75

Pre-Retirement Webinar Presented by the Oklahoma Public Employees Retirement System

Pre-Retirement WebinarPresented by the Oklahoma Public Employees Retirement System

Detailed information on topics covered

• Pre-Retirement Seminar Workbook• Medicare Gap Benefit Option brochure• EssentialOPERS• Retirement Application• Copy of the slideshow• Insurance information• Evaluation

www.opers.ok.gov/pre-retirement-webinar-materialYour Materials

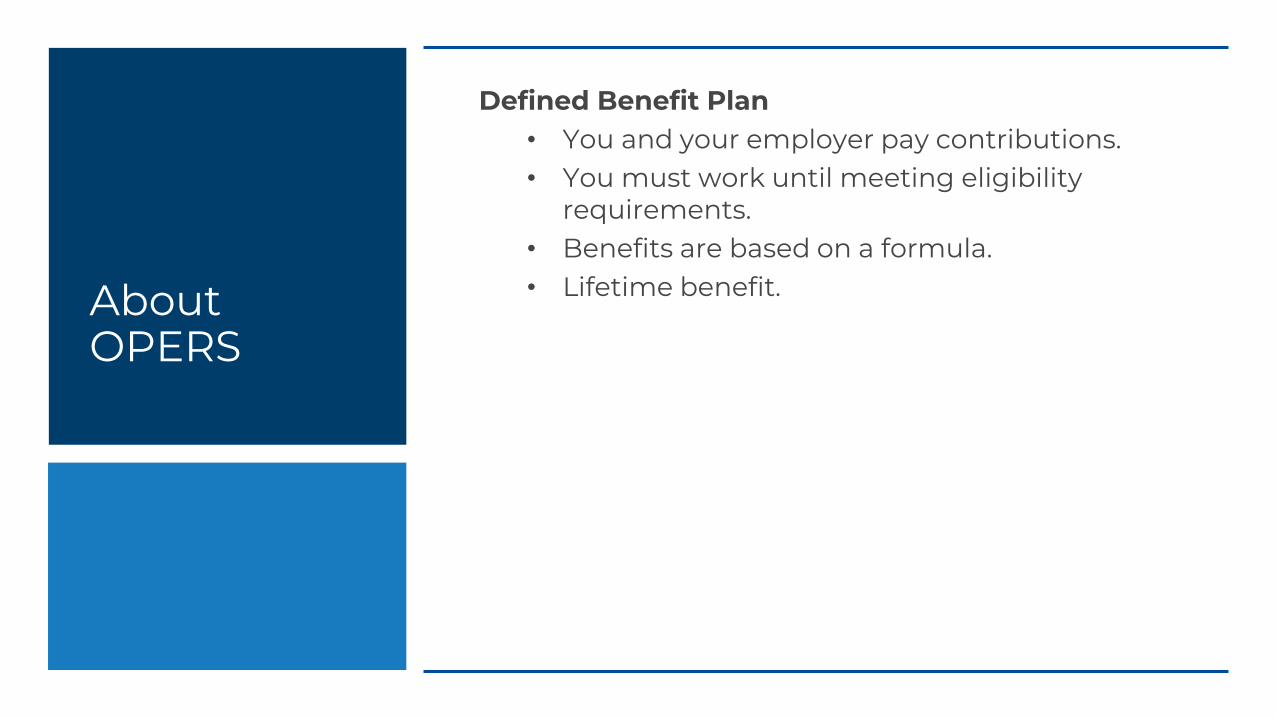

Defined Benefit Plan• You and your employer pay contributions.• You must work until meeting eligibility

