18

www.pwc.co.uk Practical guide to corporate governance Governance reporting – Moving it forward April 2013

www.pwc.co.uk

Practical guideto corporategovernance

Governance reporting –Moving it forward

April 2013

Practical guide to corporate governance Draft

Governance reporting – Moving it forward PwC Contents

Contents

Governance reporting – Moving it forward 1

What’s the issue? 1

How to address the issue 1

Conclusion 3

Appendices 4

Appendix 1: Sources of governance reporting requirementsand guidance 5

Appendix 2: Mapping the Main Principles and disclosureprovisions of the 2012 UK Corporate Governance Code tothe skeleton governance report 8

Practical guide to corporate governance

Governance reporting – Moving it forward PwC 1

This report grew out of discussions with a range ofcompanies late in 2012 and at the start of 2013 duringwhich it was apparent that there is widespreadfrustration with the content of governance reportingin today’s annual reports. Though this may soundnegative, we took away a positive message: everyonewe spoke to saw the value in making a change andthere was a real appetite to understand what mightbe done.

This report seeks to answer that question. Ouranswers are not revolutionary; they are built arounddemonstrating compliance and are intended to bepractical steps that any company can take now.

What’s the issue?Premium listed companies could be forgiven forconcluding that they receive mixed messages from theregulators when it comes to preparing the corporategovernance report.

The DTR1 would allow them to make the reportavailable exclusively on their website, while the FRCin ‘Cutting Clutter’2 advocated focusing on the keymessages in the governance report and moving therest into an appendix. And yet the UK CorporateGovernance Code3 (‘the Code’) and the Listing Rules4

combine to prevent either of these approaches at thepresent time.

Online reporting could help to allow companies tofocus on the key messages in their annual report but itnow appears unlikely to be addressed when therevised narrative reporting regulations are finalised inthe next few months.

1 The Disclosure Rules and Transparency Rules Chapter 7.2:http://fsahandbook.info/FSA/html/handbook/DTR/7/2 .2 FRC ‘Cutting Clutter’:

http://www.frc.org.uk/Our-Work/Publications/ASB/Cutting-Clutter-Combating-Clutter-in-Annual-Report.aspx.3 FRC UK Corporate Governance Code:http://www.frc.org.uk/Our-Work/Publications/Corporate-Governance/UK-Corporate-Governance-Code-September-2012.aspx .4 FSA Listing Rules 9.8:http://fsahandbook.info/FSA/html/handbook/LR/9/8 .

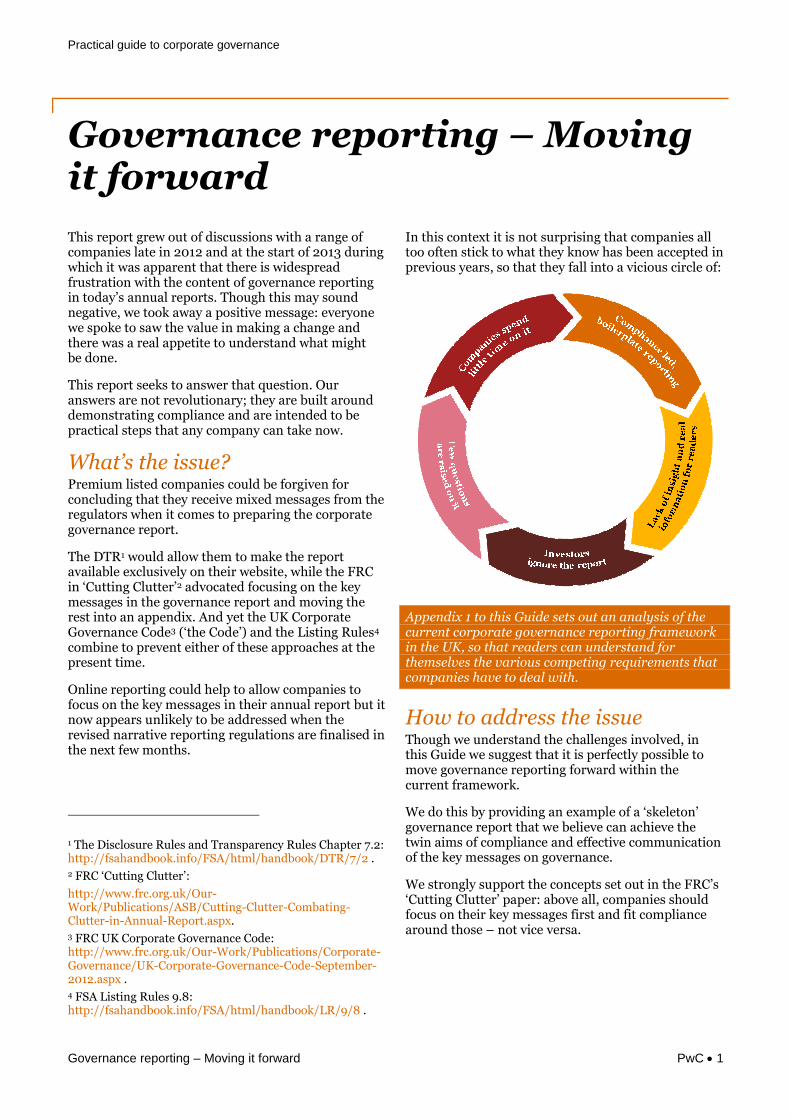

In this context it is not surprising that companies alltoo often stick to what they know has been accepted inprevious years, so that they fall into a vicious circle of:

Appendix 1 to this Guide sets out an analysis of thecurrent corporate governance reporting frameworkin the UK, so that readers can understand forthemselves the various competing requirements thatcompanies have to deal with.

How to address the issueThough we understand the challenges involved, inthis Guide we suggest that it is perfectly possible tomove governance reporting forward within thecurrent framework.

We do this by providing an example of a ‘skeleton’governance report that we believe can achieve thetwin aims of compliance and effective communicationof the key messages on governance.

We strongly support the concepts set out in the FRC’s‘Cutting Clutter’ paper: above all, companies shouldfocus on their key messages first and fit compliancearound those – not vice versa.

