21

FC Research May 2017

FC Research

May 2017

• Monetary Policy Review…………..……………………………………………………...............

• $1.5Bn International Sovereign Bond…………………………………………………………….

3

4

• Inflation…………………………………………………………………………………….............. 5

• M2B & Sector Credit…………………………………………………………………............... … 7

• Reserves & Liquidity………………………………………………………………………............ 8

• Currency Movement…………………………………………………………………................... 9

• Government Securities……………………………………………………………….................. 11

• Finance Sector Rate Movement……………………………………………………………..... … 13

• External Sector……………………………………………………………………………………... 14

• Tourist Arrivals……………………………………………………………………………………... 18

• Global Markets……………………………………………………………………………………... 19

May 2017FC Research 2

Policy rates unchanged

Private sector credit growth decelerated gradually to 21.0% in February 2017 and20.4% in March 2017. The Earlier tightening of monetary policy by central bank andresultant increase in interest rates impacted the credit growth.

Combined impact of the decline in export earning and increased expenditure onimports as a result of the drought conditions expanded Trade deficit to USD 1.7Bn tillFebruary 2017.

Gross official reserves dipped to USD 5.1Bn by end April 2017 from USD 6.0Bn by end2016. Both the government securities market and the Colombo Stock Exchangeexperienced foreign inflows in recent months.

Accordingly policy rates were increased,

Standing Deposit Facility Rate – 7.25%

Standing Lending Facility Rate – 8.75%

Statutory Reserve Ratio (SRR) – 7.50%

May 2017FC Research 3

May 2017FC Research 4

The Central Bank of Sri Lanka, on behalf of the Government of Sri Lanka, successfully priceda new US $1.5Bn 10-year International Sovereign Bond on May 4th, 2017. The Bonds havebeen rated ‘B1’, ‘B+’ and ‘B+' by Moody's Investors Service, Standard and Poor’s and FitchRatings respectively.

Sri Lanka has narrowed the country's risk premium by 1.475% thus the bond was priced at6.20%,lower than the initial price guidance of 6.625%. Last sold 10-yr SL sovereign bond on11 July 2016 priced at 6.825%. On July 12,the US 10-yr bond yield at 1.530%, indicating arisk premium of 5.345% at the time. The US 10-yr bond yield is now about 2.330%, indicatinga risk premium over the US yield of only 3.870%

Date

10-Yr SL

Sovereign bond

10-Yr US

Treasury Yield Risk Premium

12-Jul-2016 6.875% 1.530% 5.345%

04-May-2017 6.200% 2.330% 3.870%

Change 0.675% (0.800%) (1.475%)

• Increase of food items by -

1.7%MoM and non-food

items by 0.1%MoM.

• On YoY basis inflation starts to

decline with food inflation

dipping to 8.6% and Non

Food to 6.3% compare with

March 2017 9.2% and 6.5%

respectively.

May 2017FC Research 5

3.4%

4.8%

5.5% 5.8%

4.4%4.2%

4.1% 4.0%

4.5%

5.5%

6.8%

7.3%6.9%

3.5%

5.6%5.4%

5.0%

3.8%

3.7% 3.8%

4.8%

5.8%

7.0%7.1%

7.3%

6.8%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

Inflation YoY Core Inflation YoY

Source: Dept. Census and Statistics

• NCPI for March 2017

increased to 8.6% from 8.2%

in February 2017.

• On YoY basis inflation started

to accelerate with food

inflation climbing to 11.2%

while Non Food to 6.7%.

