177

Tapping CARES Cash Quickly

PPP/Other Loans, Loss Carrybacks and Tax BreaksDon’t Let Opportunity Slip Away

Bradley Burnett, J.D., LL.M. (Taxation)

BradleyBurnettTaxSeminars.com

Disclaimer

• This presentation and accompanying course materials are designed to provide accurate and authoritative information as to the subject matter covered

• Neither the sponsor(s), distributor, publisher author, nor presenter, by and through this presentation, is rendering legal, accounting or other professional service

• This presentation and accompanying course materials does not create an attorney-client or accountant-client relationship

• If legal advice or other expert advice is required, the services of a competent professional should be sought

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 6

Managing Cash FlowDuring Crisis

• Article: Maintaining Cash Flow During Covid-19https://www.avma.org/resources-tools/animal-health-and-welfare/covid-19/maintaining-cashflow-covid-19

• Article: Focus on Cash Flow and Liquidity for Covid-19 Resilience (Grant Thornton)

https://www.grantthornton.com/library/articles/insights/2020/focus-cash-flow-liquidity-COVID-19-resilience.aspx

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 7

Clients Need Our Help

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 8

Covid Crisis DrivenNew Services to Client

1. Cash flow projections

a. Overall

b. Near term vs. long term

2. Tax cash flow projections

a. Analyze approach to lowest overall tax cost

b. 2020

c. Future years

d. Past years

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 9

Covid Crisis DrivenNew Services to Client

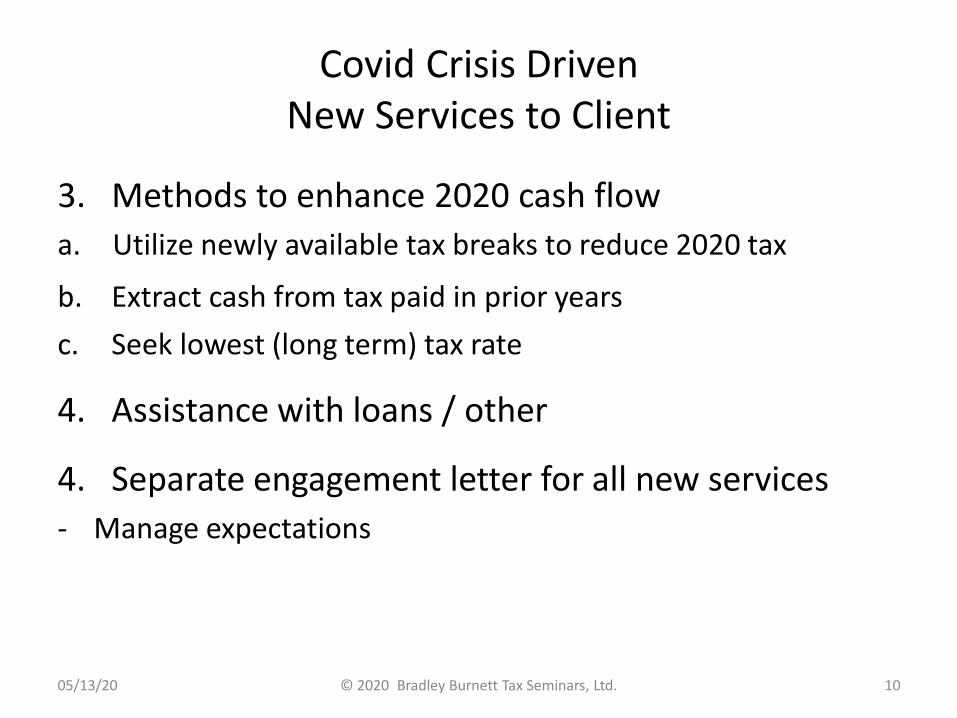

3. Methods to enhance 2020 cash flow

a. Utilize newly available tax breaks to reduce 2020 tax

b. Extract cash from tax paid in prior years

c. Seek lowest (long term) tax rate

4. Assistance with loans / other

4. Separate engagement letter for all new services

- Manage expectations

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 10

Polling Question 1

• How may an accountant assist a client through the Covid cash flow crisis

A. Cash flow projections

B. Compute best approach to reduce tax

C. Guide to PPP forgiveness

D. All of the above

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 11

Tapping CARES Cash Quickly

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 12

Tapping CARES Cash Quickly9 Ways

1. Delay 2020 Tax (or Other) Payments

2. Reduce 2020 Tax Liability / Payments

3. Reduce Payments on Unfiled Returns

4. Amended Returns (or Not?)

5. Loans

6. Employee Retention Credit

7. Defer Contributions to Retirement Plans

8. Retirement Plan Withdrawals

9. Loans from Retirement Plans

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 13

Delay 2020 Tax Payments

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 14

Notice 2020-23Payments Due

• Notice 2020-18 and 2020-23 – Any person w/ a federal tax payment due from 04/01/20 to 07/14/20 is affected by COVID-19

1. Payment (no dollar limit) due date extended (from 04/01/20 through 07/14/20) to 07/15/20

- If tax already paid, no effect

2. Waiver (until 07/15/20) of statutory additions for

a. Interest

b. Penalties

c. Additions to tax

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 15

Delay 2020 Tax Payments

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 16

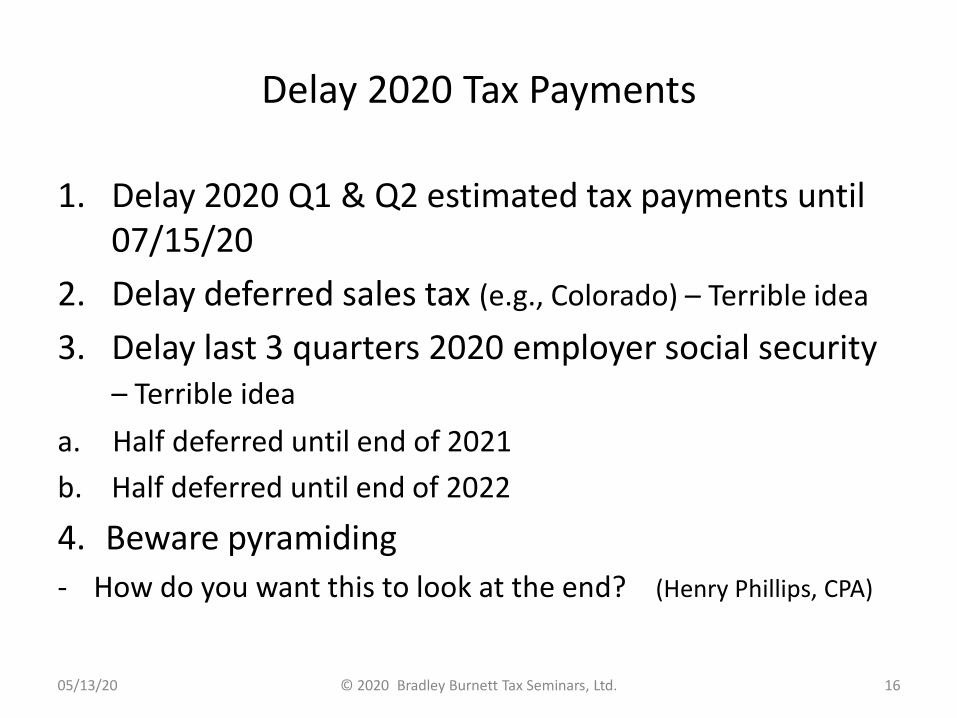

1. Delay 2020 Q1 & Q2 estimated tax payments until 07/15/20

2. Delay deferred sales tax (e.g., Colorado) – Terrible idea

3. Delay last 3 quarters 2020 employer social security – Terrible idea

a. Half deferred until end of 2021

b. Half deferred until end of 2022

4. Beware pyramiding

- How do you want this to look at the end? (Henry Phillips, CPA)

Pyramidsof Taxes

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 17

Pyramidsof Taxes

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 18

1. Delay in payment of taxes until 07/15/20 defers $300B in tax payments

- If spend or lose the money, in trouble on 07/15/20

2. In my 38 years of practice, 85-90% of time client falls behind on payroll (or sales or income) tax, they don’t climb out of it

Cutting Taxes

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 19

Reduce 2020 Tax Payments

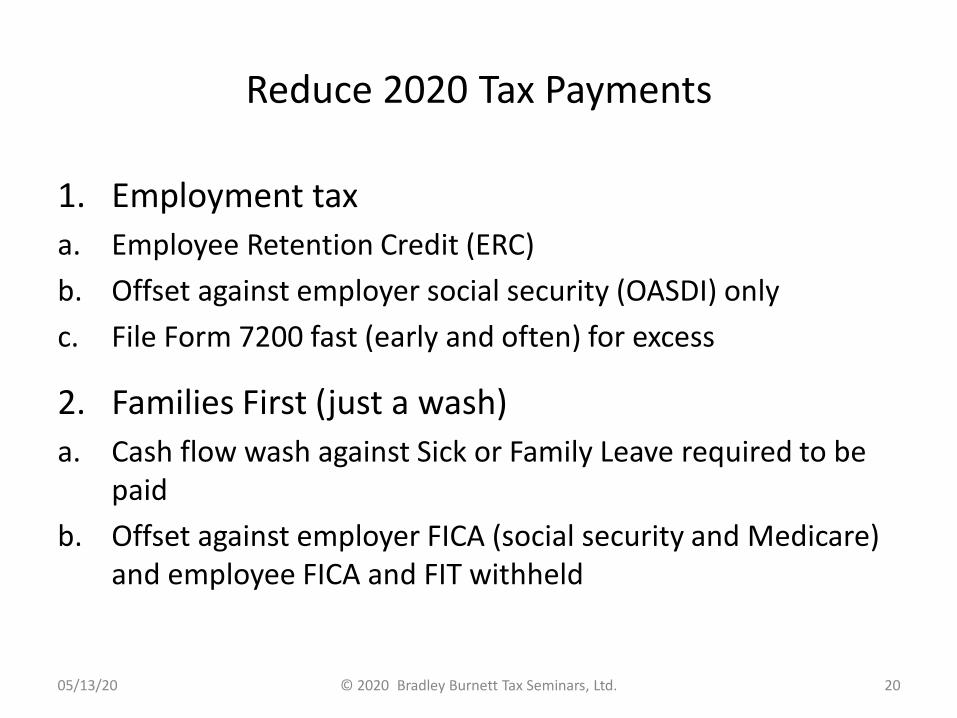

1. Employment tax

a. Employee Retention Credit (ERC)

b. Offset against employer social security (OASDI) only

c. File Form 7200 fast (early and often) for excess

2. Families First (just a wash)

a. Cash flow wash against Sick or Family Leave required to be paid

b. Offset against employer FICA (social security and Medicare) and employee FICA and FIT withheld

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 20

Reduce 2020 Tax Payments

3. Income tax

a. Recompute to include faster QIP if QIP PPIS > 12/31/17

b. Elect out of bonus?

c. Elect out of §179 claimed in past to free up basis for 2020?

d. In 2020, prospective Form 3115 for legislative tweaks to past?

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 21

Polling Question 2

• Employment tax credits against Family First mandated payments are just a wash

A. Yep

B. Not so much

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 22

Reduce Payments on Unfiled Returns

• Reduce payments with unfiled returns (2019)* (*or, 2018 and/or prior if late)

1. Recompute to include QIP if QIP PPIS > 12/31/17 2. Elect out of §179 if prior taken?3. If §163(j) applies, factor in new 50% (not 30%) 2019 ATI cap

(or elect out)4. Recompute usable loss after deletion of tweaked §461(l) for

2018, 2019 and 20205. Adjust for NOL 100% absorption rate6. Adjust for carryback 5 years (instead of carryforward only) or

waive carryback7. In 2020, prospective Form 3115 for legislative tweaks to

past?

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 23

Amended Returns (or Not?)