Governance reporting – Movingit forward

Practical guide to corporate governance

Governance reporting – Moving it forward PwC 2

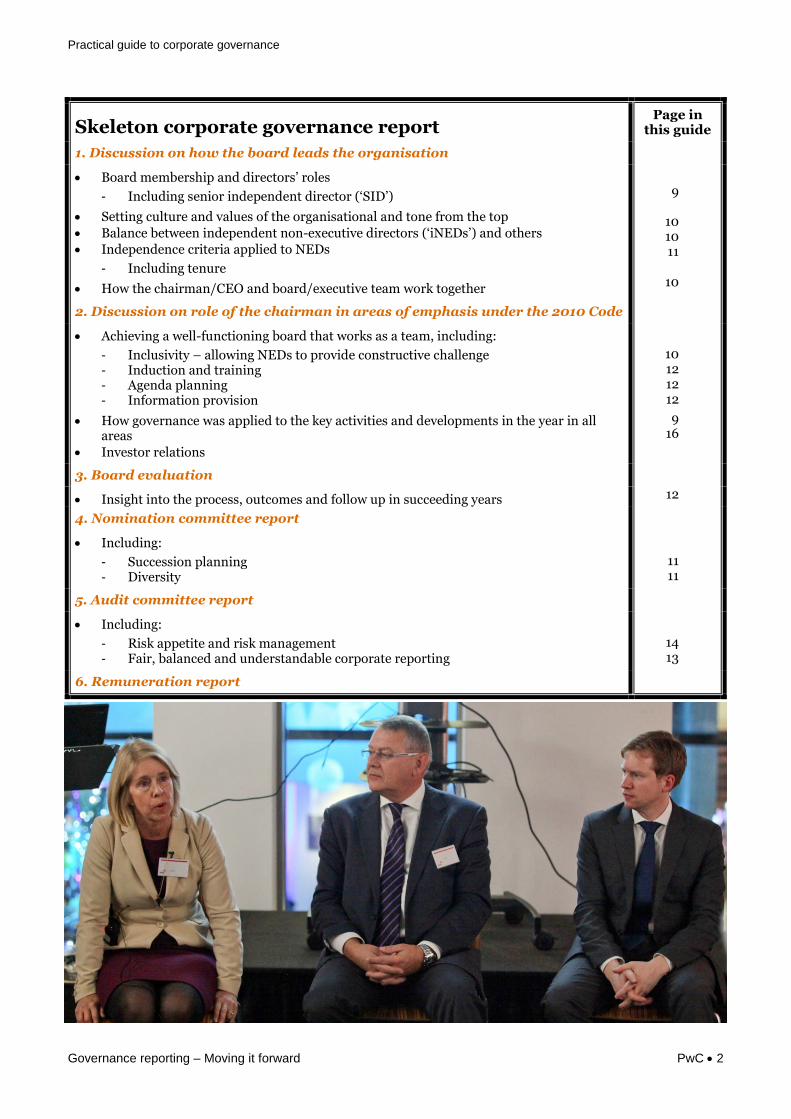

Skeleton corporate governance reportPage in

this guide

1. Discussion on how the board leads the organisation

Board membership and directors’ roles

Including senior independent director (‘SID’)

Setting culture and values of the organisational and tone from the top Balance between independent non-executive directors (‘iNEDs’) and others Independence criteria applied to NEDs

Including tenure

How the chairman/CEO and board/executive team work together

9

101011

10

2. Discussion on role of the chairman in areas of emphasis under the 2010 Code

Achieving a well-functioning board that works as a team, including:

Inclusivity – allowing NEDs to provide constructive challenge Induction and training Agenda planning Information provision

How governance was applied to the key activities and developments in the year in allareas

Investor relations

10121212

916

3. Board evaluation

Insight into the process, outcomes and follow up in succeeding years 12

4. Nomination committee report

Including:

Succession planning Diversity

1111

5. Audit committee report

Including:

Risk appetite and risk management Fair, balanced and understandable corporate reporting

1413

6. Remuneration report

Practical guide to corporate governance

Governance reporting – Moving it forward PwC 3

Our proposition is that the skeleton corporategovernance report opposite covers off the technicalcompliance requirements in a way that also deals withthe key messages on governance. In other words, it:

addresses the Listings Rules requirement to showhow the Main Principles have been applied; and

covers most of the specific disclosure provisions ofthe Code; those that are not covered can easily bedealt with in an appendix to the governancereport of the sort that the FRC recommended inCutting Clutter:

‘...we are acutely aware that currently explanatoryinformation cannot be provided on a website.In developing our disclosure aids, we have assumedthat progress is made in this area. Unfortunatelywe are not there yet. Accordingly, in the currentenvironment we suggest moving explanatoryinformation into an appendix withinan annual report.” [FRC ‘Cutting Clutter’ page 33].

Appendix 2 to this Guide maps each Main Principle ofthe Code and the related disclosure provisions to theskeleton set out above and explains how it coversthem – or where specific information may need to beadded specifically for compliance purposes.

The skeleton report presented here is not, of course,meant as a template or checklist for a governancereport; it is intended only to demonstrate thatfocusing on a number of key governance messagescan actually drive compliant disclosures.

ConclusionThere are some very good governance reportersamong UK companies but too many simply rollforward the basic structure of their governance reportyear on year. Our proposals would allow a move awayfrom this in order to break out of the vicious circle ofreporting only for the sake of compliance.

Our earlier publication under the Report Leadershipbanner ‘Simple, practical proposals for betterreporting of corporate governance5’ provided ideas forcontent to help communicate the key governancemessages.

In that publication we also suggested a format thatcould be used for the appendix such as that suggestedin ‘Cutting Clutter’ to demonstrate Code compliance.

The PwC Corporate Reporting team can explain moreand help to implement these proposals in practice.

5 See http://www.reportleadership.com/

Please enquire of your usual PwC contact or thepeople shown below.

The editorial team for this publication consists of:

PwC Corporate reporting team

Mark O’Sullivan

Tel : +44 (0) 20 7804 3459

Email: [email protected]

John Patterson

Tel : +44 (0) 12 2355 2413

Email: [email protected]

Although the Code has relatively few provisions thatrequire specific disclosures, the Listing Rules requirecompanies to provide a narrative statement of howthey have applied the Main Principles of the Code[LR 9.8.6 (6)]. This has often led companies to runthrough all the provisions that relate to each MainPrinciple, including those that do not require specificdisclosures, as a means of showing how they havedone this.

This Guide particularly encourages companies tomove away from this approach.

