27

PPCmetrics AG Investment & Actuarial Consulting, Controlling and Research. www.ppcmetrics.ch

PPCmetrics AG

Investment & Actuarial Consulting,

Controlling and Research. www.ppcmetrics.ch

PPCmetrics AG

Investment Consulting

© PPCmetrics AG

Responsible Investing – General Considerations and

Implications for Fixed Income

EPFIF

Dr. Diego Liechti, Senior Investment Consultant

Bern, September 21, 2016

Introduction

Definition

According to Cambridge Dictionary:

• Sustainability

1. The ability to continue at a particular level for a period of

time.

2. Environment, natural resources:

The idea that goods and services should be produced in ways

that do not use resources that cannot be replaced and that do

not damage the environment.

• Socially responsible investment

1. An investment in a company whose business is not harmful

to society or the environment.

2 © PPCmetrics AG

Source: http://dictionary.cambridge.org/dictionary/english/

Introduction

Brief History of Socially Responsible Investing

• At the end of the 17th century, religious investors refused investing in

alcohol, gambling and tobacco companies.

– In 1928, a group of 24 funds (“pioneer group”) conducted a sin screening

of the investments, which led to the exclusion of the above mentioned

industries.

• In the 60s, student protests against the war in Vietnam led to a

continued exclusion of the arms industry (e.g., at the Pax World

Fund).

• In 1972, the Dreyfuss Corporation excluded companies that were

doing business in South Africa due to the Apartheid.

• In the 80s, socially responsible investing became “mainstream” (e.g.,

Calvert established 9 funds).

• Around 1990, the first sustainable index was introduced (Domini 400

Social Index).

3 © PPCmetrics AG

Source: Cory (2012)

Investment Case

Arguments for Socially Responsible Investments

• Avoiding reputation risks (also from employer’s perspective)

• Anticipating a possible regulation

• Act in the beneficiary's best interest

• Achieving an outperformance compared to the benchmark

(Does it pay to be good? Or to be bad?)

• Combine business with pleasure: earn money and make a

difference

4 © PPCmetrics AG

Investment Case

Critical Evaluation of Arguments (1)

• Avoiding reputation risks (also from employer’s side)

Avoiding negative news paper articles

? However: in what way is reputation relevant for the achievement of

the pension fund’s main purpose, i.e., securing rents?

? Possible goal: align the investment policy of the pension fund with

the strategy of the company and the values of the employees.

5 © PPCmetrics AG

Investment Case

Critical Evaluation of Arguments (2)

• Anticipating a possible regulation

Weak argument due to transition periods.

• Act in the beneficiary's best interest

According to open-ended surveys, monetary

and service-oriented aspects are important

for employees.

However, in closed-ended surveys, where

sustainability is explicitly a possibility,

the insured employees think it is important.

6 © PPCmetrics AG

Investment Case

Critical Evaluation of Arguments (3)

• Achieving an outperformance compared to the benchmark

(Does it pay to be good? Or to be bad?)

? There are arguments and studies which argue for an out- or and

underperformance ?!

7 © PPCmetrics AG

Source: Dimson, Marsh and Staunton (2015)

Investment Case

Critical Evaluation of Arguments (4)

• Expecting an outperformance compared to the benchmark

Sustainability reduces risks, e.g., litigation or reputation risks.1

Sustainable companies have a better governance. 2

These risks could be compensated by the financial markets.

The price of a “sin” stock is lower and as a consequence, the

expected return increases.

Investors require compensation to hold such “noxious and

nasty” stocks.

“Sin” companies have steady demand for their goods and services

and high entry barriers. high-margins business

Academic and empirical studies indicate a lower return for

sustainable stocks.3

8 © PPCmetrics AG

1, 3 Nofsinger and Varma (2014) 2 Renneboog, ter Horst and Zhang (2007) 3 e.g., Fabozzi, Ma, Oliphant (2008)

Investment Case

Critical Evaluation of Arguments (5)

• Empirically, “sin

stocks”, i.e., alcohol,

tobacco, and gambling

outperform.1

– The same with

weaponry.

