133

Practice of Banking & Insurance COH 331 HARESH R Asst. Professor Department of Commerce Christ University, Bengaluru

Practice of Banking & Insurance COH 331

HARESH RAsst. Professor

Department of CommerceChrist University, Bengaluru

• Introduction• Classification of Banking Institutions

Banking - Introduction• Banks are the important segment in Indian Financial System. • An efficient banking system helps the nation’s economic

development.• Various categories of stakeholders of the Society use the

banks for their different requirements.• Banks are financial intermediaries between the depositors and

the borrowers. • Apart from accepting deposits and lending money, banks in

today’s changed global business environment offer many more value added services to their clients.

• The Reserve Bank of India as the Central Bank of the country plays different roles like the regulator, supervisor and facilitator of the Indian Banking System.

Introduction – Contd.

• Banks are institutions that take care of the money of individuals and corporates, provide loans to people for business or personal use.

• They also offer a wide range of services like exchange of foreign currency, Investment Banking, Mutual Funds, Insurance Business, D-mat services, Online trading of shares, providing public utility services like e-tickets, payment of bills, educative services etc.

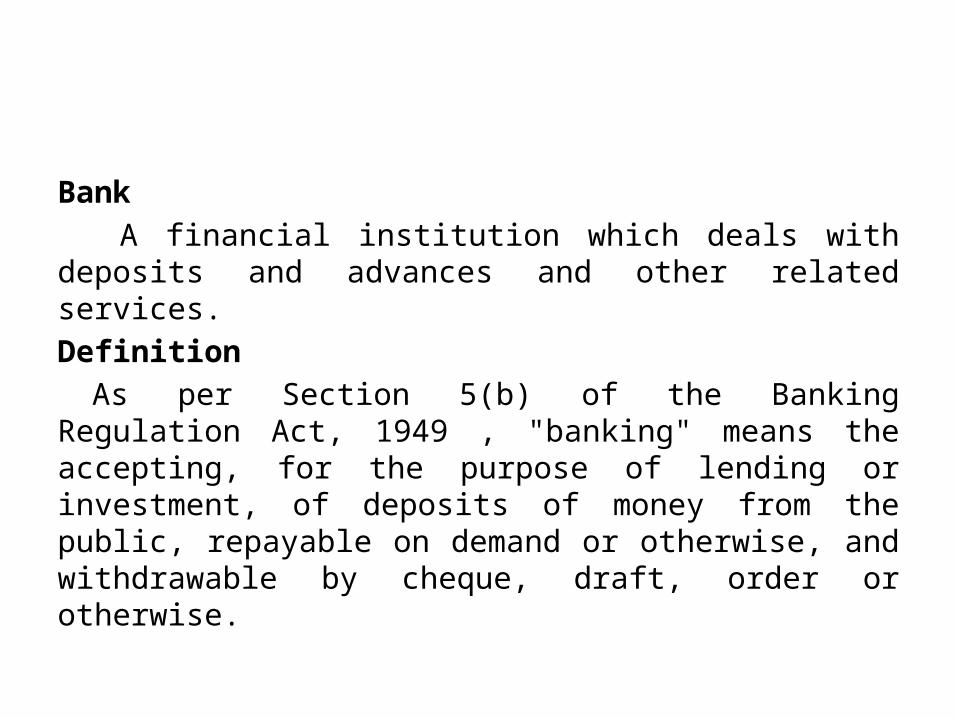

Bank A financial institution which deals with deposits

and advances and other related services.Definition

As per Section 5(b) of the Banking Regulation Act, 1949 , "banking" means the accepting, for the purpose of lending or investment, of deposits of money from the public, repayable on demand or otherwise, and withdrawable by cheque, draft, order or otherwise.

Evolution of Banking• The term bank is either derived from Old Italian word

banca or from a French word banque both mean a Bench or money exchange table.

• European money lenders or money changers used to display (show) coins of different countries in big heaps (quantity) on benches or tables for the purpose of lending or exchanging.

• According to some authorities, the work “Bank” itself is derived from the words “bancus” or “banqee,” that is, a bench.

• The early bankers, the Jews in Lombardy, transacted their business on benches in the market place.

• There are others, who are of the opinion that the word “bank” is originally derived from the German word “back” meaning a joint stock fund, which was Italianized into “banco” when the Germans were masters of a great part of Italy. This appears to be more possible.

• But whatever is the origin of the word ‘bank’, “It would trace the history of banking in Europe from the Middle Ages.”

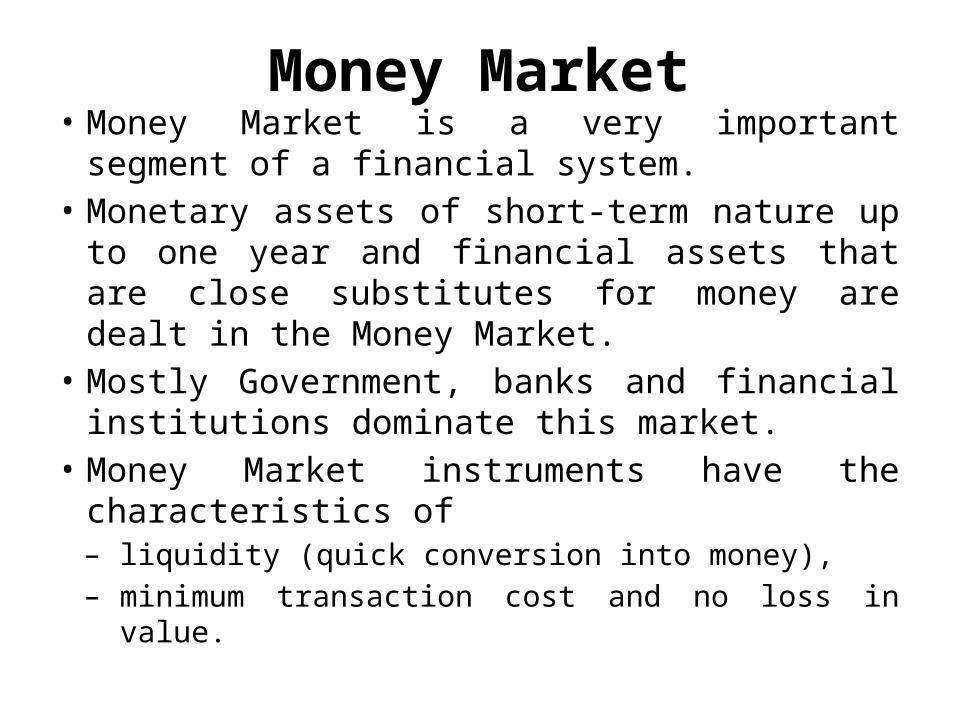

Money Market• Money Market is a very important segment of a

financial system. • Monetary assets of short-term nature up to one

year and financial assets that are close substitutes for money are dealt in the Money Market.

• Mostly Government, banks and financial institutions dominate this market.

• Money Market instruments have the characteristics of – liquidity (quick conversion into money), – minimum transaction cost and no loss in value.

