68

PowerPoint to accompany Chapter 11 Government Interventio n in the Market

| Date post: | 18-Dec-2015 |

| Category: |

Documents |

| Upload: | asher-leslie-bradford |

| View: | 223 times |

| Download: | 2 times |

PowerPoint

to accompany

Chapter 11

Government Intervention in

the Market

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

1. Know the nature and extent of government expenditure in Australia.

2. Understand why a market economy with competition is generally efficient, and understand the economic bases for government intervention.

3. Distinguish between market failure and government failure.

Learning Objectives

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

4. Use graphs to show how externalities affect economic efficiency, and discuss how economic efficiency can be achieved in a market with an externality.

5. Explain how goods can be categorised on the basis of whether they are rival or excludable, and define a public good and a common resource.

6. Discuss how the government and the market deal with contract enforcement and asymmetric information.

Learning Objectives

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

To open a restaurant, there is a large number of regulations that have to be satisfied, including business registration, health and safety, fire prevention regulations, alcohol licenses, etc..

Moreover, tax, insurance and industrial relations laws should also be taken into account.

Selling noodles is harder than you think

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

The size of the public sectorLEARNING OBJECTIVE 1

There are three commonly used ways of measuring the size of the public (government) sector

1. The value of the goods and services produced by the government as a proportion of total production in the economy (gross domestic product, GDP).

2. The number of people employed as a proportion of total employment in the economy.

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

The size of the public sectorLEARNING OBJECTIVE 1

3. The level of government expenditure as a proportion of total expenditure in the economy (as measured by GDP).

This measure includes transfer payments, such as pensions, unemployment benefits and family support payments.