• Amended returns or not

1. 2019, 2018 and, resultingly, back 5 years to prior years

2. Same factors as with “unfiled returns” slides above

3. Determine effects on cash now, later

4. Income tax rates then, now, later?

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 24

Loans

• Loans – PPP, EIDL or both (and/or other)

1. Next move? Apply for PPP, EIDL and/or other?

2. PPP a. Proper app / accounting for max forgiveness, avoid fraud

b. Structure for best use of expenditures funded by loan

3. EIDL proper application / accounting to avoid fraud

4. Borrowing from other sources?

5. Structure all loans for interest expense deductibilitya. §163(j)

b. Interest tracing rules

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 25

Employee Retention Credit

• Employee retention credit for employers subject to closure due to Covid who continue to pay employees wages during closure (CARES §2301)

1. Credit = Up to $5,000/employee (i.e., 50% of compensation ($10,000/’ee comp cap) to each ‘ee)

2. Credit offsets against ‘er share of FICA, excess refunded

3. Not available if receive Paycheck Protection Program loan

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 26

Minimum Required Contributions toSingle Employer Qualified Retirement Plans

• CARES permits minimum contributions to certain single employer qualified retirement plans otherwise due in 2020 to be delayed until 01/01/21

1. Delayed contributions carry interest to be paid on delay

2. For defined benefit plans, sponsors may use adjusted funding target attainment percentage for prior year

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 27

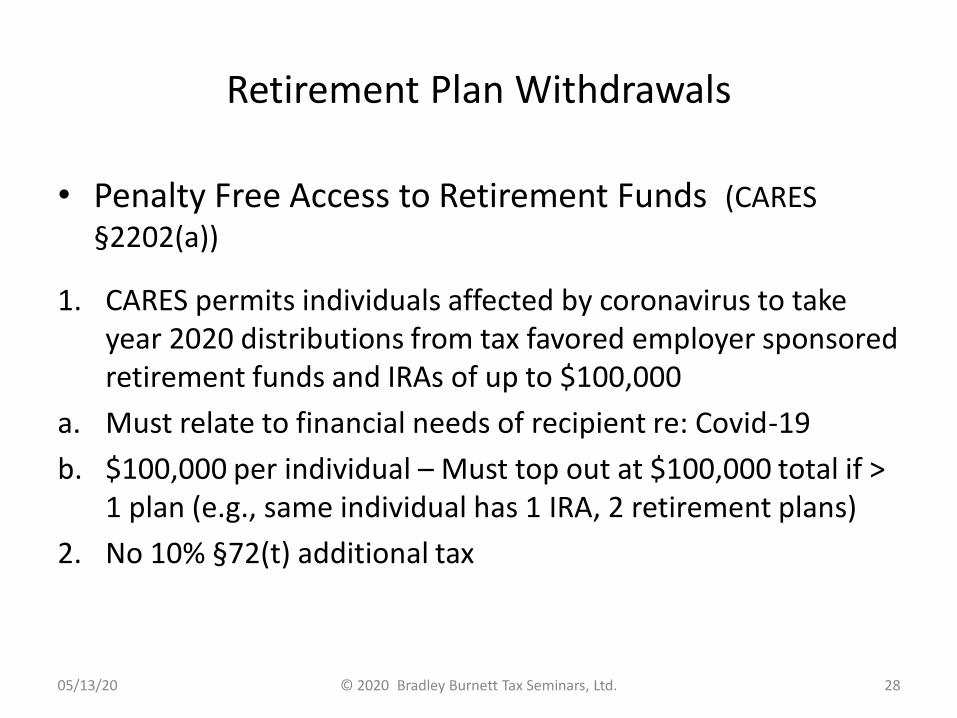

Retirement Plan Withdrawals

• Penalty Free Access to Retirement Funds (CARES §2202(a))

1. CARES permits individuals affected by coronavirus to take year 2020 distributions from tax favored employer sponsored retirement funds and IRAs of up to $100,000

a. Must relate to financial needs of recipient re: Covid-19

b. $100,000 per individual – Must top out at $100,000 total if > 1 plan (e.g., same individual has 1 IRA, 2 retirement plans)

2. No 10% §72(t) additional tax

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 28

Retirement Plan Withdrawals

• Penalty Free Access to Retirement Funds (CARES §2202(a))

3. Income spread ratably over 3 years at recipient’s election on 2020 return

a. Individual may repay within 3 year period

b. Any amount repaid (by 3 years after distribution received) treated as rollover (FAQ #7)

c. If 2020 distribution repaid in 2022, then distribution not taxable (FAQ #7)

- Amended returns for tax refund available for 2020 and 2021

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 29

Retirement Plan Withdrawals

4. FAQs: Coronavirus-related relief for retirement plans and IRAs questions and answers (IRS Notice expected soon)

https://www.irs.gov/newsroom/coronavirus-related-relief-for-retirement-plans-and-iras-questions-and-answers

5. Coronavirus-related distribution (FAQ #4 (05/04/20))

= Distribution made from eligible retirement plan to qualified individual from 01/01/20 to 12/30/20 up to total of $100,000 from all plans and IRAs

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 30

Retirement Plan Withdrawals

6. Qualified individual (FAQ #3 (05/04/20))

a. Diagnosed w/ COVID-19 by test approved by CDC

b. Spouse or dependent diag. w/ COVID-19 by test approved by CDC

c. Adverse financial consequences as result of quarantine, furlough or lay off or work hours reduced due to COVID-19

d. Adverse financial consequences if unable to work (or lack of child care) due to COVID-19

e. Adverse financial consequences for owner or operator of business if closing or reducing hours of business due to COVID-19

f. IRS and Treasury may expand list

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 31

Increased Limits on LoansFrom Retirement Plans

• Increased Limits on Loans From Retirement Plans for Individual Affected by Covid (CARES §2202(b))

1. To qualify, loans must be taken from qualified plan during 180 days after 03/27/20 (from 03/27/20 to 09/22/20) (FAQ #8)

2. Loan may be up to 100% of participant’s vested accrued benefit

3. Increases loan dollar limit to lesser of:

a. $100,000 (minus individual’s outstanding plan loans), or

b. Individual's vested benefit under plan

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 32

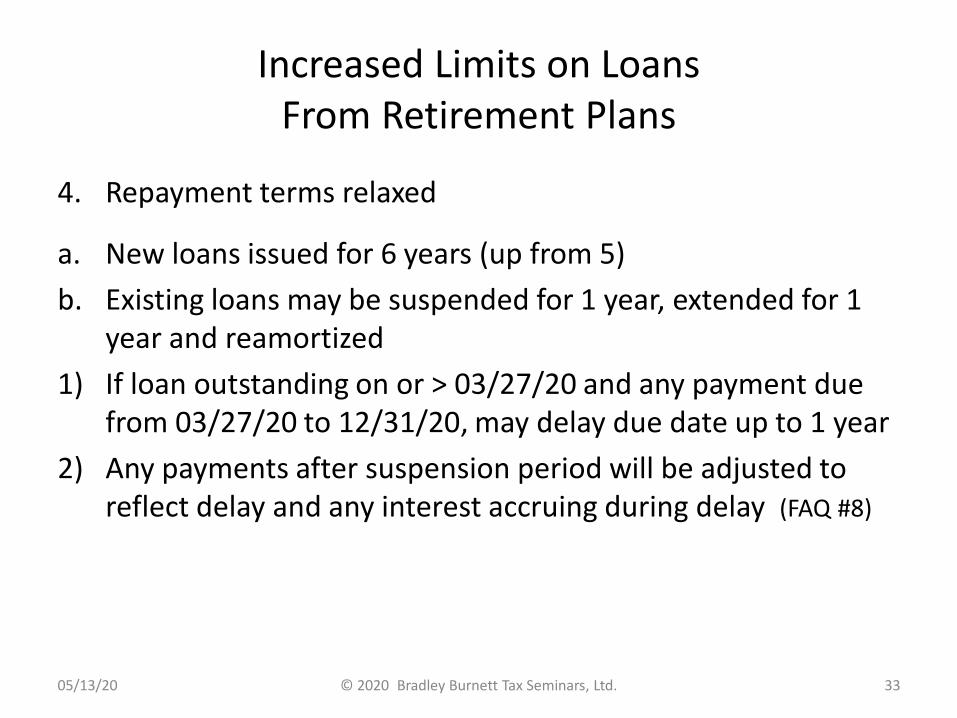

Increased Limits on LoansFrom Retirement Plans

4. Repayment terms relaxed

a. New loans issued for 6 years (up from 5)

b. Existing loans may be suspended for 1 year, extended for 1 year and reamortized

1) If loan outstanding on or > 03/27/20 and any payment due from 03/27/20 to 12/31/20, may delay due date up to 1 year

2) Any payments after suspension period will be adjusted to reflect delay and any interest accruing during delay (FAQ #8)

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 33

CARES Distribution and Loan Rule AdoptionOptional to Employers

1. Employer permitted to choose whether, and to what extent, to amend its plan to provide for Covid related distributions and/or loans CARES provisions (FAQ #9)

2. Example: Employer may choose to provide for Covid related distributions, but choose not to change its plan loan provisions or loan repayment schedules

3. Even if employer does not treat a distribution as Covidrelated, a qualified individual may treat a distribution that meets requirements to be a Covid related distribution on individual's Form 1040

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 34

PPP Loan App AcceptanceRound 2 Began 04/27/20

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 35

PPP

1. Timing, timing, timing

2. File new app or tweak unapproved app

3. PPP – How much?

4. PPP – How to use?

5. PPP – How much forgiven?

6. Guidance – Huge holes

7. PPP vs. EIDL vs. Other

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 36

PPP Loans The Law of the Street

05/13/20

1. The law of the law

vs.

2. The law of the street

vs.

3. The law of later

© 2020 Bradley Burnett Tax Seminars, Ltd. 37

PPP LoansFirst Come, First Served

1. PPP loans are first come, first served (Treasury Interim Rule, p.

13)

a. 1st batch of money ($349B) ran out in about 2 weeks

b. 2nd batch ($310B) signed by President (04/24/20)

c. New apps accepted on 04/27/20

2. Applicant may only apply for one PPP loan (Treasury Interim

Rule, p. 12)

3. PPP loan applied for to commercial lender via PPP Loan App (New SBA Form 2483)

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 38

PPPStatutory Provisions

• CARES Act PPP statutory provisions (H.R. 748, P.L. 116-136

(03/27/20), Act §§1102, 1106)

1. CARES Act §1102 - Paycheck Protection Program (amending Act

§7(a) of Small Business Act (15 U.S.C. §636(a))

2. CARES Act §1106 – PPP Loan Forgiveness (amending Act §7(a) of

Small Business Act (15 U.S.C. §636(a))

3. https://www.congress.gov/bill/116th-congress/house-bill/748/text

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 39

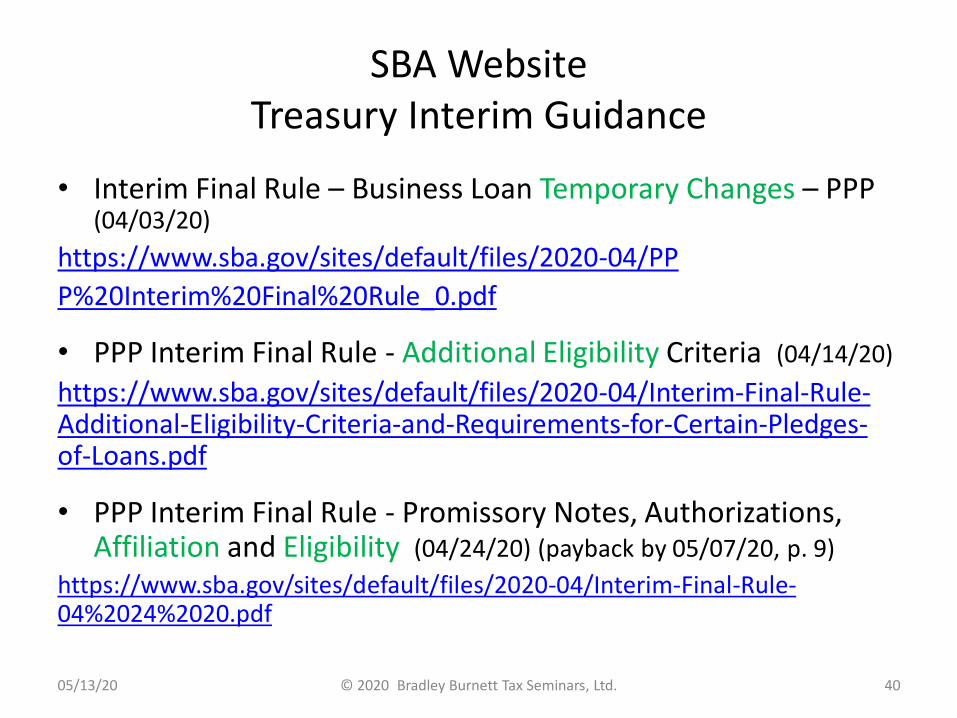

SBA WebsiteTreasury Interim Guidance

• Interim Final Rule – Business Loan Temporary Changes – PPP (04/03/20)

https://www.sba.gov/sites/default/files/2020-04/PP

P%20Interim%20Final%20Rule_0.pdf

• PPP Interim Final Rule - Additional Eligibility Criteria (04/14/20)

https://www.sba.gov/sites/default/files/2020-04/Interim-Final-Rule-Additional-Eligibility-Criteria-and-Requirements-for-Certain-Pledges-of-Loans.pdf

• PPP Interim Final Rule - Promissory Notes, Authorizations, Affiliation and Eligibility (04/24/20) (payback by 05/07/20, p. 9)

https://www.sba.gov/sites/default/files/2020-04/Interim-Final-Rule-04%2024%2020.pdf

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 40

SBA WebsiteFAQ and Other Guidance

• FAQs for Lenders and Borrower (Updated 05/13/20) (Updated almost daily, so keep checking)

https://www.sba.gov/sites/default/files/2020-05/Paycheck-Protection-Program-Frequently-Asked-Questions_05%2013%2020.pdf

• PPP Affiliation Interim Final Rule (04/03/20) (Excellent 1 ½ page summary of complex SBA affiliation rules) (Best ”forest for trees” read)

https://www.sba.gov/document/policy-guidance--ppp-affiliation-interim-final-rule

• PPP Additional Criterion for Seasonal Employers (04/28/20)

https://home.treasury.gov/system/files/136/Interim-Final-Rule-Additional-

Criterion-for-Seasonal-Employers.pdf

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 41

Paycheck Protection Program (PPP)Nitti Articles re: Chaotic Guidance

• Nitti article (Forbes (04/05/20)) re: payroll costshttps://www.forbes.com/sites/anthonynitti/2020/04/05/paycheck-protection-program-loans-three-things-the-sba-and-banks-need-to-agree-on-now/#7031c2f41a32

• Nitti article (Forbes (04/15/20)) re: PPP loan forgivenesshttps://www.forbes.com/sites/anthonynitti/2020/04/15/ten-things-we-need-to-know-about-paycheck-protection-program-loan-forgiveness/?utm_source=newsletter&utm_medium=email&utm_campaign=forbes-announcements#11185b1e3291

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 42

Paycheck Protection Program (PPP)AICPA Resource Center

• AICPA Coronavirus (COVID-19) Resource Center

https://www.aicpa.org/news/aicpa-coronavirus-resource-center.html

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 43

Should Taxpayer’s Accountant or AttorneyServe as Agent on PPP Loan App?