• Tobacco made a

transition from neutral to

sinful between 1947 -

1965. During that time,

those stocks

underperformed.

– After 1965 it was known

that smoking is harmful,

they outperformed again.

9 © PPCmetrics AG

1 Hong and Kacperczyk (2009)

Investment Case

Critical Evaluation of Arguments (6)

10 © PPCmetrics AG

0

20

40

60

80

100

120

12.1

99

9

05.2

00

0

10.2

00

0

03.2

00

1

08.2

00

1

01.2

00

2

06.2

00

2

11.2

00

2

04.2

00

3

09.2

00

3

02.2

00

4

07.2

00

4

12.2

00

4

05.2

00

5

10.2

00

5

03.2

00

6

08.2

00

6

01.2

00

7

06.2

00

7

11.2

00

7

04.2

00

8

09.2

00

8

02.2

009

07.2

00

9

12.2

00

9

05.2

01

0

10.2

01

0

03.2

011

08.2

01

1

01.2

01

2

06.2

01

2

11.2

01

2

04.2

013

09.2

01

3

02.2

01

4

07.2

01

4

12.2

01

4

05.2

015

10.2

01

5

03.2

01

6

Diagrammtitel

Dow Jones Global

Dow Jones Sustainability World

Dow Jones Sustainability World ex Tobacco

Dow Jones Sustainability World ex Gambling

Total Returns of Sustainable DJ Indices

Source: Bloomberg, own calculations

Investment Case

Critical Evaluation of Arguments (7)

11 © PPCmetrics AG

• Stock returns are the highest in the most corrupt countries.

Source: Dimson, Marsh and Staunton (2015)

Investment Case

Critical Evaluation of Arguments (8)

• Combine business with pleasure: earn money and make a

difference.

In theory, the financing costs should increase. As a

consequence, the company could change its policy to lower its

financing costs.

There is no academic evidence that avoiding such “sin”

investments has a positive impact.

? Interestingly, evidence suggests that investing in a “noxious

and nasty” company and changing its behaviour through

shareholder activism leads to a higher risk-adjusted return.1

However, shareholder activism funds are expensive.

12 © PPCmetrics AG

1 Dimson, Karakas, and Li (2015)

Investment Case

Further Aspects: Higher Costs

• Ceteris paribus, socially responsible investments come with

additional costs (e.g., asset management fees, transaction

costs, etc.).

– A sustainable strategy excludes an indexed implementation for

smaller pension funds.1

13 © PPCmetrics AG

*Source: PPCmetrics Peer Group ** Source: Tender documents of selection with a broad universe

1 There are usually no passive collective investment schemes. A segregated mandate would be between 0.04% and 0.10% more expensive than standard indexed

mandates.

0.00% 0.05% 0.10% 0.15% 0.20% 0.25% 0.30% 0.35% 0.40%

Active Balanced Mandate**

Sustainable Balanced Mandate**

Passive Balanced Mandate*

Fee p.a.

Diagrammtitel Management Fees of Mandates with a Size of CHF 100 Million

Investment Case

Further Aspects: Definition Problems

• Disagreement on the definition

– Should car manufacturers be excluded or included (carbon

emissions vs. development of energy-efficient vehicles)?

– What about oil firms investing in “clean energy”?

• Definition problems

– What about suppliers or firms that buy products (or services) of

“sin” companies?

– What about banks financing such companies?

– What about countries using the death penalty? What about

countries financing nuclear plants?

– A lot of products can be used for several purposes: e.g., micro

chips are used both for mobile phones and missiles.

• Pilatus: Indian Air Force vs. Royal Flying Doctor Service of Australia

14 © PPCmetrics AG

Investment Case

Further Aspects: Can such Cases be Anticipated?