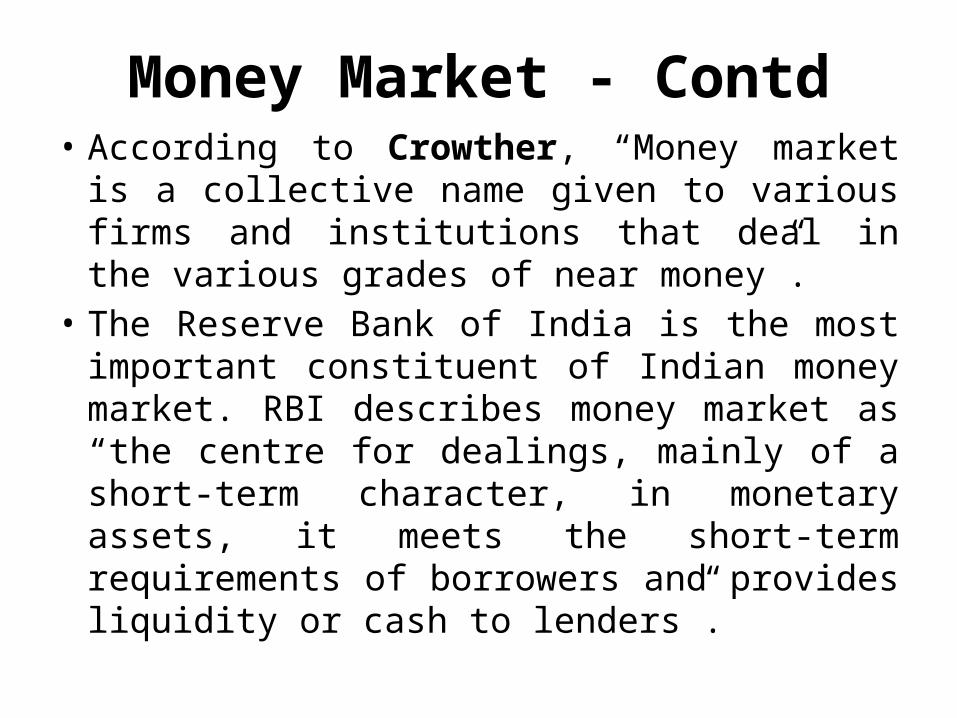

Money Market - Contd• According to Crowther, “Money market is a

collective name given to various firms and institutions that deal in the various grades of near money”.

• The Reserve Bank of India is the most important constituent of Indian money market. RBI describes money market as “the centre for dealings, mainly of a short-term character, in monetary assets, it meets the short-term requirements of borrowers and provides liquidity or cash to lenders”.

Functions of Money MarketMoney market performs the following functions:

1. Facilitating adjustment of liquidity position of commercial banks, business undertakings and other non-banking financial institutions.2. Enabling the central bank to influence and regulate liquidity in the economy through its intervention in the market and control on the creation of credit.3. Providing a reasonable access to users of short term funds to meet their requirements quickly at reasonable costs.4. Providing short term funds to government institutions.

Functions of Money Market

5. Enabling businessmen to invest their temporary surplus funds for short period.6. Facilitating flow of funds to the most important uses.7. Money market plays a crucial role in financing both internal as well as international trade.8. Money market provides short-term funds to businessmen, industrialists, traders etc. to meet their day-to-day requirements of working capital.

Players in Money Market

• Central Bank(RBI)• Government• Financial Institutions/Institutional Investors• Corporates, Private Individuals, Partnerships

and companies.• Mutual Funds• FII’s (Foreign Institutional Investors)

MONEY MARKET INSTRUMENTS– Government Securities– Gilt-edged (Government ) Securities– Repo Market– Money at Call and Short Notice– Bills Rediscounting– Money Market Mutual Funds– Call Money Market and Short-term Deposit Market– Treasury Bills– Certificates of Deposits– Inter-Corporate Deposits– Commercial Bills– Commercial Paper

Structure of the Money Market

Reserve Bank of India (RBI)• Central Bank of our country. • Financial and monetary system. • RBI came into existence on 1st April, 1935 as per the RBI act

1935. • Nationalised by the government after Independence. • It became the public sector bank from 1st January, 1949. • Thus, RBI was established as per the Act 1935 and

empowerment took place in banking regulation Act 1949. • RBI has 4 local boards basically in North, South, East and West

– Delhi, Chennai, Calcutta, and Mumbai.• It issues notes, buys and sells government securities, regulates

the volume, direction and cost of credit, manages foreign exchange and acts as banker to the government and banking institutions.

• An active role in the development activities by helping the establishment and working of specialised institutions, providing term finance to agriculture, industry, housing and foreign trade.

Functions of the RBI

• According to the preamble of the Reserve Bank of India Act, the main functions of the bank is “to regulate the issue of bank notes and the keeping of reserves with a view to securing monetary stability in India and generally to operate the currency and credit system of the country to its advantage.”

Functions of the RBI – Contd.

The functions of RBI can be conveniently classified in three parts as follows:– Traditional Central Banking Functions– Promotional functions– Supervisory functions

Traditional Central Banking Functions

• Monopoly of Note Issue• Banker to the Government• Banker’s Bank• Lender of the Last Resort• National Clearing House• Credit Control• Custodian of foreign exchange reserve• Collection of data and publication

Promotional Functions• Promotion of commercial banking• Promotion of co-operative banking• Promotion of agricultural and rural credit• Promotion of industrial finance• Promotion of finance for exports.

Supervisory Functions• Licensing of Banks• Approval of Capital, Reserves and Liquid Assets of Bank• Branch Licensing Policy• Inspection of Banks• Control Over Management• Control Over Methods ( Operation of banks)• Audit• Credit Information Service• Control Over Amalgamation and Liquidation• Deposit Insurance• Training and Banking Education

Credit Control

• Commercial Banks Loans & advance creates credit or bank deposits excessive creation of credit leads to inflation excessive contraction of credit leads to deflation central bank has to control and regulate the availability of credit, the cost of credit and the use of credit flow in the economy.

Methods of Credit Control

• Quantitative or General Methods– Bank Rate ( “the standard rate at which it (the Bank) is

prepared to buy or rediscount bills of exchange or other commercial paper eligible for purchase under the Act.”)

– Open Market Operations (Direct buying and selling of government securities by the central bank)

– Cash-Reserve Requirement (CRR)– Statutory Liquidity Ratio (SLR)

Methods of Credit Control• Qualitative or Selective Credit Control

Methods – Variation of Margin Requirements – Credit Authorisation Scheme (CAS)– Control of Bank Advances– Differential Interest Rates– Credit Squeeze Policy– Moral Suasion

Classification of Banking Institutions• Apex Banking Institutions( IDBI, NABARD,

EXIM, IRBI, NHB)• Banking Institutions– Commercial Banks• Public sector banks

– State Bank Group – Nationalised Banks

• Private Sector Banks– Indian Banks– Foreign Banks

– Regional Rural Banks

• Co-operative Banks– Primary Credit Societies• Primary Agricultural Credit Societies• Primary Urban Co-operative Banks

– Secondary Credit Institutions• Central or District Co-operative Banks• State Co-operative Banks

• Development Banks– All India Level Development Banks• Industrial Finance Corporation of India• Industrial Credit & Investment Corporation of India• Small Industries Development Bank of India

– State Level Development Banks• State Finance Corporations• State Industrial Development Corporations• North Eastern Development Finance Corporation Ltd.

• Investment Institutions– Life Insurance Corporation of India– General Insurance Corporation of India– Unit Trust of India

• Credit Guarantee Institutions– Export Credit & Guarantee Corporation of India– Deposit Insurance & Credit Guarantee Corporation

of India

• Money Market Institutions– Discount & Finance House of India Ltd.– Stock Holding Corporation of India Ltd.– Securities Trading Corporation of India Ltd.

