CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 246/278 CFA, CMT, CAIA, FRM, EFA, CFTe

PPRRAACCTTIICCEE EEXXAAMM VVIIIIII..

Question Topic Point Range

Question 1 MTA Code of Ethics 12 points

Question 2 Behavioral Finance 20 – 40 points

Question 3 Intermarket Analysis 20 – 40 points

Question 4 Strategy and Techniques 20 – 40 points

Question 5 Candlestick Analysis 20 – 40 points

Question 6 Elliott Wave 20 – 40 points

Question 7 Point and Figure 20 – 40 points

Question 8 Risk Management 20 – 40 points

Question 9 System Development 20 – 40 points

240 points

Questions 8 and 9 (Risk Management and System Development) refer to CMT level II reading assignments.

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 247/278 CFA, CMT, CAIA, FRM, EFA, CFTe

Question 1. MTA Code of Ethics. 12 points.

1A. During a recent interview, Stuart Diamond, CMT, was asked to give his opinion on the stock market, his

recent market commentary and several stock picks. The following sentence comes from this interview.

”Recently we started a marketing campaign to increase our client base. As we have not increased the

number of employees, we have received some complaints from current clients. This will be temporary and

the quality of our service will be reestablished as soon as possible.”

Based on this information, which of the following statements is most accurate? (2 points).

A. Stuart has not violated any of the Ethics Standards.

B. Stuart has violated Ethics Standard 1 by behaving unprofessionally.

C. Stuart has violated Ethics Standard 2 by making misleading statements.

D. Stuart has violated Ethics Standards 7 because they have received complaints from current clients.

1B. During a recent interview, Stuart Diamond, CMT, was asked to give his opinion on the stock market, his

recent market commentary and several stock picks. The following sentence comes from this interview. “As

we have also less time to develop our technical weekly report, we have subscribed to some third-party

research, and we are repackaging this research with our logo to fill the recommendations in our weekly

report.”

Based on this information, which of the following statements is most accurate? (2 points).

A. Stuart has not violated any of the Ethics Standards.

B. Stuart has violated Ethics Standard 1 by behaving unprofessionally.

C. Stuart has violated Ethics Standard 2 by making misleading statements.

D. Stuart has violated Ethics Standards 8 by repackaging the research with the company logo as if the

research was proprietary.

1C. During a recent interview, Stuart Diamond, CMT, was asked to give his opinion on the stock market, his

recent market commentary and several stock picks. The following sentence comes from this interview:

“Because we base all our research in technical analysis, we have little problems with basing our

recommendations on material non-public information. However, we hired an expert on this area to study

the financial regulations of all countries in which we are promoting our services.”

Based on this information, which of the following statements is most accurate? (2 points).

A. Stuart has not violated any of the Ethics Standards.

B. Stuart has violated Ethics Standard 1 by behaving unprofessionally.

C. Stuart has violated Ethics Standard 2 by making misleading statements.

D. Stuart has violated Ethics Standards 5 regarding insider trading.

1D. During a recent interview, Stuart Diamond, CMT, was asked to give his opinion on the stock market, his

recent market commentary and several stock picks. The following sentence comes from this interview: “We

recently introduced a financial education plan for our analysts. Nowadays, technical analysts think that just

after reading two books they can beat the market. Yesterday I was invited to a conference by technical

analyst John Triangle, and it was completely useless, the whole conference was garbage.”

Based on this information, which of the following statements is most accurate? (2 points).

A. Stuart has not violated any of the Ethics Standards.

B. Stuart has violated Ethics Standard 1 by discrediting the analytical work of others.

C. Stuart has violated Ethics Standard 2 by making misleading statements.

D. Stuart has violated Ethics Standards 5 regarding insider trading.

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 248/278 CFA, CMT, CAIA, FRM, EFA, CFTe

1E. During a recent interview, Stuart Diamond, CMT, was asked to give his opinion on the stock market, his

recent market commentary and several stock picks. The following sentence comes from this interview:

“However, after this technical analyst, a trading system developer exposed a simple strategy that looked

quite interesting, I programmed it when I came back to the office and the backtesting was quite brilliant, I

changed the parameters of the model and fully documented the whole procedure and rationale. This is now

one of our star strategies.”

Based on this information, which of the following statements is most accurate? (2 points).

A. Stuart has not violated any of the Ethics Standards.

B. Stuart has violated Ethics Standard 1 by discrediting the analytical work of others.

C. Stuart has violated Ethics Standard 8 by copying the strategy and included as a proprietary strategy.

D. Stuart has violated Ethics Standards 5 regarding insider trading.

1F. Johnathan Dos Santos, CMT, works as an analyst for a big management and advisory company. Dos Santos

issued a research report with an initial buy recommendation on Panton Colors. The report includes an

analysis using some very new and controversial methods of technical analysis, along with complete

documentation as to the procedure and rationale. Ten minutes after emailing the report to all his clients,

Johnathan starts to buy Panton Colors stock for his premium clients.

Based on this information, which of the following statements is most accurate? (2 points).

A. Dos Santos committed no violation.

B. Dos Santos violated Ethics Standard 7 regarding the trading conducted in his premium client’s accounts.

C. Dos Santos violated Ethics Standard 3 regarding the technical methodologies employed.

D. Dos Santos violated Ethics Standards 3 and 7.

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 249/278 CFA, CMT, CAIA, FRM, EFA, CFTe

Question 2. Behavioral Finance. 20 - 40 points.

2A. Psychologists have spent many years documenting the fact that group decisions are among the worst

decisions ever made, effectively endorsing the view that committees are groups of people who keep

minutes but waste hours. The key reason for this appears to that when we come together as a group we not

only have to deal with our own biases, but also with everyone else’s biases. As with all biases the solutions

are never easy to implement. However, three possible routes to reducing group biases can be applied.

Determine and explain these routes.

2B. Determine whether Behavioral Finance in general and James Montier in particular, consider CAPM as a

valid financial model for practitioners. Explain your answer.

2C. Despite the wide range of assets that have witnessed bouts of irrational exuberance (tulips, coins, bonds,

cotton, wheat, land, equities, etc), bubbles seem to follow a similar pattern. Name the five phases of an

asset price bubble following the Kindleberger/Minsky model, and explain the phase in which the boom is

further exacerbated by monetary expansion and/or credit creation.

2D. Not all bubbles are the same. James Montier states four major types. Name them and explain the one

characterized by the following reasoning: “new era seems invincible and is supported by rapid expansion of

the economy and a seemingly inexorable rise in stock prices. This process leads to feelings of

over-optimism and overconfidence."

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 250/278 CFA, CMT, CAIA, FRM, EFA, CFTe

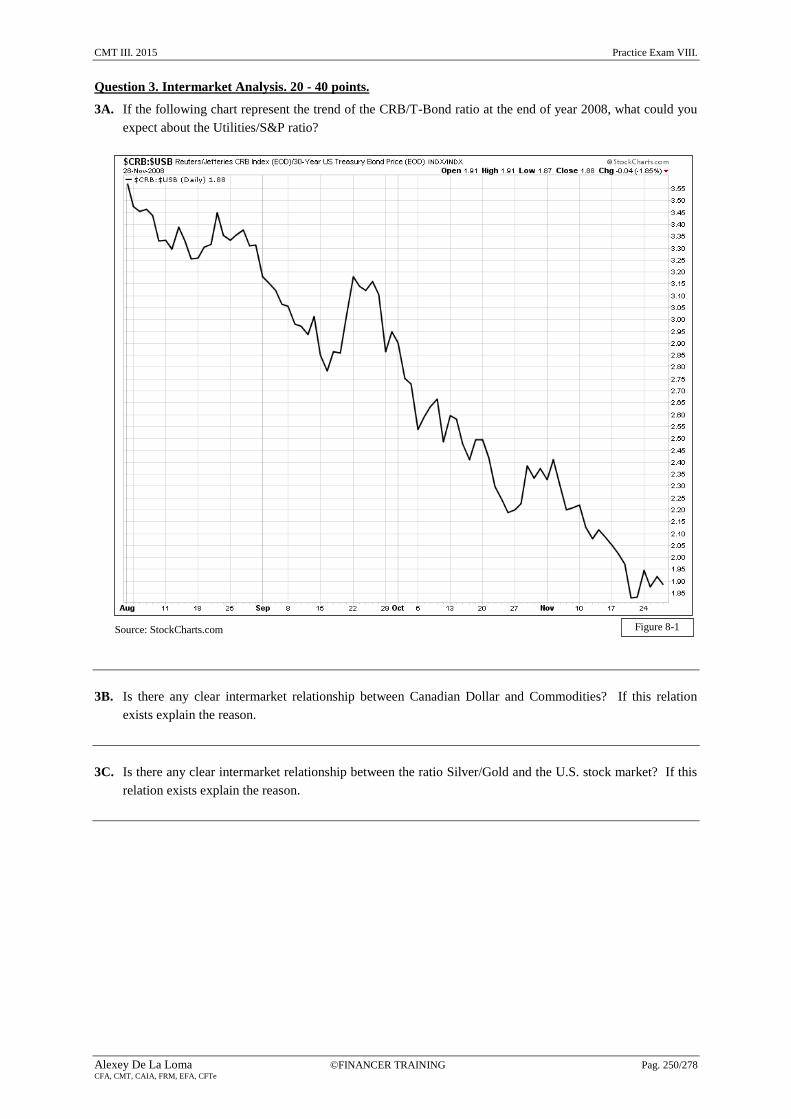

Question 3. Intermarket Analysis. 20 - 40 points.