May 2017FC Research 6

2.2%

4.3%

5.3%

6.4%

5.8%

4.5%

4.7%

5.0%

4.1%

4.2%

6.5%

8.2%

8.6%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

Source: Dept. Census and Statistics

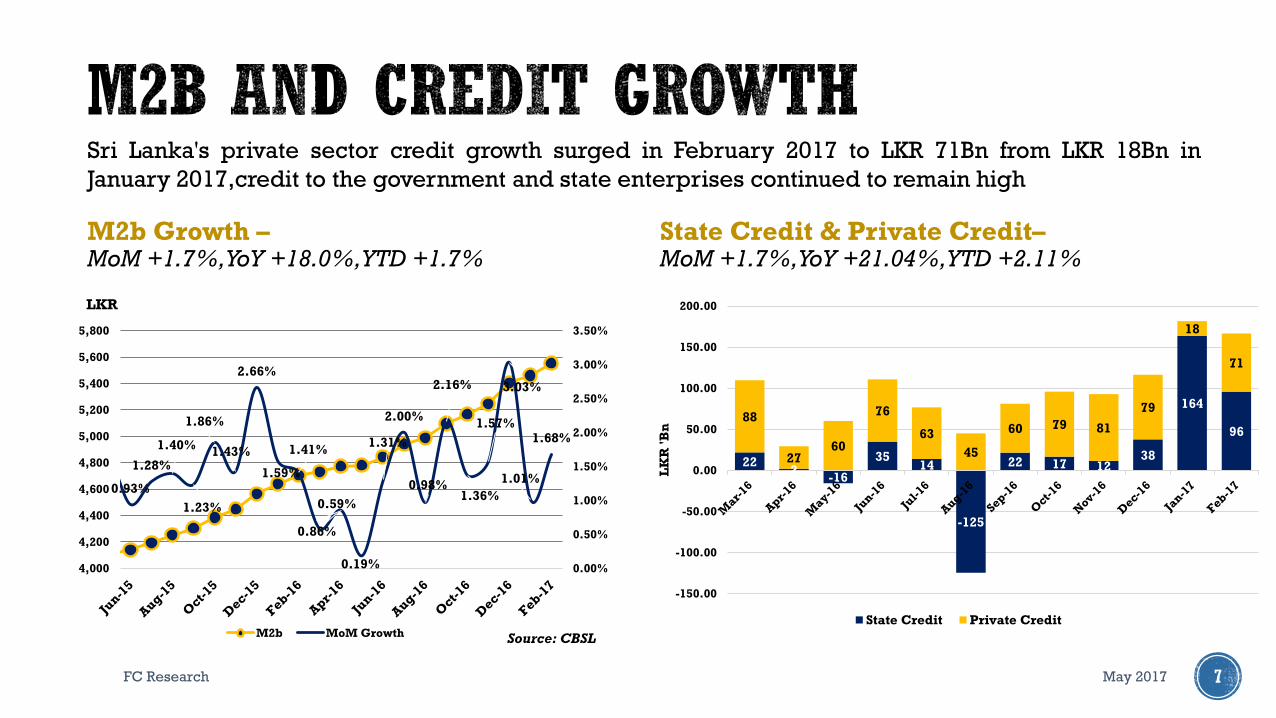

M2b Growth –MoM +1.7%, YoY +18.0%, YTD +1.7%

May 2017FC Research 7

Sri Lanka's private sector credit growth surged in February 2017 to LKR 71Bn from LKR 18Bn in

January 2017,credit to the government and state enterprises continued to remain high

0.93%

1.28%

1.40%

1.23%

1.86%

1.43%

2.66%

1.59%

1.41%

0.59%

0.86%

0.19%

1.31%

2.00%

0.98%

2.16%

1.36%

1.57%

3.03%

1.01%

1.68%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4,000

4,200

4,400

4,600

4,800

5,000

5,200

5,400

5,600

5,800

M2b MoM Growth Source: CBSL

LKR

State Credit & Private Credit–MoM +1.7%, YoY +21.04%, YTD +2.11%

222

-16

3514

-125

22 17 1238

164

9688

2760

76

63

45

60 79 81

79

18

71

-150.00

-100.00

-50.00

0.00

50.00

100.00

150.00

200.00

LK

R '

Bn

State Credit Private Credit

May 2017FC Research 8

Foreign Reserves continue to dip sharply falling to a 84 month (6.9 years) low

Money market continued to stay in deficit due to heavy foreign debt repayments .