Practical guide to corporate governance

Governance reporting – Moving it forward PwC 4

Appendices

Practical guide to corporate governance

Governance reporting – Moving it forward PwC 5

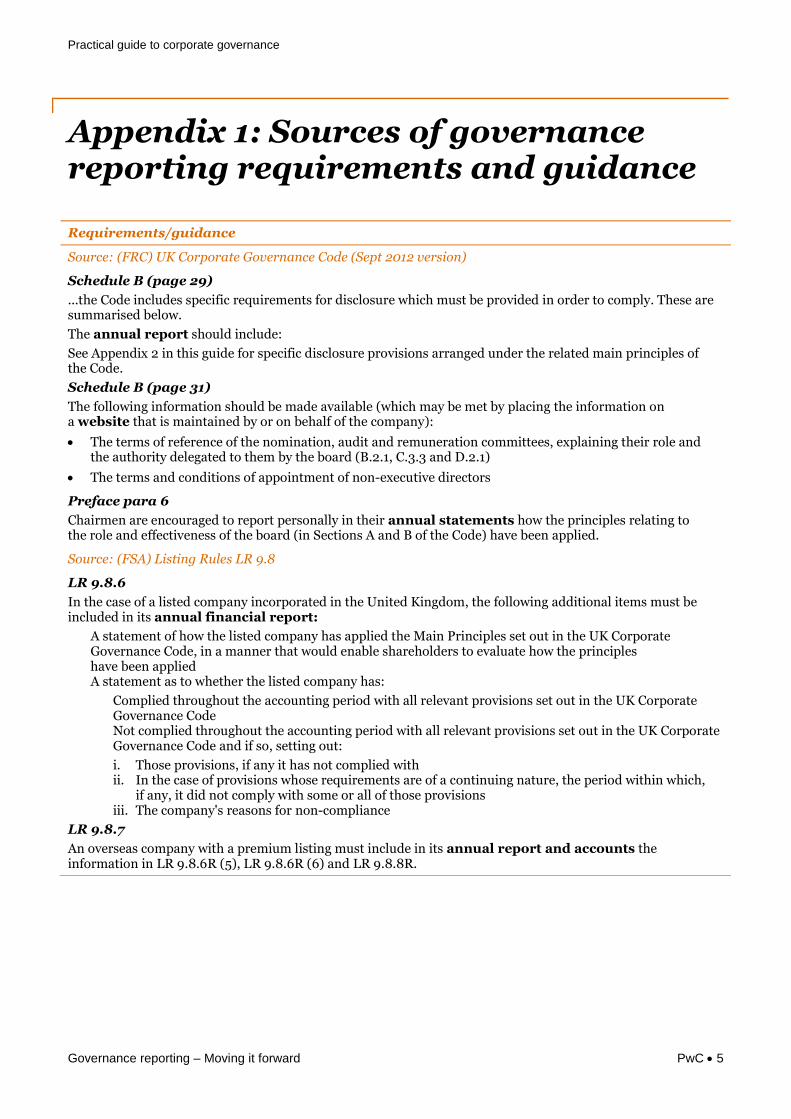

Requirements/guidance

Source: (FRC) UK Corporate Governance Code (Sept 2012 version)

Schedule B (page 29)

...the Code includes specific requirements for disclosure which must be provided in order to comply. These aresummarised below.

The annual report should include:

See Appendix 2 in this guide for specific disclosure provisions arranged under the related main principles ofthe Code.

Schedule B (page 31)

The following information should be made available (which may be met by placing the information ona website that is maintained by or on behalf of the company):

The terms of reference of the nomination, audit and remuneration committees, explaining their role andthe authority delegated to them by the board (B.2.1, C.3.3 and D.2.1)

The terms and conditions of appointment of non-executive directors

Preface para 6

Chairmen are encouraged to report personally in their annual statements how the principles relating tothe role and effectiveness of the board (in Sections A and B of the Code) have been applied.

Source: (FSA) Listing Rules LR 9.8

LR 9.8.6

In the case of a listed company incorporated in the United Kingdom, the following additional items must beincluded in its annual financial report:

A statement of how the listed company has applied the Main Principles set out in the UK CorporateGovernance Code, in a manner that would enable shareholders to evaluate how the principleshave been appliedA statement as to whether the listed company has:

Complied throughout the accounting period with all relevant provisions set out in the UK CorporateGovernance CodeNot complied throughout the accounting period with all relevant provisions set out in the UK CorporateGovernance Code and if so, setting out:

i. Those provisions, if any it has not complied withii. In the case of provisions whose requirements are of a continuing nature, the period within which,

if any, it did not comply with some or all of those provisionsiii. The company's reasons for non-compliance

LR 9.8.7

An overseas company with a premium listing must include in its annual report and accounts theinformation in LR 9.8.6R (5), LR 9.8.6R (6) and LR 9.8.8R.

Appendix 1: Sources of governancereporting requirements and guidance

Practical guide to corporate governance

Governance reporting – Moving it forward PwC 6

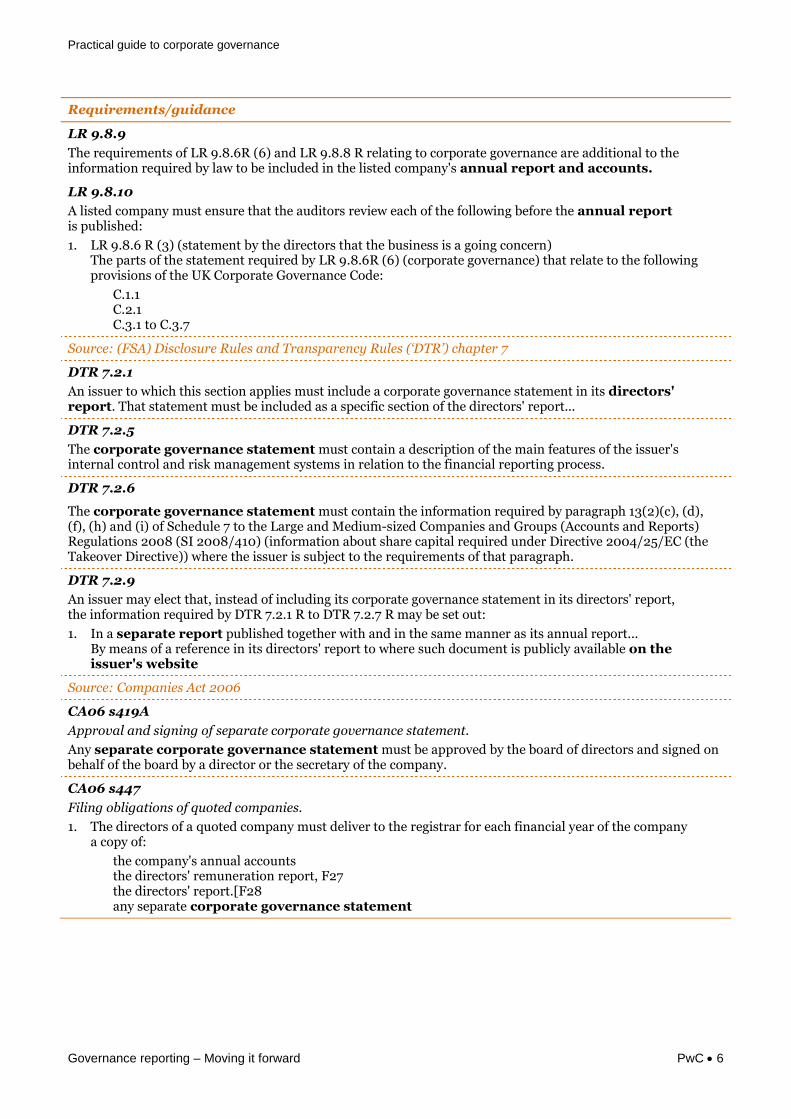

Requirements/guidance

LR 9.8.9

The requirements of LR 9.8.6R (6) and LR 9.8.8 R relating to corporate governance are additional to theinformation required by law to be included in the listed company's annual report and accounts.