• Should Taxpayer’s Accountant or Attorney Serve as Agent on PPP Loan App (SBA Form 2483) ?

1. Absolutely not. Potential liability stunningly unacceptable.

2. New SBA Form 2483 (04/20) need not be signed by agent. Should not be done by agent, even via POA.

a. Client attests to info, not agent

b. How could agent know all of that info anyway?

3. Agent fees paid from lender fees. Banks don’t want to share.

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 44

Should Taxpayer’s Accountant or AttorneyServe as Agent on PPP Loan App?

3. Agents may not collect fees from the borrower or be paid out of the PPP loan proceeds (Treasury Interim Rule p. 11)

4. AICPA opinion: Accountant can be paid usual fees to answer questions as to consequences and tax effects of various answers to questions on app

5. Engagement letter highly recommended for Covid issues

https://www.aicpa.org/interestareas/privatecompaniespracticesection/qualityservicesdelivery/sba-paycheck-protection-program-resources-for-cpas/aicpa-statement-on-cpas-as-agents-for-ppp-applications.html

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 45

Polling Question 3

• Should an advisor sign a client’s PPP loan app in good faith?

A. No way, Jose

B. Go for it in a blaze of glory

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 46

Loans

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 47

Paycheck Protection ProgramLoans

• Loan program to any business, §501(c)(3) non-profit, veteran’s org or tribal business with 500 or < ‘ees(that live in U.S.) (CARES Act §§1102, 1106)

1. Designed to keep workforce together

2. Borrow PPP, spend on (mostly) payroll costs

3. May be forgiven in whole or part if pay (mostly) payroll

4. Self-employed qualify for themselves

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 48

PPP LoansThree Aspects

• Three aspects of PPP loans

1. Source

- Whether, when and how to apply

2. Use

- Discipline to apply proceeds to allowable uses

3. Forgiveness

- Achieving forgiveness by jumping through hoops

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 49

PPP Source

• How Much Can You Borrow?

Loan cap = Lesser of

1. $10M, or

2. Average monthly payroll x 2.5 *

* Plus, if applicable, refinancing into PPP of SBA EIDL loan made between 01/31/20 and 04/03/20

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 50

PPPUse

• Allowed use of PPP loans (CARES Act §1102(a)(2))

1. Payroll costs (CARES Act §1102(a)(2), 15 USC §636(a)(36)(A)(viii))

2. Mortgage interest payments (but not prepayments or principal

payments) (CARES Act §1102(a), 15 USC §636(a)(36)(F)(i)(VI))

3. Rent payments (including rent under a lease agreement) (CARES Act

§1102(a), 15 USC §636(a)(36)(F)(i)(V))

4. Utilities (CARES Act §1102(a), 15 USC §636(a)(36)(F)(i)(IV))

5. Interest on any other debt (incurred before 02/15/20) (CARES Act

§1102(a), 15 USC §636(a)(36)(F)(i)(VII))

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 51

PPPForgiveness

• Allowed forgiveness of PPP loans (CARES Act §1106(b)) – Any below

amount paid or incurred in 8 weeks beginning w/ date of loan origination:

1. Payroll costs (CARES Act §1106(a)(8) refers to §1102(a)(2), 15 USC §636(a)(36)(A)(viii))

2. Mortgage interest payments (liability of borrower, mortgage on real or personal property and incurred before 02/15/20) (but not prepayments or principal payments) (CARES Act §1106(a)(7)(B))

3. Rent payments (“lease agreement in force before 02/15/20”) (CARES Act §1106(a)(4))

4. Utility payments (electric, gas, water, transportation, telephone or internet access for which service began before 02/15/20) (CARES Act §1106(a)(5))

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 52

PPPUse vs. Forgiveness

Allowed (or Not) Item Use Forgiveness

Payroll costs Yes Yes

Mortgage interest payments (but not prepayments or principal payments)

Yes No, unless specifics below met

Mortgage interest payments (liability of borrower, mortgage on real or personal property

and incurred before 02/15/20) (but not prepayments or principal payments)

Yes Yes

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 53

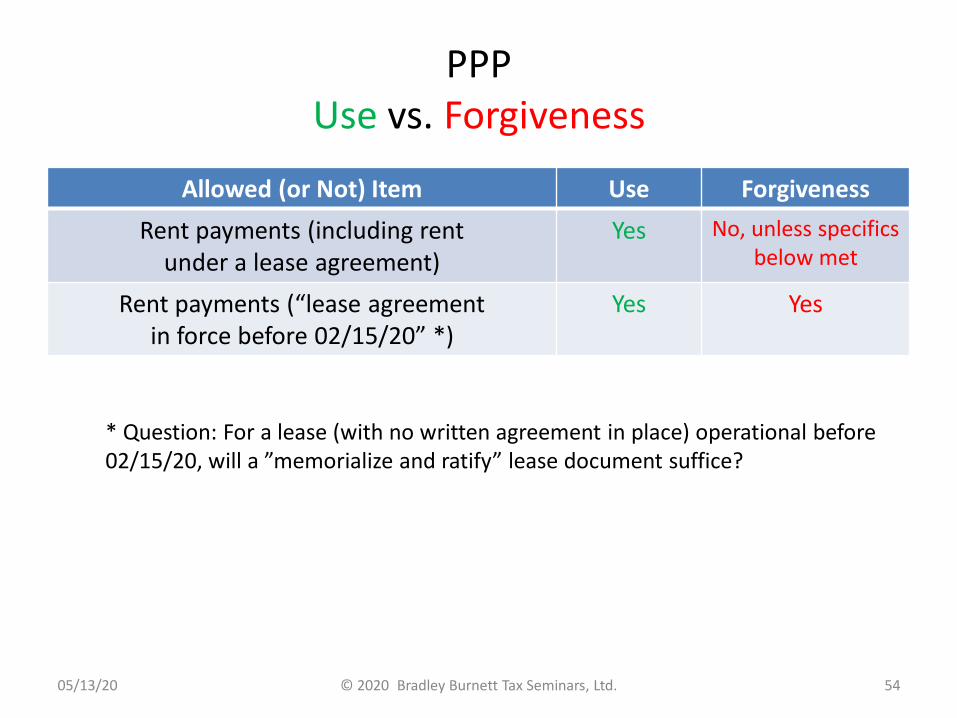

PPPUse vs. Forgiveness

Allowed (or Not) Item Use Forgiveness

Rent payments (including rent under a lease agreement)

Yes No, unless specifics below met

Rent payments (“lease agreement in force before 02/15/20” *)

Yes Yes

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 54

* Question: For a lease (with no written agreement in place) operational before02/15/20, will a ”memorialize and ratify” lease document suffice?

PPPUse vs. Forgiveness

Allowed (or Not) Item Use Forgiveness

Utility payments Yes No, unless specifics below

met

Utility payments (electric, gas, water, transportation, telephone or internet access for

which service began before 02/15/20)

Yes Yes

Interest on any other debt (only debt incurred before 02/15/20)

Yes No

Other No No

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 55

PPPSource vs. Use vs. Forgiveness

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 56

Source Use Forgive (but 75%)

Period 2.5 months 8 weeks 02/15/20 - 06/30/20

Salary (max $100,000) X X X

’Ee benefits X X X

Interest (debt < 02/15/20) X X

Rent (in force < 02/15/20) X X

Utility (service began < 02/15/20) X X

Interest on other mortgages X

Non-mortgage interest X

Other rent X

Other utilities X

Other

Polling Question 4

• If a PPP borrower does not utilize PPP loan proceeds properly for forgiveness, they will suffer

A. Truth

B. Falsity

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 57

SBA PPP Loan Application

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 58

PPPMechanics of Use

• Mechanics of use of covered loans*

1. Deposit entire loan proceeds into separate bank** account

a. Directly pay allowables from that separate bank accountb. Track on a separate spreadsheet!!

c. Perhaps track in separate set of books, then merge

* How the accountant saves the company

** Either new account or existing other (shell or savings) account

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 59

PPPMechanics of Use

• Mechanics of use of covered loans

2. Other less direct approaches quite risky

a. Burden of proof on borrower (taxpayer)

b. Risks 1) Not all of loan forgiven

2) Recourse debt may result

3) Origination fees may not be reimbursed by SBA

4) Violates certification that $ will go to allowable uses – Possible fraud

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 60

PPPMechanics of Use

• Mechanics of use of covered loans

3. Less preferable method = From separate account, reimburse operating account for expenditures made from it

a. Carefully account in detail for exact items reimbursed

b. Make accounting extremely careful (like w/ an accountable plan

(under §62(c), §1.62-2))

1) Problem: People in chaos are not careful

2) Imprecise transfers (to cover broad spending) leave you exposed

4. Think interest tracing rules (§1.163-8T and -10T) by analogy- There, if you don’t prove what spent loan proceeds on, you’re toast

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 61

PPPMechanics of Use

Approach Good Result Bad Result

Drop loan proceeds in separate PPP bank account, pay allowed items directly

Best approach Not bad if done correctly

Other less direct approaches Not as good Maybe OK

From separate account, reimburse operating account for items made from it

Not as good Maybe OK

Drop PPP into general operating account Not best at all Potentially horrible result

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 62

Protect the permanent over the temporary – Temporary inconvenience is tolerable

PPPPayroll Costs

• Loan cap = Lesser of

1. $10M, or

2. Average monthly payroll x 2.5

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 63

PPPPayroll Costs

Allowed (or Not) Item Use Forgiveness

Employee principal place of residence inside U.S. Yes Yes

Employee principal place of residence outside U.S. No No

Employee salary, wages, commissions, similar comp Yes Yes

Portion of individual ’ee salary exceeding $100,000 annual salary (prorated for covered period)

No No

Wages paid by employee leasing company (e.g. PEO)* Yes Yes

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 64

(CARES Act §1102(a)(2), 15 USC §636(a)(36)(A)(viii)(I)) * Treas. FAQ #10

PPPPayroll Costs

Allowed (or Not) Item Use Forgiveness

Cash tips or equivalent (based on employer records or reasonable, good-faith employer estimate)

Yes Yes

Allowance for separation or dismissal Yes Yes

Vacation, parental, family*, medical* or sick* leave (*but, not under Families First Act)

Yes Yes

Sick, family or medical leave under Families First Act No No

Payment of group health care coverage, including insurance premiums

Yes Yes

Payment by ‘er of retirement plan contributions Yes Yes

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 65

(CARES Act §1102(a)(2), 15 USC §636(a)(36)(A)(viii)(I))

PPP Payroll CostsEmployment Taxes

Allowed (or Not) Item Use Forgiveness

Employee salary, wages, commissions, similar comp Yes Yes

Fed (OASDI and Medicare (HI), FIT, RR) withheld from employee

Yes Yes

State / local (SIT, other) withheld from employee Yes Yes

Employer OASDI and Medicare (HI) No No

Employer FUTA No No

Payment of state / local tax on ’ee comp (e.g., SUTA) Yes Yes

Workers’ Comp No No

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 66

(CARES Act §1102(a)(2), 15 USC §636(a)(36)(A)(viii)(I))

Payroll CostsHot Spots

1. How to compute the $100,000/employee cap on compensation (in computation of “payroll costs”)?

a. Though statute poorly written, it appears any comp in excess of $100,000/employee excluded from “payroll costs”

b. Is it:

1) Salary capped at $100,000, with other payroll costs (e.g., health insurance premium) in addition*, or

2) Are “combined salary plus extras”** subject to $100,000 cap?