3A. If the following chart represent the trend of the CRB/T-Bond ratio at the end of year 2008, what could you

expect about the Utilities/S&P ratio?

3B. Is there any clear intermarket relationship between Canadian Dollar and Commodities? If this relation

exists explain the reason.

3C. Is there any clear intermarket relationship between the ratio Silver/Gold and the U.S. stock market? If this

relation exists explain the reason.

Source: StockCharts.com Figure 8-1

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 251/278 CFA, CMT, CAIA, FRM, EFA, CFTe

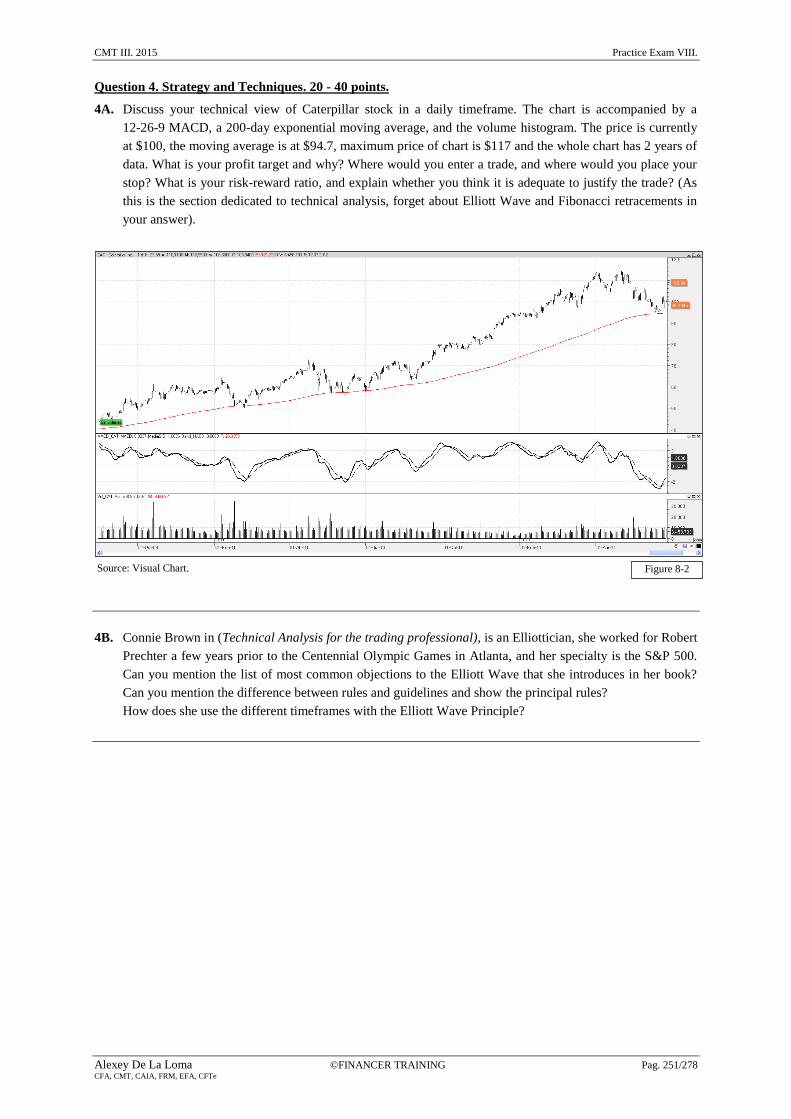

Question 4. Strategy and Techniques. 20 - 40 points.

4A. Discuss your technical view of Caterpillar stock in a daily timeframe. The chart is accompanied by a

12-26-9 MACD, a 200-day exponential moving average, and the volume histogram. The price is currently

at $100, the moving average is at $94.7, maximum price of chart is $117 and the whole chart has 2 years of

data. What is your profit target and why? Where would you enter a trade, and where would you place your

stop? What is your risk-reward ratio, and explain whether you think it is adequate to justify the trade? (As

this is the section dedicated to technical analysis, forget about Elliott Wave and Fibonacci retracements in

your answer).

4B. Connie Brown in (Technical Analysis for the trading professional), is an Elliottician, she worked for Robert

Prechter a few years prior to the Centennial Olympic Games in Atlanta, and her specialty is the S&P 500.

Can you mention the list of most common objections to the Elliott Wave that she introduces in her book?

Can you mention the difference between rules and guidelines and show the principal rules?

How does she use the different timeframes with the Elliott Wave Principle?

Figure 8-2 Source: Visual Chart.

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 252/278 CFA, CMT, CAIA, FRM, EFA, CFTe

Question 5. Candlestick. 20 - 40 points.

5A. Identify and explain the significance of the following candlestick pattern within the oval.

5B. Identify and explain the significance of the following candlestick pattern within the oval.

Figure 8-3

Figure 8-4 Source: Visual Chart.

Source: Visual Chart.

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 253/278 CFA, CMT, CAIA, FRM, EFA, CFTe

5C. Identify and explain the significance of the following candlestick pattern within the oval.

5D. Identify and explain the significance of the following candlestick pattern within the oval.

Figure 8-5

Figure 8-6

Source: Visual Chart.

Source: Visual Chart.

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 254/278 CFA, CMT, CAIA, FRM, EFA, CFTe

5E. Identify and explain the significance of the following candlestick pattern within the oval.

5F. Identify the four candlestick patterns; explain their significance and classify them from the more relevant to

the less relevant.

Figure 8-7

Figure 8-8 Figure 8-9 Figure 8-10 Figure 8-11

Source: Visual Chart.

Source: Visual Chart.

Source: Visual Chart. Source: Visual Chart. Source: Visual Chart.

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 255/278 CFA, CMT, CAIA, FRM, EFA, CFTe

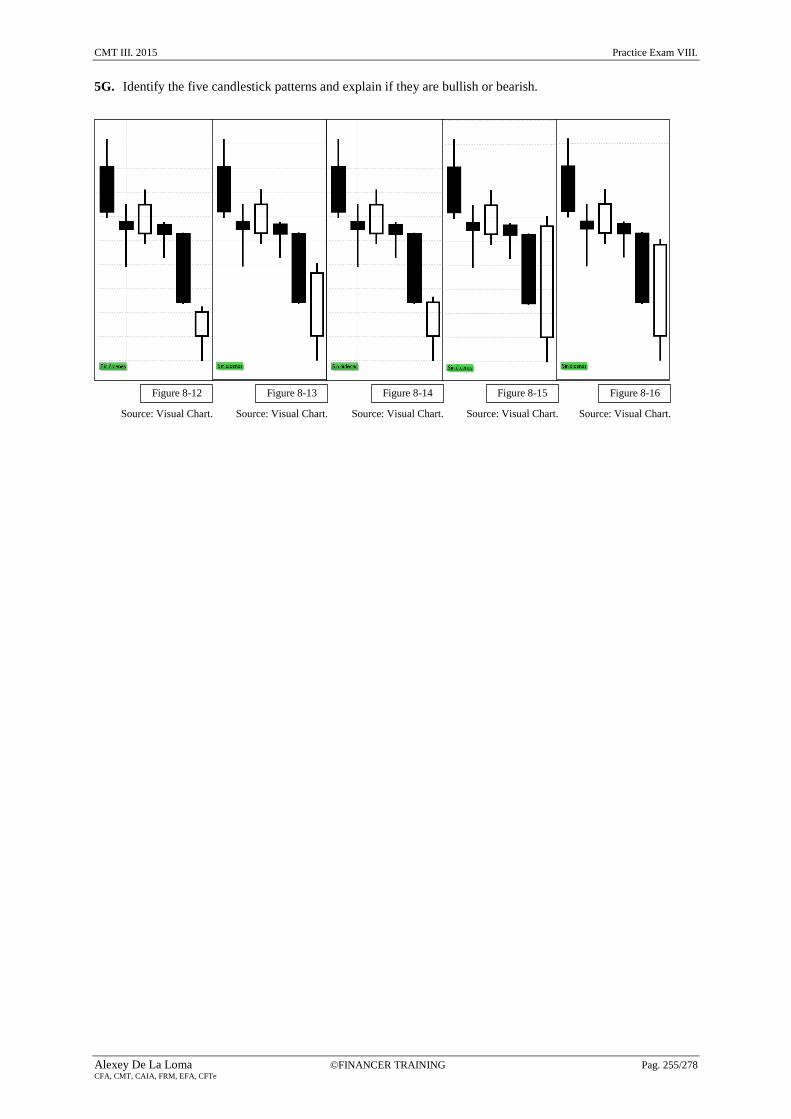

5G. Identify the five candlestick patterns and explain if they are bullish or bearish.