requirements.• Benefits are based on a formula.• Lifetime benefit.About

OPERS

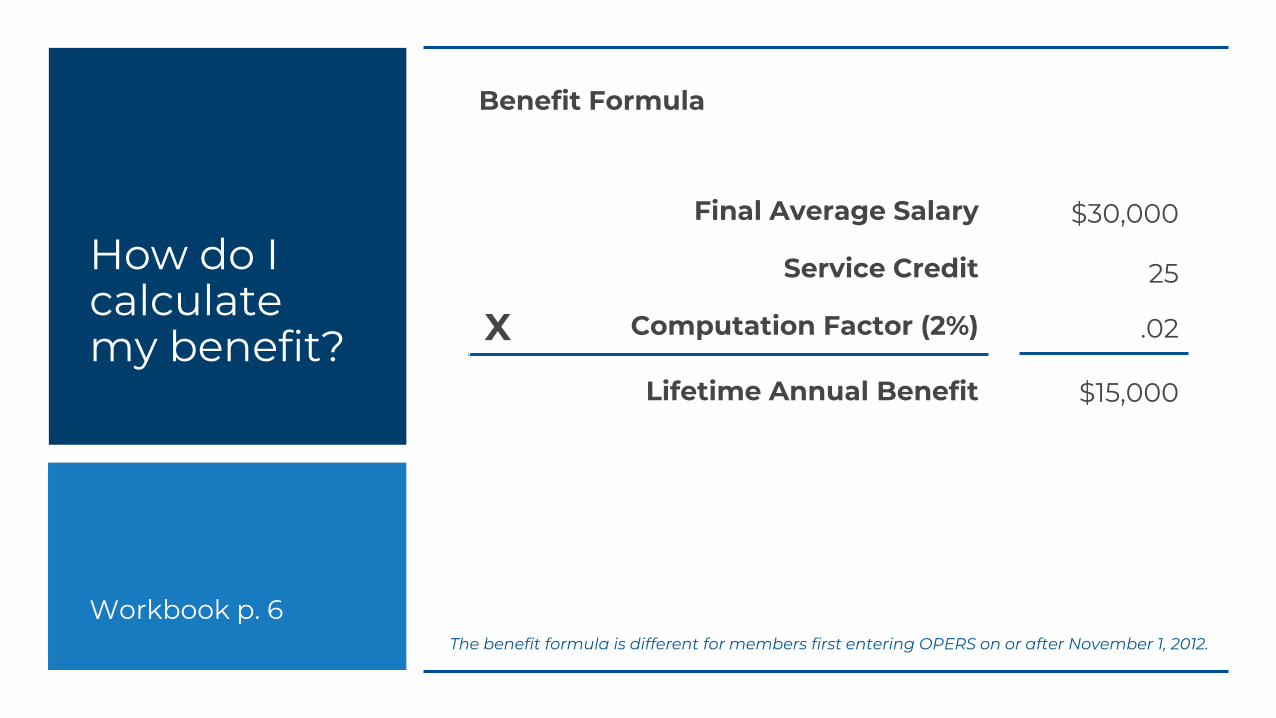

Final Average Salary

X

Service Credit

Computation Factor (2%)

Lifetime Annual Benefit

Benefit Formula

How do I calculate my benefit?

The benefit formula is different for members first entering OPERS on or after November 1, 2012.

$30,000

25

.02

$15,000

Workbook p. 6

May be added to member’s service credit• If addition causes total credited service to

equal or exceed 6 months, service is rounded up to the next year.

Unused Sick Leave

Workbook p. 7

Hours of Unused Sick Leave

Months of OPERS Service Credit

0 – 159 0

160 – 319 1

320 – 479 2

480 – 639 3

640 – 799 4

800 – 959 5

960 (maximum) 6

*Rounding eliminated for members who begin on or after November 1, 2012. These members will be credited with full years and months of participation.

Unused Sick Leave

When it adds a year:

21 years 0 months Service Credit

+ 6 months Unused Sick Leave

21 years 6 months Total Service

22 years Total Service Credit

Workbook p. 7

When it does NOT add a year:

21 years 9 months Service Credit

+ 6 months Unused Sick Leave

22 years 3 months Total Service

22 years Total Service Credit

• Within two years of retirement eligibility

• Calculated by our Analysts

• Benefit and Service Calculations form is available online

www.opers.ok.gov/formsBenefit Estimate

Normal (Full) Retirement

Age 62 with 6 years of full-time equivalent employment (2,076 hours per year)

-------------------- OR -------------------

80 points (age + service credit) if you became a member before July 1, 1992

90 points (age + service credit) if you became a member on or after July 1, 1992

When Can You Retire?

Workbook p. 3*For members who began participation in OPERS before November 1, 2011.

Early Retirement

• Ages 55 to 62• 10 years of participating

service• Permanently reduced

benefitsWhen Can You Retire?

Early Retirement Reduction Factors

Age Percentage

62 100.00

61 93.33

60 86.67

59 80.00

58 73.33

57 66.67

56 63.33

55 60.00

*For members who began participation in OPERS before November 1, 2011.Workbook p. 3

• We recommend you meet with your Retirement Coordinator 3 to 6 months prior to your retirement date to obtain retirement and insurance forms.

www.opers.ok.gov/coordinator-listing

• You must complete a Retirement Application and submit your application to OPERS at least 60 days before your retirement date.

www.opers.ok.gov/dates-and-deadlines

Getting Started

Workbook p. 10

p. 10

• Contact your retirement coordinator3 to 6 months before

• Retirement Application deadline60 days before

• Acknowledgement letter45 day before

• Preliminary statement15 days before

Retirement Day

• Final benefit statement55 days after

• First two deposits60 days after

Retirement Timeline

Workbook p. 13

Retirement Application Packet

Retirement Application

Workbook p. 9

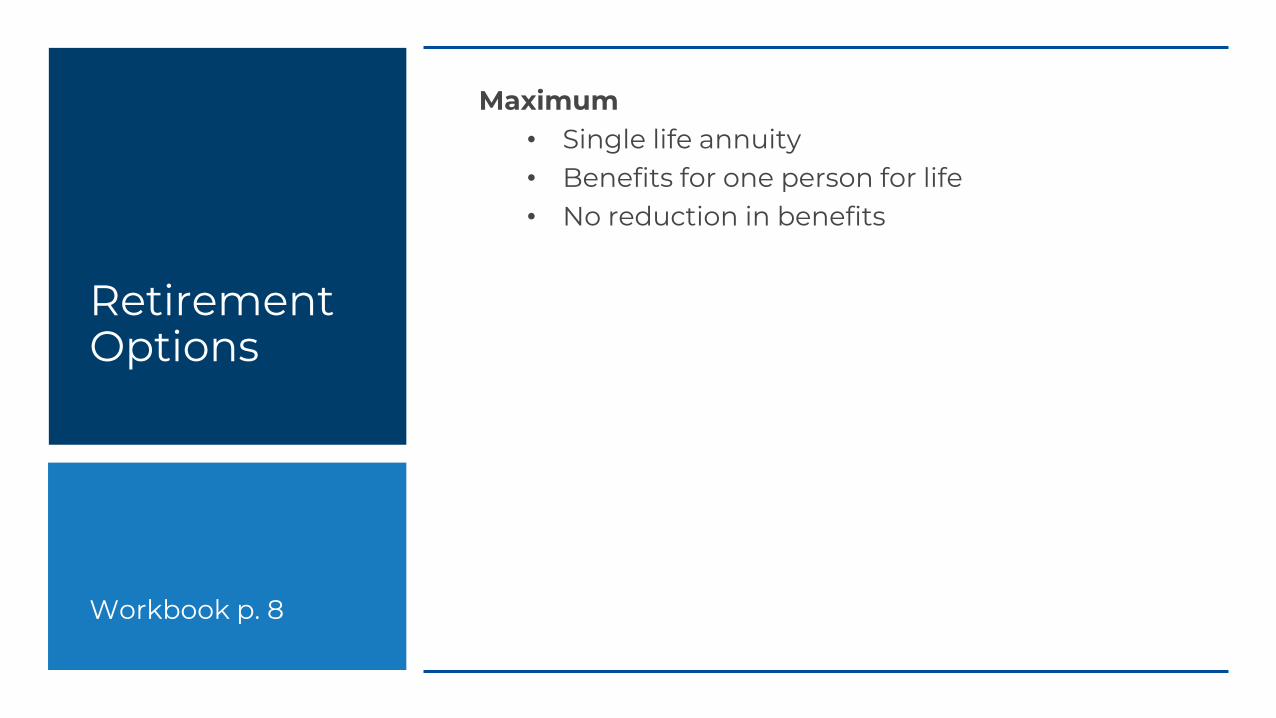

Maximum• Single life annuity• Benefits for one person for life• No reduction in benefits