LR 9.8.10

A listed company must ensure that the auditors review each of the following before the annual reportis published:

1. LR 9.8.6 R (3) (statement by the directors that the business is a going concern)The parts of the statement required by LR 9.8.6R (6) (corporate governance) that relate to the followingprovisions of the UK Corporate Governance Code:

C.1.1C.2.1C.3.1 to C.3.7

Source: (FSA) Disclosure Rules and Transparency Rules (‘DTR’) chapter 7

DTR 7.2.1

An issuer to which this section applies must include a corporate governance statement in its directors'report. That statement must be included as a specific section of the directors' report...

DTR 7.2.5

The corporate governance statement must contain a description of the main features of the issuer'sinternal control and risk management systems in relation to the financial reporting process.

DTR 7.2.6

The corporate governance statement must contain the information required by paragraph 13(2)(c), (d),(f), (h) and (i) of Schedule 7 to the Large and Medium-sized Companies and Groups (Accounts and Reports)Regulations 2008 (SI 2008/410) (information about share capital required under Directive 2004/25/EC (theTakeover Directive)) where the issuer is subject to the requirements of that paragraph.

DTR 7.2.9

An issuer may elect that, instead of including its corporate governance statement in its directors' report,the information required by DTR 7.2.1 R to DTR 7.2.7 R may be set out:

1. In a separate report published together with and in the same manner as its annual report...By means of a reference in its directors' report to where such document is publicly available on theissuer's website

Source: Companies Act 2006

CA06 s419A

Approval and signing of separate corporate governance statement.

Any separate corporate governance statement must be approved by the board of directors and signed onbehalf of the board by a director or the secretary of the company.

CA06 s447

Filing obligations of quoted companies.

1. The directors of a quoted company must deliver to the registrar for each financial year of the companya copy of:

the company's annual accountsthe directors' remuneration report, F27the directors' report.[F28any separate corporate governance statement

Practical guide to corporate governance

Governance reporting – Moving it forward PwC 7

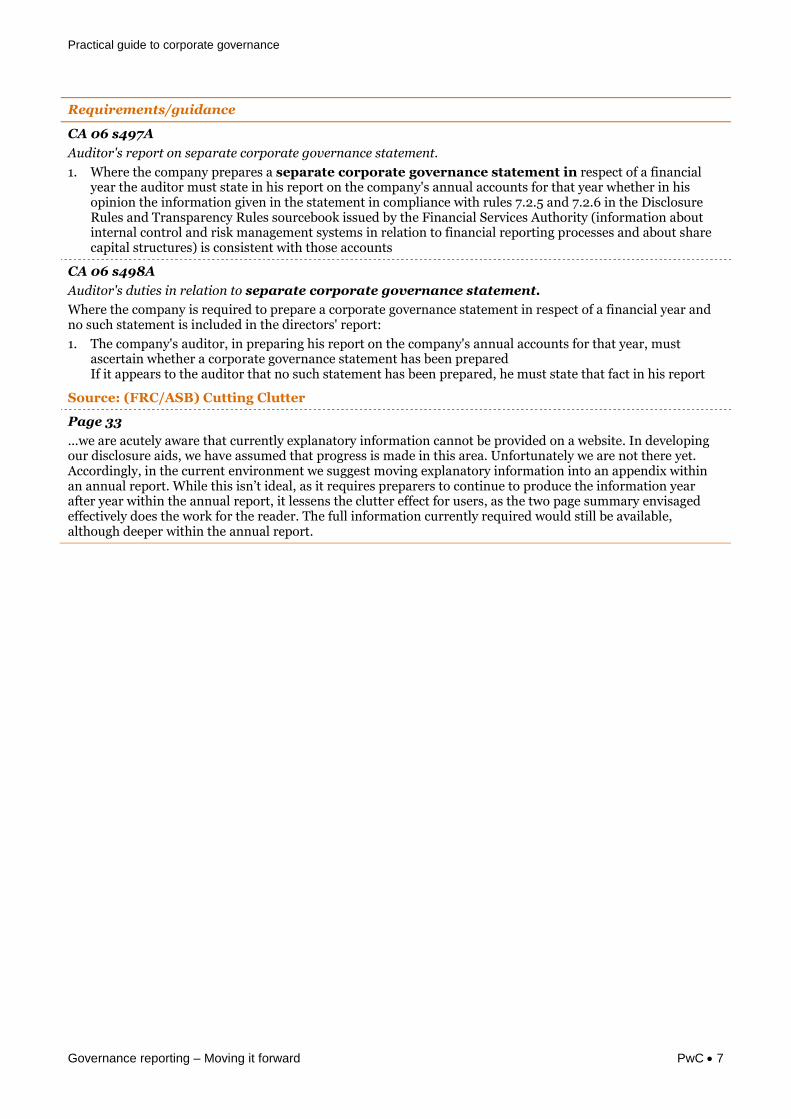

Requirements/guidance

CA 06 s497A

Auditor's report on separate corporate governance statement.

1. Where the company prepares a separate corporate governance statement in respect of a financialyear the auditor must state in his report on the company's annual accounts for that year whether in hisopinion the information given in the statement in compliance with rules 7.2.5 and 7.2.6 in the DisclosureRules and Transparency Rules sourcebook issued by the Financial Services Authority (information aboutinternal control and risk management systems in relation to financial reporting processes and about sharecapital structures) is consistent with those accounts

CA 06 s498A

Auditor's duties in relation to separate corporate governance statement.

Where the company is required to prepare a corporate governance statement in respect of a financial year andno such statement is included in the directors' report:

1. The company's auditor, in preparing his report on the company's annual accounts for that year, mustascertain whether a corporate governance statement has been preparedIf it appears to the auditor that no such statement has been prepared, he must state that fact in his report

Source: (FRC/ASB) Cutting Clutter

Page 33

...we are acutely aware that currently explanatory information cannot be provided on a website. In developingour disclosure aids, we have assumed that progress is made in this area. Unfortunately we are not there yet.Accordingly, in the current environment we suggest moving explanatory information into an appendix withinan annual report. While this isn’t ideal, as it requires preparers to continue to produce the information yearafter year within the annual report, it lessens the clutter effect for users, as the two page summary envisagedeffectively does the work for the reader. The full information currently required would still be available,although deeper within the annual report.