Figure 8-16 Figure 8-12 Figure 8-13 Figure 8-14 Figure 8-15

Source: Visual Chart. Source: Visual Chart. Source: Visual Chart. Source: Visual Chart. Source: Visual Chart.

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 256/278 CFA, CMT, CAIA, FRM, EFA, CFTe

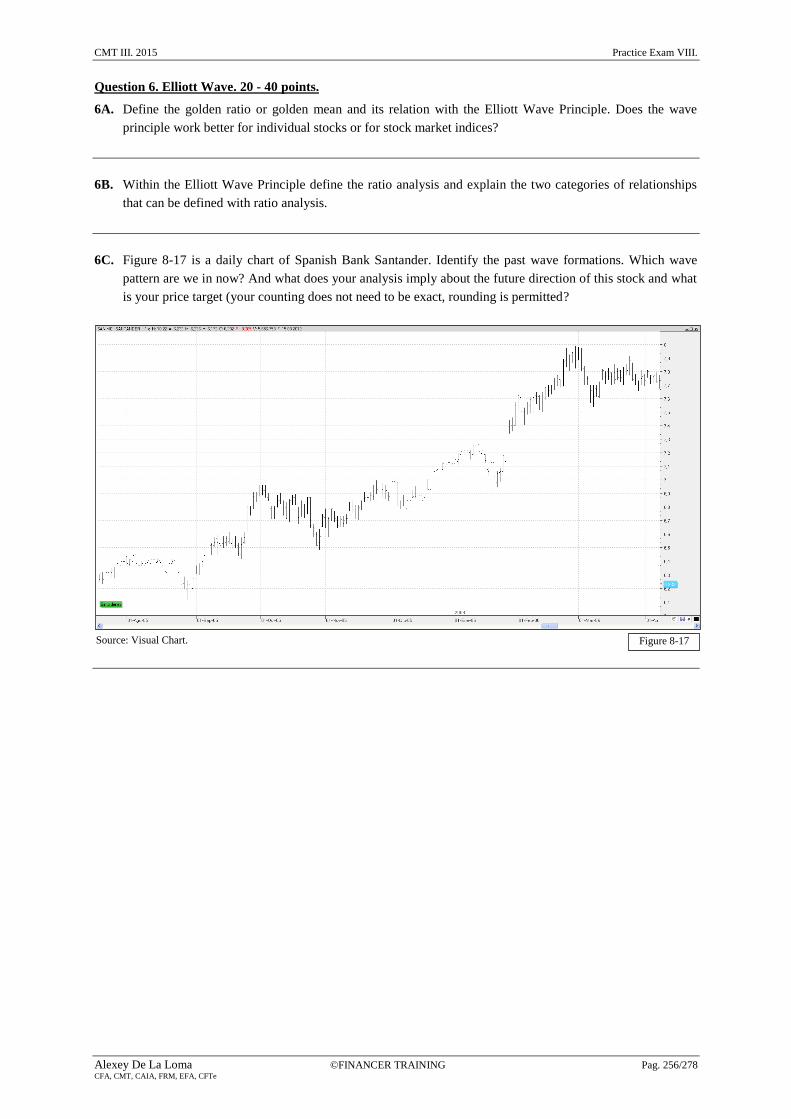

Question 6. Elliott Wave. 20 - 40 points.

6A. Define the golden ratio or golden mean and its relation with the Elliott Wave Principle. Does the wave

principle work better for individual stocks or for stock market indices?

6B. Within the Elliott Wave Principle define the ratio analysis and explain the two categories of relationships

that can be defined with ratio analysis.

6C. Figure 8-17 is a daily chart of Spanish Bank Santander. Identify the past wave formations. Which wave

pattern are we in now? And what does your analysis imply about the future direction of this stock and what

is your price target (your counting does not need to be exact, rounding is permitted?

Figure 8-17 Source: Visual Chart.

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 257/278 CFA, CMT, CAIA, FRM, EFA, CFTe

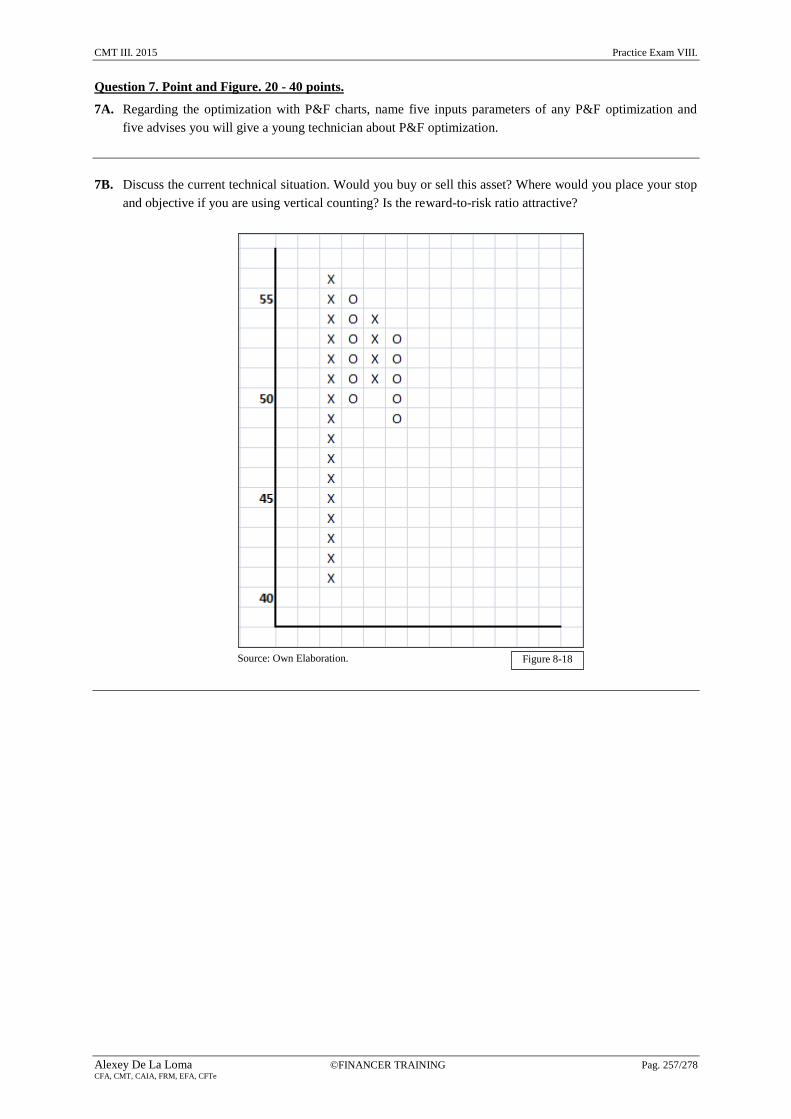

Question 7. Point and Figure. 20 - 40 points.

7A. Regarding the optimization with P&F charts, name five inputs parameters of any P&F optimization and

five advises you will give a young technician about P&F optimization.

7B. Discuss the current technical situation. Would you buy or sell this asset? Where would you place your stop

and objective if you are using vertical counting? Is the reward-to-risk ratio attractive?

Figure 8-18 Source: Own Elaboration.

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 258/278 CFA, CMT, CAIA, FRM, EFA, CFTe

Question 8. Risk Management. 20 - 40 points.

8A. The Value at Risk (VaR) is one the most common ways of measuring risk. Explain this concept and

illustrate the VaR equation for two assets as it appears in the book of Perry Kaufman.

