

19,00

20,00

21,00

22,00

23,00

24,00

25,00

26,00

27,00

28,00

29,00

30,00

31,00

32,00

33,00

€ /

ΜW

h

WA Gas Price (€/MWh)

MYT Gas Price Indication (€/MWh)

-8%

-9%-12%

-11% -12%-11%

-13%

-18%

-10%

-7%-9% -6%

-18%

-26%-15%

-26%

-37%

-25%-27%

-35%

-19%

-33%

-37%

-26%

16

Power & Gas: Sourcing of natural gas at below weighted average gas prices for electricity in 2019

Source: LAGIE

(mn. €)up to 1

year1-3 years 3-5 years Total

Ghana 52.0 1.1 - 53.1

Libya 0 347.1 - 347.1

Greece 82.3 66.0 51.1 199.5

UK 60.7 - - 60.7

Spain 61.2 - - 61.2

Slovenia 88.2 24.2 - 112.4

Other 39.3 40.6 - 79.9

Total 383.8 479.1 73.7 914.0

17

EPC & Infrastructure

Backlog

(amounts in mil €)

Revenues EBITDA EBITDA margin

(in mn. €) FY2019 FY2018 Δ % FY2019 FY2018 Δ % FY2019 FY2018

EPC & Infrastructure 254.2 242.5 4.8% 20.3 41.4 -50.9% 8.0% 17.1%

Solar Parks 388.2 85.2 355.8% 29.1 4.5 547.4% 7.5% 5.3%

Maintenance Services & Other 23.4 39.7 -41.1% 1.9 9.0 -79.3% 8.0% 22.7%

Total 665.8 367.3 81.2% 51.2 54.9 -6.6% 7.7% 14.9%

18

Contact Information

Cleo Lymberis

IR DirectorT: +30 210 6877 412F: +30 210 6877 400E: [email protected]

Dimitris Katralis

IR OfficerT: +30 210 6877 476F: +30 210 6877 400E: [email protected]

MYTILINEOS S.A.8 Artemidos Str.

15125 Maroussi Athens GreeceT: +30 210 6877 300F: +30 210 6877 400