Practical guide to corporate governance

Governance reporting – Moving it forward PwC 8

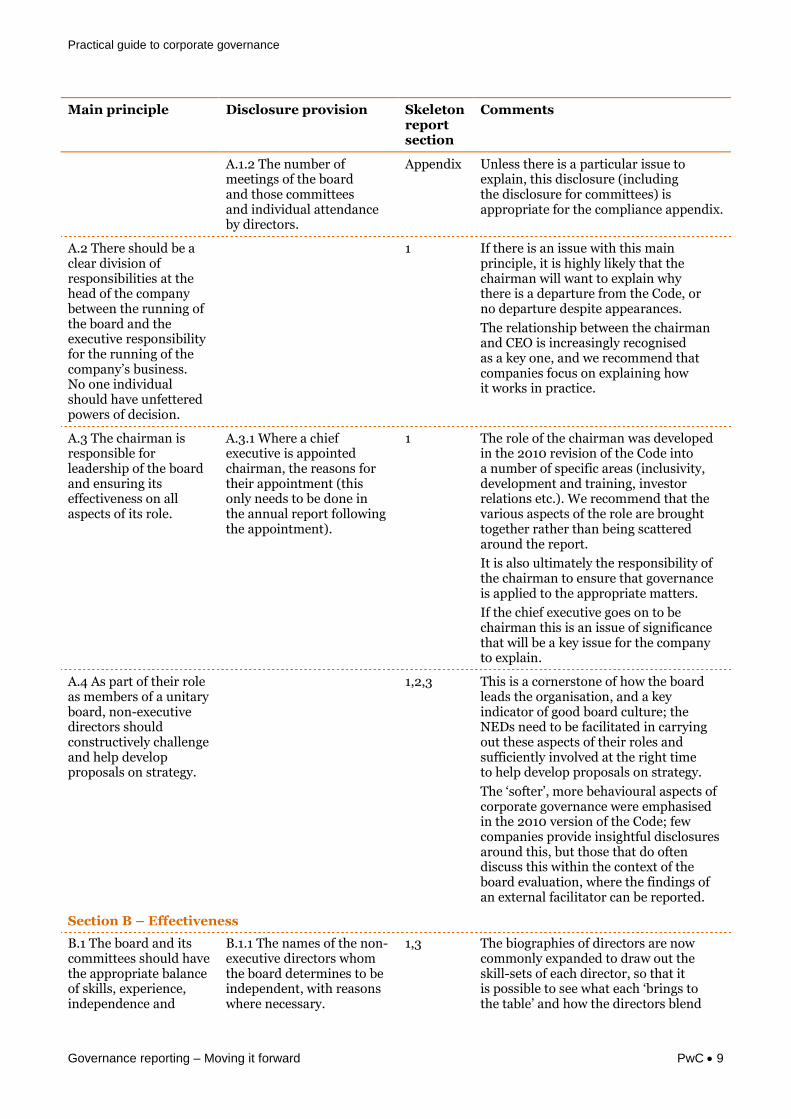

This appendix maps each Main Principle of the Code and the related disclosure provisions to the skeleton setout on page 2 and explains how it covers them – or where specific information may need to be addedspecifically for compliance purposes.

Main principle Disclosure provision Skeletonreportsection

Comments

Section A – Leadership

A.1 Every companyshould be headed by aneffective board which iscollectively responsiblefor the long-termsuccess of the company.

A.1.1 A statement of howthe board operates,including a high levelstatement of which typesof decisions are to be takenby the board and whichare to be delegatedto management.

1,2,3 The preface to the Code (para 6) suggeststhat the chairman reports personally onhow the principles relating to the roleand effectiveness of the board have beenapplied, and the chairman’s introductionto the governance report is a goodopportunity to address this. We wouldsuggest that the most effective way todo this is for the chairman to explainhow the board dealt with the keydevelopments in the business in the year(whether these are backward or forwardlooking, or both).

The chairman’s introduction to thegovernance report also commonlysummarises the findings of the boardevaluation process – it’s significant thatthe main principle on leadership includesthe word ‘effective’ – these are two sidesof the same coin.

Provision A.1.1 appears to ask fora summary of the matters reserved forthe board; if the key developmentshave been addressed then thisprocedural requirement could be setout in the compliance appendix to thegovernance report.

A.1.2 The names of thechairman, the deputychairman (where thereis one), the chief executive,the senior independentdirector and the chairmenand members of theboard committees

2 The identity, skills and qualificationsof board members are of course veryimportant; this information is bestcombined with the effectivenessdisclosures under main principleB.1, however.

Appendix 2: Mapping the MainPrinciples and disclosure provisions ofthe 2012 UK Corporate GovernanceCode to the skeleton governance report

Practical guide to corporate governance

Governance reporting – Moving it forward PwC 9

Main principle Disclosure provision Skeletonreportsection

Comments

A.1.2 The number ofmeetings of the boardand those committeesand individual attendanceby directors.

Appendix Unless there is a particular issue toexplain, this disclosure (includingthe disclosure for committees) isappropriate for the compliance appendix.

A.2 There should be aclear division ofresponsibilities at thehead of the companybetween the running ofthe board and theexecutive responsibilityfor the running of thecompany’s business.No one individualshould have unfetteredpowers of decision.

1 If there is an issue with this mainprinciple, it is highly likely that thechairman will want to explain whythere is a departure from the Code, orno departure despite appearances.

The relationship between the chairmanand CEO is increasingly recognisedas a key one, and we recommend thatcompanies focus on explaining howit works in practice.

A.3 The chairman isresponsible forleadership of the boardand ensuring itseffectiveness on allaspects of its role.

A.3.1 Where a chiefexecutive is appointedchairman, the reasons fortheir appointment (thisonly needs to be done inthe annual report followingthe appointment).

1 The role of the chairman was developedin the 2010 revision of the Code intoa number of specific areas (inclusivity,development and training, investorrelations etc.). We recommend that thevarious aspects of the role are broughttogether rather than being scatteredaround the report.

It is also ultimately the responsibility ofthe chairman to ensure that governanceis applied to the appropriate matters.

If the chief executive goes on to bechairman this is an issue of significancethat will be a key issue for the companyto explain.

A.4 As part of their roleas members of a unitaryboard, non-executivedirectors shouldconstructively challengeand help developproposals on strategy.

1,2,3 This is a cornerstone of how the boardleads the organisation, and a keyindicator of good board culture; theNEDs need to be facilitated in carryingout these aspects of their roles andsufficiently involved at the right timeto help develop proposals on strategy.