8B. If a company holds $100 millions in asset 1, and another $100 millions in asset 2. The daily standard

deviation of returns of assets 1 and 2 are, 0.565% and 0.605%. Using 1.65 standard deviations to represent

the 95% confidence levels, and making the assumption that r/σ is normally distributed. In this example the

cross correlation of the returns of the two markets is –0.27. Determine the VaR of both assets

independently and combined, and determine if the combined value is higher or lower than the sum of both

individual VaRs.

8C. The Ulcer Index is introduced by Perry Kaufman as a management risk measure. Illustrate this concept and

explain the equation of this measure.

8D. Illustrate the equation of the Sharpe Ratio and determine graphically why this ratio cannot distinguish

between

Consecutive small losses and alternating small losses.

Consecutive small losses and large surges of profits.

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 259/278 CFA, CMT, CAIA, FRM, EFA, CFTe

Question 9. System Development. 20 - 40 points.

9A. According to David Aronson (Evidence-Based Technical Analysis) there are three approaches to reduce the

risk of having all expected returns equal to zero or even less when developing a trading system. All three

approaches try to deal with the data-mining bias. One of these approaches is known as “out-of-sample

testing”. Explain how this approach works.

9B. According to David Aronson (Evidence-Based Technical Analysis) there are three approaches to reduce the

risk of having all expected returns equal to zero or even less when developing a trading system. All three

approaches try to deal with the data-mining bias. One of these approaches is known as “walk-forward

testing”. Explain how this approach works.

9C. Trend-following systems are based on taking positions in the direction of the trend. They are based on

taking a long position when prices are high, in order to close that position even higher, or taking a short

position when prices are low, in order to sell that position even lower. Trend-following do not attempt to

catch peaks and valleys as counter-trend system do. Because, we need to be sure a trend has started before

taking a position, they send lagging signals and suffer in trading range markets. According to Charles

Kirkpatrick, there are two types of trend-following systems. Name them and explain their characteristics.

9D. Define the concept and state the equations for the next backtesting measures: net profit, profit factor, payoff

ratio, and the recovery ratio.

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 260/278 CFA, CMT, CAIA, FRM, EFA, CFTe

Answer to Question 1. MTA Code of Ethics. 12 points.

1A. During a recent interview, Stuart Diamond, CMT, was asked to give his opinion on the stock market,

his recent market commentary and several stock picks. The following sentence comes from this

interview. ”Recently we started a marketing campaign to increase our client base. As we have not

increased the number of employees, we have received some complaints from current clients. This will

be temporary and the quality of our service will be reestablished as soon as possible.”

Based on this information, which of the following statements is most accurate? (2 points)

B. Stuart has violated Ethics Standard 1 by behaving unprofessionally.

1B. During a recent interview, Stuart Diamond, CMT, was asked to give his opinion on the stock market,

his recent market commentary and several stock picks. The following sentence comes from this

interview. “As we have also less time to develop our technical weekly report, we have subscribed to

some third-party research, and we are repackaging this research with our logo to fill the

recommendations in our weekly report.”

Based on this information, which of the following statements is most accurate? (2 points)

D. Stuart has violated Ethics Standards 8 by repackaging the research with the company logo as if the

research was proprietary.

1C. During a recent interview, Stuart Diamond, CMT, was asked to give his opinion on the stock market,

his recent market commentary and several stock picks. The following sentence comes from this

interview: “Because we base all our research in technical analysis, we have little problems with

basing our recommendations on material non-public information. However, we hired an expert on

this area to study the financial regulations of all countries in which we are promoting our services.”

Based on this information, which of the following statements is most accurate? (2 points)

A. Stuart has not violated any of the Ethics Standards.

1D. During a recent interview, Stuart Diamond, CMT, was asked to give his opinion on the stock market,

his recent market commentary and several stock picks. The following sentence comes from this

interview: “We recently introduced a financial education plan for our analysts. Nowadays, technical

analysts think that just after reading two books they can beat the market. Yesterday I was invited to

a conference by technical analyst John Triangle, and it was completely useless, the whole conference

was garbage.”

Based on this information, which of the following statements is most accurate? (2 points)

B. Stuart has violated Ethics Standard 1 by discrediting the analytical work of others.

1E. During a recent interview, Stuart Diamond, CMT, was asked to give his opinion on the stock market,

his recent market commentary and several stock picks. The following sentence comes from this

interview: “However, after this technical analyst, a trading system developer exposed a simple

strategy that looked quite interesting, I programmed it when I came back to the office and the

backtesting was quite brilliant, I changed the parameters of the model and fully documented the

whole procedure and rationale. This is now one of our star strategies.”

Based on this information, which of the following statements is most accurate? (2 points)

C. Stuart has violated Ethics Standard 8 by copying the strategy and included as a proprietary strategy.

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 261/278 CFA, CMT, CAIA, FRM, EFA, CFTe

1F. Johnathan Dos Santos, CMT, works as an analyst for a big management and advisory company. Dos

Santos issued a research report with an initial buy recommendation on Panton Colors. The report

includes an analysis using some very new and controversial methods of technical analysis, along with

complete documentation as to the procedure and rationale. Ten minutes after emailing the report to

all his clients, Johnathan starts to buy Panton Colors stock for his premium clients.

Based on this information, which of the following statements is most accurate? (2 points).

C. Dos Santos violated Ethics Standard 3 regarding the technical methodologies employed.

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 262/278 CFA, CMT, CAIA, FRM, EFA, CFTe

Answer to Question 2. Behavioral Finance. 20 - 40 points.

2A. Psychologists have spent many years documenting the fact that group decisions are among the worst

decisions ever made, effectively endorsing the view that committees are groups of people who keep

minutes but waste hours. The key reason for this appears to that when we come together as a group

we not only have to deal with our own biases, but also with everyone else’s biases. As with all biases

the solutions are never easy to implement. However, three possible routes to reducing group biases

can be applied. Determine and explain these routes.

Secret Ballots.

The use of secret ballots reduces the risk of group members coming under social pressure. So perhaps

before the meeting starts members should write down their views and their preferences for asset

allocation, then count the votes, and debate the outcome if it is really necessary – bearing in mind the

dangers inherent in this process.

Devil’s Advocates.

Appointing a devil’s advocate may help. However, all too often the person selected may not truly

believe the role he is asked to play, and hence does not really try too hard to prevent the group reaching

its consensus decision. Selecting prickly disagreeable individuals with a strong contrarian view and the

ability and desire to argue on almost anything would be perfect.

Respect for other group members.

When the group members are acknowledged to be experts in their field, and hence disparate viewpoints

are easier to deal with and unshared information may be easier to uncover. However, all too often

people tend to believe that they know best on almost every subject and hence tend not to display respect

for the views of others.

2B. Determine whether Behavioral Finance in general and James Montier in particular, consider CAPM

as a valid financial model for practitioners. Explain your answer.

Over the long run there has been essentially no relationship between beta and return. The evidence is clear:

CAPM doesn’t work, and if we are asking why? The answer is clearly understood when you see the

incredible and super restrictive assumptions:

1. No transaction costs (no commissions, no bid-ask spread).

2. Investors can take any position (long or short) in any stock in any size without affecting the market

price.

3. No taxes (so investors are indifferent between dividends and capital gains).

4. Investors are risk averse.

5. Investors share a common time horizon.

6. Investors view stocks only in mean-variance space (so they all use the Markowitz Optimization model).

7. Investors control risk through diversification.

8. All assets, including human capital, can be bought and sold freely in the market.

9. Investors can lend and borrow at the risk-free rate (RFR).

2C. Despite the wide range of assets that have witnessed bouts of irrational exuberance (tulips, coins,

bonds, cotton, wheat, land, equities, etc), bubbles seem to follow a similar pattern. Name the five

phases of an asset price bubble following the Kindleberger/Minsky model, and explain the phase in

which the boom is further exacerbated by monetary expansion and/or credit creation.

Displacement.

Credit creation.

Just as fire can’t grow without oxygen, so a boom needs liquidity to feed on. The boom is then further

exacerbated by monetary expansion and/or credit creation. Effectively the model holds money/credit as

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 263/278 CFA, CMT, CAIA, FRM, EFA, CFTe

endogenous to the system, such that for any given banking system, monetary means of payment may be

expanded not only within the existing system of banks, but also by the formation of new banks, the

developments of new credit instruments and the expansion of personal credit outside the banking

system.

Monetary and credit creation in the US high tech bubble were largely the result of overly

accommodative monetary policy on the part of the Fed in 1998, resulting in a massive liquidity surge.

The prominent role that investment played in the cite US bubble is evident looking at the investment as

a percentage of GDP; this percentage soared from around the 14% in the late 1980s to nearly 19% at the

peak in 2000.

Euphoria.