• Credit Rating Institutions– Credit Rating Information & Services of India Ltd.

(CRISIL)– Investment Information & Credit Rating Agency of

India (ICRA)– Credit Analysis & Research Ltd. (CARE)

Banking System in IndiaThe constituents of the Indian Banking System can be broadly listed as under :(a) Commercial Banks:

(i) Public Sector Banks(ii) Private Sector Banks(iii) Foreign Banks

(b) Cooperative Banks:(i) Short term agricultural institutions(ii) Long term agricultural credit institutions(iii) Non-agricultural credit institutions

(c) Development Banks:(i) National Bank for Agriculture and Rural Development (NABARD)(ii) Small Industries Development Bank of India (SIDBI)(iii) EXIM Bank(iv) National Housing Bank

Commercial Banks• A FI which accepts deposits against which

cheques can be drawn, lends money to commerce and industry and renders a number of other useful services to the customers and the society.

• The commercial banks may be owned by government or owned by private sector. For eg: Canara Bank, Punjab National Bank, Lakshmi Vilas Bank, Karur Visya Bank etc., are called as commercial banks.

Commercial banks

• Receive deposits in the form of fixed deposits, savings bank accounts and current accounts and advance money, generally for short periods, in the form of cash credits, overdrafts and loans.

• They also render a number of service to their customers, such as collection of cheques, safe custody of valuables, remittance facilities and payment of insurance premium, electricity bills, etc.

• Public Sector Banks: These types of banks are owned and controlled by the government. The nationalized banks and regional rural banks come under this category.

• Private sector Banks: These Banks are owned by private individuals and corporations.

FUNCTIONS OF COMMERCIAL BANKS

Sections 5 & 6 of Banking Regulation Act, 1949 contain the functions which a commercial banks can transact.These functions can be divided into two parts:(a) Major functions(b) Other functions/ancillary services(a) Major functions:(i) Accepting Deposits(ii) Granting Advances

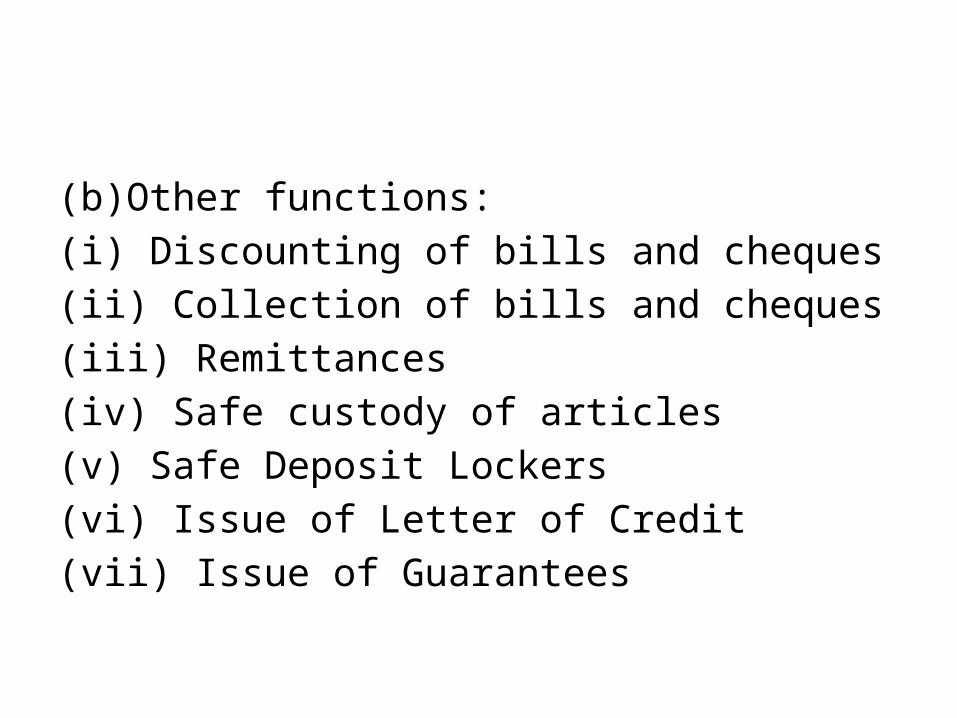

(b)Other functions:(i) Discounting of bills and cheques(ii) Collection of bills and cheques(iii) Remittances(iv) Safe custody of articles(v) Safe Deposit Lockers(vi) Issue of Letter of Credit(vii) Issue of Guarantees

• Besides the above functions, Banks now-a-days associate themselves in the following activities also either by opening separate departments or through separately floated independent subsidiaries:

(i) Investment Counseling(ii) Investment Banking(iii) Mutual Fund(iv) Project Appraisal(v) Merchant Banking Services(vi) Taxation Advisory Services(vii) Executor Trustee Services

(viii) Credit Card Services(ix) Forex Consultancy(x) Transactions of Government Business(xi) Securities Trading(xii) Factoring(xiii) Gold/Silver/Platinum Trading(xiv) Venture Capital Financing(xv) Bankassurance - Selling of Life and General Insurance policies as Corporate Agent

Co-operative Banks

• These banks are operated on cooperative principles. It is a voluntary association of members for self-help and caters to their financial needs on a mutual basis. These banks are also subject to control and inspection by Reserve Bank of India.

• The main function of co-operative banking is to link the farmers with the money markets of the country.

Banking

• The term banking is defined as per Banking Regulation Act 1949 Sec 5(i) (b), “as acceptance of deposits of money from the public for the purpose of lending and/or investment. Such deposits can be repayable on demand or otherwise and withdraw able by means of cheque, drafts, order or otherwise.”

Characteristics of Banking Business

• Acceptance of deposits from public• For the purpose of lending or investment• Repayable on demand or otherwise• Withdrawable by means of any

instrument whether a cheque or otherwise.

FUNCTIONS OF COMMERCIAL BANKS

‘General Banking’ functions of the commercial banks.

Primary FunctionsSecondary Functions

Commercial Banks

Primary Functions

Acceptance of Deposits

Lending of Funds

Overdraft

Cash Credi

t

Discounting Trade Bills

Money at Call

Term Loans

Consumer

Credit

Miscellaneous Advanc

es

Creation of Credit

Clearing of Cheques

Financing Foreign trade

Remittance of Funds

Secondary Functions

Agency Services

General Utility Services

A. Primary Functions

1. Acceptance of deposits2. Lending of Funds3. Creation of credit 4. Clearing of cheques 5. Financing foreign trade 6. Remittance of funds

1. Acceptance of Deposits

• Main source of funds for commercial banks.• Bank mobilise savings of the household sector.• Banks receives the idle savings of people in the

form of deposits and finances the temporary needs of commercial and industrial firms.

• The bank acts as an intermediary by accepting deposits and paying interest on them and making loans and charging the borrowers interest at a higher rate.(Profit/Spread)

Commercial bank accepts following types of deposits.

a) Demand depositsb) Time deposits

Demand Deposits

• Deposits, which are withdrawn by depositor at any time without previous notice.

• It is withdrawable by cheque/draft.• They are in two forms – Current account deposits– Savings account deposits.

