20

“Any fool can lend money, but it takes lot of skills to get it back” Presented By-Rahamat Ali Sardar

| Date post: | 04-Apr-2018 |

| Category: |

Documents |

| Upload: | bhavna-arya |

| View: | 226 times |

| Download: | 0 times |

7/30/2019 ppt on rece

http://slidepdf.com/reader/full/ppt-on-rece 1/20

“Any fool can lend money,

but it takes lot of skills to get it back”

Presented By-Rahamat Ali Sardar

7/30/2019 ppt on rece

http://slidepdf.com/reader/full/ppt-on-rece 2/20

INTRODUCTION

WHAT IS RECEIVABLES? Receivables is defined as the debt owed to the firm by customers arising from

Sales of goods and services in the ordinary course of business. When a firm

makes an ordinary sale of goods or services and does not receive payment ,the

firm grants trade credits and creates accounts receivable which could becollected in future. Receivables Management is also called Trade CreditManagement.

WHY DO WE NEED RECEIVABLES? Reach Sales potential

Compete with Competitors Optimize the return on investments on the assets

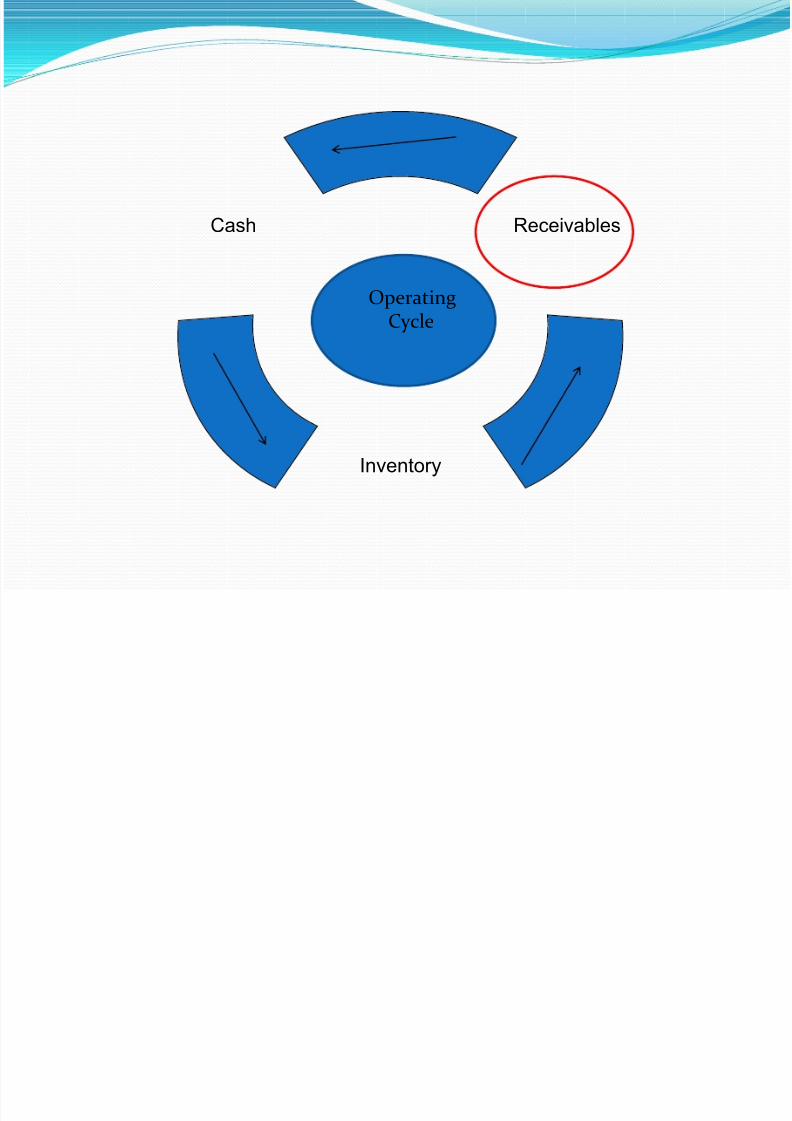

UNDERSTANDING RECEIVABLES As a part of Operating Cycle

A time lag between sales and receivables creates need for Working Capital

7/30/2019 ppt on rece

http://slidepdf.com/reader/full/ppt-on-rece 3/20

7/30/2019 ppt on rece

http://slidepdf.com/reader/full/ppt-on-rece 4/20

OBJECTIVES Achieving growth in sales and profit.