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

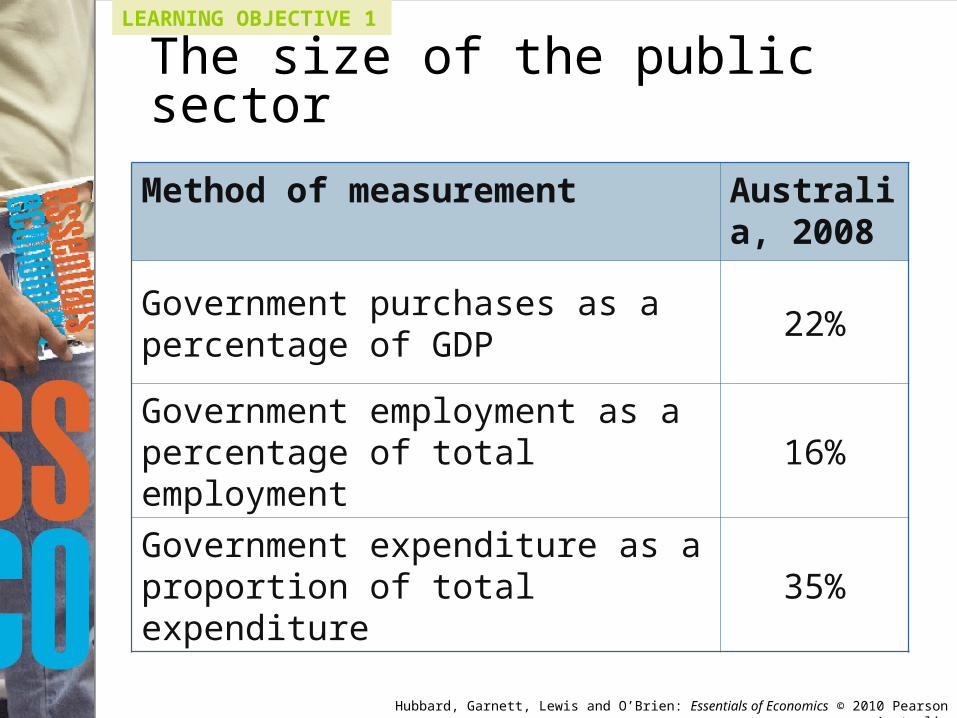

The size of the public sector

LEARNING OBJECTIVE 1

Method of measurement Australia, 2008

Government purchases as a percentage of GDP

22%

Government employment as a percentage of total employment

16%

Government expenditure as a proportion of total expenditure

35%

Source: Annex Table 25, General GovernmentTotal Outlays, OECD, 2008

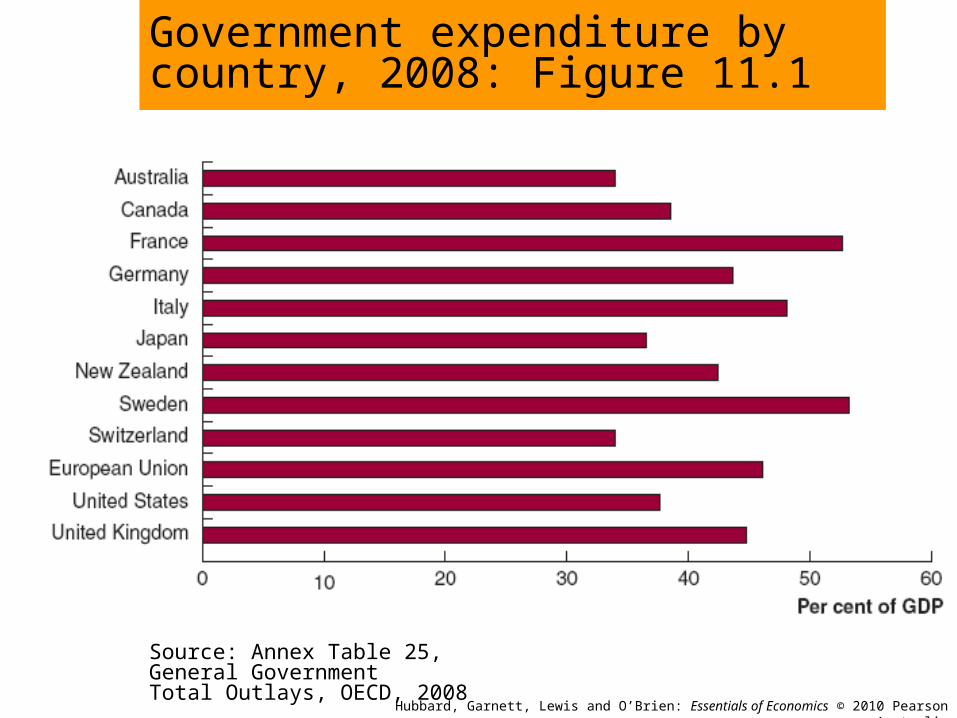

Government expenditure by country, 2008: Figure 11.1

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

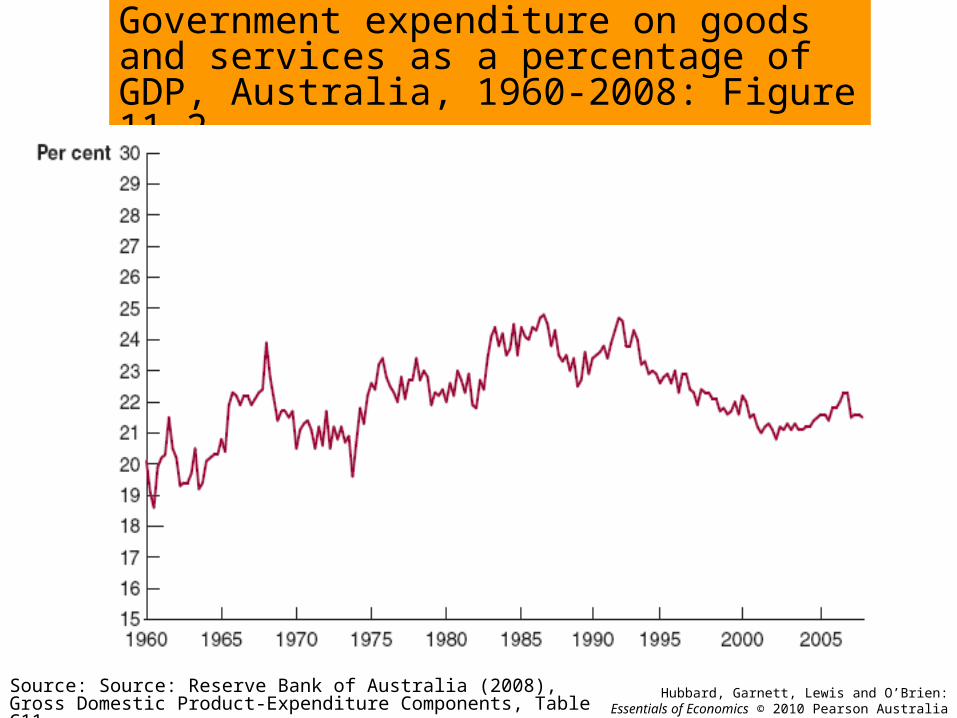

Government expenditure on goods and services as a percentage of GDP, Australia, 1960-2008: Figure 11.2

Source: Source: Reserve Bank of Australia (2008), Gross Domestic Product-Expenditure Components, Table G11.

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

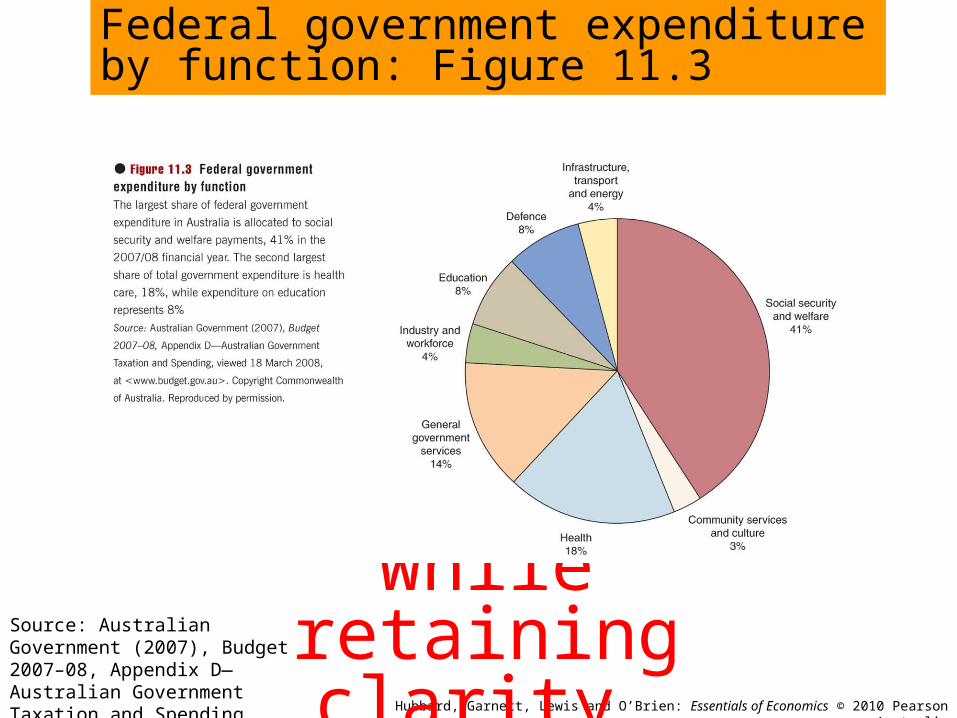

Source: Australian Government (2007), Budget 2007–08, Appendix D—Australian Government Taxation and Spending.

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Federal government expenditure by function: Figure 11.3

Please insert Figure 11.3 from page 328, as large as possible

while retaining clarity.

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Equilibrium in a competitive market results in the economically efficient level of output, where marginal benefit equals marginal cost.

Also, equilibrium in a competitive market results in the greatest amount of economic surplus, or total net benefit to society, from the production of a good or service.

LEARNING OBJECTIVE 2

What’s good about markets?

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Although markets often lead to economic efficiency, the majority of economists acknowledge the necessity for some government intervention.

LEARNING OBJECTIVE 2

The economic bases for government intervention

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Reasons for government intervention include:

1. The legal system and the rule of law.

2. Maintaining or enforcing competition. In Australia, the Australian Competition and

Consumer Commission (ACCC) aims to ensure that trade practices foster competition.

Contestable market: A market in which the potential for competition exists due to minimal entry and exit costs. Even monopoly markets may have the potential to be competitive with government intervention.

Governments at times try to make markets contestable, eg: telecommunications.

LEARNING OBJECTIVE 2

The economic bases for government intervention

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

3. Natural monopolies: A situation in which economies of scale are so large that one firm can supply the entire market at a lower than average total cost than can two or more firms.