Current Deposits• RBI defines current account as “ a form of demand deposit wherefrom

withdrawals are allowed for any number of times depending upon the balance in the account or upto a particular agreed amount and shall also deemed to include other deposit account that are neither a savings deposit or a term deposit.”

Features• Short term deposits or demand deposits• Generally, no interest is allowed on current deposits. However some banks offer

interest.• Businessmen, industrialists and people who meet a large number of monetary

transactions in their routine.• Incidental charges on the customer for the services rendered.• Overdraft facilities are also available on current account. • The current accounts do not have any fixed maturity as these are on continuous

basis accounts

Saving Bank Deposits

• Savings account is defined as “ a deposit account, which is subject to restrictions as to the number of withdrawals as also the amount of withdrawals permitted by the bank during any specified period.”

• Can be held by individuals and non-profit institutions.• The rate of interest allowed on saving bank deposits

is less than that on fixed deposits. • Depositor is given a pass book and a cheque book.

Withdrawals are allowed by cheques and withdrawal form.

Bank Interest Rate on Savings Deposit

Citibank 7.25%

Yes Bank, Kotak Mahindra 6%

IndusInd 5.5%

SBI, IDBI, PNB, ICICI, AXIS, HDFC 4%

• W.e.f. 25th October, 2011, RBI has deregulated Saving Fund account interest rates and now banks are free to decide the same within certain conditions imposed by RBI.

• Under directions of RBI, now banks are also required to open no frill accounts (this term is used for accounts which do not have any minimum balance requirements).

Time Deposits

• Deposits, which are repayable after a certain period of time, are known as time deposits. They are in two forms: – Recurring Deposits – Fixed Deposits– Cash Certificates

Recurring Deposits(RD)• Popularly known as RD accounts and are special kind of Term Deposits.• Suitable for people who do not have lump sum amount of savings, but are ready to save a

small amount every month.• The person has to usually deposit a fixed amount of money every month (usually a minimum

of Rs,100/- p.m.). • Any default in payment within the month attracts a small penalty. • Fixed installment RD, have also introduced a flexible / variable RD. • These are best if you wish to create a fund for your child's education or marriage of your

daughter or buy a car without loans or save for the future. • Recurring Deposit accounts are normally allowed for maturities ranging from 6 months to

120 months. • A Pass book is usually issued wherein the person can get the entries for all the deposits

made by him / her and the interest earned. • Banks also indicate the maturity value of the RD assuming that the monthly instalments will

be paid regularly on due dates. • Premature withdrawal of accumulated amount permitted is usually allowed (however,

penalty may be imposed for early withdrawals). These accounts can be opened in single or joint names. Nomination facility is also available.

Fixed Deposits

• A fixed or time deposit is defined as “ a deposit received by a bank for a fixed period and which is withdrawable only after expiry of the said fixed period and shall include deposits such as recurring, cumulative, annuity, reinvestment deposits, cash certificates and so on.”

• Fixed period, interest rate is higher, repayable on expiry of the period.

Cash Certificates

• Issued to public for a longer period of time.• Maturity value is in multiples of sum invested.• Attractive and highly yielding to meet future

financial requirements.• Cash certificates are generally issued at a

discount to face value. (eg. Rs. 1,00,000 payable after 4 years issued at Rs.25,000)

2. Lending of Funds• Overdraft• Cash Credit• Discounting of Bills• Loans and Advances• Money at call• Housing Finance• Educational Loan Scheme• Loans against shares/securities• Loans against savings certificates.(NSC, FDR,IVP)• Consumer loans and advances• Securitisation of loans( transferring a part of credit risk – non liquid asset

into liquid asset)• Others (Jewellery loans, venture capital loans)

Overdraft

• Current account holders enjoy this facility.• Customer can withdraw money over and above

the balance in his account.• “the act of overdrawing from a bank account.”• An extension of credit from a lending institution

when an account reaches zero. • An overdraft allows the individual to continue

withdrawing money even if the account has no funds in it.

Cash Credit

• Cash credit is the most popular method of lending by the banks in India.

• Under cash credit system, a limit, called the credit limit is specified by the bank. A borrower is entitled to borrow upto that limit.

• It is granted against the security of tangible assets or guarantee. The borrower can withdraw money, any number of times upto that limit.

• He can also deposit any amount of surplus funds with him from time to time. He is charged interest on the actual amount withdrawn and for the period such amount is drawn.

Discounting of Bills

• It is another important way of giving loans. The bank provides the customers with the facility of purchasing and discounting their bills receivable.

• After the maturity of the bills, the banks get back its full value. Thus these bills are good liquid assets and moreover this investment is also very safe.

Loans & AdvancesLoans– A loan is granted for a specific time period. The

borrower may withdraw the entire amount in lumpsum or in instalments. However, interest is charged on the full amount of loan.

– Loans are generally granted against the security of certain assets. A loan may be repaid either in lumpsum or in instalments.

Advances• An advance is a credit facility provided by the

bank to its customers.• Advances are normally granted for a short

period of time. The purpose of granting advances is to meet the day to day requirements of business.

• The rate of interest charged on advances varies from bank to bank. Interest is charged only on the amount withdrawn and not on the sanctioned amount.

• Clean, Secured, Unsecured Loans and Advances.

• Loans – Demand Loans, Term Loans(Short, Medium & Long Term)

• Personal, Business, Education, Gold, Housing, Vehicle, Loan against Insurance Policy, Loan against PPF.

3. Credit Creation

• It is a unique function of Commercial Banks. • Primary Deposit , Derivative Deposit.• Whenever a bank grants loan, it creates an equal

amount of bank deposits. Creation of deposits is called Credit Creation.

• In simple words we can define Credit creation as multiple expansions of deposits.

• Methods of credit creation by banks include loans & advances, money at call & short notice, discounting of bills, investments.

4. Clearing of Cheques

• A cheque is nothing but an instruction to the bank by the account holder to pay money to someone or to the account holder herself.

• It is evident that the use of cheques for settling any transaction, is much more convenient than the use of cash.

5. Financing Internal and Foreign Trade

• The bank finances internal and foreign trade through discounting of exchange bills.

• Sometimes, the bank gives short-term loans to traders on the security of commercial papers.

• This discounting business greatly facilitates the movement of internal and external trade.

6. Remittance of Funds

• Commercial banks, on account of their network of branches throughout the country, also provide facilities to remit funds from one place to another for their customers by issuing bank drafts, mail transfers or telegraphic transfers on nominal commission charges.

Secondary FunctionsAgency Services Banks also perform certain agency functions for and on behalf of their customers.

• Collection and Payment of Credit Instruments• Execution of Standing Orders (payment of rent,

insurance premium, etc.)• Purchase and Sale of Securities• Collection of Dividends on Shares• Acts as Correspondent, Trustee and Executor • Deal in foreign exchange transactions• To accept tax proceeds, tax returns and to provide

Income-tax Consultancy

General Utility Services• Locker facility• Traveller’s cheques • Credit cards, Debit cards and Smart cards• Letter of Credit• Collection of Statistics• Money transfer facility• Acting as a Referee• Underwriting Securities• Gift cheques• Insurance related services• Wealth management services• Accepting Bills of Exchange on Behalf of Customers• Merchant Banking functions

PLASTIC CARDS

CREDIT CARDDEBIT CARD

SMART CARD…

History of Credit Cards• 3000 B.C. the term “credit” was first used in

Assyria, Babylon and Egypt .• 1887 – Socialist writer Edward Bellamy used

the phrase “Credit Card” in his novel “Looking Backward”.