Meeting Competition.

Establish and communicate the credit policies.

Evaluation of customers and setting credit limits.

Ensure prompt and accurate billing.

Maintaining up-to-date records.

Initiate collection procedures on overdue accounts.

7/30/2019 ppt on rece

http://slidepdf.com/reader/full/ppt-on-rece 5/20

COSTS OF MAINTAINING DEBTORS

CAPITAL COST: It is the cost on the use of additional capital to

support credit sales which alternatively could have been employed

elsewhere.

COLLECTION COSTS: Administrative costs incurred in

collecting the accounts receivable. Costs of additional steps to increasethe chances for eventful payment.

DELINQUENCY COSTS: Cost of financing the debtors forextended period, and cost of additional steps to collect over-due debtors.

DEFAULT COSTS: Amounts which are to be written off as Bad-

debts, which cannot be collected in spite of serious efforts.

7/30/2019 ppt on rece

http://slidepdf.com/reader/full/ppt-on-rece 6/20

CREDIT POLICIES

It is the determination of credit statandard and credit analysis.The credit policy of a firm provides the framework

to determine whether or not to extend credit to a customer

and how much credit to extend.The credit policy decision of

a firm has two dimensions.

A)CREDIT STANDARD-It is the minimum requirement for

extending credit to a customer.

B)CREDIT ANALYSIS-This involves obtaining credit information

and evolution of credit applicant.

7/30/2019 ppt on rece

http://slidepdf.com/reader/full/ppt-on-rece 7/20

CREDIT STANDARDSFollowing factors should be considered while deciding whether to relax creditcredit standards or not.

COLLECTION COST-The implications of relaxed credit standards

are more credit,a large credit departments to service accounts receivable andincrease in collection cost while opposite in case of strict credit standards.

AVERAGE COLLECTION PERIOD-The extension of trade

credit to slow paying customers would results in a higher level of accountsreceivable and vice versa.

BAD DEBT EXPENSES-Bad debt can be expected to increase withrelaxation in credit standards and vice versa.

SALES VOLUME-Sales volume is expected to increase as standards are

relaxed,conversely tightening decreases sales.

7/30/2019 ppt on rece

http://slidepdf.com/reader/full/ppt-on-rece 8/20

EFFECT OF RELAXATION OF

STANDARDSITEM DIRECTION OF

CHANGE(Increase=1Decrease =D)

EFFECT ON PROFITS(Positive+ Negative -)

Sales Volume 1(D)+(-)

Average Collection period

1(D)

-(+)

Bad Debts 1(D)-(+)

7/30/2019 ppt on rece

http://slidepdf.com/reader/full/ppt-on-rece 9/20

CREDIT ANALYSISTwo basic steps are involved in the credit investigation Process.

A)OBTAINING CREDIT INFORMATION-The first step incredit analysis is obtaining the information which form the basis for theevaluation of customers.The sources of information may be internal such asthe historical payment pattern of a customers,or may be external such as :

I)FINANCIAL STATEMENTS-The published financial statements such asbalance sheet and profit and loss account.

II)BANK REFERENCES-The firm’s banker collects the necessary information

from the applicant’s Bank.

III)TRADE REFERENCES-Reputed Credit organization are approached aboutthe credit worthiness of proposed customers.

IV)CREDIT BUREAU REPORTS-Credit Bureau reports from organization which specializes in supplying credit information can also be utilized.