Retirement Options

Workbook p. 8

Option A• ½ Joint and Survivor Annuity• Payment for two lives• Reduced lifetime benefit for you• ½ survivor benefit for life

Retirement Options

Workbook p. 8

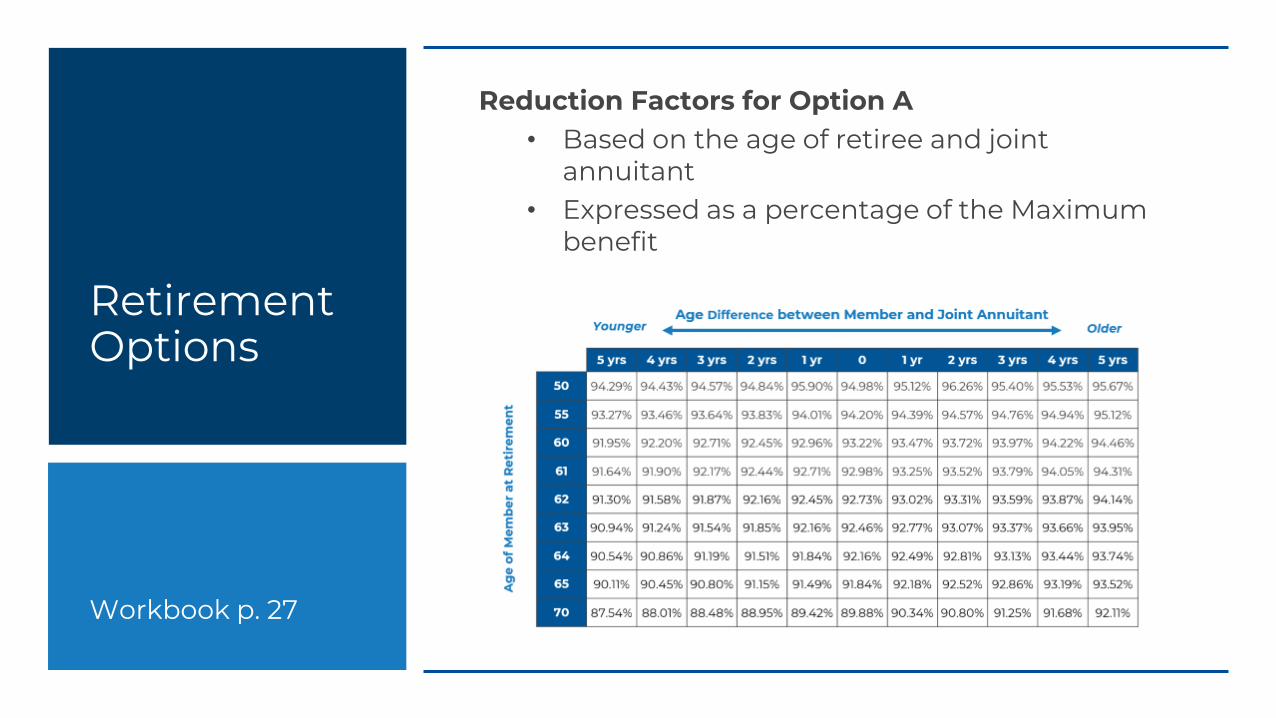

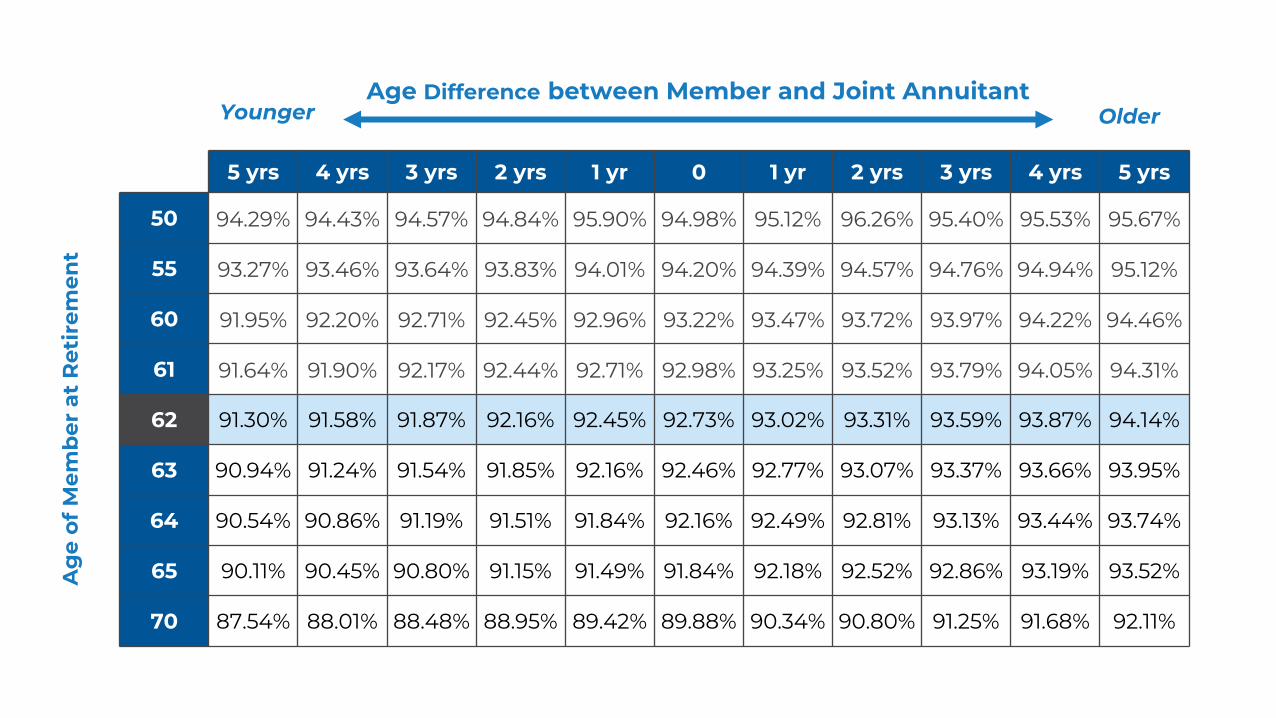

Reduction Factors for Option A• Based on the age of retiree and joint

annuitant• Expressed as a percentage of the Maximum

benefit

Retirement Options

Workbook p. 27

Zoom OptionAChart

5 yrs 4 yrs 3 yrs 2 yrs 1 yr 0 1 yr 2 yrs 3 yrs 4 yrs 5 yrs

50 94.29% 94.43% 94.57% 94.84% 95.90% 94.98% 95.12% 96.26% 95.40% 95.53% 95.67%

55 93.27% 93.46% 93.64% 93.83% 94.01% 94.20% 94.39% 94.57% 94.76% 94.94% 95.12%

60 91.95% 92.20% 92.71% 92.45% 92.96% 93.22% 93.47% 93.72% 93.97% 94.22% 94.46%

61 91.64% 91.90% 92.17% 92.44% 92.71% 92.98% 93.25% 93.52% 93.79% 94.05% 94.31%

62 91.30% 91.58% 91.87% 92.16% 92.45% 92.73% 93.02% 93.31% 93.59% 93.87% 94.14%

63 90.94% 91.24% 91.54% 91.85% 92.16% 92.46% 92.77% 93.07% 93.37% 93.66% 93.95%

64 90.54% 90.86% 91.19% 91.51% 91.84% 92.16% 92.49% 92.81% 93.13% 93.44% 93.74%

65 90.11% 90.45% 90.80% 91.15% 91.49% 91.84% 92.18% 92.52% 92.86% 93.19% 93.52%

70 87.54% 88.01% 88.48% 88.95% 89.42% 89.88% 90.34% 90.80% 91.25% 91.68% 92.11%

Younger OlderAge Difference between Member and Joint Annuitant

Ag

e of

Mem

ber

at

Ret

irem

ent

Zoom OptionAChart

5 yrs 4 yrs 3 yrs 2 yrs 1 yr 0 1 yr 2 yrs 3 yrs 4 yrs 5 yrs

50 94.29% 94.43% 94.57% 94.84% 95.90% 94.98% 95.12% 96.26% 95.40% 95.53% 95.67%

55 93.27% 93.46% 93.64% 93.83% 94.01% 94.20% 94.39% 94.57% 94.76% 94.94% 95.12%

60 91.95% 92.20% 92.71% 92.45% 92.96% 93.22% 93.47% 93.72% 93.97% 94.22% 94.46%