4. Externality: A benefit or cost that affects someone who is not directly involved in the production or consumption of a good or service.

LEARNING OBJECTIVE 2

The economic bases for government intervention

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

5. Common resource: An extreme case of externality where no one can be denied access to the good or service but one person’s use of the resource reduces the possible use by others. The resource is rival but not excludable.

6. Public good: A good or service which an additional consumer does not ‘use up’ or prevent another’s use of it, and no one can be excluded from consuming the good or service. It is both non-rival and non-excludable.

LEARNING OBJECTIVE 2

The economic bases for government intervention

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

7. Merit good: A good which is beneficial to society irrespective of the preferences of consumers.

Examples may include museums and art galleries.

8. Asymmetric information.

9. Equity.

10. Stabilisation (macroeconomic) policy.

LEARNING OBJECTIVE 2

The economic bases for government intervention

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Should drugs be legal?

How far should individual freedoms extend?

MAKING THE CONNECTION11.1

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Market failure and government failure

LEARNING OBJECTIVE 3

Market failure: Occurs when the market does not result in an economically efficient outcome.

Public interest view of government sees it as the role of government to correct for areas of market failure.

Government failure: Occurs when the government fails to correct adequately for market failure or takes actions that lead to a more inefficient outcome than the market.

Private interest view focuses on the activities and policies of governments that bring about government failure.

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Market failure and government failure

LEARNING OBJECTIVE 3

Private interest view: Rent seeking individuals or groups lobby the government for certain types of regulations and policies that will enable them to capture economic rents at the expense of the general public and economic efficiency.

Rent-seeking behaviour: An unproductive activity of an individual or firm in the pursuit of economic profit above that which would result from a competitive market outcome.

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Market failure and government failure

LEARNING OBJECTIVE 3

Market failure may require government intervention and regulations to increase efficiency, however, sometimes the removal of regulations may be what is required to increase efficiency.

Deregulation: The policy of reducing government intervention in the market to enable more competition and the unhindered allocation of resources in the economy.

Privatisation: The sale of government-owned businesses and assets to the private sector.

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Externalities and efficiency

Externality: A benefit or cost that affects someone who is not directly involved in the production or consumption of a good or service.

Economic efficiency is reduced, as externalities lead to a divergence between:

Private benefits and social benefits

Private costs and social costs

LEARNING OBJECTIVE 4

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Externalities and efficiency Private cost: The cost borne by the producer of

a good or service. Social cost: The total cost of producing a good

or service, including both the private cost and any external cost.

Private benefit: The benefit received by the consumer of a good or service.

Social benefit: The total benefit from consuming a good or service, including both the private benefit and any external benefit.

LEARNING OBJECTIVE 4

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Externalities and efficiencyHow a negative externality in production reduces economic efficiency

Negative production externalities occur when a production activity imposes costs on others who are not directly associated with that activity, and no compensation is paid.

The social cost of the production activity is greater than the private cost of production.

Production occurs at a level that is higher than the socially efficient level, and price is lower than the socially efficient price.

A deadweight loss occurs.

LEARNING OBJECTIVE 4

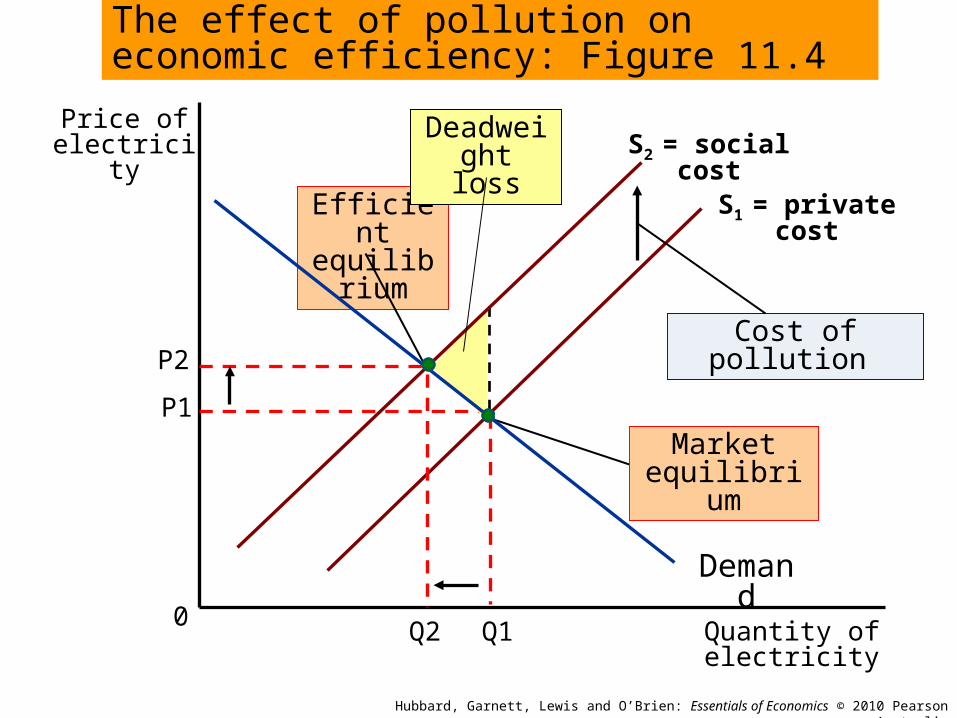

Price of electricity

Quantity of electricity0

Q1

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

P1

S1 = private cost

The effect of pollution on economic efficiency: Figure 11.4

Demand

Cost of pollution P2

Q2

S2 = social cost

Market equilibrium

Efficient equilibrium

Deadweight loss

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Externalities and efficiency