Critical stage / financial distress.

Revulsion.

2D. Not all bubbles are the same. James Montier states four major types. Name them and explain the one

characterized by the following reasoning: “new era seems invincible and is supported by rapid

expansion of the economy and a seemingly inexorable rise in stock prices. This process leads to

feelings of over-optimism and overconfidence."

Rational/Near Rational Bubbles.

Intrinsic Bubbles.

Fad Bubbles.

It is the psychology of the euphoria stage that is of relevance to us in the present context. The euphoria

stage might, for example, be characterized by a general belief in the “new era”. Groupthink is an

important contributor in such environments. People come under immense pressure to conform to the

majority’s view, frequently suppressing their own views in the process.

The “new era” seemed invincible and was supported by rapid expansion of the economy and a

seemingly inexorable rise in stock prices. This process leads to feelings of overoptimism and

overconfidence. These two traits are a potent combination leading people to overestimate returns,

understate the risk, and be far too sure about their knowledge and ability to control the situation.

Informational Bubbles.

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 264/278 CFA, CMT, CAIA, FRM, EFA, CFTe

Answer to question 3. Intermarket Analysis. 20 - 40 points.

3A. If the following chart represent the trend of the CRB/T-Bond ratio at the end of year 2008, what

could you expect about the Utilities/S&P ratio?

Usually, this relationship is negative. When the CRB/Bond ratio is rising, investors favor economically

sensitive stock groups that benefit from a stronger economy. A falling CRB/Bond ratio favors more

defensive stocks groups like consumer staples and utilities. That makes the CRB/Bond ratio a useful

indicator for sector rotation purposes.

3B. Is there any clear intermarket relationship between Canadian Dollar and Commodities? If this

relation exists explain the reason.

The direction of the Canadian Dollar (CAD) has important implications for the Canadian and U.S. stock

markets, as well as commodities. Canadian stocks have a close historical correlation to U.S. stocks. There

is also a close historic correlation between the CAD and the Canadian stocks, and both are closely tied to

fortunes of commodity markets. Canada is one of the world’s biggest exporters of natural resources.

Canadian companies that produce energy and basic materials make up half of the Toronto Stock Index. The

three markets, therefore, are highly correlated.

3C. Is there any clear intermarket relationship between the ratio Silver/Gold and the U.S. stock market?

If this relation exists explain the reason.

Source: StockCharts.com Figure 8-1

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 265/278 CFA, CMT, CAIA, FRM, EFA, CFTe

Although silver is considered to be a precious metal, it is also an industrial metal. It is the industrial role

that gives it some value in helping to measure economic trends. Generally speaking, a rising silver price

implies economic strength. Using the same rationale that compares the price of copper to gold, the direction

of the silver/gold ratio can also be employed as a useful stock market indicator. The relation has a positive

correlation coefficient.

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 266/278 CFA, CMT, CAIA, FRM, EFA, CFTe

Answer to question 4. Strategy and Techniques. 20 - 40 points.

4A. Discuss your technical view of Caterpillar stock in a daily timeframe. The chart is accompanied by a

12-26-9 MACD, a 200-day exponential moving average, and the volume histogram. The price is

currently at $100, the moving average is at $94.7, maximum price of chart is $117 and the whole

chart has 2 years of data. What is your profit target and why? Where would you enter a trade, and

where would you place your stop? What is your risk-reward ratio, and explain whether you think it

is adequate to justify the trade? (As this is the section dedicated to technical analysis, forget about

Elliott Wave and Fibonacci retracements in your answer).

This is a long-term bull trend of a stock (stock market asset). The moving average of parameter 200 is

working as a dynamic support with three contact points and the price has already touched again this

moving average so the bull trend is still in place. The last months show a small bear trend that is

represented by an oversold level in the MACD oscillator. However this oscillator is showing a buy

signal (MACD is crossing over the Signal line), so we are facing a long-term bull trend and the

technical situation in the short-term is also bullish. During this oversold period, the volume has not been

especially strong and this adds to the before mentioned technical view in the short-term.

Regarding the trading opportunities, as the price is near the support area, we could open a long position

with a price target in the relative maximum price at $117 and a stop before the moving average, at $94

and that gives us a reward-to-risk ratio close to 3, so it will be a good trading opportunity for a short-

term trade. Another option will be to take a long position with a trailing stop under the exponential

moving average without profit target (position trading).

Figure 8-2 Source: Visual Chart.

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 267/278 CFA, CMT, CAIA, FRM, EFA, CFTe

4B. Connie Brown in (Technical Analysis for the trading professional), is an Elliottician, she worked for

Robert Prechter a few years prior to the Centennial Olympic Games in Atlanta, and her specialty is

the S&P 500. Can you mention the list of most common objections to the Elliott Wave that she

introduces in her book? (10 points). Can you mention the difference between rules and guidelines and

show the principal rules? (5 points). How does she use the different timeframes with the Elliott Wave

Principle?

1) Although she disagree with most common objections to the Elliott Wave principle, these are the

following:

a) “It is too subjective”.

b) “Analysts have been caught on the wrong side of the market or with diametrically opposing views

about the Dow Jones Industrial Average”.

c) “Too many alternative market scenarios can be suggested by the same analyst” and “Different

analysts can interpret the exact same pattern in different ways”.

d) “If you scan different time horizons for the same market, you can find any pattern you want to prove

your market opinion”.

2) The Wave Principle only has three rules. Everything else is a guideline.

a) Rule 1: Wave 2 may not break below the origin of wave 1.

b) Rule 2: Wave 3 cannot be the shortest. This rule actually leads to a common misunderstanding.

Wave 3 does not have to be the longest; it just cannot be the shortest when compared to waves 1 and

5.

c) Rule 3: Wave 4 cannot overlap the end or termination of wave 1.

3) Constance Brown analyzes some intraday charts with the Elliott Wave Principle and makes the

statement that she works from the smallest building block possible (avoiding tick charts) and work

upward into a longer time horizon. On the other hand, Robert Prechter starts with an extremely long

horizon interpretation and then looks for substructure within progressively shorter timeframes to

compliment his longer-horizon view. Connie Brown takes the approach of building from the small and

working upward because her risk management dictates accuracy in the very short time horizons.

However, Prechter is interested in the big picture.

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 268/278 CFA, CMT, CAIA, FRM, EFA, CFTe

Answer to question 5. Candlestick. 20 - 40 points.

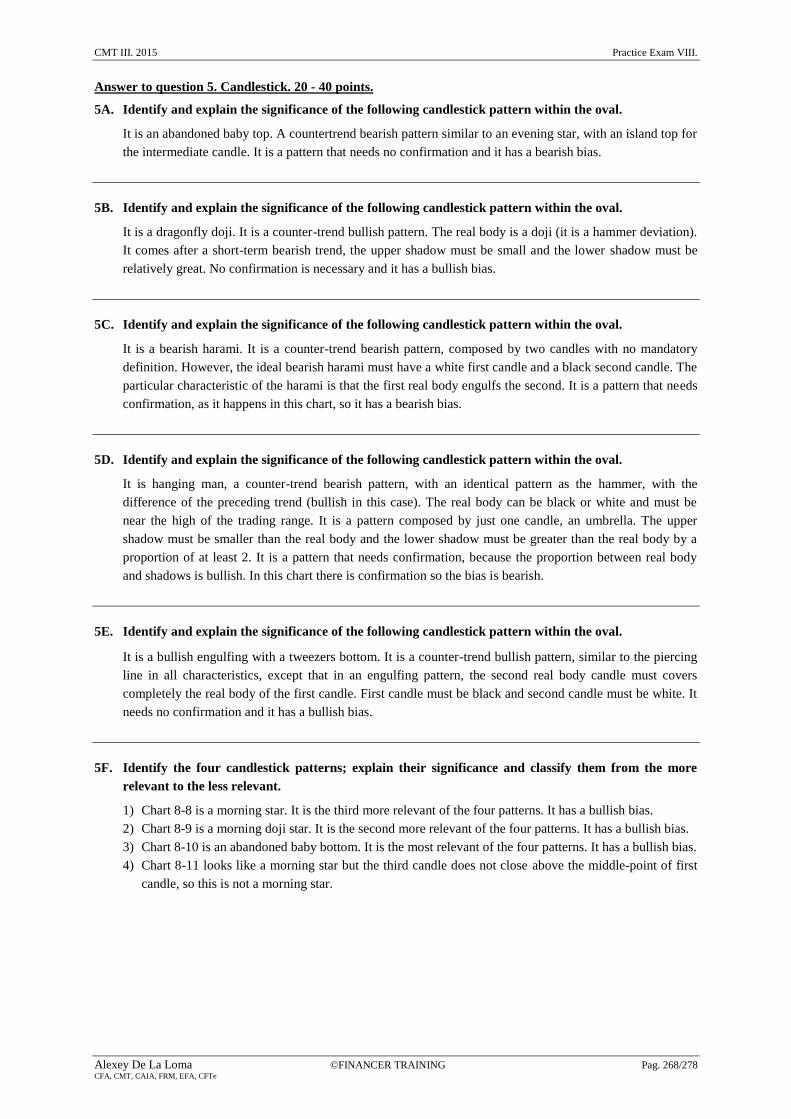

5A. Identify and explain the significance of the following candlestick pattern within the oval.