* Statute and Form 2483 Instructions support this position

** Treasury Interim Rule supports this position

c. Answer: $100,000 salary + other payroll costs (Treas FAQ #7 4/07/20)

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 67

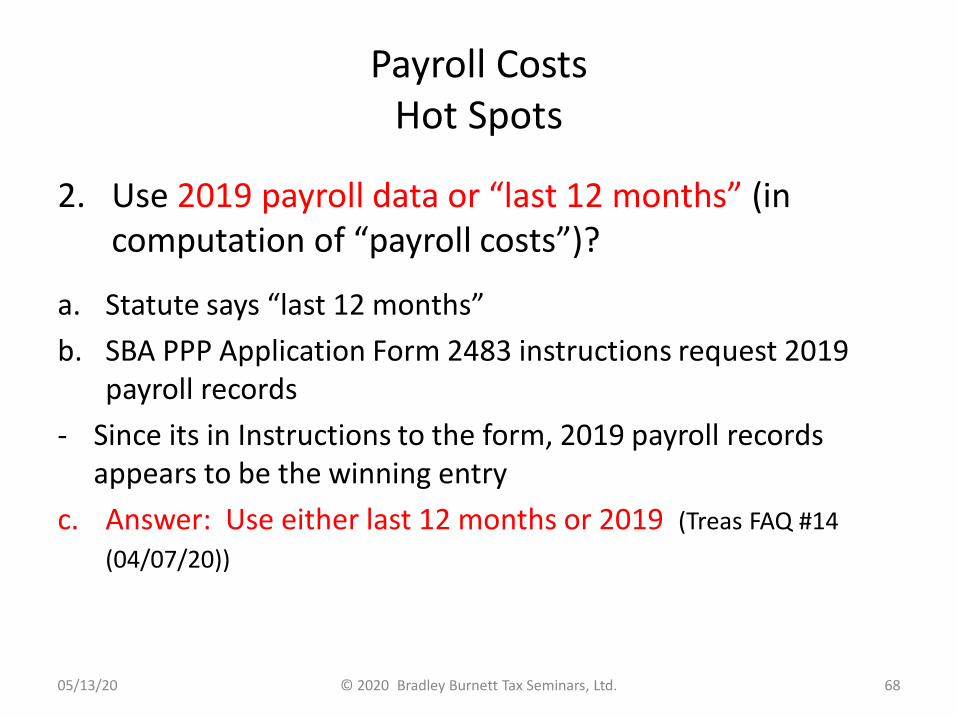

Payroll CostsHot Spots

2. Use 2019 payroll data or “last 12 months” (in computation of “payroll costs”)?

a. Statute says “last 12 months”

b. SBA PPP Application Form 2483 instructions request 2019 payroll records

- Since its in Instructions to the form, 2019 payroll records appears to be the winning entry

c. Answer: Use either last 12 months or 2019 (Treas FAQ #14

(04/07/20))

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 68

Payroll CostsHot Spots

3. How to test for eligibility for PPP for a seasonal business? (Treas. FAQ #9 (04/07/20))

a. General requirement that business be operational on 02/15/20

b. If not in operation on 02/15/20 (e.g., concessions at baseball park), business may be eligible if either

1) In operation on 02/15/20, or

2) For 8 week period between 02/15/20 and 06/30/20

Note: For seasonal business, to determine payroll cost time period, see Treas. FAQ #14 (04/07/20)

• PPP Additional Criterion for Seasonal Employers (04/28/20)

https://home.treasury.gov/system/files/136/Interim-Final-Rule-Additional-

Criterion-for-Seasonal-Employers.pdf

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 69

Payroll CostsHot Spots

4. Are S Corp shareholder salaries included in payroll costs?

a. Salaries count as “payroll costs” in both statute and Treas. Interim Guidance

b. Not prohibited in Treas. Interim Guidance or elsewhere

c. These are compelling arguments for inclusion as “payroll costs”

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 70

PPP – SBA Additional GuidanceIndependent Contractors, Partnerships, Partners

• PPP Interim Final Rule - Additional Eligibility Criteria Requirements for Certain Pledges of Loans (04/14/20)

1. Details rules for computing loan eligibility for IC

2. Clarifies how partnerships apply for comp of partners

https://www.sba.gov/document/policy-guidance--ppp-interim-final-rule-additional-eligibility-criteria-requirements-certain-pledges-loans

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 71

Payroll CostsHot Spots

5. Are guaranteed payments to partners included in payroll costs or not?

a. Partnerships apply for partners1) “Self-employment income of general active partners may be

reported as a payroll cost”

2) Cap of “$100,000 annualized”

b. Partners do not apply on own behalf

SBA Business Loan Program Temporary Changes: Paycheck Protection Loan – Additional Eligibility Criteria and Requirements for Certain Pledges of Loans (04/14/20) (p. 5)

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 72

PPP Payroll CostsPartnerships and Partners

Payroll Costs (Source) Use Forgiveness

Partnership submits app to borrow for payroll cost of “SE income” of “general active partners”

5 categories

Need guidance

Appears to include guaranteed payments for services paid to partners

“ “

Appears to include all SE taxable income reported to partner by partnership

“ “

Does not appear to add health insurance premium or retirement plan contribution on top of SE income

“ “

Capped at $100,000 per partner (annualized) “ “

Does not specify as to 2019 vs. 2020 “ “

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 73

SBA Business Loan Program Temporary Changes: Paycheck Protection Loan –Additional Eligibility Criteria … (04/14/20) (p. 5)

Payroll CostsHot Spots

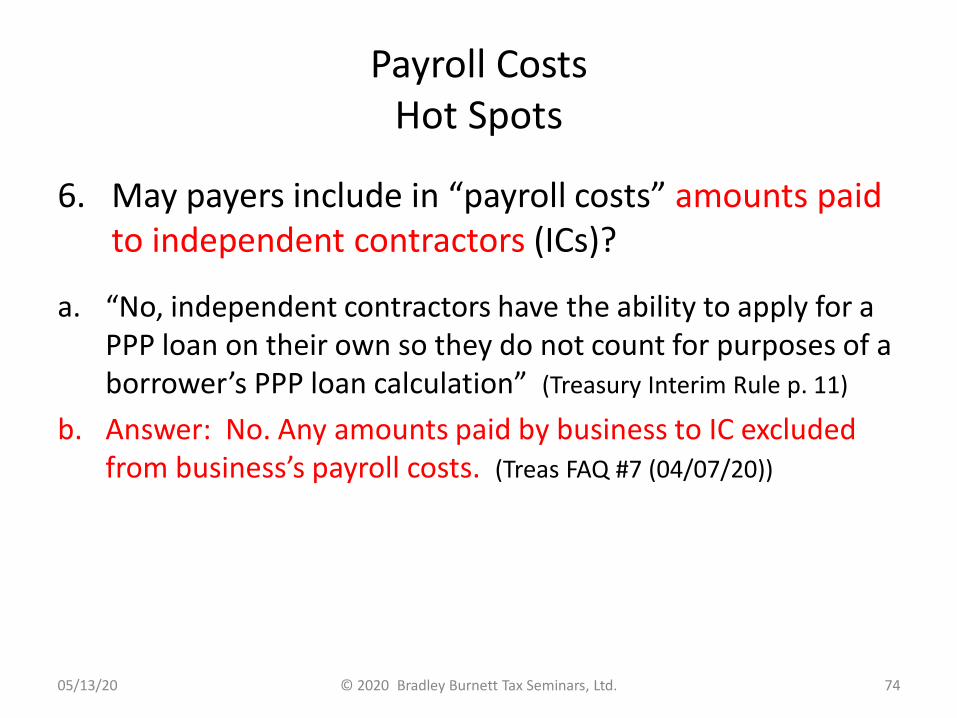

6. May payers include in “payroll costs” amounts paid to independent contractors (ICs)?

a. “No, independent contractors have the ability to apply for a PPP loan on their own so they do not count for purposes of a borrower’s PPP loan calculation” (Treasury Interim Rule p. 11)

b. Answer: No. Any amounts paid by business to IC excluded from business’s payroll costs. (Treas FAQ #7 (04/07/20))

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 74

Payroll CostsHot Spots

7. Eligibility for PPP loan for sole proprietor

a. Must be in business on 02/15/20

b. SE income

c. Principal place of residence in U.S.

d. Filed 2019 Form 1040 Schedule C

- If no 2019 Sch. C, special rules soon (not available yet)*

- If did not (or not entitled to) claim expense on 2019 Sch. C, not permissible use during 8 weeks after receipt of loan proceeds (Treas. Temp. Changes (04/14/20) (p. 9), but also see p. 5)

* Law of the street – Some will apply even if no 2019 Schedule C – Some banks will go along with it

05/01/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 75

Payroll CostsHot Spots

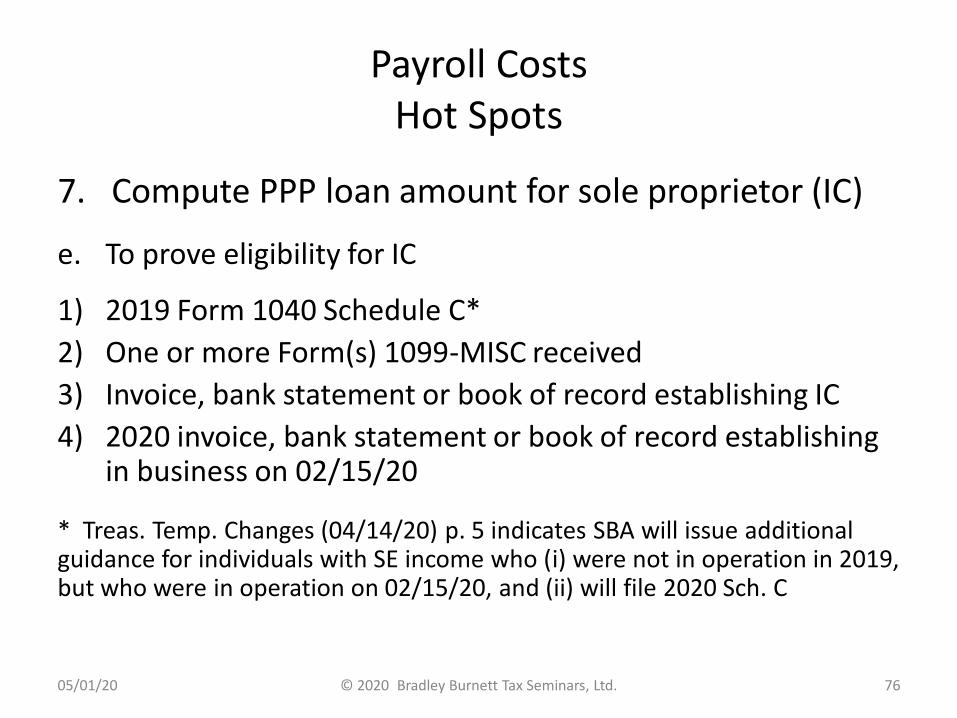

7. Compute PPP loan amount for sole proprietor (IC)

e. To prove eligibility for IC

1) 2019 Form 1040 Schedule C*

2) One or more Form(s) 1099-MISC received

3) Invoice, bank statement or book of record establishing IC

4) 2020 invoice, bank statement or book of record establishing in business on 02/15/20

* Treas. Temp. Changes (04/14/20) p. 5 indicates SBA will issue additional guidance for individuals with SE income who (i) were not in operation in 2019, but who were in operation on 02/15/20, and (ii) will file 2020 Sch. C

05/01/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 76

Payroll CostsHot Spots

8. Compute PPP loan amount for sole proprietor (IC)

a. Two types of computations (Treas. Temp. Changes (04/14/20) (p. 6))

1) IC w/ no employees

2) IC w/ employees

b. For IC alone

1) To compute, divide 2019 Schedule C line 31 net profit (or $100,000 if less) by 12, multiply by 2.5

2) Add EIDL loan (01/31/20 – 04/03/20) refinanced

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 77

Polling Question 5

• How does an independent contractor compute how much to borrow under PPP?

A. 2019 Schedule C Line 31 Net Profit

B. Projected 2020 income

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 78

PPP SourcePayroll Cost Independent Contractor

Allowed (or Not) Item Use Forgive

If 2019 Schedule C (filed or not)

2019 Schedule C line 31 net profit (or $100,000 if less) divided by 12, multiplied by 2.5

Big 5 Need guidance

Does not appear to add health insurance premium or retirement plan contribution on top of line 31 total

If no 2019 Schedule C

Either: 1. Wait for later guidance (bad idea), -or- - -

2. Make reasonable projection * Big 5 Need guidance

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 79

* Plus, add in payroll costs for IC’s employees

Payroll CostsHot Spots

8. Compute PPP loan amount for sole proprietor (IC)

c. To prove employee expenses (Treas. Temp. (04/14/20) (p. 8))

1) 2019 Form 1040 Schedule C reflecting payroll costs

2) 2019 Forms 941 reflecting Medicare wages and tips (Box 5c)

3) Fringe benefits – Copy of plan, cancelled checks

4) Tip records

5) State taxes – Payroll records

6) Health insurance – Transfers, cancelled checks, pay stubs, plan docs

7) Retirement plan employer expenses – Plan docs, proof of deposit

8) SUTA records – SUTA reports filed, proof of payment

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 80

Covered ExpensesHot Spots

9. Are self rentals included in covered expenses or not?

a. Rentals allowed in covered expenses by statute and Treasury

b. Self rentals not prohibited either place

c. These are compelling arguments for inclusion as covered expenses

d. These bother me:1) Newly (after 02/15/20) executed self leases

2) High (above commercially reasonable) self rents

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 81

Polling Question 6

• Is paying a self rental with PPP loan proceeds strictly prohibited?