The ‘softer’, more behavioural aspects ofcorporate governance were emphasisedin the 2010 version of the Code; fewcompanies provide insightful disclosuresaround this, but those that do oftendiscuss this within the context of theboard evaluation, where the findings ofan external facilitator can be reported.

Section B – Effectiveness

B.1 The board and itscommittees should havethe appropriate balanceof skills, experience,independence and

B.1.1 The names of the non-executive directors whomthe board determines to beindependent, with reasonswhere necessary.

1,3 The biographies of directors are nowcommonly expanded to draw out theskill-sets of each director, so that itis possible to see what each ‘brings tothe table’ and how the directors blend

Practical guide to corporate governance

Governance reporting – Moving it forward PwC 10

Main principle Disclosure provision Skeletonreportsection

Comments

knowledge of thecompany to enablethem to discharge theirrespective duties andresponsibilitieseffectively.

as a team.

Independence is still a key criterion forboard composition, using the indicatorsset out in provision B.1.1. In some casesthere are particular sensitivities in thisarea (such as some of the more recentIPOs from overseas) and we adviseproviding sufficient information to headoff any preconceptions in such situations.

Succession planning is now recognisedas a key part of board effectiveness andmost nomination committee reports(or even the chairman’s introductionto the governance report) explain thearrangements in place.

B.2 There should bea formal, rigorous andtransparent procedurefor the appointmentof new directors tothe board.

B.2.4 A separate sectiondescribing the work of thenomination committee,including the process it hasused in relation to boardappointments;a description of the board’spolicy on diversity,including gender; anymeasurable objectives thatit has set for implementingthe policy, and progress onachieving the objectives.

An explanation should begiven if neither externalsearch consultancy noropen advertising has beenused in the appointment ofa chairman or a non-executive director. Wherean external searchconsultancy has been usedit should be identified anda statement made asto whether it has anyother connection withthe company.

1,2,4 It’s important to focus these disclosureson any appointments that have beenmade, and how these were handled;general descriptions of process are notgenerally very meaningful.

The Code suggests that the board’s policyon diversity should be set out in thenomination committee report; where thisis of particular significance it may be thatthe chairman should cover the issue inpart (and of course the chairman of thenomination committee and the companychairman are often the same individual).Our advice on the diversity disclosures isto be frank; if there is a real challenge forsome reason (industry or geography, forinstance) recognise this. Actions to createa pipeline of candidates for seniorpositions are important to draw out too.

The disclosures on the use of externalsearch consultants are an important partof demonstrating a commitment tobreaking down the ‘old boys’ network’and should be done for eachappointment.

Practical guide to corporate governance

Governance reporting – Moving it forward PwC 11

Main principle Disclosure provision Skeletonreportsection

Comments

B.3 All directors shouldbe able to allocatesufficient time tothe company todischarge theirresponsibilitieseffectively.

B.3.1 Any changes to theother significantcommitments of thechairman during the year.

3,4 There are specific (non-disclosure)provisions on making the letters ofappointment of NEDs available, andsetting out in that letter the expectedtime commitment (provision B.3.2).In the year of appointment it can beadvisable to give information on this inthe annual report; otherwise this is likelyto be covered in the board evaluation.

Significant changes to the chairman’sother commitments would likely featurein his or her introduction to thegovernance report with an explanationof how any issues are being handled.

B.4 All directors shouldreceive induction onjoining the board andshould regularly updateand refresh their skillsand knowledge.

2 These are both part of the increasedfocus on the role of the chairman –see main principle A.3 above. They alsonaturally fit within the board evaluationprocess. Long descriptions of processare not necessary.

B.5 The board should besupplied in a timelymanner withinformation in a formand of a qualityappropriate to enable itto discharge its duties.

B.6 The board shouldundertake a formal andrigorous annualevaluation of its ownperformance and that ofits committees andindividual directors.

B.6.1 A statement of howperformance evaluationof the board, its committeesand its directors hasbeen conducted

3 This has become one of the higher profilegovernance disclosures, and we believethat it represents a good opportunity toconfirm that the board has effectivelycarried out its leadership andeffectiveness roles. The Code requiresdisclosure of how the evaluation hasbeen conducted, and this is importantbecause of the range of providers andtechniques used; of most significance,however, are the findings and actionsarising and also how these have beenfollowed up in subsequent periods(though these disclosures are not anexplicit part of the provision).

There are specific requirements aroundthe evaluation of board committees andof individual directors that should not beomitted even if they are outside the mainboard evaluation process.

B.6.2 Where an externalfacilitator has been used,they should be identifiedand a statement made asto whether they haveany other connection tothe company.

3,Appendix

Provided there is no connection, thisdisclosure could be given in thecompliance appendix.