7/30/2019 ppt on rece

http://slidepdf.com/reader/full/ppt-on-rece 10/20

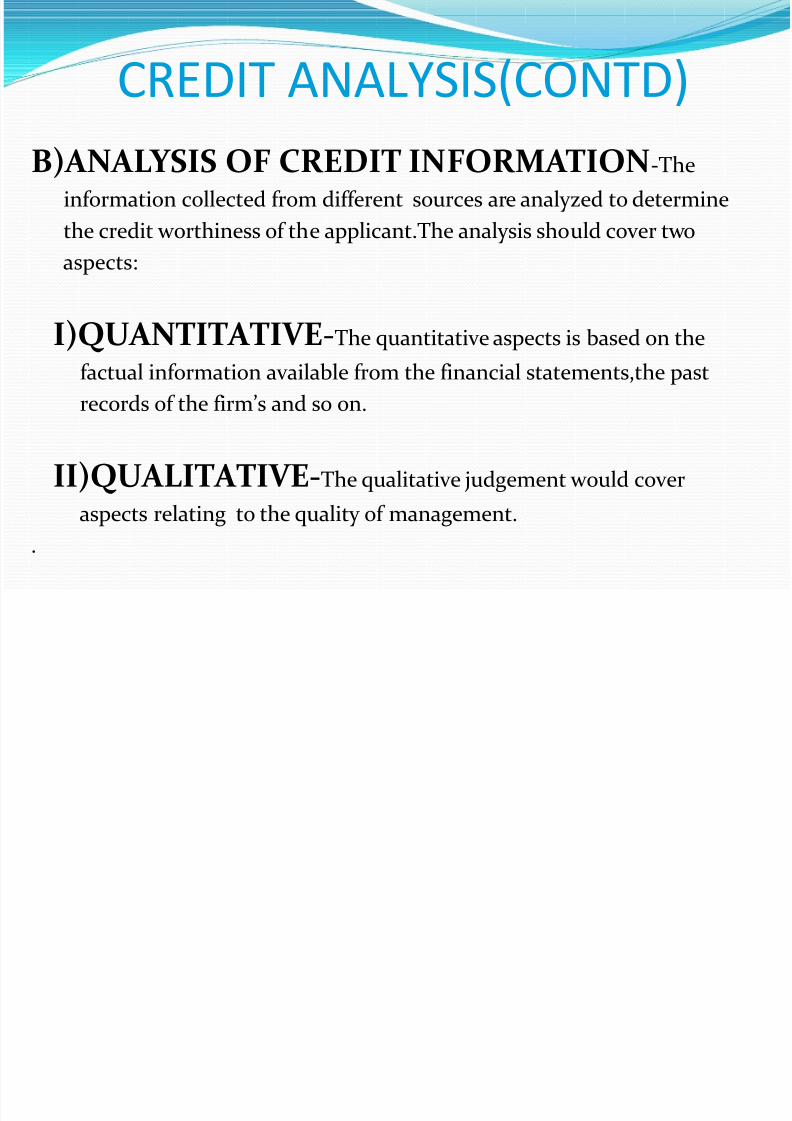

CREDIT ANALYSIS(CONTD)

B)ANALYSIS OF CREDIT INFORMATION-The

information collected from different sources are analyzed to determine

the credit worthiness of the applicant.The analysis should cover two

aspects:

I)QUANTITATIVE-The quantitative aspects is based on the

factual information available from the financial statements,the past

records of the firm’s and so on.

II)QUALITATIVE-The qualitative judgement would cover

aspects relating to the quality of management.

.

7/30/2019 ppt on rece

http://slidepdf.com/reader/full/ppt-on-rece 11/20

STEPS IN CREDIT ANALYSIS“Investing The Customers”

Customers Evaluation-The 5 C’s-

CHARACTER - Reputation, Track Record

C APACITY - Ability to repay( earning capacity)

C APITAL- Financial Position of the co.

COLLATERAL- The type and kind of assets pledged

CONDITIONS- Economic conditions & competitivefactors that may affect the profitability of the customers

7/30/2019 ppt on rece

http://slidepdf.com/reader/full/ppt-on-rece 12/20

FACTORS AFFECTING SIZE OF DEBTORS

LEVEL OF SALES: The most important factors indetermining the volume of Debtors is the level of credit sales. Othersbeing constant ,more credit sales mean more Debtors and vice versa.

CREDIT TERMS: A change in credit terms will have a directeffects on Debtors.When credit terms are relaxed in leads to a nincrease in Debtors balance and vice versa.

COLLECTION POLICY:Collection policy of a firm alsohas some influences on the actual Debtors balance.Due to a relatively lax collection policy,customers do not meet their commitments ontime.