61 91.64% 91.90% 92.17% 92.44% 92.71% 92.98% 93.25% 93.52% 93.79% 94.05% 94.31%

62 91.30% 91.58% 91.87% 92.16% 92.45% 92.73% 93.02% 93.31% 93.59% 93.87% 94.14%

63 90.94% 91.24% 91.54% 91.85% 92.16% 92.46% 92.77% 93.07% 93.37% 93.66% 93.95%

64 90.54% 90.86% 91.19% 91.51% 91.84% 92.16% 92.49% 92.81% 93.13% 93.44% 93.74%

65 90.11% 90.45% 90.80% 91.15% 91.49% 91.84% 92.18% 92.52% 92.86% 93.19% 93.52%

70 87.54% 88.01% 88.48% 88.95% 89.42% 89.88% 90.34% 90.80% 91.25% 91.68% 92.11%

Younger OlderAge Difference between Member and Joint Annuitant

Ag

e of

Mem

ber

at

Ret

irem

ent

Zoom OptionAChart

5 yrs 4 yrs 3 yrs 2 yrs 1 yr 0 1 yr 2 yrs 3 yrs 4 yrs 5 yrs

50 94.29% 94.43% 94.57% 94.84% 95.90% 94.98% 95.12% 96.26% 95.40% 95.53% 95.67%

55 93.27% 93.46% 93.64% 93.83% 94.01% 94.20% 94.39% 94.57% 94.76% 94.94% 95.12%

60 91.95% 92.20% 92.71% 92.45% 92.96% 93.22% 93.47% 93.72% 93.97% 94.22% 94.46%

61 91.64% 91.90% 92.17% 92.44% 92.71% 92.98% 93.25% 93.52% 93.79% 94.05% 94.31%

62 91.30% 91.58% 91.87% 92.16% 92.45% 92.73% 93.02% 93.31% 93.59% 93.87% 94.14%

63 90.94% 91.24% 91.54% 91.85% 92.16% 92.46% 92.77% 93.07% 93.37% 93.66% 93.95%

64 90.54% 90.86% 91.19% 91.51% 91.84% 92.16% 92.49% 92.81% 93.13% 93.44% 93.74%

65 90.11% 90.45% 90.80% 91.15% 91.49% 91.84% 92.18% 92.52% 92.86% 93.19% 93.52%

70 87.54% 88.01% 88.48% 88.95% 89.42% 89.88% 90.34% 90.80% 91.25% 91.68% 92.11%

Younger OlderAge Difference between Member and Joint Annuitant

Ag

e of

Mem

ber

at

Ret

irem

ent

Option B• 100% Joint and Survivor Annuity• Payment for two lives• Reduced lifetime benefit for you• 100% survivor benefit for life