Practical guide to corporate governance

Governance reporting – Moving it forward PwC 12

Main principle Disclosure provision Skeletonreportsection

Comments

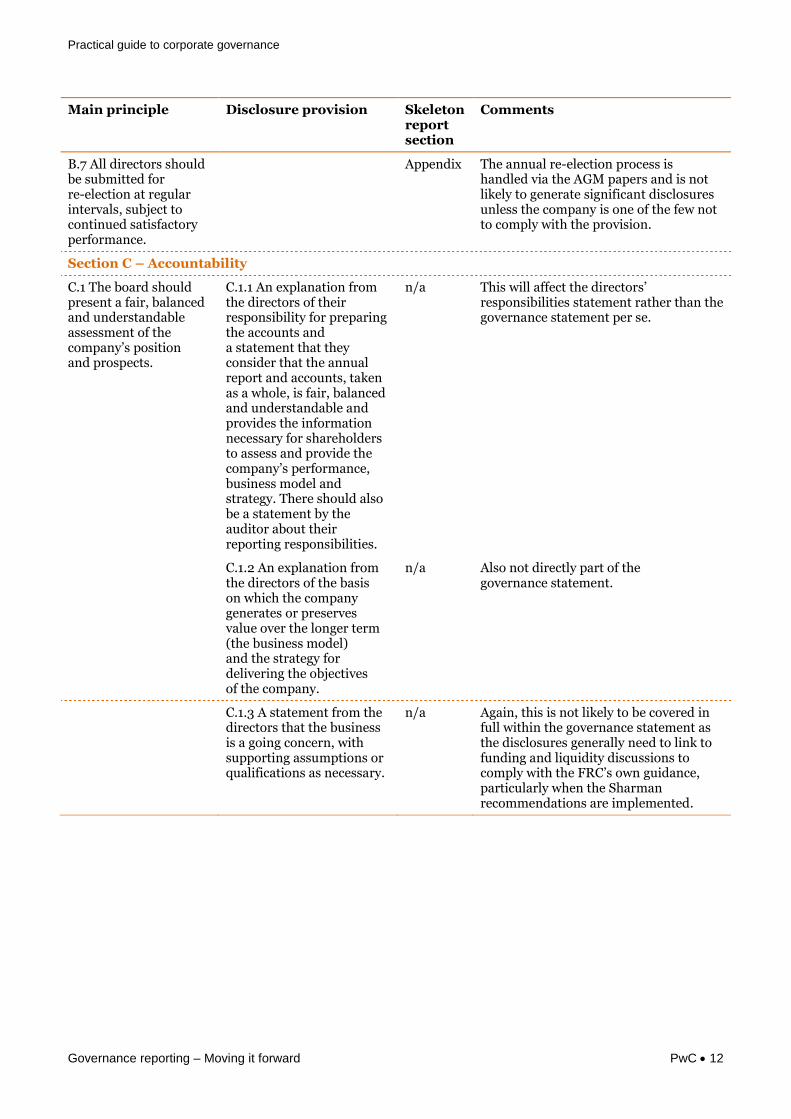

B.7 All directors shouldbe submitted forre-election at regularintervals, subject tocontinued satisfactoryperformance.

Appendix The annual re-election process ishandled via the AGM papers and is notlikely to generate significant disclosuresunless the company is one of the few notto comply with the provision.

Section C – Accountability

C.1 The board shouldpresent a fair, balancedand understandableassessment of thecompany’s positionand prospects.

C.1.1 An explanation fromthe directors of theirresponsibility for preparingthe accounts anda statement that theyconsider that the annualreport and accounts, takenas a whole, is fair, balancedand understandable andprovides the informationnecessary for shareholdersto assess and provide thecompany’s performance,business model andstrategy. There should alsobe a statement by theauditor about theirreporting responsibilities.

n/a This will affect the directors’responsibilities statement rather than thegovernance statement per se.

C.1.2 An explanation fromthe directors of the basison which the companygenerates or preservesvalue over the longer term(the business model)and the strategy fordelivering the objectivesof the company.

n/a Also not directly part of thegovernance statement.

C.1.3 A statement from thedirectors that the businessis a going concern, withsupporting assumptions orqualifications as necessary.

n/a Again, this is not likely to be covered infull within the governance statement asthe disclosures generally need to link tofunding and liquidity discussions tocomply with the FRC’s own guidance,particularly when the Sharmanrecommendations are implemented.

Practical guide to corporate governance

Governance reporting – Moving it forward PwC 13

Main principle Disclosure provision Skeletonreportsection

Comments

C.2 The board isresponsible fordetermining the natureand extent of thesignificant risks itis willing to take inachieving its strategicobjectives. The boardshould maintain soundrisk managementand internalcontrol systems.

C.2.1 A report that theboard has conducted areview of the effectivenessof the company’s riskmanagement and internalcontrols systems.

5 The FRC’s Turnbull Guidance providesassistance with implementing thisprovision; the disclosures around themain features of the risk managementsystems are often given alongside the riskreporting in the annual report; thedescription of how the annual review ofthe effectiveness of internal control hasbeen conducted is usually included in theaudit committee report. The disclosuresgenerated are often less insightful thanthe main risk disclosures – this maychange when the Turnbull Guidance isreviewed later in 2013.

The ‘nature and extent of the significantrisks’ refers to the company’s ‘riskappetite’; this is most relevant forfinancial services companies, most ofwhich have a separate risk committeeand risk committee reporting.

There is a current focus on thegovernance applied to subsidiaries at thepresent time, and the FSA alsochallenges regulated entities on this.Disclosures should demonstrate thatappropriate arrangements are in place atsignificant operations around the group.

C.3 The board shouldestablish formal andtransparentarrangements forconsidering how theyshould apply thecorporate reporting,risk management andinternal controlprinciples and formaintaining anappropriaterelationship with thecompany’s auditors.

C.3.6 Where there is nointernal audit function, thereasons for the absence ofsuch a function.

Appendix See C.1 and C.2 above for the corporatereporting and risk management andinternal control aspects of this principle.For the relationship with the company’sauditors see provision C.3.8 below.

The disclosures for C.3.6 are likely tosuitable for the compliance appendix.

C.3.7 Where the board doesnot accept the auditcommittee’srecommendation on theappointment,reappointment or removalof an external auditor,a statement from the auditcommittee explaining therecommendation and thereasons why the board hastaken a different position.

5 Unlikely to be an issue, and would becovered by chairman of the auditcommittee (at least) if it arose.

Practical guide to corporate governance

Governance reporting – Moving it forward PwC 14

Main principle Disclosure provision Skeletonreportsection

Comments

C.3.8 A separate sectiondescribing the work of theaudit committee indischarging itsresponsibilities, including:

The significant issuesthat it considered inrelation to the financialstatements, andhow these issueswere addressed

An explanation of howit has assessed theeffectiveness of theexternal audit processand the approach takento the appointment orreappointment of theexternal auditor,including the length oftenure of the currentaudit firm and when atender was lastconducted

If the external auditorprovides non-auditservices, anexplanation of howauditor objectivity andindependenceis safeguarded

5 Note: this requirement for a ‘separatesection’ is not new – it was simplyincluded in a different provision withinthe earlier Codes.

The relationship with the externalauditors is likely to be a focus forinvestors, particularly with the newprovision requiring the external auditcontract to be put out to tender at leastevery ten years on a comply-or-explainbasis. The disclosure of the assessment ofthe effectiveness of the external auditprocess has been strengthened in the2012 Code to include how this was done,and the provision of non-audit services(often including the ratio of non-auditto audit fees and comments thereon)is of course a frequent focus ofinvestor attention.

The ‘significant issues’ reporting of thekey accounting judgements andestimates considered by the auditcommittee has generated considerableattention. PwC has issued a separatePractical Guide to this area6 (and to thefair, balanced and understandablereporting under provision C.1.1 above).

Section D – Remuneration

D.1 Levels ofremuneration should besufficient to attract,retain and motivatedirectors of the qualityrequired to run thecompany successfully,but a company shouldavoid paying more thanis necessary for thispurpose. A significantproportion of executivedirectors’ remunerationshould be structured soas to link rewards tocorporate andindividual performance.

D.1.2 A description of thework of the remunerationcommittee as requiredunder the Large andMedium-Sized Companiesand Groups (Accounts andReports) Regulations 2008,including, where anexecutive director serves asa non-executive directorelsewhere, whether or notthe director will retain suchearnings and, if so, whatthe remuneration is.

n/a This is covered in the remunerationreport, which is outside the scopeof this paper.