CREDIT CARDS

• A form of money that provides both the capacity to buy goods and services and the capacity to borrow funds (i.e., gain access to credit).

• The term “credit card” usually/generally refers to – a plastic card assigned to a cardholder, – with a credit limit, that can be used to purchase goods

and services on credit or obtain cash advances.

• Credit card purchases normally become payable after a free credit period, during which no interest or finance charge is imposed.

• Interest is charged on the unpaid balance after the payment is due.

• Cardholders may pay the entire amount due and save on the interest that would otherwise be charged.

• Alternatively, they have the option of paying any amount, as long as it is higher than the minimum amount due, and carrying forward the balance.

1. Issuing Bank Logo2. EMV chip (only on "smart cards")3. Hologram4. Card number

5. Card Network Logo6. Expiration Date7. Card Holder Name8. Contactless Chip

1. Magnetic Stripe

2. Signature Strip

3. Card Security Code

Parties Involved in Credit Card Processing

• Cardholders - persons who are authorized to use credit cards for the payment of goods and services;

• Card issuers - institutions which issue credit cards;• Merchants - entities which agree to accept credit cards for

payment of goods and services;• Merchant acquirers – Banks/NBFCs which enter into

agreements with merchants to process their credit card transactions; and

• Credit card associations - organisations that license card issuers to issue credit cards under their trademark, e.g. Visa and MasterCard, and provide settlement services for their members (i.e. card issuers and merchant acquirers).

Types of credit cards

• Credit cards can be broadly categorised into two types:– General purpose cards: issued under the trademark of

credit card associations (VISA and Mastercard) and accepted by many merchants

– Private label cards: only accepted by specific retailers (e.g. a departmental store).

• General purpose credit cards are normally categorised by banks as platinum, gold or classic to differentiate the services offered on each card and the income eligibility criteria.

Funds Transfer MechanismNEFTRTGS

NEFT• National Electronic Funds Transfer (NEFT) • a nation-wide payment system facilitating one-to-one funds transfer. • individuals, firms and corporates can electronically transfer funds

from any bank branch to any individual, firm or corporate having an account with any other bank branch in the country participating in the Scheme.

• cash remittances will be restricted to a maximum of Rs.50,000/- per transaction.

• customers have to furnish full details including complete address, telephone number, etc.

• NEFT operates in hourly batches - there are twelve settlements from 8 am to 7 pm on week days (Monday through Friday) and six settlements from 8 am to 1 pm on Saturdays.

IFSC

• IFSC or Indian Financial System Code• an alpha-numeric code that uniquely identifies a bank-branch

participating in the NEFT system. • IFSC is used by the NEFT system to identify the originating /

destination banks / branches and also to route the messages appropriately to the concerned banks / branches.

• This is an 11 digit code with – the first 4 alpha characters representing the bank, and– the last 6 characters representing the branch. – The 5th character is 0 (zero).

RTGS

• Real Time Gross Settlement• the continuous (real-time) settlement of funds transfers

individually on an order by order basis.• 'Real Time' means the processing of instructions at the time

they are received rather than at some later time; 'Gross Settlement' means the settlement of funds transfer instructions occurs individually (on an instruction by instruction basis).

• The RTGS system is primarily meant for large value transactions. The minimum amount to be remitted through RTGS is Rs. 2 lakh. There is no upper ceiling for RTGS transactions.

ECS• ECS is an electronic mode of payment / receipt for

transactions that are repetitive and periodic in nature. • ECS is used by institutions for making bulk payment of

amounts towards distribution of dividend, interest, salary, pension, etc.,(ECS credit) or for bulk collection of amounts towards telephone / electricity / water dues, cess / tax collections, loan installment repayments, periodic investments in mutual funds, insurance premium etc. (ECS debit).

• Essentially, ECS facilitates bulk transfer of money from one bank account to many bank accounts or vice versa.

MICR

• MICR is an acronym for Magnetic Ink Character Recognition.

• The MICR Code is a numeric code that uniquely identifies a bank-branch participating in the ECS Credit scheme.

• This is a 9 digit code to identify the location of the bank branch; – the first 3 characters represent the city, – the next 3 the bank and– the last 3 the branch.

• The MICR Code allotted to a bank branch is printed on the MICR band of cheques issued by bank branches.

Core Banking Solutions(CBS)

• CBS is networking of branches, which enables customers to operate their accounts, and avail banking services from any bank on CBS network, regardless of where they maintain their account.

• The customer is no more the customer of a particular bank. Thus, CBS is a step towards enhancing customer convenience through “Anywhere and Anytime Banking “.

Objectives of CBS

• To increase the number of customers• To provide multiple delivery channels like

internet, mobile banking, ATMs, thereby bringing access to financial services to the doorsteps of the customers

• To enable faster fund transfers to reach out to more customers

• To become one stop solution for financial inclusion initiatives of the Government of India

Benefits of CBS

• Anytime and Anywhere banking • Standardised, simple and automated processes • Increase in quality of the service provided to the customers • Timely and accurate information for management decision

making• Strong audit and internal controls • Bring down the cost of transaction and thereby improving

operational efficiency • Paving way for new value added services thereby

generating additional revenue for the Department

Cheques• Cheques? Used to withdraw money from bank• A negotiable instrument.• According to Sec.6 of the Negotiable

Instruments Act defines, “ a cheque is a bill of exchange drawn on a specified banker and not expressed to be payable otherwise than on demand and it includes the electronic image of a truncated cheque and a cheque in the electronic form.”

A cheque is defined in Sec 6 of NI Act as under :-– A cheque is a bill of exchange – Drawn on a specified banker– Payable on demand– Electronic image of a truncated cheque is

recognized under law. The Information Technology Act, 2002 recognizes (a) digital signatures and (b) electronic transfer as well

Features of a Cheque

• Unconditional written order• Parties to a cheque• Date of the cheque(validity)• Amount• Signature

Parties to a ChequeDrawer

Drawer

Payee

Cheque

CTS

• Truncation is the process of stopping the flow of the physical and an electronic image of the cheque is transmitted to the paying branch through the clearing house, along with relevant information like data on the MICR band, date of presentation, presenting bank, etc.

CTS 2010

• In the year 2010, RBI came up with the guidelines for Cheque Truncation system. (CTS 2010)

• The banks would need to upgrade a few things to comply with CTS 2010 standards of RBI.

• Banks to have scanners and install special software provided by RBI, to securely transfer and receive the scanned image and data.

• Changes in the color-scheme of cheque books so that signature and handwriting is visible in the scanned image.

Benefits of Cheque Truncation

• Eliminates the time, money and manpower wasted during physical movement of cheques (from banks to clearing house).

• Cheque Truncation =faster clearing = better service to customers

• Cheque Truncation system reduces the scope for clearing-related frauds

• There is no fear of losing cheque in transit.

BANKER & CUSTOMER

• Banker– a person or company carrying on the business of

receiving moneys, and – collecting drafts, for customers subject to the

obligation of honouring cheques drawn upon them from time to time by the customers to the extent of the amounts available on their current accounts.

• Customer– In the ordinary language, a person who has an account in a bank is

considered its customer.(a) There must be some recognizable course or habit of dealing between the customer and the banker.(b) The transactions must be in the form of regular banking business.