650

700

750

800

850

900

950

1000

-80.00

-60.00

-40.00

-20.00

0.00

20.00

40.00

60.00

80.00

100.00

CB

SL

Re

se

rve

s (L

KR

'Bn

)

Ms

rke

t L

iqu

idit

y (

LK

R '

Bn

)

Market Liquidity

CBSL ReservesSource: CBSL

6,4

81

7,2

81

7,3

04

6,2

94

6,5

73

6,2

25

6,0

69

5,6

45

5,2

92

6,4

89

6,5

99

6,4

56

6,0

54

5,6

64

6,0

19

5,4

52 5,6

19

5,1

20

5,0

46

4,500

5,000

5,500

6,000

6,500

7,000

7,500USD 'Mn

Gross Official Reserves (USD mn) Source: CBSL

USD:LKR MovementSri Lankan Rupee vs Global Currencies

May 2017FC Research 9

Source: CBSL

Ap

r 2

01

7Y

TD

20

17

Source: CBSL

-3.5%

-1.9%

-1.3%

-0.9%

-0.1%

0.0%

2.1%

2.1%

UK Pound

Euro

India Rupee

Japan YEN

US Dollar

China Renmiibi

Can Dollar

Aus Dollar

-7.4%

-6.5%

-6.2%

-4.7%

-4.6%

-2.4%

-1.4%

-0.2%

India Rupee

UK Pound

Japan YEN

Aus Dollar

Euro

China Renmiibi

US Dollar

Can Dollar

151.80

152.00

152.20

152.40

152.60

May 2017FC Research 10

-100

-50

0

50

100

150

200

250

300

350

Apr-16 May-16 Jun-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16 Dec-16 Jan-17 Feb-17 Mar-17 Apr-17

Excess Liquidity CBSL Holdings of Gov. Securities Source: CBSL

May 2017FC Research 11

Week EndingBills

('Mn)

Bonds

('Mn)Total

07-Apr-17 25,000 11,480 36,480

12-Apr-17 23,092 23,092

21-Apr-17 21,413 21,413

28-Apr-17 29,500 25,000 54,500

Total Issued 135,485

Apr 2017 YTD

Maturities 126,872 643,332

New Issues 135,485 499,902

Excess/(Deficit) 8,613 -143,430

CBSL Holdings of Gov. Securities YTD

As at End Mar 2017 263,197

As at End Apr 2017 273,544

Increase/ (Decrease) 10,347 -56,534

Interest Rate Change (bps)

Tenure 31-Mar 30-Apr Change (bps) 31-Mar Change (bps)

3M 9.68% 9.73% 5 9.68% 5

6M 10.68% 10.30% -38 10.68% -38

1 Yr 11.03% 10.58% -45 11.03% -45

2 Yrs 11.58% 11.00% -58 11.58% -58

3 Yrs 11.95% 11.45% -50 11.95% -50

4 Yrs 12.55% 11.70% -85 12.55% -85

5 Yrs 12.75% 11.75% -100 12.75% -100

6 Yrs 12.80% 11.80% -100 12.80% -100

8 Yrs 12.80% 12.00% -80 12.80% -80

10 Yrs 12.83% 12.05% -78 12.83% -78

15 Yrs 12.95% 12.38% -57 12.95% -57

20 Yrs 13.18% 12.63% -55 13.18% -55

30 Yrs 13.25% 12.63% -62 13.25% -62

May 2017FC Research 12

Sudden increase in the market liquidity towards the last two weeks the month and renewed

foreign and local buying interest resulted in yields dipping by 50-100bps specifically in the 2 year

to 15 year bonds. The increasing activity during latter part of the month saw an overall net foreign

inflow of LKR 7.25Bn April 2017.

9.00%

10.00%

11.00%

12.00%

13.00%

14.00%

31-Mar 30-Apr Source: CBSL

AWPR vs AWDR Interest Spread

May 2017FC Research 13

Source: CBSLSource: CBSL

Source: CBSL

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

12.0%

13.0%

AWPR AWDR

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

May 2017FC Research 14

Exports decline by 3.8%YoY during Jan 2017 reflecting subdued performance mainly in

earning from industrial exports declined by 6.7%YoY, from textiles and garments, rubber

products and gems, diamonds and jewelry.

Exports

Category 2016

(USD ‘Mn)

2017

(USD ‘Mn)

Change

(%)

Industrial Exports

- Jan

- YTD

716.2

716.2

668.0

668.0

(6.7)

(6.7)

Agricultural

- Jan

- YTD

179.5

179.5

193.7

193.7

7.9

7.9

Mineral and other

- Dec

- YTD

2.9

2.9

3.0

3.0

3.7

3.7

Total

- Dec

- YTD

898.6

898.6

864.7

864.7

(3.8)

(3.8)

89

9

88

8

94

5

70

7

77

6

89

7

89

1

86

6

89

8

85

5

81

0

85

9

86

5

600

650

700

750

800

850

900

950

1,000

USD 'Mn

2016 2017Source: CBSL

Imports

May 2017FC Research 15

Import expenses grew by 13.2% during Jan 2017 Dec 2016 despite 2.6% decline in an

investment goods. The expenditure on intermediate and Consumer goods was driven

mainly by expenditure on refined petroleum, sugar and confectionary, dairy products and

seafood.