Examples of negative production externalities include: noise, air, visual and water pollution

land degradation and/or contamination

LEARNING OBJECTIVE 4

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

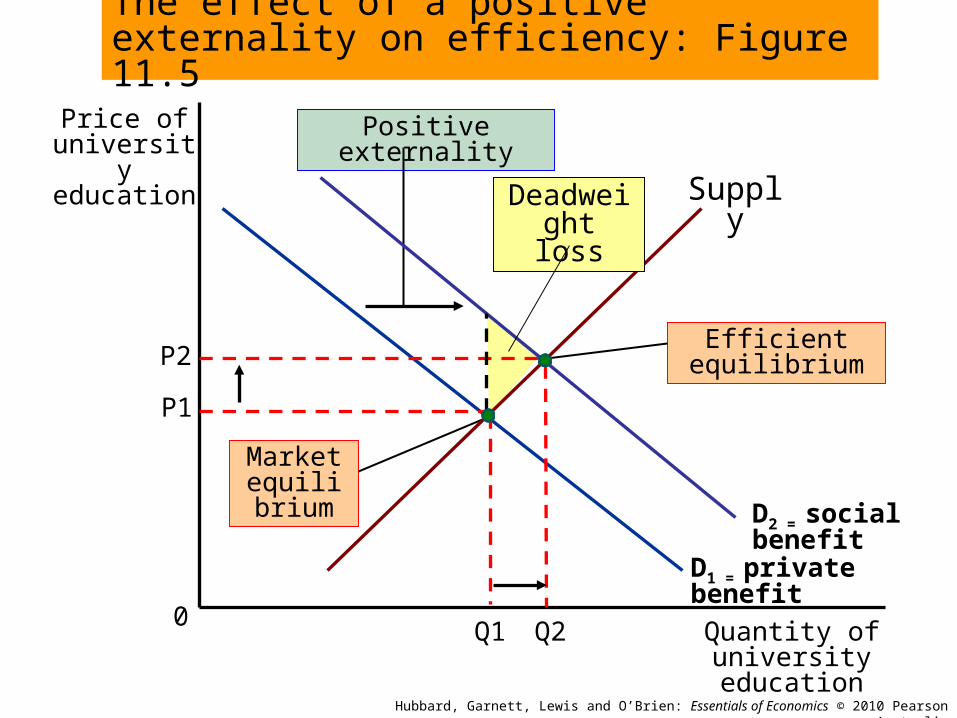

Externalities and efficiencyHow a positive externality in consumption reduces economic efficiency

Positive consumption externalities occur when a consumption activity benefits others who are not directly involved, and who do not pay for it.

The social benefit from the consumption activity is greater than the private benefit from the activity.

Consumption occurs at a level that is lower than the socially efficient level, and price is higher than the socially efficient price.

A deadweight loss occurs.

LEARNING OBJECTIVE 4

Price of university education

Quantity of university education

0Q1

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

P1

Supply

Positive externality

Efficient equilibrium

Market equilibrium

D2 = social benefit

P2

Q2

D1 = private benefit

The effect of a positive externality on efficiency: Figure 11.5

Deadweight loss

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Externalities and efficiency

LEARNING OBJECTIVE 4

Externalities can result in market failure Market failure: Situations where the market

fails to produce the efficient level of output.

What causes externalities? Externalities and market failure result from

incomplete property rights or from the difficulty of enforcing property rights in certain situations.

Property rights: The rights individuals or businesses have to the exclusive use of their property, including the right to buy or sell it.

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Externalities and efficiency

The economically efficient level of pollution reduction

The efficient level of pollution is not zero, (neither is this possible).

The optimal decision is to continue an activity up to the point where the marginal benefit from that activity is equal to the marginal cost.

This concept also applies to the activity of pollution reduction.

LEARNING OBJECTIVE 4

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Externalities and efficiency

The economically efficient level of pollution reduction

There are benefits from pollution reduction and costs of pollution reduction.

As more pollution is reduced, the additional benefits become smaller, and the additional costs of pollution reduction become greater.

LEARNING OBJECTIVE 4

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Externalities and efficiencyThe economically efficient level of

pollution reduction

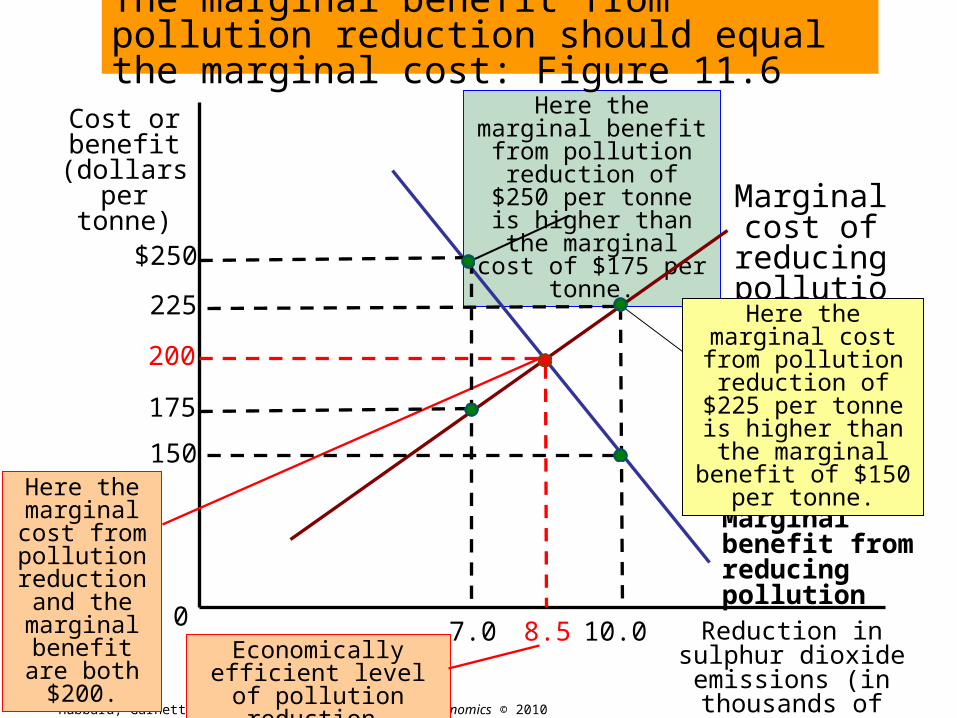

The efficient level of pollution reduction is up to the point where the marginal benefit from pollution reduction is equal to the marginal cost of pollution reduction: MB = MC.

LEARNING OBJECTIVE 4

If MB > MC Further reduction will make society better off

If MB < MC Further reduction will make society worse off

If MB = MC Efficient level of pollution reduction has been achieved

Cost or benefit

(dollars per tonne)

Reduction in sulphur dioxide emissions (in thousands of tonnes

per year

07.0

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

175

Marginal cost of reducing

pollution

Here the marginal benefit from pollution reduction of $250 per tonne is higher than the marginal cost of

$175 per tonne.

Economically efficient level of pollution reduction.