A. Yes

B. No

C. Bail to get out of jail is expensive

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 82

Paycheck Protection ProgramLoan Particulars

1. Loan nonrecourse

- Becomes recourse if proceeds used for unallowed purpose

2. No personal guarantee or collateral required

3. No requirement that loan not available elsewhere

4. MAKE SURE APPLICATION OF LOAN PROCEEDS ARE A VERY CLEAR MATCH TO PERMITTED USE

5. Good faith certification required

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 83

Paycheck Protection ProgramUnauthorized Use of Loan Proceeds

• What happens if PPP loan funds misused? (Treasury Interim Rule, p. 17)

1. If use PPP funds for unauthorized purposes, SBA will direct perpetrator to repay those amounts

2. If knowingly use the funds for unauthorized purposes, will be subject to additional liability such as charges for fraud

3. If shareholder, member or partners uses PPP funds for unauthorized purposes, SBA will have recourse against shareholder, member or partner

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 84

Paycheck Protection ProgramCertification / Consequences of Foul Behavior

• “I certify that the information provided in this application and the information provided in all supporting documents and forms is true and accurate in all material respects”

“Knowingly making a false statement to obtain a guaranteed loan from SBA is punishable under the law, including:

1. Under 18 USC §§1001 and 3571 by imprisonment of not more than 5 years and/or a fine of up to $250,000;

2. Under 15 USC §645 by imprisonment of not more than two years and/or a fine of not more than $5,000; and

3. If submitted to a federally insured institution, under 18 USC §1014 by imprisonment of not more than thirty years and/or a fine of not more than $1,000,000

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 85

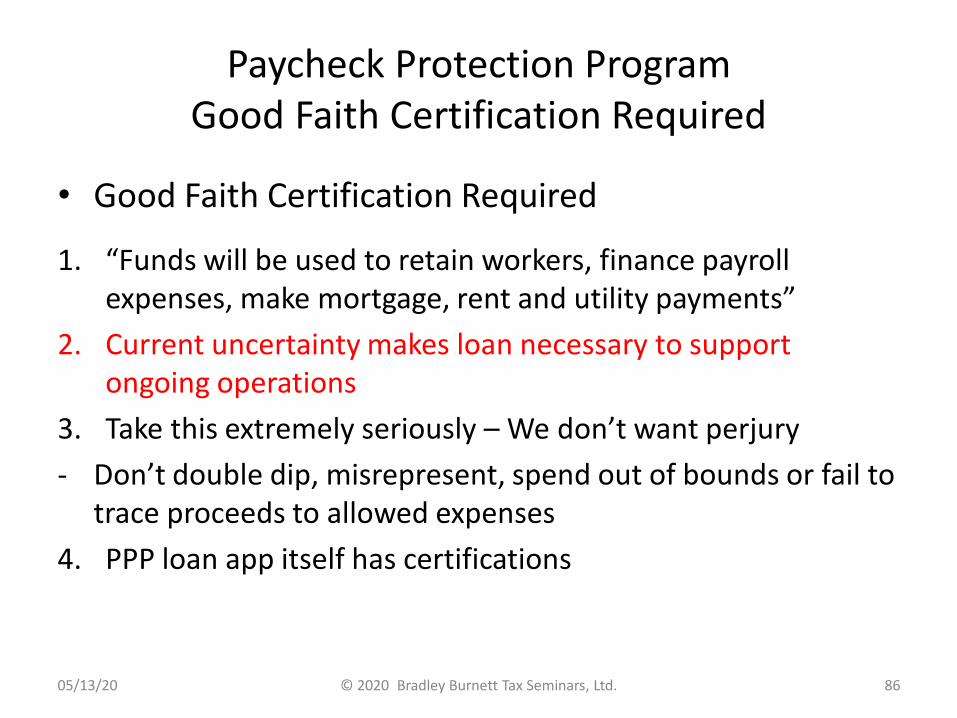

Paycheck Protection ProgramGood Faith Certification Required

• Good Faith Certification Required

1. “Funds will be used to retain workers, finance payroll expenses, make mortgage, rent and utility payments”

2. Current uncertainty makes loan necessary to support ongoing operations

3. Take this extremely seriously – We don’t want perjury

- Don’t double dip, misrepresent, spend out of bounds or fail to trace proceeds to allowed expenses

4. PPP loan app itself has certifications

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 86

Paycheck Protection ProgramGood Faith Certification Required

• FAQ #31 (04/23/20) Do businesses owned by large companies w/ adequate sources of liquidity to support ongoing operations qualify for a PPP loan? (Same for “private” companies w/ adequate sources of liquidity) (FAQ #37 (05/13/20))

1. “All borrowers must assess their economic need for a PPP loan.

2. “Review carefully the required certification that “[c]urrent economic uncertainty makes this loan request necessary to support the ongoing operations of the Applicant.

3. “Make this certification in good faith, taking into account current business activity and ability to access other sources of liquidity sufficient to support ongoing operations in a manner that is not significantly detrimental to the business.

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 87

Paycheck Protection ProgramGood Faith Certification Required

• FAQ #31 (04/23/20) Do businesses owned by large companies w/ adequate sources of liquidity to support ongoing operations qualify for a PPP loan?

4. “For example, it is unlikely that a public company with substantial market value and access to capital markets will be able to make the required certification in good faith.

5. “Any borrower that applied for a PPP loan prior to the issuance of this guidance and repays the loan in full by May 7, 2020 will be deemed by SBA to have made the required certification in good faith.“

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 88

Paycheck Protection ProgramGood Faith Certification Required

• FAQ #46 (05/13/20) Question: How will SBA review borrowers’ required

good-faith certification concerning the necessity of their loan request?

• Answer: When submitting a PPP application, all borrowers must certify in good faith that “[c]urrent economic uncertainty makes this loan request necessary to support the ongoing operations of the Applicant”

• Any borrower that, together with affiliates, received PPP loans with original principal amount of less than $2 million will be deemed to have made required certification re: necessity of loan request in good faith

• This safe harbor is appropriate because borrowers with loans below this threshold are generally less likely to have had access to adequate sources of liquidity in the current economic environment than borrowers that obtained larger loans

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 89

Recourse vs. Nonrecourse

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 90

Paycheck Protection ProgramIncome Tax Effect of Nonrecourse Loan

1. PPP loan nonrecourse (but, recourse if proceeds used for unauthorized purpose(s))

2. If loan used for covered purpose, it remains nonrecourse

3. Any operating loss funded by loan may not be deductible right away

a. §465 at-risk, §752 basis or S Corp basis rules may not allow basis allocation or current write-off

b. Structure, if possible, for maximum immediate deduction

c. Subsequent income tax free debt forgiveness also potentially threaten deductibility of expenses funded by forgiven portion (§265, tax benefit rule, court cases) (Congress needs to clarify)

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 91

Paycheck Protection ProgramLoan Forgiveness

• Principal and interest forgiven in amount equal to covered costs paid (and incurred?) during 8 weeks from loan origination (covered forgiveness period):

1. Wages, etc., payroll costs

2. Mortgage interest for qualifying debt existing < 02/15/20

3. Rent, utilities

Tony Nitti article re: PPP loan forgiveness: https://www.forbes.com/sites/anthonynitti/2020/04/15/ten-things-we-need-to-know-about-paycheck-protection-program-loan-forgiveness/?utm_source=newsletter&utm_medium=email&utm_campaign=forbes-announcements#11185b1e3291

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 92

Paycheck Protection ProgramGeneral Terms

1. Interest rate – 1% (by statute, not to exceed 4%)

2. Payment deferment – 6 month deferment includes principal, interest and fees

3. Origination fees – Lender reimbursed by SBA

4. Forgiveness of all or portion of loan available

5. Remaining balance after forgiveness guaranteed by SBA

- Maturity 2 years from date loan forgiveness applied for

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 93

PPPSource vs. Use vs. Forgiveness

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 94

Source Use Forgive (but 75%)

Period 2.5 months 8 weeks 02/15/20 - 06/30/20

Salary (max $100,000) X X X

Employee benefits X X X

Interest (debt < 02/15/20) X X

Rent (in force < 02/15/20) X X

Utility (service began < 02/15/20) X X

Interest on other mortgages X

Non-mortgage interest X

Other rent X

Other utilities X

Other

The Whole Point of PPPGovernment Wants Wages To Be Paid

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 95

Paycheck Protection ProgramLoan Forgiveness

1. Borrower not responsible for any loan payment if borrower uses all of loan proceeds for forgiveable purposes and employee and compensation levels levels maintained (CARES §1106)

2. Actual forgiveness amount depends on total (paid or incurred?*) over the 8 week period following the date of the loan:

a. Payroll costs

b. Payments of interest on mortgage debt incurred before 02/15/20

c. Rent payments on leases in force before 02/15/20, and

d. Utility payments under service agreements dated before 02/15/20

* Up for grabs – Statute messy, Treasury owes us guidance

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 96

Paycheck Protection ProgramLoan Forgiveness

3. However, not more than 25% of loan forgiveness amount may be attributable to nonpayroll costs (Treasury Interim Rule, p.

11)

4. Example: PPP loan $100,000. All disbursed on covered expenses. Disbursed $80,000 on payroll and $20,000 on rent. All of loan is forgiven (100%).

5. Example: PPP loan $100,000. All disbursed on covered expenses. Disbursed $70,000 on payroll and $30,000 on rent. $70,000 of loan is forgiven (70%). Or, different approach? Treas future guidance

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 97

Paycheck Protection ProgramLoan Forgiveness

• Loan forgiveness amount reduced if salaries reduced

1. Forgiveness reduced by amount of reduction of salaries and wages of any employee in excess of 25% during covered period, compared to most recent full quarter

- Employees not fungible – Hiring new ‘ee no helps here

2. Excludes employees with annualized pay > $100,000

3. Exemption from loan forgiveness reduction for employees rehired [w/in 30 days] or [by 06/30/20] if tests met

- Rehire workers fast to get back into good graces of PPP forgiveness

- Treasury owes us future guidance

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 98

Paycheck Protection ProgramLoan Forgiveness

• Timing of loan forgiveness

1. No loan may be forgiven until > 8 weeks after PPP loan proceeds received

2. Application submitted to lender by borrower

- Will lenders have tons of subjective power?

3. Treasury will issue more guidance in future re: forgiveness (Treasury Interim Rule, p. 16)

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 99

Paycheck Protection ProgramLoan Forgiveness Taxability

• Loan Forgiveness Taxability (CARES Act §1106)

1. Any amount forgiven does not have to be paid back

2. Any amount forgiven is excluded from gross income

- This is incredible!!

3. Is related payroll expense deductible? Need Congressional

guidance

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 100

SBA PPP Loan Application

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 101

SBA PPP Loan ApplicationCertifications

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 102

SBA WebpageClick, Click, Click

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 103

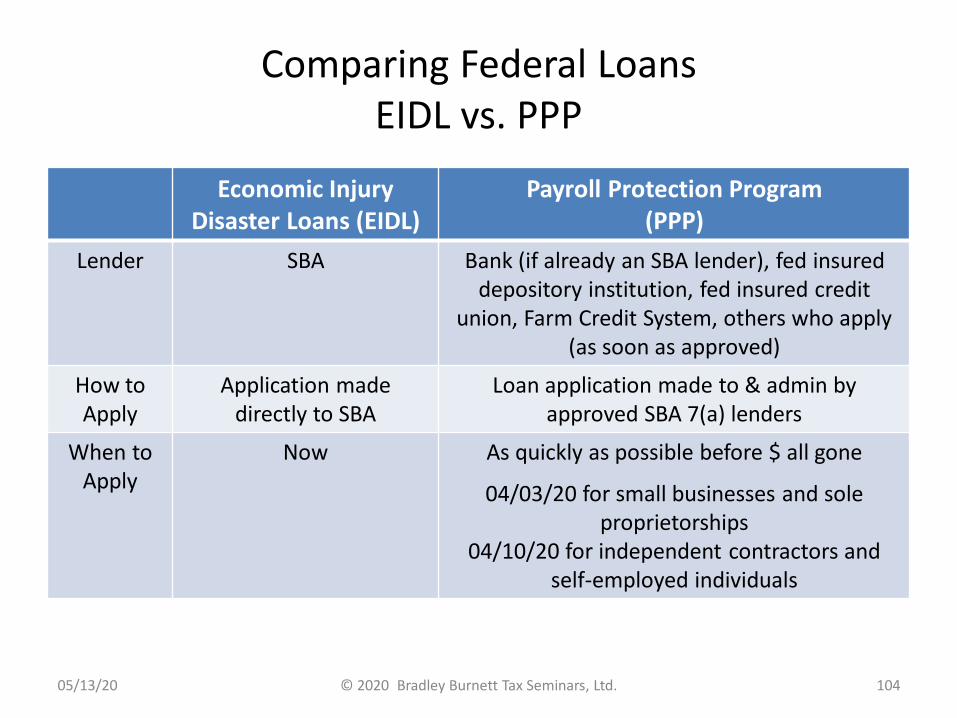

Comparing Federal LoansEIDL vs. PPP

Economic InjuryDisaster Loans (EIDL)

Payroll Protection Program(PPP)

Lender SBA Bank (if already an SBA lender), fed insured depository institution, fed insured credit

union, Farm Credit System, others who apply (as soon as approved)

How toApply

Application made directly to SBA

Loan application made to & admin by approved SBA 7(a) lenders

When to Apply

Now As quickly as possible before $ all gone

04/03/20 for small businesses and sole proprietorships

04/10/20 for independent contractors and self-employed individuals

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 104

Comparing Federal LoansEIDL vs. PPP

Economic Injury Disaster Loans (EIDL)

Payroll Protection Program(PPP)

WhoCan

Apply

Business w/ 500 or lessemployees, or tribal business w/

Business, 501(c)(3) non-profit, 501(c)(9) vet. org, tribal business w/ 500 or < ‘ees

Cooperative w/ not > 500 employees not > 500 ‘ees

Businesses and entitiesin operation on 02/15/20

Sole proprietor Self-employed individuals

Business, ag co-op, aquaculture, nursery, producer coop small

under SBA standards

Business operating in a certain industry meeting SBA employee-based size

standards for that industry

To meet financial obligations & operating exp. that would not h/

been incurred if no disasterCannot borrow for same

expenditures as PPP

Use loan for payroll, mortgage interest, rent or utilities

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 105

Comparing Federal LoansEIDL vs. PPP

Economic Injury Disaster Loans (EIDL) Payroll ProtectionProgram (PPP)

AffiliationRules

A business’ affiliations could precludethem from being “small” (i.e., eligible)

Same, except affiliation rules waived for hotels, restaurants, franchises

Affiliation exists where either:1. Business controls (or has power to

control) another; or2. 3rd party(ies) controls (or has power

to control) both businesses

https://www.sba.gov/sites/default/files/affiliation_ver_03.pdf

Cite 13 CFR 121.301(b)(2), (f) FAQs #5, 6 Same

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 106

https://www.sba.gov/document/policy-guidance--ppp-affiliation-interim-final-rule

Comparing Federal LoansEIDL vs. PPP

Economic Injury Disaster Loans (EIDL) Paycheck ProtectionProgram (PPP)

Maximum $2 million $10 million or, if less, 2.5 x average monthly payroll

over 12 months

Advance on Loan

May request advance up to $10,000 (only $1,000/FT employee). No requirement to pay

back. Distributed w/in 3 days.