Retirement Options

Workbook p. 8

Option B• 100% Joint and Survivor Annuity• Payment for two lives• Reduced lifetime benefit for you• 100% survivor benefit for life

Retirement Options

Workbook p. 28

Zoom Option B Chart

5 yrs 4 yrs 3 yrs 2 yrs 1 yr 0 1 yr 2 yrs 3 yrs 4 yrs 5 yrs

50 89.19% 89.44% 89.69% 89.94% 90.19% 90.44% 90.70% 90.95% 91.20% 91.45% 91.70%

55 87.39% 87.72% 88.04% 88.37% 88.70% 89.04% 89.37% 89.71% 90.04% 90.37% 90.70%

60 85.10% 85.53% 85.97% 86.41% 86.85% 87.30% 87.74% 88.19% 88.63% 89.07% 89.51%

61 84.57% 85.02% 85.48% 85.95% 86.42% 86.89% 87.36% 87.83% 88.30% 88.77% 89.23%

62 84.00% 84.48% 84.96% 85.46% 85.95% 86.45% 86.95% 87.45% 87.95% 88.44% 88.93%

63 83.38% 83.89% 84.40% 84.93% 85.45% 85.98% 86.51% 87.04% 87.56% 88.08% 88.60%

64 82.71% 83.25% 83.80% 84.35% 84.91% 85.47% 86.02% 86.58% 87.14% 87.68% 88.23%

65 82.00% 82.57% 83.15% 83.73% 84.32% 84.91% 85.50% 86.09% 86.67% 87.25% 87.82%

70 77.85% 78.59% 79.34% 80.09% 80.86% 81.62% 82.38% 83.15% 83.90% 84.65% 85.38%

Younger OlderAge Difference between Member and Joint Annuitant

Ag

e of

Mem

ber

at

Ret

irem

ent

Zoom Option B Chart 2

5 yrs 4 yrs 3 yrs 2 yrs 1 yr 0 1 yr 2 yrs 3 yrs 4 yrs 5 yrs

50 89.19% 89.44% 89.69% 89.94% 90.19% 90.44% 90.70% 90.95% 91.20% 91.45% 91.70%

55 87.39% 87.72% 88.04% 88.37% 88.70% 89.04% 89.37% 89.71% 90.04% 90.37% 90.70%

60 85.10% 85.53% 85.97% 86.41% 86.85% 87.30% 87.74% 88.19% 88.63% 89.07% 89.51%

61 84.57% 85.02% 85.48% 85.95% 86.42% 86.89% 87.36% 87.83% 88.30% 88.77% 89.23%

62 84.00% 84.48% 84.96% 85.46% 85.95% 86.45% 86.95% 87.45% 87.95% 88.44% 88.93%

63 83.38% 83.89% 84.40% 84.93% 85.45% 85.98% 86.51% 87.04% 87.56% 88.08% 88.60%

64 82.71% 83.25% 83.80% 84.35% 84.91% 85.47% 86.02% 86.58% 87.14% 87.68% 88.23%

65 82.00% 82.57% 83.15% 83.73% 84.32% 84.91% 85.50% 86.09% 86.67% 87.25% 87.82%

70 77.85% 78.59% 79.34% 80.09% 80.86% 81.62% 82.38% 83.15% 83.90% 84.65% 85.38%

Younger OlderAge Difference between Member and Joint Annuitant

Ag

e of

Mem

ber

at

Ret

irem

ent

Zoom Option B Chart 3

5 yrs 4 yrs 3 yrs 2 yrs 1 yr 0 1 yr 2 yrs 3 yrs 4 yrs 5 yrs

50 89.19% 89.44% 89.69% 89.94% 90.19% 90.44% 90.70% 90.95% 91.20% 91.45% 91.70%

55 87.39% 87.72% 88.04% 88.37% 88.70% 89.04% 89.37% 89.71% 90.04% 90.37% 90.70%

60 85.10% 85.53% 85.97% 86.41% 86.85% 87.30% 87.74% 88.19% 88.63% 89.07% 89.51%

61 84.57% 85.02% 85.48% 85.95% 86.42% 86.89% 87.36% 87.83% 88.30% 88.77% 89.23%

62 84.00% 84.48% 84.96% 85.46% 85.95% 86.45% 86.95% 87.45% 87.95% 88.44% 88.93%

63 83.38% 83.89% 84.40% 84.93% 85.45% 85.98% 86.51% 87.04% 87.56% 88.08% 88.60%

64 82.71% 83.25% 83.80% 84.35% 84.91% 85.47% 86.02% 86.58% 87.14% 87.68% 88.23%

65 82.00% 82.57% 83.15% 83.73% 84.32% 84.91% 85.50% 86.09% 86.67% 87.25% 87.82%

70 77.85% 78.59% 79.34% 80.09% 80.86% 81.62% 82.38% 83.15% 83.90% 84.65% 85.38%

Younger OlderAge Difference between Member and Joint Annuitant

Ag

e of

Mem

ber

at

Ret

irem

ent

Option B• Option B joint annuitant selection is limited to

either the member’s spouse or a non-spouse who is no more than 10 years younger than the member.

Retirement Options

Workbook p. 8

• If you are married at the time of retirement, you have a default choice of Option A or B.

• Your spouse must consent to you choosing one of the other retirement options.

• Your spouse must also consent to you choosing an alternate joint annuitant.