• Take a look at some cases:

– BP Deepwater horizon

– Union Carbide Bhopal

– Exxon Exxon Valdez

– Japan Fukushima

– Lockheed bribery

– Grünenthal children with malformation of the limbs

– Siemens corruption

– Enron false accounting

– Walmart child labor

– Mattel lead paint

15 © PPCmetrics AG

Implementation in Case of Bonds

Basic Questions

16 © PPCmetrics AG

Reporting (from the asset manager and to beneficiaries)

Mandate structure? Asset manager (selection)?

Active or passive?

Implementation strategy (Exclude industries? Exclude firms? Best in class? Thematic Funds)

Shall those criteria be applied to all bond segments (including treasuries)?

What is the sustainability target?

What criteria is important to us, i.e., what do the beneficiaries think is important?

Implementation in Case of Bonds

Sustainable Treasuries: Some Food for Thought (1)

• Implementation with corporates is not a problem, but …

why are there (at least at the moment) no sustainable

indices for treasuries?

• Because you might end up with an undiversified portfolio.

Example Citigroup WGBI:

– Exclude:

• USA (e.g., climate protection, death penalty, nuclear weapons)

• Japan (e.g., climate protection, death penalty, whaling)

• France (nuclear power, nuclear weapons)

• UK (nuclear weapons)

• ….

• Switzerland (euthanasia)

• So how does the portfolio look like?

17 © PPCmetrics AG

Implementation in Case of Bonds

Sustainable Treasuries: Some Food for Thought (2)

18 © PPCmetrics AG

Source: Citigroup Yieldbook, Indexdata per August 31, own calculations.

United States

JapanAustria

France

Germany

Ireland

Italy

Spain

DenmarkUnited Kingdom

Diagrammtitel

United States Canada Mexico Australia Japan Malaysia

Singapore Austria Belgium Finland France Germany

Ireland Italy Netherlands Spain Denmark Norway

Poland Sweden Switzerland United Kingdom South Africa

Citigroup WGBI vs. sustainable WGBICitigroup WGBI vs. Sustainable WGBI

Austria

Germany

Ireland

Spain

Denmark

Summary

19 © PPCmetrics AG

There are reasons to invest socially responsible.

However, you have to keep in mind the consequences.

And…. it is not always easy to distinguish good from

bad … there might be an ugly as well.

Appendix

References

• Cory, J, 2012. Business Ethics: The Ethical Revolution of Minority

Shareholders. Springer.

• Dimson, E., Karakas, O. and Li, X., 2015. Active Ownership. Review of

Financial Studies 28, 3225-3268.

• Fabozzi, F.J., MA, K.C., Oliphant, B.J., 2008. Sin Stock Returns.

Journal of Portfolio Management, Autumn

• Hong, H., Kacperczyk, M., 2009. The Price of Sin: The Effects of

Social Norms on Markets. Journal of Financial Economics 93,15–36.

• Renneboog, L., Horst, J., Zhang, Ch., Socially Responsible

Investments: Methodology, Risk Exposure and Performance. ECGI

Working Paper.

• Nofsinger, J., Varma, A., 2014. Socially Responsible Funds and

Market Crises. Journal of Banking & Finance 48, 180–193.

20 © PPCmetrics AG

Appendix

Survey Results (1)