-

Amount of advance based on number of pre-disaster (as of 01/31/20) employees. $1,000/employee up to $10,000 max.

-

PersonalGuarantee

Yes, for loans > $200,000, > 20% owners and managing owners. No liens against real estate

of guarantor.

No

Collateral SBA places UCC lien against assets None

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 107

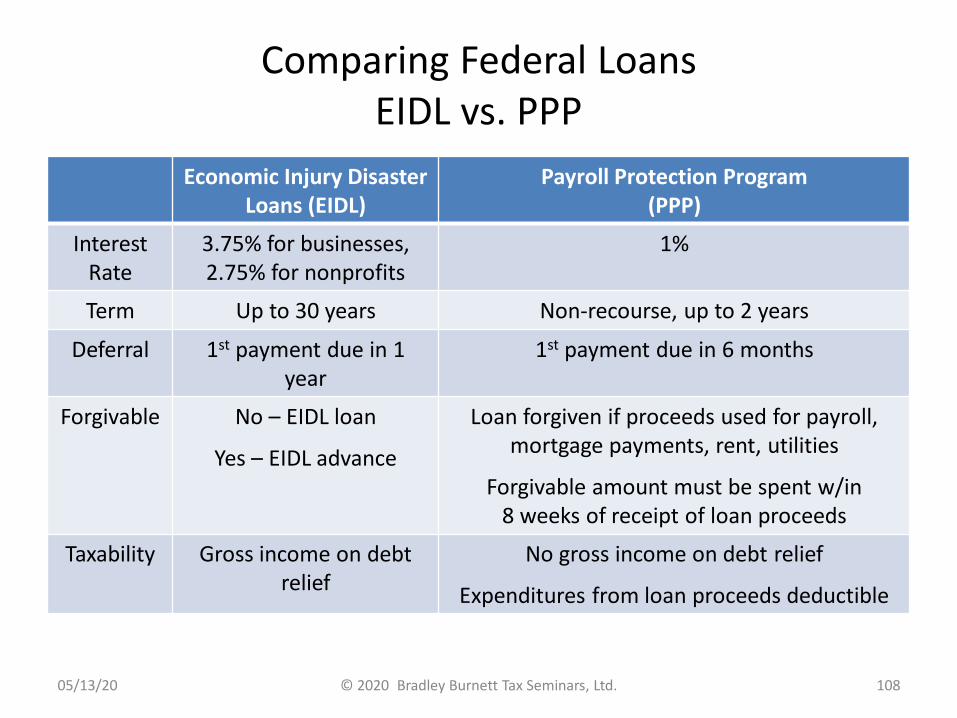

Comparing Federal LoansEIDL vs. PPP

Economic Injury Disaster Loans (EIDL)

Payroll Protection Program(PPP)

Interest Rate

3.75% for businesses,2.75% for nonprofits

1%

Term Up to 30 years Non-recourse, up to 2 years

Deferral 1st payment due in 1year

1st payment due in 6 months

Forgivable No – EIDL loan

Yes – EIDL advance

Loan forgiven if proceeds used for payroll, mortgage payments, rent, utilities

Forgivable amount must be spent w/in 8 weeks of receipt of loan proceeds

Taxability Gross income on debt relief

No gross income on debt relief

Expenditures from loan proceeds deductible

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 108

CARES Act Alternativesto PPP Loans

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 109

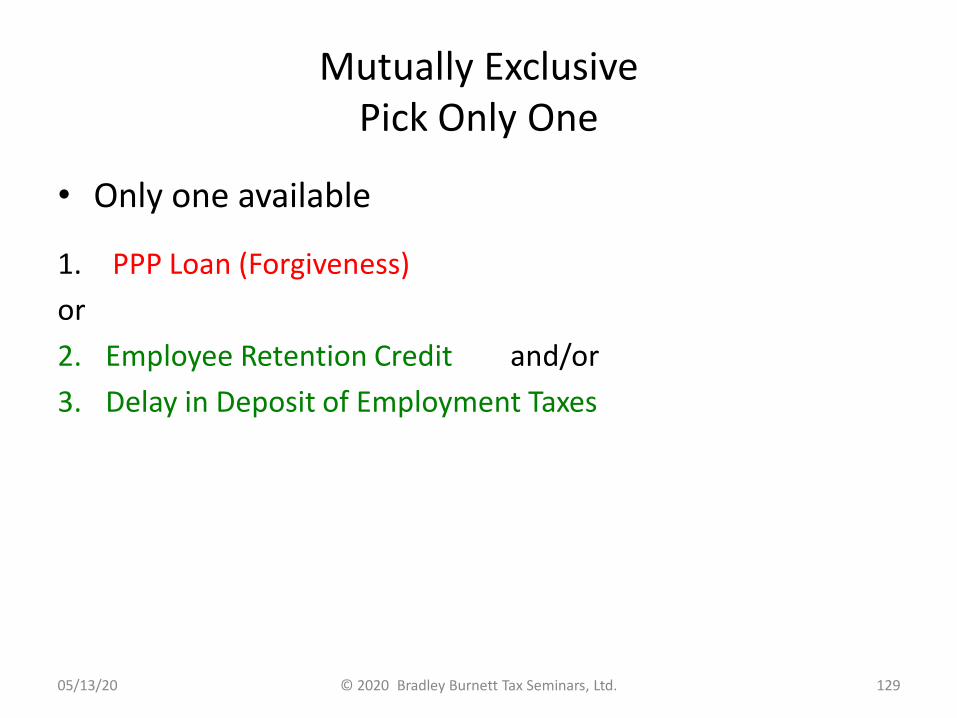

Mutually Exclusive Pick Only One

• Only one available

1. PPP Loan (Forgiveness)

or

2. Employee Retention Credit and/or

3. Delay in Deposit of Employment Taxes

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 110

Delay in Deposit of Employment Taxes

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 111

Delay in Deposit of Employment Taxes

• Delay in Deposit of Employment Taxes (CARES §2302)

1. May delay (or not) deposit of employer share of OASDI- Employer share of Medicare (HI) tax not eligible

2. Eligible for deferral = Tax incurred 03/27/20 thru 12/31/20

3. “Interest and penalty free loan” if paid back on timea. Half required to be deposited by end of 2021

b. Other half required by end of 2022

4. Self-employed individual may delay one half of SE tax

- OASDI (social security) portion (but not Medicare (HI) portion)

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 112

Delay in Deposit of Employment Taxes

• Delay in Deposit of Employment Taxes (CARES §2302)

5. Delay in deposit of employer OASDI not available to any tp that’s had PPP debt forgiven (CARES §1106)

a. PPP loan may derail deferral of ‘er OASDI (CARES §2302(a)(3))

b. Entitlement to forgiveness of PPP loan depends on spending loan proceeds on “covered expenses”

c. IRS FAQ #4 (04/16/20)

1) May defer employer OASDI through date lender issues decision to forgive PPP

2) No deferral for newly arising employer OASDI after that date

3) However, prior amounts deferred through date PPP loan forgiven continue to be deferred until (half) 12/31/21 and (half) 12/31/22

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 113

Employment Tax Crackdown

• IRS touts “Though We Be But Little, We Are Fierce”

1. 1,992 Revenue Officers (RO) - Field visits up 40% over last 3 years

2. IRS visits in-person 7,000 employers a year re: delinquent employment taxes (per IRS webinar (08/01/19))

- 1.3 million cases in the queue

3. Employment tax referrals largest source of referrals to Criminal Investigation (CID)

a. 80% of those referrals accepted by CID

b. 90% of referrals accepted result in conviction

c. Average prison term 2 to 2 ½ years

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 114

Jail Isn’t So Comfortable

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 115

Polling Question 7

• Falling behind paying trust fund employment taxes to the government is comfortable and fun

A. Being in jail is a great time in life

B. Not true

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 116

Employee Retention Credit

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 117

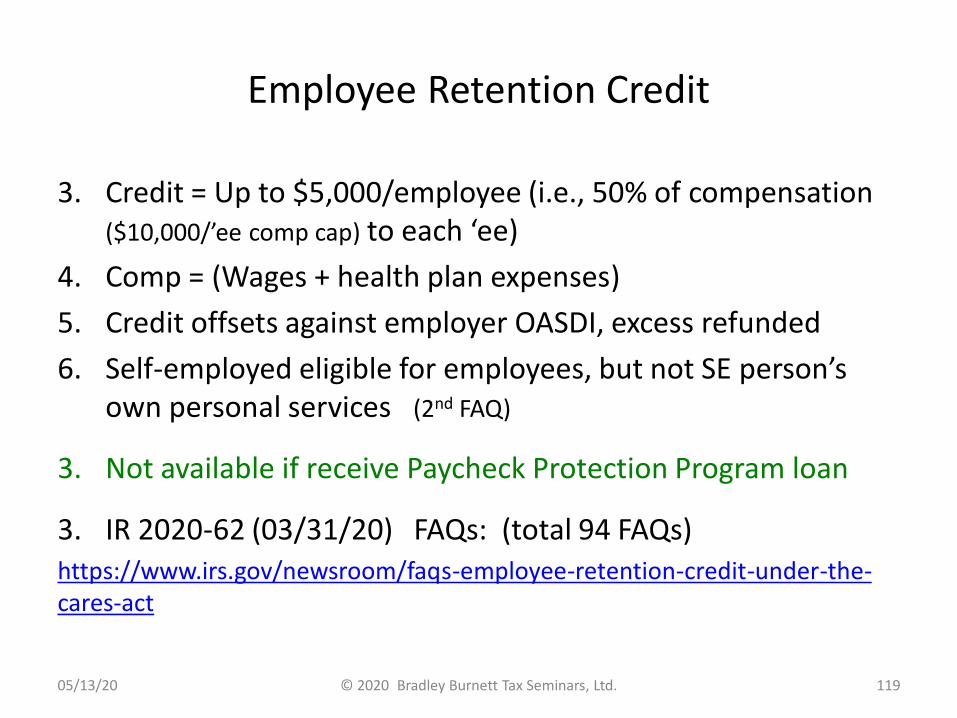

Employee Retention Credit

• Employee retention credit for employers subject to closure due to Covid who continue to pay employees wages during closure (CARES §2301)

1. Businesses and tax exempts qualify, but not government

2. To be eligible, must carry on business in 2020, and either:

a. Ordered by a government to shut down (or reduce operations) due to Covid-19; or

b. Suffered significant decline in business during a calendar quarter in 2020

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 118

Employee Retention Credit

3. Credit = Up to $5,000/employee (i.e., 50% of compensation ($10,000/’ee comp cap) to each ‘ee)

4. Comp = (Wages + health plan expenses)

5. Credit offsets against employer OASDI, excess refunded

6. Self-employed eligible for employees, but not SE person’s own personal services (2nd FAQ)

3. Not available if receive Paycheck Protection Program loan

3. IR 2020-62 (03/31/20) FAQs: (total 94 FAQs)https://www.irs.gov/newsroom/faqs-employee-retention-credit-under-the-cares-act

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 119

Employee Retention Credit (ERC)

9. Amount of ERC claimed reduces income tax deduction of related wage expense (FAQ #85)

10. Employer may elect not to apply ERC for any calendar quarter by not claiming the credit on Form 941 (FAQ #93)

11. If employer elected not to claim ERC in one calendar quarter, employer not prohibited from claiming ERC in a subsequent calendar quarter if eligible (FAQ #94)

12. Employer can file claim for refund (Form 941-X) to claim ERC for prior quarter (interest-free adjustment )

https://www.irs.gov/newsroom/covid-19-related-employee-retention-credits-special-issues-for-employers-faqs

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 120

Employee Retention Credit

13. Qualified wages

a. Employers w/ > 100 full-time employees (30 hrs or > a week)

1) Wages qualifying for ERC = Employees not currently providing services due to Covid-19

2) Example: Employees at mega gym (credit only for wages paid to employees not working)

b. Employers w/ 100 or < full-time employees

1) All employees receiving wages, whether currently providing services to employer or not

2) Example: Small town YMCA (credit for all wages paid whether each employee continues to work or not)

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 121

Employee Retention Credit

14. Qualified health plan expenses

a. Include amounts paid or incurred by employer to provide and maintain a group health plan, but only to extent excluded from employee’s gross income under §106

b. Self-employed health insurance of S Corp shareholder, partner or sole proprietor (including single member LLC owned by individual) don’t qualify

c. How to allocate expenses among employees?

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 122

Employee Retention Credit

15. Significant decline in gross receipts

a. Begins w/ 1st quarter in which gross receipts for a calendar quarter in 2020 are < 50% of gross receipts for same cal. quarter in 2019

b. The significant decline in gross receipts ends with 1st calendar quarter that follows 1st calendar quarter for which 2020 gross receipts for quarter > 80% of gross receipts for same calendar quarter in 2019

c. In other words, if receipts drop by > 50%, employer continues to qualify for credit until quarter after receipts drop by < 20%

d. Example: 1Q 2020, receipts 48% of 1Q 2019. 2Q receipts 83% of 2Q 2019. Eligible for credit for 1Q and 2Q (not 3Q) 2020

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 123

Newly Minted IRS Form 941 2Q 2020

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 124

Newly Minted IRS Form 7200

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 125

Small Business, Big BusinessWho Gets What?