Options and Spouse Consent

Workbook p. 8

• Your joint annuitant must be a specific person (not a trust, charity, pet, etc.).

• Your joint annuitant cannot be changed after retirement.

• If your joint annuitant dies before you, you can change to Maximum benefit (unreduced) from that point on.

• Consult with OPERS before selecting a joint annuitant 15+ years younger.

Joint and Survivor Annuitant (Option A or B)

Workbook p. 8

Option C• Single life annuity/10-year term certain• Reduced lifetime benefit• If you die within the first 10 years of benefit

payments, your beneficiary will receive payments for balance of the 10-year period.

• Your beneficiary does not have to be a person and may be changed at any time.

Retirement Options

Workbook p. 8

Reduction Factors for Option C

Retirement Options

Workbook p. 29

Age Factor

55 98.14%

56 98.05%

57 97.94%

58 97.82%

59 97.69%

60 97.55%

61 97.38%

62 97.19%

Age Factor

63 96.95%

64 96.67%

65 96.33%

66 95.93%

67 95.47%

68 94.94%

69 94.34%

70 93.65%

Retirement Application

Workbook p. 13

Retirement Application

Workbook p. 13

At least 60 days before retirement date• Retirement Application must be complete

and submitted to OPERS by the deadline.• The Retirement Application is the only

document that must be submitted by the deadline.

www.opers.ok.gov/dates-and-deadlines

Retirement Application Deadline

Submit with your Retirement Application:

Required Documents

Vital Documents Beneficiaries

Direct Deposit Tax Withholding

Submit with your Retirement Application:

Required Documents

Vital Documents Beneficiaries

Direct Deposit Tax Withholding

Retiree Death Benefit(s)• $5,000 Death Benefit*If applicable: • Excess Accumulated Employee Contributions• Final Monthly Benefit Payment

Taxed as ordinary income• Can be rolled over to defer taxes if 1) spouse is

beneficiary, or 2) a non-spouse beneficiary rolls it over to an Inherited IRA.

* This is separate from any life insurance you may have and is provided for by OPERS.

Beneficiary Designation

Workbook p. 19

Submit with your Retirement Application:

Required Documents

Vital Documents Beneficiaries

Direct Deposit Tax Withholding

Submit with your Retirement Application:

Required Documents

Vital Documents Beneficiaries

Direct Deposit Tax Withholding

Benefits are considered income for tax purposes.

You can have state and federal taxes withheld from your retirement benefits.

OPERS will send you a 1099-R at the end of January each year.

Taxes

Workbook p. 15

Submit with your Retirement Application:

Required Documents

Vital Documents Beneficiaries

Direct Deposit Tax Withholding

Approximately 45 days before retirement date• Acknowledgement Letter• Confirms your retirement date• Request any outstanding forms or documents

What Happens Next?

Approximately 15 days before retirement date• Preliminary Benefit Statement with

estimated gross benefit amount• Medicare Gap Letter and Brochure• Returning to Work MemoWhat

Happens Next?

• Allows members, under age 65 at retirement, to temporarily increase their monthly benefit amount

• Increase is intended to help pay health insurance premiums which are typically higher before Medicare eligibility

• After age 65, there is a permanent decrease in your monthly benefit amount

• Decrease will sometimes be MOREthan the increase amount

Medicare Gap Benefit Option

Workbook p. 18

• Election is irrevocable

• Actuarially neutral to OPERS

• Individual calculations will be provided after you have submitted your Retirement Application

• Retiring in 2021, additional $277 a month

• IMPORTANT: If you elect the Medicare Gap Benefit Option and return to work, you may not waive benefits and retire a second time.