6 See http://www.pwc.co.uk/governance-risk-compliance/publications/insight-and-guidance-on-revised-the-uk-corporate-governance-code.jhtml

Practical guide to corporate governance

Governance reporting – Moving it forward PwC 15

Main principle Disclosure provision Skeletonreportsection

Comments

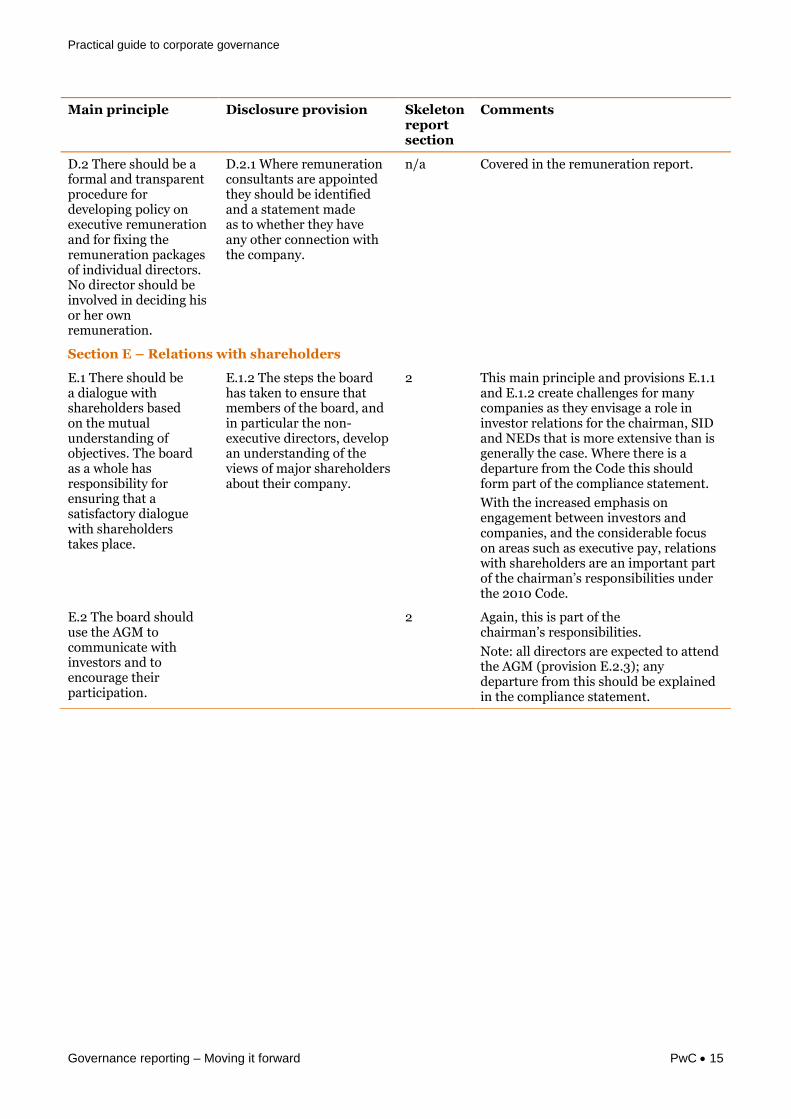

D.2 There should be aformal and transparentprocedure fordeveloping policy onexecutive remunerationand for fixing theremuneration packagesof individual directors.No director should beinvolved in deciding hisor her ownremuneration.

D.2.1 Where remunerationconsultants are appointedthey should be identifiedand a statement madeas to whether they haveany other connection withthe company.

n/a Covered in the remuneration report.

Section E – Relations with shareholders

E.1 There should bea dialogue withshareholders basedon the mutualunderstanding ofobjectives. The boardas a whole hasresponsibility forensuring that asatisfactory dialoguewith shareholderstakes place.

E.1.2 The steps the boardhas taken to ensure thatmembers of the board, andin particular the non-executive directors, developan understanding of theviews of major shareholdersabout their company.

2 This main principle and provisions E.1.1and E.1.2 create challenges for manycompanies as they envisage a role ininvestor relations for the chairman, SIDand NEDs that is more extensive than isgenerally the case. Where there is adeparture from the Code this shouldform part of the compliance statement.

With the increased emphasis onengagement between investors andcompanies, and the considerable focuson areas such as executive pay, relationswith shareholders are an important partof the chairman’s responsibilities underthe 2010 Code.

E.2 The board shoulduse the AGM tocommunicate withinvestors and toencourage theirparticipation.

2 Again, this is part of thechairman’s responsibilities.

Note: all directors are expected to attendthe AGM (provision E.2.3); anydeparture from this should be explainedin the compliance statement.

This publication has been prepared for general guidance on matters of interest only, and does not constitute professionaladvice. You should not act upon the information contained in this publication without obtaining specific professional advice.No representation or warranty (express or implied) is given as to the accuracy or completeness of the information containedin this publication, and, to the extent permitted by law, PricewaterhouseCoopers LLP, its members, employees and agentsdo not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, orrefraining to act, in reliance on the information contained in this publication or for any decision based on it.

© 2013 PricewaterhouseCoopers LLP. All(a limited liability partnership in the United Kingdom), which is a member firm of PricewaterhouseCoopers InternationalLimited, each member firm of which is a separate legal en

130404-113137-SK-OS

This publication has been prepared for general guidance on matters of interest only, and does not constitute professionaladvice. You should not act upon the information contained in this publication without obtaining specific professional advice.

sentation or warranty (express or implied) is given as to the accuracy or completeness of the information containedin this publication, and, to the extent permitted by law, PricewaterhouseCoopers LLP, its members, employees and agents

ume any liability, responsibility or duty of care for any consequences of you or anyone else acting, orrefraining to act, in reliance on the information contained in this publication or for any decision based on it.

© 2013 PricewaterhouseCoopers LLP. All rights reserved. In this document, "PwC" refers to PricewaterhouseCoopers LLP(a limited liability partnership in the United Kingdom), which is a member firm of PricewaterhouseCoopers InternationalLimited, each member firm of which is a separate legal entity.

This publication has been prepared for general guidance on matters of interest only, and does not constitute professionaladvice. You should not act upon the information contained in this publication without obtaining specific professional advice.

sentation or warranty (express or implied) is given as to the accuracy or completeness of the information containedin this publication, and, to the extent permitted by law, PricewaterhouseCoopers LLP, its members, employees and agents

ume any liability, responsibility or duty of care for any consequences of you or anyone else acting, orrefraining to act, in reliance on the information contained in this publication or for any decision based on it.

rights reserved. In this document, "PwC" refers to PricewaterhouseCoopers LLP(a limited liability partnership in the United Kingdom), which is a member firm of PricewaterhouseCoopers International