CARES Act Liquidity / Tax Relief

Small Business(up to 500 employees)

Large Business(> 500 employees)

EIDL Loans Yes No

Paycheck Protection Program Loans

Yes No

Other Loans Yes Yes

Employee Retention Credit Yes Yes

Deferral of Employer FICA Yes Yes

Paid Sick & FMLA Leave Yes Yes (other programs)

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 126

Comparing AlternativesFor Better or For Worse?

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 127

Comparing AlternativesFor Better or For Worse?

Better Worse

PPP Loan Partially operational nowOperations will fire back

up before 06/30/20Able to spend on payroll

Operations won’t fire back up by 06/30/20

Proceeds will be spent on other screaming needs (e.g. supplies)

Employee Retention Credit

Low paid employees, lots of employee turnover

Income tax loss perhaps more useable (no at-risk

or basis limits)

Higher paid workers, not much turnover (hit $10,000

wage/employee and $5,000 credit cap/employee fast)

Defer Employer FICA

NeverBut, maybe, if desperate,client far above average

You have better choicesYour mother raised you better

than to do this

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 128

Mutually Exclusive Pick Only One

• Only one available

1. PPP Loan (Forgiveness)

or

2. Employee Retention Credit and/or

3. Delay in Deposit of Employment Taxes

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 129

Losses

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 130

TCJANet Operating Losses

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 131

NOL Tweaks by TCJAPercentage of Absorption

• Net Operating Loss (NOL) Percentage of Application (Regular Tax)

1. Prior law – NOLs generated before 2018 offset 100% of taxable income (TI) in year carried to

2. TCJA – NOLs generated in years beginning after 2017 may only offset 80% of TI of year NOL carried to

© 2020 Bradley Burnett Tax Seminars, Ltd. 13205/13/20

NOL Tweaks by TCJACarryback or Carryforward

• Carrybacks and carryforwards

1. Prior law – NOLs carry back 2 years, forward 20

- However, §172(b)(1) allowed for 3 year loss carryback periods for casualty, theft and farmers

2. TCJA – For NOLs generated in years beginning > 2017

a. No more NOL carrybacks (except 2 years for farmers)

b. NOLs indefinitely carry forward

© 2020 Bradley Burnett Tax Seminars, Ltd. 13305/13/20

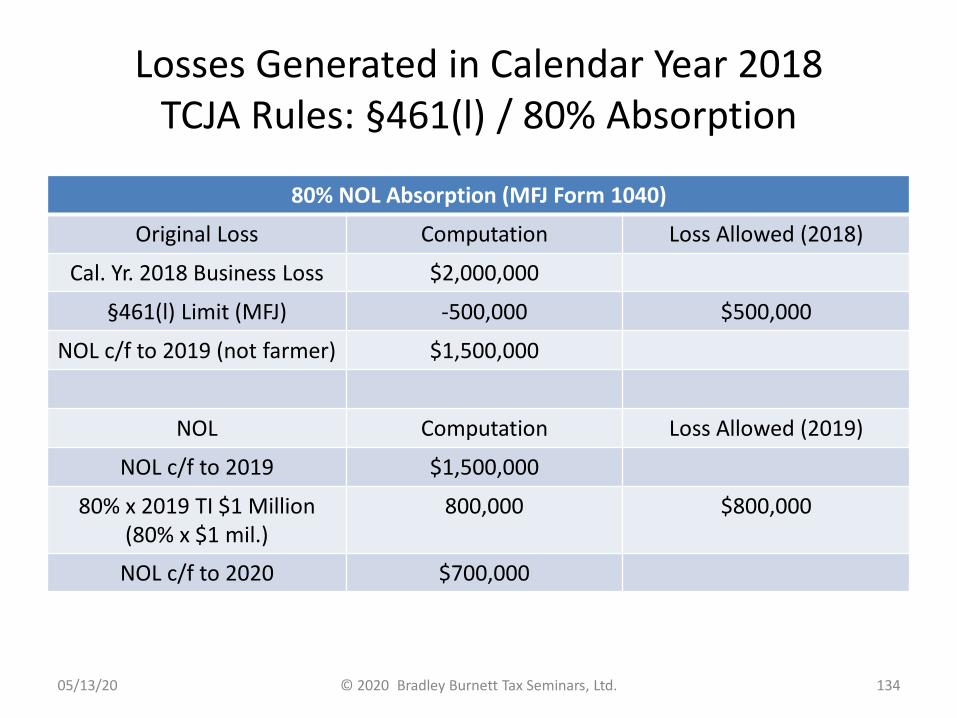

Losses Generated in Calendar Year 2018TCJA Rules: §461(l) / 80% Absorption

80% NOL Absorption (MFJ Form 1040)

Original Loss Computation Loss Allowed (2018)

Cal. Yr. 2018 Business Loss $2,000,000

§461(l) Limit (MFJ) -500,000 $500,000

NOL c/f to 2019 (not farmer) $1,500,000

NOL Computation Loss Allowed (2019)

NOL c/f to 2019 $1,500,000

80% x 2019 TI $1 Million (80% x $1 mil.)

800,000 $800,000

NOL c/f to 2020 $700,000

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 134

CARES (CARES §2303)

NOL Tweaks and More Tweaks

1. Repeals 80% limit for years beginning < 01/01/21

a. Helps C Corps that generated NOLs in 2018 or 2019 or will generate NOL in 2020

b. May help or hurt non-C Corp depending on rate brackets

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 135

CARES (CARES §2303)

NOL Tweaks and More Tweaks

2. For NOLs arising in years > 12/31/17 and < 01/01/21, NOLs allowed as carrybacks to each of 5 years prior

a. Helps C Corps that generated NOLs in 2018 or 2019 (or 2020) get refunds at up to 35% rate if amended returns filed

- C Corp AMT existed prior to 2018

b. May help or hurt non-C Corp depending on rate brackets

c. May waive NOL carryback (deadline 1 year after 03/27/20))

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 136

Net Operating LossesTimeline

Pre-TCJA TCJA CARES Act

Time Frame Pre- 2018 Tax Years Beginning After 2017*

Retroactive to After 2017

Regular Tax Absorption Rate

100% of TI in year carried to

80% of TI in year carried to

100% of TI in year carried to

Carrybacks Back 2 (or 3), unless elect not to

Back 2 (farmers),unless elect not to

For 2018, 2019 & 2020, back 5, unless

elect not to (elect w/in 1 yr after 03/27/20)

Carryforwards 20 years Forever Forever

AMT Absorption Rate

90% of AMTI in year carried to

90% of AMTI in year carried to

90% of AMTI in year carried to

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 137

* As corrected by CARES Act

Net Operating LossesCARES Act NOL Shuffle

• IR 2020-67 (04/09/20) – IRS guidance re: NOLs under CARES Act

1. Rev. Proc. 2020-24 (04/09/20) – Procedures for NOLs carried back (for 5 years) under CARES

a. For 2018, 2019 and 2020 – Waive a carryback period for NOL arising in year beginning > 12/31/17 and < 01/01/21

b. For TCJA transition fiscal year – Waive a carryback period, reduce a carryback period or revoke an election to waive a carryback period for yr begin < 01/01/18 and end > 12/31/17

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 138

Net Operating LossesHow to Waive NOL Carryback

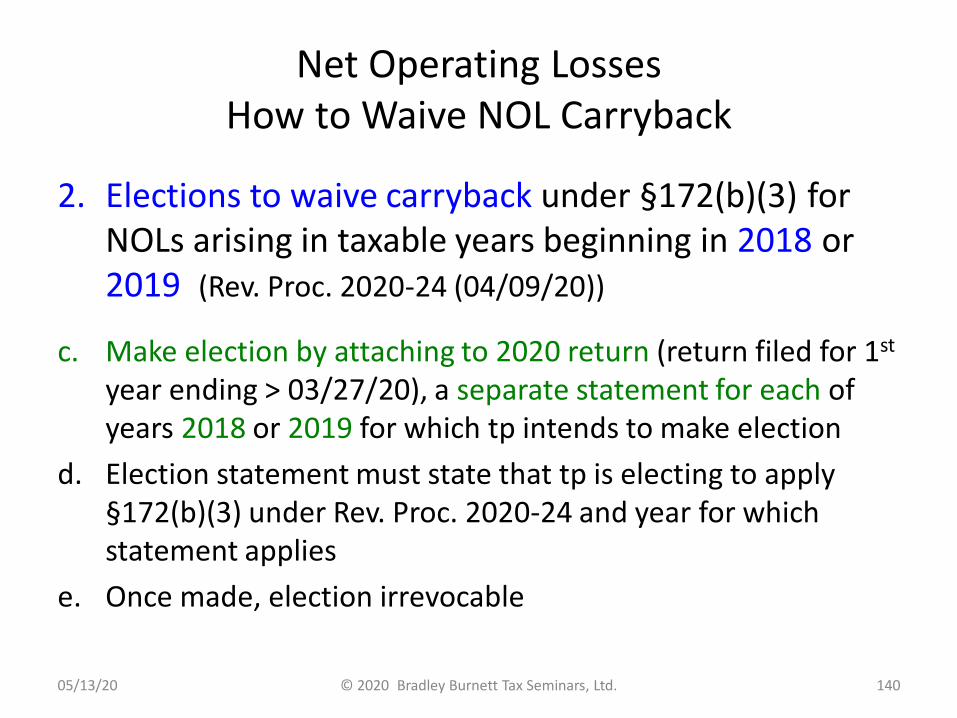

2. Elections to waive carryback under §172(b)(3) for NOLs arising in taxable years beginning in 2018 or 2019 (Rev. Proc. 2020-24 (04/09/20))

a. May elect under §172(b)(3) to waive carryback period for an NOL arising in year beginning in 2018 or 2019

b. Time window to make election – Election must be made no later than due date, including extensions, for filing income tax return for 1st year ending > 03/27/20

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 139

Net Operating LossesHow to Waive NOL Carryback

2. Elections to waive carryback under §172(b)(3) for NOLs arising in taxable years beginning in 2018 or 2019 (Rev. Proc. 2020-24 (04/09/20))

c. Make election by attaching to 2020 return (return filed for 1st

year ending > 03/27/20), a separate statement for each of years 2018 or 2019 for which tp intends to make election

d. Election statement must state that tp is electing to apply §172(b)(3) under Rev. Proc. 2020-24 and year for which statement applies

e. Once made, election irrevocable

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 140

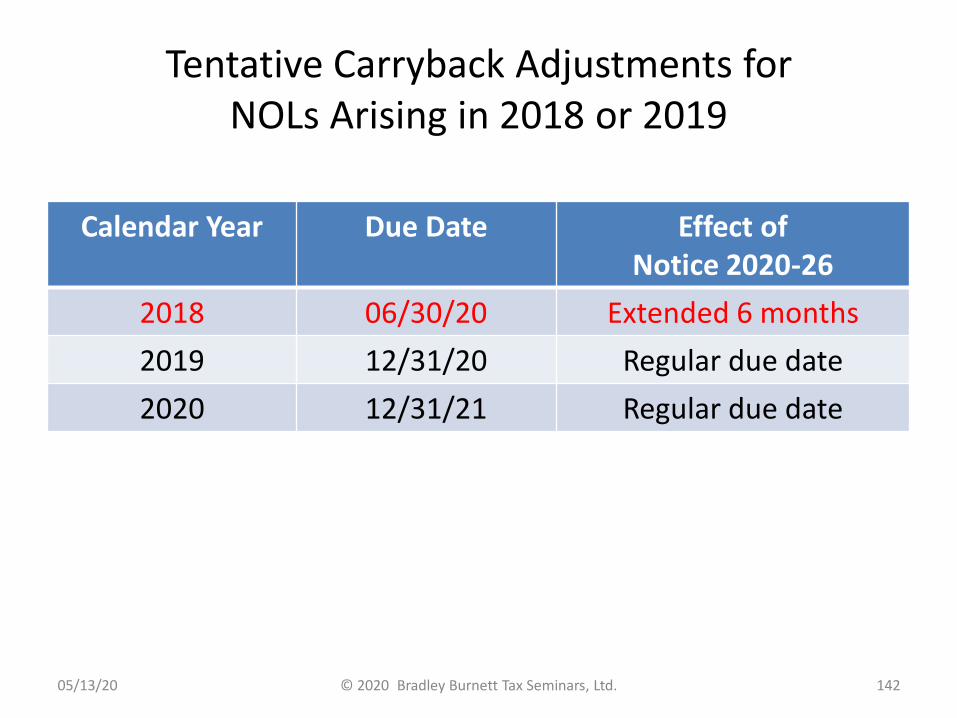

Tentative Carryback Adjustments for NOLs Arising in 2018 or 2019

3. Notice 2020-26 – Six month extension to file forms for tentative carryback adjustments (§6411) re: NOLS arising in 2018*

a. Form 1045 (individuals, trusts and estates)

b. Form 1139 (corporations)

c. To file tentative refund based on 2018 NOL carryback

1) File form no later than 18 months after close of year in which NOL arose (no later than 06/30/20, for tax year ending 12/31/18)

2) Include at top of applicable form “Notice 2020-26, Extension of Time to File Application for Tentative Carryback Adjustment”

* NOL that arose in year beginning in 2018 and ended on or > 06/30/19

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 141

Tentative Carryback Adjustments for NOLs Arising in 2018 or 2019

Calendar Year Due Date Effect of Notice 2020-26

2018 06/30/20 Extended 6 months

2019 12/31/20 Regular due date

2020 12/31/21 Regular due date

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 142

Polling Question 8

• Filing NOL carryback claims under the CARES Act is a bit time sensitive

A. True

B. Not true in any respect

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 143

Tentative Carryback Adjustments for NOLs Arising in 2018 or 2019

3. Notice 2020-26 – Six month extension to file forms for tentative carryback adjustments re: NOLS arising in 2018 (Forms 1045 and 1139)

d. IRS FAQs (updated 04/17/20): From 04/17/20 until future notice, how to submit 1045s and 1139s? Fax them