7/30/2019 ppt on rece

http://slidepdf.com/reader/full/ppt-on-rece 13/20

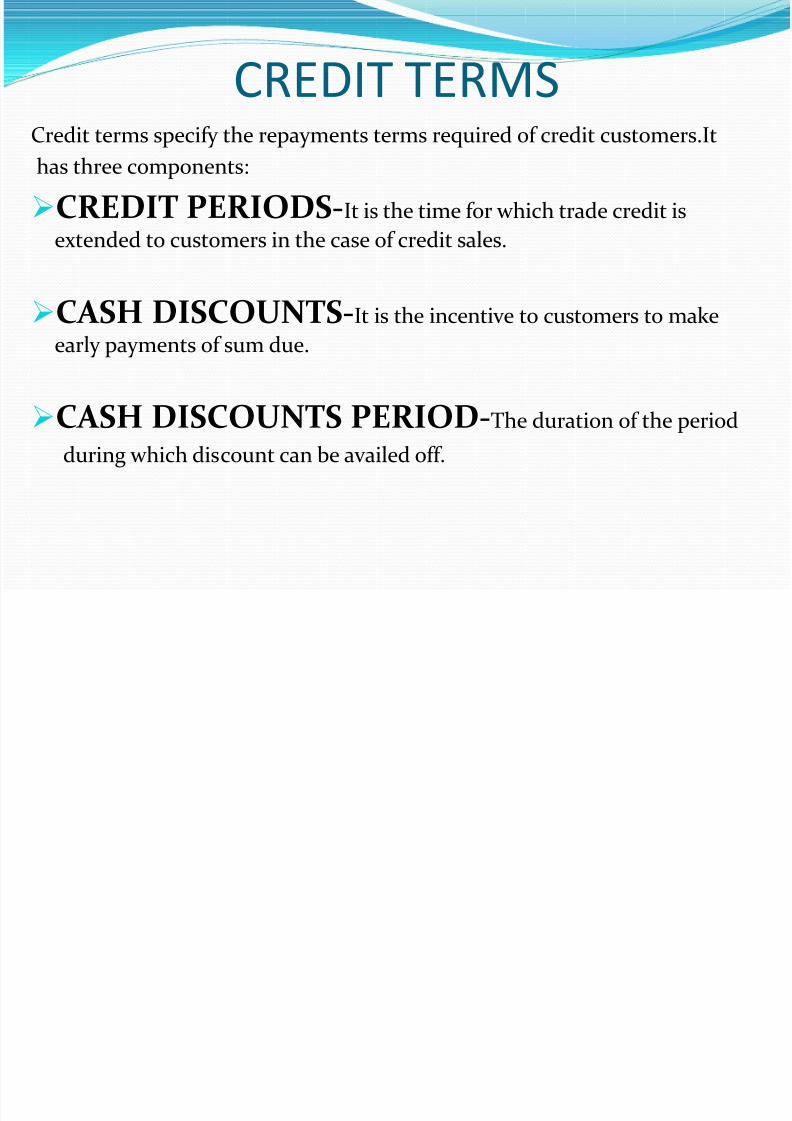

CREDIT TERMSCredit terms specify the repayments terms required of credit customers.Ithas three components:

CREDIT PERIODS-It is the time for which trade credit is

extended to customers in the case of credit sales.

CASH DISCOUNTS-It is the incentive to customers to make

early payments of sum due.

CASH DISCOUNTS PERIOD-The duration of the period

during which discount can be availed off.