It is an abandoned baby top. A countertrend bearish pattern similar to an evening star, with an island top for

the intermediate candle. It is a pattern that needs no confirmation and it has a bearish bias.

5B. Identify and explain the significance of the following candlestick pattern within the oval.

It is a dragonfly doji. It is a counter-trend bullish pattern. The real body is a doji (it is a hammer deviation).

It comes after a short-term bearish trend, the upper shadow must be small and the lower shadow must be

relatively great. No confirmation is necessary and it has a bullish bias.

5C. Identify and explain the significance of the following candlestick pattern within the oval.

It is a bearish harami. It is a counter-trend bearish pattern, composed by two candles with no mandatory

definition. However, the ideal bearish harami must have a white first candle and a black second candle. The

particular characteristic of the harami is that the first real body engulfs the second. It is a pattern that needs

confirmation, as it happens in this chart, so it has a bearish bias.

5D. Identify and explain the significance of the following candlestick pattern within the oval.

It is hanging man, a counter-trend bearish pattern, with an identical pattern as the hammer, with the

difference of the preceding trend (bullish in this case). The real body can be black or white and must be

near the high of the trading range. It is a pattern composed by just one candle, an umbrella. The upper

shadow must be smaller than the real body and the lower shadow must be greater than the real body by a

proportion of at least 2. It is a pattern that needs confirmation, because the proportion between real body

and shadows is bullish. In this chart there is confirmation so the bias is bearish.

5E. Identify and explain the significance of the following candlestick pattern within the oval.

It is a bullish engulfing with a tweezers bottom. It is a counter-trend bullish pattern, similar to the piercing

line in all characteristics, except that in an engulfing pattern, the second real body candle must covers

completely the real body of the first candle. First candle must be black and second candle must be white. It

needs no confirmation and it has a bullish bias.

5F. Identify the four candlestick patterns; explain their significance and classify them from the more

relevant to the less relevant.

1) Chart 8-8 is a morning star. It is the third more relevant of the four patterns. It has a bullish bias.

2) Chart 8-9 is a morning doji star. It is the second more relevant of the four patterns. It has a bullish bias.

3) Chart 8-10 is an abandoned baby bottom. It is the most relevant of the four patterns. It has a bullish bias.

4) Chart 8-11 looks like a morning star but the third candle does not close above the middle-point of first

candle, so this is not a morning star.

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 269/278 CFA, CMT, CAIA, FRM, EFA, CFTe

5G. Identify the five candlestick patterns and explain if they are bullish or bearish.

1) Chart 8-12 is an on-neck pattern. It is a continuation-trend bearish pattern.

2) Chart 8-13 is an in-neck pattern. It is a continuation-trend bearish pattern.

3) Chart 8-14 is a thrusting pattern. It is a continuation-trend bearish pattern.

4) Chart 8-15 is a piercing line. It is a counter-trend bullish pattern.

5) Chart 8-16 is a bullish engulfing pattern. It is a counter-trend bullish pattern.

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 270/278 CFA, CMT, CAIA, FRM, EFA, CFTe

Answer to question 6. Elliott Wave. 20 - 40 points.

6A. Define the golden ratio or golden mean and its relation with the Elliott Wave Principle. Does the

wave principle work better for individual stocks or for stock market indices?

In Liber Abacci, Fibonacci establishes the sequence of numbers 1, 1, 2, 3, 5, 8, 13, 21, 34, 55, 89, 144,

and so on to infinity, known today as the Fibonacci sequence. The Fibonacci sequence has many

interesting properties and reflects an almost constant relationship among its components. The sum of

any two adjacent numbers in the sequence forms the next higher number in the sequence: 1 plus 1

equals 2, 1 plus 2 equals 3, 2 plus 3, equals 5, 3 plus 5 equals 8, and so on to infinity.

After the first several numbers in the sequence, the ratio of any number to the next higher is

approximately .618 to 1 and to the next lower number approximately 1.618 to 1. The further along the

sequence, the closer the ratio approaches Phi (Ф) which is an irrational number, .618034… between

alternate numbers in the sequence, the ratio is approximately .382. Phi is the only number that when

added to 1 yields its inverse: 1 + 0.618 = 1/0.618.

1.618 (or 0.618) is known as the Golden Ratio or Golden Mean. Its proportions are pleasing to the eye

and ear. It appears throughout biology, music, art and architecture. Nature uses the Golden Ratio in its

most intimate building blocks and in its most advanced patterns, in forms as minuscule as microtubules

in the brain and the DNA molecule. It is used extensively in the Wave Theory, to calculate retracements

and impulse proportions.

As a mass psychological phenomenon, the market averages unfold in Elliott wave patterns regardless of

the price movements of individual stocks. While the wave principle has some application to individual

stocks, the count for many issues is often too fuzzy to be of great practical value. In other words, Elliott

will tell you if the track is fast but not which horse is going to win. With regard to individual stocks,

other types of analysis are probably more rewarding than trying to force the stock’s price action into an

Elliott count that may or may not exist.

6B. Within the Elliott Wave Principle define the ratio analysis and explain the two categories of

relationships that can be defined with ratio analysis.

Ratio analysis is the assessment of the proportionate relationship, in time and amplitude, of one wave to

another. In discerning the working of the Golden Ratio in the five up and three down movement of the

stock market cycle, one might anticipate that on completion of any bull phase, the ensuing correction would

be three-fifths of the previous rise in both time and amplitude. Such simplicity is seldom seen. Ratio

analysis has revealed a number of precise price relationships that occur often among waves. There are two

categories of relationships: retracements and multiples.

Retracements.

Occasionally, a correction retraces a Fibonacci percentage of the preceding wave. Sharp corrections

tend more often to retrace 61.8% or 50% of the previous wave, particularly when they occur as wave 2

of an impulse, wave B of a larger zigzag, or wave X in a multiple zigzag. A leading diagonal triangle in

the wave one position is typically followed by a zigzag retracement of 78.6% (√Ф). Sideways

corrections tend more often to retrace 38.2% of the previous impulse wave, particularly when they

occur as wave 4. Retracements come in all sizes.

Motive Waves Multiples.

When wave 3 is extended, waves 1 and 5 tend towards equality or a 0.618 relationship. Actually, all

three motive waves tend to be related by Fibonacci mathematics, whether by equality, 1.618 or 2.618

(whose inverses are 0.618 and 0.382). These impulse wave relationships usually occur in percentage

terms. Of course, at small degrees, arithmetic and percentages scales produce essentially the same

result, so that the number of points in each impulse wave reveals the same multiples.

Another typical development is that wave 5’s length is sometimes related by the Fibonacci ratio to the

length of wave 1 through wave 3, showing an extended fifth wave 0.382 and 0.618 relationships occur

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 271/278 CFA, CMT, CAIA, FRM, EFA, CFTe

when wave five is not extended. In those rare cases when wave 1 is extended, it is wave 2, quite

reasonably, that often subdivides the entire impulse wave into the Golden Section.

6C. Figure 8-17 is a daily chart of Spanish Bank Santander. Identify the past wave formations. Which

wave pattern are we in now? And what does your analysis imply about the future direction of this

stock and what is your price target (your counting does not need to be exact, rounding is permitted?

The time series shows a bull trend with a complete five Elliott wave movement. Wave 1 starts at €6.15 and

finishes at €6.95, so it has a length of €0.8, wave 2 retraces €0.50, wave 3 retakes the bullish side and has a

length equal to the first wave, wave 4 retraces a length of €0.4 and the bull impulse conclude with a wave 5

with a length of €1. Once this 5 wave cycle is completed we are ready for a Fibonacci retracement (down

move) with a first objective in the 38.2% of the whole down impulse, a second objective in the 50% of the

whole down impulse, and a third and last retracement in the 61.8%. In this chart we have included price

action after the wave counting to show how the time series stopped in the third Fibonacci retracement level.

Before that we could have confirmed the down movement when the double top was confirmed (the price

violates the intermediate local minimum between the two tops).