1) Fax Form 1139 to 844-249-6236

2) Fax Form 1045 to 844-249-6237

e. If prior mailed, fax anyway for faster service – Mailed forms won’t be processed until IRS processing centers reopen

https://www.irs.gov/newsroom/temporary-procedures-to-fax-certain-forms-1139-and-1045-due-to-covid-19

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 144

That’s All Folks

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 145

Appendix

1. Loss limitation – Hurdles

2. §163(j) Business Interest Expense Limit

3. §461(l) – Excess Business Losses

4. §168(k) – Qualified Improvement Property (QIP)

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 146

Loss Limitation - Hurdles

© 2020 Bradley Burnett Tax Seminars, Ltd. 14705/13/20

Loss Limitation Hurdles

• Loss limitation (TCJA) (2018 and >): 6 hurdles

1. Basis (§§705 and 1367)

2. §163(j) (newly expanded)

3. At-risk (§465)

4. Passive loss (§469)

5. Excess loss (new §461(l))

6. NOL (§172) (major changes by TCJA)

148© 2020 Bradley Burnett Tax Seminars, Ltd.05/13/20

TCJA §163(j) Business Interest Expense Limit

© 2020 Bradley Burnett Tax Seminars, Ltd. 14905/13/20

§163(j) TCJA Rule

• §163(j)(1) – For years beginning > 12/31/17, deduction for business interest expense (BIE) cannot exceed sum of:

1. “Business interest income” (BII);

2. 30% of “adjusted taxable income” (ATI*); and

3. Floor financing interest expense (vehicle dealers) (§163(j)(9))

• However, exempt small business or excepted business not subject to limit

* ATI cannot be < zero

© 2020 Bradley Burnett Tax Seminars, Ltd. 15005/13/20

§163(j) ATI LimitTCJA (2018) Example

• Not exempt or excepted business or vehicle dealer

- Business interest expense $4 million

- Taxable income (before BIE) $8 million. Depreciation $2 million (added back through 2021).

§163(j) Business Interest Expense Limit

Interest Expense $4 mil.

Allowed (Limit) ($8 + 2 = $10mil. (ATI) x 30%)

- 3 mil.

EBIE* Carryforward $1 mil.

© 2020 Bradley Burnett Tax Seminars, Ltd. 151

* EBIE = Excess (disallowed) business interest expense

05/13/20

§163(j) – Partnerships and Partners

© 2020 Bradley Burnett Tax Seminars, Ltd. 15205/13/20

§163(j) ATI Limit – TCJA ExamplePartnership – Year 1

§163(j) Business Interest Expense Limit

Interest Expense $4 mil.

Allowed (Limit) ($8 + 2 = $10mil.(ATI) x 30%)

- 3 mil.

EBIE Carryforward $1 mil.

© 2020 Bradley Burnett Tax Seminars, Ltd. 153

1. Partnership income (loss), net of $3 million allowed BIE, passes through K-1 to partners. Not subject to further §163(j) limit at partner level.

2. $1 mil. EBIE split 50/50 ($500,000 each) between two equal partners. Each partner’s basis reduced by $500,000. EBIE stacks (siloes) at partner level.

3. Siloed EBIE carryforward for each offset later only by future ETI and/or EBII from same partnership.

05/13/20

Silos of EBIEPartnership by Partnership

© 2020 Bradley Burnett Tax Seminars, Ltd. 15405/13/20

§163(j) ATI Limit – TCJA ExamplePartnership – Year 2

§163(j) Business Interest Expense Limit

BIE (includes EBIE) Yr 2 $4 mil. + EBIE $0 mil. $4 mil.

Limit ($18 + 2 deprec. = $20mil. (ATI) x 30%)

$6 mil.

ETI $6 mil. Cap - $4 mil. BEI $2 mil.

EBIE Carryforward No EBIE at pshp level $0

© 2020 Bradley Burnett Tax Seminars, Ltd. 155

1. Partnership income (loss), net of $4 million allowed BIE, passes through K-1 to partners. Not subject to further §163(j) limit at partner level.

2. The $4 mil. BIE passed through as non-separately stated income (loss) reduces basis in partnership interest. Not further §163(j) limited at partner level.

3. $2 mil. ETI passes to partners. 50/50 $1 mil. each. Soaks up siloed $500,000 (from year 1) for each partner from same partnership.

05/13/20

CARES ActTweaks to §163(j)

1. For years beginning in 2019 and 2020, CARES increased 30% of ATI limit to 50% (CARES §2306)

- Can elect out of 50% rule

2. Special rule for partnerships – 50% of 2019 excess business interest expense allocated by partnership to partner deductible by partner in 2020 not subject to §163(j) limit

- Partnerships and partners can elect for this rule not to apply

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 156

CARESTweaks to §163(j)

2018 2019 2020

BIE DeductionLimit

30% x ATI 50% x ATI, unless elect out to 30%

50% ATI, unless elect out to 30%

Partnerships Partnership level EBIE siloed until future ETI from

same partnership

Partnership level EBIE siloed until future ETI from

same partnership

Partnership level EBIE siloed until future ETI from

same partnership

However, 50% of siloed BIE from 2019 allowed,

unless elect out

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 157

Excess Business Losses§461(l)

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 158

Non-C Corp Excess Business LossesTCJA Rule: §461(l)

• For tax years beginning after 12/31/17 and before 01/01/26,

excess business losses of a taxpayer (non-C Corp) not allowed for tax year

1. Excess business loss (EBL) = Excess of aggregate deductions attributable to trades or businesses, over sum of aggregate gross business income or gain, plus a threshold amount

2. Threshold amount $250,000* non-MFJ, $500,000* MFJ

3. Disallowed amount = Excess business loss (EBL)

4. EBL becomes NOL carryover under §172

* $255,000 (2019), $510,000 (2019), $259,000 (2020), $518,000 (2020)

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 159

IRS Form 461

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 160

§461(l) Computation Basics

$500,000 Loss Allowed (MFJ Form 1040)

Original Loss Computation Loss Allowed (2018)

2018 Business* Loss $2,000,000

§461(l) Limit (MFJ) -500,000 $500,000

Excess business loss (EBL) becomes NOL c/f to 2019 (not farmer) (farmers get 2 yr carryback)

$1,500,000

* Material participation – Not subject to §469 passive loss rules

2018 nonbusiness income exceeding $500,000 will (may) be subject to tax

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 161

CARES ActDeferral of EBL Effective Date

• CARES postpones effective date of §461(l) excess business loss (EBL) limitation from years beginning after 12/31/17 to years beginning after 12/31/20 (CARES §2304)

1. If 2018 or 2019 return filed reporting EBL, amended return (possibly generating a refund) available

2. CARES technical correction: In EBL computation, wages not business income

3. CARES technical correction: In EBL computation, capital gains only included to extent of lesser of net cap gain attributable to trade or business or capital gain net income

4. On Form 1065 Schedule K-1 Box 20 Code AH and Form 1120S Schedule K-1 Box 17 Code AC, all reporting §461(l) info, disclosures not needed for 2018, 2019 and 2020

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 162

Non-C Corp Excess Business LossesTimeline of §461(l)

Pre-TCJA TCJA CARES

Effective Date Prior to 2018 > 2017 and < 2026 After 2020

CARESReshuffle

N/A Deletes §461(l) for 2018, 2019 & 2020

Reinstates §461(l) for after 2020

CARES re: Wage Income

N/A Wages income = Business income ? *

Wages income not business income

CARES re: cap gain income generated

in a business

N/A Capital gain inside business = Business

income ?

Capital gain inside business = Business

income

1065 and 1120S K-1 disclosures re: §461(l)

N/A After postponement, not needed for 2018,

2019 & 2020

Back on table in 2021

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 163

* §461(l) silent , IRS Instructions “yes”, Blue Book “no”

§168(k)Qualified Improvement Property (QIP)

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 164

§168(k)Qualified Improvement Property (QIP)

• Qualified improvement property = Improvements (to interior of commercial building) placed in service after building placed in service (§168(e)(6), §1.168(b)-1(a)(5))

a. Not residential

b. Not exterior

c. Not expansion

d. Not structural

e. Not elevators and escalators

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 165

Qualified Improvement Property (QIP)TCJA Timeline

Qualified Improvement Property (QIP)

2015 2016-2017 2018 and Later

39 Year Property N/A Yes Yes

Bonus Eligible N/A Yes No (BotchedAttempt)

Elect Out if Don’t Want

N/A Yes N/A

15 Year Property N/A No No (BotchedAttempt)

§179 Eligible N/A No Yes

Elect In if Want N/A No Yes

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 166

Qualified Improvement Property (QIP)Timeline (CARES §2307)

Qualified Improvement Property (QIP)

2015 2016-2017 2018 and Later

39 Year Property N/A Yes Yes

Bonus Eligible N/A Yes No (BotchedAttempt) Yes

Elect Out if Don’t Want

N/A Yes N/A Yes

15 Year Property N/A No No (BotchedAttempt) Yes

§179 Eligible N/A No Yes

Elect In if Want N/A No Yes

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 167

QIP15 Year Property Prior to 2018

1 Prior, prior law: Prior to TCJA, 3 categories of 15 year prop:

a. Qualified leasehold improvement property (QLIP);

b. Qualified retail improvement property (CRIP); and

c. Qualified restaurant property (QRP)

2. In TCJA, Congress collapsed these 3 categories into QIP

a. Intended to be 15 year prop bonus eligible, but inadvertently became 39 year property (not bonus eligible)

b. All of this went into purgatory (no man’s land), until CARES

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 168

QIP Under CARES15 Year Bonus Eligible Retroactive to 2018

1. CARES (CARES §2307), retroactive to property placed in service (PPIS) > 12/31/17, renders QIP as:

a. 15 year property (20 year ADS); and

b. Bonus eligible under §168(k) (if all bonus requirements met)

2. CARES Technical Correction – Used QIP not eligible for bonus

a. 15 year recovery period and bonus only apply to improvements made by tp (must be new QIP)

b. Example: If tp buys building containing QIP (that was depreciable by seller), purchasing tp cannot bonus such QIP

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 169

QIP – Rev. Proc. 2020-25How to Go Retro (or Not)

Post-2017 QIPBefore CARES

Post-2017 QIPCARES

AmendedReturn

Current Year and Forward Form 3115

39 Year Property Yes No No

15 Year Property No Yes Yes

Bonus Eligible - Automatic No Yes Yes

Stay in Bonus, Bonus Elect Outor Revoke Elect Out

N/A Yes Yes

Retro via Amended Return N/A Yes* -

Current Year Forward via 3115 N/A - Yes**

§179 Eligible Yes Yes Yes

§179 Change Amended Return Yes Yes Yes

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 170

* May generate refund of prior year tax ** Does not generate refund of prior year taxFor both * and **, general deadline to file for change 10/15/21

QIP Under CARES20 Year ADS Depreciation Retroactive to 2018

1. CARES (CARES §2307), retroactive to property placed in service > 12/31/17, renders QIP as 15 yr prop (20 year ADS)

2. ADS depreciation may be elected or required

3. ADS required for:

a. Tax-exempt use property

b. Tax-exempt bond-financed property

c. Property used outside U.S.

d. Etc.

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 171

QIP Under CARES Act20 Year ADS Depreciation Retroactive to 2018

2. ADS required for:

a. Nonresidential real prop, residential real prop and QIP held by an electing real property trade or business (§163(j)(7)(B), Rev. Proc. 2019-8, IRB 2019-3, p. 347) www.irs.gov/irb/2019-03_IRB#RP-2019-08 )

b. Property w/ GDS recovery period 10 yrs or > held by electing farming business (§163(j)(7)(C), Rev. Proc. 2019-8, IRB 2019-3, p. 347 www.irs.gov/irb/2019-03_IRB#RP-2019-08 )

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 172

QIP Under CARES Act20 Year ADS Depreciation Retroactive to 2018

3. Rev. Proc. 2020-22 (04/10/20) allows tps who prior elected out of §163(j) to

a. Make a late election, or

b. Withdraw an election,

c. Under §163(j)(7)(B) or §163(j)(7)(C), as applicable,

d. On an either amended Federal income tax return, amended Form 1065 or administrative adjustment request (AAR) under §6227

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 173

QIPPlaced in Service by Partnership

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 174

QIP for Partnerships (Under CARES)15 Year Bonus Eligible Retroactive to 2018

1. Partnerships under new Centralized Partnership Audit (CPAR) regime (enacted by BBA 2015) (BBA partnerships*), must generally file AAR to take prior year adjustments into account

2. Adjustments relating back to 2018 would be generally taken into account in 2020 only at partnership, not partner, level

- Would affect 2020, not 2018, partners

* BBA partnerships are those that did not elect out of CPAR on Form 1065

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 175

QIP Procedure (Under CARES Act)?15 Year Bonus Eligible Retroactive to 2018

3. In Rev. Proc. 2020-23 (04/08/20), IRS allows BBA partnerships (those who did not elect out of CPAR) to

a. File amended 2018 and 2019 Forms 1065 to retroactively benefit from claiming QIP for PPIS > 2017, or

b. Form 3115 per usual protocol

05/13/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 176