Medicare Gap Benefit Option

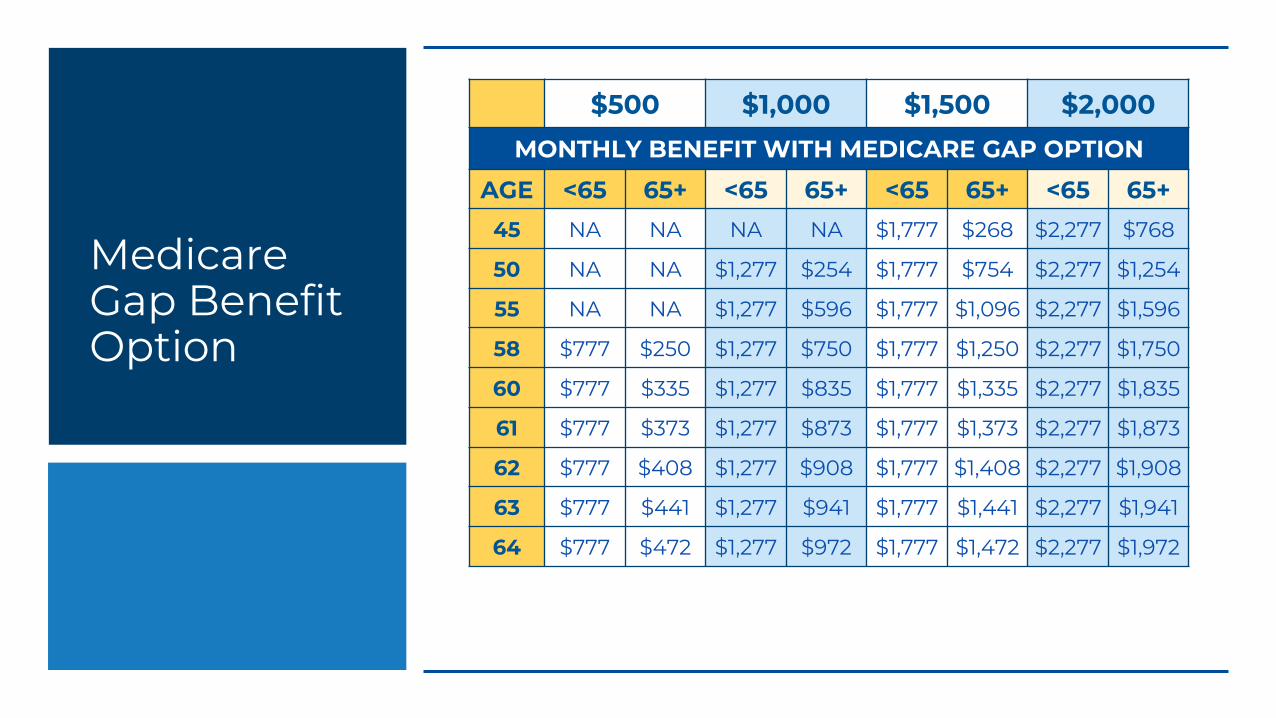

$500 $1,000 $1,500 $2,000 MONTHLY BENEFIT WITH MEDICARE GAP OPTION

AGE <65 65+ <65 65+ <65 65+ <65 65+45 NA NA NA NA $1,777 $268 $2,277 $768

50 NA NA $1,277 $254 $1,777 $754 $2,277 $1,254

55 NA NA $1,277 $596 $1,777 $1,096 $2,277 $1,596

58 $777 $250 $1,277 $750 $1,777 $1,250 $2,277 $1,750

60 $777 $335 $1,277 $835 $1,777 $1,335 $2,277 $1,835

61 $777 $373 $1,277 $873 $1,777 $1,373 $2,277 $1,873

62 $777 $408 $1,277 $908 $1,777 $1,408 $2,277 $1,908

63 $777 $441 $1,277 $941 $1,777 $1,441 $2,277 $1,941

64 $777 $472 $1,277 $972 $1,777 $1,472 $2,277 $1,972

Medicare Gap Benefit Option

Retirement Date• Your retirement date will be on the first of the

month.

Approximately 55 days after Retirement Date• Your Monthly Benefit Statement is issued

showing final benefit amount.

60 days after Retirement Date• Your first two retirement checks are issued.

What Happens Next?

• Contact your retirement coordinator90 days before

• Retirement Application deadline60 days before

• Acknowledgement letter45 day before

• Preliminary statement15 days before

Retirement Day

• Final benefit statement55 days after

• First two deposits60 days after

Retirement Timeline

Workbook p. 13

One-year “cooling-off” period• An OPERS retiree is prohibited from returning

to work with the same employer from which he/she retired for a period of one year without waiving benefits.

No pre-arranged employment agreement• Pre-retirement employment agreements that

permit a member to retire then be rehired by same employer on any basis are prohibited by state law and IRS Code.

Retirees Returning to Work

Workbook p. 16

• You may return to work for a non-participating employer at any time without affecting your retirement.

• If you return to a different participating employer, you must wait at least one month following your retirement date or your benefit will be cancelled.

• Complete Post-Retirement Employment Election form to continue benefits or waive benefits and be eligible to retire again after three years

• Continue paying contributions• Benefit increases every additional 2,076 hours worked

Retirees Returning to Work

Workbook p. 16

OPERS-Participating Employer & OPERS Retirement Benefit

• Benefit subject to Social Security earnings limitation

• Complete Status of Post-Retirement Employment form• When you approach Social Security earnings

limitation• Choose to continue or terminate employment

Retirees Returning to Work

Workbook p. 16

Social Security Administration (SSA) Earnings Limitation• Will not reach SSA Full Retirement Age in 2021 - $18,960• Up to the point you reach SSA Full Retirement Age in 2021 - $50,520• Once you reach SSA Full Retirement Age - No Limit

Defined Contribution Plan• Voluntary• No specific benefit promised• Participant is primarily responsible for making

contributions and managing those assets• Supplements retirement income from

Defined Benefit PlanAbout SoonerSave

Workbook p. 20

The SoonerSave program is comprised of two separate plans:

• 457 Plan – Your deferrals and investment income

• 401(a) Plan – $25 monthly contribution by the State and investment income.

SoonerSave

Workbook p. 20

2021 IRS Contribution Limit:• You can contribute up to 100% of your taxable

income or $19,500 (whichever is less).• Age 50 and Over Catch-Up: you may

contribute an additional $6,500, for a total of $26,000.

• Regular 457 Plan Catch-Up: you may be able to contribute up to $39,000 per year for the last three years prior to eligible retirement age, based on contributions not made in previous years. Contact SoonerSave for more information.

SoonerSave

Annual Leave:• Accumulated annual leave may be put into

SoonerSave at retirement.• Contact your agency coordinator and

SoonerSave the month before annual leave would be paid out or approximately 30-45 days before last day on payroll.

• You must not exceed the IRS contribution limit for the year.

SoonerSave

When you retire:• No additional deferrals to either plan once

retired, but funds may still be rolled into SoonerSave after retirement.

• Funds may be left in the plan at retirement and withdrawn at a later date

• You can withdraw funds beginning 31 days after retirement

• Set up banking information online now for faster withdrawals later

• Update your SoonerSave beneficiaries online

SoonerSave

Workbook p. 21

Taking distributions:• You can withdraw funds in a number of ways• Call Empower Retirement when ready to

begin a distribution: 877-538-3457• Distributions paid by direct deposit or check

• Set up banking information online now for faster withdrawals later

• Taxed as regular income• NOTE: 401(a) - penalty may apply to

withdrawals prior to age 59½, unless rollover to IRA or qualified plan

SoonerSave

Workbook p. 20

You can delay distribution until the latter of:• The year you turn age 72* • The year you retire from a SoonerSave

participating employer

Failure to receive required minimum distribution

could lead to a tax penalty.

*age 70 ½ if you reach 70 ½ before January 1, 2020

SoonerSaveRequired Minimum Distribution (both plans)

Workbook p. 23

The following insurance information is provided by the Employees Group Insurance Division (EGID) as a courtesy.