Here the marginal cost from pollution reduction and the marginal

benefit are both $200.

Marginal benefit from reducing pollution

200

8.5

The marginal benefit from pollution reduction should equal the marginal cost: Figure 11.6

Here the marginal cost from pollution reduction

of $225 per tonne is higher than the marginal

benefit of $150 per tonne.

10.0

150

225

$250

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

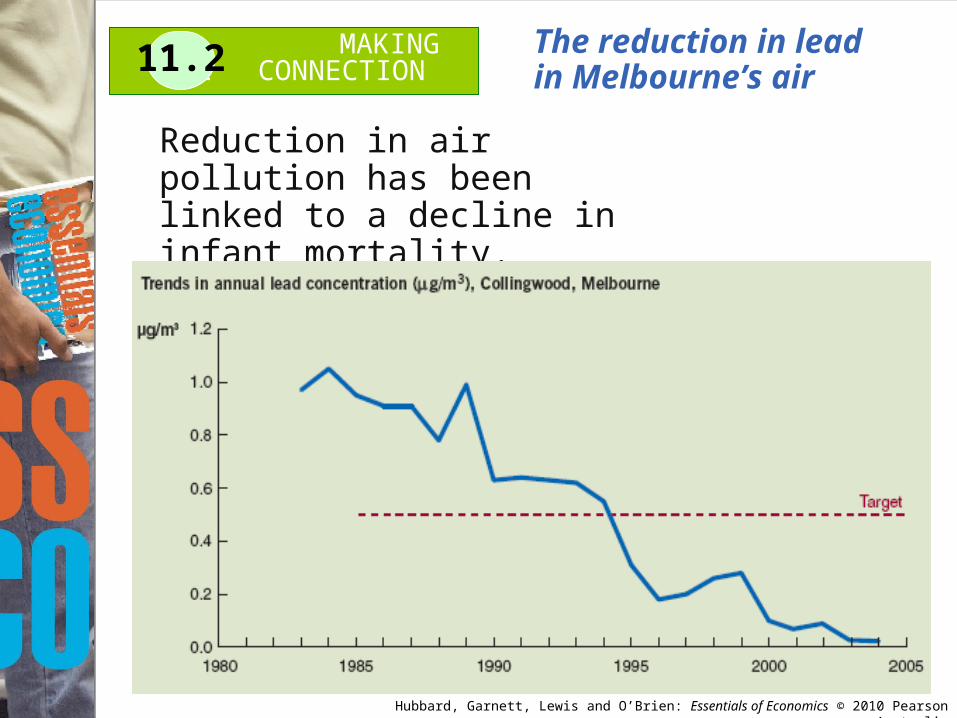

The reduction in lead in Melbourne’s air

Reduction in air pollution has been linked to a decline in infant mortality.

MAKING THE CONNECTION11.2

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

LEARNING OBJECTIVE 4

The Coase Theorem: The basis for private solutions to externalities

Economist Ronald Coase argued:

If transaction costs are low, private bargaining will result in an efficient solution to the problem of externalities.

Transactions costs: The costs in time and other resources that parties incur in the process of agreeing to and carrying out an exchange of goods or services.

Externalities and efficiency

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

LEARNING OBJECTIVE 4

The Coase Theorem: The basis for private solutions to externalities

The company causing the pollution could pay the victims for the right to pollute, or,

The victims could pay the polluting company to reduce pollution.

Limitations to the Coase Theorem Large number of parties involved in

bargaining. Unreasonable demands. All parties must have full information about

the costs and benefits of pollution reduction.

Externalities and efficiency

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

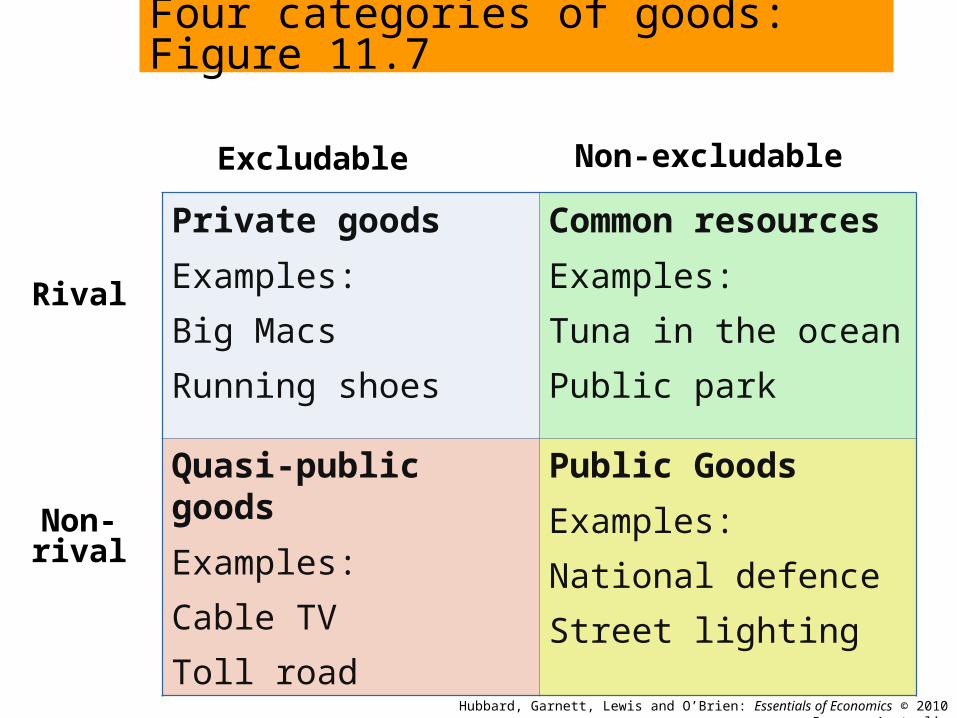

Four categories of goods

LEARNING OBJECTIVE 5

All goods differ on the basis of whether their consumption is rival and excludable.

Rivalry: The situation that occurs when one person consuming a unit of a good means no one else can consume it.

Excludability: The situation in which anyone who does not pay for a good cannot consume it.

There are four categories of goods: private, public, quasi-public and common resources.

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Four categories of goods

LEARNING OBJECTIVE 5

Private good: A good or service that is both rival and excludable.