Category 2016

(USD ‘Mn)

2017

(USD ‘Mn)

Change

(%)

Consumer goods

- Jan

- YTD

343.5

343.5

358.8

358.8

4.4

4.4

Intermediate

- Jan

- YTD

801.2

801.2

950.1

950.1

18.6

18.6

Investment goods

- Jan

- YTD

443.9

443.9

432.2

432.2

(2.6)

(2.6)

Total

- Jan

- YTD

1,589.1

1,589.1

1,798.4

1,798.4

13.2

13.2

1,5

89

1,4

39

1,5

66

1,4

61

1,5

90 1

,67

6

1,4

33

1,6

49

1,5

43

1,9

06

1,7

32 1

,81

6

1,7

98

1,200

1,300

1,400

1,500

1,600

1,700

1,800

1,900

2,000

2016 2017Source: CBSL

May 2017FC Research 16

-725

-733

-791

-630

-824

-695

-552

-621

-754

-814

-779

-542

-783

-645

-1,051

-922

-957

-934

-1,200 -1,000 -800 -600 -400 -200 0

Balance of Trade

Source: Central Bank

Nov

Trade Balance -13.2%

May 2017FC Research 17

January

USD ‘Mn

2016 2017 Change

(%)

Trade Balance -690.5 -933.7 +35.2%

Earnings from

Tourism333.3 376.7

+12.9%

Workers’

Remittances563.4 571.6

+1.4%

YTD

USD ‘Mn

2016 2017 Change

(%)

Trade Balance -690.5 -933.7 +35.2%

Earnings from

Tourism333.3 376.7

+12.9%

Workers’

Remittances563.4 571.6

+1.4%

Balance of Payments remains negative

Tourism Earnings and Worker Remittances together reach USD

10.7Bn (+8.0%)

-619

-212

-700

-600

-500

-400

-300

-200

-100

0

Jan-16 Jan-17

-691

-934

333 376

563 572

-1,500

-1,000

-500

0

500

1,000

1,500

Jan-16 Jan-17

Trade Balance Earnings from Tourism Workers’ Remittances

US

D '