Insurance

Insurance

Terms• Vest – worked long enough to retain benefits,

but not ready to receive a retirement check• Retire – worked long enough to retire and

receive a retirement check• COBRA – not eligible to vest or retire; you may

keep COBRA for up to 18 monthsInsurance

Benefits• You may continue or begin any benefits your

employer has with EGID (Life coverage must be in effect at least 30 days prior to your retirement)

• Retain all coverage you think you will need.• After retirement, you can reduce benefits, but

you cannot add benefits (except for vision coverage).

• Plan changes can be made if you or your covered dependent are Medicare eligible or if you move outside your plan’s service area. All covered dependents must enroll in the same plan.

• You will receive a confirmation statement.

Insurance

Dependents• You may elect to continue or begin coverage

for dependents at retirement. • Dependents cannot be added after

retirement.• Exceptions:

• Loss of other group insurance• Adoption or legal guardianship

(up to age 26)• Marriage (Spouse must be

added within 30 days)

Notify EGID in writing within 30 days

Insurance

Life Insurance• Retain all life insurance in effect while you

were an active employee.• Life insurance must be retained in $5,000

increments.• $2.16 per $1,000 up to $40,000; $41,000 and

greater are age-rated.• Complete a beneficiary form if you are

retaining life insurance – please keep this information current.

Dependent Life Coverage• You may retain all of the amount carried on

your dependents while you were an active employee.

• $1.08 per $500

Insurance

Deferring to Spouse Status• If you have a spouse who is still employed

with an entity that is covered by EGID, you may defer health, dental and vision to your spouse’s coverage. Life must be kept in your retirement account.

• Your spouse must contact their benefits coordinator to add dependent coverage.

• You may transfer back to your own account at any time by notifying EGID.

Insurance

Working Past Age 65

Contact Social Security• You may delay your enrollment in Medicare

Part B. • Active employment insurance is primary to

Medicare.• As long as you provide proof of credible

coverage, you will not incur a late enrollment penalty.

• If you delayed Medicare Part B, you should contact Social Security 60 days before your employer coverage ends to enroll in Part B.

Insurance

Forms Required• Application for Retiree/Vest/Non-

Vested/Defer Insurance(A1-A3) must be sent in 30 days before your retirement date.

• Medicare Supplement Plan Application (B1-B4)

• MAPD Application (C1-C4)• Any break in coverage will cancel your

insurance and future eligibility.

Special note to Medicare-eligible member:

It is critical that your application is received the month before you terminate current

employment.

Insurance

Medicare• Medicare is the federal health insurance

program for people who are 65 or older and for those with disabilities or end-stage renal disease.

• Administered by CMS – the Centers for Medicare and Medicaid Services.

• Generally, you are notified by Medicare about 90 days before your 65th birth month.

• It is the member’s responsibility to enroll in Medicare Part A and Part B.

Insurance

Parts of Medicare

Part A• Hospitalization (no monthly fee).

Part B• Outpatient services (monthly fee).

Part C• Medicare Advantage plans (replaces original

Medicare).

Part D• Prescription drug coverage governed by

Medicare, but offered through insurance companies or their affiliates.

Insurance

EGID provides two types of plans

•Medicare Supplements • A supplement to original Medicare and Part D

included

•Medicare Advantage Prescription Drug Plans (MAPD)

• “All in one” plans offered by private companies that contract with Medicare to provide your Part A and Part B benefits and Part D included.

Insurance

Medicare Supplement plans:

•BCBSOK – BlueSecure and HealthChoice SilverScript

• Enrollment in Medicare Part A and Part B recommended.

• Provide nationwide coverage.• Pay Part A deductible and coinsurance.• After you meet Part B deductible, Medicare

pays 80 percent and the supplement pays 20 percent of allowed Part B services.

• Provide Part D or creditable prescription drug coverage.

• A new ID card will be issued.

Insurance

Medicare Advantage MAPD HMO

•CommunityCare Senior and Generations• Must live in designated ZIP code service area.

• Designated PCP must coordinate all your medical and hospital services, with exception in cases of non-network emergency or urgent care.

• Must use your PCP for routine care or be financially responsible for any related charges.

• Cannot change plans if PCP leaves your plan.

• Provides Part D or creditable prescription drug coverage.

Insurance

Medicare Advantage MAPD PPO

•BCBSOK and Humana National• Obtain routine and other scheduled services

anywhere in the U.S. as long as the provider participates in Medicare and agrees to accept the MAPD plan.

• Designated PCP not required.

• No referrals required.

• Medical precertification may be required.

• Provide Part D or creditable prescription drug coverage.

Insurance

Insurance

Surviving Dependents• Surviving dependents have 60 days to notify

EGID that they wish to continue insurance coverage.

• Surviving dependent children may continue coverage including Dependent Life until age 26.

• A surviving spouse may continue coverage, including Dependent Life, as long as the premiums are paid. The spouse will pay the primary member rate.

(Retirement system contributions will not apply)

Insurance

Moving • Contact EGID if you move to update your

address.• If you are pre-Medicare and on an HMO, you

may need to enroll in a new plan.• Medicare members can live anywhere in the

USA and use any providers contracted with Medicare with certain plans.

Option Period• You will continue to have an annual Option

Period

Contribution• $105 from OPERS toward medical premiums

(rate sheet does not include the $105 contribution)

Insurance

Thank You!OPERS / SoonerSave

P.O. Box 53007

Oklahoma City, OK 73152-3007

(405) 858-6737 (local)

(800) 733-9008 (toll-free)

www.opers.ok.gov

www.soonersave.com

EGID

Office of Management and

Enterprise Services

(405) 717-8780 (local)

(800) 752-9475 (toll-free)

www.omes.ok.gov

www.healthchoiceok.com

How Did We Do?

tinyurl.com/OPERS-Eval