21 © PPCmetrics AG

Source: gfs-zürich RobecoSAM «Pensionskasse & ESGIntegration» 2014

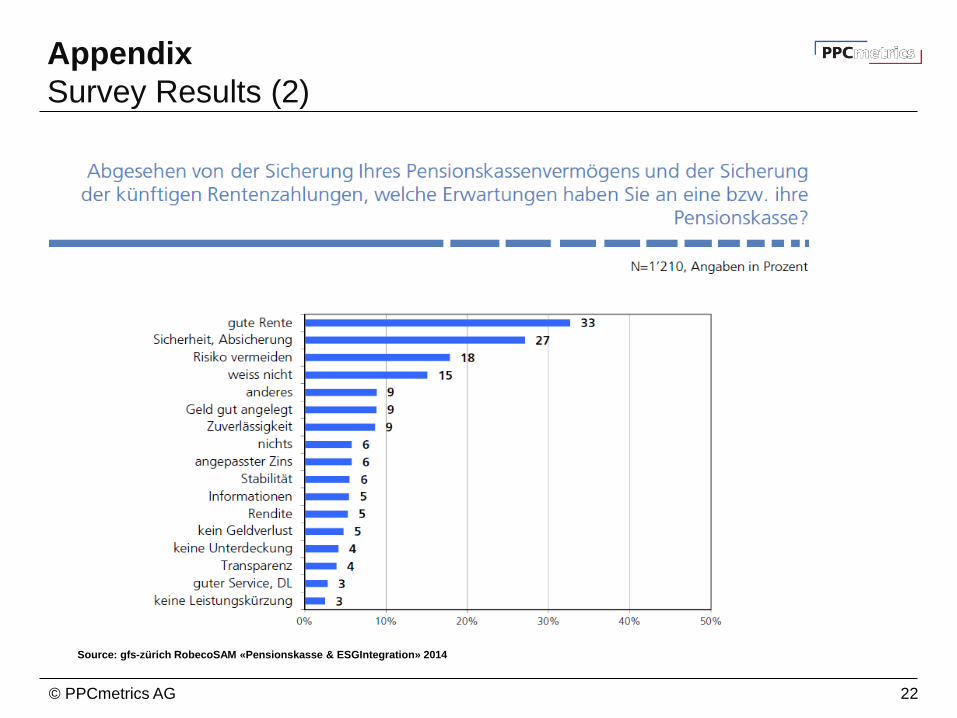

Appendix

Survey Results (2)