Bn

UP 17.5% UP 6.1%

May 2017FC Research 18

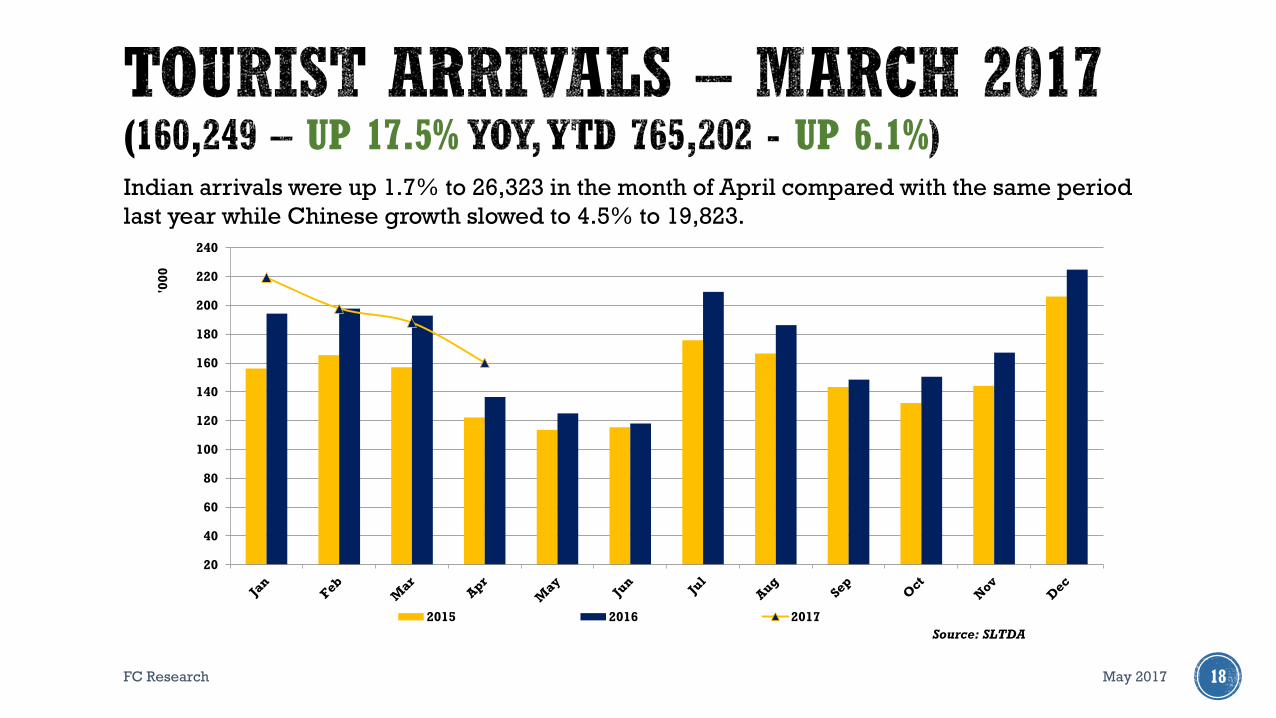

Indian arrivals were up 1.7% to 26,323 in the month of April compared with the same period

last year while Chinese growth slowed to 4.5% to 19,823.

20

40

60

80

100

120

140

160

180

200

220

240

'00

0

2015 2016 2017

Source: SLTDA

FC Research 19

China March Industry Profits Narrowed On Higher Input

Prices: The profitability of Chinese industrial companies rose

more slowly in March compared to earlier in the year because of a

rapid rise in input prices and a higher basis for comparison, data

from the National Bureau of Statistics (NBS) released.

https://www.marketnews.com

Japan Exports Post 4th Straight Rise in Mar, Down in FY2016:

Japan's March exports +12.0% on year (the MNI median

economist forecast: +6.6%), the fourth straight rise after +11.3%

in February, led by higher shipments of auto parts, optical

equipment and steel on a gradual pickup in global demand

http://www.marketnews.com

Euro zone money markets see more chance of ECB hike in

early 2018 after French vote: Euro zone money markets on

Monday priced in a higher chance of a rise in European Central

Bank interest rates after Emmanual Macron won the first round of

the French presidential election.

http://www.reuters.comSource: Bloomberg

May 2017

-2.50% -1.50% -0.50% 0.50% 1.50% 2.50%

FTSE 100

VN Index

S&P 500

Dow Jones

Nifty

Nikkei 225

Euro Stoxx 50

KSE100

FC Research 20

This Review is prepared and issued by First Capital Holdings PLC. based on information in the public domain, internallydeveloped and other sources, believed to be correct. Although all reasonable care has been taken to ensure the contents ofthe review are accurate, First Capital Holdings PLC and/or its Directors, employees, are not responsible for the correctness,usefulness, reliability of same. First Capital Holdings PLC may act as a Broker in the investments which are the subject of thisdocument or related investments and may have acted on or used the information contained in this document, or the researchor analysis on which it is based, before its publication. First Capital Holdings PLC and/or its principal, theirrespective Directors, or Employees may also have a position or be otherwise interested in the investments referred to in thisdocument. This is not an offer to sell or buy the investments referred to in this document. This Review may contain data whichare inaccurate and unreliable. You hereby waive irrevocably any rights or remedies in law or equity you have or may haveagainst First Capital Holdings PLC with respect to the Review and agree to indemnify and hold First Capital Holdings PLCand/or its principal, their respective directors and employees harmless to the fullest extent allowed by law regarding allmatters related to your use of this Review. No part of this document may be reproduced, distributed or published in whole orin part by any means to any other person for any purpose without prior permission.

May 2017

CONTACT

FC Research +94 11 2639 898

• Amanda Lokugamage +94 11 2639 868

• Michelle Weerasinghe +94 11 2639 866

• Dimantha Mathew +94 11 2639 853

• Atchuthan Srirangan +94 11 2639 863

• Hansinee Beddage +94 11 2639 864

21