Public good: A good or service which an additional consumer does not ‘use up’ or prevent another’s use of it, and no one can be excluded from consuming the good or service. It is both non-rival and non-excludable. Free riding: Benefiting from a good without paying

for it.

Quasi-public good: A good that is excludable but not rival.

Common resource: A resource that is rival but not excludable.

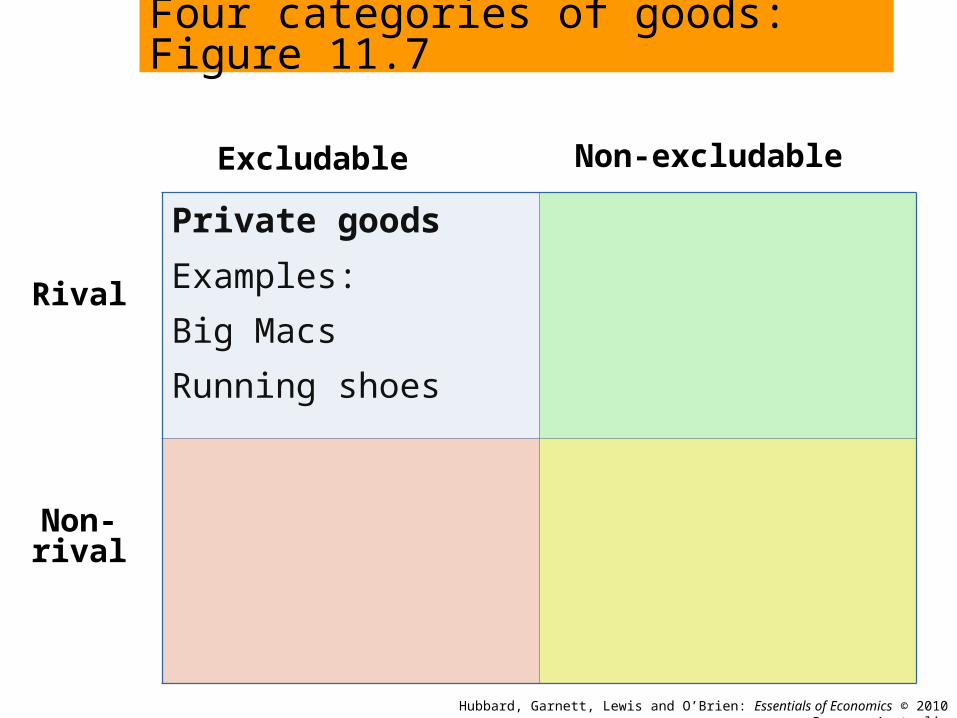

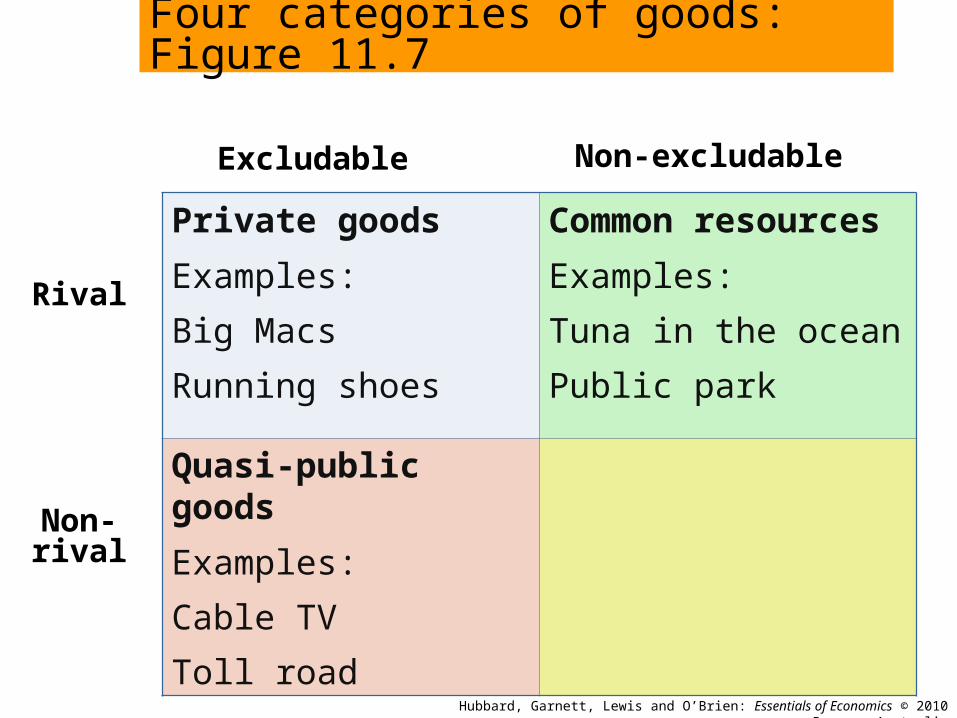

Four categories of goods: Figure 11.7

Private goods

Examples:

Big Macs

Running shoes

Excludable Non-excludable

Rival

Non-rival

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Four categories of goods: Figure 11.7

Private goods

Examples:

Big Macs

Running shoes

Common resources

Examples:

Tuna in the ocean

Public park

Excludable Non-excludable

Rival

Non-rival

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Four categories of goods: Figure 11.7

Private goods

Examples:

Big Macs

Running shoes

Common resources

Examples:

Tuna in the ocean

Public park

Quasi-public goods

Examples:

Cable TV

Toll road

Excludable Non-excludable

Rival

Non-rival

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Four categories of goods: Figure 11.7

Private goods

Examples:

Big Macs

Running shoes

Common resources

Examples:

Tuna in the ocean

Public park

Quasi-public goods

Examples:

Cable TV

Toll road

Public Goods

Examples:

National defence

Street lighting

Excludable Non-excludable

Rival

Non-rival

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Four categories of goodsLEARNING OBJECTIVE 5

The optimal quantity of a public good

Difficult for the government to know what quantity to supply, because:

Consumer preferences are not revealed in the market.

A price cannot be charged so there is not price mechanism.

Cost-benefit analysis is sometimes used to determine what quantity of public goods to supply.

The political process is frequently used to determine supply, eg: national defence.

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Four categories of goods

LEARNING OBJECTIVE 5

Common resources

Tragedy of the commons: The tendency for a common resource to be overused.

The source of the tragedy of the commons is the lack of clearly defined and enforced property rights.