– According to Dr. Hart “a customer is one who has an account with a banker or for whom a banker habitually undertakes to act as such.”

– The word ‘customer’ has been derived from the word ‘custom’, which means a ‘habit or tendency’ to do certain things in a regular or a particular manner’s .

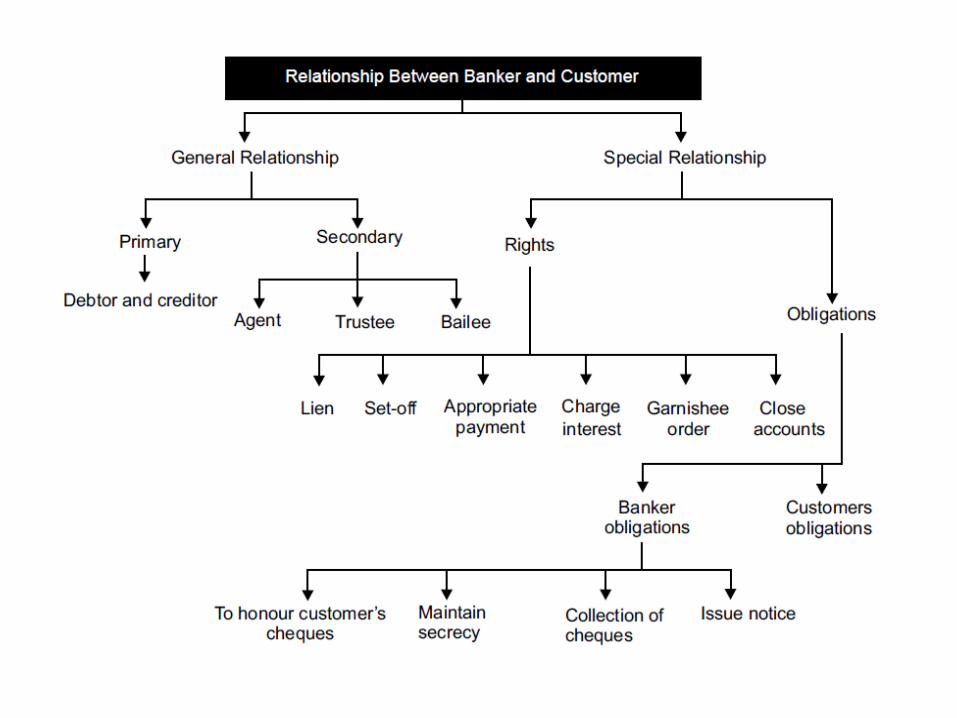

Relationship Between Banker and Customer

• Depends on the activities; products or services provided by bank to its customers or availed by the customer.

• Transactional relationship. • Strong bondage with the customer. • “Trust” plays an important role in building

healthy relationship between a banker and customer.

Bank customers

• Existing customers.• Former Customers• Those who do not maintain any account

relationship with the bank but frequently visit branch of a bank for availing banking facilities such as for purchasing a draft, encashing a cheque, etc.

• Prospective/ Potential customers

Duration Theory

• Single transaction with banker is enough to constitute a customer.(Ladbroke & Co., vs. Todd(1914), Commissioner of Taxation vs. English Scottish and Irish Bank Ltd.(1920)).

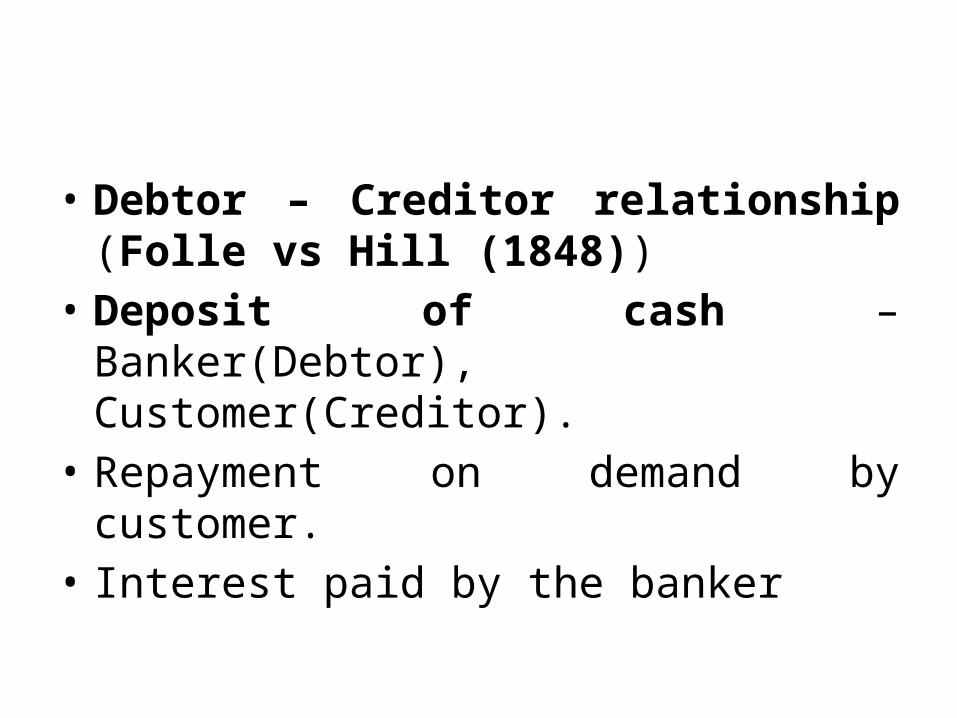

• Debtor – Creditor relationship (Folle vs Hill (1848))

• Deposit of cash – Banker(Debtor), Customer(Creditor).

• Repayment on demand by customer. • Interest paid by the banker

• Loan from Bank, Cash Credit facility, Overdraft–Banker(Creditor), Customer(Debtor).

TRANSACTION-RELATIONSHIP

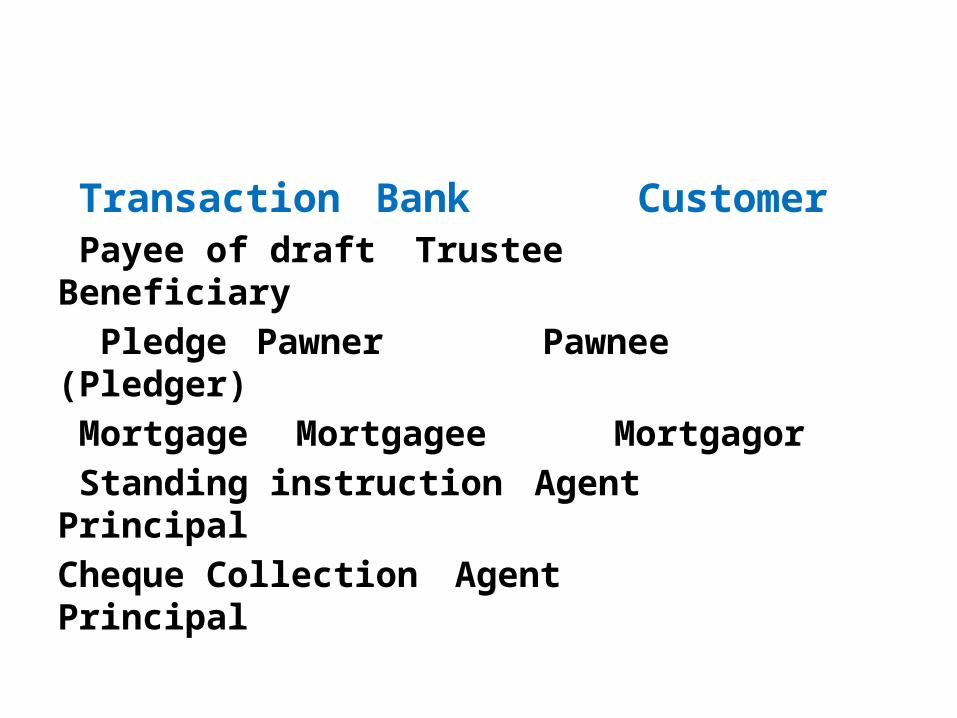

Transaction Bank CustomerDeposits in the bank Debtor CreditorLoan from bank Creditor DebtorLocker Lessor LesseeSafe custody Bailee BailorPurchase of draft Debtor Creditor