7/30/2019 ppt on rece

http://slidepdf.com/reader/full/ppt-on-rece 14/20

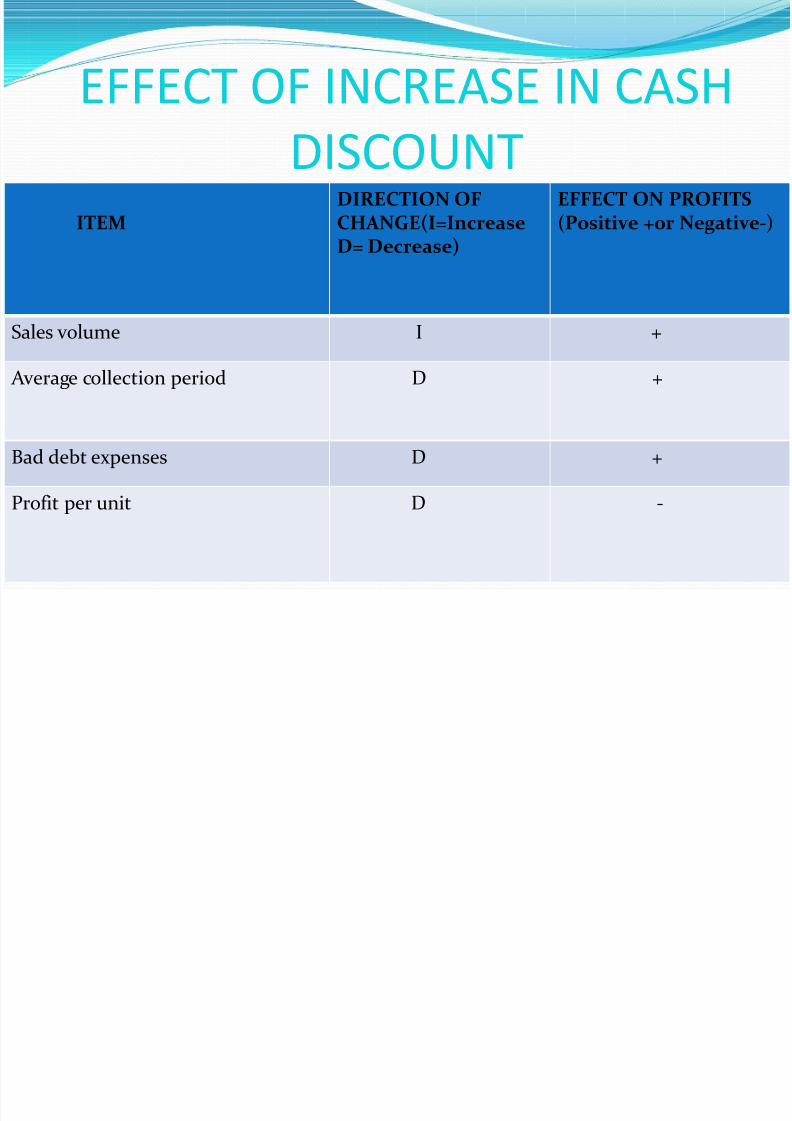

EFFECT OF INCREASE IN CASH

DISCOUNTITEM

DIRECTION OFCHANGE(I=IncreaseD= Decrease)

EFFECT ON PROFITS(Positive +or Negative-)

Sales volume I +

Average collection period D +

Bad debt expenses D +

Profit per unit D -

7/30/2019 ppt on rece

http://slidepdf.com/reader/full/ppt-on-rece 15/20

TYPE OF COLLECTION EFFORTS

Steps usually taken are

Letters, including reminders

Telephone call for personal contact

Personal visit

Help of collection agencies

Legal action

7/30/2019 ppt on rece

http://slidepdf.com/reader/full/ppt-on-rece 16/20

BENEFITS

INCREASED SALES-The impact of liberal trade policy result

in increased in sales volume.

STREAMLINE REVENUE ALLOCATION-To fit

business needs calculations are managed.

ENHANCE PRODUCTIVITY-The decrease in administrative

cost enhances productivity.

HELPS IMPROVE CUSTOMER SATISFACTION-Enhances service level and increase retention with customizedinformation.

7/30/2019 ppt on rece

http://slidepdf.com/reader/full/ppt-on-rece 17/20

PROFORMAType A-if fixed Cost Is Given

Credit Policy Present Policy Option 1 Option 2 Option 3

Credit Period (days/ weeks/months) xx xx xx xxParticulars Rs. Rs. Rs. Rs.

Sales xxxx xxxx xxxx xxxx

Less: Variable Cost xx xx xx xx

Contribution xxx xxx xxx xxx

Less: Fixed Cost xx xx xx xx

Profit [Benefits (A)] xxx xxx xxx xxx

Total Cost= Variable Cost +Fixed Cost

Average Investment in Receivables

(Based on Total Costs)

xxx xxx xxx xxx

Costs of Extending Credit:

1) ____ % Opportunity Cost of Capital(Calculated on Avg. Invst. in Receivables)