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Four categories of goods

LEARNING OBJECTIVE 5

Solutions to the tragedy of the commons?

Legal restrictions on access to the common resource.

Taxes

Tradable permits

Quotas

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Policy for business and individual behaviour that can increase economic efficiency

LEARNING OBJECTIVE 6

The rule of law

The rule of law: The ability of a government to enforce the laws of the country, particularly with respect to protecting private property and enforcing contracts.

The rule of law is essential for economic development. Entrepreneurs will not risk investing in a business if

their property is not protected by law. Contracts will not be entered in to unless they can be

enforced.

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Policy for business and individual behaviour that can increase economic efficiency

LEARNING OBJECTIVE 6

Patents and copyright protection

Patent: The exclusive right to a new product for a specified number of years from the date the product is invented.

Copyright: The legal right of the creator of a book, movie, piece of music or software program to exclusively use the creation during their lifetime.

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Policy for business and individual behaviour that can increase economic efficiency

LEARNING OBJECTIVE 6

Asymmetric information

Asymmetric information: When one party to an economic transaction has less information than the other party.

Adverse selection: The situation in which one party to a transaction takes advantage of knowing more than the other party to the transaction.

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Policy for business and individual behaviour that can increase economic efficiency

LEARNING OBJECTIVE 6

Reducing adverse selection in the car market

Warranties: Free repairs on the car for a specified time period after purchase.

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Policy for business and individual behaviour that can increase economic efficiency

LEARNING OBJECTIVE 6

Reducing adverse selection in the insurance market

Applicants for health insurance undergo medical examinations/ submit medical records.

Applicants for car insurance will have their driving record reviewed and may be charged higher premiums.

Group coverage to large firms.

Use of excess payments and co-payments.

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Policy for business and individual behaviour that can increase economic efficiency

LEARNING OBJECTIVE 6

Reducing moral hazard in the insurance market

Moral hazard: The tendency of people who have insurance to change their actions because they have insurance. More broadly, it is an action taken by one party to a transaction that is different to what the other party expected at the time of the transaction.

Use of specific requirements, eg: require the installation of smoke detectors in buildings.

Use excess payments and co-payments.

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Why is the cost of health care rising in Australia?

Government policy has previously tried to increase the uptake of private health insurance in Australia.

MAKING THE CONNECTION11.3

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Hourly wages in the retail sector, and adverse selection and moral hazard

LEARNING OBJECTIVE 6

Li Jong Tan is opening a new furniture store. She is hiring two store salespeople and planning to pay them an hourly wage that is above the minimum wage required by Federal legislation. By paying a higher wage she is hoping that salespeople will provide better quality customer service and care.

Do you think Li is making the right decision to pay a higher hourly wage? Will she be able to avoid adverse selection and moral hazard problems?

What kind of compensation arrangement would be better to avoid these problems?

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

LEARNING OBJECTIVE 6

Hourly wages in the retail sector, and adverse selection and moral hazard

STEP 1: Review the chapter material. This problem is about moral hazard, which also occurs in labour markets, so you may want to review the sections on adverse selection and moral hazard.

STEP 2: Use the ideas of adverse selection and moral hazard to answer question 1. When salespeople are paid an hourly wage their compensation is determined by how many hours they are at work, rather than how much they sell. So, if they are not monitored they may have an incentive to expend as little effort as possible. Moreover, this type of compensation arrangement may discourage most capable salespeople from applying.

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

LEARNING OBJECTIVE 6

Hourly wages in the retail sector, and adverse selection and moral hazard

STEP 3: Answer question 2 by offering another compensation system for Li. Li should consider a commission-based arrangement where part of the wage (above the Federal minimum) would be linked to the number of furniture pieces sold. That way, she may be able to attract people who are prepared to work harder and she will provide them with incentives to sell more furniture, so her sales and profits should be higher.