Transaction Bank Customer Payee of draft Trustee Beneficiary Pledge Pawner Pawnee

(Pledger) Mortgage Mortgagee Mortgagor Standing instruction Agent PrincipalCheque Collection Agent Principal

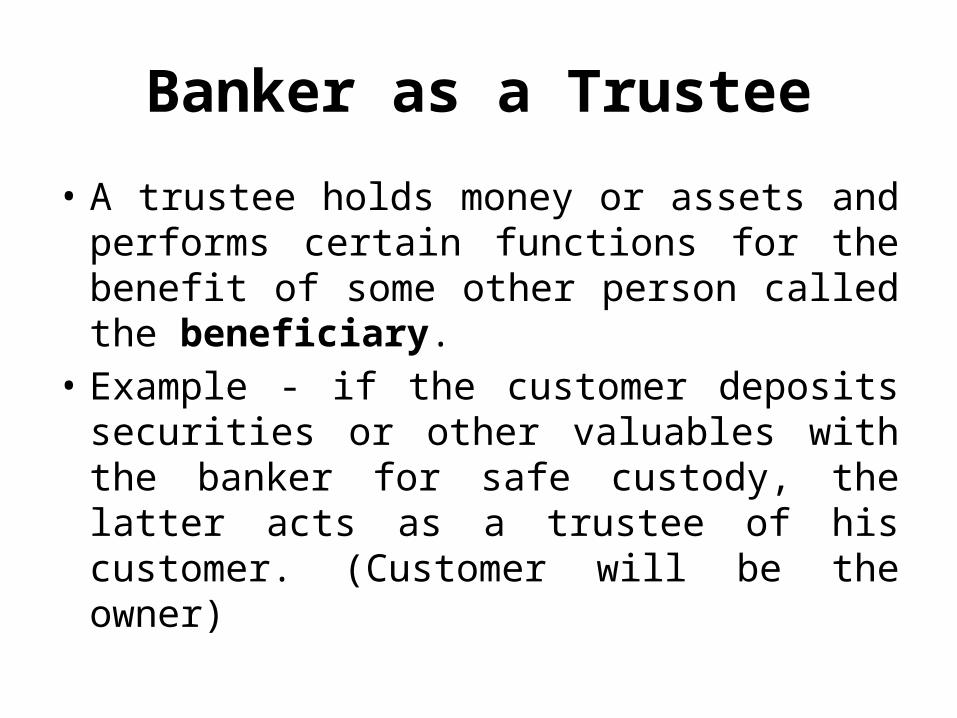

Banker as a Trustee

• A trustee holds money or assets and performs certain functions for the benefit of some other person called the beneficiary.

• Example - if the customer deposits securities or other valuables with the banker for safe custody, the latter acts as a trustee of his customer. (Customer will be the owner)

BANKER AS A BAILOR / BAILEE

• Section 148 of Indian Contract Act,1872• The delivery of goods by one person to another

for some purpose upon a contract. As per the contract, the goods should when the purpose is accomplished, be returned or disposed off as per the directions of the person delivering the goods.

• The person delivering the goods is called the bailor and the person to whom the goods are delivered is called the bailee.

• Banks secure their loans and advances by obtaining tangible securities.

• In such loans and advances, the collateral securities are held by banks and the relationship between banks and customers are that of bailee (bank) and bailor(borrowing customer).

BANKER AS A LESSER / LESSEE

• Section 105 of ‘Transfer & Property Act’ deals with lease, lesser, lessee.

• Banks lease the safe deposit lockers to the clients on hire basis. Banks allow their locker account holders the right to enjoy (make use of ) the property for a specific period against payment of rent.

OBLIGATIONS OF A BANKER

• Obligations to honour the cheques.• Obligation to maintain secrecy of customer’s

account.• Obligation to render proper accounts of

deposits made and withdrawn by customers.• Obligation to give reasonable notice before

closing the customer’s accounts.

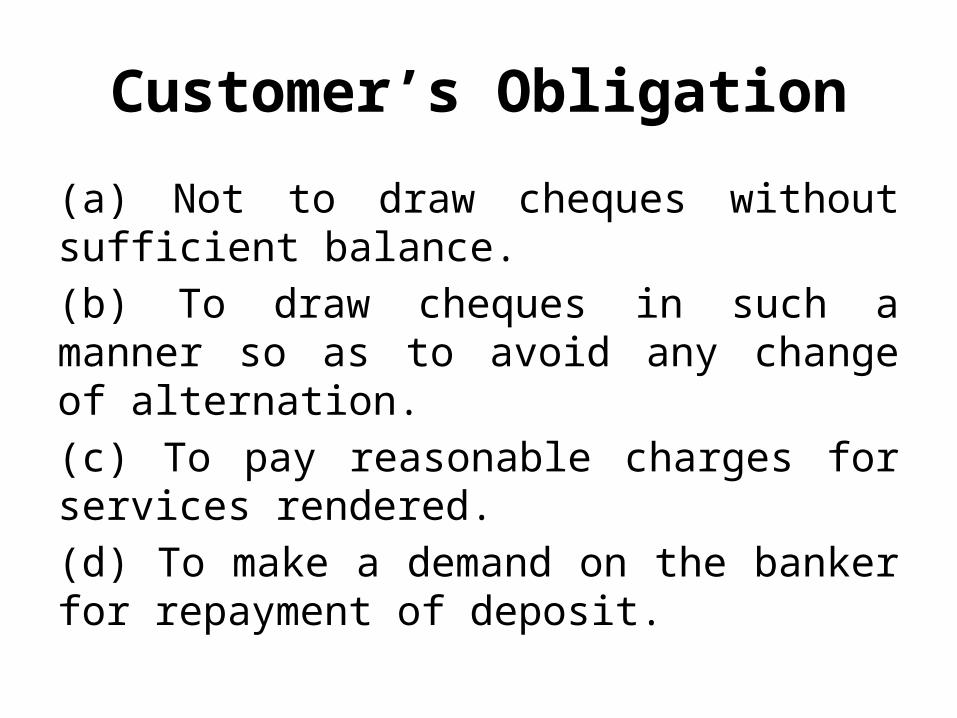

Customer’s Obligation

(a) Not to draw cheques without sufficient balance.(b) To draw cheques in such a manner so as to avoid any change of alternation.(c) To pay reasonable charges for services rendered.(d) To make a demand on the banker for repayment of deposit.