22 © PPCmetrics AG

Source: gfs-zürich RobecoSAM «Pensionskasse & ESGIntegration» 2014

Appendix

MSCI World vs. MSCI Tobacco

23 © PPCmetrics AG

0

200

400

600

800

1'000

1'200

07

.2000

01

.2001

07

.2001

01

.2002

07

.2002

01

.2003

07

.2003

01

.2004

07

.2004

01

.2005

07

.2005

01

.2006

07

.2006

01

.2007

07

.2007

01

.20

08

07

.2008

01

.2009

07

.2009

01

.2010

07

.2010

01

.2011

07

.2011

01

.2012

07

.2012

01

.2013

07

.2013

01

.2014

07

.20

14

01

.2015

07

.2015

01

.2016

Diagrammtitel

MSCI World TR

MSCI World Tobacco Index TR

Absolute Return in CHF

Source: Bloomberg, own calculations, since inception of MSCI industry indices

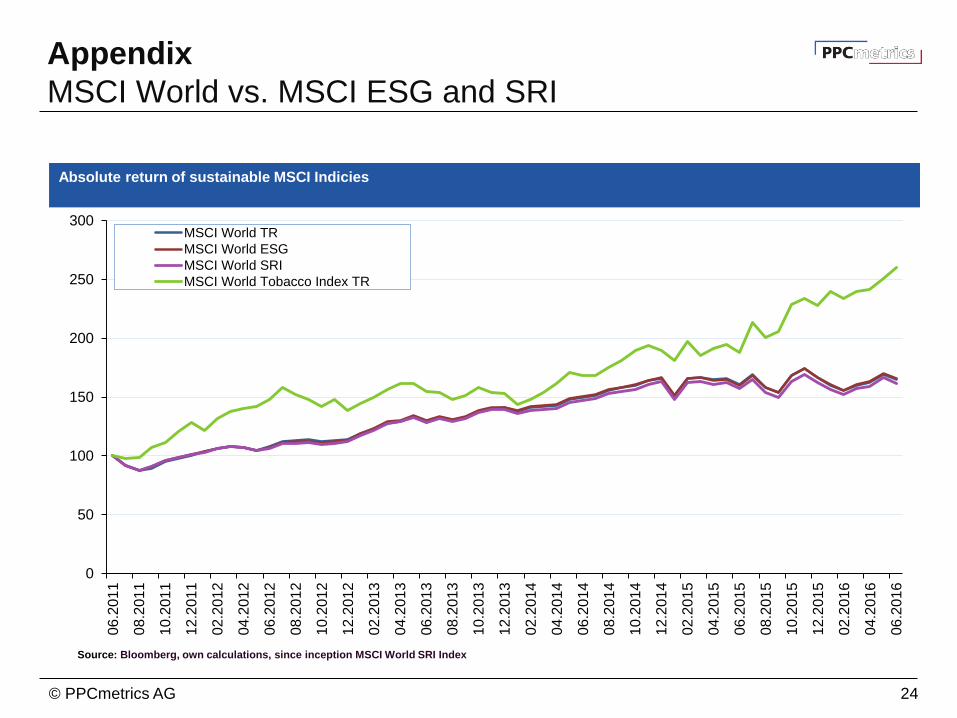

Appendix

MSCI World vs. MSCI ESG and SRI

24 © PPCmetrics AG

Source: Bloomberg, own calculations, since inception MSCI World SRI Index

0

50

100

150

200

250

300

06.2

01

1

08.2

011

10.2

01

1

12.2

01

1

02.2

01

2

04.2

01

2

06.2

01

2

08.2

01

2

10.2

01

2

12.2

01

2

02.2

01

3

04.2

01

3

06.2

01

3

08.2

01

3

10.2

01

3

12.2

01

3

02.2

014

04.2

01

4

06.2

01

4

08.2

01

4

10.2

01

4

12.2

01

4

02.2

01

5

04.2

01

5

06.2

01

5

08.2

01

5

10.2

01

5

12.2

01

5

02.2

01

6

04.2

01

6

06.2

01

6

Diagrammtitel

MSCI World TR

MSCI World ESG

MSCI World SRI

MSCI World Tobacco Index TR

Absolute return of sustainable MSCI Indicies

PPCmetrics (www.ppcmetrics.ch) ist ein führender Schweizer Investment Consultant, Investment Controller, strategischer Anlageberater und Pensionskassenexperte. Unsere Kunden sind institutionelle Investoren

(beispielsweise vom Typ Pensionskasse, Vorsorgeeinrichtung, Personalvorsorgestiftung, Versorgungswerk, Versicherung, Krankenversicherung, Stiftung, NPO und Treasury-Abteilung) und Privatkunden (beispielsweise

Privatanleger, Family Office, Familienstiftung oder UHNWI - Ultra High Net Worth Individuals). Unsere Dienstleistungen umfassen das Investment Consulting und die Anlageberatung sowie die Definition einer

Anlagestrategie (Asset Liability Management - ALM), die Portfolioanalyse, die Asset Allocation, die Entwicklung eines Anlagereglements, die juristische Beratung (Legal Consulting), die Auswahl von Vermögensverwaltern

(Asset Manager Selection), die Durchführung öffentlicher Ausschreibungen, das Investment Controlling, die aktuarielle und versicherungstechnische Beratung und die Tätigkeit als Pensionskassenexperte.

PPCmetrics AG

Badenerstrasse 6

Postfach

CH-8021 Zürich

Telefon +41 44 204 31 11

Telefax +41 44 204 31 10

E-Mail [email protected]

PPCmetrics SA

23, route de St-Cergue

CH-1260 Nyon

Téléphone +41 22 704 03 11

Fax +41 22 704 03 10

E-Mail [email protected]

Website www.ppcmetrics.ch

Social Media

Investment & Actuarial Consulting,

Controlling and Research

Contact

25 © PPCmetrics AG

Videos

© PPCmetrics AG

Publicat-

ions

Conferen

-ces

We publish more than

40 articles on various

topics per year.

Our experts share their

knowledge and opinions

with the public.

Experience our

conferences, which we

organize several times

per year.

Website

PPCmetrics AG

Investment & Actuarial

Consulting, Controlling,

and Research. Read more