xx xx xx xx

2) Bad debts as % of Sales xx xx xx xx

3) Credit Collection and Admin costs xx xx xx xx

Total Costs [B] xxxx xxxx xxxx xxxx

Net Benefits [A-B] xxx xxx xxx xxx

Incremental Net Benefits --- xx xx xx

7/30/2019 ppt on rece

http://slidepdf.com/reader/full/ppt-on-rece 18/20

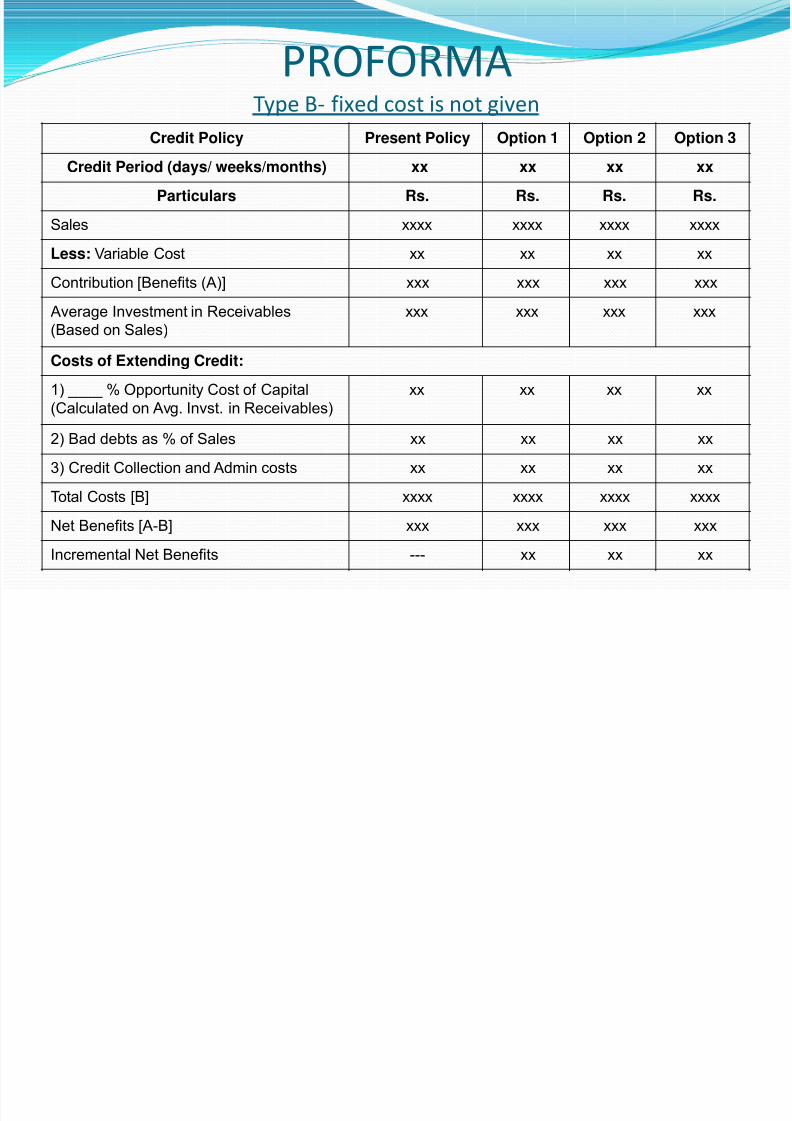

PROFORMAType B- fixed cost is not given

Credit Policy Present Policy Option 1 Option 2 Option 3

Credit Period (days/ weeks/months) xx xx xx xx

Particulars Rs. Rs. Rs. Rs.

Sales xxxx xxxx xxxx xxxx

Less: Variable Cost xx xx xx xx

Contribution [Benefits (A)] xxx xxx xxx xxx

Average Investment in Receivables

(Based on Sales)

xxx xxx xxx xxx

Costs of Extending Credit:

1) ____ % Opportunity Cost of Capital

(Calculated on Avg. Invst. in Receivables)

xx xx xx xx

2) Bad debts as % of Sales xx xx xx xx

3) Credit Collection and Admin costs xx xx xx xx

Total Costs [B] xxxx xxxx xxxx xxxx

Net Benefits [A-B] xxx xxx xxx xxx

Incremental Net Benefits --- xx xx xx

7/30/2019 ppt on rece

http://slidepdf.com/reader/full/ppt-on-rece 19/20

CONCLUSION

The framework of analysis of all decisions areain receivables management is to secure a

trade-off between the costs and benefits off the measurable effects on the sales volume,capital costs due to change in investment in

debtors ,collection costs, bad debts and so on.The firm should select the alternative whichhas potentials of more benefits than the costs.

7/30/2019 ppt on rece

http://slidepdf.com/reader/full/ppt-on-rece 20/20

THANK YOU

![Jeffery Deaver [Lincoln Rhyme] 7 - Luna Rece [v.1.0]](https://static.documents.pub/doc/80x56/577cc7041a28aba7119fc7c5/jeffery-deaver-lincoln-rhyme-7-luna-rece-v10.jpg)