Figure 8-17 Source: Visual Chart.

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 272/278 CFA, CMT, CAIA, FRM, EFA, CFTe

Answer to question 7. Point and Figure. 20 - 40 points.

7A. Regarding the optimization with P&F charts, name five inputs parameters of any P&F optimization

and five advises you will give a young technician about P&F optimization.

Inputs:

3-box reversal charts only.

Log scale charts only.

Box size range from 0.5% to 5%, stepping up 0.1% at a time. This means that 0.5% will be tested,

then 0.6%, then 0.7% and so on.

Test using close only and the high/low construction methods.

Entry and exit signals. Buy on first occurrence of a double-top signal. Ignore any subsequent

double-top buys. Sell on first occurrence of a double-bottom sell. Ignore all subsequent double-

bottom sells, until the next double-top buy starts to process again.

Data. This is discussed in the data consistency and adaptability section.

Recommendations.

Optimization is only of value with 3-box reversal charts, because of their unambiguous signals.

Unless you are looking very short-term, percentage box sizes should be used.

Including uncommon Point and Figure patterns is fine for entry signals, but they should never be

included as possible exit signals.

Optimization should always be conducted using the latest data because this allows the parameters to

adjust as new data is received.

The unrealized profit from any open position should be excluded from the optimization, so box sizes

are calculated on closed positions only.

Dealing costs must be taken into account to prevent lots of small trades from being included.

Optimization can tell you what box size is working best, based on double-top and bottom signals. In

doing so, it tells you about the characteristics of the instruments.

In most cases, profits are increased considerably when trailing stop loss is used as the exit rather

than a double-column signal.

Optimization can tell you whether the close only or high/low construction method is working best

for the particular instrument.

Optimization results show that the shorter your time horizon, the smaller the box size is required.

Optimization does not tell you how to read the chart, but gives you a starting point from where your

subjective analysis must take over.

Signal delay may need to be considered, although it is more difficult to administer with Point and

Figure charts.

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 273/278 CFA, CMT, CAIA, FRM, EFA, CFTe

7B. Discuss the current technical situation. Would you buy or sell this asset? Where would you place

your stop and objective if you are using vertical counting? Is the reward-to-risk ratio attractive?

This is a 1x3 Point and Figure chart that is reversing a bull trend, so the current trendline is bearish. The

current price is in a down column and this pattern is called a reversal double bottom. We could not

recommend opening a short position at current prices because both reward-to-risk ratios are quite poor

(below the recommended 3:1).

Vertical Target.

56 - (6*1*3) = 38.

Reward.

49 - 38 = 11.

Risk 1.

55 - 49 = 6 and the Risk1-Reward ratio is 11/6 = 1.8.

Risk 2.

57 - 49 = 8 and the Risk2-Reward ratio is 12/8 = 1.5.

Figure 8-18 Source: Own Elaboration.

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 274/278 CFA, CMT, CAIA, FRM, EFA, CFTe

Answer to question 8. Risk Management. 20 - 40 points.

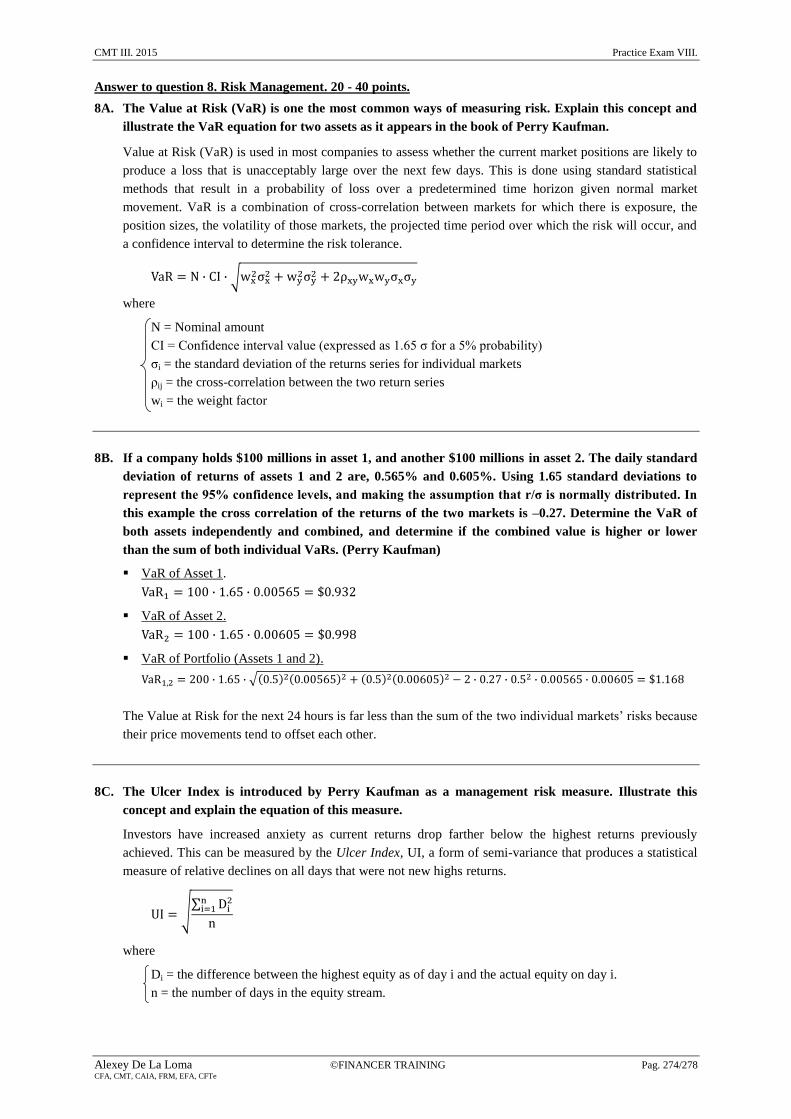

8A. The Value at Risk (VaR) is one the most common ways of measuring risk. Explain this concept and

illustrate the VaR equation for two assets as it appears in the book of Perry Kaufman.

Value at Risk (VaR) is used in most companies to assess whether the current market positions are likely to

produce a loss that is unacceptably large over the next few days. This is done using standard statistical

methods that result in a probability of loss over a predetermined time horizon given normal market

movement. VaR is a combination of cross-correlation between markets for which there is exposure, the

position sizes, the volatility of those markets, the projected time period over which the risk will occur, and

a confidence interval to determine the risk tolerance.

where

N = Nominal amount

CI = Confidence interval value (expressed as 1.65 σ for a 5% probability)

σi = the standard deviation of the returns series for individual markets

ρij = the cross-correlation between the two return series

wi = the weight factor

8B. If a company holds $100 millions in asset 1, and another $100 millions in asset 2. The daily standard

deviation of returns of assets 1 and 2 are, 0.565% and 0.605%. Using 1.65 standard deviations to

represent the 95% confidence levels, and making the assumption that r/σ is normally distributed. In

this example the cross correlation of the returns of the two markets is –0.27. Determine the VaR of

both assets independently and combined, and determine if the combined value is higher or lower

than the sum of both individual VaRs. (Perry Kaufman)

VaR of Asset 1.

VaR of Asset 2.

VaR of Portfolio (Assets 1 and 2).

The Value at Risk for the next 24 hours is far less than the sum of the two individual markets’ risks because

their price movements tend to offset each other.

8C. The Ulcer Index is introduced by Perry Kaufman as a management risk measure. Illustrate this

concept and explain the equation of this measure.

Investors have increased anxiety as current returns drop farther below the highest returns previously

achieved. This can be measured by the Ulcer Index, UI, a form of semi-variance that produces a statistical

measure of relative declines on all days that were not new highs returns.

where

Di = the difference between the highest equity as of day i and the actual equity on day i.

n = the number of days in the equity stream.

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 275/278 CFA, CMT, CAIA, FRM, EFA, CFTe

System B

System A

System B

System A

Time Time

If the equity on day i is a new high equity, then Di = 0. As the UI increases, investors are more anxious

about performance.

8D. Illustrate the equation of the Sharpe Ratio and determine graphically why this ratio cannot

distinguish between

Consecutive small losses and alternating small losses.

Consecutive small losses and large surges of profits.

The classic measurement of performance is the Sharpe ratio (SR), expressed as

where

μ = the expected return (the annualized rate of return)

rRF = the risk free rate (usually the 3-month rate)

σμ = the standard deviation of the periodic returns

Kaufman considers that the risk free rate can be omitted in some occasions. For example, it cannot be

omitted when there is a risk free rate return on unused capital that has been imbedded in the performance.