Garnishee Order

• If a debtor fails to pay the debt owed to his creditor, the latter may apply to the Court for the issue of a Garnishee Order on the banker of his debtor.

• The account of the customer with the banker, thus, becomes suspended and the banker is under an obligation not to make any payment from the account concerned after the receipt of the Garnishee Order.

Rights of a Banker

1. Right of general lien2. Right of set-off3. Right to appropriation4. Right to charge interest, incidental charges5. Right not to produce books of accounts6. Right to close accounts

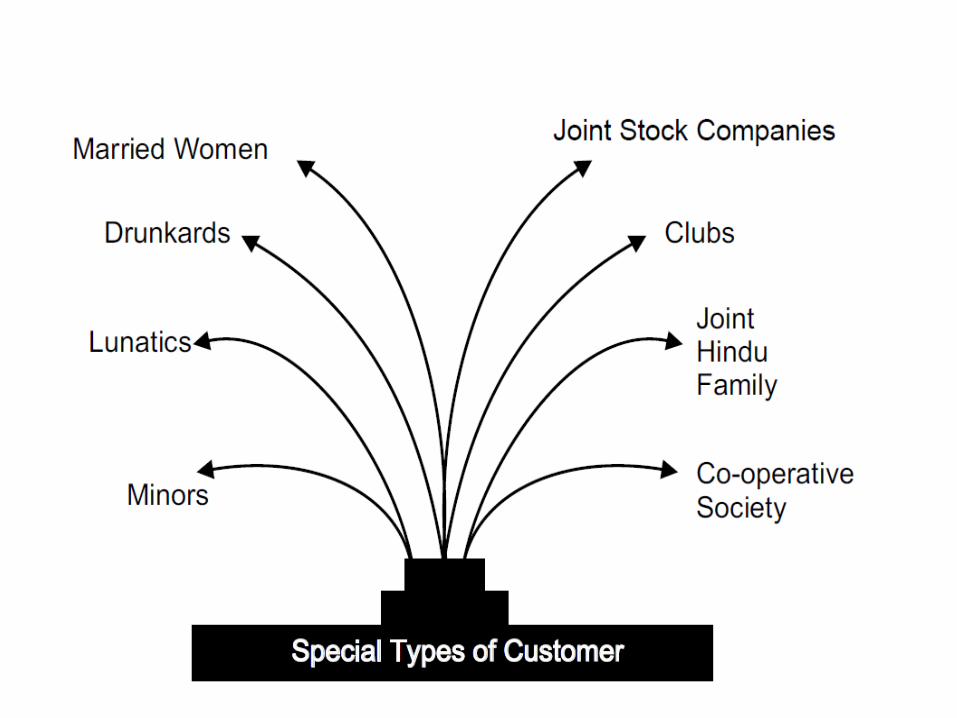

VARIOUS TYPES OF CUSTOMERS

• Minors• Joint Account Holders• Illiterate Persons• Hindu Undivided Family (HUF)• Firms• Companies• Trusts• Clubs• Local Authorities• Co-operative societies

TERMINATION OF BANKER-CUSTOMER RELATIONSHIP

• Voluntary Termination• Bank desires to close the account(Un-

operated A/c, not a desirable customer)• Termination by law– Death– Bankruptcy– Garnishee order– Insanity

CUSTOMER GRIEVANCES BANKING OMBUDSMAN

Bank’s Lending

• Deposits – repayable – interest – on demand.• Banks – deploy deposit money in – investments

– lend loans – keeping apart some reserves.• While lending banks must take into account

risks inherent. So certain principles need to be adhered.

• Lending principles can be conveniently divided into two areas (i) activity, and (ii) individual.

Activity(a) Principle of Safety of Funds(b) Principle of Liquidity(c) Principle of Profitability(d) Principle of Purpose(e) Principle of Risk Spread(f) Principle of Security

Safety – Borrower’s capacity to repay loan along with interest. Security of tangible assets also ensure safety.Liquidity – Banks lend mainly to meet working capital requirements. Liquidity means possibility of converting loans into cash without loss of time and money.Profitability - The funds of the bank should be invested to earn highest return, so that it may pay a reasonable rate of interest to its customers on their deposits, reasonably good salaries to its employees and a good return to its shareholders. However, a bank should not sacrifice either safety or liquidity to earn a high rate of interest.

Diversification- ‘One should not put all his eggs in one basket’. According to the principle of diversification, the bank should diversify its investments in different industries and should give loans to different borrowers in one industry or different industries. It is less probable that all the borrowers and industries will fail at one and the same time.

Object of Loan/ Purpose- A banker should not grant loan for unproductive purposes or to buy fixed asset. The bank may grant loan to meet working capital requirements. However, after nationalisation of banks, the banks have started granting loans to meet long-term requirements. National policy and objectives also to be considered.The Central Government and the Reserve Bank have issued a number of directions in this regard, highlighting the social purpose which they have to sub serve.

Security- In case of unsecured loans chances of bad debt will be very high. So banks must grant secured loans. In case the borrower fails to return the loan, the banker may recover his loan after realising the security. Loans to weaker sections of society may be given without security if so directed by the government.

Margin Money- Difference between the value of security and amount of loan is usually termed as margin money. The amount of loan, should not exceed 60 to 70% of the value of the security.(Jewel Loans)

Individual

• Credit worthiness – – Character / Reliability (honesty, integrity,

regularity, promptness)– Capacity/ Responsibility (ability, competence and

experience)– Capital/ Resourcefulness.

Types of Credit Facilities

• Fund Based– Cash Credits– Overdrafts– Demand Loans– Term Loans– Bill Finance

• Non-Fund Based– Bank Guarantees– Letter of Credit

Priority Sector Lending

• 1968 - National Credit Council meeting emphasized that commercial banks should increase their involvement in the financing of priority sectors, viz., agriculture and small scale industries.

• A new dimension of social banking was added to bank’s lending.

Categories under Priority Sector

(i) Agriculture(ii) Micro and Small Enterprises (MSE)(iii) Education(iv) Housing(v) Export Credit(vi) Others

Agriculture• Loans to individual farmers [including SHGs or

Joint Liability Groups (JLGs)], directly engaged in Agriculture and Allied Activities, viz., dairy, fishery, animal husbandry, poultry, bee-keeping and sericulture (up to cocoon stage).

• Finance may be direct or indirect.

Agriculture – Direct Finance

• Short-term loans for raising crops • Medium & Long-term loans to farmers for agriculture &

allied activities• Loans to farmers under KCC scheme(Kisan Credit Card)• Distressed farmers indebted to non-institutional lenders.• Production & processing of hybrid seeds.• Construction of farm buildings.• Construction & running of storage facilities.• Payment of irrigation charges for hired facilities• Export credit to farmers.

Agriculture – Indirect Finance

• Loans to corporates including farmers’ producer companies of individual farmers, partnership firms and co-operatives of farmers directly engaged in Agriculture and Allied Activities

(i) If the aggregate loan limit per borrower is more than Rs. 2 crore, the entire loan should be treated as indirect finance to agriculture.

(ii) Loans up to Rs. 50 lakh against pledge/hypothecation of agricultural produce (including warehouse receipts) for a period not exceeding 12 months, irrespective of whether the farmers were given crop loans for raising the produce or not.

• Bank loans to Primary Agricultural Credit Societies (PACS), Farmers’ Service Societies (FSS) and Large sized Adivasi Multi- Purpose Societies (LAMPS)