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

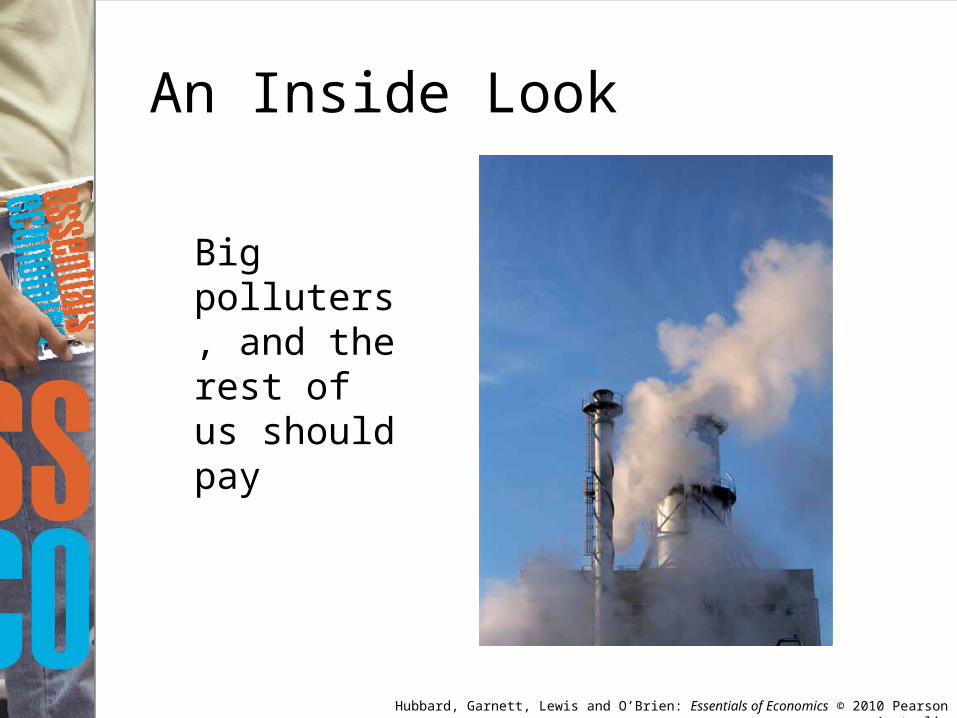

An Inside Look

Big polluters, and the rest of us should pay

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

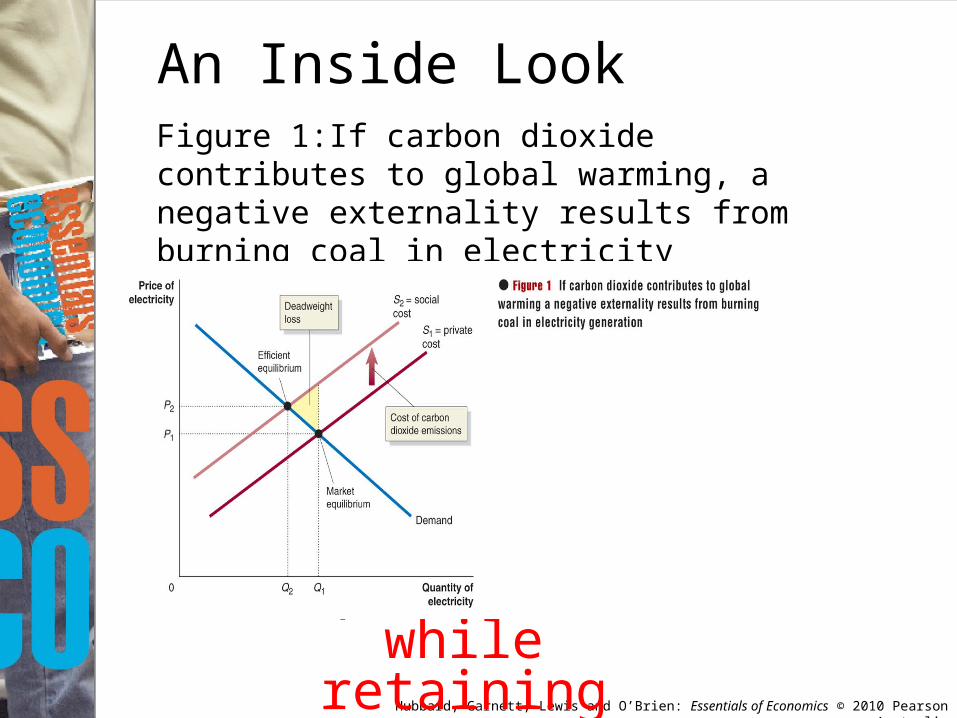

An Inside LookFigure 1:If carbon dioxide contributes to global warming, a negative externality results from burning coal in electricity generation.

Insert Figure 1 from page 354, as large as possible

while retaining clarity

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Key Terms Adverse selection Asymmetric information Coase theorem Common resource Contestable market Copyright Deregulation Excludability Externality Free riding Government failure Market failure Merit good Moral hazard Natural monopoly Patent

Private benefit Private cost Private good Public good Privatisation Property rights Public good Quasi-public good Rent-seeking behaviour Rivalry Social benefit Social cost The rule of law Tragedy of the commons Transactions costs

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Get Thinking!In November 2008, the Rudd Labour Government removed the 2005 Howard Government’s ‘WorkChoices’ legislation that allowed workers and employers to negotiate individual contracts of employment (and avoid collective agreements).

1) Putting aside your views on the other aspects of the WorkChoices 2005 legislation, do you think it was a good law to reduce adverse selection and moral hazard in the labour market?

2) Compare advantages and disadvantages of individual contracts versus collective agreements.

http://www.wrc.org.au/documents/WP39.pdf

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Check Your Knowledge

Q1. The majority of economists agree that:

a. there is some scope for government intervention in the market.

b. there is no role for government intervention in the market.

c. governments should play a dominant role in the economy.

d. there is no dominant view among the economists if the scope for government intervention exists.

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Check Your Knowledge

Q1. The majority of economists agree that:

a. there is some scope for government intervention in the market.

b. there is no role for government intervention in the market.

c. governments should play a dominant role in the economy.

d. there is no dominant view among the economists if the scope for government intervention exists.

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Check Your Knowledge

Q2. The net benefit to society from reducing pollution is equal to ________.

a. the sum of the benefits of reducing pollution minus the costs.

b. the benefits multiplied by the costs.

c. the additional benefit plus the additional costs.

d. the quantity of pollution, such as the tons of reduction in sulfur dioxide.

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Check Your Knowledge

Q2. The net benefit to society from reducing pollution is equal to ________.

a. the sum of the benefits of reducing pollution minus the costs.

b. the benefits multiplied by the costs.

c. the additional benefit plus the additional costs.

d. the quantity of pollution, such as the tons of reduction in sulfur dioxide.

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Check Your Knowledge

Q3. How would you characterise the solution to externalities proposed by the Coase Theorem?

a. A private solution to externalities.

b. A public solution to externalities.

c. The only solution to externalities.

d. The least preferred solution.

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Check Your Knowledge

Q3. How would you characterise the solution to externalities proposed by the Coase Theorem?

a. A private solution to externalities.

b. A public solution to externalities.

c. The only solution to externalities.

d. The least preferred solution.

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Check Your Knowledge

Q4. When uninformed buyers are willing to pay the average of the price of ‘lemons’ and good used cars, which of the following will occur?

a. Most used cars offered for sale will be good used cars.

b. Most used cars offered for sale will be ‘lemons’.

c. The quantity supplied of ‘lemons’ will be identical to the quantity supplied of good used cars.

d. Only good used cars will remain in the market.

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Check Your Knowledge

Q4. When uninformed buyers are willing to pay the average of the price of ‘lemons’ and good used cars, which of the following will occur?

a. Most used cars offered for sale will be good used cars.

b. Most used cars offered for sale will be ‘lemons’.

c. The quantity supplied of ‘lemons’ will be identical to the quantity supplied of good used cars.

d. Only good used cars will remain in the market.

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Check Your Knowledge

Q5. If potential buyers have difficulty separating ‘lemons’ from good used cars, what will they do?

a. They will not take this into account in the prices they are willing to pay.

b. They will be absolutely indifferent between cars, and will pay the same price for either type of car.

c. They will take this into account in the prices they are willing to pay.

d. They will pay a price for a car that is always too high.

Hubbard, Garnett, Lewis and O’Brien: Essentials of Economics © 2010 Pearson Australia

Check Your Knowledge

Q5. If potential buyers have difficulty separating lemons from good used cars, what will they do?

a. They will not take this into account in the prices they are willing to pay.

b. They will be absolutely indifferent between cars, and will pay the same price for either type of car.

c. They will take this into account in the prices they are willing to pay.

d. They will pay a price for a car that is always too high.