The Sharpe Ratio satisfies the first universal criterion of system selection, that all else being equal, higher

profits are better. It does not satisfy either of the other criteria illustrated in figures A and B, because it

cannot distinguish between:

Consecutive small losses (system B) and alternating small losses (system A).

Consecutive small losses (system B) and large surges of profits (system A).

Clearly, system A is best in both cases.

Equit

y

Equit

y

Source: Perry Kaufman. Source: Perry Kaufman. Figure B Figure A

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 276/278 CFA, CMT, CAIA, FRM, EFA, CFTe

Answer to question 9. System Development. 20 - 40 points.

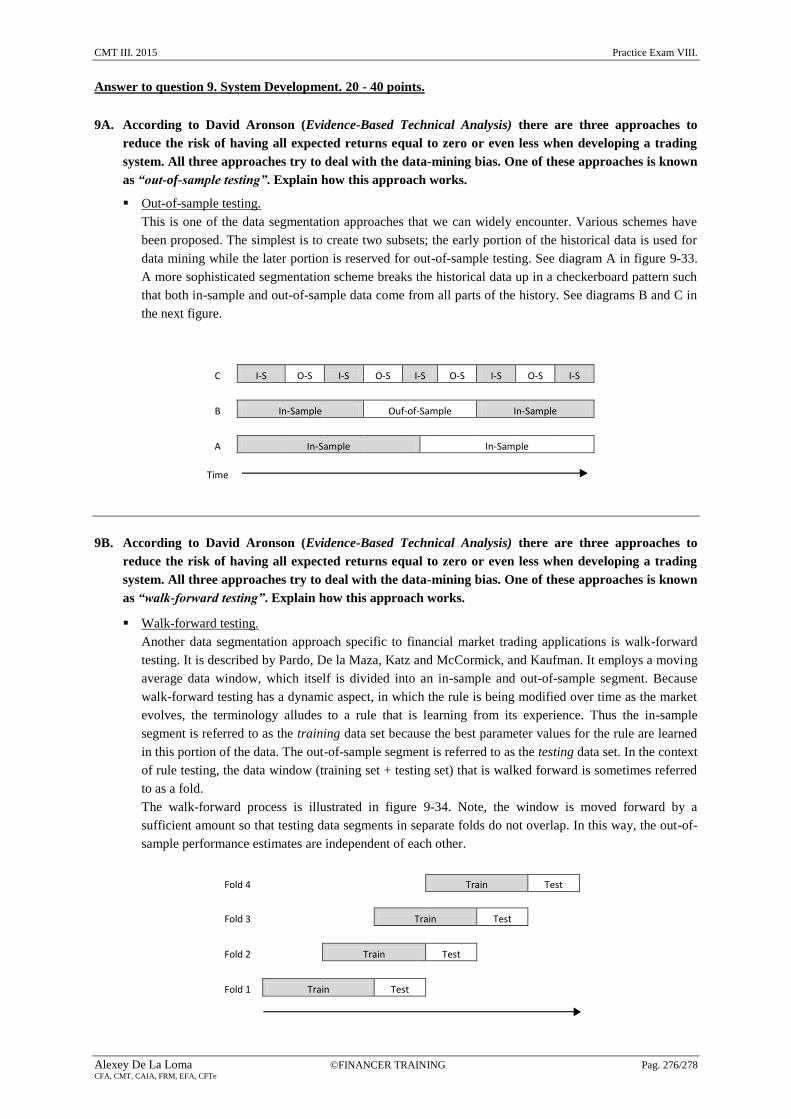

9A. According to David Aronson (Evidence-Based Technical Analysis) there are three approaches to

reduce the risk of having all expected returns equal to zero or even less when developing a trading

system. All three approaches try to deal with the data-mining bias. One of these approaches is known

as “out-of-sample testing”. Explain how this approach works.

Out-of-sample testing.

This is one of the data segmentation approaches that we can widely encounter. Various schemes have

been proposed. The simplest is to create two subsets; the early portion of the historical data is used for

data mining while the later portion is reserved for out-of-sample testing. See diagram A in figure 9-33.

A more sophisticated segmentation scheme breaks the historical data up in a checkerboard pattern such

that both in-sample and out-of-sample data come from all parts of the history. See diagrams B and C in

the next figure.

C I-S O-S I-S O-S I-S O-S I-S O-S I-S

B In-Sample Ouf-of-Sample In-Sample

A In-Sample In-Sample

Time

9B. According to David Aronson (Evidence-Based Technical Analysis) there are three approaches to

reduce the risk of having all expected returns equal to zero or even less when developing a trading

system. All three approaches try to deal with the data-mining bias. One of these approaches is known

as “walk-forward testing”. Explain how this approach works.

Walk-forward testing.

Another data segmentation approach specific to financial market trading applications is walk-forward

testing. It is described by Pardo, De la Maza, Katz and McCormick, and Kaufman. It employs a moving

average data window, which itself is divided into an in-sample and out-of-sample segment. Because

walk-forward testing has a dynamic aspect, in which the rule is being modified over time as the market

evolves, the terminology alludes to a rule that is learning from its experience. Thus the in-sample

segment is referred to as the training data set because the best parameter values for the rule are learned

in this portion of the data. The out-of-sample segment is referred to as the testing data set. In the context

of rule testing, the data window (training set + testing set) that is walked forward is sometimes referred

to as a fold.

The walk-forward process is illustrated in figure 9-34. Note, the window is moved forward by a

sufficient amount so that testing data segments in separate folds do not overlap. In this way, the out-of-

sample performance estimates are independent of each other.

Fold 4

Train Test

Fold 3

Train Test

Fold 2

Train Test

Fold 1 Train Test

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 277/278 CFA, CMT, CAIA, FRM, EFA, CFTe

9C. Trend-following systems are based on taking positions in the direction of the trend. They are based

on taking a long position when prices are high, in order to close that position even higher, or taking a

short position when prices are low, in order to sell that position even lower. Trend-following do not

attempt to catch peaks and valleys as counter-trend system do. Because, we need to be sure a trend

has started before taking a position, they send lagging signals and suffer in trading range markets.

According to Charles Kirkpatrick, there are two types of trend-following systems. Name them and

explain their characteristics.

Moving Average Systems.

There are three popular trending-following trading systems based on moving averages. If we use only

one moving average, we can define a trading system whose signals are generated when prices cross the

moving average. If we include two moving averages, signals are generated when both moving averages

cross over each other. We can even include one more moving average and design a trading system with

three moving averages. According to Charles Kirkpatrick and Larry Williams (The Definitive Guide to

Futures Trading) the most efficient way to trade using moving averages is the intermediate system. In

other words, using two moving averages is better than using three or just one.

Breakout Systems.

Additionally to the popular moving averages, we can develop trend-following trading systems through

the concept of “breakout”. In a breakout trading systems, signals are generated when price moves out of

a channel or band. These systems can be based on static bands, as the popular Richard Donchian’s

four-week rule, or dynamic, as the volatility breakout systems using Bollinger bands, ranges ATRs or

other measures of range volatility. The most productive are based on longer timeframes (daily or

weekly). However, they can also be applied to shorter timeframes as the open range breakout systems,

based on intraday data.

9D. Define the concept and state the equations for the following backtesting measures: net profit, profit

factor, payoff ratio, and recovery ratio.

Net Profit.

It is the difference between gross profit (total profit from profitable trades) and gross loss (total loss

from losing trades). The net profit of our system must positive, if not we have a negative mathematical

expectancy.

Profit Factor.

It is the absolute value of the ratio between the gross profit and the gross loss. It shows the profitability

of the system. It must be above 1.0 or the system will have a negative mathematical expectancy.

According to Charles Kirkpatrick, “it is one of the most commonly used statistics to screen for systems

from optimization.” However, it does not tell us anything different than the previous net profit. If a

system has a positive mathematical expectancy, net profit must be positive, and profit factor must be

above 1.

Payoff ratio.

This is one of the most relevant figures of a trading system. It is just a ratio between the average

winning trade and the average losing trade, so when combined with the profitability percentage it

illustrates the mathematical expectancy of the trading system. It can also be used to determine the risk

of ruin. Trend-following systems have a higher payoff ratio than countertrend systems. Charles

Kirkpatrick considers that trend-following systems should have a ratio greater than 2.0.

CMT III. 2015 Practice Exam VIII.

Alexey De La Loma ©FINANCER TRAINING Pag. 278/278 CFA, CMT, CAIA, FRM, EFA, CFTe

Recovery Ratio.

This is one of the most important figures of a backtesting, and a great indicator to rank the results of an

optimization process. According to Charles Kirkpatrick, it should be above 2.0.